财务报表分析(英文版)标准答案

- 格式:doc

- 大小:630.00 KB

- 文档页数:39

一.经营活动产生的现金流量cash flows from operating activities 销售商品,提供劳务收到的现金现金流量表cash flows statement项目items金额amountcash received from sales of goods or rendering of services收到的税费返还refund of taxes收到的其他与经营活动有关的现金other cash received relating to operating activities现金流入小计sub-total of cash inflows购买商品接受劳务支付的现金cash paid for goods and services支付给职工以及为职工支付的现金cash paid to and on behalf of employees支付的各项税费taxes paid支付的其他与经营活动有关的现金other cash paid relating to operating activities现金流出小计sub-total of cash outflows经营活动产生的现金流量净额net cash flows from operating activities二.投资活动产生的现金流量cash flows from investing activities收回投资所收到的现金cash received from return of investments取得投资收益所得到的现金cash received from income of investments处置固定资产,无形资产和其他长期资产而收到的现金净额net cash received from disposal of fixed assets,intangible assets and other long-term assets 收到的其他与投资活动有关的现金other cash received relating to investing activities现金流入小计sub-total of cash inflows购建固定资产,无形资产和其他长期资产所支付的现金cash paid to acquire fixed assets,intangible assets and other long-term assets 投资所支付的现金cash paid to acquire investments支付的其他与投资活动有关的现金other cash paid relating to investing activities现金流出小计sub-total of cash outflows投资活动产生的现金净额net cash flows from investing activities三.筹资活动产生的现金流量cash flows from finacing activities吸收投资所收到的现金proceeds from invested assets借款所收到的现金proceeds from borrowings收到的其他与筹资活动有关的现金other proceeds relating to financing activities现金流入小计sub-total of cash inflows偿还债务所支付的现金cash repayments of amounts borrowed分配股利,利润或偿付利息所支付的现金cash payments for distribution of dividends,profit or interest expenses支付的其他与筹资活动有关的现金other cash payments relating to finacing activities现金流出小计sub-total of cash outflows筹资活动产生的现金流量净额net cash flows from finacing activities四.汇率变动对现金的影响effect of foreign exchange rate changes on cash五.现金及现金等价物净增加额net increase in cash and cash equivalents补充资料supplemental information1.将净利润调节为经营活动的现金流量reconciliation of net profit to cash flows from operating activities净利润net profit加:计提的资产减值准备add:assets shrink provision固定资产折旧depreciation of fixed assets无形资产摊销amortization of intangible assets长期待摊费用摊销amortization of long term deferred expenses待摊费用的减少(减:增加)decrease in prepaid and deferred expenses(less:increase)预提费用的增加(减:减少)increase in accrued expenses(less:decrease)处置固定资产,无形资产和其他长期资产的损失(减:收益)losses on disposal of fixed assets,intanglble assets and other long-term assets(less:gains)固定资产报废损失losses on scrapping of fixed assets财务费用financial expenses投资损失(减:收益)income on investment(less:losses)递延税款贷项(减:借项)deferred tax credit(less:debit)存货的减少(减:增加)decrease in inventories(less:increase)经营性应收项目的减少(减:增加)decrease in operating receivables (less:increase)经营性应付项目的增加(减:减少)increase in operating payables(less:decrease)其他others经营活动产生的现金流量净额net cash flows from operating activities2.不涉及现金收支的投资和筹资活动investing and financing activities that do not involve in cash receipts and payments:债务转为资本liabilities to be transfer captial一年内到期的可转换公司债券matured convertible bonds within a year融资租入固定资产fixed assets under finacing leasing3.现金及现金等价物净增加情况net increase in cash and cash equivalents现金的期末余额cash at the end of the period减:现金的期初余额less:cash at the beginning of the period加:现金等价物的期末余额plus:cash equivalents at the beginning of the period 减:现金的期初余额less:cash equivalents at the beginning of the period 现金及现金等价物净增加额net increase in cash and cash equivalents。

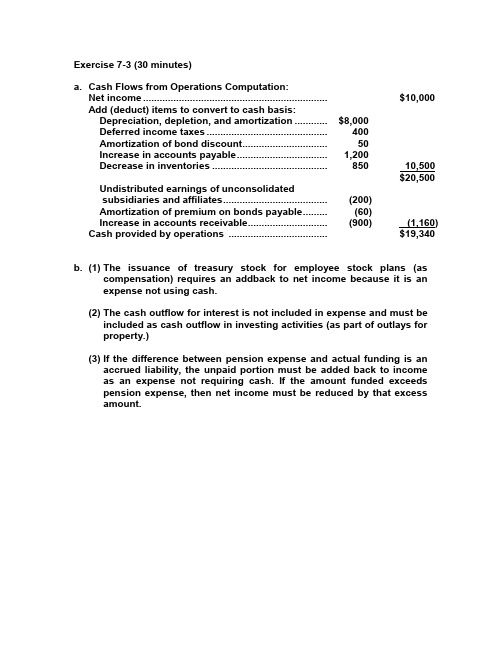

a. Cash Flows from Operations Computation:Net income ................................................................... $10,000 Add (deduct) items to convert to cash basis:Depreciation, depletion, and amortization ............ $8,000Deferred income taxes (400)Amortization of bond discount (50)Increase in accounts payable ................................. 1,200Decrease in inventories .......................................... 850 10,500$20,500 Undistributed earnings of unconsolidatedsubsidiaries and affiliates (200)Amortization of premium on bonds payable (60)Increase in accounts receivable ............................. (900) (1,160) Cash provided by operations .................................... $19,340 b. (1) The issuance of treasury stock for employee stock plans (ascompensation) requires an addback to net income because it is anexpense not using cash.(2) The cash outflow for interest is not included in expense and must beincluded as cash outflow in investing activities (as part of outlays forproperty.)(3) If the difference between pension expense and actual funding is anaccrued liability, the unpaid portion must be added back to incomeas an expense not requiring cash. If the amount funded exceedspension expense, then net income must be reduced by that excessamount.a. Beginning balance of accounts receivable ........ $ 305,000Net sales ............................................. 1,937,000Total potential receipts $2,242,000Ending balance of accounts receivable ............. - 295,000Cash collected from sales $1,947,000b. Ending balance of inventory ................................ $ 549,000Cost of sales ......................................................... +1,150,000Total ............................................. $1,699,000Beginning balance of inventory .......................... - 431,000Purchases ............................................................. $1,268,000 Beginning balance of accounts payable $ 563,000Purchases (from above) ....................................... 1,268,000Total potential payments ..................................... $1,831,000Ending balance of accounts payable .................. - 604,000Cash payments for accounts payable ................ $1,227,000c. Issuance of common stock.................................. $ 81,000Issuance of treasury stock .................................. 17,000Total nonoperating cash receipts ....................... $ 98,000d. Increase in land .................................................... $ 150,000Increase in plant and equipment ......................... 18,000Total payments for noncurrent assets ............... $ 168,000 Exercise 7-5 (20 minutes)b. X Fc. X Fd. X Ie. X Ff. NCNg. X Ih. NCSi. X Fj. X X Ob. X Fc. NCNd. X Ie. NCSf. NCNg. X Ih. NCSi. NE j. NE Exercise 7-7 (30 minutes)Net Cash from Cash2. NE NE +3. + + +4a. - NE NE4b. NE(1)+(2)+(2)4c. - +(2)+(2)5. NE + +6. - + (long-run -) + (long-run -)7. - -(5)+8. + NE NE9. +(3)+(4)+(4)10. NE + +11. + + +12. NE NE +13. NE NE +(1) Deferred tax accounting.(2) Depends on whether tax savings are realized in cash.(3) If profitable.(4) If accounts receivable collected.(5) Depends on whether interest is paid or accrued.Further explanations (listed by proposal number):1. Substituting payment in stock for payment in cash for its dividends will not affectincome or CFO but will increase cash position.2. In the short run, postponement of capital expenditures will save cash but have noeffect on income or CFO. In the long term, both income and CFO may suffer due to lower operating efficiency.Exercise 7-7—continued3. Cash not spent on repair and maintenance will increase all three measures. However,the skimping on necessary discretionary costs will adversely impact future operating efficiency and, hence, profitability.4. Managers advocating an increase in depreciation may have spoken in the mistakenbelief that depreciation is a source of cash and that consequently increasing it would result in a higher cash inflow. In fact, the level of depreciation expense has no effect on cash flow—the same amount of depreciation deducted in arriving at net income is added back in arriving at CFO. On the other hand, increasing depreciation for tax purposes will in all cases result in at least a short-term savings.5. Quicker collections will not affect income but will increase CFO because of loweraccounts receivable. Cash will also increase by the speedier conversion of receivables into cash. In the longer run this stiffening in the terms of sale to customers may result in sales lost to competition.6. Payments stretched-out will lower income because of lost discounts but doespositively affect CFO by increasing the level of accounts payable. Cash conservation will result in a higher cash position. Relations with suppliers may be affected adversely. Note: Long-term cash outflow will be higher because of the lost discount. 7. Borrowing will result in interest costs that will decrease income and CFO. Cashposition will increase.8. This change in depreciation method will increase income in the early stages of anasset's life. The opposite may hold true in the later stages of the asset's life.9. In the short term, higher sales to dealers will result in higher profits (assuming we sellabove costs) and, if they pay promptly, both CFO and cash will increase. However, unless the dealers are able to sell to consumers, such sales will be made at the expense of future sales.10. This will lead to less income from pension assets in the future which could causefuture pension expense to increase.11. The cost of funding inventory will be reduced in the future. In the current period netincome may also be increased by a LIFO liquidation from reduced inventory levels. 12. The current period decline in the value of the trading securities has been reflected incurrent period income, as has the previous gain. Although the sale will increase cash, it will have no effect on current period income. If the current period decline is deemed to be temporary, the company is selling a potentially profitable security for a short-term cash gain.13. Reissuance of treasury shares will increase cash, but will have no effect on currentperiod income as any “gain” or “loss” is reflected in additional paid in capital, not income. If the stock price is considered to be temporarily depressed, the company is foregoing a future sale at a greater market price and is, thus, suffering current dilution of shareholder value.Exercise 7-9 (60 minutes)Notes:[a] Balance at 7/29/Year 10 ........................................... $624.5 [33]Less: increase in Year 10 ........................................ (60.4) [61]$564.1[b]This amount is overstated by the provision for doubtful accounts expense that is included in another expense category.Note [a]: Item [89] represents dividends declared, not dividends paid (see also Item [77]).d. The entry for the income tax provision for Year 11 is:Income tax expense [27] ...................................... 265.9Deferred income tax (current) plug .................. 12.1Income tax payable ............................................ 230.4Deferred income tax (noncurrent) [a] .............. 23.4Notes:(1) The entry increases current liabilities by $12.1 since deferred income tax (current)is credited by this amount. It also increases current liabilities by $230.4 [124A], the amount of income taxes payable.(2) The [a] is the difference in the balance of the noncurrent deferred income tax item[176] = $258.5 - $235.1 = $23.4.(3) Also, $23.4 + $12.1 = $35.5, which is total deferred tax [59] or [127A]Exercise 7-9—continuede. Depreciation expense has no effect on cash from operations. The credit,when recording the depreciation expense, goes to accumulated depreciation, a noncash account.f. These provisions are added back because they affect only noncashaccounts, the charge to earnings must be removed in converting it to the cash basis.g. The “Effect of exchange rate changes on cash” represents translationadjustments (differences) arising from the translation of cash from foreign currencies to the U.S. dollar.h. Any gain or loss is reported under "other, net"—Item [60].i. Free cash flows =Cash flow from operations –Cash used for capital additions –Dividends paidYear 11: $805.2 – $361.1 – $137.5 = $306.6Year 10: $448.4 – $387.6 – $124.3 = $(63.5)Year 9: $357.3 – $284.1 – $86.7 = $(13.5)j. Start-up companies usually have greater capital addition requirements and lower cash inflows from operations. Also, start-ups rarely pay cash dividends. Free cash flow earned by start-up companies is usually used to fund the growth of the company, especially if successful.k. During the launch of a new product line, the statement of cash flows can be affected in several ways. First, cash flow from operations is lower because substantial advertising and promotion is required and sales growth has not yet been maximized. Second, substantial capital additions are usually necessary to provide the infrastructure for the new product line. Third, cash flow from financing can be affected if financing is obtained to launch this new product line.。

会计英语报表试题及答案1. 单项选择题A. 资产负债表的英文表达是什么?a) Balance Sheetb) Income Statementc) Cash Flow Statementd) Statement of Changes in Equity答案:a) Balance Sheet2. 填空题B. 在会计英语中,“流动资产”通常被翻译为________。

答案:Current Assets3. 判断题C. 利润表通常用来展示一个企业在一定时期内的财务状况。

(对/错)答案:错4. 简答题D. 请简述资产负债表和利润表的主要区别。

答案:资产负债表展示了企业在某一特定时间点的财务状况,包括资产、负债和所有者权益。

而利润表则展示了企业在一定时期内的经营成果,包括收入、成本和利润。

5. 翻译题E. 将以下会计术语翻译成英文:1) 存货2) 长期债务3) 营业收入答案:1) Inventory2) Long-term Debt3) Operating Revenue6. 计算题F. 假设某公司年初资产总额为$100,000,年末资产总额为$120,000,年初负债总额为$50,000,年末负债总额为$60,000。

请计算该公司年末所有者权益总额。

答案:年末所有者权益总额 = 年末资产总额 - 年末负债总额 = $120,000 - $60,000 = $60,0007. 案例分析题G. 阅读以下财务报表摘要,并回答以下问题:- 公司名称:XYZ公司- 销售收入:$500,000- 销售成本:$300,000- 营业费用:$50,000- 净利润:$100,000- 请计算XYZ公司的毛利润和营业利润。

答案:- 毛利润 = 销售收入 - 销售成本 = $500,000 - $300,000 = $200,000- 营业利润 = 毛利润 - 营业费用 = $200,000 - $50,000 = $150,0008. 论述题H. 讨论现金流量表在企业财务管理中的重要性。

财务报表分析相关知识概述(英文版Exercise 7-3 (30 minutes)a. Cash Flows from Operations Computation:Net income ................................................................... $10,000 Add (deduct) items to convert to cash basis:Depreciation, depletion, and amortization ............ $8,000Deferred income taxes (400)Amortization of bond discount (50)Increase in accounts payable ................................. 1,200Decrease in inventories .......................................... 850 10,500$20,500 Undistributed earnings of unconsolidatedsubsidiaries and affiliates (200)Amortization of premium on bonds payable (60)Increase in accounts receivable ............................. (900) (1,160) Cash provided by operations ................................... $19,340 b. (1) The issuance of treasury stock for employee stock plans (ascompensation) requires an addback to net income because it is anexpense not using cash.(2) The cash outflow for interest is not included in expense and must beincluded as cash outflow in investing activities (as part of outlays forproperty.)(3) If the difference between pension expense and actual funding is anaccrued liability, the unpaid portion must be added back to income asan expense not requiring cash. If the amount funded exceeds pensionexpense, then net income must be reduced by that excess amount.a. Beginning balance of accounts receivable ........ $ 305,000Net sales ............................................ 1,937,000Total potential receipts $2,242,000Ending balance of accounts receivable ............. - 295,000Cash collected from sales $1,947,000b. Ending balance of inventory ................................ $ 549,000Cost of sales ......................................................... +1,150,000Total ............................................. $1,699,000Beginning balance of inventory .......................... - 431,000Purchases ............................................................. $1,268,000 Beginning balance of accounts payable $ 563,000Purchases (from above) ....................................... 1,268,000Total potential payments ..................................... $1,831,000Ending balance of accounts payable .................. - 604,000Cash payments for accounts payable ................ $1,227,000c. Issuance of common stock.................................. $ 81,000Issuance of treasury stock .................................. 17,000Total nonoperating cash receipts ....................... $ 98,000d. Increase in land .................................................... $ 150,000Increase in plant and equipment ......................... 18,000Total payments for noncurrent assets ............... $ 168,000 Exercise 7-5 (20 minutes)b. X Fc. X Fd. X Ie. X Ff. NCNg. X Ih. NCSi. X Fj. X X Ob. X Fc. NCNd. X Ie. NCSf. NCNg. X Ih. NCSi. NE j. NE Exercise 7-7 (30 minutes)Net Cash from Cash2. NE NE +3. + + +4a. - NE NE4b. NE(1)+(2)+(2)4c. - +(2)+(2)5. NE + +6. - + (long-run -) + (long-run -)7. - -(5)+8. + NE NE9. +(3)+(4)+(4)10. NE ++11. + ++12. NE NE +13. NE NE +(1) Deferred tax accounting.(2) Depends on whether tax savings are realized in cash.(3) If profitable.(4) If accounts receivable collected.[a] B alance at 7/29/Year 10 ........................................... $624.5 [33]Less: increase in Year 10 ........................................ (60.4) [61]$564.1[b]This amount is overstated by the provision for doubtful accounts expense that is included in another expense category.Note [a]: Item [89] represents dividends declared, not dividends paid (see also Item [77]).d. The entry for the income tax provision for Year 11 is:Income tax expense [27] ...................................... 265.9Deferred income tax (current) plug ................ 12.1Income tax payable ............................................ 230.4Deferred income tax (noncurrent) [a] .............. 23.4Notes:(1) The entry increases current liabilities by $12.1 since deferred income tax (current) iscredited by this amount. It also increases current liabilities by $230.4 [124A], the amount of income taxes payable.(2) The [a] is the difference in the balance of the noncurrent deferred income tax item[176] = $258.5 - $235.1 = $23.4.(3) Also, $23.4 + $12.1 = $35.5, which is total deferred tax [59] or [127A]Exercise 7-9—continuede. Depreciation expense has no effect on cash from operations. The credit,when recording the depreciation expense, goes to accumulated depreciation, a noncash account.f. These provisions are added back because they affect only noncashaccounts, the charge to earnings must be removed in converting it to the cash basis.g. The “Effect of exchange rate changes on cash” represents translationadjustments (differences) arising from the translation of cash from foreign currencies to the U.S. dollar.h. Any gain or loss is reported under "other, net"—Item [60].i. Free cash flows =Cash flow from operations –Cash used for capital additions –Dividends paidYear 11: $805.2 – $361.1 – $137.5 = $306.6Year 10: $448.4 – $387.6 – $124.3 = $(63.5)Year 9: $357.3 – $284.1 –$86.7 = $(13.5)j. Start-up companies usually have greater capital addition requirements and lower cash inflows from operations. Also, start-ups rarely pay cash dividends. Free cash flow earned by start-up companies is usually used to fund the growth of the company, especially if successful.k. During the launch of a new product line, the statement of cash flows can be affected in several ways. First, cash flow from operations is lower because substantial advertising and promotion is required and sales growth has not yet been maximized. Second, substantial capital additions are usually necessary to provide the infrastructure for the new product line. Third, cash flow from financing can be affected if financing is obtained to launch this new product line.。

Financial Statement AnalysisTo develop techniques for evaluating firms using financial statement analysis for equity and credit analysis.Integrates financial statement analysis with corporate finance, accounting and fundamental analysis.Adopts activist point of view to investing: the market may be inefficient and the statements may not tell all the truth.What Will You Learn From the Course• How statements are generated• The role of financial statements in determining firms’ values• How to pull ap art the financial statements to get at the relevant information• How ratio analysis aids in valuation• The relevance of cash flow and accrual accounting information • How to calculate what the P/E ratio should be ?• How to calculate what the price-to-book ratio ?Need for financial statement analysisGAAP – ComplexEconomic events about the firm to be reported to the public Relevance vs ReliabilityReporting: Recognition vs Disclosure (where)Users of Firms’ Financial InformationEquity InvestorsInvestment analysisLong term earnings powerManagement performance evaluationAbility to pay dividendRisk – especially marketDebt InvestorsShort term liquidityProbability of defaultLong term asset protectionCovenant violationsUsers of Firms’ Financ ial InformationManagement: Strategic planning; Investment in operations;Performance EvaluationLitigants - Disputes over value in the firmCustomers - Security of supplyGovernments: Policy making and Regulation– Taxation– Government contractingEmployees: Security and remunerationInvestors and management are the primary users of financial statementsFundamental AnalysisStep 1 - Knowing the Business•The Products; The Knowledge Base•The Competition’ The Regulatory ConstraintsStep 2 - Analyzing Information•In Financial Statements•Outside of Financial StatementsStep 3 - Forecasting Payoffs•Measuring Value Added•Forecasting Value AddedStep 4 - Convert Forecasts to a ValuationStep 5 - Trading on the Valuation•Outside Investor: Compare Value wi th Price to; BUY, SELL, or HOLD•Inside Investor: Compare Value with Cost to; ACCEPT orREJECT StrategyA valuation model guides the process: Forecasting is at the heartof the process and a valuation model specifies what is to be forecasted (Step 3) and how a forecast is converted to a valuation (Step 4). What is to be forecasted (Step 3) dictates the information is implied?Balance Sheet•Assets (SFAC6): “probable future economic benefits obtained or controlled by a particular entity as a resultof past transaction or events-- no reference to risk (eg, assets sold but in which entityretains a risk)•Liabilities (SFAC6): ‘probable future sacrifice of economic benefits arising from present obligations of a particularentity to transfer assets or provide services to other entities in the future as a result of past transactions or events”-- not always followed (eg, certain leases and, until recently, pension benefits)•Equity (SFAC6): the residual interest in the net assets of an entity that remains after deducting its liabilities”-- does not handle situations where a source of capitalhas elements of debt & equity (eg, convertibles)•Classified by liquidityCA : converted to cash or used within 1-year oroperating cycle (if longer)CL: obligations expected to be settled within 1-year oroperating cycle•Tangible A&L reported above intangibles (goodwill, contingent liabilities)Measurement of Assets & Liabilities•Historical Cost, for most components of Balance Sheet •May be at market under “lower of cost or market rule”•Reversals of prior write downs allowed for marketable equity securities but not for inventories•Financial service firms (banks, brokerage, insurance) report certain A&L at market•A&L of foreign affiliates reported at end-of-period X-rate or a combination of it and specified historicalX-rates•Intangible assets have uncertain and hard to measure benefits and are reported only when acquired via a“purchase method” acquisition-- brand names-- when reported, called Goodwill, Patents, etc.Two Fundamental shortcomings of the Balance Sheet Elusiveness of valueValue cannot be assigned to all assetsOther Balance Sheet issues: Book Value vs. Market ValueInflation: The correct way to think about inflation is that inflation represents a decline in the value of one good – the currency of denomination (i.e., the U.S. dollar in our case). When the value of the currency declines, prices of all other goods & services rise because those prices are measured in terms of dollarsWeakness of Historical Cost Accounting: it ignores the impact of changes in the purchasing power of the currency. The net impact of not considering inflation is that book value understates the market value.Obsolescence causes book value to overstate market valueHow to Measure Effect of Obsolescencea. Observe difference between market value & book value (after adjustingfor inflation)b. Estimate the value of the asset’s earning power. But this is simply thediscounted cash flow approach & thus it represents circular reasoning.Inflation & ObsolescenceInflation causes book value to understate market valueObsolescence causes book value to overstate market valueThe effect of inflation & obsolescence may not be apparent in an examination of book values because they offset one anotherOrganizational Capitala. The whole is worth more than the sum of the partsb. Returns to Entrepreneurshipc. Difficult to separate from the firm as a going concernd. Can be estimated only by examining the earning power of the companySources of Organizational Capital Valuesa. Long-term relationshipsb. Reputational “brand name” capitalc. Growth optionsd. Network of suppliers and distributorsMore on Organizational Capitala. It is difficult to separate the firm’s organizational capital from the firm as anongoing concernb. The value of a brand name is not reflected in the replacement cost of assetsc. Can only be estimated by examining the earning power of the company (DCF)Adjustments to Book ValueEstimate Replacement CostEstimate Liquidation ValueDrawbacksDo adjusted book values reflect market values?Adjusted book values do not consider organizational capital Drawbacks of AdjustmentsIt is often difficult to determine if we have made the correct adjustments Adjustments often fail to consider the value of off-balance sheet itemsReplacement CostNo universal agreementCan use price indexCPI, PPI, GDP implicit deflatorIgnores organizational capitalLiquidation ValueSecondary markets do not existAsset specificityContestable marketsIncome statementNet SalesCost of Goods SoldGross ProfitSelling & Administrative expensesAdvertisingLease paymentsDepreciation and amortizationRepairs and maintenanceOperating ProfitOther income (expense)Interest incomeInterest expenseEarnings before Income taxesIncome taxesNet earningsStatement of Consolidated Retained Earnings Retained earnings at beginning of yearNet earningsCash DividendsRetained earnings at end of yearIncome Statement•Based on Accrual accounting•Based on Matching Principle•Revenues(SFAC6) “inflows of an entity from delivering or producing goods, rendering services, or carrying out otheractivities that constitute the entities ongoing major or centraloperations”•Expenses(SFAC6) “outfl ows from delivering or producing goods, rendering services, or carrying out other activities thatconstitute the entities ongoing major or central operations”•COMPREHENSIVE INCOME CONCEPT“the change in equity from transactions from non-owner sources. It includes all changes in equity during a period except those resulting frominvestments by owners and distributions to owners”•Gains“Increases in equity from peripheral or incidental transactions of an entity except those that result from revenuesor invest ment by owners.”•Losses“Decreases in equity from peripheral or incidental transactions of an entity except those that result from revenuesor investment by owners.”Revenues+ Other income and revenues- E xpenses= Income from CONTINUING OPERATIONS∀Unusual or infrequent events= Pre tax earnings from continuing operations- I ncome tax expense= After tax earnings from continuing operations*∀Discontinued operations (net of tax)*∀Extraordinary operations (net of tax)*∀Cumulative effect of accounting changes (net of tax) * = Net Income ** Per share amounts are reported for each of these itemsHigh quality income statement reflect repeatable income statementGain from non-recurring items should be ignoredwhen examining earningsHigh quality earnings result from the use of conservative accounting principles that do not overstate revenues or understate costsLow Quality of Earnings Indicators1.Unstable Income Statement Elements unrelated to normalbusiness operations2 Earnings that reflect dubious adjustments to estimatedliability accounts3 Earnings that have been determined using liberal accountingpolicies (methods and estimates) because of the resultingoverstatement of net income. Such overstatement alsoresults in the overstatement of future earnings projections income based on ultraconservative accounting policiessince the resulting net income is misleading as a basis forpredicting future earningsWhat to do?Compare the company’s accounting polices to theprevalent accounting policies in the industry5.Unreliable and inaccurate accounting estimatesWhat to watch for?Prior estimates materially differ from actualexperience, such as where the company’s assumed interest rate onpension fund assets significantly differs from the actual interestrate earned as reflected by significant actuarial gains and losses.What to do?Restate net income as if realistic accounting estimateswere used.6. Earnings that have been artificially smoothed or managed.What to watch for?a. Revenue reflected earlier or later than the realistic time periodb. Shifting of expense among reporting periodsc. Smoothly rising earnings trendd. Sharp increase or decrease in sales in the last quarter of the yearsas reflected in the 4th quarter income statemente. Trading of investment securities among affiliated companiesf. Significant modification in estimated liability accounts in the lastquarterg. Writing down a good asset (inventory) and selling it next year toshow higher earningsh. The “big bath”, in whic h everything is written off in a really badyear so that it will be easier to show good profits in the followingyears. This sometimes occurs when new management takes overand wishes to blame old management for poor profits or whenearnings are already so low that their further reduction my nothave significant impactWhat to do?Look at the functional relationship of sales and netincome over time. An inconsistent relationship may be a manipulator indicator. Restate earnings by taking out profit increments orreductions due to income management ploys7.Deferral of costs that do not have future economic benefitWhat to watch fora. Inventory of unsalable items in view of current environment (8track tapes, typewriters, large automobiles during oil shortage)b. Sudden write-offs of inventoryc. Goodwill on the balance sheet but the company has none(operating at losses, significant decline in market share, badpublicity)d. Costs that are currently capitalized when in prior years, they wereexpensed (e.g. Tooling costs in inventory)What to doRestate net income as if the unrealistic deferral had not been made.8. Unjustified Changes in Accounting Principles and EstimatesWhat to watch fora. A firm has a past history of making frequent accounting changesb. Accounting changes that create earnings growthc. The company fires the auditor and hires another one because of adisagreement over a proposed accounting change.What to doa. Determine whether the accounting change is justified by seeing if itconfirms to requirements in FASB statements, Industry Audit Guides& IRS regulationsb. Ascertain whether the accounting change is preferable, given nature ofbusiness (e.g., decreasing the life of a computer because of newtechnological advances in the industry)c. Does change make sense? (Lowering bad debt expense as % ofaccounts receivable does NOT make sense when customer defaultsare rising)d. If accounting change results in increasing net income, restate earningsas they would have been if the old method had been retained.9.Premature or Belated Revenue RecognitionWhat to watch fora. Accruing unbilled salesb. Is there a sufficient provision for future losses in connection withthe recognition of revenue?c. Improper deferral of revenue to a later periodd. Reversal of previously recorded profitsWhat to do- Restate revenue as if proper revenue recognition were made10.Underaccrual or Overaccrual of ExpensesWhat to watch fora. Failure to incur necessary maintenance expendituresb. Inadequate warranty provisionWhat to do- Adjust net income for difference between expenseprovided & normal expense11.Improper Accounting PoliciesWhat to watch fora. Reduction of expense for overly anticipated recoveries of excesscosts due to modifications in government contractsb. Substantial provision for future costs in present year (e.g.warranties) because firm was remiss in making sufficientprovisions in prior yearsWhat to do-restate earning of years affected so can determineproper earnings trend12.Modification in Loan Agreements Due to FinanciallyWeak BorrowersWhat to watch for - lowering of interest on loanWhat to do - downwardly adjust net income for inclusion ofaccrued interest income on risky loans13.Change in corporate policy for the current year, whichimpacts earnings (e.g., writing insurance renewal contracts in the 4th quarter of the current year rather than the 1stquarter of the next year).14.Unjustified Cutback in Discretionary CostsWhat to watch fora. Declining tend in discretionary costs as a % of net sales or toassets to which they applyb. Vacillation in the ratio of discretionary costs to sales over theyears as this may indicate management of earningsWhat to doa. Determine trend in discretionary costs over time throughuse of index numbersb. Determine ratio of discretionary costs to sales over last 5years. An example is ratio of repairs & maintenance tosales and/or to fixed assets15.Book Income Substantially Exceeds Taxable IncomeWhat to watch for - A continual, significant rise in deferred income tax credit account due to liberal accounting policies16.Residual Income that is Substantially less than Net IncomeResidual Income may be determined by deducting the imputedcost of capital (weighted average cost of capital time total assets)from net income.What to do - Determine ratio over time of residual income to netincome17. A High Degree of Uncertainty Associated with IncomeStatement ComponentsWhat to watch fora. Firm engaged in long-term activities requiring many estimates inincome measurement processb. Significant future loss provisionsc. Estimates have been consistently materially different from actualexperienceWhat to doa. Compare over time firm’s estimated liability provisions withactual losses occurring. – e.g., warranty cost sb. Determine what percent of total assets are intangible, which bytheir nature require material estimates to be made18.Unreliably Reported EarningsWhat to watch fora. Poor system of internal control because it infers possibleerrors in reporting systemb. High turnover rate in auditorsc. Company has reputation for managing earnings and/or usingliberal accounting policiesd. Indications of lack of management integrity as evidenced bysuch things as bribesWhat to doa. Determine trend in audit fees over timeb. Examine for disclosure made by company related toadjustments due to prior years' accounting errorsc. Look at accounting, financial and brokerage researchpublications that note and give examples of companies withquestionable accounting policies.High Quality of Earnings Indicators: Income Backed up by Cash Income not involving the Inclusion of amortizationcosts related to questionable assets, such as deferredcharges Income that reflects Economic Reality4.Income Statements Components that are RecognizedClose to the Point of Cash Inflow and Cash OutflowPolicies that lower quality of earnings1. reduce expense for expected recovery of excess costs resultingfrom changes in government contract – only collected 65%2. unrealistic decline in percentage of sales allowance to sales3. provision for future costs (warranties) high becauseunderprovided in past4. “Big Bath”5. re-negotiate terms of loan with weak borrower6. transfer from 1 sub to another7. sell securities at a gain and buy them back at higher price- haveto recognize lossHow company smoothes earnings Check list1Does level discretionary cost conform to past2Is there a drop in trend of discretionary costs as percentage of sales3Does cost cutting program involve significant cut in discretionary costs4Does cost cutting program eliminate fat?5Do discretionary costs show fluctuations relative to sales 6Is there a sizable jump in discretionary costs?Summary checklist of key pointsA. No single “real” net income figure existsB. The analyst must adjust reported net income to anearnings figure that is relative to him/her.C. Earnings quality evaluation is important in investment,credit, audit & management decision making.D. Appraising the quality of earnings requires anexamination of accounting, financial, economic andpolitical factors.E. Earnings quality elements are both quantitative andqualitativeCash flow statement1. SCF (Statement of Cash Flows) adds in situations where Balance Sheetand Income Statement provide limited insight2. SCF helps identify the categories into which companies fit3. Financial flexibility is a useful weapon to gain a competitiveadvantage and is best measured by studying the SCFThe key analytical lessonsThe cash flow statement – not the income statement – provides the best information about a highly leveraged firm’s financial healthThere is no advantage in showing an accounting profit, the main consequence of which is incurring taxes, resulting, in turn, in reduced cash flowsCash Flow and Company Life CycleCash Flow and Start-up CompaniesLittle or no operating cash flowsLarge cash outflows for investing activitiesLarge need for external financing (mostly from issuing common stock, issue long term debt)Cash Flows and Emerging Growth CompaniesSome operating cash flow (not enough to sustain growth)Large cash outflows to expand activitiesRequires cash flows from financingPay back some short-term debt, issue some common stockCash Flows and Established Growth CompaniesFund growth from operating cash flowDepreciation is substantialRepayment of long term debt, begin to pay dividendCash Flows and Mature Industry Companies Modest capital requirementsDepreciation and amortization is significantNet negative reinvestmentLarge dividend payout, reduction in long term debt Cash Flows and Declining Industry Companies Net cash user (similar to emerging growth)Lower dividends, Slim operating cash flowssell assetsCash Flows and Financial FlexibilitySafety of dividendFinance growth with internal fundsMeet other financial obligationsFinancial Ratios Analysis:Ratios are more informative than raw numbers1. Ratios provide meaningful relationships between individual values inthe financial statements2. Ratios help investors evaluate management3. Enable comparison of a firm’s performance toThe aggregate economyIts industry or industriesIts major competitorsIts past performanceRatios and Financial AnalysisComparability among firms of different sizesProvides a profile of the firmCaution:Economic assumption of Linearity – ProportionalityNonlinearity can cause problems:Fixed costs, EOQ for inventoriesBenchmarks; Is high Current ratio good? For whom?Industry-wide norms.Accounting Methods; Timing & Window DressingLIMITATIONS1. No theory to define ‘good’2. Historical, not economic3. Most as of a single point in time4. Seasonal operations5. One-time effects6. Designed for manufacturersLiquidity Ratios: attempt to measure the ability to pay obligations such as current liabilities and the pool of assets available to cover the obligations. Liquidity is the ability of an asset to be converted to cash quickly at low cost. Converting an asset to cash occurs in one of two ways. Sell the asset, hoping it has reasonable liquidity, or in the case of a financial asset, like accounts receivable or Treasury bill, maturity brings cash. Working capital circulates from inventory to accounts receivable to cash, etc. Accounting value estimates of liquid assets are reasonable estimates of their value.Current assets (the pool of circulating cash assets available to be allocated to pay bills) minus current liabilities (the pool of obligations the business must pay in the near future) is an analytical amount called net working capital (NWC).NWC = current assets - current liabilitiesNWC/total asset ratio = net working capital / total assetsThe current ratio is the classic liquidity ratio, but is merely a variation of the idea above—what pool of circulating assets is available relative to the pool of current obligations:Current ratio = current assets / current liabilitiesQuick ratio =(cash + marketable securities + accounts receivable) /current liabilitiesCash ratio = (cash + marketable securities) / current liabilitiesCash flow from operation ratio = OCF / current liabilitiesLeverage ratios are two types: balance sheet ratios comparing leverage capital to total capital or total assets, and coverage ratios which measure the earnings or cash-flow times coverage of fixed cost obligations.Balance sheet ratiosLong-term debt ratio = long-term debt / ( long-term debt + equity)Debt-equity ratio = long-term debt/equityTotal debt ratio = total liabilities / total assetsA coverage ratio, such as the times interest earned ratio, measures an amount available relative to amount owed. How many times is the obligation covered?Times interest earned = EBIT / interest expense= (EAT+Tax+Interest Exp)/ interest expenseTimes Cash flow coverage =(OCF+Tax+Interest Exp)/ interest expenseTotal assets turnover = Sales / Total assetsAccounts Receivable turnover = Sales / AR[Days A/R outstanding = 365 / Accounts Receivable turnover]Inventory turnover = Sales / Average Inventory, orCOGS / Average Inventory[Inventory Conversion = 365 / Inventory turnover]Payable turnover (deferral) = Purchase (or COGS) / AP[Days A/P outstanding = 365 / Payable turnover]Note: Cash Cycle = Inventory Conversion + Days A/R outstanding –Days A/P outstandingProfitability Ratios: refers to some measure of profit relative to revenue or an amount invested.The net profit margin measures the proportion of sales revenue that is profit available for sources of funds (EBIT-tax).Gross profit margin = gross profit / salesOperating profit margin = EBIT / salesNet profit margin = net income / salesReturn on assets = (net income + interest )/ average total assetsReturn on equity = net income/ average equityPayout ratio = dividends / net earningsPlowback ratio = 1 - payout ratio= (earnings – dividends)/(net earnings) = (earnings retained in period)/( net earnings)Growth in equity = plowback ratio x ROEMarket Based Ratios•For pricing an IPO if business going public•P/E RatioWhat investors are willing to pay for a $ of earnings (Current/ Forecast)What creates a high P/E?•Market/BookUsually much different than 1.•Price/Cash FlowThe Du Pont System is a process of analyzing component ratios, (also called decomposition) of the ROA and ROE to explaintheir level or changesRatio Pr 1 Leverage Turnover Asset y ofitabilit Equity Debt ROA EquityTA TA Sales Sales NI EquityTA TA NI Equity NI ROE ⨯⨯=⎪⎪⎭⎫ ⎝⎛+⨯=⨯⨯=⨯==Industry analysis:Definition of an industry: the group of firms producing products that are close substitutes for each other.Forces driving industry competition: There are five forces in determining the competitive structure of an industry, they are: (1)Entry, (2)Threats of substitutions, (3)bargaining power of buyers, (4)Bargaining power of suppliers, and (5)rivalry among current competitors, and can be pictured as:Five forces model:Potential EntrantsThreats of new entrants(Suppliers) (Buyers )0 bargaining power Industry competitors bargaining powerRivalry among existing firmsThreats of substitutesSubstitutesThreats of entry: new entrants bring to an industry new capacity, the desire to gain market share, and often substantial resources. Price can bid down or incumbent’s costs inflated as a result, reducing profitability.Barriers to entry:A. Economics of scales deter entry by forcing the entrants to come in at alarge scale and risk strong reaction from existing firms or come in at a small scale and accept a cost disadvantage.B. Product differentiation: product differentiation means that establishedfirms have brand identification and customer loyalties. Differentiation creates a barrier to entry by forcing entrants to spend heavily toovercome existing customer loyalties.C. Capital requirement: the need to invest large financial resources inorder to compete creates a barrier to entry, particularly if the capital is required for risky or unrecoverable up-front advertising or R&D.Capital requirement maybe also needed for customer credit, inventory start-up cost, as well as production cost.D. Switching costs: A barrier to entry is created by the switching cost,that is, one-time cost facing the buyer of switching from one supplier’s product to another’s.E. Access to distribution channels: the more limited the wholesale orretail channels for a product are and the more existing competitors have these tied up, obviously the tougher entry into the industry.F. Cost disadvantages independent of scale: proprietary producttechnology, favorable access to raw materials, favorable locations,government subsidy, and learning or experience curve.G. Government policy:Expected retaliation: conditions that signal the strong likelihood of retaliation to entry and hence to deter it are the following:A. A history of vigorous retaliation to entrants.B. Established firms with substantial resources to fight back.C. Established firms with great commitments to the industryand highly illiquid assets employed in it.D. slow industry growth, which limits the ability of the industryto absorb a new firm without depressing the sales andfinancial performance of established firms.。

Exercise 7-3 (30 minutes) a. Cash Flows from Operations Computation: Net income ................................................................... $10,000 Add (deduct) items to convert to cash basis: Depreciation, depletion, and amortization ............ $8,000 Deferred income taxes ............................................ 400 Amortization of bond discount ............................... 50 Increase in accounts payable ................................. 1,200 Decrease in inventories .......................................... 850 10,500 $20,500 Undistributed earnings of unconsolidated subsidiaries and affiliates ...................................... (200) Amortization of premium on bonds payable ......... (60) Increase in accounts receivable ............................. (900) (1,160) Cash provided by operations .................................... $19,340

Chapter 1Page 81.Classify following items as either an expense (E),a revenue(R),an asset(A),or a liability( L);Cash, buildings, salaries of the sales force, $5 owed to a company for work performed, Mortgage to a bank, sales.Answer:Cash—A Buildings—A Salaries of the sales force—E$5 owed—L Mortgage to a bank—L Sales—R2. Classify each of the following as n operating (O), bank (I) , or financing (F) in a statement of cash flows; Wage paid to workers, Cash received form a bank in the form of a mortgage, cash dividends paid to a supplier of inventory, Cash paid to purchase a new machine.Answer:Wage paid—O Cash of mortgage-- F Cash dividends paid -- FCash paid to supplier of inventory—O Cash paid to purchase a machine—IPage111.List several economic decisions that rely on accountinginformation.Answer:·Whether to grant a loan·How much to pay for a share of common stock.·Whether to grant a rate increase to an electric utility·How much in damages the loser of a lawsuit must pay·How much of a bonus to pay a plant manager·Whether to enter a new market2. Why do financial statements have footnotes, and what kinds of information might you find in them?Answer:Financial statements have footnotes because financial disclosure is a complex business. The notes tell us some of the specifics about the company environment , what accounting methods the company has used, what the accounting numbers might be if alternative methods had been used, and some of the major contingencies that are not formally included in the statement proper.Page 201.Describe the process of setting accounting standards. What are the roles of all the parties you mention?Answer:The FASB, a private, not-for-profit organization ,sets GAAP in the U.S. It publicly declares an agenda, promulgates "ExposureDrafts" of proposed standards, holds open meetings, and invites input from interested parties. The FASB has been delegated this authority by the SEC, a government agency with legal authority to determine GAAP.2.Think of an example, like the executive compensation example in the chapter, where incentives might exist to bias accounting numbers one way or another.Answer:There are other examples, but here is one that is different. A taxpayer has incentives to bias reported income downward in order to minimize income tax payments. However, it is important to understand that tax accounting rules are different from GAAP, and this book is about GAAP. Chapter 14 covers GAAP for taxes in more detail.Other examples include:·An entrepreneur seeking a loan from a bank or funding from a venture capitalist might have incentives to bias accounting numbers to look favorable.·A firm that is subject to scrutiny for earning excess profits(e.g.,an oil company)might have incentives to bias accounting numbers to look less favorable.·A utility subject to rate regulation might have an incentive tobias accounting numbers to look less favorable in order to gain more generous increases in its rates. (At this writing, there is a rather severe controversy about whether electric utilities in California are genuinely in financial difficulty and should be allowed to continue to impose large rate increase.)Chapter 2Page 381 Define assets, liabilities, and equities.Gave an example of each.How are assets valued? How are liabilities valued? Answer:An asset is a probable future economic benefit obtained or controlled by an entity as a result of a past transaction. Cash marketable securities, accounts receivable, inventories, prepaid expenses, patents, copyrights, trademarks, and property, plant and equipment are all examples of assets. A liability isa probable future sacrifice of economic benefits arising frompresent obligations of an entity to transfer assets or provide services as a result of a past transaction or event. Accounts payable, accrued liabilities, unearned revenues, warranties, and bonds payable are all examples of liabilities.Accounting valuation of assets uses several different methods, includingmarket value, expected realizable value, lower of cost or market, present value of future cash flows, and historical cost. Accounting valuation of liabilities is the expected amount that will be paid, perhaps adjusted for the time value of money.2. Explain what is meant by the entity concept.Answer:The entity is the person or organization about which accounting's financial history is being written.3 .A company signs a ten-year employee contract with a vicepresident. The salary is $500000 per year, guaranteed. Is this contract an asset? W ould it appear on the balance sheet?Explain.Answer:The rights conveyed by the contrat may be an asset from an economic point of view, but they are not an asset under GAAP. The contract would not appear on the balance sheet as an asset, because GAAP does not record executory contracts, which are contracts that require future performance form both parties. That is ,GAAP views the contract as determining what services will be provided, no asset is recognized under GAAP.(Neither is a liability for payment recognized until services have beenperformed.)4 .A company purchased a parcel of land 10 years ago at a cost of $300000.The land has recently been appraised at $900000. At what value is the land carried in the balance sheet? How does the appraisal affect the carrying value in the balance sheet? Answer:The land is on the balance sheet at its historical cost of $300000.The carrying value of the land is unaffected by the appraisal.Page 421、Define debit and credit .What kind of balance ,debit or credit ,would you expect to find in the inventory T-account?In the Common Stock T-account?Answer:A debit is an entry on the left side of a T-account. A credit is an entry on the right side of a T-account. We would except to find a debit balance in Inventory, and credit balances in Bonds Payable and Common Stock. The reason is the convention that increases in assets are debits and increases in liabilities and equities are credits.2、If the trial balances, it means that you have analyzed all theeffects of transactions correctly. True or false?Explain. Answer:False. A balanced means that the trial balance is consistent, not necessarily correct. For example. If an arbitrary entry is made that debits Cash and credits Common Stock for an equal amount, the trial balance will balance but it will be wrong. An accounting can receipt of cash and the issuance of common stock, but it alone can not make cash or additional common shares.3﹑Suppose Web sell leases a portion of its space to another company. Web sell’s accounts are debited and credited to record this transaction?Answer:Web sell would debit Cash and a liability, Rent Received in Advance, for the prepayment.Chapter 3Page 571. Define revenue and expense. How does one decide to list an item as revenue in an income statement? What is matching? Answer:Revenues are increases in net assets resulting from operations over a period of time .Expense are decreases in net assets resulting from operations over a period of time .Revenue isrecognized the earnings process is substantially complete , a transaction2. Give an example not found in the text , of an expense that is paid for in cash in a prior accounting period .In a subsequent accounting period.Answer:There are many allowable responses . An example is a patent that is purchased and paid for in one year and used in next .3. Give an example, not found in the text , of a revenue that is received in cash in a prior accounting period . In a subsequent accounting period .Answer:An example is a house painting contractor that receives payment for one-third of the contract price before beginning the painting .4. Explain why it is right to think of an asset as a cost and an expense as an expired cost .Answer:An asset is a future benefit . And there is an opportunity cost associated with not selling it for cash or exchanging it to settleChapter 6Page 120:1.The following table lists the adjustments and has an X in thecolumn indicating the approach:2. We first take adjustment for prepaid insurance and insurance expense. It would be easy to think of this adjustment as focusing on how much of the insurance coverage remained, as opposed to how much was used. In fact, the same type of logic could be used---computing a monthly rate for the coverage and applying that to the months reminding, instead of the months used.Now take adjustment for depreciation expense and accumulated depreciation. Estimating the value of the equipment at year end might be easy, for example, if there is a market for used equipment, or very difficult, for example, if the equipment was specially designed for Websell. Once a value estimate for the equipment at year end is obtained, depreciation expense would be the change in value over the year.Page 1231.$5000×(1+0.06)^10=$5000×1.79085=$8954.242.$5000×(1+0.06/2)^(10×2)=$5000×(1+0.03)^20=$5000×1.80611=$9030.563. $1000×(1.05)^3+$1000×(1.05)^2+$1000×(1.05)^1=$3310.134. ($1000×0.05/5)^13+$1000×(1+0.05/5)^10+$1000×(1+0.05/5)^5=($1000×(1.01)^15)+($1000×(1.01)^10)+($1000×(1.01)^5) =$1160.97+$1104.62+$1051.01=$3316.6Page 1241.x×.(1.07)^3=$3000 x=$3000/(1.07)^3=$2448.892. Calculate the present value at 10% of $1300 received two years from now. If that is greater than $1000, you are better offwith the $1300 to be received in two years. If its present value is less that $1000, you better off with $1000 now. $1300/(1.10)^2=$1074.38Therefore, you are better off receiving $1300 two years from now.Another way to do this problem is to take the future value at 10% of $1000. At the end of two years, the $1000 would compound up to:$1000×(1.10)^2=$1210,Which is less than you would have at that point if you took the $1300.3.The most I would be willing to pay is the present value at 8% of the stream of $1000 payment:$1000/(1.08)^1+$1000/(1,08)^2+$1000/(1,08)^3=$925.926+857.339+793.832=$ 2577.1(rounded)Chapter 8Page 1681.Aging takes the balance in accounts receivable at the end of the year, and sorts it by how long ago the transaction occurred that gave rise to that receivable. Experience has shown that ―older‖ accounts have less likelihood of ever being collected.Percentages of likely uncollectibles for each category are applied to the totals in that category , and the results added to obtain an estimate of the allowance for uncollectibles required to value properly the estimated amount that will be collected from the accounts receivable. The bad debts expense then falls out as a ―plug‖ in the allowance for uncollectibles.The percentage-of-sales method just estimates bad debt expense as a percent of sales, and plug the balance in the allowance account.2. Cash (118)Accounts receivable (118)12/31/2003(to recognize collection of cash from companies owing service co. from 2002 sales)Allow ance for doubtful accounts (7)Accounts receivable (7)12/31/2003(to write off accounts we know will not be collected) Ac counts receivable (125)Sales reven ue (125)12/31/2003(to recognize revenue and to anticipate collection of the receivable)If we focus on recording the bad debts expense that is associated with billings for 2003, we would record.06×$125000=$7500 inbad debts expense.B ad debts expense………………………………………7.5 Allowan ce for doubtful accounts…………………………7.5 12/31/2003(to record bad debt expense in anticipation of not collecting 100% of receivables)Method one: focus on the percentage of sales expected not to be collected.Allowance for doubtful accounts(10.5 is the ―plug”,i.e., the number that drops out)Now we move to 2004, where events now proceed as expected . Collections are $117.5 thousand. Cash………………………………………………..117.5 Accounts receivable…………………………………117.512/31/2004(to recognize collection of cash form companies owing service co. from 2003 sales)Allowance for doubtful ac counts………………………7.5 Accounts receivable………………………………….7.512/31/2004(to write off accounts we know will not be collected)Accounts receivable (125)Sales revenue (125)12/31/2004(to recognize revenue and to anticipate collection of the receivable)If we focus on recording the bad debts expense that is associated with billings for 2004, we would record.06×$125000=$7500 in bad debts expense.Bad debts expense……………………………………7.5 Allowance for doubtful accounts…………………………7.5 12/31/2003(to record bad debt expense in anticipation of not collecting 100% of receivables)The allowance for doubtful accounts using the peentage-of-sales method looks like this:Method one: focus on the percentage of sales expected not to be collected.Allowance for doubtful accountsOnly the entries recording bad debt expense are different using the aging method. Instead of the above entries recording bad debt expense, we would have the following analysis: Each year, we would adjust the balance in the allowance for doubtful accounts so that the net receivable ends up at $117500. That is, we would solve $125000-X=$117500,and find that the ending balance in the allowance for doubtful accounts must be $7500.Analyzing the account, we would determine that at 12/31/2003 we must add $4500 to the allowance for doubtful accounts: Bad debts expense………………………………..4.5 Allowanc e for doubtful accounts…………………….4.512/31/2004(to record bad debt expense in anticipation of not collecting 100% of receivables)At 12/31/2004, we must add $7500 to the allowance for doubtful accounts:Bad debts expense………………………………..7.5 Allowan ce for doubtful accounts…………………….7.512/31/2004(to record bad debt expense in anticipation of not collecting 100% of receivables)Using aging, the allowance for doubtful accounts T-accountlooks like this:Method two: focus on the ending balance in the allowance for doubtful accounts.Allowance for doubtful accountsChapter 9Page 1831.LIFO is last-in first-out. It means that in computing ending inventoryand cost of goods sold, the cost of items sold is assigned in reverse chronological order of their purchase, beginning from the most regent items purchased in a period. FIFO is first-in, first-out .It means that in computing ending inventory and cost of goods sold, the cost of items sold is assigned in chronological order of their purchase, beginning from the goods on hand at the beginning of the period. Average cost means that in computing ending inventory and cost of goods sold, the average unit cost of the beginning inventory and items purchased in aperiod is used to determine the cost of goods sold and remaining inventory.2.Y es, it is still a positive net present value project. In fact, its netpresent value is higher than when the purchase was made at$1.05 per unit, since the cash outflow is reduced but the cash inflow remains the same. The cash outflow on 12/31/01 when purchases are at $0.95 per unit is $114.This means the net cash flow at 12/31/01 is ($4) instead of ($16),and the NPV for Widget Company is:NPV=-100-$4/1.1+$10/ (1.1^2) +$144/ (1.1^3) =$12.82First, we redo the case of FIFO. The inventory T-account is:Widget Co. Inventory Account under FIFO Flow AssumptionInventory (FIFO)Ending inventory values can be read from the above T-account. Netincomes are:Widget Incomes using FIFONow we redo the case of FIFO. First, the inventory T-account is: Widget Co. Inventory Account under FIFO Flow AssumptionInventory (FIFO)Ending inventory values can be read from the above T-account. Net incomes are:Page 186To calculate the market-to-book ratios and accounting returns on equity: Market-to-book Ratios under Average CostAccounting Rates of Return under Average CostCollecting the results for FIFO from the chapter and these results for average cost, we have:Market-to-book Ratios under V arious Cost Flow AssumptionAccounting Rates of Return under V arious Cost Flow AssumptionAs is apparent, the market-to-book ratios and accounting rates of return for average cost are between for LIFO and FIFO.2. Because it has more recent costs on the balance sheet in the inventory account, FIFO has market-to-book ratios closer to 1regardless of whether prices rise or fall.Chapter 10Page 1961. The total profit on the transaction is the sales price of $880.00 less the original cost of $734.03:Sales price of securities $880.00Less : original cost ($735.03)Profit on transaction $144.97The cash flows were: $735.03 out on January1, 2001, and $880.00 in on January 3, 2003.There were profit in 2001, 2002, and 2003.In 2001, there was a profit of $81.17.In 2003,there was a profit of $5.00.2. The unadjusted book value of the security on December 31,2002 was $793.83.If the market value of the security on that date was $790.00,an adjustment reducing its carrying value by $3.83 is required to write it down to its market value: Unrealized loss on market value securities-trading ……3.83 Marketable securities –trading ………… 3.83 If the security were sold for $810.00 on January 3, 2003, the entry would be:Cash ………………………………810.00Marketable securities –trading ………………790.00Gain on marketable securities-trading …………20.001/03/2003(To record the sale of the Marketable securities—trading )Page 1981. When a securities is classified as trading security, profits or losses show up on the income statement in every period from when the security is purchased until when it is sold. when a security is classified as available-for-sale ,profits or losses only show up on the income statement in the period in which the security is sold.2. the unadjusted book value of the security on December 31,2002 was $793.83.If the market value of the security on that date was $790.00,an adjustment reducing it’s carrying value by $3.83 is required to write it down to it’s market value. however unlike the trading security case ,the unrealized loss is an equity account ,not a temporary account:Unrealized loss on marketable securities-available-for-sale 3.38 Marketable securities –trading ………………3.83To record the sale of the security for $810.00 on January 3,2003: Cash ………810.00Unrealized gain on marketable securities-available-for-sale(58.80-3.83) ………54.97Marketable securities-trading …………790.00Realized gain on marketable securities-available-for-sale ……………74.9712/31/2002(To mark-to-market the Marketable securities—available-for-sale)Chapter 111.a. Under straight-line depreciation, the depreciation expense each year is$600-$100/5 years=$100 per year.b. Under double-declining balance depreciation, the depreciation expense each year is given in the following table:c. Under sum-of-year’-digits depreciation, the depreciation expense each year is given in the following table:Sum-of years’-digits depreciation2. Intangible assets are most often shown in one line that is cost net of amortization. Tangible assets are sometimes shown in three lines: cost , accumulated depreciation, and net .3. Economic depreciation is the change in the economic value of the asset. Economic depreciation can be appreciation when the asset increases in value. We seen this already withmarketable debt securities, which sometimes increase in value because of unpaid interest4.It is easy and fulfills the requirement of GAAP to provide depreciation using a systematic and rational method. No GAAP depreciation method likely correctly reflects economic depreciation anyway ,so a simple expedient may be good enough.1.Sraight-line depreciation is $100 per year ($300/3 years).Double-declining balance depreciation is given in the following table:2.For straight-line depreciation,the entry is the same each year: Depreciation expense (100)Accumulateddepreciation (100)For double-declining balance depreciation,the entries are: Year1Depr eciation expense (200)Accu mulated depreciation (200)Year2Depreciation expense………………………………66.67 Acc umulated depreciation………………………66.67 Year3.declining balance because depreciation expense under straight-line is only $100,while under double-declining balance depreciation expense is $200.4.If the company buys one asset every year and each asset lasts three years,then in year 4 it will have three assets.Under straight-line depreciation,each of those assets generates a depreciation expense of $100;therefore total depreciation expense would be 3*$100,or $300.Under double-declining balance depreciation,total depreciation expense depends on the age of each asset.The company would have one asset in its first year of life,one in itssecond year of life,and one in its third year.Therefore,total depreciation expense would be:$200+$66.67+$33.33=$300,the same as under straight-line.Both depreciation methods give the same total depreciation because:1.Both methods fully depreciate the assets over their lives.2.The cost of the assets has remained constant.3.The company is in a steady state in which the number ofnew assets purchased in a period equals the number ofold assets being retired in that period.。

Financial Statement AnalysisIntroductionFinancial statement analysis is a crucial tool for assessing the financial performance and stability of a company. By analyzing a company’s financial statements, investors and other stakeholders can gain insights into its profitability, liquidity, solvency, and overall financial health. This document provides an overview of financial statement analysis, including the different types of financial statements, key financial ratios used in analysis, and the importance of using a systematic approach for analyzing financial statements.Types of Financial StatementsFinancial statements are a collection of reports that provide a snapshot of a company’s financial position and performance over a specific period. The three main types of financial statements include:1. Balance SheetThe balance sheet is a statement that shows the financial position of a company at a given point in time. It provides information about a company’s assets, liabilities, and shareholders’ equity. The balance sheet is divided into two main se ctions: the left side shows the company’s assets, while the right side shows its liabilities and shareholders’ equity.2. Income StatementThe income statement, also known as the profit and loss statement, reports a company’s revenues, expenses, and net in come over a specific period. It provides insights into a company’s profitability and helps identify trends in its revenue and expenses. The income statement follows a simple equation: revenues minus expenses equal net income.3. Cash Flow StatementThe cash flow statement shows the inflows and outflows of cash in a company over a specified period. It provides information about a company’s operating, investing, and financing activities. The cash flow statement helps assess a company’s ability to generate cash and its liquidity.Key Financial RatiosFinancial ratios are used to analyze the relationships between different items in a company’s financial statements. They help evaluate a company’s financialperformance, efficiency, liquidity, and solvency. Some key financial ratios used in financial statement analysis include:1. Profitability RatiosProfitability ratios measure a company’s ability to generate profits. Common profitability ratios include gross profit margin, operating profit margin, and net profit margin.2. Liquidity RatiosLiquidity ratios assess a company’s ability to meet its short-term obligations. These ratios include the current ratio and quick ratio.3. Solvency RatiosSolvency ratios evaluate a company’s long-term financial stability and ability to meet its long-term obligations. Examples of solvency ratios include the debt-to-equity ratio and the interest coverage ratio.4. Efficiency RatiosEfficiency ratios measure a company’s ability to utilize its assets and resources effectively. Examples include the inventory turnover ratio and the accounts receivable turnover ratio.Systematic Approach for Financial Statement AnalysisTo conduct an effective financial statement analysis, it is important to follow a systematic approach. The key steps in this approach include:1. Gathering Financial StatementsCollect the company’s financial statements, including the balance sheet, income statement, and cash flow statement.2. Analyzing Financial RatiosCalculate the relevant financial ratios and analyze them to assess the company’s financial performance and condition.3. Comparing RatiosCompare the calculated financial ratios with industry averages or with the company’s historical performance to identify trends and benchmark the company’s performance.4. Conducting a Trend AnalysisAnalyze the company’s financial statements over multiple periods to identify any significant changes or trends in its financial performance.5. Making Informed DecisionsBased on the analysis of the financial statements and ratios, make informed decisions about the company’s financial health, investment potential, and future prospects.ConclusionFinancial statement analysis is an important tool for assessing a company’s financial performance and stability. By analyzing a comp any’s financial statements and calculating key financial ratios, investors and stakeholders can make informed decisions about the company’s financial health, stability, and investment potential. Following a systematic approach for financial statement analysis ensures a comprehensive evaluation and helps identify trends and benchmarks for comparison.。