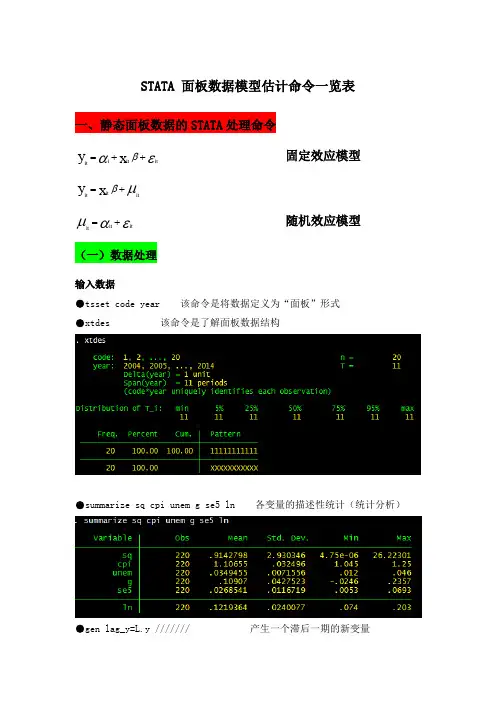

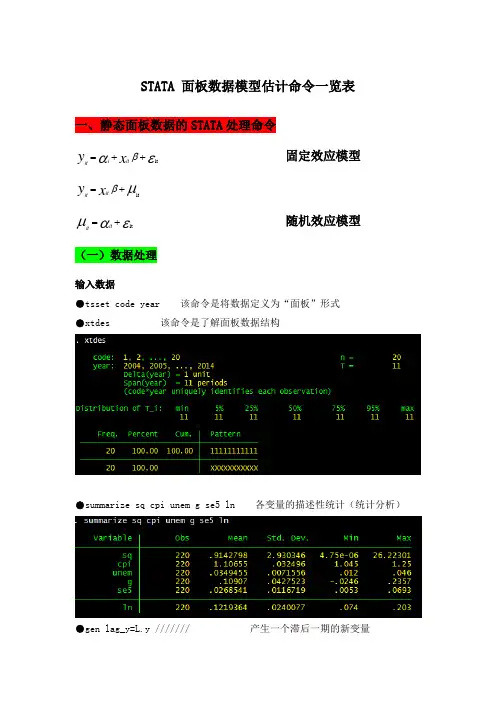

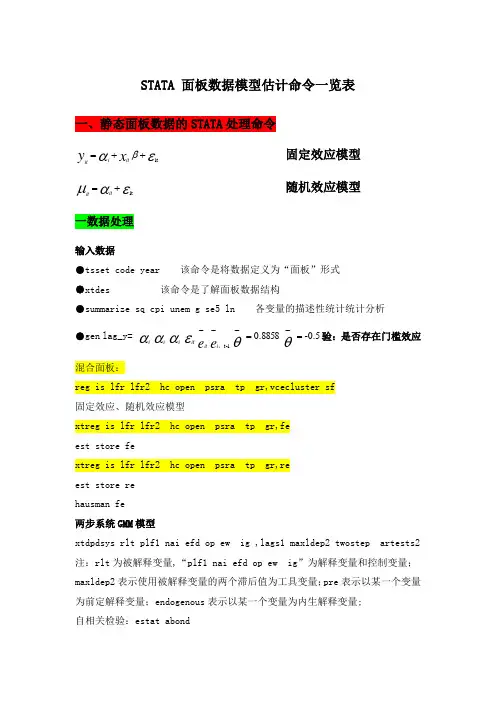

面板PCSE估计stata操作

- 格式:pdf

- 大小:54.27 KB

- 文档页数:2

面板PCSE估计stata操作步骤

面板模型回归结果对样本数据的方差极为敏感,行业面板数据会

因为不同行业规模差异往往存在较严重的异方差,而且面板自相关也

不容忽视,为得到一致回归结果,我们可以采用PCSE(panel-corrected

standard error)方法进行稳健估计。运用PCSE估计,首先要检验面

板数据是否存异方差和自相关问题。

一、异方差检验

命令:

. xtgls y x1 x2 x3,igls panel(het)

. estimates store hetero

. xtgls y x1 x2 x3,igls

. estimates store homo

. local df = e(N_g) - 1

. lrtest hetero homo, df(`df')

注意:原假设为面板数据扰动项属于同方差。

输出结果示范: (Assumption: homo nested in hetero) Prob > chi2 = 0.0000Likelihood-ratio test LR chi2(19) = 362.04. lrtest hetero homo, df(`df')

结果解读:P值等于0,因此结果拒绝原假设,即认为存在异方差。

二、自相关检验

首先安装一个小程序

. net install st0039

然后用下面命令皆可检验自相关问题:

. xtserial fatal beertax spircons unrate

输出结果示范:

Prob > F = 0.0000 F( 1, 19) = 53.595H0: no first-order autocorrelationWooldridge test for autocorrelation in panel data

注意:只能检验组内自相关,不能检验其他形式自相关。而且,原假

设为无自相关。

结果解读:P值等于0,因此结果拒绝原假设,即认为存在自相关。

三、PCSE估计

由于第一步和第二步检验结果表明样本数据存在异方差和自相

关,因此采用PCSE估计会得到稳健结果。

具体命令为:

xtpcse y x1 x2 x3,corr(ar1)

或者:

xtpcse y x1 x2 x3,corr(psar1)