HKICPA_QP_Module D (Dec 15)_Answer

- 格式:pdf

- 大小:204.07 KB

- 文档页数:13

eclipse调试(debug)弹出错误

警告信息:

Cannot connect to VM

com.sun.jdi.connect.TransportTimeoutException

控制台错误信息:

FATAL ERROR in native method: JDWP No transports initialized, jvmtiError=AGENT_ERROR_TRANSPORT_INIT(197)

ERROR: transport error 202: unable to create socket: winsock error 87

ERROR: JDWP Transport dt_socket failed to initialize, TRANSPORT_INIT(510)

JDWP exit error AGENT_ERROR_TRANSPORT_INIT(197): No transports initialized [../../../src/share/back/debugInit.c:741]

百度了两天都没能解决这个问题,我⼀直都不开防⽕墙的,ping localhost也能连上,神奇的是java6能debug,java7不能debug

刚刚仔细看错误信息,看到⾥⾯有socket这个词,难道debug还需要socket吗?事实确实如此,不管是java project调试,tomcat调试、远程调试都需要socket。

既然跟socket有关,那就是跟⽹络有关。

但是我电脑也能上⽹啊,难道配置不对?抱着这个想法,我打开万能的360断⽹急救箱强⾏恢复⽹络配置,重启机器后就能debug啦~

哟西哟西~。

香港会计师公会专业资格课程(QP)认证院校有哪些?香港会计师公会(HKICPA)消息,公会已顺利完成对暨南大学五个财会类本科专业的「专业资格课程Qualification Programme(QP)」认证评审。

6月7日,HKICPA执行总监伍大成先生率团队向暨南大学授予认证牌匾。

自此,香港会计师公会在内地的QP认证院校版图扩大至16家。

中国内地的16家QP认证院校:中央财经大学、中国人民大学、北京大学、对外经济贸易大学、首都经济贸易大学、天津大学、南开大学、上海交通大学、复旦大学、浙江大学、厦门大学、暨南大学、中山大学、广东外语外贸大学、联合国际学院及澳门大学。

据了解,暨南大学获QP认证的五个财会类本科专业包括管理学院会计学、会计学专业(注册会计师方向)、会计学专业(ACCA方向)、财务管理专业以及国际学院会计学(CPA Canada方向)专业。

QP优势★香港会计师是搭通国际及国内的桥梁★国际认可,与五大洲特许及美国会计师公会互认安排根据2011年11月签订的《内地与香港更紧密经贸关系安排》(CEPA)补充协议五,中、港两地政府已率先把两地专业考试的相互豁免科目增加至四科。

CICPA会员报读QP,可获豁免「财务汇报」、「企业财务」和「业务鉴证」三科。

而HKICPA会员报考中国注册会计师全国统一考试时,亦获得「会计」、「审计」、「财务成本管理」和「公司战略与风险管理」四科豁免。

学员可于2年内既完成国际认可的香港会计师资格证及内地的中国注册会计师资格证,能帮助你丰富个人履历表。

一直以来,香港会计师公会与国内各会计协会、两地会计师事务所都保持着长久的友好合作关系,在涉及行业发展的许多重要问题上互通有无,交流渠道日益畅通,合作方式日益多样,友谊日益深厚,共同推动注册会计师行业的发展你,香港会计师公会执业证书HKICPA在内地的认可度逐年提高。

伙伴们,2018年9月起,香港会计师公会将推出新版专业资格课程(QP)测试。

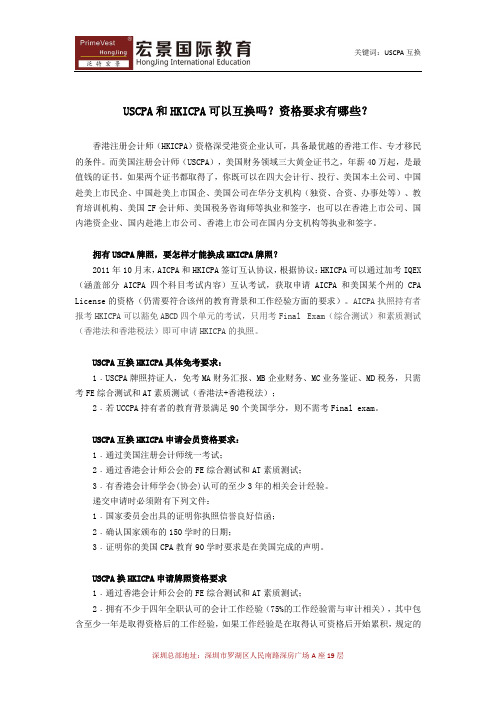

香港注册会计师证书:就业前景好,起薪高!2017年6月30日,HKICPA官方发布数据显示:HKICPA会员人数总数为41,332人。

根据会员类型划分其中资深会员为:5,455,占总人数的13%;普通会员为:35,877,占总人数的87%。

根据会员类型划分资深会员13%普通会员87%资深会员普通会员根据执照类型划分执业会员人数为:4,627,占总人数的11%;非执业会员为:36,705,占总人数的89%。

根据职位划分其中公司合伙人人数为:1,642,占总体的35.5%; 股东或董事会成员人数为:775,占总体的16.7%; 公司的授权签字人人数为:133,占总体的2.9%; 个人为:2,077,占总体的44.9%。

11%89%根据执业类型划分执业会员非执业会员35%17%3%45%根据职位划分公司合伙人股东或董事会成员公司授权签字人个人根据注册地点划分其中香港居民人数为39,281,占总人数的95%;其他地区为:2,051,占总人数的5%。

根据地区划分392812051根据工作地点划分香港地区人数为28805,占总人数的69.7%;澳门地区人数为:118,占总人数的0.3%;大陆地区人数为:1330,占总人数的3.2%;其中北京:296,占22.3%;上海:362,占27.2%;广州:143,占10.8%;深圳:224,占16.8%;其他城市:305,22.9%;海外地区人数为:1088,占总人数2.6%;工作地点不明确人数:9991,占24.2%。

根据工作地区划分通过对以上数据的分析,可总结出以下几点:香港地区的HKICPA会员人数为39,281,占总人数的95%;而在香港工作的人数仅28805,占总人数的69.7%。

由此可推测近1100会员人士流出到大陆或海外工作。

细思极恐,职场上的竞争者将越来越多,再不努力,将会被更优秀的人取代;大陆地区HKICPA会员人数仅为1330,占总人数的3.2%;北上广深各大一线城市HKICPA会员人数仅不到400人,实属行业或缺人才;考取HKICPA不仅能转换其他证书,也能让你成为行业领头人,职场中的佼佼者,强势碾压竞争者。

香港注册会计师(HKICPA)考试难度及通过率分析

展开全文

香港注册会计师(HKICPA)的考试难度相对于国内的CICPA来讲,是简单一些的,从考试科目的数量,内容难度,每年的考试次数以及通过所有考试的时长就可以看出,很多人都是通过考HKICPA来豁免掉CICPA中最难的四科,但HKICPA对于国内的考生来讲还是有一定难度的,主要是考试资格限制(对所读的院校和专业都是有严格的要求的,Qp考试属于严进宽出);第二是全英语考试(英语薄弱是目前国内很多考生面临的共同的问题),且多为案例分析。

香港注册会计师通过率

香港注会官方给出的回答是总合格率平均为50%以上。

HKICPA证书适合人群有哪些?

学历:专科毕业以上学历,若毕业于本科会计专业且毕业时间不超五年,可获得相应科目的豁免(基础associate阶段)。

专科学历需参加香港学术及职业资历评审局(HKCAAVQ)评估,达到香港High Diploma/associate degree/Level 4以上即可获得QP考试资格。

行业:大型上市公司,银行、保险、证券等金融机构,通信、地产、互联网、制造业、航空等行业,会计师事务所等。

职务:企业的总经理、公司财务总监/经理,会计事务所合伙人,董秘等;

专业人才:会计师、审计师、税务师、财务分析师、金融分析师、保险咨询师、财务顾问、投资顾问、税务专家等。

在香港,无论是在会计师事务所、外资企业、跨国公司还是积极进军海外市场的中国企业,HKICPA资格都备受推崇和认可。

总之,以后想在香港深度发展的朋友可以考虑拿下HKICPA证书给自己拓展下职业前景,加油!。

香港注册会计师HKICPA专业资格QP常见问题导读:香港注册会计师(HKICPA)资格深受港资企业认可,具备最优越的香港工作、专才移民的条件,以致越来越多的人投入到HKICPA 资格考试中来,但是很多人对HKICPA资格考试还是一头雾水。

看完以下文章,你就拨开云雾见天日!【关于QP】Q1: QP是一个怎样的课程?A: QP全名是Qualification Programme,是香港会计师公会开办的专业资格考试,是在香港晋身为执业会计师的最直接途径。

QP课程全面,所教授的国际会计准则和会计实务规范,有助学员扩阔环球视野和提升竞争力。

Q2: QP有什么国际认可?A:QP已取得世界五大洲国际认可,完成QP (包括4个单元及综合考试) 的公会会员可以向英国(苏格兰、英格兰及威尔斯、爱尔兰)、加拿大、津巴布韦、南非、澳大利亚及新西兰的特许会计师公会申请会籍及执业资格(须符合有关协议及当地的要求条件)。

公会于2011年10月25日与美国会计师公会(AICPA)及美国国家会计委员会全国联合会(NASBA)签署互认协议,标志着香港的会计师国际认可资格进一步被肯定。

【报名资格】Q3: 报考QP需要什么资格?A:申请人必须持有认可的内地大学或学位授予机构认可的学士或硕士学位证书及须符合报读QP的胜任能力要求,当中包括:财务报告、管理会计、财务管理、审计、税务、商业法、公司法、管理信息系统、经济学、统计学、市场营销和专业的道德学。

Q4: 报考QP需要什么文件?A:报名表需连同以下文件一同交上:学士学位证书及考试成绩单相关专业资格证明文件中国、香港(如有)身份证或护照中国注册会计师协会全国统一考试全科合格证或会员证(如有) 近照两张Q5: 目前国内获香港会计师公会认证的院校有哪些?A:目前获香港会计师公会认证的内地高校包括人民大学、上海交通大学、上海财经大学、天津大学、中央财经大学、对外经济贸易大学、南开大学、复旦大学、首都经济贸易大学及联合国际学院等10所。

USCPA和HKICPA可以互换吗?资格要求有哪些?香港注册会计师(HKICPA)资格深受港资企业认可,具备最优越的香港工作、专才移民的条件。

而美国注册会计师(USCPA),美国财务领域三大黄金证书之,年薪40万起,是最值钱的证书。

如果两个证书都取得了,你既可以在四大会计行、投行、美国本土公司、中国赴美上市民企、中国赴美上市国企、美国公司在华分支机构(独资、合资、办事处等)、教育培训机构、美国ZF会计师、美国税务咨询师等执业和签字,也可以在香港上市公司、国内港资企业、国内赴港上市公司、香港上市公司在国内分支机构等执业和签字。

拥有USCPA牌照,要怎样才能换成HKICPA牌照?2011年10月末,AICPA和HKICPA签订互认协议,根据协议:HKICPA可以通过加考IQEX (涵盖部分AICPA四个科目考试内容)互认考试,获取申请AICPA和美国某个州的CPA License的资格(仍需要符合该州的教育背景和工作经验方面的要求)。

AICPA执照持有者报考HKICPA可以豁免ABCD四个单元的考试,只用考Final Exam(综合测试)和素质测试(香港法和香港税法)即可申请HKICPA的执照。

USCPA互换HKICPA具体免考要求:1﹒USCPA牌照持证人,免考MA财务汇报、MB企业财务、MC业务鉴证、MD税务,只需考FE综合测试和AT素质测试(香港法+香港税法);2﹒若UCCPA持有者的教育背景满足90个美国学分,则不需考Final exam。

USCPA互换HKICPA申请会员资格要求:1﹒通过美国注册会计师统一考试;2﹒通过香港会计师公会的FE综合测试和AT素质测试;3﹒有香港会计师学会(协会)认可的至少3年的相关会计经验。

递交申请时必须附有下列文件:1﹒国家委员会出具的证明你执照信誉良好信函;2﹒确认国家颁布的150学时的日期;3﹒证明你的美国CPA教育90学时要求是在美国完成的声明。

USCPA换HKICPA申请牌照资格要求1﹒通过香港会计师公会的FE综合测试和AT素质测试;2﹒拥有不少于四年全职认可的会计工作经验(75%的工作经验需与审计相关),其中包含至少一年是取得资格后的工作经验,如果工作经验是在取得认可资格后开始累积,规定的四年经验可减为三十个月。

CheckStyle报错的常见问题及解决⽅式CheckStyle报错的常见问题及解决⽅式声明:本⽂摘⾃百度⽂库。

希望这篇⽂章提到的规范能对⼤家编程起到好的效果,此⽂不定期更新,将推出更加详尽的编程规范。

1 提⽰:Type is missing a javadoc commentClass说明:缺少类型说明解决⽅法:增加javadoc说明2 提⽰:“{” should be on the previous line说明:“{”应该位于前⼀⾏。

解决⽅法:把“{”放到上⼀⾏去3 提⽰:Methos is missing a javadoc comment说明:⽅法前⾯缺少javadoc注释。

解决⽅法:添加javadoc注释4 提⽰: Expected @throws tag for“Exception”说明:在注释中希望有@throws的说明解决⽅法:在⽅法前得注释中添加这样⼀⾏:* @throws Exception if has error(异常说明)5 提⽰:“.” Is preceeded with whitespace说明: “.” 前⾯不能有空格。

解决⽅法:把“.”前⾯的空格去掉6 提⽰:“.” Is followed by whitespace说明:“.” 后⾯不能有空格。

解决⽅法:把“.”后⾯的空格去掉7 提⽰:“=” is not preceeded with whitespace说明:“=” 前⾯缺少空格。

解决⽅法:在“=”前⾯加个空格8 提⽰:“=” is not followed with whitespace说明:“=” 后⾯缺少空格。

解决⽅法:在“=”后⾯加个空格9 提⽰:“}” should be on the same line说明:“}” 应该与下条语句位于同⼀⾏。

解决⽅法:把“}”放到下⼀⾏的前⾯10 提⽰:Unused @param tag for “unused”说明:没有参数“unused”,不需注释解决⽅法:“* @param unusedparameter additional(参数名称)” 把这⾏unused参数的注释去掉“11 提⽰: Variable “CA” missingjavadoc说明:变量“CA”缺少javadoc注释解决⽅法:在“CA“变量前添加javadoc注释:/** CA. */(注意:⼀定记得加上CA后⾯的“.”)12 提⽰: Line longer than 80characters说明:⾏长度超过80 。

1."mons.collections.SequencedHashMap"'s signer information does not match signer information of other classes in the same package这是由于struts提供的commons-beanutils.jar和hibernate提供的commons-collections.jar冲突成的,可以从spring提供的lib中找到这个两个jarng.IllegalStateException: No data type for node:org.hibernate.hql.ast.tree.IdentNode用hql 时,忘了给表名加别名,如select p from Position,应该是select p from Position p3.The Server didn 't send back a proper XML response用FCKEditor时原因:解析不了xml文件解决方法:情况一:web.xml的配置是否正确,具体查看《FCKEditor使用指南.pdf》,还有fckeditor自带的几个jar 包情况二:加入serializer.jar,xalan.jar情况三:把项目下的fckeditor包删了,重新加入一遍.eclipse.swt.SWTError: No more handles [Unknown Mozilla path (MOZILLA_FIVE_HOME not set)]SWTError:没有更多的处理[未知Mozilla的路径(MOZILLA_FIVE_HOME未设置)]环境:linux下运行swt程序(我出现此问题是,在linux下嵌套浏览器)原因:firefox版本不一致解决:重装一个firefox,并设置相关变量5.Exception in thread "main" org.eclipse.swt.SWTError: No more handles [Could not detect registered XULRunner to use]环境:用XULRunner 在java application中嵌套浏览器原因:没有注册XULRunner解决:window下环境中,在程序中加入,如(第二个参数是下载解压后的存放路径):static{System.setProperty("org.eclipse.swt.browser.XULRunnerPath", "C:\\xulrunner");}6.Exception in thread "main" ng.UnsatisfiedLinkError: noswt-win32-3536 or swt-win32 in swt.library.path, java.library.path or the jar file环境:用DJ Natvie Swing时,在java application中嵌套浏览器,且在windows环境下运行正常,但在linux下却包此异常原因:windows下与linux下使用的swt jar包不一样解决:在windows下用swt-3.5M6-win32-win32-x86.jar,在linux下用swt-3.5.1-gtk-linux-x86.jar7.Exception in thread "main" .ProtocolException:cannot write to a URLConnection if doOutput=false - call setDoOutput(true)环境:用URLConnection送某url发送数据时原因:doOutput=false时,不能发送数据解决:如urlConnection.setDoOutput(true).SocketException: Connection resetat .SocketInputStream.read(SocketInputStream.java:168)at sun.nio.cs.StreamDecoder.readBytes(StreamDecoder.java:264)at sun.nio.cs.StreamDecoder.implRead(StreamDecoder.java:306)at sun.nio.cs.StreamDecoder.read(StreamDecoder.java:158)at java.io.InputStreamReader.read(InputStreamReader.java:167)at java.io.BufferedReader.fill(BufferedReader.java:136)at java.io.BufferedReader.readLine(BufferedReader.java:299)at java.io.BufferedReader.readLine(BufferedReader.java:362)at com.eagle.service.AutoUpdate.run(AutoUpdate.java:43)环境:j2se socket编程时,服务器端报错原因1:服务器端用BufferedReader,时,没有读到一行解决:客户端用PrintWriter, pw.println(),不能用pw.print(),因为br.readLine()是读一行环境:j2se socket编程时,服务器端/客户端在br.readLine()时报错原因2:服务器端用BufferedReader,br.readLine()时,客户端/服务器已经退出,但是并未通过服务器/客户端,即服务器端/客户端的socket还没有关闭,当用br.readLine()时就会出现这种情况解决:在关闭客户端时要socket.close(),同时还要向服务器发送一条退出的信息,这样让服务器知道某个客户端已经关闭,它就可以终止对此客户端的线程了,反之服务器也是一样.hibernate.PropertyAccessException: Null value was assigned toa property of primitive type setter of er环境:hibernate原因:oolean类型的值为null,boolean类型的值必须是true/false解决:save or update时给boolean类型的值赋true/false10.用占位符查询时出现空指针ng.NullPointerExceptionatorg.hibernate.hql.ast.ParameterTranslationsImpl.getNamedParameterExpectedType(ParameterTranslat ionsImpl.java:63)at org.hibernate.engine.query.HQLQueryPlan.buildParameterMetadata(HQLQueryPlan.java:245)at org.hibernate.engine.query.HQLQueryPlan.<init>(HQLQueryPlan.java:95)at org.hibernate.engine.query.HQLQueryPlan.<init>(HQLQueryPlan.java:54)at org.hibernate.engine.query.QueryPlanCache.getHQLQueryPlan(QueryPlanCache.java:71)at org.hibernate.impl.AbstractSessionImpl.getHQLQueryPlan(AbstractSessionImpl.java:133)at org.hibernate.impl.AbstractSessionImpl.createQuery(AbstractSessionImpl.java:112)at org.hibernate.impl.SessionImpl.createQuery(SessionImpl.java:1583)at .struts.action.LoginAction.execute(LoginAction.java:72)at org.apache.struts.action.RequestProcessor.processActionPerform(RequestProcessor.java:419)at org.apache.struts.action.RequestProcessor.process(RequestProcessor.java:224)at org.apache.struts.action.ActionServlet.process(ActionServlet.java:1194)at org.apache.struts.action.ActionServlet.doPost(ActionServlet.java:432)at javax.servlet.http.HttpServlet.service(HttpServlet.java:709)at javax.servlet.http.HttpServlet.service(HttpServlet.java:802)at org.apache.catalina.core.ApplicationFilterChain.internalDoFilter(ApplicationFilterChain.java:252)at org.apache.catalina.core.ApplicationFilterChain.doFilter(ApplicationFilterChain.java:173)at org.apache.catalina.core.StandardWrapperValve.invoke(StandardWrapperValve.java:213)at org.apache.catalina.core.StandardContextValve.invoke(StandardContextValve.java:178)at org.apache.catalina.core.StandardHostValve.invoke(StandardHostValve.java:126)at org.apache.catalina.valves.ErrorReportValve.invoke(ErrorReportValve.java:105)at org.apache.catalina.core.StandardEngineValve.invoke(StandardEngineValve.java:107)at org.apache.catalina.connector.CoyoteAdapter.service(CoyoteAdapter.java:148)at org.apache.coyote.http11.Http11Processor.process(Http11Processor.java:869)atorg.apache.coyote.http11.Http11BaseProtocol$Http11ConnectionHandler.processConnection(Http11Ba seProtocol.java:664)at .PoolTcpEndpoint.processSocket(PoolTcpEndpoint.java:527)at .LeaderFollowerWorkerThread.runIt(LeaderFollowerWorkerThread.java:80) at org.apache.tomcat.util.threads.ThreadPool$ControlRunnable.run(ThreadPool.java:684)at ng.Thread.run(Thread.java:595)环境:hibernate原因:HQL 不能解析解决:错误写法:String hql = "select m from com.eagle.oa.model.Message m where m.ids like: id";正确写法:String hql = "select m from com.eagle.oa.model.Message m where m.ids like:id";ng.IndexOutOfBoundsException: Remember that ordinal parameters are 1-based!原因:在使用hibernate的session.createQuery(.....)时设置参数的下标应该从0开始解决:如:return session.createQuery("from User u where erName = ? and password = ?").setParameter(0, name).setParameter(1, password).uniqueResult();.hibernate.TransientObjectException: object references an unsaved transient instance - save the transient instance before flushing: com.wxj.entities.Group环境:hibernate原因:某个实例的属性一个对象,这个对象没有保存,还是暂态的对象解决:先保存这个对象,或是在另一端加inverse = true13.ORA-01461: can bind a LONG value only for insert into a LONG column环境:oracle原因:jar冲突解决:换成classes12.jar包即可14.ERROR LazyInitializationException:19 - could not initialize proxy - the owning Session was closed环境:SSH原因:当一个类或属性设置了lazy="true",操作对象时,session已经关闭了解决:使用Spring的过滤器openSessionInView.springframework.dao.InvalidDataAccessApiUsageException: Write operations are not allowed in read-only mode (FlushMode.NEVER/MANUAL): Turn your Session into MIT/AUTO or remove 'readOnly' marker from transaction definition.环境:SSH原因:这个异常产生的主要原因是DAO采用了Spring容器的事务管理策略,如果操作方法的名称和事务策略中指定的被管理的名称不能够匹配上,spring 就会采取默认的事务管理策略(PROPAGATION_REQUIRED,read only).如果是插入和修改操作,就不被允许的,所以包这个异常解决:修改spring配置文件中相关事务管理部分mon.beans.ProbeException: There is no READABLE property named 'eid' in class 'com.wxj.entity.Student'环境:ibatis原因:在给对象做操作,设置参数时,指定的参数不是对象中有的属性,就会抛出此异常解决:核对对象的属性ng.OutOfMemoryError: PermGen space环境:很多,如ssh整合时原因:不断的更新class,造成应用重启,最终造成代码区的内存空间满了解决:方法很多,1重启,2增加代码区的大小,3少更新class,4有时可能是log4j造成的问题,建议使用common-loggin.jar 5,优化代码以下来自CSDN的jinhuiyu:在JVM中如果98%的时间是用于GC且可用的Heap size 不足2%的时候将抛出此异常信息,可以用如下方法解决(根据你的实际情况设置大小),但是这只是临时的解决方法,更重要的是改造你的CODE1.可以在windows 更改系统环境变量加上JAVA_OPTS=-Xms64m -Xmx512m2,如果用的tomcat,在windows下,可以在C:\tomcat5.5.9\bin\catalina.bat 中加上:set JAVA_OPTS=-Xms64m -Xmx256m位置在: rem Guess CATALINA_HOME if not defined 这行的下面加合适.3.如果是linux系统Linux 在{tomcat_home}/bin/catalina.sh的前面,加set JAVA_OPTS='-Xms64 -Xmx512'18.在客户端使用dwr时,即跨域访问时,出现“拒绝访问“及“找不到某个属性”的问题(在服务器端调用时却正常)环境:在客户端使用dwr原因:1。

新版AndroidStudio使⽤gitpullpush报错ng.Runti。

2022年2⽉28⽇最新版版本如下Android Studio Bumblebee | 2021.1.1 Patch 2Build #AI-211.7628.21.2111.8193401, built on February 17, 2022Runtime version: 11.0.11+9-b60-7590822 amd64VM: OpenJDK 64-Bit Server VM by Oracle CorporationWindows 10 10.0GC: G1 Young Generation, G1 Old GenerationMemory: 5120MCores: 24Registry: external.system.auto.import.disabled=true, ide.instant.shutdown=false, ages.page.size=100000,ide.images.show.chessboard=trueNon-Bundled Plugins: org.intellij.plugins.markdown (211.7142.37)环境配置好后,使⽤git pull 代码,在⽂件夹使⽤ git 命令正常,在studio 中使⽤,报错 push pull 均报错,报错如下16:39:55.811: [android] git -c credential.helper= -c core.quotepath=false -c log.showSignature=false -c mentChar=pull --no-stat -v --progress origin spring31Invocation failed Unexpected end of file from serverng.RuntimeException: Invocation failed Unexpected end of file from serverat org.jetbrains.git4idea.GitAppUtil.sendXmlRequest(GitAppUtil.java:30)at org.jetbrains.git4idea.http.GitAskPassApp.main(GitAskPassApp.java:58)Caused by: .SocketException: Unexpected end of file from serverat java.base/.www.http.HttpClient.parseHTTPHeader(HttpClient.java:866)at java.base/.www.http.HttpClient.parseHTTP(HttpClient.java:689)at java.base/.www.http.HttpClient.parseHTTPHeader(HttpClient.java:863)at java.base/.www.http.HttpClient.parseHTTP(HttpClient.java:689)at java.base/.www.protocol.http.HttpURLConnection.getInputStream0(HttpURLConnection.java:1615)at java.base/.www.protocol.http.HttpURLConnection.getInputStream(HttpURLConnection.java:1520)at org.apache.xmlrpc.DefaultXmlRpcTransport.sendXmlRpc(DefaultXmlRpcTransport.java:87)at org.apache.xmlrpc.XmlRpcClientWorker.execute(XmlRpcClientWorker.java:72)at org.apache.xmlrpc.XmlRpcClient.execute(XmlRpcClient.java:194)at org.apache.xmlrpc.XmlRpcClient.execute(XmlRpcClient.java:185)at org.apache.xmlrpc.XmlRpcClient.execute(XmlRpcClient.java:178)at org.jetbrains.git4idea.GitAppUtil.sendXmlRequest(GitAppUtil.java:27)... 1 moreerror: unable to read askpass response from 'C:\Users\xxxxxxx\AppData\Local\Google\AndroidStudio2021.1\tmp\intellij-git-askpass-local.sh'bash: /dev/tty: No such device or addresserror: failed to execute prompt script (exit code 1)fatal: could not read Username for '': No such file or directory解决办法:File | Settings | Version Control | Git勾选 : Use credential helper重新尝试 git pull push OK 了另:新主机 64G 内存,以前build 10分钟,现在2分,⽣产⼒⼯具⽆疑了。

持HKICPA证书可免考CPA四门,那你了解HKICPA吗?HKICPA证书与CICPA/USCPA豁免政策HKICPA转CICPA,可豁免:会计、审计、财务成本管理、公司战略与风险管理,只需要考税法和经济法;HKICPA转USCPA,只需参加IQEX考试+满足某特定州的执照申请条件;既然考HKICPA可以免考CPA4科,那你了解HKICPA吗?HKICPA全称是 Hong Kong Institute of Certified Public Accountants,中文名香港会计师公会。

严格来讲,HKICPA不是一种考试,而是一个香港法定的会计师协会,是香港会计届的权威。

而香港注册会计师考试,全称Qualification Programme,简称QP,是由香港注册会计师公会一手包办的。

HKICPA报名首先你想要参加考试,就要知道自己有没有报名资格,QP和国内的CPA考试有一点很大不同在于,QP考试不是所有人都有资格报名。

总的来说,具有会计背景的人有资格报名。

一般而言,申请人必须持有认可的内地大学或学位授予机构认可的学士或硕士学位证书及须符合报读QP的胜任能力要求,当中包括:财务报告、管理会计、财务管理、审计、税务、商业法、公司法、管理信息系统、经济学、统计学、市场营销和专业的道德学。

报考条件1.本科会计专业,毕业的学校是香港会计公会列出的大学,日本和台湾的学历无考试资格。

2.非会计专业或其他大专以下学历,可以通过参加HKIAAT和PBE课程来达到满足申请要求。

如果有了资格之后,第一步就是要注册成为QP Student,言下之意就是你已经成为了这个programme的学生并且会为了这个考试而努力。

别小看这个student的身份,它也是一种专业性质的认可,是可以写进你的简历里面的,或者说是可以在你的名片后面加上的称号(估计很少有人会这么做==),这也是为什么要设置报名门槛的原因之一。

此外,student 的身份是要缴纳年费的,每年450港币。

SECTION A – CASE QUESTIONSAnswer 1(a)The five transfer pricing methods are discussed in detail in the OECD Transfer Pricing Guidelines and Departmental Interpretation and Practice Notes No. 46 viz. comparable uncontrolled price (“the CUP”) method, cost plus method, resale price method, transactional net margin method (“TNMM”) and profit split method.In the present case, the CUP method is the most appropriate method. The CUP method is essentially a comparison of price. It compares the price of a controlled transaction to the price of a comparable uncontrolled transaction. In applying the CUP method, there are two possible types of comparable price – internal comparable uncontrolled price and external comparable uncontrolled price. The former refers to the comparison between the price of the controlled transaction and the price charged in a comparable transaction between one of the enterprises to the transaction and an independent party. The latter refers to the comparison between the price of the controlled transaction and the price of a comparable transaction between independent parties.The Shares at issue are identical to the shares in Saffron being traded on the Hong Kong Stock Exchange both in terms of the product and the market. Although internal comparable uncontrolled price is not available in the present case as the Company had not traded any shares in Saffron apart from the Shares, transaction prices are, however, readily available on the Hong Kong Stock Exchange. They provide the external comparable uncontrolled prices to establish the arm’s length price of the Shares. Hence, there is little, or no, difficulty in finding an external comparable uncontrolled price for the Shares when applying the CUP method.With regard to the cost plus method, which compares the different mark up on the costs commanded by different suppliers, and the resale price method, which compares the gross margin commanded by different resellers or distributors, the former is mostly used in the case of manufacturers while the latter is used for distributors. Although it is not incorrect to say that a share dealer may have a target mark up or gross margin, to a certain extent, that mark up or gross margin is determined, among others, by the investment strategy and the financial position of that share dealer. Such being the case, the mark up or gross margin commanded by other share dealers is not a good comparable in establishing the arm’s length price of the Shares as there may be differences in the position of the Company and that of the other share dealers. Reasonably accurate adjustments have to be made to eliminate the effects of those differences. The cost plus method and the resale price method are therefore less appropriate, or probably not preferred, in the present case.As to TNMM, it is a comparison of the net profit margin, which may be operating net profit as a percentage of sales, cost or assets. This method is not appropriate in the present case which is an issue concerning the selling of the Shares, not net profit margin.Turning to the profit split method. This method is concerned with the splitting of the aggregate profits between the associated enterprises based on an economically valid basis. This method is applicable in cases where the functions of the group are intertwined and it is necessary to examine the whole process to ascertain the real economic contribution of each group member. In the present case, the Shares were initially acquired by the Company for trading purposes. ABC (Investments) Limited played no role on the acquisition. Indeed, ABC (Investments) Limited had not been incorporated when the Company acquired the Shares. The function of ABC (Investments) Limited is only to streamline the business of the Company, which is why the Shares were transferred. The present case is not a case where the functions of the group are intertwined. Hence, the profit split method is not appropriate.As Arrangement B is a qualified investment arrangement, it is to be regarded as a debt arrangement between the Company as borrower and ABC (Financing) Limited as lender. The investment return payable (i.e., the rental expense incurred by the Company in respect of the Property) is to be regarded as interest payable on the money borrowed by the Company from ABC (Financing) Limited under s.22(2)(b) of Schedule 17A (“the Schedule”) of the Inland Revenue Ordinance (“the IRO”). Also, by virtue of s.22(7) of the Schedule, the relevant interest expense is deductible under s.16(2)(f)(iii) of the IRO.Further, as ABC (Financing) Limited is to be regarded as not having any legal or beneficial interest in the Property over the term of the qualified investment arrangement by virtue of s.22(2)(c) of the Schedule and that the selling of the Property by the Company to ABC (Financing) Limited is to be disregarded under s.22(3)(a) of the Schedule, it follows that the Company remains the owner of the Property. Coupled with the fact that the Company occupies the Property throughout, the Company is entitled to the deduction of the commercial building allowance in respect of the Property.Answer 3As the Collector of Stamp Revenue accepts that the Arrangements are an alternative bond scheme, the relevant parties are entitled to stamp duty relief by virtue of s.47E and s.47F(1) of the Stamp Duty Ordinance (“the SDO”). Accordingly, the sale and purchase agreements / assignments on the transfer of the Property from the Company to ABC (Financing) Limited and vice versa, the lease agreement entered into between ABC (Financing) Limited and the Company on the leasing of the Property at a monthly rent of HK$300,000 for a term of 4 years, the purchase undertaking entered into by the Company and the declaration of trust executed by ABC (Financing) Limited in favour of the Investors are not chargeable to stamp duty.S.8(1)(a) of the IRO provides that salaries tax shall be charged for each year of assessment on every person in respect of his income arising in or derived from Hong Kong from any office or employment of profit. S.8(1A)(a) of the IRO extends the basic charge on salaries tax in respect of income arising in or derived from Hong Kong from any employment while s.8(1A)(b) and (c) exclude certain income derived from Hong Kong from any employment. As the extension of the basic salaries tax charge under s.8(1A) and the exclusion under s.8(1A)(b) or (c) only cover income from employment, neither the extension charge nor the exclusion provisions has any application to income derived from an office. S.9 of the IRO provides that income from any office or employment includes fees.Turning to the relevant case law, a guiding principle has been laid down by the High Court in CIR v Goepfert (1987) 2 HKTC 210 in which Macdougall J ruled that the totality of facts have to be considered in determining the source of an employment. Though Geopfert was a case dealing with the source of employment, in the Board of Review Decision No. D123/02 18 IRBRD 150, the Board held that the totality of facts test is equally applicable to determine the source of income from an office. As to the issue on the locality of an office, on the authority of McMillan v Guest 24 TC 190, the office of a director of a corporation is where the central management and control of the corporation is exercised. And, following the decision in Swedish Central Railway Company Ltd v Thompson(1925) 9 TC 342, a company may have more than one residence for the purposes of establishing liability to income tax.In the present case, the director’s fee received by Mr Au for the year of assessment 2013/14 is chargeable to tax under s.8(1)(a) of the IRO as it was an income derived by Mr Au from an office located in Hong Kong. First, the central management and control of the Company was in Hong Kong. The Company conducted substantial business operations in Hong Kong. Mr Chan made decisions on his own in Hong Kong on the running of the Company. Also, he had meetings with Mr But and their employees in Hong Kong. Although Mr Chan and Mr But did discuss the business of the Company through emails and teleconferences, it does not necessarily follow that the place of central management and control is not in Hong Kong as, after all, Mr Chan and the senior management were stationed in Hong Kong. Second, the Company kept house in Hong Kong. Its statutory registers as well as its accounting records were kept in Hong Kong. Hence, the Company was resident in Hong Kong. It therefore follows that Mr Au’s office was located in Hong Kong.Although Mr Au stayed in Hong Kong for less than 60 days in the year of assessment 2013/14 and that he paid tax of the same nature in Country X, that director’s fee, however, is not to be excluded under s.8(1A)(b)(ii) nor s.8(1A)(c) of the IRO as those exclusions are restricted to the income derived by the taxpayer in connection with his employment. The director’s fee received by Mr Au is therefore fully chargeable to salaries tax in Hong Kong.Mr and Mrs Au (“the Couple”) migrated to Country X in early April 2013. They have not ordinarily resided in Hong Kong since then. It follows that both of them were not permanent residents of Hong Kong for the year of assessment 2013/14.The Couple were not temporary residents for that year of assessment either. They stayed in Hong Kong for 50 days only, which is less than 180 days, for the year of assessment 2013/14. Also, in the relevant two consecutive years of assessment (a) 2012/13 and 2013/14; (b) 2013/14 and 2014/15, they stayed in Hong Kong for (a) 270 days and (b) 70 days, both of which were less than 300 days. Hence, Mr Au was not eligible to have his income assessed under personal assessment for the year of assessment 2013/14 as both he and his wife did not satisfy the conditions set out in s.41(1) of the IRO. Such being the case, Mr Au’s total tax liability will be computed on a schedular basis as follows:Year of assessment 2013/14Salaries tax liabilityHK$Assessable income 250,000Less: Married person’s allowance (240,000)Net chargeable income 10,000Salaries tax payable at progressive ratefirst HK$40,000 @2% 200Salaries tax payable at standard rateHK$250,000 @15% 37,500Salaries tax payable at lower of the200aboveProfits tax liabilityHK$Assessable Profits 30,000Tax @15% 4,500The relevant salaries tax assessment was issued on 1 June 2012. Unless there is evidence which proves to the satisfaction of the Commissioner that Mr Au was prevented from lodging a notice of objection within one month of the issue of the assessment, it is unlikely that his late objection will be accepted by the Commissioner by virtue of the proviso to s.64(1) of the IRO.Unfortunately, Mr Au cannot rely on s.70A of the IRO to request the revision of the relevant salaries tax assessment either. S.70A(1) provides, inter alia, that, if upon application made within 6 years after the end of the year of assessment or within 6 months after the date on which the relevant notice of assessment was served, whichever is the later, it is established to the satisfaction of an Assessor that the tax charged for that year of assessment is excessive by reason of an error or omission in the return, the Assessor shall correct such assessment. In the present case, the year of assessment in dispute is 2006/07. The relevant assessment was issued on 1 June 2012. The later of 6 years after the end of the year of assessment 2006/07 or within 6 months after the issue of that assessment was 31 March 2013. Mr Au came to notice the over-reporting of the bonus in April 2013. It was beyond the six years’ time limit by the time Mr Au was aware of the error. Not to mention that it was also six months after the issue of the relevant salaries tax assessment.To conclude, the relevant salaries tax assessment has become final and conclusive in terms of s.70 of the IRO. Also, s.79 of the IRO provides that if it is proved to the satisfaction of the Commissioner within six years of the end of a year of assessment or within six months after the date on which the relevant notice of assessment was served, whichever is the later, any person who has paid tax in excess of the proper amount shall be entitled to be refunded the amount paid in excess. Proviso to s.79 provides that nothing in that section shall operate to extend the time limit for objection or repayment specified in other sections of the IRO. As such, Mr Au cannot resort to s.79 to request for a refund of the excess amount of the tax which he paid.* * * END OF SECTION A * * *SECTION B – ESSAY / SHORT QUESTIONSAnswer 6Deductible expenditure on replacement of implement, utensil or article under s.16(1)(f) of the IRO: HK$500,000 (carpet replacement)Deduction of capital expenditure on renovation of building or structure (other than domestic buildings) under s.16F of the IRO: (HK$4,000,000 + HK$850,000) ÷5 = HK$970,000Deduction of capital expenditure for Prescribed Fixed Assets under s.16G(1) of the IRO: HK$130,000 for the computer system (HK$30,000 trade-in value should be deemed as taxable trading receipt under s.16G(3) of the IRO.)Deduction of capital expenditure for environmental protection facilities under s.16I(2)&(3) of the IRO: HK$760,000 + (HK$600,000 ÷5) = HK$880,000Depreciation allowance attributable to Suckling for the year:-20% poolHK$ 30% poolHK$TotalallowancesHK$T.W.D.V. b/fwd 1,276,000 96,000Addition (furniture) 253,000 -Less: I.A. @ 60% on addition (151,800) ___-____ 151,8001,377,200 96,000Less: A.A. (275,440) (28,800) 304,240 T.W.D.V. c/fwd 1,101,760 67,200 456,040 Depreciation allowance for hire purchase asset (motor vehicle):HK$Total allowancesHK$Addition 500,000Less: I.A.[HK$100,000 + HK$ (500,000 –100,000) x 8] x 60%40 (108,000) 108,000392,000Less: A.A.@ 30% (117,600) 117,600274,400 225,600Interest expense deduction for monthly installments on motor vehicle under s.16(1)(a) & 16(2)(d) of the IRO: (HK$11,000 – HK$10,000) x 8 = HK$8,000Commercial building allowance attributable to Suckling for the year:HK$Ranking cost b/fwd 6,354,000Less: Disposal during the year (500,000)Add: Addition during year (renovation of directors’quarters) 380,000Ranking cost c/fwd 6,234,000HK$Total allowancesHK$T.W.D.V. b/fwd 4,652,400Les: Balancing allowance (Residue of expenditure) (300,000) 300,000 Add: Addition during the year as per above 380,0004,732,400Less: A.A.@ 4% of ranking cost c/fwd (249,360) 249,3604,483,040 549,360As Mr Tam is a non-PRC tax resident with employment income from a non-Chinese enterprise, he would be subject to the China Individual Income Tax (“IIT”) on his employment income sourced from the PRC pursuant to Article 1 of Individual Income Tax Law (Revised 2011).As Taiwan and the PRC have not entered into any tax treaty arrangement, Mr Tam would be subject to IIT if he resides in the PRC for more than 90 days during a calendar year. To count the number of days for the abovesaid purpose, the day of entry into the PRC and the day of departure from the PRC are each counted as a one-day presence in the PRC pursuant to Guoshuifa (2004)97, Article 1. Specifically Mr Tam would be subject to IIT on his employment income derived during his “actual working days”in the PRC pursuant to Guoshuifa (2004)97, Articles 2 & 3.Answer 7(b)In the course of providing the tax consultancy services, Kwan & Co. should ensure that they have competent professional knowledge for their tax practice. In addition, Kwan & Co. should put forward the best position in favor of their clients, provided that it does not in any way impair the standard of integrity and objectivity under Section 430 “Ethics in Tax Practice” in the Code of Ethics for Professional Accountants (Revised Jan 2015) issued by the Hong Kong Institute of Certified Public Accountants.Kwan & Co. should not hold out to Mr Tam the assurance that their tax advice is beyond challenge. In addition, tax advice given to Mr Tam should be recorded either in the form of a letter or memorandum for record purposes.Possible arguments for subject to salaries taxUnder s.9(1)(a) of the IRO, income from employment includes wages, salary, etc, derived from the employer or others. In this regard, the income of Mr Koo derived from the employment with Ocean View Limited can be paid by others, especially from Mr Cheung as he is the sole director and shareholder of the company. The payment is possibly part and parcel of the remuneration of Mr Koo attributable to his employment with Ocean View.There is no concrete evidence substantiating the argument that the money was a gift given because of personal friendship. The assertion of Mr Cheung is self-serving and has no objective justification.The amount received by Mr Koo is substantially in proportion to his annual salary and the date of receipt is also the eve of Chinese New Year. This pattern is in line with the payment of a performance-based bonus typically found in generic employment arrangements. Answer 8(b)Possible arguments for not subject to salaries taxThere was no implicit or explicit agreement entered into by Mr Koo with Ocean View nor Mr Cheung for any new employment contract or extension of existing employment covering the payment of the subject amount to Mr Koo. Substantially the amount is a spontaneous payment and has no connection to the present or any other employment of Mr Koo.The amount was substantially higher than Mr Koo’s existing annual salary. The quantum was unlikely to be in line with any performance-based bonus paid principally and directly by the employer or others, and therefore should not be regarded as part of his employment income.The payment to Mr Koo was unexpected and was solely on a discretionary basis made by Mr Cheung personally. This is not likely to be a pattern generically found in any contractual arrangement for employment of income.Relevant additional information for further evaluation could be obtained from the following perspectives:-∙Details of similar payments, if any, paid to Mr Koo by Mr Cheung in prior years.∙Details of similar payments, if any, paid by Mr Cheung to other employees of Ocean View and / or other close contacts of Mr Cheung.∙Evidence justifying the long-term friendship between Mr Koo and Mr Cheung.∙Financial information and business performance of Ocean View for examination if there is any co-relation between the payment and the profitability of Ocean View during the relevant financial period.∙Detailed comparison of the remuneration package of Mr Koo in current and prior years in order to evaluate if the prevailing package had been revised in line with the incorporation of the subject payment.∙Examine whether Mr Koo has reached the retirement age and if the amount received by him is substantially a retirement gratuity paid by Mr Cheung.Under s.5(1) of the IRO, rental income derived by Mr Lee from his owned property situated in Hong Kong is subject to property tax. By way of election of personal assessment under Part 7 of the IRO, the interest expenses on money borrowed for producing the rental income can only be deducted to the extent of the nominal rental income received from Ms Wong under s.42(1) of the IRO. Excessive interest expenses, if any, incurred by Mr Lee cannot be allowed for deduction against his other taxable income under s.42(1) of the IRO.Under s.30(1) of the IRO and on the basis that Mr Lee continues to maintain and resides with his mother, Ms Wong, he can be entitled to claim Dependent Parent and Additional Dependent Parent Allowances continuously notwithstanding that Ms Wong has derived rental income subject to tax.In the context of Ms Wong, the rental income derived by her under the arrangement would be subject to profits tax under s.14(1) of the IRO instead of property tax on the basis that she carries on a property sub-letting business in Hong Kong.In order to minimise the respective tax liabilities, Ms Wong may consider applying for personal assessment and claim the Personal Allowance to deduct against the property rental income. However, Ms Wong cannot deduct the interest expenses, if any, incurred on the loan borrowed for the acquisition of the respective property under s.42(1) of the IRO as the loan, if any, is borrowed by her son Mr Lee as the owner of the property instead of by herself.In view of the possible overall tax benefit derived by Ms Wong from the arrangement proposed by Mr Lee, the IRD may challenge the plan and seek to apply respective anti-avoidance provisions in the IRO to counteract the tax benefit derived thereon. Specifically, the IRD may apply s.61 and / or s.61A of the IRO in the circumstances.Under s.61 of the IRO, the IRD may disregard any transaction or disposition, and the person concerned shall be assessed accordingly where an assessor of the IRD is of the opinion that:-(a) any transaction which reduces or would reduce the amount of tax payable by anyperson is artificial and fictitious, or that(b) any disposition is not in fact given effect.Alternatively under s.61A(2) of the IRO, the assistant commissioner may raise an assessment on the relevant person (i) as if the transaction or any part thereof had not been entered into or carried out, or (ii) in such manner as he considers appropriate to counteract the tax benefit which would otherwise be obtained, in the circumstances that:-(a) there must be a transaction as defined;(b) the transaction has or would have had the effect of conferring a tax benefit on aperson; and(c) having regard to the seven specific matters under s.61A(1)(a) to (g) of the IRO, itwould be concluded that the sole or dominant purpose of entering into that transaction was to enable the relevant person, either alone or in conjunction with other persons, to obtain a tax benefit.As Mr Lee intended to use a nominal value instead of the market price for leasing the property to his mother for further leasing out to generate rental income, and in which the tax liabilities of Ms Wong could be reduced by the election of personal assessment, the IRD may use the abovesaid general anti-avoidance provisions to assess the respective tax liabilities of Mr Lee and Ms Wong on the basis that the transaction (i.e. the use of nominal value in leasing the property to Ms Wong for further leasing out in the property market) is artificial and fictitious, and / or the sole or dominant purpose of entering into that transaction was to obtain tax benefit.In this regard, Mr Lee should review the proposed transaction and explore the genuine and commercial justification of the arrangement in order to defend their tax positions and the possible challenge from the IRD.* * * END OF EXAMINATION PAPER * * *。