ACCOUNTING exam 3

- 格式:docx

- 大小:87.03 KB

- 文档页数:17

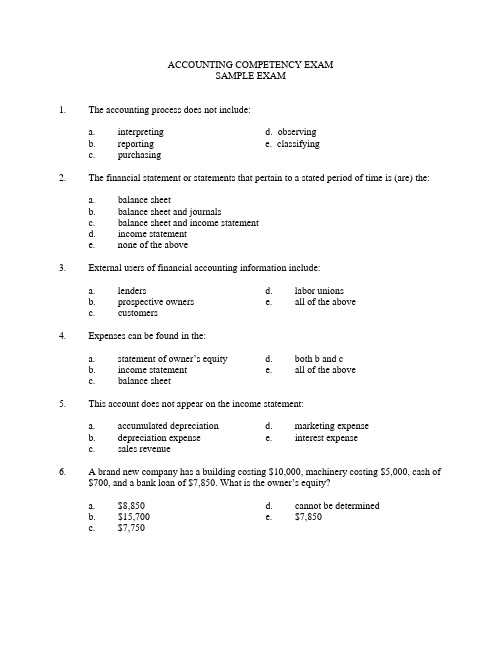

ACCOUNTING COMPETENCY EXAMSAMPLE EXAM1. The accounting process does not include:observingd.a. interpretingclassifyingb. reporting e.c. purchasing2. The financial statement or statements that pertain to a stated period of time is (are) the:sheeta. balanceb. balance sheet and journalsc. balance sheet and income statementstatementd. incomee. none of the above3. External users of financial accounting information include:unionsd. labora. lenderstheaboveofe. allb. prospectiveownersc. customers4. Expenses can be found in the:a. statement of owner’s equity d. both b and cb. income statement e. all of the abovesheetc. balance5. This account does not appear on the income statement:a. accumulated depreciation d. marketing expensee. interestexpenseexpenseb. depreciationrevenuec. sales6. A brand new company has a building costing $10,000, machinery costing $5,000, cash of$700, and a bank loan of $7,850. What is the owner’s equity?determinedbea. $8,850d. cannotb. $15,700 e. $7,850c. $7,7507. An example of an economic exchange includes:a. a business owner purchases inventory on creditb. a dry cleaning business cleans 3 dresses for a customerc. an insurance agent sells a whole life policyd. a contractor purchases a new truck for cashe. all of the above8. If a company has owner’s equity of $100,000,a. assets minus liabilities equal $100,000b. total assets must equal $100,000c. net income for the past year was $100,000d. a total of $100,000 was invested by the ownere. none of the above9. Providing services on account for $40,000 would:a. increase cash $40,000, decrease accounts receivable $40,000b. decrease accounts receivable $40,000, decrease owner’s equity $40,000c. increase accounts receivable $40,000, increase owner’s equity $40,000d. increase accounts receivable $40,000, decrease owner’s equity $40,000e. none of the aboveUse the following information to answer the next four questions.Joseph Forbes is the owner of his own business. On December 31, Forbes’ assets, liabilities, revenues and expenses were:Insurance Expenses $3,000 Accounts Payable $4,000Receivable5,000AccountsExpenses 900Miscellaneous14,000CashExpenses 2,500Rent11,000EquipmentExpense 19,000SalariesPayable4,600NotesSupplies1,200Expenseonhand 700Supplies45,000ServicesPerformed10. On December 31, total assets are equal to:a. $25,700 d. $30,700abovetheofb. $19,700 e. nonec. $22,10011. On December 31, net income is equal to:a. $18,400 d. $17,400abovetheofb. $45,000 e. none12. On December 31, if net income equals $15,000 and the ending owner’s equity is $20,000,and Forbes invested an additional $2,600 in his business, while withdrawing $6,000during the year, the beginning owner’s equity for this year was:d. $7,430a. $7,100ofabovethee. noneb. $7,400c. $8,40013. On December 31, current assets equal:a. $9,000b. $19,700c. $19,000d. $23,000e. none of the above14. New Font Software provided services for customers of $7,000. What is the entry if itbilled customers for the total amount.a. Debit accounts receivable $7,000; credit service revenue $7,000b. Debit notes receivable $7,000; credit service revenue $7,000c. Debit cash $7,000; credit service revenue $7,000d. Debit service revenue $3,000; credit accounts receivable $7,000e. none of the above15. Current Landscaping paid salaries of $560 in cash. The accounting e ntry is:a. Debit salaries expense $560; credit salaries payable $560b. Debit salaried expense $560; credit cash $560c. Debit cash $560; credit salaries expense $560d. Debit accounts payable $560; credit cash $560e. none of the above16. The Philip Company received a bill for natural gas. The bill is for $550 and is payable in30 days. The accounting entry is:a. Debit accounts receivable $550; credit service revenue $550b. Debit accounts payable $550; credit cash $550c. Debit natural gas expense $550; credit accounts payable $550d. Debit natural gas expense $550; credit cash $550e. none of the above17. The following includes the accounts of the Perry Company on December 31. What is thetotal trial balance?Accounts Receivable $1,000 Supplies Expense 250Cash 4,500 Drawing Account 30050ExpenseAdvertisingEquipment 4,000Salaries Expense 1,600 Accounts Payable 3,050Revenue Earned 2,800 Capital Account 6,050Rent Expense 200a. $11,900 d. $11,600abovetheofb. $12,000 e. nonec. $9,10018. Which of the following transactions require a compound journal entry?a. An owner invests personal cash on his/her businessb. Purchase of $ 100 of supplies; some cash and the rest on accountc. Purchase three kinds of supplies for cashd. Received cash from customers as payment for servicese. none of the above19. Cross-indexing:a. shows the analysis of each transaction.b. ties the journal and ledger together.c. supplies an explanation of each transactionexplanations from the accounts.d. removescomplicatede. c and d20. A truck was purchased on July 1 for $20,000. The estimated salvage value is $2,000. Theestimated useful life is 3 years. Using straight-line method of depreciation, the amount of depreciation in the adjusting entry at fiscal year-end on December 31 is:$555.56a. DepreciationExpense-Truck$555.56Depreciation-TruckAccumulatedb. Accumulated Depreciation- Truck $1,500$1,500TruckExpense-Depreciation$500Truckc. DepreciationExpense-$500TruckAccumulatedDepreciation-Truck$3,000Expense-d. Depreciation3,000TruckDepreciation-Accumulated21. A company paid in advance $4,800 for two years of prepaid insurance, which started onMay 1. The adjusting entry on fiscal year ending December 31 of that year is:a. Debit Insurance Expense; Credit Prepaid Insurance, $1,200b. Debit Insurance Expense; Credit Prepaid Insurance, $800c. Debit Prepaid Insurance; Credit Insurance Expense , $1,600d. Debit Insurance Expense; Credit Prepaid Insurance, $1,60022. On December 1 a company purchased supplies for $1,300. On December 31, an actualphysical inventory showed that $800 of supplies were on hand. The closing adjustingentry is:a. Debit Supplies Expense; Credit Supplies on Hand, $800b. Debit Supplies Expense; Credit Supplies on Hand, $1,300c. Debit Supplies Expense; Credit Supplies on Hand, $500d. Debit Supplies on Hand; Credit Cash, $50023. The first step in the accounting cycle is:a. Preparestatementsfinancialb. Post journal entries to the accounts in the ledgerc. Journalize transactions in the journald. Analyze transactions by examining source documents24. The Futures Company had revenues of $50,000 and expenses of $30,000 for the year. Mr.Futures withdrew $5,000 from the business during the year. The accounting entry to close the Income Summary Account is:$20,000a. IncomeSummarycapital$20,000FuturesMr.$20,000capitalFuturesb. Mr.$20,000IncomeSummary$5,000Summaryc. IncomeDrawing$5,000Mr.Futuresd. Mr. Futures, Drawing $5,0005,000$SummaryIncome25. An example of an adjusting entry for deferred items is:liabilitytoa. expenseasset c. revenuetotoexpensetob. assetexpense d. liability26. CMU Corp, has 4 500,000 of accounts receivable and has found an average 3 percent ofits credit sales are uncollectible. Suppose CMU Corp. determines that a customer owing$10,000 will never pay. What would be the journal entry?a. Uncollectible Accounts Expense $300Allowance for Uncollectible Accounts $300b. Allowance for Uncollectible Accounts 300Accounts Receivable 300c. Uncollectible Accounts Expense 10,000Allowance for Uncollectible Accounts 10,000d. Allowance for Uncollectible Accounts 10,000Accounts Receivable 10,00027. Rowe Inc. has a contract to construct a building for a price of $100. So far it has spent$60 of costs and it estimates an additional $20 will be needed to finish the building. Howmuch profit can be recognized using the percentage of completion method?a. 0 d. $40b. $15 e. none of the abovec. $2028. Warriner, Ltd. Sells widgets for $100, costing $70 with payments to be made in 10 equalinstallments of $10. If 3 payments have been received this year, using the installmentbasis of revenue recognition, what is the realized profit?a. o c. $9b. $3 d. $3029. Identify the advantage(s) of recognizing revenue at the time of sale.a. The actual transaction is an observable event.b. The likelihood of the sold item being returned for credit is remote.c. All of the aboved. None of the above30. Rowe, Inc. has a contract to construct a building for a price of $100. So far it has spent$60 of costs and it estimates an additional $20 will be needed to finish the building. Howmuch profit can be recognized using the completed contract method?a. 0 c. $20b. $15 d. $40Using the following 2 tables, answer the next four questions.Table of Inventory PurchasesDate Units Unit Cost Total costBeginning Inventory 10 $3 $30February 3 5 4 20April 10 15 5 75 June 12 12 7 84 August 20 20 8 160Total 62 369SalesDate Units Identified Units Price Total March 5 February 5 $6 $30May 2 April 10 6 60July 4 June 2 10 20September 1 June 8 10 8025 $19031. Determine the cost of ending inventory under specific identificationa. $190 c. $160b. $229 d. $36932. Determine the FIFO cost of ending inventorya. $179 c. $269b. $190 d. $36933. Determine the LIFO cost of ending inventorya. $185 c. $190b. $174 d. $36934. Determine the ending inventory under weighted average method.a. $190 c. $249b. $220 d. $36935. From merchandiser’s income statement you know that Sales revenue is $ 650,000 and thegross margin is 20%. What is the cost of Goods Sold?a. $650,000 c. $26,000b. $130,000 d. $520,00036. A manufacturer has beginning and ending finished goods inventory of $70, 000 and$90,000 respectively. Also, the cost of goods manufactured is $200,000. What is the Cost of Goods Sold?a. $20,000 c. $180,000b. $70,000 d. $270,000Using the following table answer the next four questions.Machine Purchase price $80,000Estimated Salvage Value $20,0005LifeyearsUsefulEstimatedEstimated Units of Production1 2,00037. What is the depreciation on the second year using the straight-line method?a. 0 c. $12,000d. $16,000b. $5,00038. What is the depreciation using the units of production method in the second year when4,000 units are made?a. $4,000c. $20,000b. $10,000 d. $27,00039. What is the depreciation in the second year using the sum-of-the-years’-digits method?a. $36,000 c. $16,000b. $48,000 d. $21,33340. What is the depreciation using the double declining balance method in the second year?a. $32,000 c. $19,200b. $11,520 d. $8,80041. When a plant asset is retired from productive service and has no salvage value, and thatoriginally cost $50,000 and had accumulated depreciation of $40,000, the correctaccounting treatment is:$50,000a. PlantAsset$40,000DepreciationAccumulatedLoss 10,00010,000b. Loss40,000DepreciationAccumulatedAsset 50,000Plantc. Loss on Plant Asset 10,000Asset 10,000Plantd. Nothing. The firm still has it.42. Brooks Company declared a cash dividend of $5,000 on June 1 and paid it on September1. What would be the journal entry or entries?$5,000a. DepletionExpenseDepletion $5,000AccumulatedExpense 5,000b. Depletion5,000CashExpense 5,000c. DepletionAsset 5,000DepletableDepletion 5,000d. Accumulated5,000DepletionExpense43. Smith. Corp. sold 100 shares of $50 par value common stock for $70 per share. Whatwould be the correct journal entry?$7,000a. CashStock $7,000Commonb. Cash 7,000Stock 5,000CommonCapital 2,000inPaidStock 7,000c. CommonCash 7,000d. Cash 7,000Stock 2,000CommonCapital 5,000Paidin44. Park Inc. earned EBIT $10,000,000 last year. If its tax rate was 40%, interest expense$2,000,000 and number of common shared 1,000,000 what would be the EPS?c. $4.80a. $8.00d. $4.00b. $6.0045. Brooks Co. declared and paid a cash dividend of $5,000. What would be the journalentries?a. Retained$5,000Earnings$5,000Cashb. Retained Earnings 5,000Payable 5,000Dividendsc. Dividends Payable 5,0005,000Cash5,000RetainedEarningsPayable 5,000Dividendsd. Retained Earnings 5,0005,000PayableDividendPayable5,000Dividends5,000Cash46. A corporation issues $50,000 of a 8% coupon, $1,000 par value bond. What would be thesemi-annual interest payment journal entry?Payable $4,000a. Bands$4,000Cashb. Bonds Interest Expense 4,000Cash 4,000Payable 2,000c. BondsCash 2,000d. Bond Interest expense 2,000Chas 2,00047. Given the following balance sheets of three firms, which appears to have greater financialleverage?Firm A Firm B Firm CDebt $2 $40 $15Equity $8 $60 $35Assets $10$100 $50TotalAa. FirmBb. Firmc. FirmCd. All the same48. Given the following income statements of three companies, which appears to havegreater financial leverage based upon the times interest earned ratio which is EBITdivided by interest?Firm A Firm B Firm CEBIT $50 $100 $75 Interest 10 15 5EBT 40 85 70Taxes 20 45 50EAT 20 40 20Aa. FirmBb. FirmCc. Firmd. All the same49. What is the maximum life that the intangible asset patent value can be amortized?a. The asset’s legal lifeb. The useful lifeyearsc. 17yearsd. 4050. A company is being sued for $100,000. What would be recorded on the balance sheet?a. Nothingb. $100,000 Set-aside Cashc. $100,000Liabilityd. $100,000 Contingent LiabilitySAMPLE EXAM KEY1. c, see p. R42. d, see p. R93. e, see pp.R5-R64. b, see p. R95. a, see p. R96. e, see p. R137. e, see p. R178. a, see pp.R18-R199. c, see p. R2210. d, see pp.R11, R2511. a, see pp.R9, R2512. c, see pp.R9-R1013. b, see p. R1114. a, see p. R3615. b, see p. R3716. c, see p. R3617. a, see p. R4318. b, see pp.R42-R4319. b, see p. R4120. d, see p. R5221. d, see p. R4922. c, see p. R5123. d, see p. R4624. a, see p. R5825. b, see p. R47 26. d, see p. R6527. b, see p. R6428. c, see p. R6329. a, see p. R6230. a, see p. R6431. b, see p. R7232. c, see p. R7333. b, see pp.R73-R7434. b, see p. R74-7535. d, see p. R6936. c, see p. R6937. c, see p. R8038. c, see p. R8039. c, see p. R8040. c, see pp.R80-R8141. b, see p. R8242. a, see p. R8143. b, see p. R9144. c, see p. R9345. d, see p. R9246. d, see p. R8847. b, see pp.R93-R9448. a, see pp.R93-R9449. c, see p. R7850. a, see p. R88。

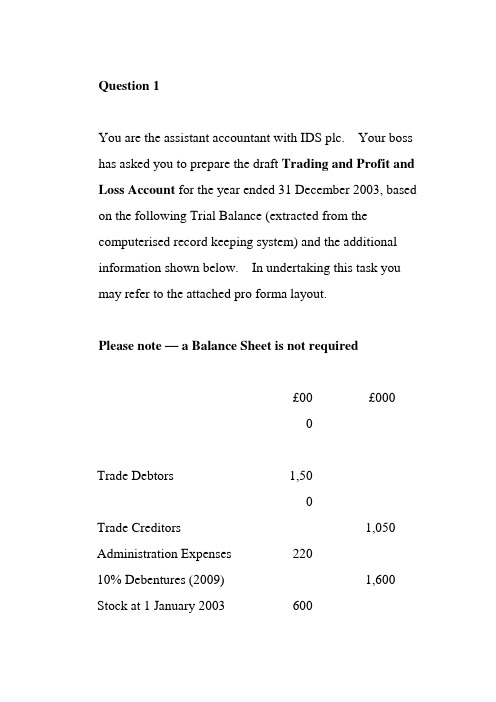

Question 1You are the assistant accountant with IDS plc. Your boss has asked you to prepare the draft Trading and Profit and Loss Account for the year ended 31 December 2003, based on the following Trial Balance (extracted from the computerised record keeping system) and the additional information shown below. In undertaking this task you may refer to the attached pro forma layout.Please note — a Balance Sheet is not required£00£000Trade Debtors 1,50Trade Creditors 1,050 Administration Expenses 22010% Debentures (2009) 1,600 Stock at 1 January 2003 600Distribution Costs 340Purchases 2,00Sales 3,550 Profit and Loss Account at 1January 20031,090Land and Buildings (NBV @ 31/12/02) 2,50Plant and Machinery (NBV@ 31/12/02)650Fixture and Fittings (NBV@ 31/12/02)150Motor Vehicles (NBV @31/12/02)150Discount Received 220 Ordinary Shares of £1 each 900 Preference Shares 5% 200 Bank 5008,618,610 Additional Information1Clerical and management staff were awarded a bonus amounting to £25,000 in mid December 2003. This bonus has not been paid yet and it should be classified as an administrative expense.2Distribution costs include £15,000 for a maintenance contract for motor vehicles which relates to the coming year.3Closing stock at 31 December 2003 was valued at £290,000.4It is estimated that corporation tax of £190,000 will be payable on the profits for the year.5Interest on the debentures for the full year should be provided.6The directors propose that a dividend should be paid on ordinary shares of 3p per share, and that the preference dividend be paid in full.7The directors propose to provide for the depreciation of fixed assets for the year as follows:Land and Buildings £50,000Plant and Machinery £40,000Fixtures and Fittings £30,000Motor Vehicles £60,000Question 2IDS plc, who are a major sports equipment manufacturer, have recently developed and tested a new trail running shoe.The management are now considering a limited launch of the new shoe over a six month period.As the project manager for the development of the new product you have compiled and collated the following sales and cost information for the review period.1Expected sales are:Month Number of shoesJanuary 200February 200March 260April 300May 350June 400Projected selling price £50All sales are expected to be on credit and customers are to pay in the month following the month of sale.2The number of shoes produced each month is based on expected sales. It is planned to keep stock levelsconstant at their current level throughout the trial period.3Each pair of shoes requires 0.2 kg of raw materials, which costs £10 per kg. All purchases of materials are on credit and suppliers are to be paid in the secondmonth following the month of purchase.4To produce one pair of shoes requires two hours of direct labour at £6 per hour. Wages are paid in themonth the shoes are produced.5Variable production overheads are to be charged at the rate of £2 per unit (pair of shoes) produced. These are to be paid in the month the units are produced.6Fixed monthly production overheads are as follows:£1,000Rent andratesInsurance £400£800Heat andlightDepreciation £200Other £250These are to be paid in the month the units are produced.7Other monthly fixed overheads are as follows:Manager’s salary£2,000Selling/distribution £1,000These are to be paid in the month the units are produced/sold.In order that senior management can assess the viability of the project and ascertain the cash flow implications, you are required to prepare and present the following information:1An income and expenditure budget in tabular format for the six month period.2A cash budget for the period (assume initial cash balance is zero).3Using the appropriate formula calculate and show the number of shoes that are required to be sold to break-even over the trial period.Question 1IDC plcTrading and Profit and Loss Account for year ending 31 December 2003£000 £000 Sales 3,550 Cost of goods soldOpening stock 600 Purchases 2,0002,600Closing stock 290 2,310 Gross Profit 1,240Other IncomeDiscount received 2201,460 ExpensesAdministration 245Distribution costs 325Interest payable 160 Depreciation 180 910550 Profit on ordinary activitiesbefore taxationCorporation tax 190360 Profit on ordinary activities aftertaxationAppropriationsPreference dividend 10Ordinary dividend 27 37 Profit for the year 323 Retained profit b/f 1,090 Retained profit c/f 1,413Question 1 (alternative/re-assessment)IDC plcBalance Sheet as at 31 December 2003£000 £000 £000 Fixed AssetsLand and Buildings 2,450 Plant and Machinery 610 Fixtures and Fittings 120 Motor Vehicles 903,270 Current AssetsStock 290Debtors 1,500Prepayments 15Bank 500 2,305Creditors: amounts falling due within 1 yearCreditors 1,050Accruals 25Corporation tax due 190Interest due 160Dividends due 37 1,462Net Current Assets 843 Total Assets less Current Liabilities 4,113Creditors: amounts falling due after more than 1yearDebentures 1,600 Net Assets 2,513Capital and ReservesOrdinary share capital 900 Preference share capital 200 Profit and Loss account 1,4132,513Question 21 Income and expenditure budget for six months2 Cash Budget for six months3 Break-even point:Selling Price/unit = £40Marginal Cost/unit = £16 (mats £2, labour £12, Var OHD £2)Contribution/unit = £40 − £16 = £24Break-even point = Fixed costs = £33,900 = 1,413 pairs of shoesCont/unit £24。

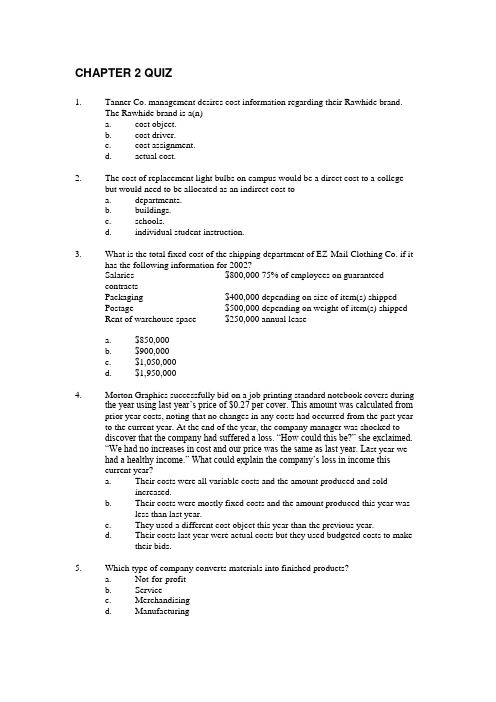

CHAPTER 2 QUIZ1.Tanner Co. management desires cost information regarding their Rawhide brand.The Rawhide brand is a(n)a.cost object.b.cost driver.c.cost assignment.d.actual cost.2.The cost of replacement light bulbs on campus would be a direct cost to a collegebut would need to be allocated as an indirect cost toa.departments.b.buildings.c.schools.d.individual student instruction.3.What is the total fixed cost of the shipping department of EZ-Mail Clothing Co. if ithas the following information for 2002?Salaries $800,000 75% of employees on guaranteedcontractsPackaging $400,000 depending on size of item(s) shippedPostage $500,000 depending on weight of item(s) shippedRent of warehouse space $250,000 annual leasea. $850,000b. $900,000c. $1,050,000d. $1,950,0004.Morton Graphics successfully bid on a job printing standard notebook covers duringthe year using last year’s price of $0.27 per cover. This amount was calculated from prior year costs, noting that no changes in any costs had occurred from the past year to the current year. At the end of the year, the company manager was shocked todiscover that the company had suffered a loss. ―How could this be?‖ she exclaimed.―We had no increases in cost and our price was the same as last year. La st year wehad a healthy income.‖ What could explain the company’s loss in income thiscurrent year?a.Their costs were all variable costs and the amount produced and soldincreased.b.Their costs were mostly fixed costs and the amount produced this year wasless than last year.c.They used a different cost object this year than the previous year.d.Their costs last year were actual costs but they used budgeted costs to maketheir bids.5.Which type of company converts materials into finished products?a.Not-for-profitb.Servicec.Merchandisingd.Manufacturing6.The three categories of inventories commonly found in many manufacturingcompanies are:a.Direct materials, direct labor, and indirect manufacturing costs.b.Purchased goods, period costs, and cost of goods sold.c.Direct materials, work in process, and finished goods.d.LIFO, FIFO, and weighted average.7.Inventoriable costs area.only purchased goods for resale.b. a category of costs used only for manufacturing companies.c.recorded as expenses when incurred and later reclassified as assets.d.recorded as assets when incurred.8.Period costs area.all costs in the income statement other than cost of goods sold.b.defined as manufacturing costs incurred this period on the schedule of costof goods manufactured.c.always recorded as assets when first incurred.d.those costs that benefit future periods.9.The cost of a product can be measured as any of the following except as costa.gathered from all areas of the value chain.b.identified as period cost.c.designated as manufacturing cost only.d.explicitly defined by contract.10.The primary focus of cost management is toa.help managers make different decisions.b.calculate product costs.c.aid managers in budgeting.d.distinguish between relevant and irrelevant information.CHAPTER 2 QUIZ SOLUTIONS1. a2. d3. a4. b5. d6. c7. d8. a9. b10. aQuiz Question Calculations3. Fixed costs = (800,000) 75% + 250,000 = $850,000CHAPTER 3 QUIZ1.Which of the following is not a factor in cost-volume-profit analysis?a.Units soldb.Selling pricec.Total variable costsd.Fixed costs of a product2.Which of the following is not an assumption of cost-volume-profit analysis?a.The time value of money is incorporated in the analysis.b.Costs can be classified into variable and fixed components.c.The behavior of revenues and expenses is accurately portrayed as linearover the relevant range.d.The number of output units is the only driver.3.Contribution margin is calculated asa.total revenue – total fixed costs.b.total revenue – total manufacturing costs (CGS).c.total revenue – total variable costs.d.operating income + total variable costs.Questions 4-6 are based on the following data.Tee Times, Inc. produces and sells the finest quality golf clubs in all of ClayCounty.The company expects the following revenues and costs in 2004 for its Elite Qualitygolf club sets:Revenues (400 sets sold @ $600 per set) $240,000Variable costs 160,000Fixed costs 50,0004.How many sets of clubs must be sold for Tee Times, Inc. to reach their breakeven point?a. 400b. 250c. 200d. 1505.How many sets of clubs must be sold to earn a target operating income of $90,000?a. 700b. 500c. 400d. 3006.What amount of sales must Tee Times, Inc. have to earn a target net income of $63,000if they have a tax rate of 30%?a. $489,000b. $429,000c. $420,000d. $300,0007.One way for managers to cope with uncertainty in profit planning is toe CVP analysis because it assumes certainty.b.recommend management hire a futurist whose work is to predict businesstrends.c.wait to see what does happen and prepare a report based on actual amounts.e sensitivity analysis to explore various what-if scenarios in order toanalyze changes in revenues or costs or quantities.8.The Beta Mu Omega Chi (BMOC) fraternity is looking to contract with a local band toperform at its annual mixer. If BMOC expects to sell 250 tickets to the mixer at $10each, which of the following arrangements with the band will be in the best interest ofthe fraternity?a.$2500 fixed feeb.$1000 fixed fee plus $5 per person attendingc.$10 per person attendingd.$25 per couple attendingUse the following information for questions 9 and 10.LSB Company has the following income statement:Revenues $100,000Variable Costs 40,000Contribution Margin 60,000Fixed Costs 30,000Operating Income 30,0009. What is LSB’s DOL?a. 3.33b. 2.00c.0.50d. 1.0010. If LSB’s sales increase by $20,000, what will be the company’s operating profit?a.$42,000b.$12,000c.$50,000d.$30,00011.Twin Products Company produces and sells two products. Product M sells for $12and has variable costs of $6. Product W sells for $15 and has variable costs of $10.Twin predicted sales of 25,000 units of M and 20,000 of W. Fixed costs are $60,000 per month. Assume that Twin achieved its sales goal of $600,000 for September,but fell short of its expected operating income of $190,000. Which of the following descriptions best describes the actual results reported of revenue of $600,000 andoperating income of less than $190,000?a.Twin sold 50,000 of M and no product W.b.Twin sold more of both products M and W than expected.c.Twin sold more of product W and less of product M than expected.d.Twin sold more of product M and less of product W than expected.12.In the situation of multiple cost drivers, CVP analysis cana.be modified so that the various simple formulas can be used by applyingthem separately to each cost driver.b.apply the same formulas as that used for a single-cost driver.c.be changed by incorporating all of the cost drivers into the breakevenformula to calculate the unique point of output at which the company wouldbreak even.d.be adapted by incorporating the cost drivers into the calculation of thevariable costs.13.Which of the following statements is true?a.Gross margin is another term for contribution margin.b.Contribution margin is acceptable for use in external financial statements.c.Contribution margin is used to help managers in decision making.d.Gross margin is revenues minus variable cost.CHAPTER 3 QUIZ SOLUTIONS1. c2. a3. c4. b5. a6. c7. d8. b9. b10. b11. c12. b13. cQuiz Question Calculations4. Variable costs per unit = $160,000/400 units sold = $400Contribution Margin = $600 – 400 = $200 per unitBreakeven point = $50,000/$200 = 250 units5. TOI = $50,000 + $90,000/$200 = 700 units6. TNI = $50,000 + $63,000/(1 – .30)/$200 = 700 units × $600 = $420,0001.Cost of option a: $2,500 Profit = 0Cost of option b: $1,000 + 5(250) = $2,250 Profit = $250Cost of option c: $10 (250) = $2,500 Profit = 0Cost of option d: $25 (125) = $3,125 Loss ($625)2.DOL = $60,000/$30,000 = 2.03.$20,000/ $100,000 = 20%20% × 2 = 40%40% × $30,000 = $12,000 increaseCHAPTER 4 QUIZ1. A cost-allocation base may be any of the following except aa.cost driver.b.cost pool.c.way to link indirect costs to a cost object.d.nonfinancial quantity.2. A company that manufactures dentures for use by local dentists would usea.process costing.b.personal costing.c.operations costing.d.job costing.3.The first step in the seven-step approach to job costing is toa.select the cost-allocation base to use in assigning indirect costs to the job.b.identify the direct costs of the job.c.identify the job that is the chosen cost object.d.identify the indirect-cost pools associated with the job.ing normal costing rather than actual costing requires that the allocating ofindirect manufacturing costs to work-in-process bea.done on a more timely basis, such as every two weeks rather than everymonth.b.journalized only at year end when adjusting entries are normally made.c.calculated by using the budgeted rate times actual quantity of allocationbase.d.calculated by using the budgeted rate times the budgeted quantity ofallocation base.5.Manufacturing Overhead Controla.represents actual overhead costs incurred.b.has a normal debit balance.c.is a control account with a subsidiary ledger detailing the components ofmanufacturing overhead.d.All of the above6.Which of the following accounts is not classified as an asset?a.Manufacturing Overhead Controlb.Materials Controlc.Work-in-Process Controld.Finished Goods Control7.The costs incurred on jobs that are currently in production but are not yet completewould appear in thea.Materials Control account.b.Finished Goods Control account.c.Manufacturing Overhead Control account.d.Work-in-Process Control account.8.The Precision Widget Company had the following balances in their accounts at theend of the accounting period:Work-in-Process $ 5,000Finished Goods 20,000Cost of Goods Sold 200,000If their manufacturing overhead was overallocated by $8,000 and Precision Widget adjusts their accounts using a proration based on total ending balances, the revisedending balance for Cost of Goods Sold would bea. $192,880.b. $200,00.c. $207,120.d. $208,000.9.Liberty Box Company calculated an indirect-cost rate of $12.50 per labor hour forfringe benefits for use in their normal costing system. At the end of the year, theactual cost of fringe benefits was $980,000. The total of labor hours worked for the year was the same amount as budgeted, 70,000 hours. If Job #640 required the useof 15 labor hours and the company used the adjusted allocation rate approach, bywhat amount would the cost of Job #640 change?a.$560.00b.$281.25c.$22.50d.$20.5010.If each professional in a service company is paid on an annual salary basis, whymight the firm want to use a predetermined or budgeted rate for direct orprofessional labor?a. A predetermined or budgeted rate is easier to justify to a client who mightquestion a billing rate.b.Professional staff persons do not keep accurate records of the jobs on whichthey work.c.Professional staff incurs more client costs, such as travel, lodging, and out-of-town meals, while working on a job.d.Year-end bonuses paid to the professional staff are difficult to trace toindividual jobs.CHAPTER 4 QUIZ SOLUTIONS1. b2. d3. c4. c5. d6. a7. d8. a9. c10. dQuiz Question CalculationsWork in Process $5,000 / 225,000 2.2% ⨯ $8,000 = 176Finished Goods $20,000 /225,000 8.9% ⨯ $8,000 = 712Cost of Goods Sold $200,000 / 225,000 88.9% ⨯ $8,000 = 7,120200,000 – 7,120 = $192,8809. 980.000/70,000 = $14.00 (actual rate)$14,000 – $12.50 = $1.50 excess of actual over budget1.50 ⨯ 15 hours – $22.50 additional costCHAPTER 5 QUIZ1.Production-cost cross-subsidization results froma.allocating indirect costs to multiple products.b.assigning traced costs to each product.c.assigning costs to different products using varied costing systems within thesame organization.d.assigning broadly averaged costs across multiple products withoutrecognizing amounts of resources used by which products.2.In refining a cost systema.total direct costs are unchanged because they can be traced in aneconomically feasible way to the product and traced costs are more accurate.b.the costs are grouped in homogeneous pools of the same or similar amounts.c.the criterion of cause and effect is used to relate indirect costs to a factorthat systematically links to a cost object.d.the organization looks for cost-allocation bases that will provide a uniformspreading of indirect costs to each product.Question 3 is based on the following data.The average cost data are for In-Sync Fixtures Company’s (a retailer) only twoproduct lines, Marblette and Italian Marble.Marblette Italian MarblePurchase volume 20,000 1,000Purchase cost per unit $50 $50Shipments received 12 12Hours used per shipment * 5 3 *These data were accumulated after a careful activity analysis.Currently, In-Sync Fixtures uses a traditional costing system with indirect costsallocated using purchased cost of goods as a basis. In-Sync Fixtures is consideringrefining the allocation of their receiving costs of $40,000. They realize that the ItalianMarble is heavier and requires more care than the Marblette but that the Marblettecomes in larger volume.3.Which statement can be made using the results of the activity analysis performed byIn-Sync Fixtures?a.The use of this refined activity-based costing system will increase theaccuracy of the resulting product costs because a more appropriate cost driverwill be used as the allocation base.b.The traditional allocation method currently being used is causing product-costcross-subsidization with the product line Marblette being undercosted.c.The cost allocated to the Italian Marble product line under the currenttraditional system is more than the activity-based costing allocated cost.d.The use of this refined activity-based costing system will increase theaccuracy of the resulting product costs because it probably will cost less totrace the costs to the product lines.4.Advertising of a specific product is an example ofa.unit-level costs.b.batch-level costs.c.product-sustaining costs.d.facility-sustaining costs.5.The allocation of indirect costs in an activity-based costing systema.may require other costs to be allocated to activities before the costs of theactivities can be allocated to the products.b.is simplified because more costs are identified as direct costs.c.requires the use of heterogeneous cost pools.d.is simplified because a limited number of activities are identified as costobjects.Information for questions 6 and 7 is given below.Jackson Enterprises manufactures two products—A basic gizmo and an advancedmodel gizmo. The company is using an activity-based costing system. They haveidentified three activities for allocation of indirect costs.Activity Cost Driver Cost-Allocation RateMaterials receiving Number of parts $2.00 per partProduction setup Number of setups $500.00 per setupQuality inspection Inspection time $90 per hourA production run for the basic model is 250 units, for the advanced model, 100 units.Each unit of product consumes the following activities:Number of Parts Number of Setups Inspection Time Basic Gizmo 10 50 10 minutesAdvanced Gizmo 15 25 20 minutesDirect costs for the two products are as follows:Direct Materials Direct LaborBasic Gizmo $50.00 $ 75.00Advanced Gizmo $95.00 $125.006.The amount of overhead allocated to one unit of the basic model would bea.$592.b.$37.c.$162.d.$65.7.The total cost of an advanced model would bea.$162.b.$65.c.$200.d.$265.8.Evaluating customer reaction of the trade-off of giving up some features of aproduct for a lower price would best fit which category of management decisionsunder activity-based management?a.Pricing and product-mix decisionsb. Cost reduction decisionsc. Design decisionsd. Discretionary decisions9.Which of the following statements is more representative of activity-based costingin comparison to a department-costing system?a.The use of multiple cost-allocation basesb.The use of indirect-cost rates for significant resource usec.The use of activities having a cause-and-effect relationshipd.The use of multiple cost pools10. A significant limitation of activity-based costing is thea.attention given to indirect cost allocation.b.many necessary calculations.c.operations staff’s attitude to ward the accounting staff.e it makes of technology.CHAPTER 5 QUIZ SOLUTIONS1. d2. c3. a4. c5. a6. b7. d8. c9. c10. bQuiz Question Calculations6. (2 ⨯10) + ($500/250) + ($90/60 ⨯ 10) = $377. $75 + $125 + ($2 ⨯ 15) + ($500/100) + ($90/60 ⨯ 20)CHAPTER 7 QUIZ1.[CMA Adapted] Flexible budgetsa.accommodate changes in the inflation rate.b.accommodate changes in activity levels.c.are used to evaluate capacity utilization.d.are static budgets that have been revised for changes in price(s).2.[CMA Adapted] The following information is available for the Gabriel ProductsCompany for the month of July:Static Budget Actual Units 5,000 5,100Sales revenue $60,000 $58,650Variable manufacturing costs $15,000 $16,320Fixed manufacturing costs $18,000 $17,000Variable marketing and administrative expense $10,000 $10,500Fixed marketing and administrative expense $12,000 $11,000The total sales-volume variance for the month of July would bea. $2,550 unfavorable.b. $1,350 unfavorable.c. $700 favorable.d. $100 favorable.3.[CMA Adapted] Bartholomew Corporation’s master budget calls for the production of6,000 units of product monthly. The master budget includes indirect labor of$396,000 annually; Bartholomew considers indirect labor to be a variable cost.During the month of September, 5,600 units of product were produced, and indirect labor costs of $30,970 were incurred. A performance report utilizing flexiblebudgeting would report a flexible budget variance for indirect labor ofa. $170 unfavorable.b. $170 favorable.c. $2,030 unfavorable.d. $2,030 favorable.4.Which of the following is not an advantage for using standard costs for varianceanalysis?a.Standards simplify product costing.b.Standards are developed using past costs and are available at a relativelylow cost.c.Standards are usually expressed on a per-unit basis.d.Standards can take into account expected changes planned to occur in thebudgeted period.rmation on Pruitt Company’s direct-material costs for the month of July 2005 wasas follows:Actual quantity purchased 30,000 unitsActual unit purchase price $2.75Materials purchase-price variance—unfavorable (based on purchases) $1,500Standard quantity allowed for actual production 24,000 unitsActual quantity used 22,000 units[CPA Adapted] For July 2005 there was a favorable direct-materials efficiencyvariance ofa. $7,950.b. $5,500.c. $5,400.d. $5,600.rmation for Garner Company’s direct-labor costs for the month of September 2005was as follows:Actual direct-labor hours 34,500 hoursStandard direct-labor hours 35,000 hoursTotal direct-labor payroll $241,500Direct-labor efficiency variance—favorable $ 3,200[CPA Adapted] What is Garner’s direct-labor price (or rate) variance?a. $21,000 favorableb. $21,000 unfavorablec. $17,250 unfavorabled. $20,700 unfavorable7.Performance evaluation using variance analysis should guard againsta.emphasis on a single performance measure.b.emphasis on total company objectives.c.basing effect of a manager’s action on total costs of the company as a whole.d.highlighting individual aspects of performance.8.The basic principles and concepts of variance analysis can be applied to activity-basedcostinga.by application as to the levels of cost hierarchy.b.through careful classification of costs as direct and indirect as applied to theproduct or job.c.with use of standard costing systems only.d.only through those activities related to individual units of product or service.9.Benchmarking isa.relatively easy to do with the amount of available financial informationabout companies.b.best done with the best in their field regardless of type of company.c.simply reporting the magnitude of differences in costs or revenues acrosscompanies.d.making comparisons to direct attention to why differences in costs existacross companies.CHAPTER 7 QUIZ SOLUTIONS1. b2. c3. a4. b5. c6. d7. a8. a9. dQuiz Question Calculations2. 5,100 – 5,000 = 100 units ⨯ $7* = $700FUnit CM = 60,000 – 15,000 –10,000/35,000 = $73. Actual DL $30,970Flexible budget 5,600 ⨯ $5.50 30,800Flexible budget variance 170 U5. Actual price 30,000 ⨯ 2.75 82,500Minus unfavorable price variance 1,500Materials at standard 81,00081,000/30,000 = $2.70 standard price per unitActual quantity 22,000 unitsStandard quantity 24,000 unitsEfficiency variance 2,000 ⨯ 1.70 = $5,400 F6. Actual direct labor cost $241,500Standard 34,500 ⨯ 6.40 $220,800Price variance 20.700 UStandard rate = 3,200/(35,000 – 34,500) = $6.40FLEXIBLE-BUDGET AND SALES-VOLUME VARIANCE ANALYSISActual Results: Flexible Budget: Static Budget:Actual Units Sold Actual Units Sold Budgeted Units SoldX Actual Sales Mix X Actual Sales Mix X Budgeted Sales MixX Actual CM/unit X Budgeted CM/unit X Budgeted CM/unit| - - - - Flexible budget variance - - - - | - - - - Sales-volume variance - - - - || - - - - - - - - - - - - - - - - - - - Static budget variance - - - - - -- - - - - - - - - - |SALES-MIX AND SALES-QUANTITY VARIANCE ANALYSISFlexible Budget: Static Budget:Actual Units Sold Actual Units Sold Budgeted Units SoldX Actual Sales Mix X Budgeted Sales Mix X Budgeted Sales MixX Budgeted CM/unit X Budgeted CM/unit X Budgeted CM/unit| - - - - - - Sales mix variance - - - - - | - - - - Sales-quantity variance - - - - || - - - - - - - - - - - - - - - - - - - Sales-volume variance - - - - - - - - - - - - - - - |MARKET-SHARE AND MARKET-SIZE VARIANCE ANALYSISFlexible Budget: Static Budget:Actual Market Size Actual Market Size Budgeted Market SizeX Actual Market Share X Budgeted Market Share X Budgeted Market Share X Budgeted CM/unit X Budgeted CM/unit X Budgeted CM/unit| - - - - - - Market share variance - - - - - | - - - - Market size variance - - - - || - - - - - - - - - - - - - - - - - - - Sales-quantity variance - - - - - - - - - - - - - - - |INPUT PRICE AND EFFICIENCY VARIANCESActual Costs: Flexible Budget: Actual Input Actual Input Budgeted Input (for actual output)X Actual Price X Budgeted Price X Budgeted Price| - - - - - - - Price variance - - - - - - - | - - - - - - - Efficiency variance - - - - - - - || - - - - - - - - - - - - - - - - - - - Flexible budget variance - - - - - -- - - - - - ----- - - - |INPUT YIELD AND MIX VARIANCESActual Input/Actual Mix : Flexible Budget:Actual Inputs Used Actual Input Used Budgeted Input (for actual output)X Actual Input Mix X Budgeted Input Mix X Budgeted Input MixX Budgeted Price X Budgeted Price X Budgeted Price| - - - - - - - - Mix variance - - - - - - - - | - - - - - - - - - Yield variance - - - - - - - || - - - - - - - - - - - - - - - - - - - Efficiency variance - - - - - - - - - - - - - - - - - - - - |。

国际会计考试题及答案英文International Accounting Exam Questions and AnswersQuestion 1: Define the term "Double Entry Accounting" and explain its significance in the accounting process.Answer 1: Double Entry Accounting is a system of recording financial transactions in which every entry to the debit side of an account must be balanced with an entry of equal value to the credit side of another account. It is significant because it ensures that all financial transactions are accurately recorded and that the accounting equation (Assets = Liabilities + Owner's Equity) remains balanced.Question 2: What is the purpose of the statement of cash flows in a set of financial statements?Answer 2: The statement of cash flows provides information about a company's cash receipts and cash payments during a particular period. It helps investors and creditors to understand the liquidity and solvency of the company, as well as its ability to generate cash and support its operations.Question 3: Explain the difference between "Historical Cost" and "Fair Value" in accounting.Answer 3: Historical Cost is the original purchase price of an asset or the original cost of a liability, while FairValue is the estimated amount for which an asset could be exchanged or a liability settled between knowledgeable,willing parties in an arm's length transaction. Historical Cost is used in the preparation of financial statements under the accrual basis of accounting, whereas Fair Value is often used for valuation purposes, particularly in the context of financial instruments.Question 4: What are the main components of the International Financial Reporting Standards (IFRS)?Answer 4: The main components of IFRS include the IFRS Standards, the International Accounting Standards (IAS), the Interpretations developed by the International Financial Reporting Interpretations Committee (IFRIC), and theStandards Advisory Council (SAC). These components provide a comprehensive set of rules and guidelines for the preparation and presentation of financial statements.Question 5: Describe the process of preparing a balance sheet.Answer 5: Preparing a balance sheet involves listing all of a company's assets, liabilities, and equity at a specific point in time. Assets are listed on the left side of the balance sheet and are categorized as current (short-term) or non-current (long-term). Liabilities are listed on the right side and are also categorized as current or non-current. Theequity section shows the owner's investment and retained earnings. The balance sheet must always balance, reflectingthe equation: Assets = Liabilities + Equity.Question 6: What is the role of an auditor in the financial reporting process?Answer 6: An auditor's role is to provide an independent assessment of a company's financial statements to ensure they are free from material misstatement and are presented fairly, in all material respects, in accordance with the applicable financial reporting framework, such as IFRS or Generally Accepted Accounting Principles (GAAP). The auditor's report provides assurance to stakeholders that the financial statements are reliable.Question 7: Explain the concept of "Conservatism" infinancial accounting.Answer 7: Conservatism is a principle in financial accounting that suggests that accountants should exercise caution when making estimates and judgments. It involves recognizing potential losses immediately but delaying the recognition of gains until they are realized. This principle helps to avoid overstatement of assets and income, thus providing a more prudent and cautious view of a company's financial position.Question 8: What is the difference between "Revenue Recognition" and "Matching Principle"?Answer 8: Revenue Recognition is the process of recognizing revenue in the accounting records when it is earned or realizable and has been measured reliably. The Matching Principle, on the other hand, is the accounting concept that requires expenses to be recognized in the same period as therevenues they helped to generate. This ensures that the financial statements reflect the actual performance of the company for a given period.Question 9: Describe the purpose of the "Going Concern" assumption in financial accounting.Answer 9: The Going Concern assumption is the basis for preparing financial statements under the accrual basis of accounting. It assumes that the business will continue to operate for the foreseeable future and that it is not in the process of liquidation or bankruptcy. This assumption allows accountants to spread the costs of assets over their useful lives and to recognize revenues and expenses when they are earned or incurred, rather than when cash is received or paid.Question 10: What is the "Materiality" concept in the context of financial statements?Answer 10: Materiality is a concept in financial accounting that refers to the significance of an item or event inrelation to the financial statements. Information is considered material if its omission or misstatement could influence the economic decisions of users taken on the basisof the financial statements. The assessment of materiality depends on the size and nature of the item, the nature of the financial statements, and the needs of the users.End of Exam。

F3 Financial Accounting –a guide to using theexaminer’s reportsF3 Financial Accounting EXAMINER’S REPORTSSTEP 1STEP 2STEP 3You can access the examiner’s reports for F3 by clicking on the image above. We suggest that at the very least you take a look at the last four – but of course you can look at as many as you like!GETTING STARTED EXAMINER’S REPORTS STEP 1STEP 2STEP 3Examiner’s reportsWhat are the examiner’s reports?The reports are produced every six months and provide an analysis of students’ performance – what they did well and what they didn’t do so well.They tell you which parts of the exam students found challenging and identify some of the key areas where students appear to lack knowledge as well as where they have demonstrated poor exam technique. The reports refer to specific questions in the exam, looking in detail at areas which caused difficulty. They also provide lots of useful tips.How will the reports help you when you are revising for your exam?If you review several of these reports you will notice that there are some key themes which the examining team comment on again and again. Typically students fail for the same reasons exam sitting after exam sitting.For you to succeed in your exam you need to try to avoid the pitfalls that have led to students failing F3.What are we going to do now?In this guide we are going to show you how to use the examiner’s reports as part of your revision phase.STEP 2STEP 3You may need to read through each of the reports a couple of times – but to get you started you might note down:Read questions carefullyYou will see this pops up again in the June 2016 report.Take noteStep 1 – Read the last four examiner’s reportsRead through each of the last four examiner’s reports for F3.✓As you go through them note down any themes you notice which come up more than once.✓Also try to note down any areas where the examining team is providing advice – for example, you may see in the December 2016 report there is some advice on reading each Section A question carefully.STEP 1EXAMINER’S REPORTS STEP 2STEP 3F3 Financial Accounting – a guide to using the examiner’s reports Now use this page to note down other themes or advice you notice which come up… include a reference to the report – so the exam sitting and the question number, the theme and then a bit of context (see example below)STEP 1GETTING STARTED EXAMINER’S REPORTS STEP 1STEP 2STEP 3Step 2 – Common themes identified by the examining team over the last four exam sittingsNow compare your list with our list over the following pages – how many did you identify?Spend some time looking through the reports again with the table over the following pages at your side, to make sure you understand where each of the points comes from. You will see we have also included an additional column ‘How to avoid the pitfalls’ and we will talk about this in Step 3.Note that some of the comments contained in the examiner’s reports, such as presenting answers as tidily as possible, apply only to the paper based examinations.Take noteF3 Financial Accounting – a guide to using the examiner’s reportsSTEP 1 STEP 2STEP 3STEP 1 STEP 2STEP 3STEP 1 STEP 2STEP 3STEP 1 STEP 2STEP 3STEP 1STEP 2 Step 3 – Question practice11STEP 3。

Session 1☆Types of business entityA business can be organized in one of the several ways:●Sole trader – a business owned and operated by one person.The simple form of business is the sole trader. This is owned and managed by one person, although there might be any number of employees. A sole trader is fully personally liable for any losses that the business might make.●Partnership – a business owned and operated by two or more people.A partnership is a business owned jointly by a number of partners. The partners are jointly and severely liable for any losses that the business might make.(Traditionally the big accounting firms have been partnerships, although some are converting their status to limited liability companies.)●Limited Liability Company– a business owned by many people and operated by many ( though not necessarily the same) people. Companies are owned by shareholders. Shareholders are also known as members. As a group, they elect the directors who run the business. Companies are always limited companies.In summary, types of business entity should be differentiated in Ownership; Operation right and Liability for the business to undertake.For all three types of entity, the money put up by the individual, the partners or the shareholders, is referred to as the business capital. In the case of a company, this capital is divided into shares.☆Business Transactions: Main types of business transactions for a business include:●Purchase of inventory for resale●Sal es of goods●Purchase of non-current assets●Payment of expenses●Introduction of new capital to the business●Withdrawal of funds from the business by the owner☆Cash and credit transactions:Cash transactions: the buyer pays for the item immediately or possibly in advance.Credit transactions: the buyer does not have to pay for the item on receipt, but is allowed some time ( a credit period) before having to make the payment.☆Definition of accountingRecording : transactions must be recorded as they occur in order to provide up-to-date information for management.Summarizing: the transactions for a period are summarized in order to provide information about the company to interested parties. ☆Types of accountingFinancial accounting vs management accountingFinancial accounting Cost and managementaccountingPurposeRecord financial transactionsInformation of cost of operationsLegal requirementLimited liability company, by law, prepare financial accountsNo legal requirement to prepare management accounts Main user ExternalInternal Time At the end of period regularlyInformationhistorichistoric and forecast☆Users of financial statementsAccounting reports users include:●Management : Need information about the co mpany’s financial situation as it is currently and it is expected to be in the future. This is to enable them to manage the business efficiently and to make effective decisions .●Investors: The providers of risk, capital and their advisers are concerned with the risk inherent in , and return provided by, their investments. They need information to helpthem determine whether they should buy, hold or sell.●Trade payables/ Suppliers: Suppliers and other trade payables. Suppliers and other trade payables are interested in information that enables them to determine whether amounts owing to them will be paid when due. Trade payables are likely to be interested in an enterprise over a shorter period than lenders unless they are dependent upon the continuance of an enterprise as a major customer.●Shareholders: Shareholders are also interested in market value of shares as well as information which enables them to assess the ability of the enterprise to pay dividends.●Lenders: Lenders are interested in information that enables them to determine whether their loans, and the interest attaching to them, will be paid when due.●Customers: Customers have an interest in information about the continuance of an enterprise, especially when they have a long term involvement with or are dependent on, the enterprise.●Government and their agencies:Governments are their agencies are interested in the allocation of resources and, therefore, the activities of enterprises. They also require information in order to regulate the activities of enterprises, determine taxation policies and as the basis for national income and similar statistics.●Employees: Employees and their representative groups are interested in information about the stability and profitability of their employers. They are also interested in information which enables them to assess the ability of the enterprise to prove remuneration, retirement benefits and employment opportunities.●General public:Enterprises affect members of the public in an variety of ways. For example, enterprises may make a substantial contribution to the local economy in many ways including the number of people they employ and their patronage of local suppliers. Financial statements may assist the public by providing information about the trends and recent developments in the prosperity of the enterprise and the range of its activities.☆The business entity conceptThe business entity concept●States that financial accounting information relates only to the activities of the business entity and not to the activities of its owner.●The business entity is treated as separate from its owners.Session 8 Irrecoverable debts and allowancesMain contents:1.Irrecoverable debts2.Allowance for receivables3.Accounting for irrecoverable debts and receivable allowances8.1 Irrecoverable debts●Trade receivables:A trade receivable is a customer who owes money to the business as a result of buying goods or service on credit.●Accruals concept:The accruals concept requires a sale to be included in the ledger accounts at the time that it is made.Credit sales are claimed when the sale is invoiced.The double entry at theinvoice date will be:Dr. Cr.Receivables xxSales xxWhen the customer eventually settles the invoice the double entry will be:Dr. Cr.Cash xxReceivables xxProblems: collecting the amounts owing from customersReasons: bankruptcy, fraud or disputes●Prudence concept:The prudence concept requires some adjustment to reflect the actual or potential loss arising from unpaid debts.●Irrecoverable debt:A debt which is considered to be uncollectible.- Highly unlikely that the amount owed will be received.- Written off by writing it out of the ledger accounts completely.●Accounting for irrecoverable debts- It is prudent to remove the irrecoverable debts from the accounts and to charge the amount as an expense for irrecoverable debts to the I.S.- The original sales remains in the accounts as this did actually take place.Dr.Irrecoverable debts expense xxCr.Receivables control account xxExample:Arctic Co.have total accounts receivable at the end of their accounting period of $45,000.Of these it is discovered that one, Mr.X who woes $790, has been declared bankruptcy, and another who gave his name as Mr.Jones has totally disappeared owing Arctic Co.$1,240.Write up the ledger accounts to reflect the writing off these debts as irrecoverable.Solution:Dr.Irrecoverable debts expense 2,030Cr.Receivables control account 2,030●Accounting for irrecoverable debts recoveredIrrecoverable debts are receivedWhen an irrecoverable debt is recovered, the accounting entry is:Dr.Cash xxCr.Irrecoverable debt expense xxExample:At 1 October 20x6 a business had total outstanding debts of $8,600.During the year to 30 September 20x7: Credit sales amounted to $44,000; Payments from various debtors amounted to $49,000; Two debts, for $180 and $420(both including sales tax)were declared irrecoverable.After the debts was written off, the payment is received before the end of the period, now what journal entry to prepare for the recovery of payment?Dr.Cash 600Cr.Irrecoverable debt expense 6008.2 An allowance for receivables:●Allowance for receivables is an estimate of the percentage of debts which are not expected to be paid.(a)When an allowance is first made, the amount of this initial allowance is charged as an expense in the income statement, for the period in which the allowance is created.(b)When an allowance already exists, but is subsequently increased in size, the amount of the increase in allowance is charged as an expense in the income statement, for the period in which the increased allowance is made.(c)When an allowance already exists, but is subsequently reduced in size, the amount of the decrease in allowance is credited back to the income statement, for the period in which the increased allowance is made.The value of trade receivable in the statement of financial position must be shown after deducting the allowance for receivables.Example:A business has trade receivables outstanding at 30 June 20x5 and decided to create 5% allowances for receivables.(a)In the income statement, the newly created allowance of $2,500 (5% x 50,000 = 2,500)will be shown as an expense.(b)In the statement of financial position, trade accounts receivables will be shownas: $Total receivables 50,000Less: allowance for receivables (2,500)47,5008.3 Accounting for irrecoverable debts and receivable allowances●Irrecoverable debts written off- When the irrecoverable debts are written off, the double entry might be:Dr.Irrecoverable debtsCr.Receivable control account- When an irrecoverable debt is subsequently received, the accounting entries are: Dr.CashCr.Irrecoverable debts●Allowance for receivables(a)Open up an allowance accountDr.Irrecoverable debts account (expense)Cr.Allowance for receivables(b)In subsequent years- calculate the new allowance required- compare it with the existing balance on the allowance account- calculate increase or decrease required(only a movement in the allowance is charged to the I.S.)(i)If a higher allowance is required:Dr.Irrecoverable debts expenseCr.Allowance for receivables(ii)If a lower allowance is required:Dr.Allowance for receivablesCr.Irrecoverable debts expenseExample:A has total receivables outstanding at 31 December 20x2 of $28,000.He believes that about 1% of these balances will not be collected and wishes to make an appropriate allowance.Before now, he has not made any allowance for receivables at all.On 31 December 20x3, his trade accounts receivable amount to $40,000.His experience during the year has convinced him that an allowance of 5% should be made.Required: What accounting entries should he make?Solution:At 31 December 20x2,Allowance required= 1% x 28,000 = $280Dr.Irrecoverable debts expense 280Cr.Allowance for receivables 280In SFPReceivables ledger balances 28,000Less: allowances for receivables 28027,720At 31 December 20x3Allowance required now( 5% x 40,000)2,000Existing allowance (280)Additional allowance required 1,720The double entry will be:Dr.Irrecoverable debts expense 1,720Cr.Allowance for receivables 1,720In SFPReceivables ledger balances 40,000Less: allowance for receivables (2,000)38,000Example 2:Irrecoverable debts are $5,000.Trade accounts receivable at the year end are $120,000.If an allowance for receivables of 5% is required, what are the irrecoverable debts in the income statement?A.$5,000B.$11,000C.$6,000D.$10,750Solution: B120,000 X 5% = 6,000$6000+ $5,000 = $11,000P.S.: The irrecoverable debt expense to be included in I/S should include:Irrecoverable debt written off xx+ Allowance ( movement )for receivables xx= Total irrecoverable debt expense charged to I/SSession 2☆Financial Statements include:- a statement of financial position at the end of the period- a statement of comprehensive income for the period- a statement of changes in equity for the period- statement of cash flows for the period- notes, comprising a summary of accounting policies and other explanatory notesThe statement of financial position:Statement of Financial Position: showing the financial position of a business at a point of time.The Vertical format of the SFP: (Statement of Financial Position as at 31 December 2007)●The top half of the balance sheet shows the assets of the business.●The bottom hal f of the balance sheet shows the capital and liabilities of the business.A Statement of financial position at the end of the period (Balance Sheet):W XangBalance Sheet as at December 31 20X6$ $ Non – current assetsMotor Van 2,400Current assetsInventory 2,390Trade receivables 1,840Cash at bank 1,704Cash in hand 565,990 Total assets 8,390$ $ Capital accountBalance at 1 January 20X6 4,200Add net profit for year 3,450Increase in capital 1,0008,650Less: Drawing for year (2,960)5,690Non – current liabilities 1,000Current liabilitiesPayable 1,700Total 8,390The horizontal format of the SFP: (Statement of Financial Position as at 31 December 2007)●The left half of the balance sheet shows the assets of the business.●The right half of the balance sheet shows the capital and liabilities of the business.W XangStatement of Financial Position as at 31 December 20x6$ $ $ $ Non-current assets Non-current liabilities1,000Motor van 2,400 Trade payable1,7002,400 Total liabilities2,700Capital accountCurrent assets Balance at 1 January 20X6 4,200Inventory 2,390 Add net profit for year 3,450Trade receivables 1,680 Increase in capital 1,000Cash at bank 1,704 8,650Cash in hand 56 Less: Drawing for year -2,960Total current assets5,990 5,690Total assets8,390 Total capital and liabilities8,390☆The accounting equationFinancial accounting is based upon a very simple idea:The amount of resources supplied by the owner is called capital. The actual resources that are then in the business are called assets. Usually, people other than the owner have supplied some, of the assets, for example, a supplier supplies stock of goods on credit. The business is said to owe a liability towards these suppliers. The following accounting equation always holds true:The accounting equation:ASSETS = PROPRITOR’S CAPITAL + LIABILITIES- Any point in time, the assets of the business will be equal to its liabilities plus the capital of the business;- Assets less liabilities equal the capital of the business, which is known as net assets.- Each and every transaction that the business makes or enters into has twoaspects to it and have a double effect on the business and the accountingequation. This is known as the duality concept.Duality concept:Each and every transaction that the business makes or enters into has two aspects to it and has a double effect on the business and the accounting equations. This is known as duality concept.Illustration:1). Carl sets up in business by opening a coffee shop –Carl’s Coffee. He puts $5,000 into a business bank account.The opening accounting equation is:Assets (Cash in bank)= Capital + Liabilities($5,000) = ($5,000) + ($0)2). Carl buys furniture (chairs and tables) for the shop for $1,500, paying the supplier out of the business bank account.The accounting equation after this transaction is:Assets Capital + Liabilties( Cash in bank $3,500) = ($5,000)($0)(Furniture $ 1,500)3). Now Carl spends a further $2,000 to buy coffee-making equipment and $800 on crockery and cutlery, paying cash out of the business bank account.The accounting equation after this transaction is:Assets Capital + Liabilties(Cash in Bank $700)= ($5,000)($0)(Equipment $2,000)(Fitting & Fixture $800)(Furniture $1,500)4). Carl persuades his bank to lend $1,000 to develop the business. The bank loan is accounted for as a liability of the business.The accounting equation is now as follows:Assets Capital + Liabilties(Cash in Bank $1,700) = ($5,000)($1,000)(Equipment $2,000)( Fitting & Fixture $800)(Furniture $ 1,500)5). Carl now buys coffee, tea, milk, sugar, biscuits and cakes for $700, and pays in cash from the business bank account.The accounting equation is now as follows:Assets Capital + Liabilties(Inventory $700) = ($5,000)($1,000)(Equipment $2,000)(Fitting & Fixture $800)(Furniture $1,500)(Cash in Bank $ 1,000)6). In his first day of trading, Carl uses up $650 of his inventory, and makes sales totaling $1,050. All his sales are in cash.The accounting equation at the end of the day is as follows:Assets Capital + Liabilities(Inventory $50) = (Beginning $5,000)($1,000)(Equipment $2,000)( Profit $400)(Fitting & Fixture $800)(Furniture $1,500)( Cash in bank $2,050)☆Classification of Assets and LiabilitiesAssets: An asset is something owned or controlled by the business that will result in future economic benefits to the business. ( an inflow of cash or other assets.)Such as:Current assets:are assets owned by the business with the intention of turning them into cash within one year (accounting period).This definition allows inventory or receivables to quality as current assets, even if they may not be realized into cash within 12 months.Non-current asset:is an asset held for and used in operation(rather than for selling to customer), with a view to earning income or making profits from its use, for over more than one year ( accounting period).Liability: is something owed by the business to someone else.Current liability: These include the debts of the business that are repayable within the next 12 months.Non-current liabilities: are liabilities that do not need to be settled for at least one year. (excluding the current portion of the debt)Capital:Capital is a type of liability. It represents the owner’s net investment in the business. Capital appears as a credit balance on the balance sheet.Assets –Liabilities = PROPRIETOR’S CAPITALNet Assets =( Total )Assets –(Total) LiabilitiesCapital (at SFP date) = Capital introduced + Profit – DrawingsDrawing: Drawings are any amounts taken out of the business by the owner for their own personal use. Drawings will reduce the capital balance reported on the balance sheet.Include:●Money taken out of the business●Goods taken for personal use●Personal expenses paid by the businessIncome statement☆Financial Statements include:- a statement of financial position at the end of the period- a statement of comprehensive income for the period- a statement of changes in equity for the period- statement of cash flows for the period- notes, comprising a summary of accounting policies and other explanatory notes The statement of financial position:Statement of Financial Position: showing the financial position of a business at a point of time.The Vertical format of the SFP: (Statement of Financial Position as at 31 December 2007)●The top half of the balance sheet shows the assets of the business.●The bottom half of the balance sheet shows the capital and liabilities of the business.A Statement of financial position at the end of the period (Balance Sheet):☆Income statement:Mr. W XangIncome statement for the year ended 31 December 20X6$ $Sales revenue33,700Opening inventory 3,200Purchases 24,49027,690Less: Closing inventory (2,390)Cost of sales (25,300)Gross profit8,400Less: Expenseswages 3,385rent 1,200Sundry expenses 365(4,950)Net profit3,450●Showing the financial performance of a business over a period of time.●Reports revenue and expenses for the period.●T he sales revenue shows the income from goods sold in the year●The cost of buying the goods sold must be deducted from the revenue●The current year’s sales will include goods bought in the previous year, so this opening inventory must be added to the current year’s purchases.●Some of this year’s purchases will be unsold at 31/12/20x6 and this closing inventory must be deducted from purchases to be set off against next year’s sales.●The first part gives gross profit. The second part gives net prof it.The I.S. prepared following the accruals concept.Accrual concept:●Income and expenses are recorded in the I.S. as they are earned / incurred regardless of whether cash has been received/ paid.(Sales revenue: income from goods sold in the year, regardless of whether those goods have been paid for.)☆Relationship between a statement of financial position and a statement of income●The balance sheets are not isolated statements, they are linked over time withthe income statement●As the business records a profit in the income statement, that profit is added tothe capital section of the balance sheet, along with any capital introduced. Cash taken out of the business by the proprietor, called drawings, is deducted.Illustration – the accounting equation:The transactions:Day 1 Avon commences business introduction $1,000 cash.Day 2 Buys a motor car for $400 cash.Day 3 Buys inventory for $200 cash.Day 4 Sells all the goods bought on Day 3 for $300 cash.Day 5 Buys inventory for $400 on credit.SFP at the end of each day’s transactions:Solution:Day 1 Assets (Cash $1,000) = Capital ($1,000) + Liabilities ($0)Day 2 Assets (Motor $400) = Capital ($1,000) + Liabilities ($0)(Cash $600)Day 3 Assets ( Inventory $200) = Capital($1,000) + Liabilities ($0)(Motor $400)(Cash $400)Day 4 Assets ( Motor$ 400) = Capital + Liabilities ($0)(Cash $700)(Beginning$1,000)(Profit $100)Day 5 Assets (Inventory $ 400) = Capital + Liabilities( Motor$ 400)(Beginning$1,000)($400)(Cash $700)(Profit $100)AvonStatement of Financial Position as at end of Day 5$ $ Non – current assetsMotor Van 400Current assetsInventory 400Cash in hand 7001,100 Total assets 1,500$ $ Capital accountBalance at Day 1 1,000Add net profit for the period 1001,100 Current liabilitiesPayable 400Total 1,500Example:Continuing from the illustration above, prepare the SFP at the end of each day after accounting for the transactions below:Day 6 Sells half of the goods bought on Day 5 on credit for $250.Day 7 Pays $200 to his supplier.Day 8 Receives $100 from a customer.Day 9 Proprietor draws $75 in cash.Day 10 Pays rent of $40 in cash.Day 11 Receives a loan of $600 repayable in two years.Day 12 Pays cash of $30 for insurance.Your starting point is the SFP at the end of Day 5, from the illustration above.Prepare: SFP at the end of Day 12I.S. for the first 12 days of trading.Solution:Day 6 Assets (Inventory $ 200) = Capital + Liabilities( Motor$ 400)(Beginning$1,000)($400)(Cash $700)(Profit $150)(A/Receivable$250)Day 7 Assets (Inventory $ 200) = Capital + Liabilities( Motor$ 400)(Beginning$1,000)($200)(Cash $500)(Profit $150)(A/Receivable$250)Day 8 Assets (Inventory $ 200) = Capital + Liabilities( Motor$ 400)(Beginning$1,000)($200)(Cash $600)(Profit $150)(A/Receivable$150)Day 9 Assets (Inventory $ 200) = Capital + Liabilities( Motor$ 400)(Beginning$1,000)($200)(Cash $525)(Profit $150)(A/Receivable$150)(Drawing $75)Day 10 Assets (Inventory $ 200) = Capital + Liabilities( Motor$ 400)(Beginning$1,000)($200)(Cash $485)(Profit $110)(A/Receivable$150)(Drawing $75)Day 11 Assets (Inventory $ 200) = Capital + Liabilities( Motor$ 400)(Beginning$1,000)($200)(Cash $1,085)(Profit $110)($600)(A/Receivable$150)(Drawing $75)Day 12 Assets (Inventory $ 200) = Capital + Liabilities( Motor$ 400)(Beginning$1,000)($200)(Cash $1,055)(Profit $80 )($600)(A/Receivable$150)(Drawing $75)AvonStatement of Financial Position as at end of Day 12$ $ Non – current assetsMotor Van 400 Current assetsInventory 200Trade receivables 150Cash in hand 1,0551,405 Total assets 1,805$ $ Capital accountBalance at Day 1 1,000Add net profit for the period 80Less: Drawing for year (75)1,005Non – current liabilities 600Current liabilitiesPayable 200Total 1,805AvonIncome statement for the period ended at Day 12$ $Sales revenue550Opening inventory 0Purchases 600Less: Closing inventory (200)Cost of sales (400)Gross profit150Less: Expensesrent 40insurance 30(70)Net profit80Session 3 Double entry bookkeeping☆The duality concept and double entry bookkeepingDuality concept: each and every transaction has a double effect on the business and the accounting equations.(A= C + L)Rules of double entry bookkeeping:● Each time a trans action is recorded, both effects must be taken into account.● These two effects are equal and opposite such that the accounting equation will always prove correct.Assets – Liabilities = Capital● Traditionally, one effect is referred to as the debi t side ( Dr.) and the other as the credit side of the entry (Cr.)☆Ledger accounts, debits and creditsLedger account:● transactions are recorded in the relevant ledger accounts. There is a ledgeraccount for each asset, liability, revenue and ex penses’ item, and for the owner’scapital.● Each account has two sides: the debit and credit sides.● The duality concept means that each transaction will affect two ledger accounts● One account will be debited and the other credited● Whether an entry is to debit or credit side of an account depend on the types of account and the transaction.☆IN ARRIVING AT RULE FOR DEBIT AND CREDIT, AN ASSUMPTION ISMADE THAT ASSETS ARE OF A DEBIT NATURE.☆Debit entries record Credit entries recordIncrease in Increase inExpense LiabilityAsset IncomeDrawings CapitalRules: treat the transactions as if all performed by cash.(Cash in--- Debit; Cash out --- Credit)Using T- accountT-accounts are frequently used to simplify the thought process behind recording complex transactions. Using T-accounts, the accountant or bookkeeper can analyze the effects to individual accounts and the impact the transactions have on account balances.Steps to record a transaction:1.Identify the two items that are affected.2.Consider whether they are being increased of decreased.3.Decide whether each account should be debited or credited.4.Check that a debit entry and a credit entry have been made and they are both for the same account.☆Recording cash transactionsCash transactions:Payment is made or received immediately.Cheque payments or receipts are classed as cash transactions.Double entry involves the bank ledger:A debit entry is where funds are receivedA credit entry is where funds are paid out.Example: Show the following transactions in ledger accounts:1.Kamran pays $80 for rent by cheque.2.Kamran sells goods for $230 cash which he banks.3.He then takes $70 out of the business for his personal living expenses.4.Kamran sells more goods for cash, receiving $3,400Solution:1.Dr. Rent expense 80Cr. Cash in bank 802.Dr. Cash in bank 230Cr. Sales 2303.Dr. Drawing 70Cr. Cash in bank 704.Dr. Cash in bank 3,400Cr. Sales 3,400。

会计英语期末试题及答案IntroductionWith the global economy becoming increasingly interconnected, proficiency in accounting English has become an essential skill for accountants and finance professionals. This article presents a comprehensive set of accounting English final exam questions and answers, enabling learners to test and enhance their knowledge in this field.Section 1: Vocabulary and Terminology1. Match the following accounting terms with their definitions:a) Accruals i) An estimate of what a company owes or is owedb) Depreciation ii) A record of all financial transactions in chronological orderc) General Ledger iii) The systematic allocation of the cost of an assetd) Accounts Payable iv) Expenses incurred but not yet paide) Trial Balance v) A summary of all accounts in a companyAnswer:a) Accruals iv) Expenses incurred but not yet paidb) Depreciation iii) The systematic allocation of the cost of an assetc) General Ledger ii) A record of all financial transactions in chronological orderd) Accounts Payable i) An estimate of what a company owes or is owede) Trial Balance v) A summary of all accounts in a companySection 2: Multiple Choice Questions1. Which of the following financial statements shows the financial position of a company at a specific point in time?a) Income Statementb) Balance Sheetc) Cash Flow StatementAnswer: b) Balance Sheet2. What is the purpose of a cash flow statement?a) To calculate net incomeb) To track the movement of cash in and out of a companyc) To analyze revenue and expenses over a period of timeAnswer: b) To track the movement of cash in and out of a companySection 3: Fill in the Blanks1. The ___________ equation states that Assets = Liabilities + Equity.Answer: Accounting2. _________ is a document used to request payment from a customer.Answer: InvoiceSection 4: Short Answer Questions1. What is the difference between financial accounting and managerial accounting?Answer: Financial accounting focuses on providing information to external stakeholders, such as investors and creditors, while managerial accounting is concerned with providing information to internal users, such as managers and decision-makers within a company.2. Explain the concept of double-entry bookkeeping.Answer: Double-entry bookkeeping is a system in which every financial transaction is recorded in at least two accounts: a debit and a credit. This system ensures that the accounting equation (Assets = Liabilities + Equity) remains in balance and provides a clear audit trail for each transaction.ConclusionMastering accounting English is crucial for professionals in the field of finance and accounting. By utilizing the provided set of accounting English final exam questions and answers, learners can enhance their understanding and proficiency in this specialized area, leading to improved job prospects and career growth.。