Corporate Governance Corporate Governance Jean Tir

- 格式:pdf

- 大小:693.23 KB

- 文档页数:36

公司的治理威廉姆森(1985)直接把企业看做是一种治理结构。

特里克尔(1993)认为公司治理包含了对现代企业行使权力的整个过程。

凯德伯瑞(1993)认为公司治理是掌握、指导和控制公司制度和过程。

青木昌彦(1995)认为公司治理的实质就是控制内部人控制。

钱颖一认为,公司治理是一套制度安排,用以支配若干在公司中有重大利害关系的团体——投资人、经理人、职工之间的关系,并从这种联盟中实现经济利益。

张维迎(1998)认为公司治理结构就是一种解决股份公司内部各种代理问题的机制。

吴敬琏认为,治理结构就是所有者、董事会和高级经理人员三者组成的一种组织结构,三者之间相互作用形成的一种制衡关系。

费方域认为,公司治理的本质就是一种关系契约。

经济学的主导观点是,公司治理是关于“公司的出资者会采取何种方式来保证他们自己从投资中获得回报”。

因此,在这个观点下的研究主要集中于如何保证公司的内部人能够可信地向外部投资者支付回报,从而能够吸引外部融资。

保证资金供给者必须得到相应的回报,而保证投资回报的主要途径就是将最关键的企业所有权配置给最主要的投资者。

这种观点在资本占绝对主导地位的企业中具有合理性,但随着科学技术的不断进步,特别是人力资本在企业中整个国民经济中地位的不断提高,表现出明显的局限性。

1、缺乏透明度2、报酬的水平3、绩效和报酬不成比例(1)、经理人报酬的结构可能不合理。

(2)、经理人的绩效和报酬存在反比情况。

(3)、经理人可以“及时脱身”。

(4)、经理人离开公司时,还能得到金色降落伞的保护。

4、会计造假(一)日本的契约治理1、治理与控制。

2、隐性的关系契约。

3、管理互动和终生雇佣。

4、监督和信息共享。

5、交叉持股。

6、选择性干预(Selective Intervention ) (二)德国的契约治理1、德国公司的所有权结构。

2、董事会组成。

3、小圈子和声誉效应(三)比较和结论1、日本契约优点:日本的契约治理最终可被视作一种以确保投资双方最大利益为目的的理性尝试。

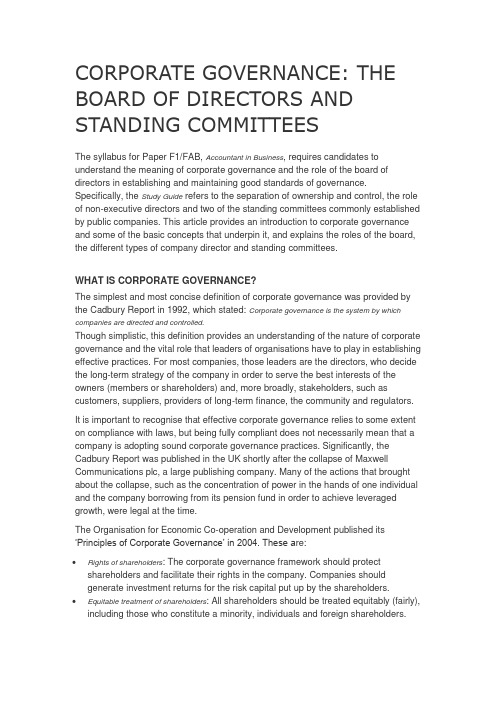

CORPORATE GOVERNANCE: THE BOARD OF DIRECTORS AND STANDING COMMITTEESThe syllabus for Paper F1/FAB, Accountant in Business, requires candidates to understand the meaning of corporate governance and the role of the board of directors in establishing and maintaining good standards of governance. Specifically, the Study Guide refers to the separation of ownership and control, the role of non-executive directors and two of the standing committees commonly established by public companies. This article provides an introduction to corporate governance and some of the basic concepts that underpin it, and explains the roles of the board, the different types of company director and standing committees.WHAT IS CORPORATE GOVERNANCE?The simplest and most concise definition of corporate governance was provided by the Cadbury Report in 1992, which stated: Corporate governance is the system by which companies are directed and controlled.Though simplistic, this definition provides an understanding of the nature of corporate governance and the vital role that leaders of organisations have to play in establishing effective practices. For most companies, those leaders are the directors, who decide the long-term strategy of the company in order to serve the best interests of the owners (members or shareholders) and, more broadly, stakeholders, such as customers, suppliers, providers of long-term finance, the community and regulators.It is important to recognise that effective corporate governance relies to some extent on compliance with laws, but being fully compliant does not necessarily mean that a company is adopting sound corporate governance practices. Significantly, the Cadbury Report was published in the UK shortly after the collapse of Maxwell Communications plc, a large publishing company. Many of the actions that brought about the collapse, such as the concentration of power in the hands of one individual and the company borrowing from its pension fund in order to achieve leveraged growth, were legal at the time.The Organisation for Economic Co-operation and Development published its‘Principles of Corporate Governance’ in 2004. These a re:∙Rights of shareholders: The corporate governance framework should protect shareholders and facilitate their rights in the company. Companies shouldgenerate investment returns for the risk capital put up by the shareholders.∙Equitable treatment of shareholders: All shareholders should be treated equitably (fairly), including those who constitute a minority, individuals and foreign shareholders.Shareholders should have redress when their rights are contravened or where an individual shareholder or group of shareholders is oppressed by the majority.∙Stakeholders: The corporate governance framework should recognise the legal rights of stakeholders and facilitate cooperation with them in order to create wealth,employment and sustainable enterprises.∙Disclosure and transparency: Companies should make relevant, timely disclosures on matters affecting financial performance, management and ownership of thebusiness.∙Board of directors: The board of directors should set the direction of the company and monitor management in order that the company will achieve its objectives. The corporate governance framework should underpin the board’s accountability to the company and its members.TO WHOM IS CORPORATE GOVERNANCE RELEVANT?Corporate governance is important in all but the smallest organisations. Limited companies have a primary duty to their shareholders, but also to other stakeholders as described above. Not-for-profit organisations must also be directed and controlled appropriately, as the decisions and actions of a few individuals can affect many individuals, groups and organisations that have little or no influence over them. Public sector organisations have a duty to serve the State but must act in a manner that treats stakeholders fairly.Most of the attention given to corporate governance is directed towards public limited companies whose securities are traded in recognised capital markets. The reason for this is that such organisations have hundreds or even thousands of shareholders whose wealth and income can be enhanced or compromised by the decisions of senior management. This is often referred to as the agency problem. Potential and existing shareholders take investment decisions based on information that is historical and subjective, usually with little knowledge of the direction that the company will take in the future. They therefore place trust in those who take decisions to achieve the right balance between return and risk, to put appropriate systems of control in place, to provide timely and accurate information, to manage risk wisely, and to act ethically at all times.The agency problem becomes most evident when companies fail. In order to make profits, it is necessary to take risks, and sometimes risks that are taken with the best intentions – and are supported by the most robust business plans – result in loss or even the demise of the company. Sometimes corporate failure is brought about by inappropriate behaviours of directors and other senior managers.As already mentioned, in the UK, corporate governance first came into the spotlight with the publication of the Cadbury Report, shortly after two large companies (Maxwell Communications plc and Polly Peck International plc) collapsed. Ten years later, in the US, the Sarbanes-Oxley Act was passed as a response to the collapse of Enron Corporation and WorldCom. All of these cases involved companies that had beenhighly successful and run by a few very powerful individuals, and all involved some degree of criminal activity on their part.The recent credit crisis has brought about renewed concern about corporate governance, specifically in the financial sector. Although the roots of the crisis were mainly financial and originated with adverse conditions in the wholesale money markets, subsequent investigations and reports have called into question the policies, processes and prevailing cultures in many banking and finance-related organisations.APPROACHES TO CORPORATE GOVERNANCEMost countries adopt a principles-based approach to corporate governance. This involves establishing a comprehensive set of best practices to which listed companies should adhere. If it is considered to be in the best interests of the company not to follow one or more of these standards, the company should disclose this to its shareholders, along with the reasons for not doing so. This does not necessarily mean that a principles-based approach is a soft option, however, as it may be a condition of membership of the stock exchange that companies strictly follow this‘comply or explain’ requirement.Some countries prefer a rules-based approach through which the desired corporate governance standards are enshrined in law and are therefore mandatory. The best example of this is the US, where the Sarbanes-Oxley Act lays down detailed legal requirements.THE ROLE OF THE BOARD OF DIRECTORSNearly all companies are managed by a board of directors, appointed or elected by the shareholders to run the company on their behalf. In most countries, the directors are subject to periodic (often annual) re-election by the shareholders. This would appear to give the shareholders ultimate power, but in most sectors it is recognised that performance can only be judged over the medium to long-term. Shareholders therefore have to place trust in those who act on their behalf. It is rare but not unknown for shareholders to lose patience with the board and remove its members en masse.The role of the board of directors was summarised by the King Report (a South African report on corporate governance) as:∙to define the purpose of the company∙to define the values by which the company will perform its daily duties∙to identify the stakeholders relevant to the company∙to develop a strategy combining these factors∙to ensure implementation of this strategy.The purpose and values of a company are often set down in its constitutional documents, reflecting the objectives of its founders. However, it is sometimes appropriate for the board to consider whether it is in the best interests of those servedby the company to modify this or even change it completely. For example, NCR Corporation is a US producer of automated teller machines and point-of-sale systems, but its origins lay in mechanical accounting machines (NCR represents National Cash Register). As cash registers would quickly become obsolete with the emergence of microchip technology, the company had to adapt very rapidly. Whitbread plc originated as a brewer in the 18th century in the UK, but in the 1990s redefined its mission and objectives completely. It is now a hospitality and leisure provider (its brands include Premier Inn and Costa coffee) and has abandoned brewing completely.The directors must take a long-term perspective of the road that the company must travel. Management writer William Ouchi attributes the enduring success of many Japanese companies to their ability to avoid short-term ‘knee-jerk’ reactions to immediate issues in favour of consensus over the best direction to take in thelong-term.STRUCTURE OF THE BOARD OF DIRECTORSThere is no convenient formula for defining how many directors a company should have, though in some jurisdictions company law specifies a minimum and/or maximum number of directors for different types of company. Tesco plc, a large multinational supermarket company, has 13 directors. Swire Pacific Limited, a large Hong Kong conglomerate, has 18 directors. Smaller listed companies generally have fewer directors, typically six to eight persons.The board of directors is made up of executive directors and non-executive directors. Executive directors are full-time employees of the company and, therefore, have two relationships and sets of duties. They work for the company in a senior capacity, usually concerned with policy matters or functional business areas of major strategic importance. Large companies tend to have executive directors responsible for finance, IT/IS, marketing and so on.Executive directors are usually recruited by the board of directors. They are the highest earners in the company, with remuneration packages made up partly of basic pay and fringe benefits and partly performance-related pay. Most large companies now engage their executive directors under fixed term contracts, often rolling over every 12 months.The chief executive officer (CEO) and the finance director (in the US, chief financial officer) are nearly always executive directors.Non-executive directors (NEDs) are not employees of the company and are not involved in its day-to-day running. They usually have full-time jobs elsewhere, or may sometimes be prominent individuals from public life. The non-executive directors usually receive a flat fee for their services, and are engaged under a contract for service (civil contract, similar to that used to hire a consultant).NEDs should provide a balancing influence and help to minimise conflicts of interest. The Higgs Report, published in 2003, summarised their role as:∙to contribute to the strategic plan∙to scrutinise the performance of the executive directors∙to provide an external perspective on risk management∙to deal with people issues, such as the future shape of the board and resolution of conflicts.The majority of non-executive directors should be independent. Factors to be considered in assessing their independence include their business, financial and other commitments, other shareholdings and directorships and involvement in businesses connected to the company. However, holding shares in the company does not necessarily compromise independence.Non-executive directors should have high ethical standards and act with integrity and probity. They should support the executive team and monitor its conduct, demonstrating a willingness to listen, question, debate and challenge.It is now recognised as best practice that a public company should have more non-executive directors than executive directors. In Tesco plc, there are five executive directors and eight independent non-executive directors. Swire Pacific Ltd has eight executive directors and 10 non-executive directors, of which six are independent non-executive directors.An individual may be accountable in law as a shadow director. A shadow director is a person who controls the activities of a company, or of one or more of its actual directors, indirectly. For example, if a person who is unconnected with a company gives instructions to a person who is a director of the company, then the second person is an actual director while the first person is a shadow director. In some jurisdictions, shadow directors are recognised as being as accountable in law as actual directors.UNITARY V TWO-TIER BOARDSThe unitary board model is adopted by, inter alia, companies in the UK, US, Australia and South Africa. The company’s directors serve together on one board comprising both executive and non-executive directors.In many countries in continental Europe, companies adopt a two-tier structure. This separates those responsible for supervision from those responsible for operations. The supervisory board generally oversees the operating board.Paper FAB, Accountant in Business, focuses mainly on the unitary board system, though knowledge of both models is required for subsequent studies for Paper P1,Governance, Risk and Ethics.KEY POSITIONSThe chairman of the company is the leader of the board of directors. It is the chairman’s responsibility to ensure that the board operates efficiently and effectively, get the best out of all of its members. The chairman should, for example, promote regular attendance and full involvement in discussions. The chairman decides thescope of each meeting and is responsible for time management of board meetings, ensuring all matters are discussed fully, but without spending limitless time on individual agenda items. In most companies the chairman is a non-executive director. The chief executive officer (CEO) is the leader of the executive team and is responsible for the day-to-day management of the organisation. As such, this individual is nearly always an executive director. As well as attending board meetings in his or her capacity as a director, the CEO will usually chair the management committee or executive committee. While most companies have monthly board meetings, it is common for management/executive committee meetings to be weekly.The secretary is the chief administrative officer of the company. The secretary provides the agenda and supporting papers for board meetings, and often for executive committee meetings also. He or she takes minutes of meetings and provides advice on procedural matters, such as terms of reference. The secretary usually has responsibilities for liaison with shareholders and the government registration body. As such, the notice of general meetings will be signed by the secretary on behalf of the board of directors. The secretary may be a member of the board of directors, though some smaller companies use this position as a means of involving a high potential individual at board level prior to being appointed as a director.SEGREGATION OF RESPONSIBILITIESIt is generally recognised that the CEO should not hold the position of chairman, as the activities of each role are quite distinctive from one another. In larger companies, there would be too much work for one individual, though in Marks & Spencer, a large listed UK retail organisation, one person did occupy both positions for several years.The secretary should not also be the chairman of the company. As the secretary has a key role in liaising with the government registration body, having the same person occupying both roles could compromise the flow of information between this body and the board of directors.STANDING COMMITTEESThe term ‘standing committee’ refers to any committee that is a permanent feature within the management structure of an organisation. In the context of corporate governance, it refers to committees made up of members of the board with specified sets of duties. The four committees most often appointed by public companies are the audit committee, the remuneration committee, the nominations committee and the risk committee.The Syllabus and Study Guide for Paper F1/FAB require students to study only two committees. These are the audit committee and the remuneration committee.AUDIT COMMITTEEThis committee should be made up of independent non-executive directors, with at least one individual having expertise in financial management. It is responsible for:∙oversight of internal controls; approval of financial statements and other significant documents prior to agreement by the full board∙liaison with external auditors∙high level compliance matters∙reporting to the shareholders.Sometimes the committee may carry out investigations and may deal with matters reported by whistleblowers.REMUNERATION COMMITTEEThis committee decides on the remuneration of executive directors, and sometimes other senior executives. It is responsible for formulating a written remuneration policy that should have the aim of attracting and retaining appropriate talent, and for deciding the forms that remuneration should take. This committee should also be made up entirely of independent non-executive directors, consistent with the principle that executives should not be in a position to decide their own remuneration.It is generally recognised that executive remuneration packages should be structured in a manner that will motivate them to achieve the long-term objectives of the company. Therefore, the remuneration committee has to offer a competitive basic salary and fringe benefits (these attract and retain people of the right calibre), combined with performance-related rewards such as bonuses linked to medium and long-term targets, shares, share options and eventual pension benefits (often subject to minimum length of service requirements).PUBLIC OVERSIGHTPublic oversight is concerned with ensuring that the confidence of investors and the general public in professional accountancy bodies is maintained. This can be achieved by direct regulation, the imposition of licensing requirements (including, where appropriate, exercising powers of enforcement) or by self-regulation. As the US operates a rules-based system of governance, these responsibilities are discharged by the Public Company Accounting Oversight Board, which has the power to enforce mandatory standards and rules laid down by the Sarbanes-Oxley Act. In the UK, regulation is the responsibility of the Professional Oversight team of the Financial Reporting Council.SAMPLE QUESTIONSCandidates may find it useful to consider questions on this topic identified in examiner’s reports as well as the pilot paper. As past questio n papers are not made available, the following questions are included in this article as examples of typical requirements. It must be emphasised that these questions are not taken from the actual question bank.Sample question 1:LLL Company is listed on its country’s stock exchange. The following individuals serve on the board of directors:Asif is a non-executive director and is the chairman of the company.Bertrand is the CEO and is responsible for the day-to-day running of the company. Chan is a professional accountant and serves as a non-executive director.Donna is the finance director and is an employee of the company.Esther is a legal advocate and serves as a non-executive director.Frederik is the marketing director of a manufacturing company and serves as anon-executive director.Which of the following is the most appropriate composition of directors for LLL Company’s audit committee?A Chan, Donna and EstherB Asif, Bertrand and FrederikC Asif, Esther and FrederikD Chan, Esther and FrederikThe correct answer is D. Executive directors should not serve on the audit committee. This eliminates options A and B. Option D is the best choice, as the audit committee should have at least one director with expertise in finance.Sample question 2:Which of the following is a duty of the secretary of a listed public company?A Maintaining order at board meetingsB Clarifying the terms of reference of the board meetingC Ensuring that all directors contribute fully to discussions at board meetingsD Reporting to the board on operational performance for the last quarterThe correct answer is B. Options A and C are responsibilities of the chairman, while option D is the responsibility of the CEO.Sample question 3:The board of directors of JJJ Company has decided to increase the basic salary of its chief executive officer by 20% in order to bring her pay into line with those occupying similar positions in the industry.This action will achieve which of the following purposes?A Improve the prospect of retaining the chief executive officerB Increase the productivity of the chief executive officer by at least 20%C Motivate the chief executive officer to achieve long-term targetsD Create greater job satisfaction for the chief executive officerThe correct answer is A.The basic pay offered by a company serves as a beacon to attract applicants, and can also deter the present incumbent of a position from seeking opportunities elsewhere, especially if they perceive themselves to be underpaid at present.A substantial pay increase is unlikely to achieve a significant increase in productivity or increase long-term motivation (though pay increases can have a short-term impacton motivation). Job satisfaction is derived from factors other than remuneration, such as challenges inherent in the work and the nature of the tasks performed.Written by a member of the Paper F1/FAB examining team。

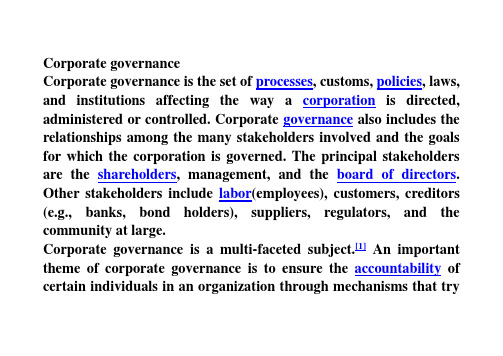

Corporate governanceCorporate governance is the set of processes, customs, policies, laws, and institutions affecting the way a corporation is directed, administered or controlled. Corporate governance also includes the relationships among the many stakeholders involved and the goals for which the corporation is governed. The principal stakeholders are the shareholders, management, and the board of directors. Other stakeholders include labor(employees), customers, creditors (e.g., banks, bond holders), suppliers, regulators, and the community at large.Corporate governance is a multi-faceted subject.[1]An important theme of corporate governance is to ensure the accountability of certain individuals in an organization through mechanisms that tryto reduce or eliminate the principal-agent problem. A related but separate thread of discussions focuses on the impact of a corporate governance system in economic efficiency, with a strong emphasis shareholders' welfare. There are yet other aspects to the corporate governance subject, such as the stakeholder view and the corporate governance models around the worldDefinitionIn A Board Culture of Corporate Governance business author Gabrielle O'Donovan defines corporate governance as 'an internal system encompassing policies, processes and people, which serves the needs of shareholders and other stakeholders, by directing and controlling management activities with good business savvy, objectivity, accountability and integrity. Sound corporategovernance is reliant on external marketplace commitment and legislation, plus a healthy board culture which safeguards policies and processes'.O'Donovan goes on to say that 'the perceived quality of a company's corporate governance can influence its share price as well as the cost of raising capital. Quality is determined by the financial markets, legislation and other external market forces plus how policies and processes are implemented and how people are led. External forces are, to a large extent, outside the circle of control of any board. The internal environment is quite a different matter, and offers companies the opportunity to differentiate from competitors through their board culture. To date, too much of corporate governance debate has centred on legislative policy, to deterfraudulent activities and transparency policy which misleads executives to treat the symptoms and not the cause.'[2]It is a system of structuring, operating and controlling a company with a view to achieve long term strategic goals to satisfy shareholders, creditors, employees, customers and suppliers, and complying with the legal and regulatory requirements, apart from meeting environmental and local community needs.Report of SEBI committee (India) on Corporate Governance defines corporate governance as the acceptance by management of the inalienable rights of shareholders as the true owners of the corporation and of their own role as trustees on behalf of the shareholders. It is about commitment to values, about ethical business conduct and about making a distinction between personal& corporate funds in the management of a company.” The definition is drawn from the Gandhian principle of trusteeship and the Directive Principles of the Indian Constitution. Corporate Governance is viewed as ethics and a moral duty.Role of Institutional InvestorsMany years ago, worldwide, buyers and sellers of corporation stocks were individual investors, such as wealthy businessmen or families, who often had a vested, personal and emotional interest in the corporations whose shares they owned. Over time, markets have become largely institutionalized: buyers and sellers are largely institutions (e.g., pension funds, mutual funds, hedge funds, exchange traded funds, other investor groups; insurance companies, banks, brokers, and other financial institutions).The rise of the institutional investor has brought with it some increase of professional diligence which has tended to improve regulation of the stock market (but not necessarily in the interest of the small investor or even of the naïve institutions, of which there are many). Note that this process occurred simultaneously with the direct growth of individuals investing indirectly in the market (for example individuals have twice as much money in mutual funds as they do in bank accounts). However this growth occurred primarily by way of individuals turning over their funds to 'professionals' to manage, such as in mutual funds. In this way, the majority of investment now is described as "institutional investment" even though the vast majority of the funds are for the benefit of individual investors.Program trading, the hallmark of institutional trading, averaged over 80% of NYSE trades in some months of 2007. (Moreover, these statistics do not reveal the full extent of the practice, because of so-called 'iceberg' orders. See Quantity and display instructions under last reference.)Unfortunately, there has been a concurrent lapse in the oversight of large corporations, which are now almost all owned by large institutions. The Board of Directors of large corporations used to be chosen by the principal shareholders, who usually had an emotional as well as monetary investment in the company (think Ford), and the Board diligently kept an eye on the company and its principal executives (they usually hired and fired the President, or Chief Executive Officer— CEO).A recent study by Credit Suisse found that companies in which "founding families retain a stake of more than 10% of the company's capital enjoyed a superior performance over their respective sectorial peers."Since 1996, this superior performance amounts to 8% per year.Forget the celebrity CEO. "Look beyond Six Sigma and the latest technology fad. One of the biggest strategic advantages a company can have, [BusinessWeek has found], is blood lines."In that last study, "BW identified five key ingredients that contribute to superior performance. Not all are qualities unique to enterprises with retained family interests. But they do go far to explain why it helps to have someone at the helm—or active behind the scenes—who has more than a mere paycheck and the prospect of a cozy retirement at stake." See also, "Revolt in the Boardroom," by Alan Murray.Nowadays, if the owning institutions don't like what the President/CEO is doing and they feel that firing them will likely be costly (think "golden handshake") and/or time consuming, they will simply sell out their interest. The Board is now mostly chosen by the President/CEO, and may be made up primarily of their friends and associates, such as officers of the corporation or business colleagues. Since the (institutional) shareholders rarely object, the President/CEO generally takes the Chair of the Board position for his/herself (which makes it much more difficult for the institutional owners to "fire" him/her). Occasionally, but rarely, institutional investors support shareholder resolutions on such matters as executive pay and anti-takeover, aka, "poison pill" measures. Finally, the largest pools of invested money (such as the mutualfund 'Vanguard 500', or the largest investment management firm for corporations, State Street Corp.) are designed simply to invest in a very large number of different companies with sufficient liquidity, based on the idea that this strategy will largely eliminate individual company financial or other risk and, therefore, these investors have even less interest in a particular company's governance.Since the marked rise in the use of Internet transactions from the 1990s, both individual and professional stock investors around the world have emerged as a potential new kind of major (short term) force in the direct or indirect ownership of corporations and in the markets: the casual participant. Even as the purchase of individual shares in any one corporation by individual investors diminishes, the sale of derivatives(e.g., exchange-traded funds(ETFs), Stockmarket index options[7], etc.) has soared. So, the interests of most investors are now increasingly rarely tied to the fortunes of individual corporations.But, the ownership of stocks in markets around the world varies; for example, the majority of the shares in the Japanese market are held by financial companies and industrial corporations (there is a large and deliberate amount of cross-holding among Japanese keiretsu corporations and within S. Korean chaebol'groups') [8], whereas stock in the USA or the UK and Europe are much more broadly owned, often still by large individual investors.Parties to corporate governanceParties involved in corporate governance include the regulatory body (e.g. the Chief Executive Officer, the board of directors,management and shareholders). Other stakeholders who take part include suppliers, employees, creditors, customers and the community at large.In corporations, the shareholder delegates decision rights to the manager to act in the principal's best interests. This separation of ownership from control implies a loss of effective control by shareholders over managerial decisions. Partly as a result of this separation between the two parties, a system of corporate governance controls is implemented to assist in aligning the incentives of managers with those of shareholders. With the significant increase in equity holdings of investors, there has been an opportunity for a reversal of the separation of ownership and control problems because ownership is not so diffuse.A board of directors often plays a key role in corporate governance. It is their responsibility to endorse the organisation's strategy, develop directional policy, appoint, supervise and remunerate senior executives and to ensure accountability of the organisation to its owners and authorities.The Company Secretary, known as a Corporate Secretary in the US and often referred to as a Chartered Secretary if qualified by the Institute of Chartered Secretaries and Administrators (ICSA), is a high ranking professional who is trained to uphold the highest standards of corporate governance, effective operations, compliance and administration.All parties to corporate governance have an interest, whether direct or indirect, in the effective performance of the organisation.Directors, workers and management receive salaries, benefits and reputation, while shareholders receive capital return. Customers receive goods and services; suppliers receive compensation for their goods or services. In return these individuals provide value in the form of natural, human, social and other forms of capital.A key factor is an individual's decision to participate in an organisation e.g. through providing financial capital and trust that they will receive a fair share of the organisational returns. If some parties are receiving more than their fair return then participants may choose to not continue participating leading to organizational collapse.PrinciplesKey elements of good corporate governance principles includehonesty, trust and integrity, openness, performance orientation, responsibility and accountability, mutual respect, and commitment to the organization.Of importance is how directors and management develop a model of governance that aligns the values of the corporate participants and then evaluate this model periodically for its effectiveness. In particular, senior executives should conduct themselves honestly and ethically, especially concerning actual or apparent conflicts of interest, and disclosure in financial reports.Commonly accepted principles of corporate governance include:Rights and equitable treatment of shareholders: Organizations should respect the rights of shareholders and help shareholders to exercise those rights. They can help shareholders exercisetheir rights by effectively communicating information that is understandable and accessible and encouraging shareholders to participate in general meetings.∙Interests of other stakeholders: Organizations should recognize that they have legal and other obligations to all legitimate stakeholders.∙Role and responsibilities of the board: The board needs a range of skills and understanding to be able to deal with various business issues and have the ability to review and challenge management performance. It needs to be of sufficient size and have an appropriate level of commitment to fulfill its responsibilities and duties. There are issues about the appropriate mix of executive and non-executive directors.∙Integrity and ethical behaviour: Ethical and responsible decision making is not only important for public relations, but it is also a necessary element in risk management and avoiding lawsuits. Organizations should develop a code of conduct for their directors and executives that promotes ethical and responsible decision making. It is important to understand, though, that reliance by a company on the integrity and ethics of individuals is bound to eventual failure. Because of this, many organizations establish Compliance and Ethics Programs to minimize the risk that the firm steps outside of ethical and legal boundaries.∙Disclosure and transparency: Organizations should clarify and make publicly known the roles and responsibilities of board and management to provide shareholders with a level ofaccountability. They should also implement procedures to independently verify and safeguard the integrity of the company's financial reporting. Disclosure of material matters concerning the organization should be timely and balanced to ensure that all investors have access to clear, factual information.Issues involving corporate governance principles include:∙internal controls and the independence of the entity's auditors ∙oversight and management of risk∙oversight of the preparation of the entity's financial statements ∙review of the compensation arrangements for the chief executive officer and other senior executives∙the resources made available to directors in carrying out theirduties∙the way in which individuals are nominated for positions on the board∙dividend policyNevertheless "corporate governance," despite some feeble attempts from various quarters, remains an ambiguous and often misunderstood phrase. For quite some time it was confined only to corporate management. That is not so. It is something much broader, for it must include a fair, efficient and transparent administration and strive to meet certain well defined, written objectives. Corporate governance must go well beyond law. The quantity, quality and frequency of financial and managerial disclosure, the degree and extent to which the board of Director(BOD) exercise their trustee responsibilities (largely an ethical commitment), and the commitment to run a transparent organization- these should be constantly evolving due to interplay of many factors and the roles played by the more progressive/responsible elements within the corporate sector. In India, a strident demand for evolving a code of good practices by the corporation, written by each corporation management, is emerging.Mechanisms and controlsCorporate governance mechanisms and controls are designed to reduce the inefficiencies that arise from moral hazard and adverse selection. For example, to monitor managers' behaviour, an independent third party (the auditor) attests the accuracy ofinformation provided by management to investors. An ideal control system should regulate both motivation and ability.Internal corporate governance controlsInternal corporate governance controls monitor activities and then take corrective action to accomplish organisational goals. Examples include:Monitoring by the board of directors: The board of directors, with its legal authority to hire, fire and compensate top management, safeguards invested capital. Regular board meetings allow potential problems to be identified, discussed and avoided. Whilst non-executive directors are thought to be more independent, they may not always result in more effective corporate governance and may not increase performance.[5]Different board structures are optimal for different firms. Moreover, the ability of the board to monitor the firm's executives is a function of its access to information. Executive directors possess superior knowledge of the decision-making process and therefore evaluate top management on the basis of the quality of its decisions that lead to financial performance outcomes, ex ante. It could be argued, therefore, that executive directors look beyond the financial criteria.Balance of power: The simplest balance of power is very common; require that the President be a different person from the Treasurer. This application of separation of power is further developed in companies where separate divisions check and balance each other's actions. One group may proposecompany-wide administrative changes, another group review and can veto the changes, and a third group check that the interests of people (customers, shareholders, employees) outside the three groups are being met.Remuneration: Performance-based remuneration is designed to relate some proportion of salary to individual performance. It may be in the form of cash or non-cash payments such as shares and share options, superannuation or other benefits. Such incentive schemes, however, are reactive in the sense that they provide no mechanism for preventing mistakes or opportunistic behaviour, and can elicit myopic behaviour.External corporate governance controlsExternal corporate governance controls encompass the controlsexternal stakeholders exercise over the organisation. Examples include:∙competition∙debt covenants∙demand for and assessment of performance information (especially financial statements)∙government regulations∙managerial labour market∙media pressure∙takeoversSystemic problems of corporate governance∙Demand for information: A barrier to shareholders using good information is the cost of processing it, especially to a smallshareholder. The traditional answer to this problem is the efficient market hypothesis(in finance, the efficient market hypothesis (EMH) asserts that financial markets are efficient), which suggests that the small shareholder will free ride on the judgements of larger professional investors.∙Monitoring costs: In order to influence the directors, the shareholders must combine with others to form a significant voting group which can pose a real threat of carrying resolutions or appointing directors at a general meeting.∙Supply of accounting information: Financial accounts form a crucial link in enabling providers of finance to monitor directors. Imperfections in the financial reporting process will cause imperfections in the effectiveness of corporate governance. Thisshould, ideally, be corrected by the working of the external auditing process.Role of the accountantFinancial reporting is a crucial element necessary for the corporate governance system to function effectively. Accountants and auditors are the primary providers of information to capital market participants. The directors of the company should be entitled to expect that management prepare the financial information in compliance with statutory and ethical obligations, and rely on auditors' competence.Current accounting practice allows a degree of choice of method in determining the method of measurement, criteria for recognition, and even the definition of the accounting entity. The exercise of thischoice to improve apparent performance (popularly known as creative accounting) imposes extra information costs on users. In the extreme, it can involve non-disclosure of information.One area of concern is whether the accounting firm acts as both the independent auditor and management consultant to the firm they are auditing. This may result in a conflict of interest which places the integrity of financial reports in doubt due to client pressure to appease management. The power of the corporate client to initiate and terminate management consulting services and, more fundamentally, to select and dismiss accounting firms contradicts the concept of an independent auditor. Changes enacted in the United States in the form of the Sarbanes-Oxley Act (in response to the Enron situation as noted below) prohibit accounting firms fromproviding both auditing and management consulting services. Similar provisions are in place under clause 49 of SEBI Act in India. The Enron collapse is an example of misleading financial reporting. Enron concealed huge losses by creating illusions that a third party was contractually obliged to pay the amount of any losses. However, the third party was an entity in which Enron had a substantial economic stake. In discussions of accounting practices with Arthur Andersen, the partner in charge of auditing, views inevitably led to the client prevailing.However, good financial reporting is not a sufficient condition for the effectiveness of corporate governance if users don't process it, or if the informed user is unable to exercise a monitoring role due to high costs .。

.Corporate Governance and Firm Value:The Case of VenezuelaUrbi Garay and Maximiliano González*ABSTRACTManuscript Type:EmpiricalResearch Question/Issue:We examine the relationship between corporate governance andfirm value,and evaluate the relatively understudied governance practices in Venezuela.Research Findings/Results:We construct a corporate governance index(CGI)for publicly-listedfirms that is free of self-selection and self-reported bias andfind that its mean value is below the emerging market average in general,and below the Latin American average in particular.This weak investor protection environment makes Venezuela a good setting to study how corporate governance practices affectfirm value.We show that an increase of1per cent in the CGI results in an average increase of11.3per cent in dividend payouts,9.9per cent in price-to-book,and2.7per cent in Tobin’s Q.These findings are robust after considering the potential endogeneity of our regression variables.Theoretical Implications:Results contrast to those reported in the US due to the higher interfirm variations in CGI.Our findings are consistent with the theoretical models that relate good corporate governance practices to higher investor confidence,and with the agency model of dividend payout.Furthermore,we conjecture that our results are generalizable mainly to other countries where investor protection is low.Practical Implications:Two direct insights to policy makers and practitioners follow from our analysis:first,managers in weak investor protection environments could differentiate theirfirms adopting corporate policies to improve their gover-nance structure;and second,our measure of governance practices gives investors a quantitative tool to better assess Venezuelanfirms.Keywords:Corporate governance rating/index,corporate performance,South AmericaINTRODUCTIONM ore companies in a growing number of countries are increasingly attempting to adopt better corporate governance practices.In the case of Latin America,the Andean Development Corporation(Corporación Andina de Fomento–CAF)recently presented an outline for a corporate governance Andean Code(CAF,2005).Furthermore,the larger companies of the region,especially those that belong to thefinancial sector,are in the process of adopting other international codes of best corporate governance practices, such as the Sarbanes-Oxley Act and the Principles of Corporate Governance developed by the Organization for Economic Co-operation and Development(OECD,1999).It is not difficult to predict that the success or failure of these initiatives will depend on the real impact that they may have on thefinancial performance and market valuation of the companies that adopt them.La Porta,López-de-Silanes,Shleifer and Vishny(1997, 1998,2000a)show that the legal framework thatfirms and investors face differs significantly around the world,in part,because of differences in legal origin.They argue that investors are less protected in French Civil Law countries, compared with countries from the Common Law origin. All countries in Latin America have the same legal origin, which is French Civil Law.They alsofind that Latin American countries perform even worse than the average French Civil Law countries in terms of investor rights,and argue that this helps explain the low level offinancial development and the small size of stock exchanges of these countries.Chong and López-de-Silanes(2007)confirm thesefindings for a more recent period.Furthermore, according to Djankov,La Porta,López-de-Silanes and*Address for correspondence:Suite11629,6910N.W.50Street,Miami,FL/33166.Tel:5713394999(ext.3369);Email:mgf@.coVolume16Number3May2008©2008The AuthorsJournal compilation©2008Blackwell Publishing Ltddoi:10.1111/j.1467-8683.2008.00680.xShleifer(2008)Venezuela exhibits one of the worst scores in terms of investor protection.The weak investor protection inherent in many Latin American countries offers an opportunity forfirms to dif-ferentiate themselves from the rest and to send strong and credible signals to attract investors by self-adopting good corporate governance practices and policies,thus partially compensating investors for the weak legal environment in which thesefirms operate.Klapper and Love(2004) and Durnev and Kim(2005)show that corporate gover-nance provisions matter more in countries with weak legal protection.We know relatively little about the potential impact that the adoption of corporate governance practices may have on company value in Latin America(see Chong and López-de-Silanes,2007,for a recent review of this evidence).Measur-ing this effect is important for the region because the success or failure of implementing good corporate governance prac-tices may be greater if the market rewards those companies that adopt them.In the case of the US,the empirical evi-dence shows either no effect or an economically small effect.1 Black(2001)argues that perhaps these weak results in the US arise because the variation infirm governance is small given that the minimum quality of corporate governance, which is set by law and by norms,is very high in that country.On the other hand,interfirm governance variation is found to be much larger in Venezuela.This should not come as a surprise,as a country with weaker laws and norms offers a wider range for governance differences between firms and,therefore,the potential for stronger results on the effects of governance onfirm value.Furthermore,even though Venezuela is the fourth largest economy in Latin America(after Brazil,Mexico,and Argentina),relatively little is known about corporate governance practices in this country.In sum,Venezuela represents a very strong case study.We evaluate the current state of corporate governance practices in Venezuela by constructing a corporate gover-nance index(CGI)for allfirms listed in the Caracas Stock Exchange(CSE)as of the end of2004and comparing the results to other emerging and Latin American countries. We then evaluate whetherfirm dividend payout policies, price-to-book multiple,and Tobin’s Q(TQ)are related to our CGI.By undertaking a single country-study approach,we attempt to perform a straightforward empirical test that has the advantage of avoiding some of the potential econometric problems involved in cross-country studies such as the omitted variable bias and the usually high across-firm heterogeneity.In general,wefind a positive and strong relation between our index of corporate governance and the payout ratio, price-to-book multiple,and TQ forfirms in Venezuela.From the composition of the index,wefind that the subindexes on ethics and conflicts of interest,composition and perfor-mance of the board of directors,and shareholders’rights explain much of the cross-sectional difference in payout ratio;on the other hand,the subindex regarding ethics and conflicts of interest can explain much of the results when price-to-book and TQ are used as dependent variables. These results add to the growing literature that supports the idea that in countries with relatively low investor pro-tection,good corporate governance practices and policies could be used as an efficient mechanism forfirms that want to distinguish themselves to attract investors.Although our results are tentative given the small size of the CSE,they passed a series of robustness checks that attempted to tackle, among other potential problems,the issue of endogeneity,a common concern found in this literature.Our paper is similar to Black(2001)and Judge,Naoumova and Koutzevol(2003)who tested the relation between cor-porate governance andfirm value in Russia,a transition economy characterized by weak investor protection.Both papers have a small sample and Russia,like Venezuela,is also a country that scores low in terms of investor protection and exhibits a high interfirm variation in corporate governance practices.Our paper is also related to recent country studies done in Latin America2and especially with Garay and González(2005),who also studied the case of Venezuela.The evidence reported in this paper is important not only for Venezuela but also for other emerging markets in the process of attempting to improve their corporate governance practices.The evidence we show here adds to the growing literature worldwide that indicates thatfirms can differenti-ate themselves by adopting better corporate governance practices and policies.That is,even in a weak investor pro-tection environment,firms can increase their market value by adopting good corporate governance measures.The rest of the paper is organized as follows:first,we review the growing literature on corporate governance and market valuation,concentrating on recent papers that are based on Latin America.Second,we construct a CGI for Venezuela and compare it with other emerging economies and,more importantly,to other Latin American countries. Third,we present the data and conduct our econometric analysis testing the relation between afirm’s dividend payout ratio,price-to-book,and TQ,and our CGI.Fourth, we perform a number of robustness checks to our main findings.In the last section we present the conclusions and policy recommendations,as well as its potential practical applications and suggestions for future studies.LITERATURE REVIEWMany definitions of corporate governance stress the poten-tial conflicts of interest between insiders(managers,boards of directors,and majority shareholders)and outsiders (minority shareholders and creditors)of the company.The set of internal and external mechanisms to balance these conflicts of interest is what it is usually known as corporate governance.The effect that a set of good corporate governance prac-tices may have onfirm’s value is,however,an empirical question.Recently,different studies,trying to measure quantitatively the quality of corporate governance,have created indexes based on legal,accounting,andfirm-level financial information.Gompers,Ishii and Metrick(2003) construct a CGI based on24governance rules for1,500 large USfirms,and show thatfirms with higher corporate governance scores had higherfirm value.La Porta et al.(1997)study a sample of49countries and conclude that countries with legal systems based on CivilVolume16Number3May2008©2008The AuthorsJournal compilation©2008Blackwell Publishing LtdLaw,especially the French legal system,provide less pro-tection to investors and have less developed capital markets,particularly when compared with countries from the Common Law origin.These authors also conclude that dividend policy constitutes an essential tool to reduce agency conflicts to minority investors.3Thesefindings are consistent with the theoretical model presented in La Porta,López-de-Silanes,Shleifer and Vishny,(2002),where the positive effects of good corporate governance practices onfirm valuation are explained by higher investor confidence.This situation lowers the cost of capital and,ultimately,increasesfirm value.Also,these results are consistent with the agency model of dividend payout in the corporate governance framework developed in La Porta,López-de-Silanes,Shleifer and Vishny(2000b). Since the seminal empirical papers of La Porta et al. (1997,1998,2000a)showing that laws that protect investors differ significantly across countries,in part because of dif-ferences in legal origin,the academic focus has shifted to study corporate governance in the international setting.4 Klapper and Love(2004)was among thefirst and more comprehensive papers focusing on corporate governance in emerging ingfirm-level evidence on corporate governance practices for495companies from25emerging markets,they show that better corporate governance is highly correlated with better operating performance and market valuation.Many country-studies have used a methodology that is very similar to that of Klapper and Love(2004).For example, Black,Jang and Kim(2006a)constructed a CGI for South Korea;and Black(2001)and Black,Love and Rachinsky (2006b)both studied how their CGI affectsfirm value in Russia.The empirical evidence for Latin America has also grown rapidly in recent years.Leal and Carvalhal-da-Silva (2005)studied Brazil,Chong and López-de-Silanes(2006) studied Mexico,Lefort and Walker(2005)studied Chile, and Garay and González(2005)studied Venezuela.All these papers show that,on average,a good set of corporate gover-nance practices and policies is positively related tofirm value. Thesefindings in Latin America are especially important because the weak investor protection inherent in this region offers an opportunity forfirms to differentiate themselves to attract investors by self-adopting good corporate gover-nance practices.Easterbrook and Fischer(1991)argue that firms themselves,when it is optimal to do so,could offer private contracts with better terms than can be offered by the rigid legal system.In the same manner,Diamond(1989, 1991)presents a theoretical discussion of the effects of a firm’s reputation on its access to externalfinancing,and Coffee(1999)argues for a“global convergence”in corporate governance that is independent of the local legal environ-ment.Empirically,Klapper and Love(2004)and Durnev and Kim(2005)find that corporate governance practices play a more important role in countries where legal protection is weak.That is,firm-level improvements in corporate governance could,in some way,bypass the obstacles and inefficiencies of a country’s legal system.That makes Venezuela a good setting to corroborate the effect good corporate governance practices have onfirm valuation,given the overall low scores this country exhibits in terms of investors’protection and the high interfirm variation in corporate governance practices observed in this country.This suggests the following hypothesis: Hypothesis1:Better corporate governance practices will be positively related tofirm valuation in Venezuela.This paper is similar to Garay and González(2005)because both papers usefirm-level data for Venezuelan listedfirms. However,the two papers differ in three important aspects. First,we present a more detailed analysis of each of the questions in our CGI and exclude all questions that are not directly applicable to the Venezuelan market.In contrast, Garay and González(2005)used a standard and more general questionnaire that was very similar to the one used by Klapper and Love(2004).Second,we answered the ques-tions directly and therefore our paper is less likely to suffer from self-selection and self-reported bias.Third,here we have directly addressed the endogeneity issue,a typical concern in this type of empirical analysis.Moreover,the focus in Garay and González(2005)was not to test whether corporate governance affects market valuation but iffinan-cial performance somehow affects CEO turnover.Corporate Governance Index(CGI)Most studies onfirm-level evidence on corporate governance practices gather their information using questionnairesfilled by the companies themselves.This methodology presents various potential problems,among others:a low response rate,especially from those companies whose corporate gov-ernance practices are poor(self-selection bias);and,for the firms that do respond to the questionnaire,there is a tendency to present themselves not as they are at the moment when the questionnaire is being completed,but as they want to see themselves in the future(self-report bias).In our paper we follow a different route to construct our CGI.In the same spirit of Leal and Carvalhal-da-Silva(2005),we answer the questions ourselves using publicly available information. From Leal and Carvalhal-da-Silva(2005)’s24questions we ended up with17questions that are applicable to the Venezuelan setting.5Each one of these17questions was answered using publicly available information.We then grouped the questions into four subindexes,namely:infor-mation disclosure(five questions),composition and perfor-mance of the board of directors(five questions),ethics and conflicts of interest(three questions),and shareholders’rights(four questions).We report our results for each sub-index in Table1for the46companies listed in the CSE in the year2004.6The disclosure subindex shows that only19.6per cent of thefirms disclose penalties against management in case of deviating from the corporate governance policy;82.6per cent report their auditedfinancial statements on time;only 17.4per cent use international accounting standards;84.8 per cent hire internationally recognized auditors;and50 per cent disclose information on managerial compensation. The arithmetic mean for this subindex is50.9per cent. According to the composition and performance of the board of directors’subindex,for60.9per cent of thefirms in the sample,the chairman of the board is also the CEO or general manager;56.5per cent have monitoring committees;Volume16Number3May2008©2008The AuthorsJournal compilation©2008Blackwell Publishing LtdTABLE 1Corporate Governance Index (CGI)These questions were answered by the authors for each of the 46Venezuelan firms that were listed in the Caracas Stock Exchange (BVC)in 2004to determine for each firm its CGI.The answer to each question is either “Yes”or “No.”If the answer is “Yes,”we add 1,and if the answer is “No,”we add 0.All answers are based on publicly available information.The primary sources of information are firms’financial statements,bylaws,minutes of meetings,and annual reports available at the CNV .At the end of each question,there are remarks in italics on whether what is stated in the question is stipulated in the Venezuelan Code of Commerce.Arithmetic Affirmative N Questionsmean answersSUBINDEX –DISCLOSURE50.9%1Does the company indicate in its charter,annual reports,or in any other manner,the penalties against the management in case of breach of its desired corporate governance practices?Required by Generally Accepted Auditing Standards.19.6%9/462Does the company present reports of its audited financial statements on time?Required by the CNV.82.6%38/463Does the company use international accounting standards?Required by Generally Accepted Auditing Standards .17.4%8/464Does the company use any recognized auditing firm?Required by the CNV and by Generally Accepted Auditing Standards.84.8%39/465Does the company disclose,in any form whatsoever,the compensation of the general manager and of the board of directors?Required by the CNV.50.0%23/46SUBINDEX –COMPOSITION AND PERFORMANCE OF THE BOARD OF DIRECTORS 54.4%6Are the chairman of the board of directors and the general manager two different people?Not required by any legal instrument.60.9%28/467Does the company have monitoring committees,such as appointment or compensation or auditing committees,or all of these?The auditing committee is established in the Venezuelan Code of Commerce.56.5%26/468Is the board of directors clearly comprised of external directors and possibly independent ones?Stipulated in the Code of Commerce,but not limited to the fact that they be independent.32.6%15/469Is the board of directors comprised of five to nine members,as per recommendation of good international corporate governance practices?Not required by any legal instrument or regulatory entity.73.9%34/4610Is there a permanent auditing committee?Stipulated in the Code of Commerce.47.8%22/46SUBINDEX –EHTICS AND CONFLICTS OF INTEREST39.9%11Is the company free of any penalty or fine for breach of good corporate governance practices or of any rules of the CNV during the last year?CNV rules.82.6%38/4612Taking into account the agreements among shareholders,are the controllingshareholders owners of less than 50%of the voting shares?Not established in any legal instrument or by any regulatory entity.30.4%14/4613Is the capital/voting rights ratio of controlling shareholders higher than 1?Not established in any legal instrument or by any regulatory entity. 6.5%3/46SUBINDEX –SHAREHOLDERS’RIGHTS16.3%14Does the company charter or any other verifiable means facilitate the voting process of the shareholders beyond that established by law?Stipulated in the Code of Commerce.28.3%13/4615Does the company charter guarantee additional voting rights to that established by law?Stipulated in the Code of Commerce.13.0%6/4616Are there pyramidal structures that reduce concentration of control?Not established in any legal instrument or by any regulatory entity.15.2%7/4617Are there agreements among shareholders that reduce concentration of control?Not established in any legal instrument or by any regulatory entity.8.7%4/46AVERAGE CGI (equally weighting the four subindexes)40.3%Source:Comisión Nacional de V alores (CNV),Código de Comercio,.The questionnaire is adapted from Leal and Carvalhal-da-Silva (2005)to the Venezuelan setting.Volume 16Number 3May 2008©2008The AuthorsJournal compilation ©2008Blackwell Publishing Ltd32.6per cent have external directors7;73.9per cent have a board composed of between5to9members;and47.8per cent have a permanent audit committee.The arithmetic mean for this subindex is54.4per cent.The ethics and conflicts of interest’s subindex shows that 82.6per cent of the companies are free from penalties orfines on the part of the regulatory agency(the Comisión Nacional de Valores);there exists a shareholder that controls less than50 per cent of thefirm’s shares in30.4per cent of thefirms in the sample;and in6.5per cent of thefirms,the capital to voting rights ratio of majority shareholders is higher than1. The arithmetic mean for this subindex is39.9per cent. Finally,the shareholders’rights subindex shows that only 28.3per cent of thefirms in the sample facilitate the voting process beyond what is required by law;only13.0per cent have voting rights beyond that required by law;only15.2per cent do not exhibit a pyramidal structure that reduces the concentration of control8;and8.7per cent report special agreements among shareholders that reduce the concentra-tion of control.The arithmetic mean for this subindex is a very low16.3per cent.Taking together these averages,we can conclude that only around half of thefirms in our sample comply with the requirements of the disclosure of the composition and per-formance of the board of directors and more work needs to be done in terms of ethics and conflicts of interest,and, especially,in terms of shareholders’rights.At thefirm level the highest overall CGI was71.7per cent and the lowest was16.7per cent.We found a much larger variation in Venezuelanfirms’corporate governance practices when compared with the US(results are not reported here).The average CGI in the sample is a low40.3per cent.In Table2Panel A we compare our CGI with the results reported by Klapper and Love(2004)who analyzed495firms in25emerging countries,9Lefort and Walker(2005) who studied181firms in Chile,and Leal and Carvalhal-da-Silva(2005)who studied214firms in Brazil.Table2shows that Venezuela is14percentage points below the emerging market average and19percentage points below Chile,which is the leading country in Latin America in terms offinancial development and investor protection(Chong and López-de-Silanes,2007).The Venezuelan average is closer to the one reported for Brazil.In Panel B we summarize the results obtained for each subindex and compare them with the results presented in Garay and González(2005)and in Lefort and Walker(2005) for Venezuela and Chile,respectively.Overall,the CGI we obtained produces a score14percentage points below the CGI reported by Garay and González(2005).As mentioned before,this difference could represent an overestimation on that paper due to the self-selection and self-reported bias generated whenfirms’executives completed the question-naires.Only in the composition and performance of the board of directors(Board)subindex do wefind similar results. We also include in this panel the score reported by Lefort and Walker(2005)for Chile.The CGI for Chile is close to20 percentage points higher than the CGI for Venezuela.Only in the subindex of ethics and conflicts of interest(Ethics)are the scores relatively close.Finally,in Table2Panel C we show the correlation matrix among the subindexes.As expected,all subindexes are posi-tively and significantly related to the overall CGI.Chong and López-de-Silanes(2006)report a similarfinding for Mexico, even though their corporate governance components are not exactly comparable to ours,and Leal and Carvalhal-da-Silva (2005)do not provide a correlation matrix for Brazil.On the other hand,each of our subindexes shows little correlation with the other subindexes(none of the correlation coeffi-cients are statistically different from zero).Interestingly,each subindex seems to be taking into account a different dimen-sion of the overall governance of thefirm.Overall,these results confirm that Venezuela represents a good case study to test whetherfirms can somehow bypass a poor investor protection environment by voluntarily adopt-ing good corporate governance practices.A relatively high CGI is an indicator thatfirms can use to attract investors.We want to verify whether investors in Venezuela recognize this signal by assigning a higher market valuation to suchfirms.DATAHaving shown that Venezuela is a strong case study to test whether corporate governance is related tofirm valuation and dividend payout,in this section we present the depen-dent,independent,and control variables used to formally test our hypothesis.Dependent VariablesWe use three alternative dependent variables to test our hypothesis.First,we use the dividend payout ratio(DPR), which is measured as the quotient between cash dividends and net Porta et al.(2000b)show thatfirms in countries where investors are better protected exhibit higher dividend payouts thanfirms in countries where investors are poorly protected.On the other hand,Black et al.(2006a) and Leal and Carvalhal-da-Silva(2005)do notfind support for this hypothesis in the cases of South Korea and Brazil, respectively.The second dependent variable is the price-to-book ratio (price-to-book value or PBV),measured as the quotient between per share market price and book value.The price-to-book is a valuation measure that has been used in corporate governance studies by authors such as Leal and Carvalhal-da-Silva(2005)for Brazil.Finally,we use the TQ as the third of our dependent variables.This variable was com-puted as the market value of thefirm’s assets(book value of assets-book value of equity+market value of equity) divided by the book value of assets.TQ can be considered the classic valuation measure and has been used extensively in the corporate governance literature(see,for instance, Morck,Shleifer and Vishny,1988;La Porta et al.,2002; Gompers et al.,2003).Information regarding each one of these variables was obtained from the CSE Anuario(2004–yearbook)and corresponds to year-end values.Economatica’s database was also used in some cases to confirm the validity of stock market prices data.Independent VariablesAs we mentioned in the previous section,the CGI was constructed based on17questions pertaining to differentVolume16Number3May2008©2008The AuthorsJournal compilation©2008Blackwell Publishing Ltdcorporate governance practices.We answered these ques-tions for each of the46Venezuelanfirms that were listed in the CSE in2004to determine for eachfirm its CGI.The answer to each question is either“Yes”or“No.”If the answer is “Yes,”we add1and if the answer is“No,”we add0.All answers are based on publicly available information.These17 questions were answered after reviewing eachfirm’sfinan-cial statements,bylaws,minutes of the boards of directors and shareholders’meetings,and annual reports available at the Comisión Nacional de Valores library.TABLE2Comparative AnalysisIn this table we compare our corporate governance index(CGI)to similar studies done in other emerging markets.Panel A presents basic statistics comparing25different emerging markets(Klapper and Love,2004)together with the CGI calculated for Chile(Lefort and Walker,2005)and Brazil(Leal and Carvalhal-da-Silva,2005).Panel B divides the CGI into its four subindexes and compares the values with a similar study for Venezuela(Garay and González,2005)and Chile(Lefort and Walker,2005).Panel C shows the correlation matrix of each of the subindexes(p-values are reported below each correlation coefficient).Panel A:Comparative statistics for the Venezuelan CGI versus other emerging market studiesDescription This paper Klapper and Love(2004)Lefort and Walker(2005)Leal and Carvalhal-da-Silva(2005)Mean40.3454.1158.8641.67 Median40.4754.97NR41.67 Standard deviation12.1114.00NR8.33 Minimum16.6711.77NR16.67 Maximum71.6792.77NR79.17 Country Venezuela25EM Chile Brazil Observations46374181214Source:The above-mentioned papers.All numbers(except the number of observations)are expressed in percentages.EM=Emerging Markets;NR=not reported.Panel B:Comparative subindex for the Venezuelan CGI versus other studies in Venezuela and in ChileThis paper(46firms)Garay and González(2005)Lefort and Walker(2005)Subindex Questions Score(%)Questions Score(%)Questions Score(%) Ethics339.9746.0737.6 Board554.42556.02664.9 Shareholders416.32454.02059.7 Disclosure550.81460.81473.4 Overall CGI1740.37054.36758.9Panel C:Subindex correlation matrixCGI Disclosure Board Ethics ShareholdersCGI1Disclosure0.4110.02Board of directors0.750.2910.000.10Ethics and conflicts of interest0.41-0.120.1210.020.560.53Shareholders’rights0.34-0.27-0.180.0910.050.130.310.64Volume16Number3May2008©2008The AuthorsJournal compilation©2008Blackwell Publishing Ltd。

Corporate Governance

Author(s): Jean Tirole

Source: Econometrica, Vol. 69, No. 1 (Jan., 2001), pp. 1-35

Published by: The Econometric Society

Stable URL: /stable/2692184

Accessed: 02/12/2009 00:23

Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at

/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content in the JSTOR archive only for your personal, non-commercial use.

Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at

/action/showPublisher?publisherCode=econosoc.

Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed page of such transmission.

JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact support@.

The Econometric Society is collaborating with JSTOR to digitize, preserve and extend access to Econometrica.。