回归分析在股票中的应用

- 格式:doc

- 大小:697.63 KB

- 文档页数:25

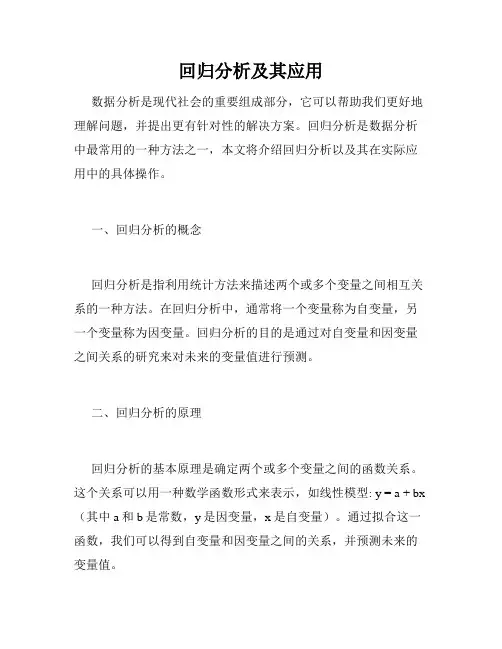

ContentsIntroduction (1)Preparation for OLS (1)The Market Model benchmark (1)Choice of Data (2)Source and validity of the data (2)Choice of test period and estimation period (3)Choice of the market index (3)Coefficient Stability Test (3)Ordinary Least Squares (4)Assumptions of Ordinary Least Squares Regression (5)1. Model is linear in parameters (5)2. The data are a random sample of the population (5)3. The expected value of the errors is always zero (7)4. The independent variables are not too strongly collinear (7)5. The independent variables are measured precisely (7)6. The residuals have constant variance (7)7. The errors are normally distributed (11)Proceed OLS Regression (12)Interpretation and Discussion of Abnormal Returns (12)Interpretation of abnormal returns for each event (12)Interpretation of abnormal returns for the series of events (16)Conclusions (19)List of References (20)The Analysis of CVRD AcquisitionIntroductionThis paper analyses the impact of acquisition events on the stock returns of CVRD 1. These events include: an announcement that proposed all-cash offer to acquire Inco by CVRD; comments on Inco Board ’s decision to recommend its Offer and announcement of extension; extension of its offer for Inco; CVRD acquires 75.66% of Inco; CVRD pays US$ 13.3 billion for the acquisition of Inco; CVRD holds 86.57% of Inco.The paper uses OLS method to calculate the abnormal returns during the event period, and then interpret the results generated by OLS. At first, the price data are gained from Yahoo Finance; then, a Market Model is set, after which the data are processed with Microsoft Office Excel and Minitab, using Chow-test, Durbin-watson test, Goldfield-Quardt test, etc, to test whether the data are suitable for regression; afterwards, a regression is made and a Market Model is adopted to calculate the abnormal returns of the event period; finally, interpretations are given to enclose the reasons underneath the abnormal returns.Preparation for OLSIn order to focus on the impact of firm-specific information on security returns, a control is needed to model daily returns conditionally expected from contemporaneous non-firm-specific information. The market model is used as a control. Besides, the data should be chosen properly on period and proper index as well. Finally, Chow test is used to test coefficient stability.The Market Model benchmarkjt mt j j jt R R εβα++= (1)Where αj and βj are parameters specific to the j th equity security, R mt is the return on a well1 Rio de Janeiro, November 29, 2007 - Companhia Vale do Rio Doce (Vale, ex CVRD) informed that from then on it started using just one global brand, Vale, in all countries where it operates and, at the same time, adopted a new global visual identity.diversified index portfolio (such as NYSE Composite) during the t th time period and εjt is the stochastic error term for the j th security during the t th time period. Equation (1) partitions R jt into a systematic component linearly related to R mt , and an unsystematic component, εjt , which is uncorrelated with R mt . The effect of firm-specific events is meant to be fully captured in the unsystematic component, the assumption being that the information signal and R mt are independent. Both αj and βj must be estimated here, resulting in a predicted abnormal return of)(mt j j jt jt R R βαε+-= (2)In this paper, there is only one security, CVRD; therefore the issue of j can be ignored. Thus, equation (1) is adapted ast mt t R R εβα++= (3)and equation(2) is adapted as)(mt t t R R βαε+-= (4)Choice of DataSource and validity of the dataThe data was drawn from Yahoo Finance adjusted close data. It has the following characteristics:♦ Close price adjusted data have been adjusted for dividends, which would be part of anyrate of return calculation. Usually, dividends are paid (if at all) every six months. Theconsequence is that for CVRD, two observations will be measured with error every year.When the data are adjusted, the dividends have been added into prices.♦ Close price adjusted data have been adjusted for split. With a split, the security pricewill drop remarkably, which will lead to an error when the data are processed. As thedata have been adjusted, there is no this problem any more.♦ Yahoo Finance records a price on days when the NYSE is closed. This excludesweekends. And all public holidays (when they don ’t fall on a weekend) will not show aprice. What this means is that these days can be simply omitted as non-existent.♦ The share prices recorded is a mid-price and not necessarily a buy or sell price. Thiswill be important in the interpretation of the evidence.These characteristics will help avoid errors stemmed from raw data.Choice of test period and estimation periodThe returns history for each security is usually divided into an estimation period (EP) and a test period (TP). The EP is used for estimating the parameters of the benchmark expected return. This allows a predicted abnormal return to be calculated within the TP. (Strong, 1992) In our case, EP is set from 01/08/2002 to 31/07/2006, and TP is set from 01/08/2006 to 06/11/2006. Although TP is set up as this period, it will be modified according to some conditions. This will be discussed later in the paper. The first event date is 11/08/2006. The form of this procedure is illustrated schematically below:Choice of the market indexIn this paper, NYSE Composite is selected as the market benchmark. The index is weighted using free-float market capitalization and calculated on both price and total return basis. It is composed to measure the performance of all ordinary securities listed on the NYSE, containing over 2,000 U.S. and non-U.S. securities. The NYSE Composite Index has been adjusted to eliminate the effects of capitalization changes, new listings and delistings. Thus, it is a suitable market index to be the benchmark for CVRD.Coefficient Stability TestChow test is used to test the coefficient stability. The Chow test is a statistical and econometric test of whether the coefficient in one linear regression is equal to the coefficient on the other different data set. It is usually used in time series analysis to test for the presence of a structural break. In program evaluation, the Chow test is often used to determine whether the independent variables have different impacts on different subgroups of the population.The Chow test statistic is tEP TPevent datet1=11/08/2006 t6=06/11/2006 T=01/08/2002 s=31/07/2006()()()()k N N S S k S S S c c 2/212121-+++-= (5) Where S c , S 1 and S 2 are SSR from the combined data, the first group and the second group respectively. N 1 and N 2 are the number of observations in each group and k is the total number of parameters (in this case, k=2)We run the test as follows:Our market model isR it =α+βR mt +εtWe split our data into two groups, two-year period for each. Then we haveR it =α1+β1R mt +εtR it =α2+β2R mt +εtSet hypothesisH 0: α1=α2, β1=β2 ;H 1: any of them are not equal.Summarizing the regression results2, we haveValue S c 0.417398653 S 10.197546678 S 20.18040653 N 1502 N 2504 K2 Chow 5.20788E-05The test statistic follows the F distribution. Checking F table with P=0.05, both 500 degrees of freedom, we have critical F is 1.16. Chow test statistic here is smaller than 1.16, so H0 can not be rejected. Therefore, coefficient αand βare stable.Ordinary Least Squaresin statistics and econometrics, ordinary least squares (OLS) is also known as linear least square. It is a method with which estimate unknown parameters in a linear regression model. This method minimizes the sum of squared vertical distances between the observed2 The regression results are available in appendices.responses in the dataset, and the responses predicted by the linear approximation. The resulting estimator can be expressed by a simple formula, especially in the case of a single regressor on the right-hand side.t mt it R R εβα++= (6)is a linear regression model with a single regressor, R mt ; R it is the regressand. α and β are constants to be estimated. We are particularly interested in the intercept α and slope coefficient β and to know the relationship between security return and market return during the test period. Afterwards, they are plugged into the equation for the event period. With the data of R it and R mt in event period, εt can be obtained, known as the abnormal return.)(mt it t it R R AR βαε+-== (7)and cumulative abnormal return is∑=t AR CAR (8)Assumptions of Ordinary Least Squares RegressionThe assumptions are the requirement of an effective OLS regression, that is without these assumptions, the result of OLS regression will probably be distorted and not be able to show a realistic situation. The assumptions are:1. Model is linear in parametersWith a similar structure of the formula, MM is suitable for this assumption. As can be seen in Equation (1), R t and R mt are assumed to be linear related.2. The data are a random sample of the populationIf the data, AR, are statistically independent from one another, we can argue that they are random. Durbin-Watson test is used to test whether the data have an auto-correlation problem.The Durbin-Watson Test for serial correlation assumes that the εt are stationary and normally distributed with mean zero. The test statistic is()∑∑==--=n t t nt t t d 12221εεε (9)We have d ≈2(1-ρ), where ρ measures the level auto -correlation. If the errors are white noise 3, d will be close to 2. If the errors are strongly auto-correlated, d will far from 2. If ρ=0 and d=2, there is no auto-correlation. If ρ=-1 and d=0, the data are perfectly positively correlated. If ρ=+1 and d=4, the data are perfectly negatively correlated.Involving d and 4-d, the interpretation of the result may be complicated. In Draper and Smith (1998), Page 184-190. In some cases, the test can be "inconclusive," i.e., H 0 of uncorrelated is neither accepted nor rejected.Steps:(1) Calculate the logarithmic returns for each day. The equation isR t = ln( P t /P t-1) (10)(2) In Excel, click Data | Data Analysis | Regression, and choose ‘display residuals’ t o obtain the residuals data. And then, the residuals data are plugged into the Equation (6), we obtain the result:d=0.797727/0.417399=1.911188(3) Check the Durbin-Watson test table:Critical values for the Durbin-Watson test: 5% significance level, T=1000, K=2(K includes intercept) areD L =1.89407, D H =1.89807(4) Results and discussiond>D H ; 4-d> D HObviously, d>D H (1.911188>1.89807), so the data are not positively correlated; 4-d> DH (4-1.911188=2.088812>1.89807), so the data are not negatively correlated. Therefore, hypothesis H 0 cannot be rejected that the errors are uncorrelated. In other words, the data are3 White noise is a random signal (or process) with a flat power spectral density. In other words, the signal contains equal power within a fixed bandwidth at any center frequency.a random sample of the population3. The expected value of the errors is always zeroE(ε) can be simply seem as the average of the residuals. So, it isE(ε) = average(residuals) = -5.44903*10-19 ≈ 04. The independent variables are not too strongly collinearAs can be seen in Figure 1, the independent variables, which is market returns in this case, vary from approximately -0.04 to +0.04 during approximately 1000 days. Therefore, they are not too strongly collinear.Figure 1 The Plot of Market Returns(Rm)-0.05-0.04-0.03-0.02-0.0100.010.020.030.040.05Observation M a r k e t R e t u r n5. The independent variables are measured preciselyThe independent variables, i.e. market returns, come from NYSE Composite Index daily data, which have 2 decimal places. Thus, they are measured precisely.6. The residuals have constant varianceThe data may have a heteroscedasticity problem if the variance is not constant. The following will use Goldfield-Quardt test to test whether these data have this problem. This test is frequently used because it is easy to apply when one of the regressors is considered the proportionality factor of heteroscedasticity.The test procedure is the following:1) The observations on R i and R m are sorted following the ascending order of the regressorR m , which is the proportionality factor.2) We divide the sample observations in three subsamples omitting the central one.3) We estimate through OLS the regression models on the first and third subsample (thenon (n-c)/2 observations each; the number of observations considered is sufficientlylarge).4) We calculate the relative RSS, denoted as RSS 1 and RSS 3. (Figure 2 and Figure 3)5) We derive the Goldfeld-Quandt test: GQ = RSS 3/RSS 1.6) The test R under the null hypothesis has F distribution with degrees of freedom(n-c-2k)/2 both for numerator and denominator.If the sample value of the test GQ is greater than the critical F value, at the chosen significance level 5%, we reject the the hypothesis of homoscedasticity.The power of this test depends on the number of omitted observations (usually n/3 observations have to be omitted). If we exclude too many observations the RSS 2 and RSS 1 have too low degrees of freedom, if we exclude too few observations the test power is low because the comparison between RSS 2 and RSS 1 becomes less effective.As can be seen in Figure 2 and Figure 3, the variance of residuals are RSS 1= 0.100273 and RSS 3= 0.093007682 respectively. As RSS 1> RSS 3, the sum of square is getting smaller, so, set RSS 1 is numerator and RSS 3 denominator.GQ= RSS 1/RSS 3=1.078116Check F-test table, we will find that critical F= 1.197676 (Alpha level=0.05, Numerator degrees of freedom=333, denominator degrees of freedom=33401/08/2002 01/12/2003 01/04/2005 31/07/2006 First Period16 monthsSecond Period (omitted) 16 months Third Period16 monthsFigure 2 The First Subsample SUMMARY OUTPUTRegression Statistics Multiple R 0.3534063R Square 0.124896 Adjusted RSquare0.122268 Standard Error 0.0173528 Observations 335 ANOVAdf SS MS F SignificanceFRegression 1 0.0143111 0.0143111 47.526195 2.731E-11 Residual 333 0.100273 0.0003011Total 334 0.1145841Coefficients StandardError t Stat P-value Lower 95% Upper 95%Lower95.0%Upper95.0%Intercept 0.0016133 0.000949 1.7000471 0.0900558 -0.000253 0.0034801 -0.000253 0.0034801 X Variable 1 0.5259608 0.0762934 6.8939245 2.731E-11 0.3758831 0.6760386 0.3758831 0.6760386Figure 3 The Third Subsample SUMMARY OUTPUTRegression StatisticsMultiple R 0.7298913R Square 0.5327413 Adjusted RSquare0.5313423 Standard Error 0.0166873 Observations 336 ANOVAdf SS MS F SignificanceFRegression 1 0.1060419 0.1060419 380.80737 3.903E-57 Residual 334 0.0930077 0.0002785Total 335 0.1990496Coefficients StandardError t Stat P-value Lower 95% Upper 95%Lower95.0%Upper95.0%Intercept 0.0002494 0.0009119 0.2734857 0.7846489 -0.001544 0.0020431 -0.001544 0.0020431 X Variable 1 2.4618052 0.126154 19.514286 3.903E-57 2.2136487 2.7099617 2.2136487 2.7099617As F<critical F, the hypothesis of homoscedasticity can not be rejected. That is, there is no heteroscedasticity problem with the data. 7. The errors are normally distributedIn order to test the data whether their errors are normally distributed, the statistical software Minitab 15 is used to prove that they are normally distributed. Ryan-Joiner test (similar to Shapiro-Wilk) test and Kolmogorov-Smirnov test are used below. If the p-value of these tests is less than your chosen level, p=0.05, we have to reject null hypothesis of normality and conclude that the population is non-normal.Figure 4 Anderson-Darling Test for Residuals Normalitya. Ryan-Joiner normality testb. Kolmogorov-Smirnov normality test0.0500.0250.000-0.025-0.050-0.07599.99995908070605040302010510.1ResidualsP e r c e n tMean -0.0004352StDev 0.02045N 85RJ0.994P-Value>0.100Kolmogorov-SmirnovNormal0.0500.0250.000-0.025-0.050-0.07599.99995908070605040302010510.1ResidualsP e r c e n tMean -0.0004352StDev 0.02045N 85KS0.049P-Value>0.150Ryan-Joiner TestNormalThe results presented above show that p-values for the tests are greater than 0.05, which means null hypothesis can not be rejected. Thus, we can tell that the population is normal. Addition to the tests above, a graphical technique can be used as well. We can assess population normality with a normal probability plot, which plots the ordered data values against values that you expect them to be near if the sample's population is normally distributed. If the population is normal, the plotted points will form an approximately straight line.Probability Plot of Normal DataProbability Plot of Non-normal DataThe graphs from both the tests tell us that the data are normally distributed.Proceed OLS RegressionSo far, the assumptions of OLS have been tested. Then, it’s ready to calculate the abnormal returns for the events. To obtain the AR and CAR, two steps, which was also mentioned by David (1980), are (1) estimatingαandβof the market model based on EP, and (2) applying this model to TP. First of all, we calculate the parameters as follows.Summarizing the relevant numbers from Figure 5, we have:Coefficient Result t-statistic α0.001298545 2.017157β 1.161725787 16.50389 According to t-test table, both are statistically significant.Then, the market model can be written asR it= 0.001298545+1.161725787R mt+εt(8) The data, Ri and Rm, from event period are plugged into this market model below; and then εare calculated daily, which are the abnormal returns for CVRD security.εt= R it– ( 0.001298545+1.161725787R mt ) (9) Interpretation and Discussion of Abnormal ReturnsInterpretation of abnormal returns for each eventBefore presenting the security abnormal returns response associated with the announcements of major events, two factors that affect their interpretation are worth highlighting.First there were many other news and announcement during the event period from August to November of 2006. Although they might not be tightly related to the acquisition, some impact on the change of security price was inevitable.Second, the impact of events may last for a couple of days, as long as there are no other information emerged. That is to say, to analyze one day abnormal return can be imprecise. Therefore, 3-day CAR are analyzed in the paper.Figure 5 Regression for Estimate Period (01/08/2002 – 31/07/2006)SUMMARY OUTPUTRegression Statistics Multiple R 0.4619516 R Square 0.2133993 Adjusted RSquare0.2126158Standard Error 0.0203896 Observations 1006 ANOVAdf SS MS FSignificanceFRegression 1 0.1132374 0.1132374 272.37824 2.532E-54 Residual 1004 0.4173987 0.0004157 Total 10050.530636Standard Lower UpperTable 1Major Events and Corresponding Percentage Abnormal Returns of CVRDaWith these considerations in mind, the analysis begins on 11th August, 2006 when CVRD proposed all-cash offer to acquire Inco. The first line of Table 1 indicates that this announcement is associated with an abnormal return of -5.498% for CVRD, with t-statistic of -2.39 indicates that this abnormal return is statistically significant. This can be interpreted in two ways. First, it can be caused by other previous events which are hardly relevant to the acquisition. As to Figure 6, CAR kept going down from May to September. As the downward trend was a result of a great deal of information, only one announcement could not make a difference. Second, the acquisition could be hostile. Inco, at that time, is the world’s second largest nickel producer possessing the world’s largest nickel reserve base. With a brilliant performance, it could refuse the proposal or repurchase. In the view of these two reasons, investors were probably waiting for a remarkable point in the market.In contrast, the second announcement is a significant abnormal return of 4.51% (t-statisticof 1.9638). As a general rule, the larger the extent of uncertainty, the greater the potential for any one release to cause a revision in security prices. (Ruback, 1983) The first announcement a month ago had given an uncertainty to the market about whether this acquisition would be succeeded. And the second announcement showed that the acquisition proposal was welcomed by the managers of Inco. Therefore, it triggered a positive abnormal return for the security.On 13th October, 2006, CVRD announces extension of its offer for Inco. CVRD declaimed that this extension is intended to provide additional time to obtain a net benefit ruling under the Investment Canada Act, and all other terms and conditions of the CVRD offer will remain unchanged. This event is associated with an insignificant positive abnormal return of 0.886% and t-statistic of -0.3858. This slight abnormal return is easily explained. As all the terms and conditions of the offer would not be changed, there was nothing new in the announcement. So, there would not be a noticeable abnormal return.On 24th October, 2006, CVRD acquired 75.66% of Inco. The abnormal return for CVRD is 5.264% with a t-statistic of 2.292095. This significant positive abnormal return is predictable. Inco is a company with excellent resources, including skillful employees, developed market, nickel resource base, a great deal of PPE, etc. With the possession of Inco, CVRD could increase its earnings, which would lead to future distribution of security returns. Ruback (1983) also mentioned that the larger the relative revision in expected cash flows, the larger the security price revaluation implication of the release.Two days later, CVRD paid US$ 13.3 billion for the acquisition of Inco. This announcement is associated with an insignificant abnormal return of -4.614% (t-stat=-0.26141). It is difficult to interpret; perhaps the remarkable positive abnormal returns in the previous days exceeded a expected range.On 6th November, 2006, CVRD announced that it had hold 86.57% of Inco. The abnormal return is 09.673% with a t-statistic of 0.421177. Unsurprisingly, there is no dramatically high abnormal return as it had when it acquired 75.66% of Inco, because this acquisition was anticipated by the market. On 13th October, it declaimed an extension to 100% of the shares of Inco, CVRD would take the steps to acquire the remaining Inco shares. Thus, the market would not have an abnormal return as market efficiency.Interpretation of abnormal returns for the series of eventsTable 2Cumulative Abnormal Returns For CVRD in the Acquisition(t-statistics b in parentheses)The cumulative abnormal return, which is presented in Figure 7a, falls with some fluctuation until September; and rises in response to the second event (CVRD comments on Inco Board’s decision to recommend its Offer and announces extension). Measured from 11th August to the day before the second announcement, the cumulative abnormal return for CVRD is -21.827% (Table 2). As it was mentioned before, this downward trend did not start from the acquisition announcement day; so it can be more objective to focus on the performance from the second announcement.The large cumulative abnormal return of 21.74% (Table 2) during the second holding period reflects the benefit obtained from the acquisition. There are a variety of ways to interpret the second period abnormal return:Figure 7 The Plots of Cumulative Abnormal ReturnsabLloyd-Davies (1978), pointed that, “As long as a stock is undervalued, clients continue to purchase, and ultimately the information contained in the recommendation is completely reflected in the price.” T he essential motivation for the continuous abnormal return was that the security price was undervalued. Inco, in 2006, was the second largest nickel company around the world, with the largest base of nickel reserve. Moreover, it was a leader in nickel technology and one of the low cost producers. The combination of CVRD and Inco will create one of the three largest diversified mining companies in the world, with leading globalmarket positions in iron ore, pellets, nickel, bauxite, alumina, manganese and ferroalloys, and an exciting world-class pipeline of projects, supported by a large-scale, long-life and low-cost asset portfolio. With the prospective value, investors continue to purchase the security, leading to a surge in the price and a positive abnormal return. Specifically, three main points should be mentioned.1)Strategic opportunitiesOne motivation for acquisition is to purchase options on future growth prospects that may have explosive upside potential. For CVRD, acquisitions of Inco can gain a great advantage in nickel market. CVRD had decided to expand its business in nickel industry; there are important strategic reasons for acquiring an existing firm in that industry rather than relying on internal development. For example, by a large acquisition, CVRD can prevent other companies from acquiring Inco to compete with them. Foster (1986), also mentioned this point, “Making a preemptive move that can preclude a competitor from gaining a similar position in the industry.” This interpretation is consistent with what the company announced, “The offer is consistent with our long-term corporate strategy and with our non-ferrous metals business strategy.”2)SynergySynergies can be found in various functional areas, such as production, marketing, distribution, finance and personnel. For example, CVRD can maximize the performance of large-scale, long-life and low-cost assets. Moreover, the combination of Inco’s specific knowledge, long-term experience in nickel mining and technological leadership in nickel metallurgy with CVRD’s global mining leadership and strong cash generation makes for a unique opportunity to create greater value in an environment of sustained demand for minerals and metals in the long-term. Foster (1986), also pointed out that synergy is one reason why company conducts a restruction.3)Risk controlThe acquisition will bring a better diversification to CVRD’s activities by products, marketsand geographic asset base contributing to reducing our business and financial risks. It is believed that every industry has a fluctuation in its development, sometimes it can be a great fluctuation. Therefore, diversification is used to minimize the risk. When one industry struggles in a bad market environment, another one may be pretty profitable.ConclusionsIn this event study, we exploited OLS regression method on a real company CVRD to analyze its abnormal return. During the regression process, tests for stability, heteroscedasticity, auto-correlation, normality were conducted. Besides, some interpretation of the security performance was given and discussion was made. Generally, the series of events had a positive impact on the security, leading to a positive abnormal return. In the discussion on the abnormal returns, the reasoning may be arbitrary, but it is based on the evidence and facts.List of References[1]David F. Larcker, Lawrence A. Gordon, George E. Pinches. (1980) Testing formarket efficiency: A comparison of the cumulative average residual methodology and intervention analysis. The Journal of Financial and Quantitative Analysis, Vol. 15, No. 2, pp.267-287.[2]Draper & Richard, N. (1998) Applied regression analysis, 3rd ed, Chapter 7. New York:Wiley.[3]Foster, G. (1986) Financial Statement Analysis, 2nd ed, Chapter 11. Englewood Cliffs,N.J.: Prentice-Hall.[4]Karafiath, I. (1994) On the Efficiency of Least Squares Regression with SecurityAbnormal Returns as the Dependent Variable. The Journal of Financial and Quantitative Analysis, V ol. 29, No. 2 (Jun., 1994), pp. 279-300.[5]Lloyd-Davies, P & M Canes. (1978) Stock Prices and the Publication of Second-HandInformation. Journal of Business, 51(1), pp 43-56.[6]Newbold, P, W L Carlson. & B Thorne. (2007) Statistics for Business and Economics,6th ed, Upper Saddle River, N.J.: Pearson Prentice Hall.[7]Ruback, R S. (1978) The Cities Service Takeover: A Case Study. Journal of Finance,38(2), May 1983, pp 319-330.[8]Strong, N. (1992) Modeling Abnormal Returns: A Review Article, Journal of BusinessFinance & Accounting, 19(4), pp 533-553.(4534 words)。