Chapter16 Derivatives and hedging activities[40页]

- 格式:ppt

- 大小:135.50 KB

- 文档页数:30

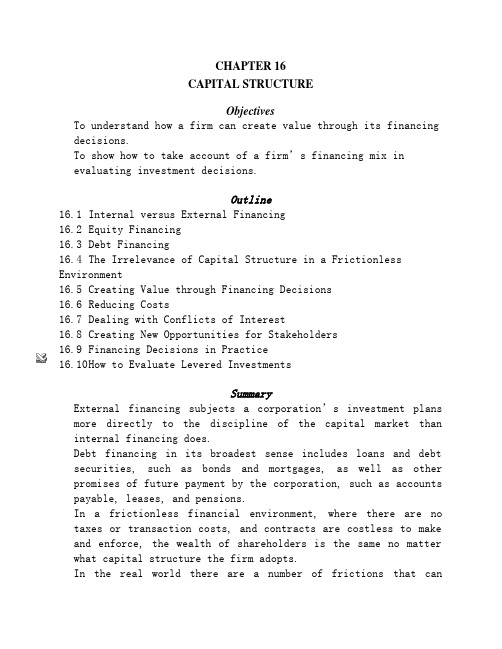

CHAPTER 16CAPITAL STRUCTUREObjectivesTo understand how a firm can create value through its financing decisions.To show how to take account of a firm’s financing mix inevaluating investment decisions.Outline16.1 Internal versus External Financing16.2 Equity Financing16.3 Debt Financing16.4 The Irrelevance of Capital Structure in a Frictionless Environment16.5 Creating Value through Financing Decisions16.6 Reducing Costs16.7 Dealing with Conflicts of Interest16.8 Creating New Opportunities for Stakeholders16.9 Financing Decisions in Practice16.10 H ow to Evaluate Levered InvestmentsSummaryExternal financing subjects a corporation’s investment plans more directly to the discipline of the capital market than internal financing does.Debt financing in its broadest sense includes loans and debt securities, such as bonds and mortgages, as well as other promises of future payment by the corporation, such as accounts payable, leases, and pensions.In a frictionless financial environment, where there are no taxes or transaction costs, and contracts are costless to make and enforce, the wealth of shareholders is the same no matter what capital structure the firm adopts.In the real world there are a number of frictions that cancause capital structure policy to have an effect on the wealth of shareholders. These include taxes, regulations, and conflicts of interest between the stakeholders of the firm. A firm’s management might therefore be able to create shareholder value through its capital structure decisions in one of three ways:By reducing tax costs or the costs of burdensome regulations.By reducing potential conflicts of interest among various stakeholders in the firm.By providing stakeholders with financial assets not otherwise available to them.There are three alternative methods used in estimating the net present value of an investment project to take account of financial leverage: the adjusted present value method, theflows to equity method, and the weighted average cost ofcapital methodSolutions to Problems at End of ChapterDebt-Equity Mix1. Divido Corporation is an all-equity financed firm with a total market value of $100 million.The company holds $10 million in cash-equivalents and has $90 million in other assets.There are 1,000,000 shares of Divido common stock outstanding, each with a market price of $100.Divido Corporation has decided to issue $20 million of bonds and to repurchase $20 million worth of its stock.a.What will be the impact on the price of its shares and on thewealth of its shareholders?Why?b.Assume that Divido’s EBIT has an equal probability of being$20 million, or $12 million, or $4million.Show the impact of the financial restructuring on the probability distribution of earnings per share in the absence of taxes.Why does the fact that the equity becomes riskier not necessarily affectshareholder wealth?SOLUTION:a.In an M&M frictionless environment, where there are no taxesand contracts are costless to make and enforce, the wealth of shareholders is the same no matter what capital structure the firm adopts. In such an environment, neither the stock pricenor shareholders’ wealth would be affected. In the real world Divido’s management might be ab le to create shareholder value by issuing debt and repurchasing shares in two ways:By reducing tax costsBy reducing the free cash flow available to management andexposing itself to greater market discipline.b.The formula for EPS without debt is:EPS all equity =EBIT1,000,000 sharesThe interest payments will be $1.2 million per year (.06 x $20 million) regardless of the realized value of EBIT. The number of shares outstanding after exchanging debt for equity will be800,000. EPS with debt is therefore:EPS with debt = Net Earnings= EBIT – $1.2 million800,000 shares 800,000 sharesAlthough the shares of stock become riskier with debt financing, the expected earnings per share go up. In a frictionlessfinancial environment, the net effect is to leave the price of the stock unaffected.Leasing2. Plentilease and Nolease are virtually identical corporations. The only difference between them is that Plentilease leases most of its plant and equipment whereas Nolease buys its plant and equipment and finances it by pare and contrast their market-value balance sheets.SOLUTION:Market-Value Balance Sheets of Nolease and Plentilease Corporationsa.b.The main difference between the bonds and the lease as a form of debt financing is who bears the risk associated with the residual market value of the leased asset at the end of the term of the lease. Since Nolease Corporation has bought itsequipment, it bears this risk. In Plentilease’s case, however, it is the lessor that bears this residual-value risk.Pension Liabilities3. Europens and Asiapens are virtually identical corporations.The only difference between them is that Europens has a completely unfunded pension plan, and Asiapens has a fully funded pension pare and contrast their market-value balance sheets.What difference does the funding status of the pension plan make to the stakeholders of these two corporations?SOLUTION:Balance Sheets of Asiapens and Europens Corporationspens Balance Sheetb.Asiapens has funded its pension plan by issuing bonds andinvesting the funds raised in a segregated pool of pension fund assets. These pension assets take the form of a diversifiedportfolio of stocks and bonds issued by other companies andserve as collateral for the pension benefits promised byAsiapens to its employees. In the case of Europens, there is no segregated pool of pension assets. The pension promises ofEuropens are backed by the assets of the company itself.Therefore, the employees of Asiapens are more secure aboutreceiving their promised pension benefits, since the benefits are collateralized by a more diversified portfolio of assets.In the case of both companies, however, any unfunded pension liability reduces shareholders equity.4. Comfort Shoe Company of England has decided to spin off its Tango Dance Shoe Division as a separate corporation in the United States.The assets of the Tango Dance Shoe Division have the same operating risk characteristics as those of Comfort.The capital structure of Comfort has been 40% debt and 60% equity in terms of marketing values, and is considered by management to be optimal. The required return on Comfort’s assets (if unlevered) is 16% per year, and the interest rate that the firm (and the division) must currently pay on their debt is 10% per year.Sales revenue for the Tango Shoe Division is expected to remain indefinitely at last year’s level of $10 million.Variable costs are 55% of sales.Annual depreciation is $1 million, which is exactly matched each year by new investments.The corporate tax rate is 40%.a.How much is the Tango Shoe Division worth in unlevered form?b.If the Tango Shoe Division is spun off with $5 million in debt,how much would it be worth?c.What rate of return will the shareholders of the Tango ShoeDivision require?d.Show that the market value of the equity of the new firm wouldbe justified by the earnings to the shareholders.SOLUTION:a.The unlevered free cash flow for the Tango Shoe Division wouldbe (in $millions):Sales: $10.0Var. Cost: -5.5Depreciation - 1.0Taxable Income $ 3.5Taxes (@40%) -1.4After-Tax Income $2.1Depreciation 1.0Investment -1.0Free Cash Flow $2.1 millionUnlevered, Tango is worth: $2.1 million / 0.16 = $13.125millionb.If Tango had $5 million of debt, its total value would be:Market Value with Debt = Market Value without Debt + PV ofInterest Tax ShieldV L = V U + T x B= $13.125 + (.4 x 5) = $15.125 millionTango Equity = $15.125 - $5 = $10.125 millionc.Tango’s cost of equity capital would be .1778k e = k + (1-T)(k - r)D/E = .16 + (1-.4)(.16-.10)x 5/10.125= .1778d.The value of the equity should be the present value of theexpected net income discounted at the required rate of return on equity. The expected net income will be the unlevered cash flow less the after-tax cost of the interest of the debt: $2.1 - (.6) (.1 x $5) = $2.1 - $.3 = $1.8 million per year S = $1.8 million / .1778 = $10.125 million5. Based on the above problem, Suppose that Foxtrot Dance Shoes makes custom designed dance shoes and is a competitor of Tango Dance Shoes.Foxtrot has similar risks and characteristics as Tango except that it is completely unlevered.Fearful that Tango Dance Shoes may try to take over Foxtrot in order to controltheir niche in the market, Foxtrot decides to lever the firm to buy back stock.a.If there are currently 500,000 shares outstanding, what is thevalue of Foxtrot’s stock?b.How many shares can Foxtrot buy back and at what value if itis willing to borrow 30% of the value of the firm?c.What if it is willing to borrow 40% of the value of the firm?d.Should Foxtrot borrow more?SOLUTION:a.Current price per share: $13.125 million /.5 million shares =$26.25 per shareb.@30% debtAmount to borrow: 30% of 13.125 million = $3.9375 millionPV of Tax Shield = .4 x $3.9375 million = $1.575 millionValue of levered firm = $13.125 + $1.575 = $14.7 millionValue of equity in levered firm = $14.7 million $3.9375million = $10.7625 millionTo compute the number of shares Foxtrot can repurchase, we need to know the price per share.If Foxtrot can repurchase shares at the existing price of$26.25 then the number of shares retired will be$3.9375 million/$26.25 per share = .15 million shares. This will leave .35 million shares outstanding, and the price of each share will be $10.7625 million/.35 million = $30.75.If the PV of the tax shield gets incorporated in the price of the shares before the repurchase, then the price of the shares will increase by $1.575 million/.5 million = $3.15. So theprice of the repurchased shares will be$26.25 + $3.15 = $29.40.Then the number of shares retired will be $3.9375million/$29.40 per share = 133,929 shares. This will leave366,071 shares outstanding each with a price of $29.40.c.@40% debtAmount to borrow: 40% of $13.125 million = $5.25 millionPV of Tax Shield = .4 x $5.25 million = $2.1 millionValue of levered firm = $13.125 + $2.1 = $15.225 millionValue of equity in levered firm = $15.225 million $5.25 million = $9.975 millionIf Foxtrot can repurchase shares at the existing price of$26.25 then the number of shares retired will be$5.25 million/$26.25 per share = .2 million shares. This will leave .3 million shares outstanding, and the price of eachshare will be $9.975 million/.3 million = $33.25.If the PV of the tax shield gets incorporated in the price of the shares before the repurchase, then the price of the shares will increase by $2.1 million/.5 million = $4.20. So the price of the repurchased shares will be$26.25 + $4.20 = $30.45.Then the number of shares retired will be $5.25million/$30.45 per share = 172,414 shares. This will leave 327,586 sharesoutstanding each with a price of $30.45.d. Foxtrot’s management must trade off the tax savings due toadditional debt financing against the costs of financialdistress that rise with the degree of debt financing.6. Hanna-Charles Company needs to add a new fleet of vehicles for their sales force.The purchasing manager has been working with a local car dealership to get the best value for the company dollar. After some negotiations, a local dealer has offered Hanna-Charles two options:1) a three year lease on the fleet of cars or 2) 15% off the top to purchase outright.Option 2 would cost Hanna-Charles company about 5% less than the lease option in terms of present value.a.What are the advantages and disadvantages of leasing?b.Which option should the purchasing manager at Hanna-Charlespursue and why?SOLUTION:a.Advantages:The lessor bears all the residual-value riskTax BenefitsNo disposal concerns (or resale) when life of equipment is expended.Disadvantages:No ownership while maintaining maintenance responsibilityb.Lease or Buy:Hanna-Charles company should lease. Although they may spendmore with the lease, they do not bear the residual-value risk. 7. Havem and Needem companies are exactly the same differing onlyin their capital structures.Havem is an unlevered firm issuing only stocks whereas Needem issues stocks and bonds. Neither firm pays corporate taxes. Havem pays out all of its yearly earningsin the form of dividends and has 1 million shares outstanding.Its market capitalization rate is 11% and the firm is currently valued at$180 million.Needem is identical except that 40% ofits value is in bonds and has 500,000 shares outstanding. Needem’s bonds are risk free and pay a coupon of 9% per year and are rolled over every year.a.What is the value of Needem’s shares?b.As an investor forecasting the upcoming year, you examineHavem and Needem using three possible states of the economy that are all equally likely: normal, bad, and exceptional.Assuming the earnings will be the same, one half, and one anda half respectively, produce a table that shows the earningsand the earnings per share for both Havem and Needem in all three scenarios.SOLUTION:a.Needem has $72 million in debt and $108 million in equity.Since there are 500,000 shares, the value of each share is $216.b.Expected EBIT = $180 million x 11% = $19.8 million per yearInterest expense for Needem = $72 million x .09 = $6.48 million per yearb EBIT – Interest Expense8. Using the foregoing example, let us now assume that Havem and Needem must pay taxes at the rate of 40% annually.Given the same distribution of possible outcomes as previously:a.What are the possible after-tax cash flows for Havem andNeedem?b.What are the values of the shares?c.If one was not risk averse, which company would that personinvest in?SOLUTION:a.After-tax CF Havem = (1 -Tax Rate) EBIT = Net incomeNet income Needem = (1 -Tax Rate) (EBIT - Int. Pmt.)CF Needem = (1 -Tax Rate) (EBIT) + Tax Rate x Int. PmtCF Needem (bad) = (.60) $9.9 + (.40) x 6.48 = $8.532 millionCF Needem (normal) = (.60) $19.8 + (.40) x 6.48 = $14.472 million CF Needem (except.) = (.60) $29.7 + (.40) x 6.48 = $20.412 millionb.The equity of Havem will be worth $11.88 million /.11 = $108million or $108 per shareThe total value of Needem’s debt + equity will be $108,000,000 + .4 x $72,000,000 = $136.8 million.Needem’s equity will be worth $136,800,000 $72,000,000 =$64.8 million. Since there are .5 million shares of Needem, each will be worth $129.60.c.Needem.9. The Griffey-Lang Food Company faces a difficult problem.In management’s effort to grow the business, they accrued a debt of $150 million while the value of the company is only $125 million. Management must come up with a plan to alleviate the situation in one year or face certain bankruptcy.Also upcoming are labor relations meetings with the union to discuss employee benefits and pension funds. Griffey-Lang at this time has three choices they can pursue: 1) Launch a new, relatively untested productthat if successful (probability of .12) will allow G-L to increase the value of the company to $200 million, 2) Sell off two food production plants in an effort to reduce some of the debt and the value of the company thus making it even (.45 probability of success), or do nothing (probability of failure =1.0).a.As a creditor, what would you like Griffey-Lang to do, and why?b.As an investor?c.As an employee?SOLUTION:a.As a Creditor:Option 2 best suits the creditor. Option 2 allows the creditor to regain some value through the sale of plant and equipment. b.As a shareholder:The shareholders have nothing to lose and everything to gain by taking a big chance with the new product.c.As an Employee:Selling off two production plants will eliminate jobs. Doing nothing means certain bankruptcy and may result in liquidation of the firm and the loss of all the jobs. For the employees, the best choice is option 1.。

A derivative is a security which “derives” its value from another underlying financial instrument, index, or other investment. Derivatives are available based on the performance of stocks, interest rates, currency exchange rates, as well as commodities contracts and various indexes. Derivatives give the buyer greater leverage for a lower cost than purchasing the actual underlying instrument to achieve the same position. For this reason, when used properly, they can serve to “hedge” a portfolio of securities against losses. However, because derivatives have a date of expiration, the level of risk is greatly increased in relation to their term. One of the simplest forms of a derivative is a stock option. A stock option gives the holder the right to buy or sell the underlying stock at a fixed price for a specified period of time. 衍⽣⼯具是⼀种⾦融⼯具,它是从其他原⽣⾦融⼯具如指数衍⽣出来的。

Chapter 16Long-Term FinancingLecture OutlineLong-Term Financing DecisionSources of EquitySources of DebtCost of Debt FinancingMeasuring the Cost of FinancingActual Effects of Exchange Rate Movements on Financing Costs Assessing the Exchange Rate Risk of Debt Financing Use of Exchange Rate ProbabilitiesUse of SimulationReducing Exchange Rate RiskOffsetting Cash InflowsContractsForwardSwapsCurrencyLoansParallelDiversifying Among CurrenciesInterest Rate Risk from Debt FinancingThe Debt Maturity DecisionThe Fixed Versus Floating-rate DecisionHedging With Interest Rate SwapsPlain Vanilla SwapChapter ThemeThis chapter introduces the long-term sources of funds available to MNCs. Should the MNC choose bonds as a medium to attract long-term funds, a currency for denomination must be chosen. This is a critical decision for the MNC. While there is no clear-cut solution, this chapter illustrates how such a problem can be analyzed. A suggested method of presenting this analysis is to run through an example under assumed exchange rates. Then stress that future exchange rates are not known with certainty. Therefore, the firm should consider the possible costs of financing under a variety of exchange rate scenarios.Topics to Stimulate Class Discussion1. Why would U.S. firms consider issuing bonds denominated in a foreign currency?2. What are the desirable characteristics related to a currency’s interest rate (high or low) and value(strong or weak) that would make the currency attractive from a borrower’s perspective?Critical debateAre swaps deceiving the market?Proposition. Yes. Interest rates are charged to firms because the market estimates that the risk is appropriate for the borrower. For MNC’s to then swap the loans is to ignore this judgment and puts lenders at risk and hence the interests of the shareholders.Opposing View. No. The difference in rates is often small and hardly related to non payment. There are other reasons for swaps to do with currencies and changing the nature of the loan, so there is no second guessing the market.With whom do you agree? Provide a reasoned argument as to why you agree or with one of the above views.ANSWER:The swap rates will be in line with forward rates, so that MNCs will not benefit from borrowing low interest rate currencies and simultaneously hedging. As the forward rates are market rates there is little by the way of deceiving the market especially as swaps are usually between highly creditworthy companies.Answers to End of Chapter Questions1. Floating-Rate Bonds.a. What factors should be considered by a UK firm that plans to issue a floating rate bonddenominated in a foreign currency?b. Is the risk of issuing a floating rate bond higher or lower than the risk of issuing a fixed ratebond? Explain.c. How would an investing firm differ from a borrowing firm in the features (i.e., interest rate andcurrency’s future exchange rates) it would prefer a floating rate foreign currency-denominated bond to exhibit?ANSWER:a. A firm should consider the interest rate for each possible currency as well as forecasts of theexchange rate relative to the firm’s home currency. The firm should also determine whether it has future cash inflows in any foreign currencies that could denominate the bond. Finally, the firm should forecast the future path of the coupon rate.b. The risk from issuing a floating rate bond is that the interest rate may rise over time. The riskfrom issuing a fixed rate bond is that the firm is obligated to pay that coupon rate even if interest rates decline. Some firms may feel that a fixed rate bond is less risky since at least they know with certainty the coupon rate they must pay in the future. This question is somewhat open-ended.c. An investing firm prefers a bond denominated in a currency that is expected to appreciate andwith an interest rate that is high and expected to increase. A borrowing firm prefers a bond denominated in a currency that is expected to depreciate and with an interest rate that is low and expected to decrease.2.Risk From Issuing Foreign Currency-Denominated Bonds. What is the advantage of usingsimulation to assess the bond financing position?ANSWER: Unlike point forecasts, simulation provides a distribution of possible outcomes. Thus, the firm can determine the probability that a particular foreign issued bond will be a less expensive source of funds than a locally issued bond.3. Exchange Rate Effects.a. Explain the difference in the cost of financing with foreign currencies during a strong-poundperiod versus a weak-pound period for a UK firm.b. Explain how a UK-based MNC issuing bonds denominated in euros may be able to offset aportion of its exchange rate risk.ANSWER:a. The cost of financing with foreign currencies is low when the pound strengthens, and highwhen the pound weakens.b. It may offset some exchange rate risk if it has cash inflows in euros. These euros could beused to make coupon payments.4.Bond Offering Decision. Columbia plc is a UK company with no foreign currency cash flows. Itplans to issue either a bond denominated in euros with a fixed interest rate or a bond denominated in UK pounds with a floating interest rate. It estimates its periodic pound cash flows for each bond. Which bond do you think would have greater uncertainty surrounding these future pound cash flows? Explain.ANSWER: Exchange rates are generally more volatile than interest rates over time. Therefore the pound value of payments made on euro-denominated bonds would likely be more uncertain than the payments made on floating-rate bonds denominated in pounds. Also, the principal payment is subject to exchange rate risk but not to interest rate risk.5. Currency Diversification. Why would a UK firm consider issuing bonds denominated inmultiple currencies?ANSWER: The firm may issue bonds in multiple currencies to reduce exchange rate risk. This is especially possible when the currencies used to denominate bonds are not highly correlated.6.Financing That Reduces Exchange Rate Risk. Kerr, Plc a major UK exporter of products toJapan, denominates its exports in pounds and has no other international business. It can borrow pounds at 9 percent to finance its operations or borrow yen at 3 percent. If it borrows yen, it will be exposed to exchange rate risk. How can Kerr borrow yen and possibly reduce its economic exposure to exchange rate risk?ANSWER: Kerr could invoice its exports in yen and use the proceeds to pay back loans. Its economic exposure would be reduced because Japanese consumers would not be subjected to exchange rate swings.7. Exchange Rate Effects. Katina, Plc is a UK firm that plans to finance with bonds denominated ineuros to obtain a lower interest rate than is available on pound-denominated bonds. What is the most critical point in time when the exchange rate will have the greatest impact?ANSWER: The most critical time is maturity, since the principal will be paid back at that time.8.Financing Decision. Ivax plc (based in Germany) is a drug company that has attempted to capitalize on new opportunities to expand in Eastern Europe. The production costs in most Eastern European countries are very low, often less than one-fourth of the cost in Germany or Switzerland. Furthermore, there is a strong demand for drugs in Eastern Europe. Ivax penetrated Eastern Europe by purchasing a 60 percent stake in Galena AS, a Czech firm that produces drugs.a. Should Ivax finance its investment in the Czech firm by borrowing euros that would then be converted into koruna (the Czech currency) or by borrowing koruna from a local Czech bank? What information do you need to know to answer this question?b. How can borrowing koruna locally from a Czech bank reduce the exposure of Ivax to exchange rate risk?c. How can borrowing koruna locally from a Czech bank reduce the exposure of Ivax to political risk caused by government regulations?ANSWER:a. Ivax would need to consider the interest rate in the Europe versus the interest rate when borrowingkoruna (the Czech currency). It would also need to consider the potential change in the koruna currency against the euro. If it finances the project in dollars, it is more exposed to exchange rate risk, because the funds would be remitted to Germany before paying the interest expenses on the loan. Conversely, if it finances the project in koruna, it could use some of its local funds to pay off its interest expenses before remitting any funds to the parent. Another reason for borrowing from a local Czech bank is that the bank may help Ivax avoid any excessive regulatory restrictions that could be imposed on foreign firms in the drug industry. These potential advantages of borrowing locally must be weighed against the potentially higher interest rate when borrowing locally.b. By borrowing koruna, the Czech subsidiary of Ivax should make its interest payments beforeremitting any funds to the parent. Therefore, there are less funds that have to be remitted (less exposure) than if the funds are remitted to Europe before interest payments are paid to a European bank.c. By borrowing from a local Czech bank, Ivax may be able to avoid excessive regulations thatcould be imposed on foreign firms by the local government. Also, there is less chance of any extreme action to be taken on a foreign firm when that firm’s failure would cause defaults on loans provided by local lenders.Advanced Questions9. Bond Financing Analysis. Sambuka plc can issue bonds in either UK pounds or in Swiss francs.Pound-denominated bonds would have a coupon rate of 15 percent; Swiss franc-denominated bonds would have a coupon rate of 12 percent. Assuming that Sambuka can issue bonds worth £10,000,000 in either currency, that the current exchange rate of the Swiss franc is £0.47, and that the forecasted exchange rate of the franc in each of the next three years is £0.50, what is the annual cost of financing for the franc-denominated bonds? Which type of bond should Sambuka issue?ANSWER:If Sambuka issues Swiss franc-denominated bonds, the bonds would have a face value of £10,000,000/£0.47 = Sf21,276,595.2Year3YearYear1SF Payment SF2,553,191 SF2,553,191 SF23,829,786£0.50£0.50rateExchange£0.50Payments in £ £1,276,596 £1,276,596 £11,914,893A UK bond at 15% on £10m would cost more (annual payments being £1.5m etc) but can wereally assume that the exchange ratte will stay as it is? A change of 1.5/1.276 – 1 = 17 ½% would make the SF more expensive, this is quite a big change but Sambuka would be wise to carry out a risk assessment.10. Bond Financing Analysis. Hatton ltd has just agreed to a long-term deal in which it willexport products to Japan. It needs funds to finance the production of the products that it will export. The products will be denominated in pounds. The prevailing UK long-term interest rate is 9 percent versus 3 percent in Japan. Assume that interest rate parity exists, and that Hatton believes that the international Fisher effect holds.a. Should Hatton finance its production with yen and leave itself open to exchange rate risk?Explain.b. Should Hatton finance its production with yen and simultaneously engage in forward contractsto hedge its exposure to exchange rate risk?c. How could Hatton plc achieve low-cost financing while eliminating its exposure to exchangerate risk?ANSWER:a. No. The exchange rate of the yen is expected to rise according to the IFE, whichwould offset the interest rate differential.b. No. The forward rate premium should reflect the interest rate differential, so the financing ratewould be 9% if Hawaii used this strategy.c. Hawaii could request that the Japanese importers pay for their imports in yen. It could financein yen at 3% and use a portion of the proceeds from its export revenue to cover its finance payments.11. Cost of Financing. Assume that Seminole, plc considers issuing a Singapore pound-denominatedbond at its present coupon rate of 7 percent, even though it has no incoming cash flows to cover the bond payments. It is attracted to the low financing rate, since UK pound-denominated bonds issued in the United Kingdom would have a coupon rate of 12 percent. Assume that either type of bond would have a four-year maturity and could be issued at par value. Seminole needs to borrow £10 million. Therefore, it will issue either UK pound-denominated bonds with a par value of £10 million or bonds denominated in Singapore dollars with a par value of S$20 million. The spot rate of the Singapore dollar is £0.33. Seminole has forecasted the Singapore dollar’s value at the end of each of the next four years, when coupon payments are to be paid:End of Year Pound Exchange Rateof Singapore1 £0.342 0.353 0.384 0.33Determine the expected annual cost of financing with Singapore pounds. Should Seminole, Plc issue bonds denominated in UK pounds or Singapore pounds? Explain.ANSWER:End of Year:1234 S$ payment S$1,400,000S$1,400,000S$1,400,000 S$21,400,000 Exchange rate £0.340.350.38 0.33£ payment £476,000£490,000£532,000 £7,062,000 S$20m is at the spot rate only worth 20 x 0.33 = £6,600,000 so some borrowing will also be needed. The question is whether the foreign borrowing in S$ is cheaper than the UK equivalent.?12% of £6,600,000 is £792,000 so it would seenm that borrowing in Singapore dollars would be much cheaper. But clearly the validity of the exchange rate predictions must be examined.12.Interaction Between Financing and Invoicing Policies. Assume that Hurricane, plc is a UKcompany that exports products to the United States, invoiced in pounds. It also exports products to Denmark, invoiced in pounds. It currently has no cash outflows in foreign currencies, and it plans to issue bonds in the near future. Hurricane could issue bonds at par value in (1) pounds with a coupon rate of 12 percent, (2) Danish kroner with a coupon rate of 9 percent, or (3) dollars with a coupon rate of 15 percent. It expects the kroner and dollar to strengthen over time. How could Hurricane revise its invoicing policy and make its bond denomination decision to achieve low financing costs without excessive exposure to exchange rate fluctuations?ANSWER: Hurricane could invoice goods exported to Denmark in kroner instead of pounds.Thus, it would now have inflows in kroner that could be used to make coupon payments on bonds denominated in kroner that it could issue. This strategy achieves a cost of financing of 9 percent,which is lower than the cost of other financing alternatives. To the extent that the inflows in kroner can cover bond payments, this strategy is not exposed to exchange rate risk.13.Swap Agreement. Grant, plc is a well-known UK firm that needs to borrow 10 million dollars tosupport a new business in the United States. However, it cannot obtain financing from US banks because it is not yet established within the United States. It decides to issue pound-denominated debt (at par value) in the United Kingdom, for which it will pay an annual coupon rate of 10 percent. It then will convert the pound proceeds from the debt issue into dollars at the prevailing spot rate (the prevailing spot rate is one pound = $1.70). Over each of the next three years, it plans to use the revenue in dollars from the new business in the United States to make its annual debt payment. Grant, plc engages in a currency swap in which it will convert dollars to pounds at an exchange rate of $1.70 per pound at the end of each of the next three years. How many pounds must be borrowed initially to support the new business in the United States? How many dollars should Grant plc specify in the swap agreement that it will swap over each of the next three years in exchange for pounds so that it can make its annual coupon payments to the UK creditors?ANSWER: Since Grant Inc. needs $10 million, Grant will need to issue debt amounting to £5.882 million (computed as $10 million / $1.70 per pound). Grant will pay 10% on the principal amount of £5.882 million annually as a coupon rate, which is equal to £0.5882 million. It should specify that 1 million dollars are to be swapped for pounds in each of the next three years.14.Interest Rate Swap. Janutis plc has just issued fixed rate debt at 10 percent. Yet, it prefers toconvert its financing to incur a floating rate on its debt. It engages in an interest rate swap in which it swaps variable rate payments of LIBOR plus 1 percent in exchange for payments of 10 percent.The interest rates are applied to an amount that represents the principal from its recent debt issue in order to determine the interest payments due at the end of each year for the next three years.Janutis plc expects that the LIBOR will be 9 percent at the end of the first year, 8.5 percent at the end of the second year, and 7 percent at the end of the third year. Determine the financing rate that Janutis plc expects to pay on its debt after considering the effect of the interest rate swap.ANSWER: The fixed rate of 10% to be received from the interest rate swap offsets the 10% payments made on the debt. Therefore, the annual cost of financing on the debt over the next three years is simply the variable rate that is paid out on the interest rate swap. This rate is derived below:End of Year LIBOR Variable Rate Paid Due to Swap1 9.0% 9.0% + 1.0% = 10.0%2 8.5% 8.5% + 1.0% = 9.5%3 7.0% 7.0% + 1.0% = 8.0%。

Chapter 10Derivatives: Risk Management with Speculation, Hedging, and Risk TransferNote:In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first currency is the quoted currency in terms of units of the second currency.For example, €:$ = 1.4 indicates that one euro is priced at 1.4 dollars. In previous editions we used the reversed convention $/€= 1.4, meaning 1.4 dollars per euro.All problems in this test bank still use the old convention and have not been adapted to reflect the new quotation symbols used in the 6th edition.Questions and Problems1. A Swiss portfolio manager has a significant portion of the portfolio invested in dollar-denominatedassets. The money manager is worried about the political situation surrounding the next U.S.presidential election and fears a potential drop in the value of the dollar. The manager decides to sell the dollars forward against Swiss francs.a. Give some reasons why the Swiss money manager should use futures rather than forwardcurrency contracts?b. Give some reasons why the Swiss money manager should use forward currency contracts ratherthan futures?Solutiona. Some reasons to use futures rather than forward currency contracts:•The money manager does not require a specific maturity as there is no specific cash flow to hedge. A futures contract with an expiration date extending beyond the election date would beacceptable.• A professional money manager is well-equipped to deal with daily marking-to-market.•Futures can be cheaper than forward as they are standardized and traded on an organized market. Forwards are customized contracts, and hence, are often more expensive unless theyare of a large size.•Futures are tradable at any time while forwards are not, so the hedge can easily be removed at any time, while removing a forward hedge usually requires the writing of an opposite contract.b. Some reasons to use forward currency contracts rather than futures:•It is easy to arrange a forward through a bank for a specific amount and maturity.•Forward contracts do not require the daily cash adjustments required by the marking-to-market procedure of futures contracts.•Currency forwards are administratively less burdensome than futures contracts.•Forward contracts can be arranged for large amounts, while the liquidity of currency futures contracts could be limited. So, the cost of implementing a currency forward could be less thanthe cost of implementing a currency futures hedge.Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 1172. Why are futures contracts commonly believed to be less subject to default risk than forward contracts?SolutionFutures markets have put in place successful procedures to protect clients from the default ofa counterparty:•The counterparty is always the clearinghouse, not a private party.• A centralized margin deposit system.•Guarantees posted by all members who are collectively responsible.•Daily marking-to-market. Variation limits can make this process take place during the day if needed.•Liquidity of an organized market for standardized contracts.3. Let’s consider a Swiss franc futures contract traded in the United States. On February 18 (a Friday),the March contract closed at 0.7049 dollar per Swiss franc. The size of the contract is 125,000 Swiss francs. The initial margin is $2,600 per contract and the maintenance margin is $1,600. Assume that you buy one March contract on February 19 at 0.7049 $/SFr and you deposit, in cash, an initialmargin of $2,600. Listed below are the futures quotations (settlement prices) observed on threesuccessive days:Feb. 18Feb. 20 Feb. 21 Feb. 220.7049 0.7009 0.6949 0.7089What are the cash flows associated with the marking-to-market procedure?SolutionLet’s review the cash flows associated with these price fluctuations:February 20: You lose 0.0040 dollars per franc, or $500 per contract which is debited from your initial deposit. Your margin is now equal to $2,100, which is above the maintenance margin.You do not have to reconstitute the initial margin.February 21: You lose an additional 0.0060 dollars per franc, or $750 per contract, which isdebited from your margin account. Your margin is now equal to $1,350, which is below themaintenance margin. You have to reconstitute the initial margin up to $2,600 by transferring$1,250 to your margin account.February 22: You gain 0.0140 dollars per franc, or $1,750 per contract. You can use this $1,750 as you like, since your initial margin is intact at $2,600.The net result on February 22, is that you have a net gain of $500 (= 1,750 - 750 - 500) from the day you initially bought the contract. If you decided to sell back the contract on February 22, your margin deposit of $2,600 would be given back to you, and the net gain of $500 would be yours.4. A German investor holds a portfolio of British stocks. The market value of the portfolio is £20 million,with a β of 1.5 relative to the FTSE index. In November, the spot value of the FTSE index is 4,000.The dividend yield, euro interest rates, and pound interest rates are all equal to 4% (flat yield curves).a. The German investor fears a drop in the British stock market (but not in the British pound).The size of FTSE stock index contracts is 10 pounds times the FTSE index. There are futurescontracts quoted with December delivery. Calculate the futures price of the index.b. How many contracts should you buy or sell to hedge the British stock market risk?118 Solnik/McLeavey •Global Investments, Sixth Editionc. You believe that the capital asset pricing model (CAPM) applies to British stocks. The expectedstock market return is 10%. What is the expected return on this portfolio before and after hedging?d. You now fear a depreciation of the British pound relative to the euro. Will the strategies aboveprotect you against this depreciation? (Assume that the margin on the futures contract isdeposited in euros.)e. The forward exchange rate is equal to 1.4 € per £. How many pounds should you sell forward?Solutiona. The arbitrage value of the futures price of a stock index contract is equal to its spot value plus thebasis. The basis is equal to the difference between the interest rate and the dividend yield, timesthe spot value of the index. In a cash and carry arbitrage, the arbitrageur buys the stocks in theindex and sells the futures contract forward. In carrying the stocks, the arbitrageur has to financethe position at the pound interest rate, but receives the dividends on the stocks (which are notpaid or received on the futures contract). The futures price should be equal to the spot price sinceall yields are equal to 4%:F=S= 4,000.b. The minimum-variance hedge ratio is equal to the beta of the portfolio. You should sell N stockindex futures contracts, adjusting for the beta of the portfolio:N=portfolio valuebeta stock index contract size⨯⨯N=?0 million 1.57,500. 4,000?0⨯=⨯c. According to the CAPM, the expected return on the British portfolio (before hedging) is:E(R) = 4% +1.5 ⨯ (10% - 4%) = 13%.If you hedge the portfolio by selling FTSE contracts as in Question (b), the expected returnbecomes the risk-free interest rate of 4%.d. Hedging with British stock index futures does not protect you against a depreciation of theBritish pound.e. Your current exposure is £20 million and this is the amount to be sold forward.5. You hold a portfolio made of French stocks and worth €10 million. The beta (β) of this portfoliorelative to the CAC index is 1.5. The interest rate for the euro is 4% for all maturities and the annual dividend yield is 2%. The spot value of the CAC index on January 1, 2000, is 5,000. A CAC contract has a size of €10 for each index point.a. What should be the future price of the CAC contract with a three-month maturity?b. You fear a fall in the French stock market. What should be your hedge ratio? How manycontracts do you buy/sell?Solutiona. F= 5,000 + ((4% – 2%)/4) ⨯ 5000 = 5,025.b. h*=β= 1.5.Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 119 andN =portfolio valuebetastock index contract size⨯⨯=€10 million/(5,000 ⨯ 10) ⨯ 1.5.N =300.6. To capitalize on your expectation of a 10% gold price appreciation, you consider buying futures oroption contracts to speculate. The spot price of gold is $400. Near-delivery futures contracts are quoted at $410 per ounce with a margin of $1,000 per contract of 100 ounces. Call options on gold are quoted with the same delivery date. A call with an exercise price of $400 costs $20 per ounce.The rate of return on your speculation will be the return on your invested capital, which is the initial margin for futures and the option premium for options.a. Based on your expectation of a 10% rise in gold price, what is your expected return at maturityon futures contracts?b. Based on your expectation of a 10% rise in gold price, what is your expected return at maturityon option contracts?c. Simulate the return of the two investments for various movements in the price of gold.Solutiona The expected rate of return on the futures margin deposit is equal to 300%. This is found byobserving that the margin per ounce of gold is $10($1,000 for contract of 100 ounces). With a10% gold price appreciation of $40, the spot price of gold will rise to $440, which will also bethe futures price on delivery date. Hence, a profit of $440 – $410 = $30, for an initial investment of $10.b. At expiration, the option is expected to be worth $40 per ounce, since the gold price is expectedto be $440 and the exercise price is $400 per ounce. This leads to a net profit of $20 and a rate of return on the initial $20 investment of 100%.c. Gold Price Simulation$320 $360 $400 $440 $480Rate of Return:Gold Bullion -20% -10% 0% 10% 20%Futures -900% -500% -100% 300% 700%Option -100% -100% -100% 100% 300%7. In Hong Kong, the size of a futures contract on the Hang Seng stock index is HK $50 times the index.The margin (initial and maintenance) is set at HK $32,500. You predict a drop in the Hong Kong stock market following some economic problems in China and decide to sell one June futurescontract on April 1. The current futures price is 7,200. The contract expires on the second-to-last business day of the delivery month (expiration date: June 27). Today is April 1, and the current spot value of the stock market index is 7,140.a. Why is the spot value of the index lower than the futures value of the index?b. Indicate the cash flows that affect your position if the following prices are subsequently observed:April 1 April 2 April 3 April 4Hang Seng Futures 7,200 7,300 7,250 6,900120 Solnik/McLeavey • Global Investments, Sixth EditionS olutiona. The futures price is higher than the spot price probably because the short-term interest rate ishigher than the dividend yield (positive basis).b.April 1 April 2April 3 April 4 Gain/Loss 0 -5,0002,500 17,500 Margin before Cash Flow 0 27,50035,000 50,000 Cash Flow -32,500 -5,0002,500 17,500 Margin after Cash Flow 32,50032,500 32,500 32,500 8. Derive a theoretical price for each of the following futures contracts quoted in the United States andindicate why and how the market price should deviate from this theoretical value. In each case,consider one unit of underlying asset. The contract expires in exactly three months, and theannualized interest rate on three-month dollar London InterBank Offered Rate (LIBOR) is 12%. All interest rates quoted are annualized.Contract Useful Information a. Gold Futures: Spot gold price = $300 per ounce; cost of storage =$0.50 per ounce per monthb. Currency Futures: $/€ spot exchange rate = 1.10 dollars per euro;3-month euro interest rate = 4%c. Eurodollar Futures: (3-month $ LIBOR):6-month $ LIBOR interest rate = 10% d. Stock Index Futures: Current value of stock index = 1,200; annualdividend yield = 2%SolutionF is the futures price and S the spot price.a. Gold futuresF = S ⨯ (1 + 3-month interest rate) + cost of storage.F = 300 ⨯ (1.03) + 1.5 = $310.5.This is a pure arbitrage relation. It must hold exactly for a forward contract and closely for afutures contract. The market price of the futures could deviate from this theoretical price because arbitrage costs on this physical asset are quite high.b. Currency futures€€$1112%/41.1 1.1218 $/114%/4r F S r ++==⨯=++where: $r is the dollar interest rate,€r is the euro interest rate. This is a pure arbitrage relation. It must hold exactly for a forward contract and hold closely for afutures contract. Arbitrage costs are very small on the currency market.Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 121c. Eurodollars futuresThe futures price is equal to 100% minus the annualized forward interest rate. The forwardinterest rate r F is the three-month interest rate that will be valid in three months (the delivery date of the futures contract). By arbitrage, it should be equivalent today to buy the futures contract or to invest for six months (r m interest rate to maturity) and simultaneously borrow for three months (r d interest rate to delivery).11.1m F dr r r ++=+Here, the interest rate to maturity is r m = 10% ⨯ 6/12 = 5%.The interest rate to delivery is r d = 12% ⨯ 3/12 = 3%.The futures interest rate is then r F = 1.05/1.03 - 1 = 1.9417%.On an annual basis, this is equal to 1.9417% ⨯ 12/3 = 7.7670%. Therefore, the futures price on the eurodollar contract should be equal to:F = 100 - 7.7670 = 92.233%.d. Stock indexF = S (1 + r s - r d )where:r s is the short-term interest rate,r d is the dividend yield.F = 1200 (1 + 12%/4 - 2%/4) = 1230.The market price may diverge from this theoretical value because:• The dividend yield is an annual approximation,• and arbitrage costs are quite high for the large number of stocks represented in the index.Note : In all these applications, one must be very careful to calculate interest pro rata temporis.Interest rates are always quoted on an annual basis. For example, the 12% rate on a three-month bill yields a 12% ⨯ 3/12 = 3% per quarter.9. You wish to establish the theoretical futures price on a Euribor contract quoted on the LondonInternational Financial Futures Exchange (LIFFE) in London. The futures contract is for a 90-day Euribor rate at expiration of the futures contract. You look at the current term structure of Euribor interest rates. Following the standard conventions for short-term rates, all interest rates are quoted as annualized linear rates. In other words, the interest paid for a maturity of T days is equal to theannualized rate quoted, divided by 360 and multiplied by T. The observed rates are as follows:60-Day 90-Day 150-Day 180-Day Euribor Rate 4.125% 4.250% 4.500% 4.550%a. What should be the Euribor futures price quoted today with an expiration date in exactly90 days?b. What should be the Euribor futures price quoted today with an expiration date in exactly60 days?122 Solnik/McLeavey • Global Investments, Sixth EditionSolutiona. This futures contract is for a 90-day bill issued in 90 days and maturing in 180 days. Theannualized forward interest rate r F is given by:180********1 4.55%1 1.01199841 4.25%F r ++==+r F = 4.80%F = 100% - 4.80% = 95.20%.b. This futures contract is for a 90-day bill issued in 60 days and maturing in 150 days. The annualized forward interest rate r F is given by:150********1 4.5%1 1.01179441 4.125%F r ++=⨯+r F = 4.72%F = 100% - 4.72% = 95.28%.10. You specialize in arbitrage between the futures and the cash market on the Paris Bourse. The CAC stock index is made up of 40 leading stocks. The futures price of the CAC contract with delivery in a month is 2,120. The size of the contract is €10 times the index. The spot value of the index is given as 2,000. Actually, there are transaction costs in the cash market; the bid –ask spread is around 40 points. You can buy a basket of stocks representing the index for 2,020 and sell the same basket for 1,980. Transaction costs on the futures contracts are assumed to be negligible. During the next month, the stocks in the index will pay dividends amounting to 5 per index. These dividends have already been announced, so there is no uncertainty about this cash flow. The current one-month interest rate in euros is 61/2 - 5/8%.a. Do you detect any arbitrage opportunity?b. What profit could you make per contract?c. What is the theoretical value of the futures bid and ask prices?Solutiona. The basis is equal to 120 per index or 6% of the spot value. This seems very large. An arbitrage would be to sell futures, buy spot, and carry the position till expiration of the futures contract. At expiration, both positions would be liquidated (futures contracts on the index are settled by cash, not by physical delivery of the shares).b. Let’s look at the exact arbitrage per index:• Sell the futures at 2,120.• Buy a basket of stocks at 2,020.• Carry the position for a month with a financing cost at a rate of 6 5/8% and with the receipt of€5 in dividends.• Buy back the futures at expiration at the prevailing spot index value S (by definition of the contract, the futures price is equal to the spot value in expiration).• Sell the basket of stocks at S minus 20.Note that the futures contract is settled in cash, so the basket of stocks cannot be used for physical delivery; it increases the transaction costs. Let’s look at the profit at the end of the month:Profit = 2120 - 2020 -2020 5865(20)12100S S ⎛⎫+-+- ⎪⨯⎝⎭= 73.85.Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 123c. By arbitrage, the bid (F bid ) and ask (F ask ) are given by the following equations:0 = - F bid + 1,980 + 1,9801265(20)12100S S ⎛⎫-+-+ ⎪⨯⎝⎭F bid = 1,980 + 10.72 - 5 -20 = 1,965.72.0 = F ask - 2,020 - 2,0205865(20)12100S S ⎛⎫+-+- ⎪⨯⎝⎭F ask = 2,020 + 11.15 - 5 + 20 = 2,046.15.The futures price should be between 1,965.72 and 2,046.15. In practice, the transaction cost on a basket of shares will generally be much less than the 2%assumed here on a return transaction.11. A few years ago when the French franc (FF) still existed, the MATIF futures exchange in Paris had avery active market for the French government bond contract. The underlying asset is a notional long-term government bond with a yield of 10%. The size of the contract is FF 500,000 of nominal value. Futures prices are quoted in percentage of the nominal value. On April 1, the French term structure of interest rate is flat. The bond futures price for delivery in June is equal to 106.21%. The three French government bonds that can be used for delivery have the following characteristics:Market Price Duration Conversion Factor Bond A107.46% 7.00 101.1771% Bond B105.57% 7.90 98.1441% Bond C 106.32% 8.80 99.3104%a. Is the futures price consistent with the spot bond prices? (Find the bond cheapest to deliver.)b. Estimate the interest rate sensitivity (duration) of the futures price.c. You are an insurance company with a portfolio of French government bonds. The portfolio has anominal value of FF 100 million and a market value of FF 110 million. Its average duration is 3.5. You are worried that social unrest in France could lead to an increase in French interest rates.Rather than selling the bonds, you wish to temporarily hedge the French interest rate risk. Howmany futures contracts would you sell and why?Note to the instructor: The section on optimal hedge ratios for bond portfolios has beenremoved from the 5th edition. We include a brief summary of the theoretical derivationsgiven at the end of the solution.Solutiona. To answer this question we need to determine which is the cheapest-to-deliver bond.We search for the cheapest-to-deliver bond. If we deliver bond i with price P i and conversionfactor CF i , the net receipt will be (assuming a flat yield-curve):F ⨯ CF i - P i .124 Solnik/McLeavey • Global Investments, Sixth EditionSince F = 106.21%Bond A: 0 B ond B:-1.33%B ond C: -0.84% B ond A is the cheapest-to-deliver bond and its price should drive the futures price:F = P A /CF A .Since P A /CF A = 106.21%, spot bond prices are consistent with the futures price.b. The duration of the futures should be equal to that of Bond A, or:D F = 7.00 since .A A AdP dF D dr F P ==-⨯ c. A naive hedge would be to sell an equal nominal quantity of futures contract, that is, a nominalvalue of FF 100 million or 200 contracts. However, the futures price is twice as sensitive tointerest rate movements as the portfolio (durations of 7 and 3.5, respectively). So, you should sell only 100 contracts.More precisely the optimal hedge ratio is (see Appendix):h * =110 3.50.518.106.217⨯=⨯ You should sell N contracts:N = 0.518100 millions 103.6.0.5 million= Appendix: Theoretical DerivationsTheoretical value of the futures price :The theoretical value of the futures price is derived by arbitrage between the futures and the cheapest-to-deliver bond. Assume that the futures price is “too high.” Then an arbitrageur could buy adeliverable bond “B ” at a price P B on the cash market and simultaneously sell the futures at F . Bond B has a conversion factor CF B . The carrying cost of this position is the difference between the short-term interest rate paid to finance the purchase of the bond and the long-term interest rate (yield)received while holding the bond. Let’s assume that the yield curve is flat, so that there is no carrying cost in this arbitrage (basis equals zero).At delivery the arbitrageur will make a profit equal to:F ⨯ CF B - P B .Chapter 10 Derivatives: Risk Management with Speculation, Hedging, and Risk Transfer 125Of course, the arbitrageur will choose the bond (Bond B) that maximizes this profit (i.e., thecheapest-to-deliver bond). By arbitrage this riskless profit must be zero (it will be negative for deliverable bonds that are not the cheapest-to-deliver). So, the futures price should be equal to:.B BP F CF = The price of the cheapest-to-deliver bond (Bond B) drives the futures prices (the conversion factor isa constant).Optimal hedge ratio :Let’s assume that we wish to hedge the interest rate risk of a portfolio with a value V (hereFF 110 million), consisting of a nominal value Q (here FF 100 million) times an average spot bond price S % (here 110%). The duration equation for the portfolio for a small variation dr in the market yield is:S dV Q dS dS D dr V Q S S⨯===-⨯⨯ or.S dV D Q S dr =-⨯⨯⨯The duration equation for the futures price is driven by the equation duration for the cheapest-to-deliver bond (remember that the conversion factor is a constant):B B BdP dF D dr F P ==-⨯ hence.B dF D F dr =-⨯⨯We hedge by selling N futures contracts with a fixed size (here FF 0.5 million). For a small variationdr in the market yield, the futures position will generate a gain of:Gain = .B N size dF N size D F dr -⨯⨯=⨯⨯⨯⨯The net result on the hedged portfolio is:().S B B S D Q S dr N size D F dr N size D F D Q S dr -⨯⨯⨯+⨯⨯⨯⨯=⨯⨯⨯-⨯⨯⨯The optimal number of contracts that will immunize the hedged portfolio to small variations inmarket yield is such that:0B S N size D F D Q S ⨯⨯⨯-⨯⨯=or.S B D S Q N Size D F⨯=⨯⨯ The optimal hedge ratio is *.S B D S h D F ⨯=⨯12. An American investor wants to invest in a diversified portfolio of Japanese stocks but can invest onlya rather small sum. The investor also worries about fiscal and transaction cost considerations. Whywould futures contracts on the Nikkei index be an attractive alternative?Solution•With little capital, an investor can only buy a few Japanese shares and will only hold a poorly diversified portfolio. Through a stock index futures contract this same investor holds aparticipation in a fully diversified Japanese stock portfolio.•Transaction costs on individual shares are higher than on a stock index futures contract.•The futures prices should be set by Japanese investors who arbitrage between the futures contracts and the stock market. On the other hand, foreign buyers of Japanese stocks tend to lose thewithholding tax on dividends paid; this is certainly the case for U.S. pension funds. Therefore, the futures contract allows a purchase at fair prices without losing the withholding tax on dividends.One has to be careful about the currency exposure, which is different in a direct stock purchase and a long position in the futures contract.13. A money manager holds $50 million worth of top-quality international bonds denominated in dollars.Their face value is $40 million, and most issues are highly illiquid. She fears a rise in U.S. interest rates and decides to hedge, using U.S. Treasury bond futures. Why would it be difficult to achieve a perfect hedge (list the various reasons)?SolutionThis is a typical example of a cross-hedge where the asset to be hedged is different from the futures contracts. Among the factors that could make the hedge imperfect:•The maturity (and duration) of the portfolio of bonds is different from that of the notional bond.•Movements in the Treasury bond rates are not perfectly correlated with those on international bonds, which are mainly corporate bonds.•Basis risk.14. A manager holds a diversified portfolio of British stocks worth £5 million. He has short-term fearsabout the market but feels that it is a sound long-term investment. He is a firm believer in betas, and his portfolio’s β is equal to 0.8. What are the alternatives open to temporarily reduce the risk on his British portfolio?SolutionOne alternative is to sell all the British shares and buy them back when his fears disappear. At least he could buy and sell shares to reduce the beta of his portfolio. This is a costly solution in terms of transaction costs.Another alternative is to sell Financial Times stock index futures contracts to hedge the Britishmarket risks and remove the hedge when the fears disappear. Given the beta of his portfolio, the investor should sell for 0.8 ⨯ 5 = £4 million.Another alternative would be to buy put options on individual shares in the portfolio or on the stock index.15. You are the treasurer of a major Japanese construction company. Today is January 15. You expect toreceive €10 million at the end of March, as payment from a client on some construction work inFrance. You know that you will need this sum somewhere else in Europe at the end of June. Meanwhile, you wish to invest these €10 million for three months. The current three-month interest rate in euros is 4%, but you are worried that it will quickly drop. Listed below are Euribor futures quotations on EUREX:Maturity (month-end) PriceFebruary 96.02%March 96.08%June 96.20%September 96.25%a. Knowing that Euribor contracts have a size of €1 million, what should you do to freeze a lendingrate when you will receive the money?b. At the end of March, when you receive the money, the three-month Euribor is equal to 3%.How much money (number of euros) have you gained by engaging in the above transaction(as opposed to doing nothing on January 15)?Solutiona. I n order to freeze a lending rate when I will receive the money, I will buy 10 futures contractsthat expire in March and have a price of 96.08%. I am now freezing a three-month lending rate of3.92% for the end of March.b. At the end of March, the futures price will converge to 97%, given the 3% interest rate at thattime. Hence, I will make a profit on the futures contracts equal to:Profit =€10 million ⨯ [97% - 96.08%]/4 =€23,000.This profit will offset the drop in interest rate from January to March. I can then invest fromMarch to June the €10 million received at a rate of 3%.16. A dollar-Swiss franc swap with a maturity of five years was contracted by Papaf Inc. three years ago.Papaf swapped $100 million for CHF 250 million. The swap payments were annual, based on market interest rates of 8% in dollars and 4% in CHF. In other words, Papaf Inc. contracted to pay dollars and receive CHF. The current spot exchange rate is 2 CHF/$, and the current interest rates are 6% in CHF and 10% in $ (the term structures are flat).a. What is the swap payment at the end of year three? Does Papaf pay or receive?b. On the final date of the swap, the spot exchange rate is 1.5 CHF/$.What is the final swap payment at the end of year five?Solutiona. At the end of year three, Papaf receives the balance of:•Receipt of CHF 10 million.•Payment of $8 million.The net cash flow is:10 – 8 ⨯ 2 =- CHF 6 million.Papaf has to pay CHF 6 million (or $3 million).。