成本与管理会计 亨格瑞 第13版 英文版 CA15

- 格式:ppt

- 大小:2.14 MB

- 文档页数:61

亨格瑞成本与管理会计

亨格瑞(Hengrui)是一家知名的成本与管理会计公司。

他们专注于提供成本管理、绩效管理和策略管理等方面的解决方案和咨询服务。

成本管理是指通过对企业资源和活动的成本进行测算、分析和控制,来提高企业效益和降低成本的管理方法。

亨格瑞通过帮助企业建立

成本计划和预算、制定成本控制策略、优化成本结构等手段,帮助

企业降低成本、提高利润。

绩效管理是指通过设定绩效目标、制定绩效评价体系、实施绩效测

算和分析,来提高企业绩效和激励员工的管理方法。

亨格瑞通过设

计和实施绩效管理制度、开展绩效评估和考核、提供培训和改进方

案等手段,帮助企业优化绩效,实现战略目标。

策略管理是指通过对企业内外环境的分析和评估,制定和执行战略

计划,来提高企业竞争力和市场地位的管理方法。

亨格瑞通过帮助

企业制定战略目标、开展战略规划和执行、提供战略改善建议等手段,帮助企业提升竞争力,实现可持续发展。

亨格瑞拥有一支专业的团队,拥有丰富的成本与管理会计经验,能

够根据企业的实际情况,提供量身定制的解决方案,帮助企业提高

运营效率和盈利能力。

成本与管理会计第15版亨格瑞简介《成本与管理会计》是由亨格瑞(Horngren)等人合著的一本经典教材,该教材详细介绍了成本和管理会计的基本概念、原则和技术。

本文将对该教材进行概览,探讨其中的关键内容。

第1章管理会计与组织绩效本章主要介绍管理会计的概念和作用,以及与组织绩效之间的关系。

管理会计是一种为管理决策提供支持的会计信息系统,通过提供与企业内部运营相关的成本和绩效信息,帮助管理层进行决策和控制。

第2章基本成本管理概念本章重点介绍成本管理的基本概念,包括成本对象、成本中心和成本效益分析等。

成本对象是指需要计算和分配成本的实体,成本中心是指组织内部负责经营活动的部门或单位,成本效益分析则是对不同决策方案进行成本与效益比较的方法。

第3章成本分类和费用估算本章讲解了成本分类和费用估算的方法和原则。

成本可以根据不同的分类方法进行归类,如按功能分类、按行业分类等。

费用估算的方法包括直接费用估算和间接费用估算,其中间接费用估算需要通过成本驱动因素进行分配。

第4章成本行为成本行为是指成本与产量或活动水平之间的关系。

本章将介绍常见的成本行为模式,如固定成本、变动成本和半固定成本。

了解成本行为模式有助于管理者预测和控制成本的变化。

第5章成本估算和预测成本估算和预测是管理会计的核心任务之一。

本章将介绍成本估算和预测的方法和技术,包括趋势分析、回归分析和敏感度分析等。

第6章作业成本系统作业成本系统是一种在生产中分配和追踪成本的方法。

本章将详细介绍作业成本系统的构成要素和运作流程,并介绍常见的作业成本方法,如作业订单和作业批次。

第7章过程成本系统过程成本系统是一种适用于连续流程生产的成本分配方法。

本章将介绍过程成本系统的特点和运作原理,以及与作业成本系统的异同。

第8章活动成本管理活动成本管理是一种基于活动的成本分析和管理方法。

本章将介绍活动成本管理的概念和技术,包括活动成本驱动因素的确定和活动成本分析模型的构建。

第9章管理会计信息系统管理会计信息系统是支持管理会计活动的信息系统。

![亨格瑞成本与管理会计(中英第15版)中文PPT (10)[42页]](https://uimg.taocdn.com/3c01b924ba0d4a7303763ac7.webp)

![亨格瑞成本与管理会计(中英第15版)中文PPT (19)[32页]](https://uimg.taocdn.com/6923d407b14e852459fb57c0.webp)

成本与管理会计第15版亨格瑞

《成本与管理会计第15版亨格瑞》是一本关于成本和管理会计的教材,由亨格瑞(Horngren)等人合著。

该教材主要涵盖了成本与管理会计的基本概念、技术和应用,旨在帮助读者理解和应用成本与管理会计的原理和方法。

该教材的内容主要包括以下几个方面:

1. 成本与管理会计的基本概念:介绍了成本与管理会计的定义、目标和作用,以及与其他会计学科的关系。

2. 成本与管理会计的基本原理:介绍了成本与管理会计的基本原理,包括成本分类、成本行为、成本估算等。

3. 成本与管理会计的技术和方法:介绍了成本与管理会计的技术和方法,包括成本核算、成本控制、成本预测、绩效评估等。

4. 成本与管理会计的应用:介绍了成本与管理会计在不同行业和组织中的应用,包括制造业、服务业、非营利组织等。

5. 成本与管理会计的决策支持:介绍了成本与管理会计在决策过程中的应用,包括定价决策、投资决策、生产决策等。

《成本与管理会计第15版亨格瑞》的特点是理论与实践相结合,内容丰富全面,注重案例分析和实际应用。

该教

材适合会计、管理和经济学专业的学生,以及从业人员和研究者参考使用。

需要注意的是,由于该教材是第15版,可能存在一些更新和修订的内容。

建议读者在使用该教材时,参考最新的版本或与教材出版社联系,以获取最准确和详细的信息。

Cost and Managerial Accounting English Version 15thEdition Course DesignIntroductionCost and Managerial Accounting is an essential course for all business-related majors. The course is designed to introduce students to the principles, techniques, and tools used in cost and managerial accounting. The m is to provide students with a clear understanding of how to manage various costs associated with the production of goods and services, and how to use this information to make informed business decisions.The fifteenth edition of the textbook Cost and Managerial Accounting is considered a comprehensive and authoritative resource in the field. The course design presented in this document is based on this textbook, and it is intended to provide a roadmap for teaching and learning the course.Learning ObjectivesThe learning objectives of the Cost and Managerial Accounting course include:•Understand the differences between cost accounting and managerial accounting•Identify and analyze various types of cost-related issues that companies encounter•Develop skills for assigning costs to products, services, and other cost centers•Use financial and non-financial information effectively to make informed decisions•Develop knowledge and skills for budgeting and forecasting•Understand the principles of performance measurement and variance analysisCourse OutlineThe Cost and Managerial Accounting course should cover the following topics:Introduction to Cost and Managerial Accounting•The role of cost and managerial accounting in decision making•Differences between financial accounting and managerial accounting•Cost concepts: direct and indirect costs, variable and fixed costs, etc.Job Order and Process Costing Systems•Job order costing and process costing systems•Assigning direct costs and indirect costs to products and services•Calculating unit costs and production volume measures Cost-Volume-Profit Analysis•Understanding the relationships between costs, volume, and profits•Breakeven analysis, contribution margin, and margin of safety•Sensitivity analysis and what-if scenariosActivity-Based Costing and Activity-Based Management•The ABC system and its advantages in management decision-making•Identifying and analyzing cost drivers and activity centers•Implementing and using the ABC system to allocate costs Budgeting and Standard Costing Systems•Preparing and using budgets for planning and control•Types of budgets: sales, production, direct material, direct labor, overhead, and cash•Variance analysis: materials, labor, and overhead variances Performance Measurement and Management•Evaluating and managing performance using various performance measures•Balanced scorecard and key performance indicators (KPIs)•Continuous improvement and the role of benchmarking Teaching StrategiesThe following teaching strategies can be used to promote effective learning in the Cost and Managerial Accounting course:Classroom LecturesClassroom lectures are a primary mode of teaching in the course, and they should cover topics from the textbook. The instructor should alsouse real-world examples to illustrate specific concepts and techniques. The lectures should also encourage student participation and provide a forum for class discussions.Team ActivitiesGroup activities, such as case studies, group projects, and team presentations, enhance student teamwork, critical thinking, and communication skills. Group activities also provide students with an opportunity to apply managerial accounting concepts in different contexts.Quizzes and ExamsQuizze s and exams serve as an assessment tool to measure students’ knowledge, understanding, and application of managerial accounting concepts. The exams should be structured to include multiple-choice questions, problem-solving questions, and short answer questions.ConclusionThe Cost and Managerial Accounting course is critical for students majoring in business. This course design provides instructors with a roadmap for teaching the course based on the fifteenth edition of the textbook Cost and Managerial Accounting. The course covers essential topics such as job order and process costing, cost-volume-profit analysis, budgeting, performance measurement, and management. The use of classroom lectures, group activities, and exams are effective teaching strategies that will help students achieve the course’s learning objectives.。

![亨格瑞成本与管理会计(中英第15版)中文PPT (21)[33页]](https://uimg.taocdn.com/ed37d655bceb19e8b9f6bab0.webp)

亨格瑞成本与管理会计

亨格瑞成本与管理会计(Hengry Cost and Management Accounting)是一种用于管理决策和成本控制的会计方法。

它提供了详细的成本信息,以帮助管理者做出准确的决策,并监控和控制企业的成本。

亨格瑞成本与管理会计主要包括以下几个方面:

1. 成本分类与分析:亨格瑞成本与管理会计通过对成本进

行分类和分析,帮助企业了解各项成本的性质和构成,并

将其与企业的经营活动相对应。

常见的成本分类包括直接

成本和间接成本、可变成本和固定成本等。

2. 成本核算与计算:亨格瑞成本与管理会计通过成本核算

和计算,确定各个产品或服务的成本,并将其分配到相应

的产品或服务上。

这有助于企业了解不同产品或服务的盈

利能力,并进行定价和销售策略的制定。

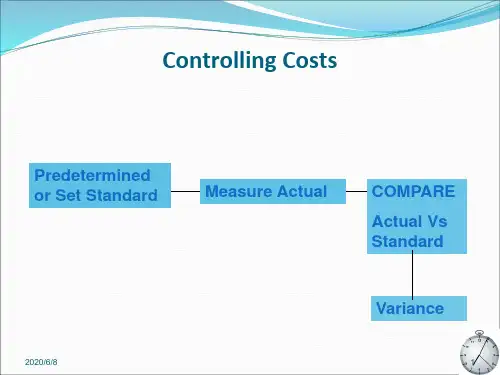

3. 成本控制与预算:亨格瑞成本与管理会计通过成本控制

和预算,帮助企业控制和管理成本,并制定合理的预算计划。

通过对实际成本与预算成本的比较,企业可以及时发

现和纠正成本偏差,并采取相应的措施进行成本控制。

4. 决策支持与绩效评估:亨格瑞成本与管理会计提供了决

策支持和绩效评估的信息。

通过对不同决策方案的成本效

益分析,帮助企业做出合理的决策,并评估和监控企业的

绩效。

总之,亨格瑞成本与管理会计是一种重要的管理工具,通过提供详细的成本信息和决策支持,帮助企业进行成本控制和管理,并提高企业的绩效和竞争力。