会计学-企业决策地基础 问题详解

- 格式:doc

- 大小:556.33 KB

- 文档页数:39

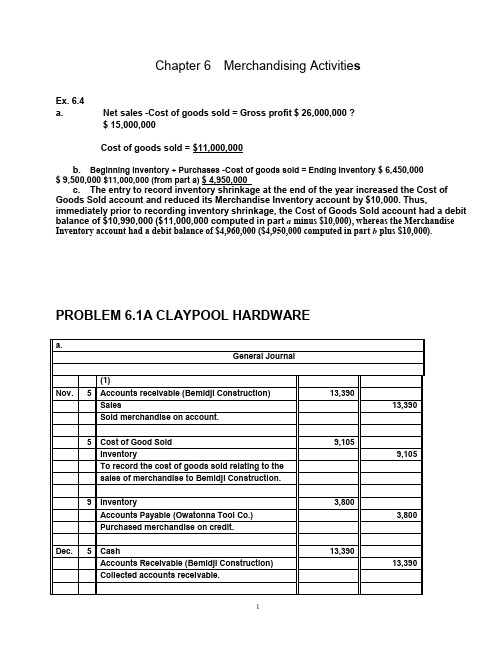

Chapter 6Merchandising Activitie sEx. 6.4a. Net sales -Cost of goods sold = Gross profit $ 26,000,000 ?$ 15,000,000Cost of goods sold = $11,000,000b. Beginning inventory + Purchases -Cost of goods sold = Ending Inventory $ 6,450,000$ 9,500,000 $11,000,000 (from part a) $ 4,950,000c. The entry to record inventory shrinkage at the end of the year increased the Cost of Goods Sold account and reduced its Merchandise Inventory account by $10,000. Thus, immediately prior to recording inventory shrinkage, the Cost of Goods Sold account had a debit balance of $10,990,000 ($11,000,000 computed in part a minus $10,000), whereas the Merchandise Inventory account had a debit balance of $4,960,000 ($4,950,000 computed in part b plus $10,000). PROBLEM 6.1A CLAYPOOL HARDWAREc. Claypool seems quite able to pass its extra transportation costs on to its customers and, in fact, enjoysa significant financial benefit from its remote location. The following data support these conclusions:Claypool Industry Hardware Average DifferenceAnnual sales …………………………….. $1,024,900 $1,000,000 $24,900Gross profit ……………………………… 327,968250,000 (1) 77,968Gross profit rate ………………………… 32% (2) 25% 7%(1) $1,000,000 sales 25% = $250,000(2) $327,968 gross profit $1,024,900 net sales = 32%Claypool earned a gross profit rate of 32%, which is significantly higher than the industry average.Claypool’s sales were above the industry average, and it e arned $77,968 more gross profit than the “average” store of its size. This higher gross profit was earned even though its cost of goods sold was $18,000 to $20,000 higher than the industry average because of the additional transportation charges.To have a higher-than-average cost of goods sold and still earn a much larger-thanaverage amount of gross profit, Claypool must be able to charge substantially higher sales prices than most hardware stores.Presumably, the company could not charge such prices in a highly competitive environment. Thus, the remote location appears to insulate it from competition and allow it to operate more profitably than hardware stores with nearby competitors.PROBLEM 6.5A SIOGO SHOES AND SOLE MATESc. Yes. Sole Mates should take advantage of 1/10, n/30 purchase discounts, even if it must borrow moneyfor a short period of time at an annual rate of 11%. By taking advantage of the discount, the company saves 1% by making payment 20 days early. At an interest rate of 11% per year, the bank charges only0.6% interest over a 20-day period (11% X 20/365 = 0.6%). Thus, the cost of passing up the discount isgreater than the cost of short-term borrowing.Chapter 7 Financial assetsChapter 8 Inventories and the cost of goods sold。

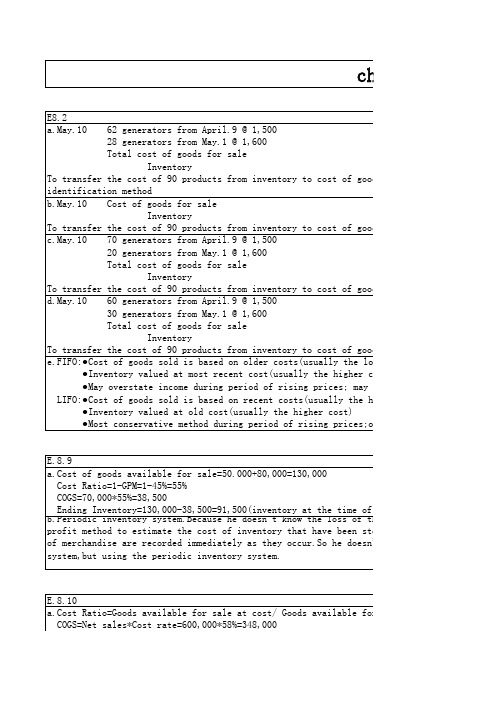

管理会计作业(chapter16-20)Chapter 16 P757 16.5AChapter 16 P761 16.4BChapter 17 P802 17.3Aa. Department One overhead application rate based onmachine-hours:ManufacturingOverhead = $420,000 = $35 per machine-hour Machine-Hours 12,000Department Two overhead application rate based on direct labor hours:ManufacturingOverhead = $337,500 = $22.50 per direct laborhourDirect Labor Hours 15,000Chapter 17 P805 17.8Ad. The Custom Cuts product line is very labor intensive in comparison to the Basic Chunksproduct line. Thus, the company’s current practice of using direct labor hours toallocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line isoverpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probably explains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e. The benefits the company would achieve by implementing an activity-based costing systeminclude: (1) a better identification of its operating inefficiencies, (2) a better understanding of its overhead cost structure, (3) a better understanding of the resource requirements of each product line, (4) the potential to increase the selling price of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrificesignificant market share, and (5) the ability to decrease the selling price of Custom Cuts without having to sacrifice product quality.Chapter 18 P835 18.1B. Ex.18.1a. job costing (each project of a construction company is unique)b . both job and process costing (institutional clients may represent unique jobs)c. job costing (each set of equipment is uniquely designed andmanufactured)d . process costing (the dog houses are uniformly manufactured in high volumes)e. process costing (the vitamins and supplements are uniformlymanufactured in high volumes)Chapter 18 P841 18.3Aa4,000 EU $61.50 = $246,000 b4,000 EU $13.50 = $54,000Chapter 18 P845 18.2Ba. (1) $49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2) $109 [($480,000 + $108,000 + $66,000) ÷ 6,000 units](3) $158 ($49 + $109)(4) $32 ($192,000 ÷ 6,000 units)(5) $18 ($108,000 ÷ 6,000 units)b. In evaluating the overall efficiency of the Engine Department, management wouldlook at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918 20.1Ad. No. With a unit sales price of $94, the break-even sales volume in units is 54,000 units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units) = $540,000$10= 54,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918 20.2AChapter 20 P920 20.6ASales volume required to maintain current operating income:Sales Volume =Fixed Costs + Target OperatingIncomeUnit Contribution Margin=$390,000 + $350,000= $20,000 units$37。

会计学-企业决策的基础答案管理会计作业(chapter16-20)Chapter 16 P757 16.5AChapter 16 P761 16.4BChapter 17 P802 17.3Aa. Department One overhead application rate based on machine-hours:Manufacturing Overhead= $420,000= $35 per machine-hourMachine-Hours 12,000Department Two overhead application rate based on direct labor hours:Manufacturing Overhead= $337,500= $22.50 per direct labor hourDirect Labor Hours 15,000Chapter 17 P805 17.8Ad. The Custom Cuts product line is very labor intensive in comparison to the BasicChunks product line. Thus, the company’s current practice of using direct laborhours to allocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line is overpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probablyexplains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e. The benefits the company would achieve by implementing an activity-based costingsystem include: (1) a better identification of its operating inefficiencies, (2) a betterunderstanding of its overhead cost structure, (3) a better understanding of theresource requirements of each product line, (4) the potential to increase the sellingprice of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrifice significant market share, and (5) the ability todecrease the selling price of Custom Cuts without having to sacrifice product quality.Chapter 18 P835 18.1a. job costing (each project of a construction company is unique)B. Ex.18.1b. both job and process costing (institutional clients may represent uniquejobs)c. job costing (each set of equipment is uniquely designed andmanufactured)d. process costing (the dog houses are uniformly manufactured in highvolumes)e. process costing (the vitamins and supplements are uniformlymanufactured in high volumes)Chapter 18 P841 18.3Ab4,000 EU @ $13.50 = $54,000Chapter 18 P845 18.2Ba. (1) $49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2) $109 [($480,000 + $108,000 + $66,000) ÷ 6,000 units](3) $158 ($49 + $109)(4) $32 ($192,000 ÷ 6,000 units)(5) $18 ($108,000 ÷ 6,000 units)b. In evaluating the overall efficiency of the Engine Department, management wouldlook at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918 20.1Ad. No. With a unit sales price of $94, the break-even sales volume in units is 54,000 units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units) = $540,000$10= 54,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918 20.2AChapter 20 P920 20.6ASales volume required to maintain current operating income:Sales Volume =Fixed Costs + Target Operating IncomeUnit Contribution Margin=$390,000 + $350,000= $20,000 units$37。

会计学企业决策的基础财务会计分册第17版下载提示:该文档是本店铺精心编制而成的,希望大家下载后,能够帮助大家解决实际问题。

文档下载后可定制修改,请根据实际需要进行调整和使用,谢谢!本店铺为大家提供各种类型的实用资料,如教育随笔、日记赏析、句子摘抄、古诗大全、经典美文、话题作文、工作总结、词语解析、文案摘录、其他资料等等,想了解不同资料格式和写法,敬请关注!Download tips: This document is carefully compiled by this editor. I hope that after you download it, it can help you solve practical problems. The document can be customized and modified after downloading, please adjust and use it according to actual needs, thank you! In addition, this shop provides you with various types of practical materials, such as educational essays, diary appreciation, sentence excerpts, ancient poems, classic articles, topic composition, work summary, word parsing, copy excerpts, other materials and so on, want to know different data formats and writing methods, please pay attention!企业决策在当前竞争激烈的市场环境中显得尤为重要。

会计学企业决策的基础第十二版教学设计课程概述本课程是为了帮助学生理解会计学与企业决策之间的关系,以及如何应用会计信息进行企业决策。

在本课程中,学生将掌握有关财务数据的基本知识和理解财务报表。

此外,学生将学习如何根据财务信息制定战略性的决策,以提高企业的绩效。

教学目标本课程旨在:•理解会计学在企业决策中的基本原则与概念;•掌握财务报表的分析方法,以及如何利用财务信息辅助企业决策;•掌握常用的投资评价方法,以及如何为企业提供有效的投资建议;•理解成本与管理会计的概念与应用,以帮助企业制定成本管理策略。

教学大纲第一章企业决策的会计基础•企业决策与会计学的关系•会计信息的特征与用户需求•会计信息系统的原理第二章财务报表分析•资产负债表的分析与应用•利润表的分析与应用•现金流量表的分析与应用第三章财务比率分析•财务比率的分类及意义•财务比率的计算与应用第四章投资评价•投资评价的基本概念•投资现值法、内部收益率法、静态投资回收期法的计算及应用•投资决策方法的比较及应用第五章成本管理•成本及其分类•传统成本计算方法、活动成本管理方法、生命周期成本管理方法的介绍及应用•管理会计的概念及应用教学方法本课程将采用多元教学法,包括授课、案例研究、小组讨论、课堂演示等多种形式。

学生需要在课堂上认真听讲,积极参与互动,完成个人或团队作业。

同时,建议学生在课后认真复习课程内容,进行模拟实践,并及时向教师反馈学习情况和问题。

评测方法本课程将采用闭卷考试的方式考核学生对课程知识的掌握程度,其中考试将包含选择题、问答题和分析题。

此外,学生还需完成个人或小组作业,并在答辩时向全班展示自己的成果。

教学资源本课程将提供以下教学资源:•《会计学企业决策的基础》第十二版教材•相关的案例材料和课件•其他相关网站和学术资源结语通过本课程的学习,学生将能够掌握会计学与企业决策之间的关系,理解如何应用财务信息进行企业决策,并且可以更好地为未来的职业生涯做好准备。

管理会计作业(chapter16-20)Chapter 16 P757 16.5AChapter 16 P761 16.4BChapter 17 P802 17.3Aa.Department One overhead application ratebased on machine-hours:Manufacturing Overhead$420,000=$35 per machine-hourMachine-Hours 12,00 0Department Two overhead application rate based on direct labor hours:Manufacturing Overhead$337,500=$22.50 per direct laborhourDirect Labor Hours 15,00 0Chapter 17 P805 17.8Ad .The Custom Cuts product line is very labor intensive in comparison to theBasic Chunks product line. Thus, the company’s current practice of using direct labor hours to allocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line is overpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probably explains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e .The benefits the company would achieve by implementing an activity-basedcosting system include: (1) a better identification of its operating inefficiencies, (2) a better understanding of its overhead cost structure, (3) a better understanding of the resource requirements of each product line, (4) the potential to increase the selling price of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrifice significant market share, and (5) the ability to decrease the selling price of Custom Cuts without having to sacrifice product quality.Chapter 18 P835 18.1B. Ex. 18.1a.job costing (each project of a construction company is unique)b.both job and process costing (institutional clients may represent unique jobs)c.job costing (each set of equipment is uniquely designed and manufactured)d.process costing (the dog houses are uniformly manufactured in high volumes)e.process costing (the vitamins and supplements are uniformly manufactured in high volumes)Chapter 18 P841 18.3AInputs:•Beginning WIP•StartedOutputs:•Units completed•Ending WIP•Beginning WIP•Units started•Units completed•Ending WIP•Cost of beginning WIP•Cost added during the period•Cost of goods transferredtransferred•Add ending WIP$246,000b4,000 EU @ $13.50 =$54,000Chapter 18 P845 18.2Ba .(1)$49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2)$109 [($480,000 + $108,000 + $66,000) ÷6,000 units] (3)$158 ($49 + $109)(4)$32 ($192,000 ÷ 6,000 units)(5)$18 ($108,000 ÷ 6,000 units)b .In evaluating the overall efficiency of the Engine Department, managementwould look at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918 20.1Ad .No. With a unit sales price of $94, the break-even sales volume in unitsis 54,000 units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units)$540,000$1054,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918 20.2AChapter 20 P920 20.6ASales volume required to maintain current operating income:Sales VolumeFixed Costs + TargetOperating IncomeUnit Contribution Margin$390,000 + $350,000= $20,000 units $37。

管理会计作业(chapter16-20)Chapter 16 P757 16.5A

Chapter 16 P761 16.4B

Chapter 17 P802 17.3A

a. Department One overhead application rate

based on machine-hours:

Manufacturing

Overhead =

$420,000

= $35 per machine-hour

Machine-Hours 12,000

Department Two overhead application rate based on direct labor hours:

Manufacturing

Overhead

= $337,500

=

$22.50 per direct labor

hour

Direct Labor

Hours 15,000

Chapter 17 P805 17.8A

d . Th

e Custom Cuts product line is very labor intensive in comparison to the Basic Chunks product line. Thus, the company’s current practice o

f usin

g direct labor hours to allocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to eac

h product, the Custom Cuts product line is overpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probably explains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.

e . The benefits the company would achieve by implementing an activity-based costing system include: (1) a better identification o

f its operatin

g inefficiencies, (2) a better understanding of its overhead cost structure, (3) a better understanding of the resource requirements of eac

h product line, (4) the potential to increase the selling price of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrifice significant market share, and (5) the ability to decrease the selling price of Custom Cuts without having to sacrifice product quality.

Chapter 18 P835 18.1

B. Ex.

18.1 a

.

job costing (each project of a construction company is unique)

b

.

both job and process costing (institutional clients may represent unique jobs)

c

.

job costing (each set of equipment is uniquely designed and manufactured)

d

.

process costing (the dog houses are uniformly

manufactured in high volumes)

e

.

process costing (the vitamins and supplements are

uniformly manufactured in high volumes)

Chapter 18 P841 18.3A

•Beginning WIP

•Started

•Units completed

•Ending WIP

•Beginning WIP

•Units started

•Units completed •Ending WIP

•Cost of beginning WIP

•Cost added during the period

•Cost of goods transferred

•Add ending WIP

a4,000 EU $61.50 =

$246,000

b4,000 EU $13.50 = $54,000

Chapter 18 P845 18.2B

a(1$49 [($192,000 + $48,000 + $54,000) ÷6,000 units]

. )

(2

)

$109 [($480,000 + $108,000 + $66,000) ÷6,000 units]

(3

)

$158 ($49 + $109)

(4

)

$32 ($192,000 ÷6,000 units)

(5

)

$18 ($108,000 ÷6,000 units)

b . In evaluating the overall efficiency of the Engine Department, management would look at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).

Chapter 20 P918 20.1A

d . No. With a unit sales pric

e o

f $94, the break-even sales volume in units is 54,000 units:

Unit contribution margin = $94 - $84 variable costs = $10

Break-even sales volume (in units) =

$540,000

$10

= 54,000 units

Unless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not

enable Thermal Tent to break even. Chapter 20 P918 20.2A

Chapter 20 P920 20.6A

Sales volume required to maintain current operating income:

Sales

Volume Fixed Costs + Target Operating

Income

Unit Contribution Margin

$390,000 + $350,000

= $20,000 units

$37。