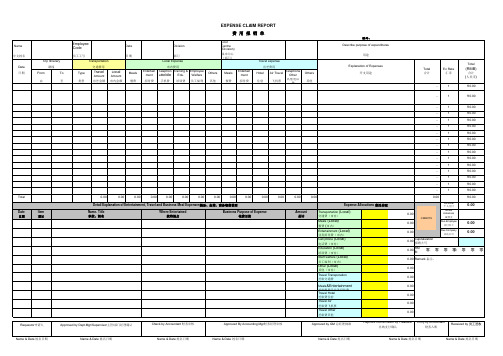

Expenses form

- 格式:xls

- 大小:41.50 KB

- 文档页数:1

DCF2013 - 2014 Academic YearD eclaration anD c ertification of f inances (Dcf) f ormUndergraduate Day ProgramsGlobal Pathways or American Classroom students moving to Undergraduate Day ProgramsUndergraduate day program at Northeastern must complete the Declaration and Certification of Finances (DCF) Form in order to obtain a form I-20 for his/her new program. This I-20 form indicates that an international applicant has been accepted as a full-time degree-seeking student, has the required proficiency in English, and that there is sufficient financial support for his/her education while studying in the U.S. Northeastern will provide an international student with a new I-20 form to enable the student to keep his/her law-ful student (F-1) status when changing program/degree within Northeastern.Please note:1. The complete DCF form and required supporting documents (listed in Section D) must be submitted to Undergraduate Admis-sions prior to completion of the Global Pathways or American Classroom Program.2. If you are planning to travel outside of the United States, before the start of your new degree program, please remember that uponre-entry the U.S. you must use the I-20 form for your new program of study issued by the ISSI.3. As an international student you are required to complete Immigration Clearance prior to course registration. Therefore you shouldarrive on campus no later than the new program/degree start date (see item # 5 on your new I-20 form), and report in person to the ISSI during the scheduled Immigration Clearance session. Please have your passport, I-94 card, and ALL I-20s with you.Completing immigration clearance is essential for compliance with University policies and federal regulations.PERSONAL INFORMATION - Please type or print in block letters.► Important: Always spell your name(s) consistently on all forms /applications.Family Name: Given (First) Name/Middle Name:Current U.S. Address (required):Street Apt City State ZipEmail Address: Telephone Number: ( )DCF INSTRUCTIONSPlease note that your Certificate of Eligibility (I-20 form) cannot be issued unless complete information and appropriate certification are submitted. This form must be completed in English, typed or printed clearly.1. Complete Section A – Financial Declaration2. Supply a bank statement to accompany the completed Financial Declaration OR have a bank representative fill in, sign and sealSection B – Certification of Sources of Funds & Amounts. Financial documents must be sertified within 12 months prior to the program start date. If a bank statement accompanies this document, it must be an Original, written in English and should include:• Sponsor’s name (written in English) on the account• Opening date of account and current balance listed in U.S. dollars.If you are being sponsored by your government or another sponsoring agency:• Complete Section A - Financial Declaration• Include original or certified copy of your award letter detailing which fees will be provided by your sponsor(s)ESTIMATE OF EXPENSES FOR THE ACADEMIC YEAR 2013-2014 – BASED ON TWO SEMESTER (8 MONTHS) These figures are estimates for the 2013-2014 academic year and are subject to change at any time by Northeastern University’s Board of Trustees (costs increase about 5% per year). All amounts in US$.Tuition$40,696University fees 952Room and board (for standard double room in a resi-dence & 15 meals per week plan)13,580Medical insurance (per academic year)2,249Books, supplies, and personal expenses2,800Total (8 Months)$ 60,277A student will need at least $60,277 for the academicyear (September to April). Additional living expensesfor the Summer (May to August) will add approxi-mately $5,000 to your yearly expenses.SECTION A: FINANCIAL DECLARATIONPlease list and document the total amount needed and sources of financial support during your program of study at Northeastern in the Declaration and Certification of Finances (DCF) Form. Current financial documents must accompany the DCF form.TO BE COMPLETED BY THE STUDENT’S SPONSOR(S) (PARENT, FAMILY MEMBER, OR PRIV ATE SPONSOR) I hereby certify that I am willing and that I promise to provide the amount of $ per year payable in US dollars for years (2-4 year’s minimum for transfer student, 4-5 years for freshmen) for the educational expenses while at Northeastern University and all living expenses of (print student’s name)who is my (identify relationship) .Documentation of my financial resources in the form of a bank letter is attached or Bank Official completed in Section B of this form.Sponsor’s name Sponsor’s signature Datemm/dd/yyyy Sponsor’s current addressPlease Note: If there is more than one sponsor or financial source(s), please submit additional letters of support and bank documentation. Please attach documentation for other types of funding you may be receiving, for example: scholarships, government sponsored grants, etc.SECTION B: OFFICIAL CERTIFICATION OF SOURCE(S) OF FUNDS AND AMOUNTSTO BE COMPLETED BY THE FINANCIAL INSTITUTION/BANKThe above sources and amounts must be verified by official bank certification below or attached letters of certification by the bank(s). Please note that bank letters must indicate the actual amount on deposit.PHOTOCOPIES OF FINANCIAL DOCUMENTS WILL NOT BE ACCEPTED.ALL DOCUMENTS MUST BE IN ENGLISH OR AN OFFICIAL NOTARIZED TRANSLATION MUST BE PROVIDED.“This is to certify that I have read the information provided by the applicant on this from, that it is a true and ac-curate statement, that the funds are available and that they can be transferred to the United States”Signature of Bank Of Bank Official Datemm/dd/yyPrint Name and Title of Bank official Name and address of BankFAILURE TO OBTAIN BANK SIGNATURE AND SEAL MAY DELAY THE ISSUANCE OF A VISA ELIGIBILTY DOCUMENT (I-20 FORM). APPLY BANK SEAL OR STAMP HERE ►TO BE COMPLETED BY THE STUDENT - Please read the following statement and sign below:“I certify that all statements on this form are true and accurate and that the stated funds are available for my educational expenses while at Northeastern University during the period specified. I understand that under the Privacy Act,the information that I provide cannot be given to anyone outside the university without my written permission.I will notify Northeastern University of any changes to my financial circumstances.Furthermore, I understand that falsification of any financial documentation or signatures is grounds for cancellation of my application for the form I-20 and subsequent enrollment.”Student’s full name Student’s Signature: Date:mm/dd/yySECTION C: DELIVERY INSTRUCTIONSDocuments will not be mailed without complete and clear instructions.Delivery (please select one A or B)□ A. Hold my visa eligibility document (form I-20) for pick-up.Please contact □ Mr. □Ms:Last/First Nametelephone: (required) e- mail: ( required)□ B. Mail my visa eligibility document (form I-20) to the following address:(please fill in address below; type or print in block letters)Required information:Street Address line 1:►Note: Express services cannot deliver to a P.O. BoxStreet Address line 2:City: State/Province:Country: ZIP/Postal Code (required):Mailing Address Telephone Number (required):IMPORTANT: The mailing address format outlined above is essential for delivery by the FedEx service.Failure to follow the exact format will result in rejection of the shipment by the express mail carrier. SECTION D: REQUIRED SUPPORTING DOCUMENTS1. The DCF form - filled out completely.2. An original financial document covering all expenses for one academic year (e.g., student’s bank statement, an affidavit of support, the letter from government agency, NU award letter, etc., ) If you have more than one source of funding, please provide the required documentation corresponding to each source. The financial documentation accompanying your DCF form must be an ORIGINAL, written in ENGLISH or an official / notarized translation must be provided.The bank statement must include:• Sponsor’s name (written in English) on the account• Opening date of account and current balance listed in U.S. dollars.• Date of statement3. Photocopy of the identity page(s) of your passport.4. Photocopy of your I-94 form (front and back)Please submit the DCF Form and all required supporting document to:Nancy Baker, Admissions AssistantUndergraduate Admissions200 Kerr Hall, Northeastern UniversityIMPORTANT: Documents will be accepted on Monday - Friday between 8:30 am -11:30 am ONLY.The ISSI will need between 8 to 10 business days after receipt of the student’s complete application from Undergraduate Admission to process a form I-20 for a new degree program. Please note incomplete or insufficient documentation will result in a delay in the processing of an I-20 form for your new degee program。

1.Accounting(会计)The process of indentifying,recording, summarizing and reporting economic information to decision makers.2.Financial accounting(财务会计)The field of accounting that serves external decision makers,such as stockholders,suppliers, banks and government agencies.3.Management accounting(管理会计)The field of accounting that serves internal decision makers,such as top executives,department headsand people at other management levels within an organization.4.Annual report(年报)A combination of financial statements,management discussion and analysis and graphs and charts that is provided annually to investors.5.Balance sheet (statement of financial position,statement of financial condition)(资产负债表)A financial statement that shows the financial status of a business entity at a particular instant in time.6.Balance sheet equation(资产负债方程式)Assets = Liabilities + Owners' equity.7.Assets(资产)Economic resources that are expected to help generate future cash inflows or help reduce future cash outflows.8.Liabilities (负债)Economic obligations of the organization to outsiders ,or claims against its assets by outsiders.9.Owners’ equity (所有者权益)The residual interest in the organization’s assets after deducting liabilities.10.Notes payable (应付票据)Promissory notes that are evidence of a debt and state the terms of payment.11.Entity (实体)An organization or a section of an organization that stands apart from other organization and individuals as a separate economics unit.12.Transaction (交易)Any event that both affects the financial position of an entity and be reliably recorded in money terms.13.Inventory (存货)Goods held by a company for the purpose of sale to customers.14.Account (帐户)A summary record of the changes in a particular assets,liability,or owne r’ equity.15.Account payable (应付帐款)A liability that results from a purchase of goods or services on account.17.Creditor (债权人)A person or entity to whom money is owed.18.Debtor (债务人)A person or entity that owes money to another.19.Sole proprietorship (个体经营、独资经营)A separate organization with a single owner.20.Partnership (合伙)A form of organization that joins two or more individuals together as co-owners(共有人).21.Corporation (公司)A business organization that is created by individual state laws.22.Limited liability (有限责任)A feature of the corporate form of organization whereby corporate creditors ordinarily have claims against the corporate assets only.23.Publicly owned (公有)A corporation in which shares in the ownership are sold to thepublic.24.Privately owned (私有)A corporation owned by a family,a small group of shareholders,or a single individual,in which shares of ownership are not publicly sold.25.Stockholders’ equity (shareholders’ equity) (股东权益)Own ers’ equity of a corporation.The excess of assets over liabilities of a corporation.26.Paid-in capital(实际投入资本)The total capital investment in a corporation by its owners both at and subsequent to the inception of business.27.Par value(票面值)The nominal dollar amount printed on stock certificates.29.Auditor (审计师)A person who examines the information used by managers to prepare the financial statements and attests to the credibility of those statements.31.Audit (审计)An examination of transactions and financial statement made in accordance with generally accepted auditing standards.33. Fiscal year (会计、财政年度)The year established for accounting purposes.34.Interim periods (中期)The time spans established for accounting purposes that are less than a year.35.Revenues(sales) (收入OR商品销售收入)Increases in owners’ equity arising from increases in assets received in exchange for the delivery of goods or services to customers.36.Expenses (费用)Decreases in owners’ equity that arise because goods or services are delivered to customers.37.Income (profit ,earnings) (收益、利润)The excess of revenues over expenses.39.Accrual basis (应计制、权责发生制)Accounting method that recognizes the impact of transactions on the financial statements in the time periods when revenues and expenses occur.40.Cash basis (收付实现制)Accounting method that recognizes the impact of transactions on the financial statements only when cash is received or disbursed.43.Cost of goods sold (cost of sales) (销售成本)The original acquisition cost of the inventory that was sold to customers during the reporting period.44.Matching (配比)The recording of expenses in the same time period as the related revenues are recognized.47.Depreciation (折旧)The systematic allocation of the acquisition cost of long-lived of fixed assets to the expenses accounts of particular periods that benefit from the use of the assets. income (净利润)The remainder after all expenses has been deducted from revenues.49.Income statement (statement of earnings, operating statement) (收益表)A report of all revenues and expenses pertaining to a specific time period.50.Statement of cash flows (cash flow statement) (现金流量表)A required statement that reports the cash receipts and cash payments of an entity during a particular period. loss (净损失)The difference between revenues and expenses when expenses exceed revenues.52.Cash dividends (现金股利)Distribution of cash to stockholders that reduce retained income.53.Statement of retained income (利润分配表)A statement that lists the beginning balance in retained income, followed by a description of any changes that occurred during the period, and the ending balance.54.Statement of income and retained income (收入及利润分配表)A statement that included a statement of retained income at the bottom of an income statement.55.Earnings per share (EPS) (每股收益)Net income divided by average number of common shares outstanding.56.Price-earnings ratio (P-E) (市盈率)Market price per share of common stock divided by earnings per share of common stock.57.Dividend-yield ratio (股息率)Common dividends per share dividend by market price per share.58.Dividend-payout ratio (派息率)Common dividends per share dividend by earnings per share.59.Double-entry system (复试记账法)The method usually followed for recording transactions, whereby at least two accounts are always affected by each transaction.60.Ledger (分类账)The records for a group of related accounts kept current in asystematic manner.61.General ledger (总分类账)The collection of accounts that accumulates the amounts reported in the major financial statements.62.T-account (T形账户)Simplified version of ledger accounts that takes the form of the capital letter T.63.Balance (余额)The difference between the total left-side and right-side amounts in an account at any particular time.64.Debit (借方)An entry or balance on the left side of an account.65.Credit (贷方)An entry or balance on the right side of an account.66.Charge (Debit)A word often used instead of debit.67.Source documents (原始凭证)The supporting original records of any transactions.68.Book of original entry (原始分录帐本)A formal chronological record of how the entity’s transactions affect the balances in pertinent accounts.69.General journal (普通日记账)The most common example of a book of original entry; a complete chronological record of transactions.70.Trial balance (试算表)A list of all accounts in the general ledger with their balance.71.Journalizing (记入分类帐)The process of entering transactions into the journal.72.Journal entry (日记帐分录)An analysis of the affects of a transaction on the accounts, usually accompanied by an explanation.81.Accumulated depreciation (allowance for depreciation) (累计折旧)The cumulative sum of all depreciation recognized since the date of acquisition of the particular assets described.82.Data processing 数据处理The totality to the procedures used to record, analyze store, and report on chosen activities.83.Explicit transactions (显性交易)Events such as cash receipts and disbursements, credit purchases, and credit sales that trigger nearly all day-to-day routine entries.84.Implicit transactions (非显性交易)Events (such as the passage of time) that do not generate source documents or visible evidence of the event and are not recognized in the accounting records until the end of an accounting period.85.Adjustments (adjusting entries) (调帐)End-of-period entries that assign the financial effects of implicit transactions to the appropriate time periods.86.Accrue (应计)To accumulate a receivable or payable during a given period eventhough no explicit transactions occurs.87.Unearned revenue (revenue received in advance, deferred revenue, deferred credit) (未实现收入)Revenue received and recorded before it is earned.88.Pretax income (税前利润)Income before income taxes.89.Classified balance sheet (分类资产负债表)A balance sheet that groups the accounts into subcategories to help readers quickly gain a perspective on the company’s financial position.90.Current assets (流动资产)Cash plus assets that are expected to be converted to cash or sold or consumed during the next 12 months or within the normal operating cycle if longer that a year.91.Current liabilities (流动负债)Liabilities that fall due within the coming year or within the normal operating cycle if longer than a year.92.Working capital (营运资金、资本)The excess of current assets over current liabilities.93.Solvency (偿付能力)An entity’s ability to meet its immediate financial obligations as they become due.94.Current ratio (working capital ratio) (流动比率)Current assets divided by current liabilities.Current ratio = Current assets / Current liabilities.95.Report format (报表格式之一)A classified balance sheet with the assets at the top. Example:Balance Sheet, January 31,20X2Assets 1999 1998Current assetsCashAccounts receivable……Total current assetsLong-term assetsStore equipmentAccumulated depreciationTotal assetsLiabilities and Owners’ Equity 1999 1998 Current liabilitiesNote payableAccounts payable…Total current liabilities Stockholder’s equityPaid-in capitalRetained incomeTotal liabilities and owners’ equity96.Account format (报表格式之二)A classified balance sheet with the assets at the left. Example:Balance Sheet, January 31,20X2Assets Liabilities and Owners’ EquityCurrent assets Current liabilitiesCash Note payableAccounts receivable Accounts payable… …Total current assets Total current liabilitiesLong-term assets Stockholder’s equityStore equipment Paid-in capitalAccumulated depreciation Retained incomeTotal Total97.Single-step income statement (单一步骤收入表)An income statement that groups all revenues together and then lists and deducts all expenses together without drawing any intermediate subtotals.98.Multiple-step income statement (复合步骤收入表)An income statement that contains one or more subtotals that highlight significant relationships.99.Gross profit (gross margin) (毛利)The excess of sales revenue over the cost of the inventory that was sold.100.Operating income (operating profit) (营业收入)Gross profit less all operating expenses.101.Profitability (收益能力)The ability of a company to provide investors with a particular rate of return on their investment.102.Gross profit percentage (gross margin percentage) (毛利率)Gross profit divided by sales.Gross profit percentage=Gross profit / Sales103.Return on sales ratio (销售收益率)Net income divided by sales,104.Return on stockholders’ equity ratio (股东权益收益率)Net income divided by invested capital (measured by average stockholder’s equity)。

Fees expenses英文合同

在英文合同中,费用和支出通常被定义和规定,以明确各方的责任和义务。

以下是一个典型的费用和支出相关的合同条款示例:费用和支出(Fees and Expenses)

费用支付:甲方同意承担以下费用,而乙方同意支付以下费用:

a、甲方费用:甲方将承担与合同履行有关的一切费用,包括但不限于劳动力成本、材料采购、设备租赁等。

b、乙方费用:乙方同意支付以下费用,包括但不限于许可证费、保险费、交付费、运输费、维护费、服务费等。

费用报销:乙方同意在收到甲方提供的费用报销请求后,迅速支付甲方支出的费用。

开支授权:甲方同意事先征得乙方书面同意,以便支出任何可能需要的额外费用。

乙方应在收到征得同意的请求后,确认同意或拒绝。

发票和记录:甲方应向乙方提供与费用相关的发票和详细记录,以支持费用报销请求。

支付期限:乙方应在收到费用报销请求后的[指定天数]内支付相关费用。

逾期支付的费用将被追加逾期利息。

争议解决:任何有关费用和支出的争议应根据合同其他争议解决条款解决。

变更通知:任何涉及费用和支出的变更应以书面形式通知并获得双方同意。

附加条款:任何与费用和支出相关的附加条款和条件将在合同的附加文件中规定。

这是一个典型的费用和支出合同条款示例,实际合同可能需要根据特定交易的性质和需求进行修改和定制。

费用和支出的合同条款通常被用于确保各方对费用的支付和管理有清晰的规定,以避免潜在的争议和误解。