Exponential and power-law probability distributions of wealth and income in the United King

- 格式:pdf

- 大小:150.55 KB

- 文档页数:8

arXiv:cond-mat/0103544v2 [cond-mat.stat-mech] 28 Mar 2001Exponentialandpower-lawprobabilitydistributionsofwealthandincomeintheUnitedKingdomandtheUnitedStates

AdrianDr˘agulescu,VictorM.Yakovenko1DepartmentofPhysics,UniversityofMaryland,CollegePark,MD20742-4111,cond-mat/0103544,v.2March28,2001USA

1IntroductionThestudyofwealthandincomedistributionshasalonghistory.Pareto[1]proposedin1897thatwealthandincomedistributionsobeyuniversalpowerlaws.Subsequentstudieshaveoftendisputedthisconjecture(seeasystematicsurveyintheWorldBankresearchpublication[2]).Mandelbrot[3]proposedthattheParetolawappliesonlyasymptoticallytothehighendsofthedis-tributions.ManyresearcherstriedtodeducetheParetolawfromatheoryofstochasticprocesses.Gibrat[4]proposedin1931thatincomeandwealtharegovernedbymultiplicativerandomprocesses,whichresultinalog-normaldistribution.Theseideaswerelaterfollowed,amongmanyothers,byMon-trollandShlesinger[5].However,alreadyin1945Kalecki[6]pointedoutthatthelog-normaldistributionisnotstationary,becauseitswidthincreasesintime.Moderneconophysicists[7–9]alsousevariousversionsofmultiplicativerandomprocessesintheoreticalmodelingofwealthandincomedistributions.Unfortunately,numerousrecentpapersonthissubjectdoverylittleornocomparisonatallwithrealstatisticaldata,muchofwhichiswidelyavailablethesedaysontheInternet.Inordertofillthisgap,weanalyzedthedataonincomedistributionintheUnitedStates(US)fromtheBureauofCensusandtheInternalRevenueService(IRS)inRef.[10].Wefoundthattheindivid-ualincomeofabout95%ofpopulationisdescribedbytheexponentiallaw.Theexponentiallaw,alsoknowninphysicsastheBoltzmann-Gibbsdistribu-tion,ischaracteristicforaconservedvariable,suchasenergy.InRef.[11],wearguedthat,becausemoney(cash)isconserved,theprobabilitydistributionofmoneyshouldbeexponential.Wealthcanincreaseordecreasebyitself,butmoneycanonlybetransferredfromoneagenttoanother.So,wealthisnotconserved,whereasmoneyis.Thedifferenceisthesameasthedifferencebetweenunrealizedandrealizedcapitalgainsinstockmarket.Unfortunately,wewerenotabletofinddataonthedistributionofmoney.Ontheotherhand,wefounddataonwealthdistributionintheUnitedKing-dom(UK),whicharepresentedinthispaper.AlsopresentedaretheincomedistributiondatafortheUKandfortheindividualstatesoftheUSA.Inallofthesedata,wefindthatthegreatmajorityofpopulationisdescribedbyanexponentialdistribution,whereasthehigh-endtailfollowsapowerlaw.

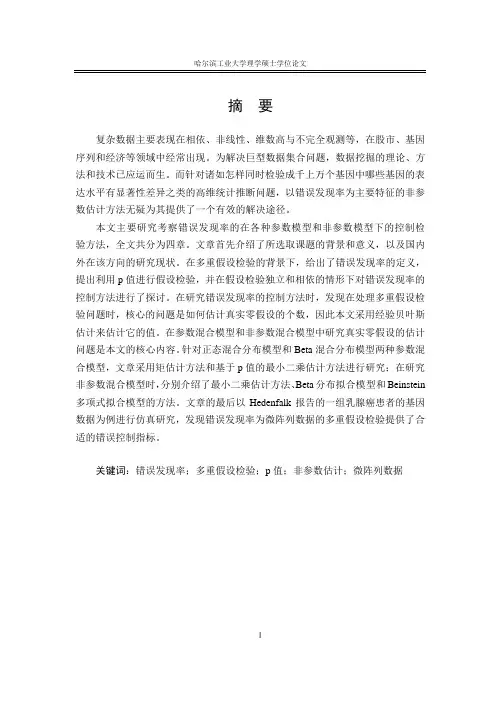

2WealthdistributionintheUnitedKingdomInthissection,wediscussthecumulativeprobabilitydistributionofwealthN(w)=(thenumberofpeoplewhoseindividualwealthisgreaterthanw)/(thetotalnumberofpeople).AplotofNvs.wisequivalenttoaplotofper-son’srankinwealthvs.wealth,whichisoftenusedfortopreachpeople[12].Wewillusethepowerlaw,N(w)∝1/wα,andtheexponentiallawN(w)∝exp(−w/W),tofitthedata.Thesedistributionsarecharacterizedbytheexponentαandthe“temperature”W.Thecorrespondingprobabil-itydensities,P(w)=−dN(w)/dw,alsofollowapowerlaworanexponen-tiallaw.Fortheexponentiallaw,itisalsousefultodefinethetemperaturesW(2)(alsoknownasthemedian)andW(10)usingthebasesof1/2and1/10:N(w)∝(1/2)w/W(2)∝(1/10)w/W(10).Thedistributionofwealthisnoteasytomeasure,becausepeopledonotreporttheirtotalwealthroutinely.However,whenapersondies,allassetsmustbereportedforthepurposeofinheritancetax.Usingthesedataandanadjustmentprocedure,theBritishtaxagency,theInlandRevenue(IR),recon-structedwealthdistributionofthewholeUKpopulation.InFig.1,wepresentthe1996dataobtainedfromtheirWebsite[13].Theleftpanelshowsthecu-mulativeprobabilityasafunctionofthepersonaltotalnetcapital(wealth),whichiscomposedofassets(cash,stocks,property,householdgoods,etc.)andliabilities(mortgagesandotherdebts).Themainpanelillustratesinthe

21010010000.01%0.1%1%10%100% Total net capital (wealth), kpoundsCumulative percent of people

United Kingdom, IR data for 1996

ParetoBoltzmann−Gibbs

02040608010010%100%

Total net capital, kpounds0102030405060708090100%0

10

2030405060708090100%Cumulative percent of peopleCumulative percent of wealth

United Kingdom, IR data for 1996

Fig.1.Cumulativeprobabilitydistributionoftotalnetcapital(wealth)showninlog-log(leftpanel),log-linear(inset),andLorenz(rightpanel)coordinates.Points:theactualdata.Solidlines:leftpanel–fitstotheexponential(Boltzmann-Gibbs)andpower(Pareto)laws,rightpanel–function(2)calculatedfortheexponentiallaw.

log-logscalethatabove100k£thedatafollowapowerlawwiththeexpo-nentα=1.9.Theinsetshowsinthelog-linearscalethatbelow100k£thedataisverywellfittedbyanexponentialdistributionwiththetemperatureWUK=59.6k£(W(2)UK=41.3k£andW(10)UK=137.2k£).TherightpanelofFig.1showstheso-calledLorenzcurve[2,10]forwealthdistribution.Thehorizontalandverticalcoordinatesarethecumulativepop-ulationx(w)andthecumulativewealthy(w):