Feenstra 高级国际贸易

- 格式:pdf

- 大小:94.41 KB

- 文档页数:19

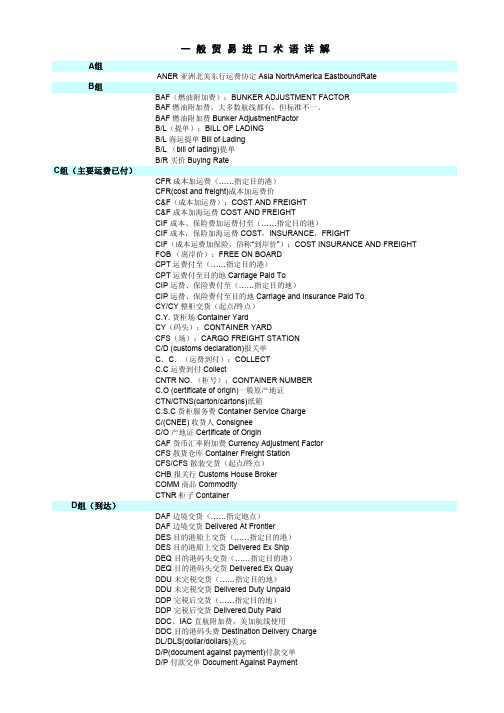

FOB,CIF,CFR的区别是什么啊?来麻烦各位了,请问FOB,CIF,CFR的区别是什么啊?我只知道他们包含的费用不同,但具体哪种好,怎样操作都很模糊,可以解释一下吗?谢谢三种贸易术语(FOB、CNF、CIF)简介和区别一、基本概念贸易术语(TRADE TERMS)又称贸易条件,价格术语(PRICE TERMS),它是一个简短的概念(SHORTHANDEXPRESSION),它确定了买卖双方相关费用、风险及责任的划分,以及买卖双方在交货和接货过程中应尽的义务,是贸易中价格的重要组成部分。

二、有关贸易术语的主要国际惯例主要惯例有三种A.1932年华沙牛津规则(WARSAW-OXFORD RULES 1932,简称W.O.RULES 1932)B.1941年美国对外贸易定义修订本(REVISED AMERICANFOREIGN TRADE DEFINITIONS 1941)C.国际商会制定的《2000年通则》英文为INCOTERMS2000,(ICC PUBLICATION NO.560)国际商会简称ICC是INTERNATIONAL CHAMBER OF COMMERCE三个单词第一个字母大写.INCOTERMS来源于INTERNATIONAL COMMERICAL TERMS三个单词合并而成。

三、当前国际贸易中广泛采用的贸易术语惯例① 是国际商会制定的《INCOTERMS 1990》或《INCOTERMS2000》② 国际商会于1919年成立,会员分布在140多个国家和地区,是全球具有重要影响的世界性民间商业组织,它是联合国的一个高级咨询机构,设立的目的是在经济和法律领域里,以有效的行动促进国际贸易和投资的发展。

③ 中国于1994年11月获得国际商会成员国地位。

④ 《INCOTERMS 1990/2000在世界上已得到广泛的承认,广泛运用于国际贸易合同及L/C中。

四、 FOB 贸易术语1、定义:FOB是FREE ON BOARD三个单词第一个字母的大写,中文意思为装运港船上交货,指定具体装运港名。

(1)FCA (Free Carrier) 货交承运人(2)FAS (Free Alongside Ship) 装运港船边交货(3)FOB (Free on Board) 装运港船上交货(4)CFR (Cost and Freight) 成本加运费(5)CIF (Cost,Insurance and Freight) 成本、保险费加运费(6)CPT (Carriage Paid To) 运费付至目的地(7)CIP (Carriage and Insurance Paid To) 运费、保险费付至目的地(8)DAF (Delivered At Frontier) 边境交货(9)DES (Delivered Ex Ship) 目的港船上交货(10)DEQ (Delivered Ex Quay) 目的港码头交货(11)DDU (Delivered Duty Unpaid) 未完税交货(12)DDP (Delivered Duty Paid) 完税后交货主要船务术语简写:(1)ORC (Origen Recevie Charges) 本地收货费用(广东省收取)(2)THC (Terminal Handling Charges) 码头操作费(香港收取)(3)BAF (Bunker Adjustment Factor) 燃油附加费(4)CAF (Currency Adjustment Factor) 货币贬值附加费(5)YAS (Yard Surcharges)码头附加费(6)EPS (Equipment Position Surcharges) 设备位置附加费(7)DDC (Destination Delivery Charges) 目的港交货费(8)PSS (Peak Season Sucharges) 旺季附加费(9)PCS (Port Congestion Surcharge) 港口拥挤附加费(10)DOC (DOcument charges) 文件费(11)O/F (Ocean Freight) 海运费(12)B/L (Bill of Lading) 海运提单(13)MB/L(Master Bill of Lading) 船东单(14)MTD (Multimodal Transport Document) 多式联运单据(15)L/C (Letter of Credit) 信用证(16)C/O (Certificate of Origin) 产地证(17)S/C (Sales Confirmation)销售确认书(Sales Contract) 销售合同(18)S/O (Shipping Order)装货指示书(19)W/T (Weight Ton)重量吨(即货物收费以重量计费)(20)M/T (Measurement Ton)尺码吨(即货物收费以尺码计费)(21)W/M(Weight or Measurement ton)即以重量吨或者尺码吨中从高收费(22)CY (Container Yard) 集装箱(货柜)堆场(23)FCL (Full Container Load) 整箱货(24)LCL (Less than Container Load) 拼箱货(散货)(25)CFS (Container Freight Station) 集装箱货运站(26)TEU (Twenty-feet Equivalent Units) 20英尺换算单位(用来计算货柜量的多少)(27)A/W (All Water)全水路(主要指由美国西岸中转至东岸或内陆点的货物的运输方式)(28)MLB(Mini Land Bridge) 迷你大陆桥(主要指由美国西岸中转至东岸或内陆点的货物的运输方式)(29)NVOCC(Non-Vessel Operating Common Carrier) 无船承运人出口国交货的贸易术语三组E 组:E.W.X.,工厂交货。

研究生推荐书目1、《国际经济学》[美]保罗·克鲁格曼,中国人民大学出版社。

2、《国际经济学》Dominink Salvatore著,清华大学出版社。

3、《战略性贸易政策与信国际经济学》,国际经济学译丛,中国人民大学出版社,保罗·克鲁格曼主编4、《流行的国际主义》国际经济学译丛,保罗·克鲁格曼著。

中国人民大学出版社。

5、《克鲁格曼国际贸易新理论》,中国社会科学出版社。

6、《汇率的不稳定性》,国际经济学译丛,保罗·克鲁格曼,中国人民大学出版社。

7、《地理和贸易》,国际经济学译丛,保罗·克鲁格曼,中国人民大学出版社。

8、《抉择——关于自由贸易与贸易保护主义的寓言》,国际经济学译丛,罗萨·罗伯茨,中国人民大学出版社,2001年版。

9、《萧条经济学的回归》,保罗·克鲁格曼,中国人民大学出版社。

10、《市场结构和对外贸易政策——报酬递增、不完全竞争和国际贸易》,保罗·克鲁格曼,上海三联出版社。

11、《新兴古典经济学和超边际分析》,杨小凯著,经济学前沿系列,中国人民大学出版社。

12、《泡沫经济与金融危机》,徐滇庆著,经济学前沿系列,中国人民大学出版社。

13、《公共选择理论——政治的经济学》,经济学前沿系列,中国人民大学出版社。

14、《市场经济前沿问题——现代经济运行方式》,魏杰,中国发展出版社。

15、《企业前沿问题——现代企业管理帆方案》,魏杰,中国发展出版社。

16、《企业制度安排》,魏杰,中国发展出版社。

17、《企业文化塑造》,魏杰,中国发展出版社。

18、《通往奴役之路》,哈耶克,西方现代思想丛书,中国社会科学出版社,1997年。

19、《西方经济学术的演变及其影响》,胡代光主编,北京大学出版社。

20、《人民币汇率研究——兼谈国际金融危机与涉外经济》,杨帆著,首都经济贸易大学出版社。

21、《经济解释》,张五常著,商务印书馆。

22、《市场经济——大师们的思考》,[美]詹姆斯·L·多蒂,江苏人民出版社。

国贸专业术语1. “FOB(Free on Board),哎呀,这就好比你去市场买东西,卖家把货物交到船上那一刻,责任就转移给你啦!比如说,你进口一批货物,FOB 条件下,货物装上船后,之后的风险就都是你的咯!”2. “CIF(Cost, Insurance and Freight),嘿,这不就像你在网上买个贵重物品,卖家不仅给你发货,还帮你买好保险!就像出口货物用 CIF,卖方要负责运费和保险费呢!”3. “L/C(Letter of Credit),哇塞,这简直就是商业交易中的一把安全锁啊!比如你和国外客户做生意,客户开个信用证,那不就等于给你吃了颗定心丸嘛,不用担心收不到钱啦!”4. “EXW(Ex Works),这就好像你去工厂直接提货,其他啥都不管,多简单直接呀!就像人家说的,EXW 条件下,买方承担的责任可大啦!”5. “DDP(Delivered Duty Paid),哎呀呀,这就跟快递员把包裹送到你家门口,所有费用和责任都搞定了一样!要是做 DDP 贸易,卖方可得操不少心呢!”6. “T/T(Telegraphic Transfer),嘿,这不就是电汇嘛,就像你给朋友转账一样迅速!在国际贸易里,T/T 也是常用的付款方式哟!”7. “DP(Documents against Payment),这可以想象成一手交钱一手交货嘛!拿着单据去收款,多靠谱呀!比如做 DP 结算,心里会踏实不少呢!”8. “DA(Documents against Acceptance),哇哦,这就像先答应后付款,给对方一个缓冲期呢!但也得小心风险呀!”9. “ETA(Estimated Time of Arrival),哈哈,这就是预计到达时间呀,就像你等快递,知道个大概啥时候能到,心里有个数!”10. “ETD(Estimated Time of Departure),这不就是预计出发时间嘛,跟你出门旅行知道啥时候出发一样重要呢!知道了 ETD,好安排后续的事情呀!”我的观点结论就是:这些国贸专业术语就像是国际贸易世界里的密码和工具,理解并运用好它们,能让贸易往来更顺畅、更安全!。

国际贸易专业术语解释1. “FOB(Free on Board),就是船上交货呀!比如说,你要出口一批货物,在货物装上船那一刻,责任就从你转移到买家啦!这就好像接力比赛,你把接力棒交到对方手里,后面的路就靠他们啦!”2. “CIF(Cost, Insurance and Freight),成本、保险加运费哟!好比你是卖家,不仅要负责货物的成本,还要买好保险,把货物安全送到目的地,就像是你给货物买了张一路平安的票呢!比如你卖东西给国外客户,用CIF 术语,你就得把这些都安排好呀!”3. “EXW(Ex Works),工厂交货呀!这就相当于你在自己工厂门口就把货物交给买家啦,之后的事情都由他们搞定,是不是很简单直接?就像你把做好的蛋糕放在店门口,顾客自己来拿走就行啦!”4. “FCA(Free Carrier),货交承运人呢!想象一下,你把货物交给运输公司的那个人,这时候责任就转移啦!就如同你把包裹交给快递员,之后就看快递员的啦!比如你和对方约定 FCA,你把货交给承运人就完成任务咯!”5. “CPT(Carriage Paid To),运费付至呀!就是说你要承担把货物运到指定地点的运费呢!这就好像你给朋友寄东西,你付了邮费一样,只不过这个距离更远啦!比如你要把货物运到某个地方,用 CPT 术语,你得把运费掏了哦!”6. “CIP(Carriage and Insurance Paid To),运费、保险费付至呢!哇塞,这就不仅要付运费,还要买保险哦!就像你送贵重物品给别人,不仅要付运费让它到对方那里,还要买保险以防万一呀!比如你用 CIP 术语,这些都得安排妥妥的!”7. “DAT(Delivered at Terminal),运输终端交货呀!就是货物到了指定的运输终端,责任就转移啦!好比你送东西到快递驿站,到了那里你就完成任务了呢!比如说你和对方约定 DAT,货物到了那个终端,你就可以松口气啦!”8. “DAP(Delivered at Place),目的地交货呢!这可厉害啦,要把货物送到指定的地点哟!就像你给朋友送礼物,直接送到他家门口一样!比如你用 DAP 术语,得把货物一路护送到目的地哦!”9. “DDP(Delivered Duty Paid),完税后交货呀!这可是最厉害的一个,你要承担所有的责任和费用,包括关税啥的!就像你给别人准备了一份超级豪华大礼包,什么都包了!比如你答应 DDP,那可真得把一切都搞定呀!”10. “L/C(Letter of Credit),信用证哟!这就像是给买家和卖家之间的一个保障,银行做担保呢!比如说买家开个信用证,卖家就放心发货,不用担心收不到钱啦!是不是很靠谱呢?”我的观点结论就是:这些国际贸易专业术语都很重要呀,搞清楚它们,才能在国际贸易中少走弯路,顺利完成交易呢!。

2020年国际贸易术语解释

国际贸易术语是在国际贸易活动中常用的一些专业术语,用于描述贸易过程中的各种操作、条款和条件。

以下是一些2020年国际贸易术语的解释:

1. CIF (Cost, Insurance, Freight),成本加保险加运费,指卖方负责将货物运至目的港并支付货物的运费和保险费用。

2. FOB (Free on Board),离岸价,指卖方将货物交至指定装运港口的船上,并承担费用和风险直至货物装上船为止。

3. EXW (Ex Works),工厂交货价,指卖方将货物交至指定地点的工厂或仓库,并由买方承担所有费用和风险。

4. DDP (Delivered Duty Paid),完税后交货,指卖方负责将货物交至买方指定的地点,并支付进口国的关税和其他费用。

5. Incoterms (International Commercial Terms),国际贸易术语,是国际贸易中常用的标准化术语,规定了买卖双方在货物交割、运费负担、风险转移等方面的责任和义务。

以上是2020年国际贸易术语的一些解释,这些术语在国际贸易中起着重要的作用,帮助买卖双方明确各自的责任和权利,确保贸易顺利进行。

Feenstra,Advanced International Trade Appendix B:Discrete Choice ModelsDiscrete choice models are commonly taught in econometrics,but the economic generality of these models is sometimes unclear.This is especially true when we consider models that incorporate not just demand but also the optimal prices charged by firms under imperfect competition.In that case,we want to derive demand and prices in a mutually consistent fashion,as will be discussed in this Appendix.We begin with an aggregation theorem due to McFadden(1978,1981).He has shown that when individual have random utility over discrete alternatives,the decisions that they made can sometimes be aggregated up to a representative consumer.McFadden focuses on the case where individual have utility functions that are linear in income,and where the goods over which a discrete choice is being made are purchased in the quantity0or1.Under certain conditions,it is possible to generalize this to the case where utility is nonlinear in income,and where the discrete-choice good is purchased in continuous quantities.This is a principal result of Anderson,de Palma and Thisse(1992,chaps.2-5)who show,for example,that the representative consumer can have a CES utility function,as we also demonstrate below.At the same time as presenting these aggregation results,we will discuss the empirical strategy to estimate discrete choice models due to Berry(1994).In this approach,we suppose that the individual-level data on consumer choices is not available.Rather,we just observe the market-level data on the quantity purchased of each product,as well as their prices and characteristics.The goal is to infer the individual taste parameters from this market-level data on quantities and prices,as well as parameters of marginal cost,so that price-cost margins can be estimated.Discrete Choice Model Suppose there is a population of consumers h,and we normalize its size to unity.Each consumer must decide which of a discrete number of alternatives j=1,…,N to purchase,and receives the following utility from consuming one unit of product j:h j j h j u V ε+=,(B1)where u j is the utility obtained from product j by every consumer,while h j εis an additional part of utility obtained by consumer h.We will treat h j εas a random variable with cumulative density function F(ε),where each consumer obtains a different draw of ε=(ε1,…,εN ).Given this draw,the consumer chooses the product with highest utility.The probability that a consumer will choose product j is:.]N 1,...,k all for ,u u Prob[]N 1,...,k all for ,u u Prob[]N 1,...,k all for ,V V Prob[P j k k j k k j j k j j =−≥ε−ε==ε+≥ε+==≥=(B2)We can think of (B2)as the probability that any consumer choose alternative j,orequivalently,as the expected fraction of the population that chooses that alternative.Thesolution for these choice probabilities depends on the distribution function F(ε),as well as on the specification of utility u j .A simplified version of utility used by Berry (1994)is,u j =y +β’z j –αp j +ξj ,α>0.(B3)Thus,utility is linear in individual income y,decreasing in the price p j ,and also depends on the characteristics z j of the product.1The term ξj is another random element in utility,but unlike h j ε,it does not vary across consumers.We could think of ξj as some unmeasured characteristics of product j,which is random across products but not consumers.In general,computing the choice probabilities from (B2)is computationally intensive since it requires integration over various subsets of the domain of F(ε).However,McFadden has shown that for a class of distribution functions F(ε)known as the generalized extreme value,the expected demands can be equivalently obtained by simple differentiation:Theorem 1(McFadden,1978,p.80;1981,p.227)Let H be a nonnegative function defined over N R +that satisfies the following properties:(i)H is homogeneous of degree one;(ii)∞→H as any of its argument approaches infinity;(iii)The mixed partial derivatives of H with respect to k variables exist and are continuous,non-negative if k is odd and non-positive if k is even,k=1,…,N.Define the generalized extreme value distribution function,)]e ...,e ,e (H exp[),...,(F N 21,N 1ε−ε−ε−−≡εε.(B4)Then the expected value of consumer utility (up to a constant)is given by the aggregate utility function,1This utility function is not homogeneous of degree zero in income y and price p j .To obtain this property,we should measure y and p j relative to a numeraire price p 0,so that utility becomes u j =y/p 0–αp j /p 0+β’z j +ξj ,which is homogeneous of degree zero in (y,p j ,p 0).)(N 21u u u N 1e ,...,e ,e H ln )u ,...,u (G ≡,(B5)and the choice probabilities P j in (B2)can be obtained as:P j =j u /G ∂∂.(B6)To interpret this theorem,consider the linear utility function in (B3).Substituting this into (B5)and using the linear homogeneity of H,the aggregate utility function is:)(N N N 111p z 'p z 'N N 11e ,...,e H ln y )y ,z ,p ,...,z ,p (G ~ξ+α−βξ+α−β+=.(B5’)Notice that 1y /G ~=∂∂,and consider the case where α=1.Then price is inversely related toutility (du j =–dp j ),so the choice probabilities in (B6)can be computed as P j =j u /G ∂∂=)y /G ~/()p /G ~(j ∂∂∂∂−.Thus,the result that P j =j u /G ∂∂in (B6)of the theorem can beinterpreted as saying that Roy’s Identity holds at the aggregate level.The conditions on H in (i)-(iii)are technical properties needed to ensure that the F(ε)defined in (B4)is indeed a cumulative distribution function.There will be many choices of H satisfying these conditions,and for each,we obtain the aggregate utility function in (B5),whose demands are identical to those aggregated from the individual choice problem in (B1)-(B2).Furthermore,this aggregate utility function can be used to make welfare statements about the individual consumers,since it reflects expected individual utility.To see the usefulness of this result,we consider the well-known example where therandom utility εj in (B1)from consuming each product are independently distributed across products,with the extreme value distribution.Example 1:Logit demand system Let us choose the function H as linear in its arguments:=ε−ε−ε−)e ...,e ,e (H N 21,j N 1j e ε−=∑.(B7)Substituting (B7)into (B4),the distribution function is:)eexp(),...,(F j N 1j N 1ε−=−=εε∏.(B8)This cumulative distribution function is therefore the product of N iid “double-exponential”or extreme value distributions,which apply to the random utility terms in (B1).Therefore,the random term in utility is distributed as iid extreme value.2Computing the choice probabilities as in (B6)using (B7)and (B3),we obtain:][][1k p z 'p z '1k u u j k k k jj j k je e e e P ∑∑=ξ+α−β===,(B9)which are the choice probabilities under the logit system.Berry (1994)discusses how estimates of αand βcan be obtained even if we do not have data on the purchases by each individual,but just observe the quantity-share s j of each product in demand,as well as their prices and characteristics.Then the probabilities in (B9)would be measured by these quantity-shares s j .Suppose in addition there is some outside option j=0,which gives utility normalized to zero,u 0=0.Then setting s j =P j ,and taking logs of the ratio of (B9)to s 0,we obtain:2A discussion of the “double exponential”or extreme value distribution is provided by Anderson,de Palma and Thisse (1992,pp.58-62).j j j 0j p z 's ln s ln ξ+α−β=−.(B10)In addition,we follow Berry to solve for the optimal prices of the firm,where we assume for simplicity that each firm produces only one product.Denoting the marginal costs of producing good j by g j (z j ),and ignoring fixed costs,the profits from producing model j are,j j j j j s )]z (g p [−=π,(B11)Maximizing (B11)over the choice of p j ,treating the prices of all other products as fixed,we obtain:1j j j j j j j j j j )p /s ln ()z (g )p /s /(s )z (g p −∂∂−=∂∂−=.(B12)For the special case of the logit system (B9)with s j =P j denoting the quantity-shares,we see that )s 1(p /s ln j j j −α−=∂∂.If we also specify marginal costs as g j (z j )=γ’z j +ωj ,where ωj is a random error,then from (B12)the optimal prices are:j j j j )s 1(1z 'p ω+−α+γ=,(B13)which can be estimated jointly with (B10).It is apparent,though,that the random error ξj influence the market shares in (B10),and therefore from (B13)will be correlated with prices p j .Accordingly,the joint estimation of (B10)and (B13)should be done with instrumentalvariables.3The problem with this simple logit example is that the demand elasticities obtained are implausible.From the market shares s j=P j in(B9)we readily see that s j/s k is independent of the price or characteristics of any third product i.This property is known as the“independence of irrelevant alternatives”in the discrete choice literature,and it implies that the cross-elasticity of demand between products j and k and the third product i must be equal.To improve on this,we consider the nested logit system.Example2:Nested Logit demand systemNow suppose that the consumers have a choice over two levels of the differentiated product.First,an individual decides whether to purchase a product in each of g=1,…,G groups (for example,small cars and big cars),and second,the individual decides which of the products in that group to purchase.Suppose that the products available in each group g are denoted by the set J g⊂{1,…,N},while J0denotes the outside option.Utility from consumer h is still given by (B1),where the errorsεj are distributed as extreme value but are not independent.Instead,we suppose that if consumer h has a high value of h jεfor some product g Jj∈,then that person will also tend to have high values of h kεfor all other products g Jk∈,soεj is positively correlated across products in each group.For example,an individual who has a preference from some small car also tends to like other small cars.3Berry(1994,p.249)suggests that appropriate instruments for prices in(B10)are characteristics of other models z k,as well as variables that affect the costs of producing product j.To achieve this correlation between the random errors in (B1),McFadden (1981,p.228)chooses the function H as,=ε−ε−)e ,...,e (H N 1)1(G 0g J j )1/(g g g j e ρ−=∈ρ−ε−∑∑ .(B14)To satisfy property (iii)of Theorem 1,we need to specify that 0<ρg <ing this choice of H,we obtain a distribution function F(ε)from (B4),=εε),...,(F N 1 −ρ−=∈ρ−ε−∑∑)1(G 0g J j )1/(g g g j e exp ,(B15)where ρg roughly measures the correlation between random terms εj within a group.4Computing the choice probabilities as in (B6)using (B14),we obtain:∑=ρ−ρ−ρ−=G 0g )1(g )1(gg )1/(u j ][g g g j D D D e P ,for g J j ∈,(B16)where the term ∑∈ρ−≡g g k J k )1/(u g e D appearing in (B16)is called an “inclusive value”,since itsummarizes the utility obtained from all products in the group g.Berry (1994,p.252)motivates this nested logit case somewhat differently.He re-writes the random errors h j εas,h j g h g h j e )1(ρ−+ζ=ε,for g J j ∈,(B17)4Johnson and Kotz (1972,p.256)report that the parameters (1-ρg )equal )k ,j (corr 1εε−,for i,k ∈J g and i ≠k,so that )k ,j (corr εε>0for ρg >0.where the errors h j e are iid extreme value.The random variable h g ζin (B17)is common to allproducts within group g,and therefore induces a correlation between the random utilities forthose products.Cardell (1997)shows that there exists a distribution for h g ζ(depending on ρg )such that when h j e are iid extreme value,then h j εare also distributed extreme value but are notindependent.Notice that as the parameter ρg approaches unity then h j εare perfectly correlatedwithin the group g (since they equal h g ζ),whereas when ρg approaches zero (in which case h gζalso approaches zero)then h j εbecome ing the errors in (B17)gives the same choice probabilities as shown in (B16).Using the nested logit choice probabilities in (B16),we can re-derive the estimatingequations for market share and optimal prices,as in Berry (1994,pp.252-253).The first term on the right of (B16)is the probability that an individual will choose product g J j ∈conditional on having already chosen the group g.Let us denote this conditional probability by g |j s .Thesecond term on the right of (B16)is the probability of choosing any product from group g,which we write as g s .So replacing P j in (B16)by the market shares s j ,we write this choice probability as g g |j j s s s =.In addition,we suppose that the outside good has u 0=0and inclusive value D 0=1,so that from (B16),1G 0g )1(g 00][g D P s −=ρ−∑==.Taking logs of the ratio 0g g |j 0j s /s s s /s =and using the linear utility u j in (B3),we therefore have,g g g j j j 0j D ln )1()p z '(s ln s ln ρ−ρ−ξ+α−β=−.(B18)To solve for the inclusive value D g ,recall that g s equals the second term on the right of (B16).Therefore,)1(g 0g g D s /s ρ−=and so g g 0g D ln )1(s ln s ln ρ−=−.Using this in (B18)and simplifying with g g |j j s s s =,we obtain,j g |j g j j 0j s ln p z 's ln s ln ξ+ρ+α−β=−,g J j ∈.(B19)This gives us a regression to estimate the parameters (α,β),where the final term g |j s ln measures the market share of product j within the group g,and is endogenous.Once again,we can use instrumental variables to estimate (B19).5In addition,we follow Berry (1994,p.255)to solve for the optimal prices of the firm,assuming for simplicity that it produces only one product j.Profits are still given by (B11),and the first-order condition by (B12).For the nested logit system with s j =P j in (B16),the derivative of the log market shares is ]s )1(s 1[)1(p /s ln j g g |j g g j j ρ−−σ−σ−α−=∂∂.With marginal costs as g j (z j )=γ’z j +ωj ,where ωj is a random error,from (B11)the optimal prices are:j j g g |j g g j j ]s )1(s 1[)1(z 'p ω+ρ−−ρ−αρ−+γ=,(B20)5Berry (1994,p.254)suggests that appropriate instruments will include the characteristics of other products or firms in group g.which can be estimated simultaneously with (B19)using instrumental variables.This pricing equation was generalized in chapter 8to allow for multi-product firms,as used by Irwin and Pavcnik (2001)in their study of export subsidies to commercial aircraft.The nested logit allows for more general substitution between products than does thesimple logit model (and does not suffer from “independence of irrelevant alternatives”).Goldberg (1995),for example,has used the nested logit in her study of automobile demand in the U.S.and the impact of the voluntary export restraint (VER)with Japan.Nevertheless,more flexible in the pattern of demand across autos can be achieved by introducing greater consumer heterogeneity,as done by Berry,Levinsohn and Pakes (1993,1999)in their work on autos and the VER with Japan.They suppose that the utilities in (B3)instead appear as,j j j h h j p z 'u ξ++α−β=,α>0,(B3’)where now the parameters βhdepend on the individual h,reflecting both demographiccharacteristics and income.Since individual income is included in βh ,without loss of generality we omit this variable from appearing explicitly in (B3’).If we observed both individual characteristics and also their discrete choices,then itwould be possible to estimate the other parameters appearing in (B3’)using standardeconometric programs for discrete choice.However,when we observe only the market-level demands and overall distribution of individual characteristics,then estimating the parameters of (B3’)becomes much more difficult.To see this,let us suppose that the individual characteristics βh are distributed as h η+β,with mean value βover the population and h ηis a randomvariable that captures individual tastes for characteristics.Substituting this into (B3’)and then into (B1),we obtain utility,)z '(p z 'V h j j h j j j h j ε+η+ξ+α−β=,(B1’)where now the random error includes the interaction term j h z 'ηbetween individual tastes and product characteristics.The presence of this interaction term means that Theorem 1cannot be used:the cumulative distribution of the combined error )z '(h j j h ε+ηis more general than allowed for in Theorem 1.It follows that there is no closed-form solution such as (B6)for the choice probabilities.Instead,the choice probabilities need to be calculated numerically from (B2).That is,given the data (p j ,z j )across products we can simulate the distribution of )z '(h j j h ε+η.For each draw from this distribution,and for given parameters ),(j ξβα,we can calculate utility h j V for each product.The choice probabilities P j in (B2)are computed as the proportion of draws for which product j gives the highest utility.Then the parameters ),,(j ξβαare chosen so that these choice probabilities match the observed market shares s j as closely as possible.Likewise,the predicted change in the market shares due to prices,)p /s (j j ∂∂in (B12),would be calculated numerically by seeing how the choice probability P j vary with prices p j .This also depends on the parameters ),(j ξβα,which are then chosen so that the pricing equations fit as closely as possible.Thus,the market share and pricing equations are simultaneously used to estimate the underlying taste and costs parameters,using simulated distributions of the random term in utility.This is the idea behind the work of Berry,Levinsohn and Pakes (1993,1999),to which you arereferred for more details.6It is also useful to compare the above approaches with a third approach to discrete choice models:rather than using a representative consumer,or individuals with random utility,we could instead use individuals that differ in terms of their preferred characteristics,in what is sometimes called the “ideal variety”approach.Anderson,de Palma and Thisse (1992)derive an equivalence between all three approaches.Bresnahan (1981)was the first to estimate a discrete choice model for autos in which consumers differ in their ideal varieties,and found that higher-priced models tended to have higher percentage markups.Feenstra and Levinsohn (1995)generalized the model of Bresnahan by allowing characteristics to differ multi-dimensionally,rather than along a line as in Bresnahan,and show how the optimal prices of firms will vary with the distance to their nearest neighbors.Discrete Choice with Continuous QuantitiesSetting aside the issue of consumer heterogeneity,there is another direction in which we can attempt to generalize Theorem 1,while still allowing the aggregate utility function to exist so that demands can be computed using Roy’s Identity.We again suppose that consumers are still choosing over products j=1,…,N,and now have the utility function:h j V =ln y –)z ,p (ln j j φ+h j ε,j=1,…,N,(B21)where p j is the price of product j,z j is a vector of characteristics,y is the consumers’income,and εj is a random term that reflects the additional utility received by consumer h from product j.6Estimating a discrete choice model by simulating the taste parameters is referred to as “mixed logit”.See,for example,McFadden and Train (1997)and Revelt and Train (1999).A distance learning course on discrete choice methods including software to estimate mixed logit models is available from Kenneth Train at /~train/distant.html .Thus,income no longer enter utility in a linear fashion,and we will allow individuals to consume continuous quantities (not restricted to 0or 1)of their preferred product j.Each consumer still chooses their preferred product j with probability:P j =Prob[V j >V k for all k=1,…,N ].(B22)If product j is chosen,then the quantity consumed is determined from the indirect utility function in (B21),using Roy’s identity:c j =y /V p /V h j jh j ∂∂∂∂−=y )j p /ln (∂φ∂.(B23)It follows that expected demand for each product is:X j =c j P j .(B24)This formulation of the consumer’s problem is somewhat more general than what we considered earlier,because now we are allowing the consumer to make a continuous choice of the quantity purchased.This falls into the category of so-called “continuous/discrete”models (see Train,1986,chap.5).However,our formulation of the problem is simplified,however,because there is no uncertainty over the quantity of purchases in (B24);the random term in utility affects only the choice of product in (B22).7It turns out that in this setting,theaggregation results of McFadden (1978,1981)apply equally well,and we can extend Theorem 1as:87In contrast,Dubin and McFadden (1984)consider an application where there is uncertainty in both the discrete choice of the product and the continuous amount to consume.8The proof of Theorem 2,based on the results of McFadden,is provided in Feenstra (1995,Prop.1).Theorem 2Let H be a nonnegative function defined over N R +that satisfies conditions (i)-(iii)of Theorem 1.Define the cumulative distribution function F as in (B3),and define an aggregate indirect utility function,]1N N 111N N 11)z ,p (,...,)z ,p ([H ln y ln )y ,z ,p ,...,z ,p (G −−φφ+=.(B25)Then:(a)Expected demand computed from (B24)equals )y /G /()p /G (j ∂∂∂∂−;(b)G equals expected individual utility in (B21)(up to a constant).Thus,we can still compute demand using Roy’s identity as in part (a),and use theaggregate utility function to infer welfare as in part (b).Notice that expected utility can be re-written in a more familiar form by taking the monotonic transformation )G exp(G ~=,so that,]1N N 111N N 11)z ,p (,...,)z ,p ([H y )y ,z ,p ,...,z ,p (G ~−−φφ=.(B25’)This can be interpreted as an indirect utility function for the representative consumer.To see the usefulness of this result,we consider again a random utility εj in (B21)that are independently distributed across products,with the extreme value distribution,and derive a CES aggregate utility function.Example 3:CES demand system Let us specify the individual utility functions as:9h j V =ln y –αln[p j /f(z j )]+h j ε,α>0,(B26)where we are measuring prices relative to consumers’perceived “quality”of products f(z j ).We will choose the function H as linear in its arguments,as in (B7).It follows that thecumulative distribution function in (B8)is the product of N iid extreme value distributions,so the errors in (B26)are distributed as iid extreme value.Then using (B7),(B25)and (B26),we obtain the aggregate utility function as:=)y ,z ,p ,...,z ,p (G N N 11∑=α−N 1j j j )]z (f /p [y,(B27)so that expected aggregate demand is,α=∂∂∂∂−∑=α−−α−N 1k k k 1j j j )]z (f /p [)]z (f /p [y y /G p /G .(B28)Thus,we obtain a CES indirect utility function in (B27)for the aggregate consumer,with elasticity of substitution with σ=1+α,and the associated CES demand in (B28).This is an alternative demonstration of the result in Anderson,de Palma and Thisse (1989;1992,pp.85-90),that the CES utility function arrives from a discrete choice model with iid extreme value errors in random utility.Notice that this CES demand system is obtained with exactly the same 9This utility function is not homogeneous of degree zero in income y and price p j .To obtain this property,we should measure y and p j relative to a numeraire price p 0,so that utility becomes ln(y/p 0)–αln[(p j /p 0)/f(z j )],which is homogeneous of degree zero in (y,p j ,p 0).assumptions on the random term in utility as the logit system (both used iid extreme value distributions),but differs from the logit system in allowing for continuous quantities of the discrete good.Example 4:Nested CES demand systemAs in our above discussion of the nested logit model,suppose that the consumers have a choice over two levels of the differentiated product.First,an individual decides whether to purchase a product in each of g=1,…,G groups,and second,the individual decides which of the products in that group to purchase.Let the products available in each group g be denoted by the set J g ⊂{1,…,N},while J 0denotes the outside option.Utility for consumer h is still given by (B26),where the errors εj are distributed as extreme value but are not independent.We will specify the function H as in (B14),with the cumulative density function F as in (B15).Then using (B14),(B25)and (B26),we obtain the aggregate utility function:=)y ,z ,p ,...,z ,p (G N N 11∑∑=ρ−∈ρ−α− G 0g )1(J j )1/(j j g g g )]z (f /p [y .(B29)Applying Roy’s Identity,we can readily obtain the expected demand for product j,∑=ρ−ρ−ρ−α− α=∂∂∂∂−=G 1g )1(g )1(g g )1/(j j j j j ]D [D D )]z (f /p [p y y /G p /G X g g g ,for g J j ∈,(B30)where the term ∑∈ρ−α−≡g g J j )1/(j j g )]z (f /p [D in (B30)is again the “inclusive value”,analogous to (B16).Notice that expected demand on the right of (B30)is composed of three terms:the first term,(αy/p j ),is a conventional Cobb-Douglas demand function,reflecting thecontinuous demand for the product given the utility function in (B26);the second term,g )1/(j j D /)]z (f /p [i ρ−α−,is the share of product j in the demand for group g;and the third term,∑=ρ−ρ−G 0g )1(g )1(g ]D /[D g g ,is the share of group g in the total demand for the product.The latter two terms both appear in the nested logit system (B16),so the new feature of (B30)is the continuous demand of (αy/p j ).We can easily relate the parameters ρ0and ρi to the elasticity of substitution between products.Notice that for two products g J j ,i ∈,we obtain relative demand from (B30),1)]1/([j i )1/(j i j i g g p p )z (f )z (f X X −ρ−α−ρ−α =,g J j ,i ∈.(B31)Thus,the elasticity of substitution between two products in the same group is 1+[α/(1–ρg )]>1.In addition,we can compute from (B29)that the ratio of expenditure on products from two different groups g and h:)1(h )1(g j J j j iJ i i h g h g D D X p X p ρ−ρ−∈∈=∑∑,h g J j and J i ∈∈.(B32)Let us define the price index for the products in group g as,αρ−−αρ−−∈ρ−α−= ≡∑/)1(g /)1(J j )1/(j j g g g g g D )]z (f /p [P .Then we can rewrite the ratio of expenditures in (B32)as,1h g h j J j j g i J i i P P P /)X p (P /)X p (h g −α−∈∈ =∑∑,h g J j and J i ∈∈.(B33)The left-side of (B33)is ratio of expenditures on groups g and h,deflated by their price indexes,so it can be interpreted as a ratio of real expenditures.We see that this depends on the ratio of price indexes for the two groups,with the elasticity 1+α>1.Feenstra,Hanson and Lin (2002)have used a slightly more general version of this nested CES structure to estimate the gains from having Hong Kong traders act as intermediaries for firms outsourcing with China.。