财务管理专业英语第二章

- 格式:ppt

- 大小:528.50 KB

- 文档页数:19

《专业英语》(会计学、财务管理专业)课程简介、教学要求、教学内容和学时分配一、课程简介(1)本课程在人才培养过程(培养计划)中的地位及作用本课程是会计学、财务管理专业的选修课程。

对于会计学、财务管理专业的学生而言,专业英语水平和应用能力的修养不仅仅是文化素质的主要部分,在很大程度上也是个人综合素质能力的补充、延伸,视野的拓宽。

本课程的任务主要是通过学习原版英文基本专业知识,培养学生独立阅读与本专业相关的英文论文和相应的写作能力。

(2)本课程支撑相关专业毕业要求的指标点:《专业英语》支撑会计学专业毕业要求的指标点是:1.具有良好人际关系和团队合作精神,具备较强的语言与文字沟通、文献检索和资料查询等信息获取能力。

2.掌握并运用高等数学、统计学、外语和计算机方面的知识技能,以及必要的信息技术知识。

《专业英语》支撑财务管理专业毕业要求的指标点是:1.具有良好人际关系和团队合作精神,具备较强的语言与文字沟通、及文献检索和资料查询等信息获取能力。

2.掌握计算机应用技术和一门外语,能熟练运用常用的办公软件。

3.熟悉我国财务管理工作的政策、法规以及国际惯例与规则。

二、教学基本要求本课程的教学要求是把财会知识和英语融为一体,使本专业学生了解最新的国际财会动态、全面提高自身的专业英语水平、扩充专业词汇、提高阅读速度的要求,近而达到准确而迅速地筛选所需信息的水平。

同时,本课程还通过一系列的专业技能训练,培养和强化学生的涉外业务英语交际能力,从而使之具备复合型人才的要求。

1.听力要求:能听懂涉及专业知识的学术报告、专题讲座等,并能理解其中立柱的事实或饮食的较为抽象的概念。

2.口语要求:能在学术会议或专业交流中较为自如地表达自己的观点和看法。

3.阅读要求:能较为顺利地阅读所学专业的英语文献和资料。

4.写作要求:能撰写专业文章摘要,能写简短的专业报告和论文。

5.翻译要求:能借助词典翻译所学专业的文献资料和英语国家报刊上有一定难度的科普、文化、评论等文章。

财务管理专业英语financialmanagement 财务管理decision-making 决策,决策得acquire获得,取得publiclytraded corporations公开上市公司公众vice president of finance财务副总裁chief financial officer 首席财务官chief executiveofficer 首席执行官balance sheet资产负债表capital budgeting 资本预算workingcapital management 营运资本管理hurdlerate最低报酬率capital structure资本结构mixof debt andequity负债与股票得组合cash dividend现金股利stockholder股东dividend policy 股利政策dividend-payout ratio股利支付率stock repurchase股票回购stock offering股票发行tradeoff 权衡,折中monstock 普通股current liability 流动负债current asset流动资产marketable security流动性资产,有价证券inventory 存货tangible fixedassets 有形固定资产in tangible fixed assets 无形固定资产patent专利trademark商标creditor债权人stockholds’ equity股东权益financing mix融资组合risk aversion 风险规避volatility 易变性不稳定性allocate 配置capital allocation资本配置business 企业商业业务financialrisk财务风险soleproprietorship 私人业主制企业partnership合伙制企业limitedpartner有限责任合伙人general partner 一般合伙人separation of ownership and control 所有权与经营权分离claim 要求主张要求权managementbuyout 管理层收购tender offer要约收购financial standards 财务准则initial public offering首次公开发行股票privatecorporation 私募公司未上市公司closely heldcorporation 控股公司boardof directors 董事会executove director执行董事non-executove director非执行董事chairperson主席controller 主计长treasurer 司库revenue收入profit 利润earnings per share 每股盈余return回报marketshare 市场份额social good社会福利financial distress 财务困境stakeholder theory 利益相关者理论value (wealth) maximization价值(财富)最大化commonstockholder普通股股东preferred stockholder 优先股股东debt holder债权人well—being福利diversity多样化going concern 持续得agency problem 代理问题free—riding problem 搭便车问题informationasymmetry 信息不对称retailinvestor散户投资者institutional investor 机构投资者agencyrelationship代理关系net present value净现值creativeaccounting 创造性会计stock option 股票期权agency cost代理成本bonding cost 契约成本monitoring costs 监督成本takeover 接管corporate annualreports公司年报balancesheet 资产负债表income statement利润表statement ofcash flows 现金流量表statementofretained earnings 留存收益表fairmarket value 公允市场价值marketable securities油价证券check 支票money order 拨款但、汇款单withdrawal 提款accounts receivable应收账款creditsale赊销inventory 存货property,plant,and equipment 土地、厂房与设备depreciation折旧accumulated depreciation累计折旧liability 负债currentliability流动负债long—term liability 长期负债accounts payout 应付账款note payout 应付票据accrued espense应计费用deferredtax 递延税款preferred stock优先股commonstock普通股book value 账面价值capital surplus资本盈余accumulated retainedearnings 累计留存收益hybrid混合金融工具treasury stock 库藏股historic cost 历史成本current market value 现行市场价值real estate 房地产outstanding 发行在外得aprofit andloss statement 损益表netincome净利润operating income 经营收益earnings per share每股收益simple capital structure 简单资本结构dilutive冲减每股收益得basicearnings per share 基本每股收益complex capital structures 复杂得每股收益diluted earningsper share 稀释得每股收益convertiblesecurities可转换证券warrant 认股权证accrual accounting 应计制会计amortization 摊销accelerated methods加速折旧法straight—line depreciation 直线折旧法statement ofchanges inshareholders’equity股东权益变动表source of cash 现金来源use ofcash 现金运用operating cash flows经营现金流cash flow from operations 经营活动现金流direct method直接法indirectmethod间接法bottom-up approach倒推法investing cash flows 投资现金流cash flow frominvesting 投资活动现金流joint venture合资企业affiliate 分支机构financing cash flows 筹资现金流cash flowsfrom financing 筹资活动现金流timevalue of money货币时间价值simple interest单利debtinstrument债务工具annuity 年金future value 终至present value现值compound interest复利pounding复利计算pricipal 本金mortgage抵押credit card信用卡terminalvalue终值discounting 折现计算discountrate折现率opportunitycost 机会成本required rateofreturn要求得报酬率costof capital资本成本ordinary annuity普通年金annuity due 先付年金financialratio 财务比率deferredannuity 递延年金restrictivecovenants 限制性条款perpetuity 永续年金bond indenture 债券契约facevalue 面值financial analyst 财务分析师coupon rate 息票利率liquidity ratio流动性比率nominal interest rate名义利率current ratio 流动比率ﻩeffective interest rate有效利率window dressing 账面粉饰going—concernvalue持续经营价值marketable securities短期证券liquidationvalue清算价值quick ratio 速动比率ﻩbook value账面价值cash ratio 现金比率marker value市场价值debt management ratios债务管理比率ﻩintrinsicvalue内在价值debtratio债务比率mispricing 给……错定价格debt-to-equity ratio 债务与权益比率valuation approach 估价方法equity multiplier权益乘discounted cash flow valuation 折现现金流量模型long-term ratio 长期比率undervaluation 低估debt—to—total—capital债务与全部资本比率ﻩovervaluation 高估leverageratios杠杆比率option-pricing model 期权定价模型interestcoverage ratio利息保障比率contingent claim valuation或有要求权估价earnings beforeinterest and taxes 息税前利润promissory note 本票cash flow coverage ratio 现金流量保障比率contractual provision契约条款asset management ratios 资产管理比率par value票面价值accounts receivable turnover ratio应收账款周转率maturity value 到期价值inventory turnover ratio 存货周转率coupon息票利息inventory processing period存货周转期coupon payment 息票利息支付accounts payable turnover ratio 应付账款周转率coupon interest rate 息票利率cashconversion cycle现金周转期maturity到期日asset turnover ratio资产周转率term tomaturity到期时间profitability ratio盈利比率ﻩcall provision赎回条款gross profit margin 毛利润ﻩcallprice 赎回价格operatingprofit margin经营利润sinkingfund provision 偿债基金条款net profitmargin 净利润ﻩconversion right转换权return on asset资产收益率ﻩput provision 卖出条款return on total equity ratio全部权益报酬率indenture债务契约return on common equity 普通权益报酬率covenant 条款market-to—book value ratio市场价值与账面价值比率trustee 托管人market valueratios市场价值比率protectivecovenant保护性条款dividendyield股利收益率negative covenant消极条款dividendpayout股利支付率ﻩpositive covenant积极条款financial statement财务报表secured deht担保借款profitability 盈利能力unsecureddeht信用借款viability生存能力ﻩcreditworthiness 信誉solvency偿付能力ﻩcollateral 抵押品collateral trust bonds 抵押信托契约debenture信用债券bond rating 债券评级current yield现行收益yield to maturity 到期收益率default risk 违约风险interest rate risk 利息率风险authorized shares 授权股outstanding shares发行股treasuryshare 库藏股repurchase 回购right to proxy代理权rightto vote 投票权independentauditor 独立审计师straight or majority voting 多数投票制cumulative voting积累投票制liquidation 清算righttotransfer ownership 所有权转移权preemptive right 优先认股权dividenddiscount model股利折现模型capitalassetpricingmodel资本资产定价模型constantgrowthmodel 固定增长率模型growth perpetuity增长年金mortgage bonds 抵押债券portfolio 组合diversifiable risk可分散风险market risk市场风险expected return期望收益volatility 流动性stand-alonerisk 个别风险randomvariable随机变量。

《财务专业英语》课程教学大纲课程代码:ABGS0519课程中文名称:财务专业英语课程英文名称:Financial English课程性质:选修课程学分数:2课程学时数:32授课对象:财务管理专业本课程的前导课程:财务管理基础、中级财务会计、财政与金融、金融市场学、财务报表分析一、课程简介《财经专业英语》是财务管理专业的一门专业选修课程。

通过本课程的学习,强化学生财务管理专业英语的综合运用能力,为学生营造一个在国际视野下用英语思考财务问题和解决财务问题的环境。

二、教学基本内容和要求1 Introduction to Financial Management (1)1.1 Financial Management and Financial Manager1.2 Financial Management Decision: Investment Decisions, Financing Decisions, Working Capital Management Decisions1.3 Risk-Return Tradeoff本章重点:Financial Management Decision.本章难点:Financial Management Decision.2 Introduction to Financial Management (2)2.1 Types of Business Organization: Sole Proprietorship, Partnership, Corporation2.2 Corporate Structure of the Company: Shareholders, Board of Directors, CEO, CFO2.3 Objectives of Financial Management: Stakeholder Theory, Value of Wealth Maximization2.4 Separation of Ownership and Control2.5 Agency Relationships: Agency Problem, Agency Costs, Practical Solutions to the Agency Problem本章重点:Objectives of Financial Management.本章难点:Objectives of Financial Management, Agency Problem and Solutions.3 Interpreting Financial Statement3.1 Basics of Annual Repots and Financial Statements: Corporate Annual Reports,Overview of Financial Statements3.2 Balance Sheet3.3 Income Statement3.4 Statement of Retained Earnings3.5 Statement of Cash Flow: Operating Cash Flows, Investing Cash Flows, Financing Cash Flows本章重点:Interpretation of Financial Statements.本章难点:Interpretation of Financial Statements.4 Financial Ratio Analysis4.1 Financial Ratio Analysis4.2 Liquidity Ratios: Current Ratio, Quick Ratio, Cash Ratio4.3 Debt Management Ratios: Debt Ratio, Long-term Debt Ratio, Cash Flow Coverage Ratio4.4 Asset Management Ratios: Accounts Receivable Turnover Ratio, Inventory Turnover Ratio, Accounts Payable Turnover Ratio, Asset Turnover Ratios4.5 Profitability Ratios: Gross Profit Margin, Operating Profit Margin, Net Profit Margin, Return on Assets, Total Return on Assets, Return on Equity, Return on Common Equity, DuPont Analysis of ROE4.6 Market Value Ratios: Price/earnings Ratio, Market-to-book Value Ratio, Dividend Yield and Payout4.7 Uses and Limitations of Financial Ratio Analysis本章重点:Principle Financial Ratios.本章难点:Calculation and Signification of Principle Financial Ratios, DuPont Analysis.5 Time Value of Money and Valuation5.1 Central Concepts in Financial Management5.2 Simple vs. Compound Interest Rates and Future vs. Present Value: Simple Interest, Compound Interest, Future Value, Present Value5.3 Annuity: Ordinary Annuity, Annuity Due, Deferred Annuity, Perpetuity, Nominal and Effective Interest Rates5.4 Valuation Fundamentals: Going-concern Value, Liquidation Value, Book Value, Market Value, Intrinsic Value, Valuation Approaches, Discounted Cash Flow Valuation5.5 Bond Valuation: Contractual Provisions of a Typical Bond, the Bond Valuation Formula, Bond Prices and Returns5.6 Common Stock Valuation: Common Stock Characteristics and Features, Common Stock Valuation本章重点:Compound Interest Rates, Future Value, Present Value, Annuity, Valuation Approaches.本章难点:Present Value of Different Annuity.6 Risk and Return6.1 Introduction to Risk and Return: Return, Risk6.2 Efficient Market Hypothesis (EMH): Introduction, Financial Market Efficiency, Anomalies in Finance6.3 Portfolio Theory: The Expected Return of a Portfolio, Risk in a Portfolio Context, Modern Portfolio Theory, Diversified Risk versus Market Risk6.4 Beta and Capital Asset Pricing Model: The Concept of Beta, CAPM6.5 Arbitrage Pricing Theory本章重点:CAPM.本章难点:CAPM.7 Capital Budgeting7.1 Capital Investment Decisions: Nature of Capital Budgeting, Project Classifications7.2 Guidelines for Estimating Project Cash Flows: Incremental Cash Flows, Focus on After-tax Cash Flows, Postpone Considering Financing Costs, Other Cash Flow Considerations7.3 Investment Rules: Payback Period, Net Present Value, Internal Rate of Return, Profitability Index7.4 Business Practice7.5 Analyzing Project Risk: Sensitivity Analysis, Break-even Analysis, Simulation7.6 Project Selection with Resource Constrains7.7 Qualitative Factors and the Selection of Projects7.8 The Post-Audit本章重点:Capital Investment Decision Indices.本章难点:Internal Rate of Return.8 Capital Market and Raising Funds8.1 Financial Markets: Role of Financial Markets, Types of Financial Markets, Recent Trend8.2 Investment Banks: Advising, Underwriting, Marketing8.3 The Decision to Go Public: Advantages of Going Public, Disadvantages of Going Public, Different Methods of Issuing New Securities8.4 Cost of Capital Concept: Use of the Cost of Capital, Capital Components, Weighted Average Cost of Capital本章重点:Cost of Capital.本章难点:Cost of Capital.9 Capital Structure9.1 The Choices: Types of Financing9.2 The Financing Mix9.3 Understanding Financial Risk9.4 Capital Structure and the Value of a Firm: The Modigliani-Miller Theorem, The M&M Theorem in the Real World, Tradeoff Theory of Optimal Capital Structure, Pecking Order Theory of Capital Structure9.5 Checklist for Capital Structure Decisions本章重点:Capital Structure Decisions.本章难点:Capital Structure Decisions.10 Dividend Policy10.1 Dividends and Dividend Policy: Dividend Payout Procedure, Types of Dividends10.2 The Dividend Puzzle: Dividend Irrelevance Theory, Dividend Relevance Theory10.3 Factors Influencing the Dividend Decision: Shareholder Factors, Firm Factors, Managerial Preferences and Constraints10.4 Dividend Policies: Residual Dividend Policy, Stable Dollar Dividend Policy, Constant Dividend Payout Ratio, Low Regular plus Specially Designated Dividends10.5 Stock Repurchases: Ways of Repurchases, Reasons for Stock Buybacks本章重点:Dividend Policies.本章难点:Stock Repurchases.11 Working Capital11.1 Introduction to Working Capital Management11.2 Cash Management: Three Motives for Holding Cash, Determining Appropriate Cash Balances, Investment Idle Cash, Types of Money Market Securities, Managing Collections and Disbursements11.3 Accounts Receivable Management: Credit Policy, Collection Policy11.4 Inventory Management: Successful Inventory Management, The Purchasing Plan, Inventory Management Techniques本章重点:Motives for Holding Cash, Determination of Appropriate Cash Balances.本章难点:Determination of Appropriate Cash Balances.12 International Financial Management12.1 Introduction: The Global Economy, Multinational Corporations12.2 Foreign Exchange Market: Exchange Rates, Currency Risk, Types of Transactions12.3 Exchange Rate Parity: Interest Rate Parity, Purchasing Power Parity, Unbiased Forward Rates, Inflation, Interest Rates and Exchange Rates12.4 Multinational Capital Budgeting12.5 International Financial Decision12.6 Working Capital Management12.7 Hedging Currency Risk: Currency Forward Contracts, Currency Futures Contracts, Currency Swaps, Currency Option Contracts本章重点:International Financial Decision.本章难点:Hedging Currency Risk.三、实验教学内容及基本要求无四、教学方法与手段教学方法:理论教学、案例教学、启发示教学、情境教学教学手段:板书教学、多媒体教学五、教学学时分配六、考核方式与成绩评定标准1、考核方法:集中考核(考核方式:考查)2、成绩评定:平时成绩(考勤、课堂表现及作业)占40%,期末考核成绩占60%。

Topic1:1、Financial management is an integrated decision-making process concerned with acquiring, financing, and managing assets to accomplish some overall goal within a business entity.财务管理是为了实现一个公司总体目标而进行的涉及到获取、融资和资产管理的综合决策过程。

2、Making financial decisions is an integral part of all forms and sizes of business organizations from small privately-hold forms to large publicly-traded corporations.做财务决策对于所有形式和规模的商业组织,无论是小型私人公司还是大型公开上市公司,都是不可分割的一部分。

3、In today’s rapidly changing environment, the financ ial manager must have the flexibility to adapt to external factors such as economic uncertainty, global competition, technological change, volatility of interest and exchange rates, changes in laws and regulations, and ethical concerns.在当今瞬息万变的环境中,财务经理必须具备足够的灵活性以适应外部因素,如经济的不确定性、国际竞争、技术变革、利息波动、汇率变动、法律法规变化以及商业道德问题。

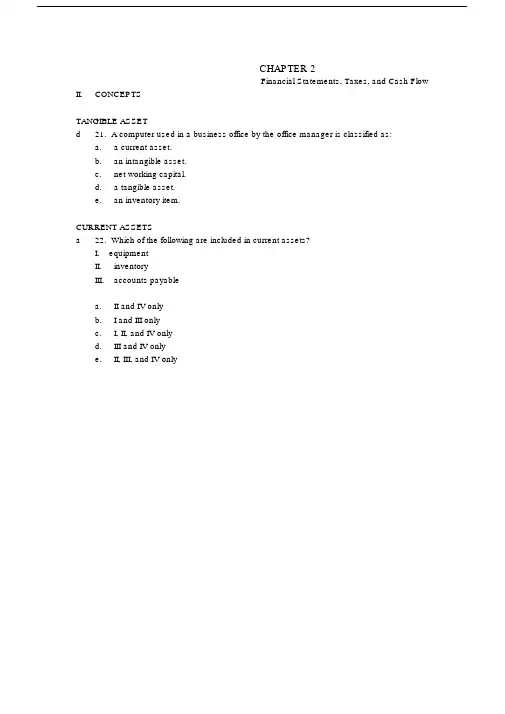

CHAPTER 2Financial Statements, Taxes, and Cash Flow II.CONCEPTSTANGIBLE ASSETd21. A computer used in a business office by the office manager is classified as:a. a current asset.b.an intangible asset. working capital.d. a tangible asset.e.an inventory item.CURRENT ASSETSa22. Which of the following are included in current assets?I. equipmentII.inventoryIII.accounts payablea.II and IV onlyb.I and III onlyc.I, II, and IV onlyd.III and IV onlye.II, III, and IV onlyCURRENT LIABILITIESb23.Which of the following are included in current liabilities?I.note payable to a supplier in eighteen monthsII.debt payable to a mortgage company in nine monthsIII.accounts payable to suppliersa.I and III onlyb.II and III onlyc.III and IV onlyd.II, III, and IV onlye.I, II, and III onlyNET WORKING CAPITALc24. Which one of the following statements concerning net working capital is correct? working capital is negative when current assets exceed current liabilities. working capital includes cash, accounts receivables, fixed assets, andaccounts payable.c.Inventory is a part of net working capital.d.The change in net working capital is equal to the beginning net workingcapital minus the ending net working capital. working capital includes accounts from the income statement.NET WORKING CAPITALa25. Which one of the following statements concerning net working capital is correct?a.The greater the net working capital, the greater the ability of a firm to meetits short-term obligations.b.The change in net working capital is equal to current assets minus current liabilities.c.Depreciation must be added back to current assets when computing the change innet working capital. working capital is equal to long-term assets minus long-term liabilities. working capital is a part of the operating cash flow.BALANCE SHEETd26. An increase in total assets:a.means that net working capital is also increasing.b.requires an investment in fixed assets.c.means that shareholders’ equity must also increase.d.must be offset by an equal increase in liabilities and shareholders ’equity.e.can only occur when a firm has positive net income.LIQUIDITYc27. Which one of the following accounts is the most liquid?a.inventoryb.buildingc.accounts receivabled.equipmente.patentBALANCE SHEETb28. Which of the following accounts generally increase in value when a firm sellssharesof its common stock at a price in excess of par value?I. retained earningsII.paid-in surplusmon stocka.I and II onlyb.II and III onlyc.III and IV onlyd.I, II, and III onlye.II, III, and IV onlyLIQUIDITYe29. Which one of the following statements concerning liquidity is correct?a.If you can sell an asset today, it is a liquid asset.b.If you can sell an asset next year at a price equal to its actual value, the asset ishighly liquid.c.Trademarks and patents are highly liquid.d.The less liquidity a firm has, the lower the probability the firm will encounterfinancialdifficulties.e.Balance sheet accounts are listed in order of decreasing liquidity.LIQUIDITYd30.Liquidity is:a. a measure of the use of debt in a firm structure’capital.b.equal to current assets minus current liabilities.c.equal to the market value of a firm’ s total assets minus its current liabilities.d.valuable to a firm even though liquid assets tend to be less profitable to own.e.generally associated with intangible assets.SHAREHOLDERS’EQUITYd31. Which of the following accounts are included in shareholders ’equity?I.interest paidII.retained earningsIII.paid in surplusIV. long-term debta.I and II onlyb.II and IV onlyc.I and IV onlyd.II and III onlye.I and III onlyf.SHAREHOLDERS’EQUITYc32. Shareholders ’ equity:a.includes common stock, paid in surplus, retained earnings, and long-term debt.b.on a balance sheet is equivalent to the market value of the outstanding sharesof stock.c.includes all of a firm’ s earnings retained by the firm to date.d.increases, all else equal, when the dividends paid are greater than the netincome for a year.e.includes the book value of any bonds issued by the firm.FINANCIAL LEVERAGEb33. The higher the degree of financial leverage employed by a firm, the:a.lower the probability that the firm will encounter financial distress.b.greater the amount of debt incurred.c.greater the number of shares of common stock issued.d.greater the cash flow to creditors each year.e.lower the potential gains to shareholders.BOOK VALUEb34. Book value:a.is equivalent to market value for firms with fixed assets.b.is based on historical cost.c.generally tends to exceed market value when fixed assets are included.d.is more of a financial than an accounting valuation.e.is adjusted to market value whenever the market value exceeds the stated bookvalue.MARKET VALUEa35. When making financial decisions related to assets, you should:a.always consider market values.b.place more emphasis on book values than on market values.c.rely primarily on the value of assets as shown on the balance sheet.d.place primary emphasis on historical costs.e.only consider market values if they are less than book values.INCOME STATEMENTd36. As seen on an income statement:a.interest is deducted from income and increases the total taxes incurred.b.the tax rate is applied to the earnings before interest and taxes when the firm hasboth depreciation and interest expenses.c.depreciation is shown as an expense but does not affect the taxes payable.d.depreciation reduces both the taxable income and the net income.e.interest expense is added to earnings before interest and taxes to gettaxable income.EARNINGS PER SHAREa37. The earnings per share will:a.increase as net income increases.b.increase as the number of shares outstanding increase.c.decrease as the total revenue of the firm increases.d.increase as the tax rate increases.e.decrease as the costs decrease.DIVIDENDS PER SHAREe38. Dividends per share:a.increase as the net income increases as long as the number of sharesoutstanding remains constant.b.decrease as the number of shares outstanding decrease, all else constant.c.are inversely related to the earnings per share.d.are based upon the dividend requirements established by Generally AcceptedAccounting Procedures.e.are equal to the amount of net income distributed to shareholders divided by thenumber of shares outstanding.REALIZATION PRINCIPLEb39. According to Generally Accepted Accounting Principles,a.income is recorded based on the matching principle.b.income is recorded based on the realization principle.c.costs are recorded based on the liquidity principle. income is recorded based on the realization principle.e.depreciation is recorded as it affects the cash flows of a firm.MATCHING PRINCIPLEc40. According to Generally Accepted Accounting Principles, costs are:a.recorded as incurred.b.recorded when paid.c.matched with revenues.d.matched with production levels.e.expensed as management desires.NONCASH ITEMSa41. Depreciation:a.is a noncash expense that is recorded on the income statement.b.increases the net fixed assets as shown on the balance sheet.c.reduces both the net fixed assets and the costs of a firm.d.is a non-cash expense which increases the net operating income.e.decreases net fixed assets, net income, and operating cash flows.FIXED COSTSc42. Fixed costs in the short-run generally include which of the following?I.manufacturing wagesII.cost of materials used in productionIII.property insurancea.I and II onlyb.II and III onlyc.III and IV onlyd.I and IV onlye.II and IV onlyMARGINAL TAX RATEc43. When you are making a financial decision, the most relevant tax rate is the _____ rate.a.averageb.fixedc.marginald.totale.variableCASH FLOW FROM ASSETSe44. The cash flow from assets is equal to:a.operating cash flow minus the change in net working capital plus net capitalspending.b.cash flow to creditors minus the cash flow to shareholders.c.earnings before interest and taxes plus depreciation plus taxes.d.earnings before interest and taxes plus depreciation plus taxes minus netcapital spending minus the change in net working capital.e.earnings before interest and taxes plus depreciation minus taxes minus net capitalspending minus the change in net working capital.CASH FLOW FROM ASSETSa45. An increase in which one of the following will cause the cash flow from assets to increase?a.depreciationb.change in net working capital working capitald.taxese.costsCASH FLOW FROM ASSETSb46. Cash flow from assets must be negative when:a.the firm has a taxable loss for the year.b.the cash flow from creditors and the cash flow from stockholders are both negative.c.the cash flow from creditors is negative and the cash flow from stockholdersis positive.d.the change in net working capital exceeds the net capital spending.e.operating cash flow is less than the change in net working capital.OPERATING CASH FLOWd47. Assume a firm has depreciation, taxes, and interest expense. In this case, operating cash flow:a.is the same as net income.b.is the same as net income plus depreciation.c.must be positive because depreciation is added to the taxable income.d.can be positive, negative, or equal to zero.e.is equal to the cash flow to creditors.CHANGE IN NET WORKING CAPITALe48. A firm starts its year with a positive net working capital. During the year, the firm acquires more short-term debt than it does short-term assets. This means that:a.the ending net working capital will be negative.b.both accounts receivable and inventory decreased during the year.c.the beginning current assets were less than the beginning current liabilities.d.accounts payable increased and inventory decreased during the year.e.the ending net working capital can be positive, negative, or equal to zero.NET CAPITAL SPENDINGb49. Net capital spending:a.is negative if the sale of fixed assets is greater than the acquisition of current assets.b.is equal to zero if the decrease in the fixed assets account is equal to thedepreciation expense for the period.c.reflects the net changes in total assets over a stated period of time.d.is equivalent to the cash flow from assets.e.is equal to the ending net fixed assets minus the beginning net fixed assets.CASH FLOW TO CREDITORSc50. The cash flow to creditors includes the cash:a.received by the firm when payments are paid to suppliers.b.outflow of the firm when new debt is acquired.c.outflow when interest is paid on outstanding debt.d.inflow when accounts payable decreases.e.received when long-term debt is paid off.CASH FLOW TO STOCKHOLDERSa51. Cash flow to stockholders must be positive when:a.the dividends paid exceed the net new equity raised.b.the net sale of common stock exceeds the amount of dividends paid.c.no income is distributed but new shares of stock are sold.d.both the cash flow to assets and the cash flow to creditors are negative.e.both the cash flow to assets and the cash flow to creditors are positive.III.PROBLEMSCURRENT ASSETSb52. A firm has $300 in inventory, $600 in fixed assets, $200 in accounts receivables, $100 in accounts payable, and $50 in cash. What is the amount of the currentassets?a.$500b.$550c.$600d.$1,150e.$1,200TOTAL LIABILITIESd53. A firm has net working capital of $350. Long-term debt is $600, total assets are $950 and fixed assets are $400. What is the amount of the total liabilities?a.$200b.$400c.$600d.$800e.$1,200SHAREHOLDERS’EQUITYc54. A firm has common stock of $100, paid-in surplus of $300, total liabilities of $400, current assets of $400, and fixed assets of $600. What is the amount of theshareholders ’ equity?a.$200b.$400c.$600d.$800e.$1,000NET WORKING CAPITALb55. The total assets are $900, the fixed assets are $600, long-term debt is $500, and short-term debt is $200. What is the amount of net working capital?a.$0b.$100c.$200d.$300e.$400NET WORKING CAPITALc56. Shareholders ’ equity in a firm is $500. The firm owes a total of $400 of which 75 percent is payable within the next year. The firm has net fixed assets of $600. Whatis the amount of the net working capital?a.-$200b.-$100c.$0d.$100e.$200LIQUIDITYd57. Brad ’ s Co.has equipment with a book value of $500 that could be sold today at a 50 percent discount. Their inventory is valued at $400 and could be sold to a competitorfor that amount. The firm has $50 in cash and customers owe them $300. What is theaccounting value of their liquid assets?a.$50b.$350c.$700d.$750e.$1,000BOOK VALUEc 58. Martha ’ s Enterprises spent $2,400 to purchase equipment three years ago. Thisequipment is currently valued at $1,800 on today ’ s balance sheet but could actuallybe sold for $2,000. Net working capital is $200 and long-term debt is $800. What isthe book value of shareholders ’ equity?a. $200b. $800c. $1,200d. $1,400e. The answer cannot be determined from the information provided.MARKET VALUEb59. Recently, the owner of Martha’ s Wares encountered severe legal problems and is trying to sell her business. The company built a building at a cost of $1.2 millionthat is currently appraised at $1.4 million. The equipment originally cost $700,000 andis currently valued at $400,000. The inventory is valued on the balance sheet at$350,000 but has market value of only one-half of that amount. The owner expectsto collect 95 percent of the $200,000 in accounts receivable. The firm has $10,000in cash and owes a total of $1.4 million. The legal problems are personal andunrelated to the actual business. What is the market value of this firm?a.$575,000b.$775,000c.$950,000d.$1,150,000e.$1,175,000NET INCOMEa60. Ivan ’ s, Inc. paid $500 in dividends and600$ in interest this past year. Commonstock increased by $200 and retained earnings decreased by $100. What is the netincome for the year?a.$400b.$500c.$600d.$800e.$1,000NET INCOMEb61. Art ’ s Boutique has sales of $640,000 and costs of $480,000. Interesexpense is $40,000 and depreciation is $60,000. The tax rate is 34%. What is the net income?a.$20,400b.$39,600c.$50,400d.$79,600e.$99,600f.MARGINAL TAX RATEc62. Given the tax rates as shown, what is the average tax rate for a firm with taxable income of $126,500?Taxable Income Tax Rate$ 0 - 50,000 15%50,001 - 75,000 25%75,001 - 100,000 34%100,001 - 335,000 39%a.21.38 percentb.23.88 percentc.25.76 percentd.34.64 percente.39.00 percentTAXESd63.The tax rates are as shown. Your firm currently has taxable income of $79,400.How much additional tax will you owe if you increase your taxable income by$21,000?Taxable Income Tax Rate$ 0 - 50,000 15%50,001 - 75,000 25%75,001 - 100,000 34%100,001 - 335,000 39%a. $7,004b. $7,014c. $7,140d. $7,160e. $7,174EARNINGS BEFORE INTEREST AND TAXESc64. Tim’ s Playhouse paid $155 in dividends and $220 in interest expense. The addition to retained earnings is $325 and net new equity is $50. The tax rate is 25 percent.Sales are $1,600 and depreciation is $160. What are the earnings before interest andtaxes?a.$480b.$640c.$860d.$1,020e.$1,440OPERATING CASH FLOWd65. Your firm has net income of $198 on total sales of $1,200. Costs are $715 and depreciation is $145. The tax rate is 34 percent. The firm does not have interestexpenses. What is the operating cash flow?a.$93b.$241c.$340d.$383e.$485NET CAPITAL SPENDINGc.66. Teddy’ s Pillows has beginning net fixed assets of $480 and ending net fixed assets of$530. Assets valued at $300 were sold during the year. Depreciation was $40. Whatis the amount of net capital spending?a.$10b.$50c.$90d.$260e.$390CHANGE IN NET WORKING CAPITALb67. At the beginning of the year, a firm has current assets of $380 and current liabilities of $210. At the end of the year, the current assets are $410 and the current liabilitiesare $250. What is the change in net working capital?a.-$30b.-$10c.$0d.$10e.$30CASH FLOW TO CREDITORSe68. At the beginning of the year, long-term debt of a firm is $280 and total debt is $340.At the end of the year, long-term debt is $260 and total debt is $350. The interestpaid is $30. What is the amount of the cash flow to creditors?a.-$50b.-$20c.$20d.$30e.$50CASH FLOW TO CREDITORSa69. Pete ’ s Boats has beginn ng long-term debt of $180 and ending long-term debt of $210. The beginning and ending total debt balances are $340 and $360, respectively. Theinterest paid is $20. What is the amount of the cash flow to creditors?a.-$10b.$0c.$10d.$40e.$50CASH FLOW TO STOCKHOLDERSa70. Peggy Grey ’ s Cookies has net income of $360. The firm pays out 40 percent of the net income to its shareholders as dividends. During the year, the company sold $80 worthof common stock. What is the cash flow to stockholders?a.$64b.$136c.$144d.$224e.$296CASH FLOW TO STOCKHOLDERSa71. Thompson’ s Jet Skis has operating cash flow of $218. Depreciation is $45 and interest paid is $35. A net total of $69 was paid on long-term debt. The firm spent$180 on fixed assets and increased net working capital by $38. What is the amountof the cash flow to stockholders?a.-$104b.-$28c.$28d.$114e.$142The following balance sheet and income statement should be used for questions#72 through #80:Nabors, Inc.2005 Income Statement($ in millions)Net sales $9,610Less: Cost of goods sold 6,310Less: Depreciation 1,370Earnings before interest and taxes 1,930Less: Interest paid 630Taxable Income $1,300Less: Taxes 455Net income $ 845Nabors, Inc.2004 and 2005 Balance Sheets($ in millions)2004 2005 2004 2005Cash $ 310 $ 405 Accounts payable $ 2,720 $ 2,570Accounts rec. 2,640 3,055 Notes payable 100 0Inventory 3,275 3,850 Total $ 2,820 $ 2,570Total $ 6,225 $ 7,310 Long-term debt 7,875 8,100Net fixed assets 10,960 10,670 Common stock 5,000 5,250Retained earnings 1,490 2,060Total assets $17,185 $17,980 Total liab.& equity $17,185 $17,980CHANGE IN NET WORKING CAPITALc72. What is the change in the net working capital from 2004 to 2005?a. $1,235b.$1,035c.$1,335d.$3,405e.$4,740NONCASH EXPENSESd73. What is the amount of the non-cash expenses for 2005?a.$570b.$630c.$845d.$1,370e.$2,000NET CAPITAL SPENDINGc74. What is the amount of the net capital spending for 2005?a.-$290b.$795c.$1,080d.$1,660e.$2,165OPERATING CASH FLOWd75. What is the operating cash flow for 2005?a.$845b.$1,930c.$2,215d.$2,845e.$3,060CASH FLOW FROM ASSETSa76. What is the cash flow from assets for 2005?a.$430b.$485c.$1,340d.$2,590e.$3,100NET NEW BORROWINGe77. What is the amount of net new borrowing for 2005?a.-$225b.-$25c.$0d.$25e.$225CASH FLOW TO CREDITORSd78. What is the cash flow to creditors for 2005?a.-$405b.-$225c.$225d.$405e.$630DIVIDENDS PAIDb79. What is the amount of dividends paid in 2005?a.$25b.$275c.$570d.$625e.$845CASH FLOW TO STOCKHOLDERSc80. What is the cash flow to stockholders for 2005?a.-$250b.-$25c.$25d.$250e.$275The following information should be used for questions #81 through #88:Knickerdoodles, Inc.2004 2005Sales $ 740 $ 785COGS 430 460Interest 33 35Dividends 16 17Depreciation 250 210Cash 70 75Accounts receivables 563 502Current liabilities 390 405Inventory 662 640Long-term debt 340 410Net fixed assets 1,680 1,413Common stock 700 235Tax rate 35% 35%NET WORKING CAPITALd81. What is the net working capital for 2005?a.$345b.$405c.$805d.$812e.$1,005CHANGE IN NET WORKING CAPITALa82. What is the change in net working capital from 2004 to 2005?a. -$93b.-$7c.$7d.$85e.$97NET CAPITAL SPENDINGb83. What is net capital spending for 2005?a.-$250b.-$57c.$0d.$57e.$477OPERATING CASH FLOWb84. What is the operating cash flow for 2005?a.$143b.$297c.$325d.$353e.$367CASH FLOW FROM ASSETSd85. What is the cash flow from assets for 2005?a.$50b.$247c.$297d.$447e.$517NET NEW BORROWINGd86. What is net new borrowing for 2005?a.-$70b.-$35c.$35d.$70e.$105CASH FLOW TO CREDITORSb87. What is the cash flow to creditors for 2005?a.-$170b.-$35c.$135d.$170e.$205CASH FLOW TO STOCKHOLDERSd88. What is the cash flow to stockholders for 2005?a.$408b.$417c.$452d.$482e.$503The following information should be used for questions #89 through #91:2005Cost of goods sold $3,210Interest 215Dividends 160Depreciation 375Change in retained earnings 360Tax rate 35%TAXABLE INCOMEe89. What is the taxable income for 2005?a.$360b.$520c.$640d.$780e.$800OPERATING CASH FLOWd90. What is the operating cash flow for 2005?a.$520b.$800c.$1,015d.$1,110e.$1,390SALESc91. What are the sales for 2005?a.$4,225b.$4,385c.$4,600d.$4,815e.$5,000IV. ESSAYSLIQUID ASSETS92.What is a liquid asset and why is it necessary for a firm to maintain a reasonable levelof liquid assets?Liquid assets are those that can be sold quickly with little or no loss in value. A firm that has sufficient liquidity will be less likely to experience financial distress.OPERATING CASH FLOW93.Why is interest expense excluded from the operating cash flow calculation?Operating cash flow is designed to represent the cash flow a firm generates from its day-to-day operating activities. Interest expense arises out of a financing choice and thus should be considered as a cash flow to creditors.CASH FLOW AND ACCOUNTING STATEMENTS94. Explain why the income statement is not a good representation of cash flow.Most income statements contain some noncash items, so these must be accounted for when calculating cash flows. More importantly, however, since GAAP is used to create income statements, revenues and expenses are booked when they accrue, not when their corresponding cash flows occur.BOOK VALUE AND MARKET VALUE95.Discuss the difference between book values and market values on the balance sheetand explain which is more important to the financial manager and why.The accounts on the balance sheet are generally carried at historical cost, not marketvalues. Although the book value of current assets and current liabilities may closelyapproximate market values, the same cannot be said for the rest of the balance sheetaccounts. Ultimately, the financial manager should focus on the firm ’stock price, which isa market value measure. Hence, market values are more meaningful than book values.ADDITION TO RETAINED EARNINGS96.Note that in all of our cash flow computations to determine cash flow from assets,we never include the addition to retained earnings. Why not? Is this an oversight?The addition to retained earnings is not a cash flow. It is simply an accounting entry that reconciles the balance sheet. Any additions to retained earnings will show up as cashflow changes in other balance sheet accounts.DEPRECIATION AND CASH FLOW97.Note that we added depreciation back to operating cash flow and to additions to fixedassets. Why add it back twice? Isn’-counting?thisdoubleIn both cases, depreciation is added back because it was previously subtracted whenobtaining ending balances of net income and fixed assets. Also, since depreciation is a noncash expense, we need to add it back in both instances, so there is no doublecounting.TAX LIABILITIES AND CASH FLOW98.Sometimes when businesses are critically delinquent on their tax liabilities, the taxauthority comes in and literally seizes the business by chasing all of the employees out of the building and changing the locks. What does this tell you about the importance of taxes relative to our discussion of cash flow? Why might a business owner want to avoid such an occurrence?Taxes must be paid in cash, and in this case, they are one of the most importantcomponents of cash flow. The reputation of a business can undergo irreparable harm ifword gets out that the tax authorities have confiscated the business, even if only for acouple of hours until the business owner can come up with the money to clear up the taxproblem. The bottom line is if the owner can ’ t come up with the cash, the tax authority has effectively put them out of business.CASH FLOW FROM ASSETS99.Interpret, in words, what cash flow from assets represents by discussing operating cashflow, changes in net working capital, and additions to fixed assets.Operating cash flow is the cash flow a firm generates from its day-to-day operations. In other words, it is the cash inflow generated as a result of putting the firm ’assets to work.Changes in net working capital and fixed assets represent investments a firm makes in these assets. That is, a firm typically takes some of the cash flow it generates from using assets and reinvests it in new assets. Cash flow from assets, then, is the cash flow a firm generates by employing its assets, net of any acquisitions.。

财务管理专业英语体目标而进行的涉及到获取、融资和资产管理的综合决策过程。

Decisions involving a firm’s short-term assets and liabilities refer to working capital management. 决断涉及一个公司的短期的资产和负债提到营运资金管理The firm’s long-term financing decisions concern the right-hand side of the balance sheet. 该公司的长期融资决断股份资产负债表的右边。

This is an important decision as the legal structure affects the financial risk faced by the owners of the company. 这是一个重要的决定作为法律结构影响金融风险面对附近的的业主的公司。

The board includes some members of top management(executiveencompasses all financial claimholders including common stockholders, debt holders, and preferred stockholders. 股东财富最大化只集中于股东,而企业价值最大化包含所有的财务债券持有者,包括普通股股东,债权人和优先股股东。

Given these assumptions,sha reholders’ wealth maximization is consistent with the best interests of stakeholders and society in the long run。

根据这些假设,从长期来看,股东财富最大化与利益相关者和社会的最好利润是相一致的。

{财务管理财务会计}会计专业英语习题答案Chapter.11-1Asinmanyethicsissues,thereisnoonerightanswer.Thelocalnewsp aperreportedonthisissueintheseterms:"Thepanycoveredupthefi rstreport,andthelocalnewspaperuncoveredthepany'ssecret.The panywasforcedtonotlocatehere(CollierCounty).Itbecamepatent lyclearthatdoingtheleastthatislegallyallowedisnotenough." 1-21.B2.B3.E4.F5.B6.F7.X8.E9.X10.B1-3a.$96,500($25,000+$71,500)b.$67,750($82,750–$15,000)c.$19,500($37,000–$17,500)1-4a.$275,000($475,000–$200,000)b.$310,000($275,000+$75,000–$40,000)c.$233,000($275,000–$15,000–$27,000)d.$465,000($275,000+$125,000+$65,000)ine:$45,000($425,000–$105,000–$275,000)1-5a.owner'sequityb.liabilityc.assetd.assete.owner'sequityf.a sset1-6a.Increasesassetsandincreasesowner’sequity.b.Increasesassetsandincreasesowner’sequity.c.Decreasesassetsanddecreasesowner’sequity.d.Increasesassetsandincreasesliabilities.e.Increasesassetsanddecreasesassets.1-71.increase2.decrease3.increase4.decrease1-8a.(1)Saleofcateringservicesforcash,$25,000.(2)Purchaseoflandforcash,$10,000.(3)Paymentofexpenses,$16,000.(4)Purchaseofsuppliesonaccount,$800.(5)Withdrawalofcashbyowner,$2,000.(6)Paymentofcashtocreditors,$10,600.(7)Recognitionofcostofsuppliesused,$1,400.b.$13,600($18,000–$4,400)c.$5,600($64,100–$58,500)d.$7,600($25,000–$16,000–$1,400)e.$5,600($7,600–$2,000)1-9 Itwouldbeincorrecttosaythatthebusinesshadincurredanetlos sof$21,750.Theexcessofthewithdrawalsoverthenetinefortheper iodisadecreaseintheamountofowner’sequityinthebusiness.1-10Balancesheetitems:1,3,4,8,9,101-11Inestatementitems:2,5,6,71-12MADRASCOMPANYStatementofOwner’sEquityFortheMonthEndedApril30,2006LeoPerkins,capital,April1,2006$297,200 Netineforthemonth$73,000 Lesswithdrawals..................12,000 Increaseinowner’sequity.........61,000LeoPerkins,capital,April30,2006$358,2001-13HERCULESSERVICESIneStatementFortheMonthEndedNovember30,2006Feesearned$232,120Operatingexpenses:Wagesexpense$100,100Rentexpense35,000Suppliesexpense4,550 Miscellaneousexpense..............3,150 Totaloperatingexpenses..........142,800Netine$..........................89,3201-14Balancesheet:b,c,e,f,h,i,j,l,m,n,oInestatement:a,d,g,k1-151.b–investingactivity2.a–operatingactivity3.c–financingactivity4.a–operatingactivity1-16a.2003:$10,209($30,011–$19,802)2002:$8,312($26,394–$18,082)b.2003:0.52($10,209÷$19,802)2002:0.46($8,312÷$18,082)c.Theratioofliabilitiestostockholders’equityincreasedfrom2002to2003,indicatinganincreaseinriskforcreditors.However, theassetsofTheHomeDepotaremorethansufficienttosatisfycredi torclaims.Chapter.22-1AccountAccountNumberAccountsPayable21AccountsReceivable12Cash11CoreyKrum,Capital31CoreyKrum,Drawing32FeesEarned41Land13MiscellaneousExpense53SuppliesExpense52WagesExpense512-2Balance Sheet Accounts Ine Statement Accounts1.Assets 11Cash 12AccountsReceivable 13Supplies14PrepaidInsurance15Equipment2.Liabilities21AccountsPayable22UnearnedRent3.Owner's Equity31MillardFillmore,Capital 32MillardFillmore,Drawing 4.Revenue41FeesEarned5.Expenses51WagesExpense52RentExpense53SuppliesExpense59MiscellaneousExpense2-3a.andb.Account Debited Account Credited TransactionTypeEffectTypeEffect(1)asset+owner'sequity+(2)asset+asset–(3)asset+asset–liability+(4)expense+asset–(5)asset+revenue+(6)liability–asset–(7)asset+asset–(8)drawing+asset–(9)expense+asset–Ex.2–4(1)Cash40,000IraJanke,Capital40,000 (2)Supplies1,800Cash1,800(3)Equipment24,000 AccountsPayable15,000Cash9,000(4)OperatingExpenses3,050 Cash3,050(5)AccountsReceivable12,000 ServiceRevenue12,000(6)AccountsPayable7,500 Cash7,500(7)Cash9,500 AccountsReceivable9,500 (8)IraJanke,Drawing5,000 Cash5,000(9)OperatingExpenses1,050 Supplies1,0502-51.debitandcredit(c)2.debitandcredit(c)3.debitandcredit(c)4.creditonly(b)5.debitonly(a)6.debitonly(a)7.debitonly(a)2-6a.Liability—creditf.Revenue—creditb.Asset—debitg.Asset—debitc.Asset—debith.Expense—debitd.Owner'sequityi.Asset—debit (CindyYost,Capital)—creditj.Expense—debite.Owner'sequity(CindyYost,Drawing)—debit2-7a.creditg.debitb.credith.debitc.debiti.debitd.creditj.credite.debitk.debitf.creditl.credit2-8a.Debit(negative)balanceof$1,500($10,500–$4,000–$8,000).Suchanegativebalancemeansthattheliabilitieso fSeth’sbusinessexceedtheassets.b.Yes.ThebalancesheetpreparedatDecember31willbalanc e,withSethFite,Capital,beingreportedintheowner’seq uitysectionasanegative$1,500.2-9a.Theincreaseof$28,750inthecashaccountdoesnotindicateearningsofthatamount.Earningswillrepresentthenetchangeinallassetsandliabilitiesfromoperatingtransactions.b.$7,550($36,300–$28,750)2-10a.$40,550($7,850+$41,850–$9,150)b.$63,000($61,000+$17,500–$15,500)c.$20,800($40,500–$57,700+$38,000)2-112005Aug.1RentExpense1,500Cash1,5002AdvertisingExpense700Cash7004Supplies1,050Cash1,0506OfficeEquipment7,500 AccountsPayable7,5008Cash3,600 AccountsReceivable3,60012AccountsPayable1,150 Cash1,15020GayleMcCall,Drawing1,000 Cash1,00025MiscellaneousExpense500 Cash50030UtilitiesExpense195 Cash19531AccountsReceivable10,150 FeesEarned10,15031UtilitiesExpense380 Cash3802-12a.JOURNALPage43Post.DateDescriptionRef.DebitCredit2006Oct.27Supplies151,320 AccountsPayable211,320 Purchasedsuppliesonaccount.b.,c.,d.Supplies15Post.Balance DateItemRef.Dr.Cr.Dr.Cr.2006Oct.1Balance✓58527431,3201,905AccountsPayable212006Oct.1Balance✓6,15027431,3207,4702-13 Inequalityoftrialbalancetotalswouldbecausedbyerrors describedin(b)and(d).2-14ESCALADECO.TrialBalanceDecember31,2006Cash13,375AccountsReceivable24,600PrepaidInsurance8,000Equipment75,000AccountsPayable11,180UnearnedRent4,250ErinCapelli,Capital82,420ErinCapelli,Drawing10,000ServiceRevenue83,750WagesExpense42,000AdvertisingExpense7,200 MiscellaneousExpense..............1,425181,600181,6002-15a.GeraldOwen,Drawing15,000WagesExpense15,000b.PrepaidRent4,500Cash4,5002-16题目的资料不全,答案略.2-17a.KMARTCORPORATIONIneStatementFortheYearsEndingJanuary31,2000and1999 (inmillions)Increase (Decrease)20001999AmountPercent1.Sales$37,028$35,925$1,1033.1%2.Costofsales(29,658)(28,111)1,5475.5%3.Selling,general,andadmin. expenses..............(7,415)(6,514)90113.8%4.Operatingine(loss)beforetaxes$............(45)$1,300$(1,345)(103.5%) b.ThehorizontalanalysisofKmartCorporationrevealsdet erioratingoperatingresultsfrom1999to2000.Whilesales increasedby$1,103million,a3.1%increase,costofsalesincreasedby$1,547million,a5.5%increase.Selling,gener al,andadministrativeexpensesalsoincreasedby$901mill ion,a13.8%increase.Theendresultwasthatoperatingined ecreasedby$1,345million,overa100%decrease,andcreate da$45millionlossin2000.Littleoverayearlater,Kmartfi ledforbankruptcyprotection.Ithasnowemergedfrombankr uptcy,hopingtoreturntoprofitability.3-11.Accruedexpense(accruedliability)2.Deferredexpense(prepaidexpense)3.Deferredrevenue(unearnedrevenue)4.Accruedrevenue(accruedasset)5.Accruedexpense(accruedliability)6.Accruedexpense(accruedliability)7.Deferredexpense(prepaidexpense)8.Deferredrevenue(unearnedrevenue)3-2SuppliesExpense801Supplies8013-3$1,067($118+$949)3-4a.Insuranceexpense(orexpenses) inewillbeoverstated.b.Prepaidinsurance(orassets)willbeoverstated.Owner ’sequitywillbeoverstated.3-5a.InsuranceExpense1,215PrepaidInsurance1,215b.InsuranceExpense1,215PrepaidInsurance1,2153-6UnearnedFees9,570FeesEarned9,5703-7a.SalaryExpense9,360SalariesPayable9,360b.SalaryExpense12,480SalariesPayable12,4803-8$59,850($63,000–$3,150)3-9$195,816,000($128,776,000+$67,040,000)3-10Error(a)Error(b)Over-Under-Over-Under-statedstatedstatedstated1.Revenuefortheyearwouldbe$0$6,900$0$02.Expensesfortheyearwouldbe0003,740inefortheyearwouldbe06,9003,74004.AssetsatDecember31wouldbe00005.LiabilitiesatDecember31wouldbe6,900003,7406.Owner’sequityatDecember31wouldbe06,9003,74003-11$175,840($172,680+$6,900–$3,740)3-12a.AccountsReceivable11,500FeesEarned11,500b.No.Ifthecashbasisofaccountingisused,revenuesarere cognizedonlywhenthecashisreceived.Therefore,earnedb utunbilledrevenueswouldnotberecognizedintheaccounts ,andnoadjustingentrywouldbenecessary.3-13a.Feesearned(orrevenues)inewilb.Accounts(fees)receivable(orassets)willbeunderstat ed.Owner’sequitywillbeunderstated.3-14DepreciationExpense5,200 AccumulatedDepreciation5,2003-15a.$204,600($318,500–$113,900)b.No.Depreciationisanallocationofthecostoftheequipm enttotheperiodsbenefitingfromitsuse.Itdoesnotnecess arilyrelatetovalueorlossofvalue.3-16a.$2,268,000,000($5,891,000,000–$3,623,000,000)b.No.Depreciationisanallocationmethod,notavaluation method.Thatis,depreciationallocatesthecostofafixeda ssetoveritsusefullife.Depreciationdoesnotattempttom easuremarketvalues,whichmayvarysignificantlyfromyea rtoyear.3-17a.DepreciationExpense7,500 AccumulatedDepreciation7,500b.(1)inewo(2)Accumulateddepreciationwouldbeunderstated,andtot alassetswouldbeoverstated.Owner’sequitywouldbeover stated.3-181.AccountsReceivable4FeesEarned42.SuppliesExpense3Supplies33.InsuranceExpense8PrepaidInsurance84.DepreciationExpense5 AccumulatedDepreciation—Equipment55.WagesExpense1WagesPayable13-19a.DellComputerCorporationAmount PercentNetsales$35,404,000100.0Costofgoodssold(29,055,000)82.1 Operatingexpenses(3,505,000)9.9 Operatingine(loss)$2,844,0008.0b.GatewayInc.Amount PercentNetsales$4,171,325100.0Costofgoodssold(3,605,120)86.4 Operatingexpenses(1,077,447)25.8 Operatingine(loss)$(511,242)(12.2)c.DellismoreprofitablethanGateway.Specifically,Dell ’scostofgoodssoldof82.1%issignificantlyless(4.3%)t hanGateway’scostofgoodssoldof86.4%.Inaddition,Gate way’soperatingexpensesareoverone-fourthofsales,whi leDell’soperatingexpensesare9.9%ofsales.Theresulti sthatDellgeneratesanoperatingineof8.0%ofsales,while Gatewaygeneratesalossof12.2%ofsales.Obviously,Gatew aymustimproveitsoperationsifitistoremaininbusinessa ndremainpetitivewithDell.4-1e,c,g,b,f,a,d4-2a.Inestatement:3,8,9b.Balancesheet:1,2,4,5,6,7,104-3a.Asset:1,4,5,6,10b.Liability:9,12c.Revenue:2,7d.Expense:3,8,114-41.f2.c3.b4.h5.g6.j7.a8.i9.d10.e4–5ITHACASERVICESCO.WorkSheet FortheYearEndedJanuary31,2006 AdjustedTrial BalanceAdjustmentsTrial Balance AccountTitleDr.Cr.Dr.Cr.Dr.Cr.1Cash8812AccountsReceivable50(a)75723Supplies8(b)5334PrepaidInsurance12(c)6645Land505056Equipment323267Accum.Depr.—Equip.2(d)5778AccountsPayable262689WagesPayable0(e)11910TerryDagley,Capital011TerryDagley,Drawing881112FeesEarned60(a)7671213WagesExpense16(e)1171314RentExpense881415InsuranceExpense0(c)661516UtilitiesExpense661617DepreciationExpense0(d)551718SuppliesExpense0(b)551819MiscellaneousExpense2219 20Totals20021321320 ContinueITHACASERVICESCO.WorkSheet FortheYearEndedJanuary31,2006 AdjustedIneBalanceTrial BalanceStatement Sheet AccountTitleDr.Cr.Dr.Cr.Dr.Cr. 1Cash8812AccountsReceivable575723Supplies3334PrepaidInsurance6645Land505056Equipment323267Accum.Depr.—Equip.7778AccountsPayable262689WagesPayable11910TerryDagley,Capital011TerryDagley,Drawing881112FeesEarned67671213WagesExpense17171314RentExpense881415InsuranceExpense661516UtilitiesExpense661617DepreciationExpense551718SuppliesExpense551819MiscellaneousExpense2219 20Totals21321Netine(loss)181821 226767164164224-6ITHACASERVICESCO.IneStatementFortheYearEndedJanuary31,2006 Feesearned$67Expenses:Wagesexpense$17Rentexpense8Insuranceexpense6Utilitiesexpense6Depreciationexpense5Suppliesexpense5 Miscellaneousexpense (2)Totalexpenses (49)Netine$18ITHACASERVICESCO.StatementofOwner’sEquityFortheYearEndedJanuary31,2006 TerryDagley,capital,February1,2005$112 Netinefortheyear$18 Lesswithdrawals (8)Increaseinowner’sequity (10)TerryDagley,capital,January31,2006$122 ITHACASERVICESCO.BalanceSheetJanuary31,2006AssetsLiabilitiesCurrentassets:Currentliabilities:Cash$8Accountspayable$26 Accountsreceivable57Wagespayable1 Supplies3Totalliabilities$27 Prepaidinsurance6Totalcurrentassets$74Property,plant,andOwner’s Equity equipment:TerryDagley,capital122Land$50Equipment$32Lessaccum.depr (725)Totalproperty,plant,andequipment75Totalliabilitiesand Totalassets$149owner’sequity$149 4-72006Jan.31AccountsReceivable7 FeesEarned731SuppliesExpense5Supplies531InsuranceExpense6 PrepaidInsurance631DepreciationExpense5 AccumulatedDepreciation—Equipment5 31WagesExpense1WagesPayable14-82006Jan.31FeesEarned67IneSummary6731IneSummary49WagesExpense17RentExpense8InsuranceExpense6UtilitiesExpense6 DepreciationExpense5SuppliesExpense5 MiscellaneousExpense231IneSummary18TerryDagley,Capital1831TerryDagley,Capital8TerryDagley,Drawing84-9SIROCCOSERVICESCO.IneStatementFortheYearEndedMarch31,2006 Servicerevenue$103,850 Operatingexpenses:Wagesexpense$56,800Rentexpense21,270Utilitiesexpense11,500 Depreciationexpense8,000 Insuranceexpense4,100 Suppliesexpense3,100 Miscellaneousexpense..............2,250 Totaloperatingexpenses..........107,020Netloss$ (3,170)4-10SYNTHESISSYSTEMSCO.StatementofOwner’sEquity FortheYearEndedOctober31,2006SuzanneJacob,capital,November1,2005$173,750 Netineforyear$44,250 Lesswithdrawals..................12,000 Increaseinowner’sequity.........32,250 SuzanneJacob,capital,October31,2006$206,0004-11a.Currentasset:1,3,5,6b.Property,plant,andequipment:2,44-12 Sincecurrentliabilitiesareusuallyduewithinoneyear,$ 165,000($13,750×12months)wouldbereportedasacurrentl iabilityonthebalancesheet.Theremainderof$335,000($5 00,000–$165,000)wouldbereportedasalong-termliabilityontheb alancesheet.4-13TUDORCO.BalanceSheetApril30,2006AssetsLiabilities CurrentassetsCurrentliabilities:Cash$31,500Accountspayable$9,500 Accountsreceivable21,850Salariespayable1,750 Supplies1,800Unearnedfees1,200 Prepaidinsurance7,200Totalliabilities$12,450 Prepaidrent4,800Totalcurrentassets$67,150Owner’s Equity Property,plant,andequipment:VernonPosey,capital114, 200Equipment$80,600Lessaccumulateddepreciation21,10059,500Totalliabili tiesandTotalassets$126,650owner’sequity$126,6504-14AccountsReceivable4,100FeesEarned4,100SuppliesExpense1,300Supplies1,300InsuranceExpense2,000PrepaidInsurance2,000DepreciationExpense2,800 AccumulatedDepreciation—Equipment2,800 WagesExpense1,000WagesPayable1,000UnearnedRent2,500RentRevenue2,5004-15c.DepreciationExpense—Equipmentg.FeesEarnedi.SalariesExpensel.SuppliesExpense4-16 Theinesummaryaccountisusedtoclosetherevenueandexpen seaccounts,anditaidsindetectingandcorrectingerrors. The$450,750representsexpenseaccountbalances,andthe$ 712,500representsrevenueaccountbalancesthathavebeen closed.4-17a.IneSummary167,550SueAlewine,Capital167,550SueAlewine,Capital25,000SueAlewine,Drawing25,000b.$284,900($142,350+$167,550–$25,000)4-18a.AccountsReceivableb.AccumulatedDepreciationc.Cashe.Equipmentf.EstellaHall,Capitali.Suppliesk.WagesPayable4-19a.1Workingcapital($143,034)($159,453)Currentratio0.810.80b.7ElevenhasnegativeworkingcapitalasofDecember31,20 02and2001.Inaddition,thecurrentratioisbelowoneatthe endofbothyears.Whiletheworkingcapitalandcurrentrati oshaveimprovedfrom2001to2002,creditorswouldlikelybe concernedabouttheabilityof7Eleventomeetitsshort-ter mcreditobligations.Thisconcernwouldwarrantfurtherin vestigationtodeterminewhetherthisisatemporaryissue( forexample,anend-of-the-periodphenomenon)andthepany’splanstoaddressitsworkingcapitalshortings. 4-20a.(1)SalesSalariesExpense6,480 SalariesPayable6,480(2)AccountsReceivable10,250FeesEarned10,250b.(1)SalariesPayable6,480 SalesSalariesExpense6,480(2)FeesEarned10,250AccountsReceivable10,2504-21a.(1)Payment(lastpaydayinyear)(2)Adjusting(accrualofwagesatendofyear)(3)Closing(4)Reversing(5)Payment(firstpaydayinfollowingyear)b.(1)WagesExpense45,000Cash45,000(2)WagesExpense18,000WagesPayable18,000(3)IneSummary1,120,800WagesExpense1,120,800(4)WagesPayable18,000WagesExpense18,000(5)WagesExpense43,000Cash43,000Chapter6(找不到答案,自己处理了哦)Ex.8–1a.Inappropriate.SinceFridleyhasalargenumberofcredit salessupportedbypromissorynotes,anotesreceivableled gershouldbemaintained.Failuretomaintainasubsidiaryl edgerwhenthereareasignificantnumberofnotesreceivabl etransactionsviolatestheinternalcontrolproceduretha tmandatesproofsandsecurity.Maintaininganotesreceiva bleledgerwillallowFridleytooperatemoreefficientlyan dwillincreasethechancethatFridleywilldetectaccounti ngerrorsrelatedtothenotesreceivable.(Thetotalofthea ccountsinthenotesreceivableledgermustmatchthebalanc eofnotesreceivableinthegeneralledger.)b.Inappropriate.Theprocedureofproperseparationofdut iesisviolated.Theaccountsreceivableclerkisresponsib lefortoomanyrelatedoperations.Theclerkalsohasbothcu stodyofassets(cashreceipts)andaccountingresponsibil itiesforthoseassets.c.Appropriate.Thefunctionsofmaintainingtheaccountsr eceivableaccountinthegeneralledgershouldbeperformed bysomeoneotherthantheaccountsreceivableclerk.d.Appropriate.Salespersonsshouldnotberesponsiblefor approvingcredit.e.Appropriate.Apromissorynoteisaformalcreditinstrum entthatisfrequentlyusedforcreditperiodsover45days. Ex.8–2-aa.Customer Due DateNumber of Days Past Due JanzenIndustriesAugust2993days(2+30+31+30) KuehnCompanySeptember388days(27+31+30)MauerInc.October2140days(10+30) PollackCompanyNovember237days SimrillCompanyDecember3NotpastdueEx.8–3Nov.30UncollectibleAccountsExpense53,315* AllowancesforDoubtfulAccounts53,315*$60,495–$7,180=$53,315Ex.8–4Estimated Uncollectible Accounts AgeIntervalBalancePercentAmountNotpastdue$450,0002%$9,0001–30dayspastdue110,00044,40031–60dayspastdue51,00063,06061–90dayspastdue12,500202,50091–180dayspastdue7,500604,500Over180dayspastdue5,500804,400Total$636,500$27,860Ex.8–52006Dec.31UncollectibleAccountsExpense29,435* AllowanceforDoubtfulAccounts29,435*$27,860+$1,575=$29,435Ex.8–6a.$17,875c.$35,750b.$13,600d.$41,450Ex.8–7a.AllowanceforDoubtfulAccounts7,130 AccountsReceivable7,130b.UncollectibleAccountsExpense7,130 AccountsReceivable7,130Ex.8–8Feb.20AccountsReceivable—DarleneBrogan12,100Sales12,10020CostofMerchandiseSold7,260 MerchandiseInventory7,260May30Cash6,000 AccountsReceivable—DarleneBrogan6,00030AllowanceforDoubtfulAccounts6,100 AccountsReceivable—DarleneBrogan6,100Aug.3AccountsReceivable—DarleneBrogan6,100 AllowanceforDoubtfulAccounts6,1003Cash6,100 AccountsReceivable—DarleneBrogan6,100Ex.8–9$223,900[$212,800+$112,350–($4,050,000×21/2%)] Ex.8–10Due DateInteresta.Aug.31$120b.Dec.28480c.Nov.30250d.May5150e.July19100Ex.8–11a.August8b.$24,480c.(1)NotesReceivable24,000 AccountsRec.—MagpieInteriorDecorators24,000(2)Cash24,480NotesReceivable24,000InterestRevenue480Ex.8–121.Saleonaccount.2.Costofmerchandisesoldforthesaleonaccount.3.Asalesreturnorallowance.4.Costofmerchandisereturned.5.Notereceivedfromcustomeronaccount.6.Notedishonoredandchargedmaturityvalueofnotetocust omer’saccountreceivable.7.Paymentreceivedfromcustomerfordishonorednoteplusi nterestearnedafterduedate.Ex.8–132005Dec.13NotesReceivable25,000 AccountsReceivable—VisageCo.25,00031InterestReceivable75*InterestRevenue7531InterestRevenue75IneSummary752006Apr.12Cash25,500NotesReceivable25,000InterestReceivable75InterestRevenue425*$25,000×0.06×18/360=$75Ex.8–14Mar.1NotesReceivable15,000 AccountsReceivable—AbsarokaCo.15,00018NotesReceivable12,000 AccountsReceivable—SturgisCo.12,000Apr.30AccountsReceivable—AbsarokaCo.15,125 NotesReceivable15,000InterestRevenue125June16AccountsReceivable—SturgisCo.12,270 NotesReceivable12,000InterestRevenue270July11Cash15,367 AccountsReceivable—AbsarokaCo.15,125 InterestRevenue242**$15,125×0.08×72/360=$242Oct.12AllowanceforDoubtfulAccounts12,270 AccountsReceivable—SturgisCo.12,270Ex.8–151.Theinterestreceivableshouldbereportedseparatelyas acurrentasset.Itshouldnotbedeductedfromnotesreceiva ble.2.Theallowancefordoubtfulaccountsshouldbedeductedfr omaccountsreceivable. Acorrectedpartialbalancesheetwouldbeasfollows: PEMBROKECOMPANYBalanceSheetJuly31,2006AssetsCurrentassets:Cash$43,750Notesreceivable300,000Accountsreceivable$576,180 Lessallowancefordoubtfulaccounts71,200504,980 Interestreceivable18,000Ex.8–16a.2003:53.0{$9,953,530÷[($216,200+$159,477)÷2]}2002:44.8{$9,518,231÷[($159,477+$265,515)÷2]}b.Theaccountsreceivableturnoverindicatesanincreasei ntheefficiencyofcollectingaccountsreceivablebyincre asingfrom44.8to53.0,afavorabletrend.Beforereachinga moredefinitiveconclusion,theratiosshouldbeparedwith industryaveragesandsimilarfirms.AppendixEx.8–17a.$20,300b.60daysc.$271($20,300×0.08×60/360)d.$20,029($20,300–$271)e.Cash20,029InterestRevenue29NotesReceivable20,000Ex.9–1 SwitchingtoaperpetualinventorysystemwillstrengthenO nsiteHardware’sinternalcontrolsoverinventory,since thestoremanagerswillbeabletokeeptrackofhowmuchofeac hitemisonhand.Thisshouldminimizeshortagesofgood-sel lingitemsandexcessinventoriesofpoor-sellingitems. Ontheotherhand,switchingtoaperpetualinventorysystem willnoteliminatetheneedtotakeaphysicalinventorycount.Aphysicalinventorymustbetakentoverifytheaccuracyo ftheinventoryrecordsinaperpetualinventorysystem.Ina ddition,aphysicalinventorycountisneededtodetectshor tagesofinventoryduetodamageortheft.Ex.9–2Includeininventory:c,e,g,i Excludefrominventory:a,b,d,f,hEx.9–3a.Balance SheetMerchandiseinventory$1,950understated Currentassets$1,950understatedTotalassets$1,950understatedOwner’sequity$1,950understatedb.Ine StatementCostofmerchandisesold$1,950overstatedGrossprofit$1,950understatedNetine$1,950understatedEx.9–4 Whenanerrorisdiscoveredaffectingthepriorperiod,itsh ouldbecorrected.Inthiscase,themerchandiseinventoryaccountshouldbedebitedandtheowner’scapitalaccountcreditedfor$12,800.Failuretocorrecttheerrorfor2005andpurposelymisstatingtheinventoryandthecostofmerchandisesoldin2006wouldcausethebalancesheetsandtheinestatementsforthetwoyearstonotbeparable.Ex.9–5PortableCDPlayersPurchases CostofMerchandiseSoldInventoryDate Quantity UnitCostTotalCostQuantityUnitCostTotalCost QuantityUnitCostTotalCostApril135501,750 526501,300950450111553795915505345079521935053450159125363628453212853424PortableCDPlayersPurchases CostofMerchandiseSoldInventoryDate Quantity UnitCostTotalCostQuantityUnitCostTotalCost QuantityUnitCostTotalCost30754378875354424378Totalcostofmerchandisesold2,121Inventory,April30:$802($424+$378)Ex.9–6CellPhonesPurchases CostofMerchandiseSoldInventoryDate Quantity UnitCostTotalCostQuantityUnitCostTotalCost QuantityUnitCostTotalCostMar.125902,250 520941,8825902,250CellPhonesPurchases CostofMerchandiseSoldInventoryDate Quantity UnitCostTotalCostQuantityUnitCostTotalCost QuantityUnitCostTotalCost 020941,880918941,69225290942,2501881321894901881,6207906302115951,42571590956301,42531895760779095630665Totalcostofmerchandisesold4,260Inventory,March31:$1,295($630+$665)Ex.9–7a.$700($50×14units)b.$663[($45×5units)+($47×4units)+($50×5units)]Ex.9–8a.$360(8unitsat$33plus3unitsat$32)b.$318(6unitsat$28plus5unitsat$30)c.$341(11unitsat$31;$1,240÷40units=$31) Costofmerchandiseavailableforsale:6unitsat$28$16812unitsat$3036014unitsat$324488unitsat$33 (264)40units(ataveragecostof$31)$1,240Ex.9–91.a.LIFOinventory<(lessthan)FIFOinventoryb.LIFOcostofgoodssold>(greaterthan)FIFOcostofgoodss oldc.LIFOnetine<(lessthan)FIFOnetined.LIFOinetax<(lessthan)FIFOinetax2.Underthelifoconformityruleapanyselectinglifoforta xpurposesmustalsouselifoforfinancialreportingpurpos es.Thus,inperiodsofrisingpricesthereportednetinewou ldbelowerthanwouldbethecaseunderfifo.However,thelow erreportedinewouldalsobeshownonthecorporation’stax return;thus,thereisataxadvantagefromusinglifo.Firmselectingtouselifobelievethetaxadvantagefromusinglif ooutweighsanynegativeimpactfromreportingalowerearni ngsnumbertoshareholders.Lifoissupportedbecausetheta ximpactisarealcashflowbenefit,whilealowerlifoearnin gsnumber(paredtofifo)ismerelytheresultofareportinga ssumption.Ex.9–10UnitUnit TotalInventoryCostMarketLower CommodityQuantityPricePriceCostMarketofCorMM768$150$160$1,200$1,280$1,200T01,5001,4001,400A,7502,6002,600JK1052,5252,6252,525Total$8,725$8,505$8,325Ex.9–11 ThemerchandiseinventorywouldappearintheCurrentAsset ssection,asfollows: Merchandiseinventory—atlowerofcost,fifo,ormarket$8 ,325Alternatively,thedetailsofthemethodofdeterminingcostandthemethodofvaluationcouldbepresentedinanote. Ex.9–12Cost Retail Merchandiseinventory,June1$160,000$180,000 PurchasesinJune(net)680,0001,020,000 Merchandiseavailableforsale$840,000$1,200,000 Ratioofcosttoretailprice:SalesforJune(net)875,000 Merchandiseinventory,June30,atretailprice$ 325,000Merchandiseinventory,June30,atestimatedcost($325,000×70%)$227,500Ex.9–13a.Merchandiseinventory,Jan.1$180,000Purchases(net),Jan.1–May17750,000 Merchandiseavailableforsale$930,000Sales(net),Jan.1–May17$1,250,000 Lessestimatedgrossprofit($1,250,000×35%)437,500 Estimatedcostofmerchandisesold812,500 Estimatedmerchandiseinventory,May17$117,500b.Thegrossprofitmethodisusefulforestimatinginventor iesformonthlyorquarterlyfinancialstatements.Itisalsousefulinestimatingthecostofmerchandisedestroyedbyf ireorotherdisasters.Ex.9–14a.Apple:147.8{$4,139,000,000÷[($45,000,000+$11,000, 000)÷2]}AmericanGreetings:3.1{$881,771,000÷[($278,807,000+$ 290,804,000)÷2]}b.Lower.AlthoughAmericanGreetings’businessisseason alinnature,withmostofitsrevenuegeneratedduringthema jorholidays,muchofitsnonholidayinventorymayturnover veryslowly.Apple,ontheotherhand,turnsitsinventoryov erveryfastbecauseitmaintainsalowinventory,whichallo wsittorespondquicklytocustomerneeds.Additionally,Ap ple’sputerproductscanquicklybeeobsolete,soitcannot riskbuildinglargeinventories.Ex.9–15a.Numberofdays’salesininventory=Albertson’s,=43daysKroger,=40daysSafeway,=42daysInventoryturnover=Albertson’s,=8.2。