香港会计准则02-利润表

- 格式:pdf

- 大小:165.08 KB

- 文档页数:14

利润表解读要点一、什么是利润表利润表,又称损益表或利润及损益表,是用于展示企业在一定时期(通常是一年)内营运活动所产生的收入、费用和利润的财务报表。

通过分析利润表,可以深入了解企业的盈利能力以及业务运营情况。

二、利润表的基本结构利润表通常由以下几部分组成:1. 收入部分:列示企业在该时期内实现的各类收入,如销售收入、利息收入、租金收入等。

2. 营业成本部分:列示企业在该时期内生产和销售所支出的直接成本,如原材料成本、人力成本、运输成本等。

3. 营业费用部分:列示企业在该时期内发生的与运营活动相关的费用,如销售费用、管理费用、研发费用等。

4. 营业利润部分:通过减去营业成本和营业费用,计算得到企业的营业利润。

5. 其他收支部分:列示企业在该时期内发生的与营业活动无直接关联的收入和支出,如投资收益、财务费用等。

6. 利润总额部分:通过将营业利润与其他收支进行合并计算得到企业的利润总额。

7. 所得税部分:计算企业在该时期内应缴纳的所得税。

8. 净利润部分:净利润是通过将利润总额减去所得税后计算得到的,代表企业在该时期内的实际盈利水平。

三、利润表解读要点在阅读和分析利润表时,我们应该关注以下几个要点:1. 销售收入的变化:利润表中的销售收入反映了企业的主营业务状况。

通过比较不同时间段的销售收入,可以评估企业的销售增长趋势以及市场份额的变化情况。

2. 营业利润率:营业利润率是企业核心盈利能力的重要指标。

通过将营业利润与收入进行比较,可以了解企业的盈利水平以及成本控制的效果。

3. 管理费用和销售费用占比:这两项费用反映了企业的运营管理水平和市场拓展投入情况。

通过比较不同时间段的费用占比,可以评估企业的运营效率和市场推广策略是否得当。

4. 利润总额和净利润的变化:利润总额和净利润是企业整体盈利状况的重要指标,直接反映了企业的经营收益和税务负担。

通过比较不同时间段的利润总额和净利润,可以了解企业的实际盈利能力和税务政策对企业的影响。

《新企业会计准则下利润表的》内容摘要利润表在财务会计报告概念框架中占有重要地位,自改革开放以来,我国利润表的名称?列报的依据?列报内容等方面都存在着很大变化,将?本文对我国改革开放以来利润表的变化情况作出分析?新会计准则的实施使利润表项目进一步增加,将部分未实现资产增值收益纳入利润表,这在增加会计信息相关性的同时降低了其可靠性。

文主要从新准则下利润表的理念变化、计量变化、列报变化以及营业利润、利润总额、净利润内涵变化等几个方面进行阐述。

提出在分析新企业会计准则下的利润表时,要在经常性收益与非经常性收益、已确认已实现收益与已确认未实现收益、计入损益的利得和损失与计入所有者权益的利得和损失等三个方面加以关注。

关键词:新准则资产负债表利润表目录一、利润表变化的原因……………………………………………………………4-6 (一)利润表变化的总体趋势……………………………………………………4-5 (二)利润表存在的问题…………………………………………………………5-6 二、新企业会计准则下利润表的变化……………………………………………6-9 (一)理念的变化:收入费用——资产负债表…………………………………7-7 (二)计量的变化:历史成本——公允价值……………………………………7-7 (三)报表列表的变化……………………………………………………………8-8 (四)营业利润、利润总额、净利润内涵的变化………………………………8-9 三、利润表的变化所带来的影响…………………………………………………9-10 (一)资产计提的减值准备,一经确认不得恢复………………………………9-9 (二)资本公积金不得用于弥补公司的亏损……………………………………9-10 (三)“公允价值”极有可能成为调节利润的工具……………………………10-10四、对新企业会计准则下利润表的分析………………………………………10-11 (一)经常性收益与非经常性收益……………………………………………10-10 (二)已确认已实现收益与已确认未实现收益………………………………10-11 (三)计入损益的利德和损失与计入所有者权益的利德和损失……………11-11 五、结论…………………………………………………………………………11-12 参考文献…………………………………………………………………………13-13新企业会计准则下利润表的变化及分析利润表是反映企业一定期间经营成果的财务报表,又被称为“收益表”和“损益表”。

香港会计财务准则体系 香港的财务会计规范体系主要由以下几部分构成:会计准则体系、公司法中关于会计的相关规定、香港联合交易所有限公司(SEHK)证券上市规则、由企业自行制定的内部会计制度。

在香港财务会计规范体系中,最重要的就是会计准则体系。

2005年1月1日起,香港并行两套会计准则:一套是香港财务报告准则,另一套是中小企业会计准则。

“香港财务报告准则”一词是指已颁布的香港会计准则(HKAS)、香港财务报告准则(HKFRS)、标准会计实务公告(HKSSAP)及香港会计师公会发布的指南。

由于历史原因,香港被英国侵占。

在英国殖民统治期间,香港在会计领域深受英国会计理论和模式的影响,香港的会计准则也在很大程度上采用了英国会计准则的模式。

1976年,香港会计师公会(HKICPA)首次颁行会计准则,它是用于指导会计实践的规范性要求。

当时主要是参照英国的会计准则制定的,并且同英国一样,作为一种非强制性的专业准则。

1995年底,香港会计师公会参照国际会计准则委员会(IASC)的声明而发出的框架说明,表明公会正转为以IAS为基础,发展一套全面以IAS为依据的香港会计准则。

2001年,IASB取代了IASC。

2003年,IASB新发布的准则改称国际财务报告准则(IFRS),香港会计师公会也决定基于IFRS将其财务报告准则命名为HKFRS。

2004年,香港会计师公会宣布2005年1月1日HKFRS与IFRS完全接轨,为了与其协调,公会按照IAS和IFRS 的编号进行排列,并发布了大量的会计准则。

根据香港会计师公会提供的准则手册,截止到2006年6月,生效的会计准则共有31个,财务报告准则7个,此外还有若干准则的解释性公告。

这些会计准则和财务报告准则无论是在准则名称和编号,或是其准则内容,还是在其后的准则指南都与国际会计几乎相同。

在每个准则后都带有附注,说明其与国际会计准则的差异之处。

可见,香港财务报告准则已经与国际财务报告准则高度趋同,实现了国际化。

新会计准则利润表的变化利润表的分析2006年,我国财政部颁布了新的会计准则。

该准则以国际上通行的规则和惯例为依据,严格界定了资产、负债、所有者权益、收入、费用、利润等会计要素的定义,明确规定了有关会计要素的确认条件、计量原则,引入了资产负债表观的理念,改变了收入费用观下利润表在企业财务报告体系中占主导地位的情况,凸显了资产负债表的核心地位。

因此,在准则下企业的利润表有很大的变化。

本文将针对新准则下利润表的变化展开论述。

关键词:新会计准则利润表的变化利润表的分析AbstractIn 2006,the ministry of finance issued new accounting standards in our country.In accordance with the international prevailing rules and practices,strictly defined the assets,liabilities,owners'equity,revenue,cost,profit,such as the definition of accounting elements,specifying terms of relevant accounting elements confirmation,measurement principle,the introduction of the concept of assets and liabilities apparent,highlighted the core position of balance sheet,change the cost income under the dominant in the income statement in corporate financial reporting system.Therefore,under the new accounting standard for business enterprises enterprise great changes have taken place in the income statement.Key words:The new accounting standards,The change of the income statement,Income statement analysis一、前言1二、新旧会计准则的比较1(一)补充新规定,形成系统化1(二)变动一般核算原则,更具操作性1 (三)增加了新的会计计量属性1(四)资产减值准备计提与转回的新规定1 (五)发出存货计价方法的变更2三、利润表的变化2(一)理念的变化:收入费用观—资产负债观2 (二)计量的变化:历史成本—公允价值3 (三)报表列报的变化3四、新准则下利润表的分析4(一)结构分析4(二)财务信息分析4(三)影响分析5五、新准则下利润表的不足及问题分析7(一)模糊了主营业务利润和其它业务利润的划分7(二)营业外收入和营业外支出容易产生误解7(三)编制基础不一致7六、结论8致谢9参考文献10前言随着经济的发展,传统的会计准则已经不能满足会计信息使用者的需求变化。

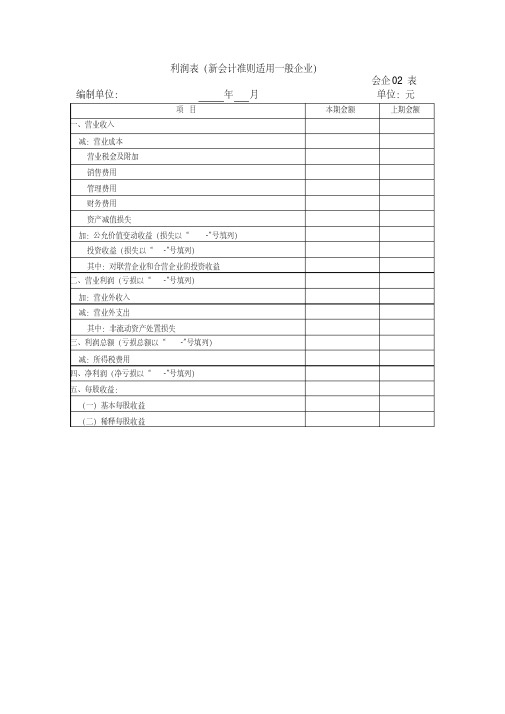

利润表(新会计准则适用一般企业)

会企02 表编制单位:年月单位:元

项目本期金额上期金额一、营业收入

减:营业成本

营业税金及附加

销售费用

管理费用

财务费用

资产减值损失

加:公允价值变动收益(损失以“-”号填列)

投资收益(损失以“-”号填列)

其中:对联营企业和合营企业的投资收益

二、营业利润(亏损以“-”号填列)

加:营业外收入

减:营业外支出

其中:非流动资产处置损失

三、利润总额(亏损总额以“-”号填列)

减:所得税费用

四、净利润(净亏损以“-”号填列)

五、每股收益:

(一)基本每股收益

(二)稀释每股收益。

香港的审计报告利润表里的Retainedearningscarriedforward是什么意思?香港的审计报告利润表里的Retained earnings carried forward是什么意思?Retained earnings brought forward: 未分配利润承前Retained earnings carried forward: 未分配利润转入审计报告是什么意思呢?1.审计报告是审计工作情况的全面总结汇报,说明审计工作的结果注册会计师审计目标的实现途径是实施审计程式,而审计目标的实现结果是通过审计报告来反映的。

审计报告反映委托方的最终要求,也反映审计方完成任务的工作质量,同时也是对被审事项的评价和结论的集中体现。

2.审计报告是一份具有法律效力的证明性档案注册会计师的审计行为是依法进行的,审计结果按照法律的规定既要对委托人负责,还要对其他相关的关系人负责。

审计报告本身要对被审会计报表的合法性、公允性和会计处理方法一致性表示意见,各方面关系人以这种具有鉴证作用的意见为基础,使用会计报表进行决策。

因此,在审计报告中的审计意见必须具有信服力、公正性和严肃性,具备法律效力,否则,委托人和各方面的关系人就无需使用审计报告。

审计报告的法定效力体现在各方面关系人使用审计报告的过程中。

3.审计报告是一种公开的资讯报告作为资讯报告的一种,审计报告不仅可以被审计委托人和被审计单位管理当局按规定范围使用,而且相关的债权人、银行等金融机构、财政部门、工商部门、税务部门和社会公众等都可以使用审计报告,并从中获得对有关专案公允反映程度的公正资讯。

是注册会计师根据审计准则的规定,在实施审计工作的基础上对被审计单位财务报表发表审计意见的书面档案。

审计报告是注册会计师在完成审计工作后向委托人提交的最终产品。

审计报告阶段是什么意思?审计报告阶段是:1.编审、复核、审理、签发审计报告和审计决定;2.公布审计结果;3.检查审计整改情况。

附件2:

企业会计准则利润表

纳税人识别号:纳税人名称:填报日期:所属时期:

金额单位:元(列至角分)

纳税人声明:我声明,该报表是按照国家税法和税务机关有关规定填报的,我保证它是真实的、准确的、可靠的、完整的,并愿意承担相应的法律责任。

纳税人公章:法定代表人(财务负责人):办税人:电话:税务机关(受理专用章):注:本表一式二份,经税务机关受理后,退纳税人一份,税务机关留存一份。

填表说明

一、适用范围及报送期限:

本表适用于执行企业会计准则的非银行、保险、担保、证券业纳税人填报;

企业所得税按月预缴的纳税人按月度、年度报送,其他纳税人按季度、年度报送,季(月)度报送期为季(月)度终了后15日内,年度报送期为年度终了后5个月内。

二、表内逻辑关系:

①11=1-2-3-4-5-6-7+8+9;

②9≥10;

③15=11+12-13;

④13≥14;

⑤17=15-16;

⑥“二、营业利润(亏损以“-”号填列)”、“三、利润总额(亏损总额以“-”号填列)”、“四、

净利润(净亏损以“-”号填列)”:为合计数据。

三、填报注意事项:

“所属时期”:为该会计年度第一日至所属期月(季)、年度最后一日。

未发生金额的行(列)次可以为“空”或在“元”对应的格内填“0”,但若逻辑公式(关系)中的某一项不为“0”的,逻辑计算(关系)的其中数、合计数或差值数必须填报。

SSAP 2STATEMENT OF STANDARD ACCOUNTING PRACTICE 2NET PROFIT OR LOSS FOR THE PERIOD,FUNDAMENTAL ERRORSAND CHANGES IN ACCOUNTING POLICIES(Revised March 1984, December 1993 and May 1999 and October 2001)The standards, which have been set in bold italic type, should be read in the context of the background material and implementation guidance and in the context of the Foreword to Statements of Standard Accounting Practice, Interpretations and Accounting Guidelines. Statements of Standard Accounting Practice are not intended to apply to immaterial items (see paragraph 8 of the Foreword). ObjectiveThe objective of this Statement is to prescribe the classification, disclosure and accounting treatment of certain items in the income statement so that all enterprises prepare and present an income statement on a consistent basis. This enhances comparability both with the enterprise's financial statements of previous periods and with the financial statements of other enterprises. Accordingly, this Statement requires the classification and disclosure of extraordinary items and the disclosure of certain items within profit or loss from ordinary activities. It also specifies the accounting treatment for changes in accounting estimates, changes in accounting policies and the correction of fundamental errors. Scope1.This Statement should be applied in presenting profit or loss from ordinary activities andextraordinary items in the income statement, and in accounting for changes in accountingestimates, fundamental errors and changes in accounting policies.2. This Statement supersedes SSAP 2 "Extraordinary items and prior period adjustments"approved in 1984 and revised in 1993.3. This Statement deals with, among other things, the disclosure of certain items of net profit orloss for the period. These disclosures are made in addition to any other disclosures required by other Accounting Standards.4. This Statement also deals with certain disclosures relating to discontinued operations. It doesnot deal with the recognition and measurement issues related to discontinued operations.Definitions5.The following terms are used in this Statement with the meanings specified:"Extraordinary items" are income or expenses that arise from events or transactions that are clearly distinct from the ordinary activities of the enterprise and therefore are not expected to recur frequently or regularly."Ordinary activities" are any activities which are undertaken by an enterprise as part of its business and such related activities in which the enterprise engages in furtherance of,incidental to, or arising from, these activities.A "discontinued operation" results from the sale or abandonment of an operation thatrepresents a separate, major line of business of an enterprise and of which the assets, netprofit or loss and activities can be distinguished physically, operationally and for financialreporting purposes."Fundamental errors" are errors discovered in the current period that are of suchsignificance as to invalidate the true and fair view of previously issued financial statements in respect of one or more prior periods."Accounting policies" are the specific principles, bases, conventions, rules and practicesadopted by an enterprise in preparing and presenting financial statements.Net profit or loss for the period6.All items of income and expense recognised in a period should be included in thedetermination of the net profit or loss for the period unless an Accounting Standard or, in the absence of a relevant Accounting Standard, the law requires or permits otherwise.7. Normally, all items of income and expense recognised in a period are included in thedetermination of the net profit or loss for the period. This includes extraordinary items and the effects of changes in accounting estimates. However, circumstances may exist when certainitems may be excluded from net profit or loss for the current period. This Statement deals with two such circumstances: the correction of fundamental errors and the effect of changes inaccounting policies.8. Other Accounting Standards deal with items which may meet the Framework definitions ofincome or expense but which are usually excluded from the determination of the net profit orloss. Examples include revaluation surpluses (see SSAP 17 "Property, plant and equipment" and SSAP 13 "Accounting for investment properties") and gains and losses arising on the translation of the financial statements of a foreign entity (see SSAP 11 "Foreign currency translation"). 9.The net profit or loss for the period comprises the following components, each of whichshould be disclosed on the face of the income statement:a.profit or loss from ordinary activities; andb.extraordinary items.Extraordinary items10.The nature and the amount of each extraordinary item should be separately disclosed.11. Virtually all items of income and expense included in the determination of net profit or loss forthe period arise in the course of the ordinary activities of the enterprise. Therefore, only on rare occasions does an event or transaction give rise to an extraordinary item12. Whether an event or transaction is clearly distinct from the ordinary activities of the enterpriseis determined by the nature of the event or transaction in relation to the business ordinarilycarried on by the enterprise rather than by the frequency with which such events are expected to occur. Therefore, an event or transaction may be extraordinary for one enterprise but notextraordinary for another enterprise because of the differences between their respective ordinary activities. For example, losses sustained as a result of an earthquake may qualify as anextraordinary item for many enterprises. However, claims from policyholders arising from an earthquake do not qualify as an extraordinary item for an insurance enterprise that insuresagainst such risks.13. Examples of events or transactions that generally give rise to extraordinary items for mostenterprises are:a. the expropriation of asset; orb. an earthquake or other natural disaster.14. The disclosure of the nature and amount of each extraordinary item may be made on the face ofthe income statement, or when this disclosure is made in the notes to the financial statements, the total amount of all extraordinary items is disclosed on the face of the income statement. The extraordinary items may be presented net of related taxation and minority interests with thegross amount of each shown in the notes to the financial statements.Profit or loss from ordinary activities15.When items of income and expense within profit or loss from ordinary activities are of suchsize, nature or incidence that their disclosure is relevant to explain the performance of theenterprise for the period, the nature and amount of such items should be disclosed separately.16. Although the items of income and expense described in paragraph 15 are not extraordinaryitems, the nature and amount of such items may be relevant to users of financial statements in understanding the financial position and performance of an enterprise and in making projections about financial position and performance. Disclosure of such information is usually made in the notes to the financial statements.17. Circumstances which may give rise to the separate disclosure of items of income and expense inaccordance with paragraph 15 include:a. the write-down of inventories to net realisable value or property, plant and equipment torecoverable amount, as well as the reversal of such write-downs;b. a restructuring of the activities of an enterprise and the reversal of any provisions for thecosts of restructuring;c. disposals of items of property, plant and equipment;d. disposals of long-term investments;e. discontinuedoperations;fe. litigation settlements; andgf. other reversals of provisions.Discontinued operations18. While the disposal of investments or other major assets may be sufficiently important to warrantdisclosure of the related items of income or expense, occasionally an enterprise sells orabandons a separate, major line of business which is distinguishable from other businessactivities. When this constitutes a discontinued operation as defined in this Statement, thedisclosures contained in paragraph 19 are relevant to users of financial statements.19.The following disclosures should be made for each discontinued operation:a.the nature of the discontinued operation;b.the industry and geographical segments in which it is reported (if applicable);c.the effective date of discontinuance for accounting purposes;d.the manner of discontinuance (sale or abandonment);e.the gain or loss on discontinuance and the accounting policy used to measure thatgain or loss; andf.the revenue and profit or loss from ordinary activities of the operation for the period,together with the corresponding amounts for each prior period presented.20. The results of a discontinued operation are generally included in profit or loss from ordinaryactivities. However, in the rare circumstances that the discontinuance is the result of events or transactions that are clearly distinct from the ordinary activities of the enterprise and therefore are not expected to recur frequently or regularly, the income or expenses that arise from thediscontinuance are treated as extraordinary items. For example, if a subsidiary is expropriated by a foreign government, the income or expense that arise from the expropriation may qualify as an extraordinary item. The disclosure requirements in paragraph 19 are applied for alldiscontinued operations including those that give rise to extraordinary items.21. When it is known at the date on which the financial statements are authorised for issue that anoperation was discontinued after the balance sheet date or that it will be discontinued, thedisclosure requirements of paragraph 19 are applied to the extent that the information can bereliably estimated. The accounting and disclosure of such post balance sheet events are alsospecified in SSAP 9 "Events after the balance sheet date" "Accounting for post balance sheetevents ".Changes in accounting estimates22. As a result of the uncertainties inherent in business activities, many financial statement itemscannot be measured with precision but can only be estimated. The estimation process involves judgements based on the latest information available. Estimates may be required, for example, of bad debts, inventory obsolescence or the useful lives or expected pattern of consumption of economic benefits of depreciable assets. The use of reasonable estimates is an essential part of the preparation of financial statements and does not undermine their reliability.23. An estimate may have to be revised if changes occur regarding the circumstances on which theestimate was based or as a result of new information, more experience or subsequentdevelopments. By its nature, the revision of the estimate does not bring the adjustment within the definitions of an extraordinary item or a fundamental error.24. Sometimes it is difficult to distinguish between a change in accounting policy and a change inan accounting estimate. In such cases, the change is treated as a change in an accountingestimate, with appropriate disclosure.25.The effect of a change in an accounting estimate should be included in the determination ofnet profit or loss in:a.the period of the change, if the change affects the period only; orb.the period of the change and future periods, if the change affects both.26. A change in an accounting estimate may affect the current period only or both the current periodand future periods. For example, a change in the estimate of the amount of bad debts affectsonly the current period and therefore is recognised immediately. However, a change in theestimated useful life or the expected pattern of consumption of economic benefits of adepreciable asset affects the depreciation expense in the current period and in each periodduring the remaining useful life of the asset. In both cases, the effect of the change relating to the current period is recognised as income or expense in the current period. The effect, if any, on future periods is recognised in future periods.27.The effect of a change in an accounting estimate should be included in the same incomestatement classification as was used previously for the estimate.28. To ensure the comparability of financial statements of different periods, the effect of a change inan accounting estimate for estimates which were previously included in the profit or loss from ordinary activities is included in that component of net profit or loss. The effect of a change in an accounting estimate for an estimate which was previously included as an extraordinary item is reported as an extraordinary item.29.The nature and amount of a change in an accounting estimate that has a material effect inthe current period or which is expected to have a material effect in subsequent periods should be disclosed. If it is impracticable to quantify the amount, this fact should be disclosed.Fundamental errors30. Errors in the preparation of the financial statements of one or more prior periods may bediscovered in the current period. Errors may occur as a result of mathematical mistakes,mistakes in applying accounting policies, misinterpretation of facts, fraud or oversights. Thecorrection of these errors even if material is normally included in the determination of net profit or loss for the current period.31. On rare occasions, an error has such a significant effect on the financial statements of one ormore prior periods that those financial statements can no longer be considered to have shown a true and fair view at the date of their issue. These errors are referred to as fundamental errors.An example of a fundamental error is the inclusion in the financial statements of a previousperiod of material amounts of work in progress and receivables in respect of fraudulentcontracts which cannot be enforced. The correction of fundamental errors that relate to priorperiods requires the restatement of the comparative information.32. The correction of fundamental errors can be distinguished from changes in accountingestimates. Accounting estimates by their nature are approximations that may need revision asadditional information becomes known. For example, the gain or loss recognised on theoutcome of a contingency which previously could not be estimated reliably does not constitute the correction of a fundamental error.33.The amount of the correction of a fundamental error that relates to prior periods should bereported by adjusting the opening balance of retained earnings. Comparative informationshould be restated, unless it is impracticable to do so and this fact is disclosed.34. The financial statements, including the comparative information for prior periods, are presentedas if the fundamental error had been corrected in the period in which it was made. Therefore, the amount of the correction that relates to each period presented is included within the net profit or loss for that period. The amount of the correction relating to periods prior to those included in the comparative information in the financial statements is adjusted against the opening balance of retained earnings in the earliest period presented. Any other information reported with respect to prior periods, such as historical summaries of financial data, is also restated.35. The restatement of comparative information does not necessarily give rise to the amendment offinancial statements which have been approved by shareholders or registered or filed withregulatory authorities.36.An enterprise should disclose the following for each separate fundamental error:a.the nature of the fundamental error;b.the amount of the correction for the current period and for each prior periodpresented;c.the amount of the correction relating to periods prior to those included in thecomparative information; andd.the fact that comparative information has been restated or that it is impracticable to doso.Changes in accounting policies37. Users need to be able to compare the financial statements of an enterprise over a period of timeto identify trends in its financial position, performance and cash flows. Therefore, the sameaccounting policies are normally adopted in each period.38 A change in accounting policy should be made only if required by statute, or by anAccounting Standard, or if the change will result in a more appropriate presentation of events or transactions in the financial statements of the enterprise.39. A more appropriate presentation of events or transactions in the financial statements occurswhen the new accounting policy results in more relevant or reliable information about thefinancial position, performance or cash flows of the enterprise.40. The following are not changes in accounting policies:a. the adoption of an accounting policy for events or transactions that differ in substancefrom previously occurring events or transactions; andb. the adoption of a new accounting policy for events or transactions which did not occurpreviously or that were immaterial.The initial adoption of a policy to carry property, plant or equipment at revalued amounts is a change in accounting policy but it is dealt with as a revaluation in accordance with SSAP 17"Property, plant and equipment" rather than in accordance with paragraphs 45 to 49 of thisStatement.41. A change in accounting policy is applied retrospectively or prospectively in accordance with therequirements of this Statement. Retrospective application results in the new accounting policy being applied to events and transactions as if the new accounting policy had always been in use.Therefore, the accounting policy is applied to events and transactions from the date of origin of such items. Prospective application means that the new accounting policy is applied to theevents and transactions occurring after the date of the change. No adjustments relating to prior periods are made either to the opening balance of retained earnings or in reporting the net profit or loss for the current period because existing balances are not recalculated. However, the new accounting policy is applied to existing balances as from the date of the change.Adoption of an Accounting Standard42. A change in accounting policy which is made on the adoption of an Accounting Standardshould be accounted for in accordance with the specific transitional provisions, if any, in that Accounting Standard. In the absence of any transitional provisions, the change in accounting policy should be applied in accordance with the treatment prescribed in paragraphs 45, 48and 49 of this Statement.43. The transitional provisions in an Accounting Standard may require either a retrospective or aprospective application of a change in accounting policy.44. When an enterprise has not adopted a new Accounting Standard which has been published bythe Hong Kong Society of Accountants but which has not yet come into effect, the enterprise is encouraged to disclose the nature of the future change in accounting policy and an estimate of the effect of the change on its net profit or loss and financial position.Other changes in accounting policies45. A change in accounting policy should be applied retrospectively unless the amount of anyresulting adjustment that relates to prior periods is not reasonably determinable. Anyresulting adjustment should be reported as an adjustment to the opening balance of retained earnings or reserves, as appropriate. Comparative information should be restated unless it is impracticable to do so.46. The financial statements, including the comparative information for prior periods, are presentedas if the new accounting policy had always been in use. Therefore, comparative information is restated in order to reflect the new accounting policy. The amount of the adjustment relating to periods prior to those included in the financial statements is adjusted against the openingbalance of retained earnings or reserves, as appropriate, of the earliest period presented. Anyother information with respect to prior periods, such as historical summaries of financial data, is also restated.47. The restatement of comparative information does not necessarily give rise to the amendment offinancial statements which have been approved by shareholders or registered or filed withregulatory authorities.48.The change in accounting policy should be applied prospectively when the amount of theadjustment to the opening balance of retained earnings required by paragraph 45 cannot be reasonably determined.49.When a change in accounting policy has a material effect on the current period or any priorperiod presented, or may have a material effect in subsequent periods, an enterprise should disclose the following:a.the reasons for the change;b.the amount of the adjustment for the current period and for each period presented;c.the amount of the adjustment relating to periods prior to those included in thecomparative information; andd.the fact that comparative information has been restated or that it is impracticable to doso.Effective date50.The accounting practices set out in this Statement should be regarded as standard in respectof financial statements relating to accounting periods beginning on or after 1 January 1999.Earlier adoption is encouraged but not required.Note on legal requirements in Hong Kong51. Paragraph 17(6) of the Tenth Schedule to the Companies Ordinance requires the following to bestated by way of note if not otherwise shown:"Any material respects in which any items shown in the profit and loss account are affected -a. by transactions of a sort not usually undertaken by the company or otherwise bycircumstances of an exceptional or non-recurrent nature; orb. by any change in the basis of accounting."Compliance with International Accounting Standards52. International Accounting Standard No 8 (revised 1993) "Net profit or loss for the period,fundamental errors and changes in accounting policies" allows a benchmark treatment forpresenting the correction of a fundamental error that relates to prior periods by restating thecomparative information and a benchmark treatment for presenting the change in accountingpolicy by making resulting adjustment to the opening balance of retained earnings. It alsopermits as alternative treatments the presentation of additional pro forma information for thecorrection of a fundamental error and the change in accounting policy. The respectiverequirements of this Statement accord very closely with the benchmark treatments permittedunder IAS 8.In addition, IAS 8 gives a different definition of fundamental errors as compared to therespective definition as stated in paragraph 5 of this Statement. Except for the above differences, compliance with this Statement ensures compliance in all material respects with IAS 8.AppendixThe Appendix is illustrative only and does not form part of the Statement of Standard Accounting Practice. The purpose of this Appendix is to illustrate the application of the Statement of Standard Accounting Practice to assist in clarifying its meaning. Extracts from income statements and statements of retained earnings are provided to show the effects on these financial statements of the transactions described below. These extracts do not necessarily conform with all the disclosure and presentation requirements of other Statements of Standard Accounting Practice. Extraordinary items and discontinued operationsAlpha CoExtract from the income statement20-2 $ 20-1 $Gross profit 10,000 12,000 Loss on sale of truck engine valve manufacturingoperation (Note 1)(3,000) - Taxation (2,100) (3,600) Profit from ordinary activities 4,900 8,400Extraordinary item - loss on expropriation of car enginevalve manufacturing operation in country R (Net oftaxation of $1,350)(Note 2) - (3,150)Net profit4,900======5,250====== Extracts from notes to the financial statements1. On 1 July 20-2, Alpha sold its truck engine valve manufacturing operation. The results of thisoperation had previously been reported in the valve manufacturing industry segment and thedomestic geographical segment. The loss is the difference between the proceeds from the sale of the operation and the net carrying amount of the assets and liabilities of the operation at the date of sale. The revenues recognised relating to this operation from 1 January 20-2 until 1 July 20-2 were $15,000 ($35,000 -- 20-1) and the profits before tax were $5,000 ($10,000 -- 20-1).2. On 1 October 20-1, Alpha's car engine valve manufacturing operation in country R wasexpropriated, without compensation, by the Government. The results of this operation hadpreviously been reported in the valve manufacturing industry segment and the Pacificgeographical segment. The loss arising from the expropriation has been accounted for as anextraordinary item. The gross loss arising from the expropriation represents the net carryingvalue of the assets and liabilities of the operation at the date of expropriation which amounted to $4,500. The revenues recognised relating to this operation from 1 January 20-1 until 1 October 20-1 were $10,000 and the profits before tax were $2,000.Fundamental errorsDuring 20-2, Beta Co discovered that certain products that had been sold during 20-1 but wereincorrectly included in inventory at 31 December 20-1 at $20,000 as the result of a fraudulent actcommitted by senior management.Beta's accounting records for 20-2 show sales of $94,000, cost of goods sold of $86,500 (including$20,000 for error in opening inventory), and taxation of $2,250.In 20-1, Beta reported:$Sales 90,000 Cost of goods sold (53,500)Profit from ordinary activities before taxation 36,500Taxation (10,950)Net profit 25,550=======20-1 opening retained earnings was $20,000 and closing retained earnings was $45,550.Beta's profit tax rate was 30% for 20-2 and 20-1.Beta CoExtract from the income statement20-2 ______20-1 (restated)$ $Sales 94,000 90,000 Costs of goods sold (66,500) (73,500)Profit from ordinary activities before taxation 27,500 16,500 Taxation (8,250) (4,950)Net profit 19,250=======11,550 =======Beta Co Statement of retained earnings20-2 ______20-1 (restated)$ $Opening retained earnings as previously reported 45,550 20,000 Correction of fundamental error (Net of taxation of$6,000) (Note 1)(14,000) - Opening retained earnings as restated 31,550 20,000 Net profit 19,250 11,550Closing retained earnings 50,800=======31,550 =======Extract from notes to financial statements1. Certain products that had been sold in 20-1 were incorrectly included in inventory at 31December 20-1 at $20,000 as the result of a fraudulent act committed by senior management.The financial statements of 20-1 have been restated to correct this error.Changes in accounting policyDuring 20-2, Gamma Co changed its accounting policy with respect to the treatment of borrowing costs that are not directly attributable to the acquisition of a hydro-electric power station which is in course of construction for use by Gamma. In previous periods, Gamma had capitalised such costs net of taxation. Gamma has now decided to expense, rather than capitalise, these costs in order to comply with SSAP 19 "Borrowing costs".Gamma capitalised borrowing costs incurred of $2,600 during 20-1 and $5,200 in periods prior to20-1.Gamma's accounting records for 20-2 show profit from ordinary activities before interest and taxation of $30,000; interest expense of $3,000 (which relates only to 20-2); and taxation of $8,100. Gamma has not yet recognised any depreciation on the power station because it is not yet in use.。