投资学 (博迪) 第10版课后习题答案19 Investments 10th Edition Textbook Solutions Chapter 19

- 格式:pdf

- 大小:148.42 KB

- 文档页数:11

Chapter 10 - Arbitrage Pricing Theory and Multifactor Models of Risk and Return

10-1

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education. CHAPTER 10: ARBITRAGE PRICING THEORY AND

MULTIFACTOR MODELS OF RISK AND RETURN

PROBLEM SETS

1. The revised estimate of the expected rate of return on the stock would be the old

estimate plus the sum of the products of the unexpected change in each factor times

the respective sensitivity coefficient:

Revised estimate = 12% + [(1 × 2%) + (0.5 × 3%)] = 15.5%

Note that the IP estimate is computed as: 1 × (5% - 3%), and the IR estimate is

computed as: 0.5 × (8% - 5%).

2. The APT factors must correlate with major sources of uncertainty, i.e., sources of

uncertainty that are of concern to many investors. Researchers should investigate

投资学10版习题答案

CHAPTER 14: BOND PRICES AND YIELDS

PROBLEM SETS

1. a. Catastrophe bond—A bond that allows the issuer to transfer

“catastrophe risk” from the firm to the capital markets. Investors in

these bonds receive a compensation for taking on the risk in the form of

higher coupon rates. In the event of a catastrophe, the bondholders will

receive only part or perhaps none of the principal payment due to them

at maturity. Disaster can be defined by total insured losses or by criteria

such as wind speed in a hurricane or Richter level in an earthquake.

b. Eurobond—A bond that is denominated in one currency, usually that

of the issuer, but sold in other national markets.

c. Zero-coupon bond—A bond that makes no coupon payments. Investors

receive par value at the maturity date but receive no interest payments

until then. These bonds are issued at prices below par value, and the

1 / 106

十万种考研考证电子书、题库视频学习平台 圣才电子书

第四部分 固定收益证券

第14章 债券的价格与收益

一、选择题

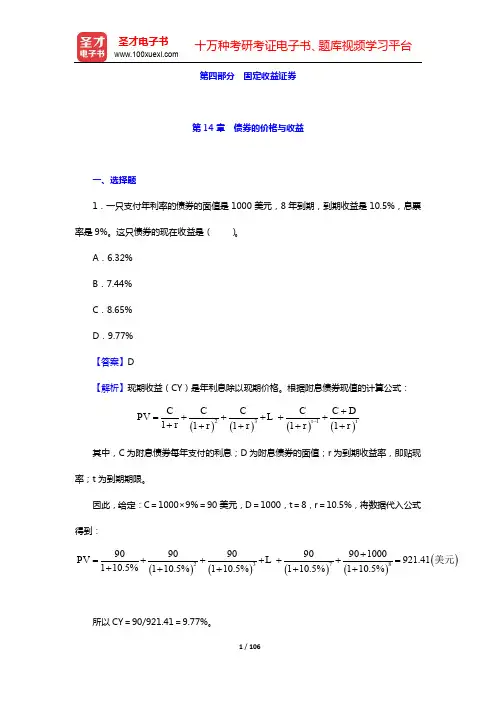

1.一只支付年利率的债券的面值是1000美元,8年到期,到期收益是10.5%,息票

率是9%。这只债券的现在收益是( )。 A.6.32% B.7.44% C.8.65%

D.9.77%

【答案】D

【解析】现期收益(CY)是年利息除以现期价格。根据附息债券现值的计算公式:

23111111ttCCCCCDPV

rrrrr

L

其中,C为附息债券每年支付的利息;D为附息债券的面值;r为到期收益率,即贴现

率;t为到期期限。

因此,给定:C=1000×9%=90美元,D=1000,t=8,r=10.5%,将数据代入公式

得到:

237890909090901000921.41

110.5%110.5%110.5%110.5%110.5%PV

L美元

所以CY=90/921.41=9.77%。

2 / 106

十万种考研考证电子书、题库视频学习平台 圣才电子书

2.一只息票债券的卖出价在《华尔街日报》上显示为1080(也就是面值1000美元的

108%)。如果最后一次的利息支付是两个月以前,息票率为12%,那么这只债券的发票价

格是( )美元。

A.1080

B.1100

C.1120

D.1210

【答案】B

【解析】债券的价格是108%×1000=1080美元,债券产生的利息:(0.12/12)×1000

=10(美元/月)。因为最后一次的利息支付在2个月以前,那么付息后的这两个月所产生

的利息就是2×10=20美元。因此,债券的发票价格=市场价格+产生的利息=1080美元

+20美元=1100美元。

3.票面利率为10%的附息债券其到期收益率为8%,如果到期收益率不变,则一年以

投资学10版习题答案10 Chapter 10 - Arbitrage Pricing Theory and Multifactor Models of Risk and Return

10-1

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education. CHAPTER 10: ARBITRAGE PRICING THEORY AND

MULTIFACTOR MODELS OF RISK AND RETURN

PROBLEM SETS

1. The revised estimate of the expected rate of return on the stock would be the

old estimate plus the sum of the products of the unexpected change in each

factor times the respective sensitivity coefficient:

Revised estimate = 12% + [(1 × 2%) + (0.5 × 3%)] = 15.5%

Note that the IP estimate is computed as: 1 × (5% - 3%), and the IR estimate is

computed as: 0.5 × (8% - 5%).

2. The APT factors must correlate with major sources of uncertainty, i.e., sources

of uncertainty that are of concern to many investors. Researchers should