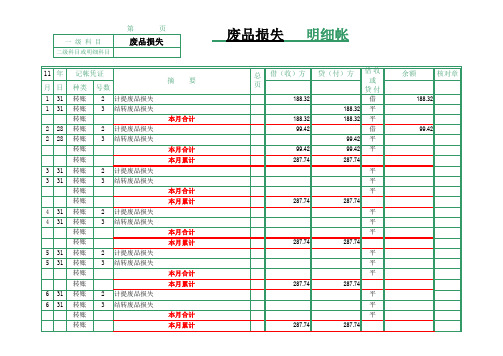

生产成本明细账简易版

- 格式:pdf

- 大小:36.85 KB

- 文档页数:1

辅助生产成本明细账

车间:**辅助生产车间20**年*月*日单位:元

直接分配法

顺序分配法

交互分配法

计划成本分配法

代数分配法

会计分录

借:制造费用——基本车间——一车间

——基本车间——二车间

管理费用

贷:辅助生产成本——供水车间

——供电车间

制造费用明细帐

车间:**辅助生产车间20**年*月*日单位:元

实际分配率分配法

预计分配率分配法

会计分录

借:基本生产成本——甲

——乙

——丙

贷:制造费用

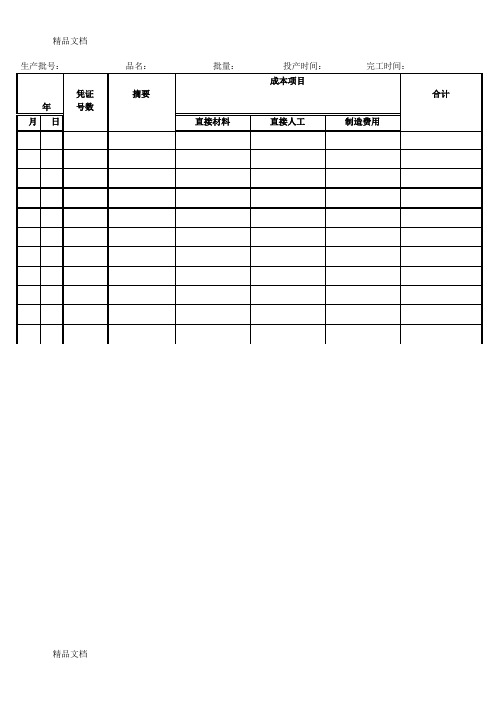

产品成本明细账

车间:**车间产品品种(或批次):*产品(或*批次)在产品数:** 完工产品数:**

倒挤法:

1、在产品数量少,成本低

2、在产品数量多,各期均衡

3、在产品按定额成本

4、在产品按耗材料成本计算

分配法:

1、按在产品和完工产品实际数量分配

2、约当产量法

3、定额分配法

会计分录

借:库存商品

贷:基本生产成本。

砂石生产成本的表格模板

说明:

1.原材料:指砂石生产所需的主要原材料,如砂、石等。

根据实际消耗量和市场价格进行填写。

2.燃料及动力:指生产过程中所需的燃料、电力等能源消耗。

根据实际消耗量和市场价格进行填写。

3.工资及福利:指生产人员的工资和福利支出。

根据实际发放情况和相关政策进行填写。

4.折旧及摊销:指生产设备的折旧和无形资产的摊销费用。

根据实际折旧和摊销情况进行填写。

5.维修及保养:指生产设备的维修和保养费用。

根据实际支出情况进行填写。

6.其他费用:指除上述成本项目外的其他生产相关费用。

根据实际情况进行填写。

7.总成本:将上述各项成本相加,得出总成本。

生产成本明细账和管理费用明细账的格式生产成本明细账是用来记录生产过程中所涉及的各种成本,包括原材料、加工费用、人工费用等,以及这些成本的变动情况。

下面是一种常用的生产成本明细账格式:| 日期 | 成本项目 | 原始单据号 | 借方金额 | 贷方金额 | 余额 || --- | --- | --- | --- | --- | --- || 1月1日 | 原材料 | 001 | 10,000.00 | | 10,000.00 || 1月2日 | 加工费用 | 002 | 5,000.00 | | 15,000.00 || 1月3日 | 人工费用 | 003 | 3,000.00 | | 18,000.00 || 1月4日 | 直接材料转入 | 004 | | 13,000.00 | 5,000.00 || 1月5日 | 成品入库 | 005 | | 30,000.00 | 25,000.00 |该表格的各列含义如下:日期:记录该笔成本发生的日期。

成本项目:有多种不同成本项目,如原材料、加工费用、人工费用等,可以按照实际情况进行分类。

原始单据号:表示该笔成本所涉及的原始单据号。

借方金额:表示该笔成本的加减情况。

如果是成本增加,则记录在借方金额中;如果是成本减少,则记录在贷方金额中。

贷方金额:同上。

余额:表示该笔成本发生后,账户余额的情况。

管理费用明细账是用来记录企业在管理过程中的各种费用,如办公用品、水电费、差旅费、人力资源费用等。

下面是一种常用的管理费用明细账格式:费用项目:按照不同的费用项目进行分类,如办公用品、水电费、差旅费、人力资源费用等。

需要注意的是,以上表格仅供参考学习之用,请根据实际情况进行合理调整。

生产成本明细账生产成本明细账是企业在生产过程中所记录的重要账目之一,它直接反映了生产过程中所涉及的各种成本及其变动情况,所以对于企业来说是非常重要的。

1. 要根据实际情况合理分类记录:生产成本包括原材料、加工费用、人工费用等等,可以按照不同的成本项目进行分类记录,以方便进行统计分析和对应的会计处理。

生产成本明细账模板英文回答:Cost accounting plays a crucial role in managing and analyzing the production costs of a business. Toeffectively track and control these costs, a detailed cost ledger or cost detail account template is essential. This template provides a systematic record of all the costs incurred during the production process, allowing businesses to identify areas of inefficiency and make informed decisions to optimize their operations.A cost detail account template typically includes various categories to capture different types of costs. These categories may include direct materials, direct labor, manufacturing overhead, and other indirect costs. For each cost category, the template should provide columns torecord the date, description of the cost, quantity, unit cost, and total cost. Additionally, it is important to have a column to indicate the specific job or product to whichthe cost is allocated.Let's take the example of a manufacturing company that produces furniture. The cost detail account template for this company would have separate sections for direct materials, direct labor, and manufacturing overhead. Under the direct materials section, the template would include columns to record the date of purchase, description of the material, quantity purchased, unit cost, and total cost. For instance, if the company purchases wood for making chairs, the template would show the date of purchase, the description of the wood, the quantity purchased (e.g., 100 board feet), the unit cost (e.g., $5 per board foot), and the total cost (e.g., $500).Similarly, the direct labor section of the template would capture the labor costs associated with the production process. It would include columns for the date of labor, description of the work performed, hours worked, hourly rate, and total labor cost. For example, if a worker spends 8 hours assembling chairs at an hourly rate of $20, the template would record the date, the description of thework (e.g., chair assembly), the hours worked (8), thehourly rate ($20), and the total labor cost ($160).The manufacturing overhead section of the templatewould account for indirect costs such as utilities, rent, and equipment depreciation. It would include columns forthe date, description of the overhead cost, allocation base (e.g., direct labor hours or machine hours), allocation rate, and total overhead cost. For instance, if the company allocates overhead costs based on direct labor hours andthe allocation rate is $10 per hour, the template would record the date, the description of the overhead cost (e.g., electricity bill), the allocation base (e.g., 20 directlabor hours), the allocation rate ($10 per hour), and the total overhead cost ($200).By using a cost detail account template, businesses can easily summarize and analyze their production costs. They can calculate the total cost per unit for each job or product, identify cost variances, and make informed decisions to improve efficiency and profitability.中文回答:成本会计在管理和分析企业生产成本方面起着至关重要的作用。

生产成本明细账登记方法

嘿,朋友们!今天咱就来好好唠唠生产成本明细账的登记方法。

这

生产成本明细账啊,就像是一个大账本,把生产过程中的各种花销都

明明白白地记下来。

咱先说说这材料成本的登记。

就好比咱做饭,买菜买调料得一笔笔

记清楚吧,不然你都不知道这顿饭花了多少钱。

生产也是一样啊,买

原材料的钱就得准确登记到明细账里。

然后是人工成本,工人们干活发的工资,那也得记下来呀。

这就好

像你请朋友帮忙做事,给人家的报酬总得心里有数吧。

还有那些制造费用,什么水电费啦,设备折旧费啦,这些杂七杂八

的费用可都不能落下。

就跟你家里的水电费账单似的,都得一一记录

清楚。

登记的时候可得仔细喽,不能记错了地方,不然就像你找东西放错

了抽屉,到时候可就难找啦。

而且要及时登记,别等过了好久才想起来,那可就容易记混啦。

咱可以想象一下,如果没有好好登记生产成本明细账,那会咋样?

那不就像闭着眼睛走路,稀里糊涂的,到最后都不知道钱花哪儿去了,这企业还怎么经营得好呀。

每一笔账都要认真对待,就像对待宝贝似的。

别嫌麻烦,这可是关系到企业的效益和发展呢。

而且登记的时候要规范,数字要写清楚,别写得模模糊糊让人看不清。

再打个比方,这生产成本明细账就像是企业的健康档案,能让我们清楚地了解企业的生产状况,有没有哪里开销过大啦,哪里可以节约成本啦。

总之呢,生产成本明细账的登记方法可重要啦,大家一定要重视起来呀!把每一笔账都登记准确、详细,这样企业才能更好地发展,我们的工作也才更有意义呀!这可不是闹着玩的,大家可得记牢了哦!。