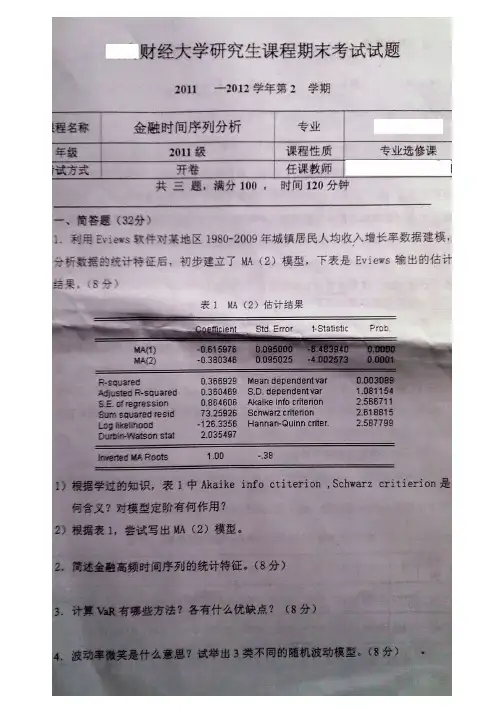

金融时间序列分析期末考试题

- 格式:pdf

- 大小:9.31 MB

- 文档页数:4

时间序列考试及答案一、单项选择题(每题2分,共20分)1. 时间序列分析中,趋势项通常用哪个字母表示?A. TB. SC. ID. C答案:A2. 季节性调整的目的是消除时间序列中的哪种成分?A. 趋势B. 季节性C. 周期性D. 随机性答案:B3. 以下哪个模型不属于时间序列的平稳模型?A. AR模型B. MA模型C. ARMA模型D. ARCH模型答案:D4. 时间序列的自相关函数(ACF)图和偏自相关函数(PACF)图的主要区别是什么?A. ACF图显示了时间序列与其滞后值之间的相关性,而PACF图显示了时间序列与其滞后值之间的偏相关性。

B. ACF图显示了时间序列与其滞后值之间的偏相关性,而PACF图显示了时间序列与其滞后值之间的相关性。

C. ACF图和PACF图没有区别。

D. ACF图和PACF图都显示了时间序列与其滞后值之间的相关性。

答案:A5. 在时间序列分析中,如果一个序列的均值随时间变化,那么这个序列被称为什么?A. 平稳序列B. 非平稳序列C. 随机序列D. 确定性序列答案:B6. 以下哪个选项是时间序列分析中常用的差分方法?A. 一阶差分B. 二阶差分C. 季节性差分D. 所有以上选项答案:D7. 以下哪个模型是时间序列分析中用于描述非平稳序列的?A. AR模型B. MA模型C. ARMA模型D. ARCH模型答案:D8. 时间序列分析中,如果一个序列的方差随时间变化,那么这个序列被称为什么?A. 平稳序列B. 非平稳序列C. 随机序列D. 确定性序列答案:B9. 在时间序列分析中,以下哪个选项是描述时间序列的周期性成分?A. 趋势B. 季节性C. 随机性答案:B10. 时间序列分析中,以下哪个选项是描述时间序列的随机波动成分?A. 趋势B. 季节性C. 随机性D. 周期性答案:C二、多项选择题(每题3分,共15分)11. 时间序列分析中,以下哪些因素可以影响时间序列的稳定性?A. 趋势B. 季节性C. 周期性答案:ABC12. 时间序列分析中,以下哪些模型属于线性模型?A. AR模型B. MA模型C. ARMA模型D. ARCH模型答案:ABC13. 时间序列分析中,以下哪些方法可以用来检验时间序列的平稳性?A. 单位根检验B. 协整检验C. 差分D. 所有以上选项答案:ABC14. 时间序列分析中,以下哪些方法可以用来进行季节性调整?A. X-12-ARIMAB. X-13ARIMA-SEATSC. TRAMO/SEATSD. 所有以上选项答案:ABCD15. 时间序列分析中,以下哪些因素可以影响时间序列的预测准确性?A. 模型选择B. 数据质量C. 参数估计D. 所有以上选项答案:ABCD三、简答题(每题10分,共30分)16. 请简述时间序列分析中趋势、季节性和随机性成分的定义。

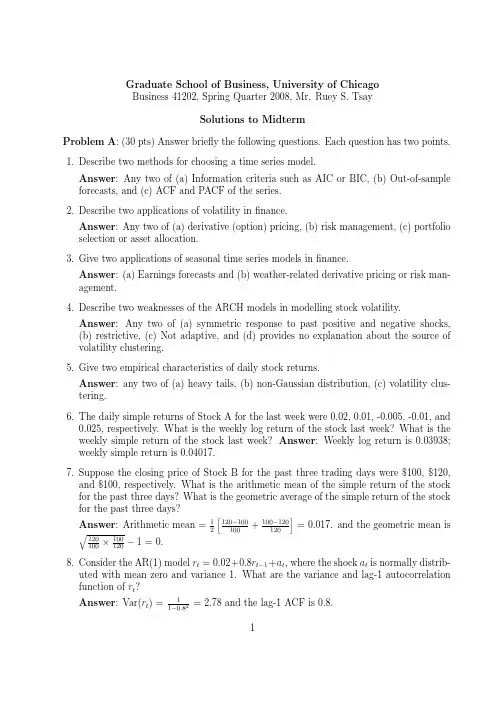

Graduate School of Business,University of ChicagoBusiness41202,Spring Quarter2008,Mr.Ruey S.TsaySolutions to MidtermProblem A:(30pts)Answer briefly the following questions.Each question has two points.1.Describe two methods for choosing a time series model.Answer:Any two of(a)Information criteria such as AIC or BIC,(b)Out-of-sample forecasts,and(c)ACF and PACF of the series.2.Describe two applications of volatility infinance.Answer:Any two of(a)derivative(option)pricing,(b)risk management,(c)portfolio selection or asset allocation.3.Give two applications of seasonal time series models infinance.Answer:(a)Earnings forecasts and(b)weather-related derivative pricing or risk man-agement.4.Describe two weaknesses of the ARCH models in modelling stock volatility.Answer:Any two of(a)symmetric response to past positive and negative shocks,(b)restrictive,(c)Not adaptive,and(d)provides no explanation about the source ofvolatility clustering.5.Give two empirical characteristics of daily stock returns.Answer:any two of(a)heavy tails,(b)non-Gaussian distribution,(c)volatility clus-tering.6.The daily simple returns of Stock A for the last week were0.02,0.01,-0.005,-0.01,and0.025,respectively.What is the weekly log return of the stock last week?What is theweekly simple return of the stock last week?Answer:Weekly log return is0.03938;weekly simple return is0.04017.7.Suppose the closing price of Stock B for the past three trading days were$100,$120,and$100,respectively.What is the arithmetic mean of the simple return of the stock for the past three days?What is the geometric average of the simple return of the stockfor the past three days? Answer:Arithmetic mean=12120−100100+100−120120=0.017.and the geometric mean is120×100−1=0.8.Consider the AR(1)model r t=0.02+0.8r t−1+a t,where the shock a t is normally distrib-uted with mean zero and variance1.What are the variance and lag-1autocorrelation function of r t?Answer:Var(r t)=11−0.82=2.78and the lag-1ACF is0.8.19.For problems6and7,suppose the daily return r t,in percentages,of Stock A followsthe model r t=1.0+a t+0.3a t−1,where a t=σt t withσ2t =1.0+0.4a2t−1and t beingstandard normal.What is the unconditional variance of a t?What is the variance of r t?Answer:Var(a t)=11−0.4=1.67.Var(r t)=(1+0.32)σ2a=1.82.10.Suppose that a n=3.0,what is the1-step ahead forecast for r n+1at the forecast originn?What is the1-step ahead volatility forecast of r t at the forecast origin n?Answer:r n(1)=1+0.3a n=1.9,andσ2n (1)=1+0.4a2n=4.6.11.Consider the simple AR(1)model r t=100+0.8r t−1+a t,where a t is normally distributedwith mean zero and variance10.Is the r t series mean-reverting?If yes,what is the half-life of the series?Answer:Yes,r t series is mean-reverting.The half-life is ln(0.5)/ln(0.8)=3.11.12.Describe two test statistics for testing the ARCH effect of an asset return series.Writedown the associated null hypotheses.Answer:(a)The Ljung-Box statistic Q(m)of the squared shocks,i.e.a2t .The nullhypothesis is H o:ρ1=ρ2=···=ρm=0,whereρi is the lag-i ACF of a2t .(b)TheEngle F-test for the regression a2t =β0+β1a2t−1+···+βm a2t−m+e t.The null hypothesisis H o:β1=β2=···=βm=0.13.Consider the following two IGARCH(1,1)models for percentage log returns:Model A:σ2t =1.0+0.1a2t−1+0.9σ2t−1Model B:σ2t =0.1a2t−1+0.9σ2t−1.Suppose thatσ2100=20and a100=−2.0.What are the3-step ahead volatility forecastsfor Models A and B?Answer:For model A:3-step ahead volatility forecast isσ2100(3)=2+(1.0+0.1×(−2.0)2+0.9×20)=21.4.For model B,the3-step ahead volatility forecast isσ2100(3)=0.1(−2.0)2+0.9×20=18.4.14.Consider the following two models for the log price of an asset:Model A:p t=p t−1+a tModel B:p t=0.00001+p t−1+a twhere the shock a t is normally distributed with mean zero and varianceσ2>0.Suppose further that p100=5.Let p n( )be the -step ahead forecast at the forecast origin n.What are the point forecasts p100( )for both models as →∞?Answer:For model A,p100( )=5for all .For model B,p100( )converges to infinity as →∞.215.Suppose that we have T =1000daily log returns for the Decile 1portfolio.Supposefurther that the sample autocorrelation at lag-12is ˆρ12=0.15.Test the hypothesis H o :ρ12=0against the alternative hypothesis H a :ρ12=pute the test statistic and draw your conclusion.Answer :t =0.151/√1000=√1000×0.15=4.74,which is highly significant.Thus,the lag-12ACF is not zero.Problem B .(20pts)It is well-known in economics that growth rate of the domestic gross product (GDP)is negatively correlated with the change in unemployment rate.Consider the U.S.quarterly real GDP and unemployment rate from the first quarter of 1948to the first quarter of 2008.Let dgdp t be the growth rate of the GDP,i.e.dgdp t =ln(GDP t )−ln(GDP t −1),and dun t be the change in unempolyment rate,i.e.dun t =U t −U t −1with U t being the civilian unemployment rate.The data were seasonally adjusted and obtained from the Federal Reserve Bank at St.Louis.The sample size after the differencing is e the attached R output to answer the following questions.1.(5points)Write down the fitted linear regression model with dgdp t and dun t representing the dependent and independent variable,respectively,including residual standard error.What is the R 2of the linear regression?Is the fitted model adequate?Why?Answer :The fitted linear regression isdgdp t =0.017−0.017dun t +e t ,ˆσe =0.0088.The R 2is 0.37.The model is not adequate because the Q (m )statistics of the residuals show that the residuals have serial correlations,i.e.Q (12)=219.4with p-value close to zero.2.(5points)To take care of the serial correlations in the residuals,a linear regression model with time-series errors is built for the two variables.Write down the fitted model,including the residual variance.Answer :The fitted linear regression model with time-series errors is(1−0.21B −0.12B 2)(1−0.86B 4)(dgdp t −0.017+0.018dun t )=(1−0.72B 4)a t ,ˆσ2a =6.01×10−5.3.(2points)Is the model in Question 2adequate?Why?Answer :Yes,the model is adequate.The Q (m )statistics of the residuals fail to indicate the existence of any serial correlations.We have Q (12)=17.53with p-value 0.13.4.(4points)Based on the fitted model in Question 2,is the growth rate of GDP negatively correlated with the change in unempolyment rate?Why?Answer :Yes,the growth rate of GDP is negatively related to the change in unemploy-ment rate.The estimated coefficient is −0.018which is highly significant,because it standard error 0.0014is small,resulting in a large t -ratio.35.(4points)To check the predictive power of the model,it was re-estimated using thefirst236data points.This re-fitted model is used to produce1-step to4-step ahead forecasts at the forecast origin t=236.The actual value of the GDP growth rates are also given.Construct the1-step ahead95%interval forecast of the model.Is the actual growth rate in the forecasting interval?Answer:The95%interval forecast is0.012±1.96×0.0077,i.e.[−0.0031,0.027].The actual value is0.0159,which is in the interval.Problem C.(16pts)Consider the quarterly earnings per share of the Microsoft stock from thefirst quarter of1992to thefirst quarter of2008.The data were obtained from First Call. To take the log transformation,we add0.5to all data points.The R output is attached. Let x t=ln(y t+0.5)be the transformed earnings,where y t is the actual earnings per share.1.(5points)Write down thefitted model for x t,including the variance of the residuals.Answer:Thefitted model is(1−B)r t=(1−0.70B+0.39B2)(1+0.39B4)a t,ˆσ2a=0.0016, where r t=ln(x t+0.5)with x t being the earnings per share.2.(2points)Is there any significant serial correlation in the residuals of thefitted model?Why?Answer:No,the Q(m)statistics of the residuals give Q(12)=9.65with p-value0.65.3.(4points)Let T=65be the forecast origin,where T is the sample size.Based on thefitted model,and,for simplicity,use the relationship y t=exp(x t)−0.5,what are the 1-step and2-step ahead forecasts of earnings per share for the Microsoft stock?Answer:The1-step and2-step earnings forecasts are0.56and0.54,respectively.4.(2points)Test the null hypothesis H o:θ4=0vs H a:θ4=0.What is the test statistic?Draw your conclusion.Answer:The test statistic is t=0.39120.1442=2.71with two-sided p-value0.0067.Thus,the seasonal MA coefficientθ4is significantly different from zero.5.(3points)Consider the regular(i.e.,non-seasonal)part of the MA model.Is it invertible?Why?Answer:Yes,it is invertible,because the polynomial1−0.6953x+0.3889x2has roots0.89±1.33i so that the absolute value of the roots(Mod in R)is1.6,which is greaterthan1.[If you compute the roots of x2−0.6953x+0.3889,the the absolute value of the roots is less than1.]Problem D.(34pts)Consider the daily log returns of the Starbucks stock,in percentages, from January1993to December2007.The relevant R output is attached.Answer the following questions.41.(2points)Is the mean log return significant different from zero?Why?Answer:No,the basic statistics show the95%confidence interval of the mean is [−0.0103,0.1624],which contains zero.2.(2points)Is there any serial correlation in the log return series?Why?Answer:Yes,the Q(m)statistics show Q(15)=38.39with p-value0.0008.3.(2points)An MA model is used to handle the mean equation,which appears to beadequate.Is there any ARCH effect in the return series?Why?Answer:Yes,because the Q(m)statistics of the squared residuals show Q(15)=112.61 with p-value close to zero.4.(6points)A GARCH(1,1)model with Student-t distribution is used for the volatilityequation.Write down thefitted model,including the degrees of freedom of the Student-t innovations and mean equation.Answer:Thefitted model isr t=0.037+a t−0.043a t−1−0.048a t−2,a t=σt t, ∼t5.27.σ2 t =0.012+0.026a2t−1+0.973σ2t−1.5.(4points)Since the constant term of the GARCH(1,1)model is not significantly differentfrom zero at the1%level,an IGARCH(1,1)model is used.Write down thefitted IGARCH(1,1)model,including the mean equation.Answer:Thefitted IGARCH(1,1)model isr t=0.077+a t−0.029a t−1−0.044a t−2,a t=σt t, t∼N(0,1).σ2 t =0.022a2t−1+0.978σ2t−1.6.(3points)Is the IGARCH(1,1)model adequate?Why?What is the3-step aheadvolatility forecast with the last data point as the forecast origin?Answer:Yes,the Q(m)statistics for the standardized residuals give Q(10)=1.77, Q(15)=10.79,and Q(20)=18.66.The p-values of these statistics are all greater than0.05.In addition,the Q(m)statistics of the squared standardized residuals also havelarge p-values.The3-step ahead volatility forecast is √3.779=1.94.7.(5points)A GJR(or TGARCH)model with Student-t distribution is alsofitted to thelog return series.Write down thefitted model,including the mean equation and all parameters.Answer:Thwfitted GJR model isr t=0.032+a t−0.043a t−1−0.048a t−2,a t=σt t, t∼t5.31.σ2 t =0.015+(0.021+0.017N t−1)a2t−1+0.970σ2t−1,where N t−1=0if a t−1≥0and=1,otherwise.58.(2points)Is the fitted GJR (or TGARCH)model adequate?Why?Answer :Yes,the Q (m )statistics of the standardized residuals and those of the squred standardized residuals all have large p-values.9.(2points)Among the GARCH(1,1),IGARCH(1,1)and GJR(1,1)models,which one is preferred?Why?Answer :The GJR(1,1)model because it has the smallest AIC value.10.(2points)Is the leverage effect of the GJR model significant?Why?Answer :Yes,the t -ratio of the leverage parameter is 2.01,which is significant at the 5%level.11.(4points)To better understand the leverage effect,use the fitted GJR to calculate theratio σ2t (a t −1=−5.10)σ2t(a t −1=5.10),assuming σ2t −1=7.5.Answer :σ2t (a t −1=−5.10)σ2t (a t −1=5.10)=0.0154+0.0379×(−5.10)2+0.97×7.50.0154+0.0208×(5.10)2+0.97×7.5=1.057.6。

金融时间序列分析英文试题(芝加哥大学)(3)Graduate School of Business,University of ChicagoBusiness41202,Spring Quarter2005,Mr.Ruey S.TsaySolutions to MidtermAll tests are based on the5%signi?cance level.Problem A:(30pts)Answer brie?y the following questions.1.For problems1to6,consider the daily log return,in percentages,of the S&P500composite index from January1996to December31,2004for2267data points.Sum-mary statistics of the percentage log returns from SCA and Splus are attached.See Page 1of the attached output.Is the mean of percentage log returns signi?cantly di?erent from zero?Why?A:t-ratio=1.187<1.96.Thus,the mean return is not signi?cantly di?erent from zero.2.Suppose one invested$1dollar on the S&P500index at the very beginning of1996andheld the investment until the end of2004.What was the value of the investment at the market closing on December31,2004?A:total log return=0.0299*2267/100=0.67783so that the value=exp(0.67783)≈1.97.3.Test the null hypothesis that the skewness of the log returns is zero.Draw your conclu-sion.A:t-ratio=?0.0939/0.0514=?1.83<1.96so that the skewness is no signi?acnt di?erent from zero.4.Given that the last percentage log return was?0.134(i.e.T=December31,2004),which is the corresponding simple return?A:R t=exp(?0.134/100)?1=?0.001339=.1339%.5.Are the log return serially correlated?You may use Q(10)of the series to answer thequestion.A:Q(10)=13.9with p-value0.178so that there is no serial correlation.6.Is there any ARCH e?ect in the log return series?You may use Q(12)of the squaredseries to answer the question.A:Yes,Q(12)of squared return is large at490(in SCA)and has a p-value of0.0from Splus.7.Give two empirical features of daily log returns of a?nancial asset.A:Any two of(a)high kurtosis,(b)volatility clustering,(3)skew to left.18.What is the purpose of studying kurtosis of an asset return series?A:Understanding the tail behavior(or risk)of the return.9.Describe two applications of studying sample autocorrelation function(ACF)of an assetreturn series.A:(a)To test serial correlations in the return series,(b)to identify MA order.10.Describe two methods that can be used to identify the order of an AR model.A:(a)PACF,(b)Criterion functions such as AIC or BIC.11.Consider the AR(1)model(1?0.9B)r t=0.2+a t,where{a t}is an independent andidentically distributed random variables with mean zero and variance1.0.What is the half-life of the series?A:Half-life=ln(0.5)/ln(0.9)=6.58time units.12.Suppose that the log return r t of an asset follows the model below:r t=0.02+a t,a t=σt t,σ2t=0.116+0.42a2t?1.Let p t be the log price of the asset at time t and p T( )be the -step ahead forecast of the log price at the forecast origin T.Then,what is the value of p T( )as increases?A:0.02is the slope of time trend so that p T( )→∞as increases.13.For problems13-14,consider quarterly series of U.S.unit labor cost from1947to2004.The data were seasonally adjusted and obtained from the Federal Reserve Bank of St Louis.Let x t=(1?B)ULC t be the?rst-di?erenced series of the data at time t.The model(1?0.371B2)x t=0.265+(1+0.171B4)a t,σa=0.5998,?ts the data reasonably well.Under the?tted model,what is the mean of x t,i.e.E(x t) =?A:E(x t)=0.265/(1?0.371)=0.421.14.Does the model imply that there exist business cycles in the unit labor cost?Why? A:No,because the two roots are real.From1?0.371x2,we have x=±1/ (0.371).15.Give two weaknesses of the GARCH-type of models for modeling asset volatility.A:Any two of(a)symmetric response to past positive and negative returns,(b)restric-tive,(c)providing no explanation of volatility clustering,(d)no adaptive in forecasting.2Problem B.(20pts)This problem is concerned with theanalysis of quarterly earnings per share of the Procter&Gamble(PG)Company from1992to the?rst quarter of2003 for45data points.The data were obtained from First Call.Log transformation was taken to stabilize the variability of the /doc/889308787.html,puter output is attached;p.2-6of output. Due to strong seasonal pattern,which results in models that are close to being non-invertible, we analyze the seasonally di?erenced series in Splus.Let x t be the logarithm of quarterly earnings per share and w t=(1?B4)x t.Thus,SCA uses x t and Splus uses w t.1.(5points)Because ACF of the log earnings shows strong seasonal pattern,the seasonaldi?erence(1?B4)is taken.The ACF of the seasonally di?erenced data indicates no further di?erencing is necessary.Write down the?tted model for the x t series(not the di?erenced w t).A:(1?0.47B)(1?B4)x t=0.0508+(1?0.307B4)a t,σa=0.0502.2.(4points)Is the AR coe?cient of the?tted model statistically signi?cant?Why?A:Yes,the t-ratio is3.26,which is greater than the critical value1.96.3.(4points)Is there any serial correlation in the residuals of the?tted model?Use Q(12)of the ACF of residuals to answer the question.[Hint:for a chi-square distribution with m degrees of freedom,the expected value is m.]A:Q(12)=8.8which is less than E(χ210)=10so that p-value>0.05.4.(4points)Let T=45be the forecast origin.What are the1-step and2-step aheadforecasts of the?tted model(after taking anti-logtransformation)?A:x45(1)=0.912and x45(2)=3.95(from SCA).For Splus,x45(1)=exp(0.0087?.1743)=0.847,x45(2)=exp(?.012479+1. 278152)=3.55.5.(3points)Give an interpretation of the estimated constant0.0508of the?tted modelfor x t.A;Slope of time trend.3and the S&P500index from January1999to December2004with sample size T=1508.We employ the market model:r t=α+βr m,t+e t,where r t and r m,t are Wal-Mart stock return and S&P500index return,respectively.Splus output is attached;page6of output.Answer the following questions.1.(4points)Write down the?tted market model.A:r t=0.0205+0.9606r m,t+e t.2.(4points)The Ljung-Box statistics of the ACF of residuals show some minor serialcorrelations,but the ACFs are relatively small so we ignore the serial correlations and perform the ARCH e?ect test.Is there an ARCH e?ect in the residuals of the?tted market model?A:Yes,archTest gives a p-value about0.0.3.(4points)We employ a GARCH(1,1)model(called“m2”in the output).Write downthe?tted /doc/889308787.html,ment on the?tted model.A:Let r t and r m,t be the Wal-Mart stock return and S&P500index return,respectively.The model isr t=0.9386r m,t+a t=0.9386+σt t, t~t6.41σ2t=?4.29×10?5+0.0377a2t?1+0.963σ2t?1.The negative estimate ofα0does not make sense,but it is statistically not di?erent from0.Also,the?α1+?β1≈1so that the?tted model indicates an IGARCH(1,1)model without the constant.4.(6points)Further analysis indicates that an EGARCH(2,1)model?ts the data better.There are two leverage e?ect parameters.Are these two e?ects statistically signi?cant?Why?You may test the e?ect individually.A:Examine the t-ratio of the two leverage parameter estimates.For Lev(1),the t-atio is?2.129.For Lev(2),the t-ratio is?1.847.In both cases,the p-values are less tha0.05so that they are both signi?cant.[It you use two-sided tests,then Lev(2)is notsigni?cant.]5.(2points)What are the1-step ahead forecasts for the return and its volatility of Wal-Mart stock at the forecast origin T=1508using the EGARCH model.A:zero for return and0.7082for volatility.4from January1995to December2004with2519observations.Splus output is attached;page 8of output.Answer the following questions.The ACFs of the returns are small so that the mean equation consists of a constant term only.1.(5points)Consider the?tted GARCH(1,1)model.The volatilityequation isσ2t=0.042+0.049a2t?1+0.944σ2t?1.Letηt=a2t?σ2t.Rewrite the prior vo latility equation in an ARMA form for the{a2t} series.A:a2t=0.042+0.993a2t?1+ηt?0.944ηt?1.2.(5points)Write down the?tted EGARCH(1,1)model with leverage e?ect(both meanand volatility equations and the parameter of the conditional distribution used).A:The model isr t=0.04918+a t=0.04918+σt t, t~t6.68ln(σ2t)=?0.06316+0.1033(|a t?1|?0.5464a t?1σt?1)+0.989ln(σ2t?1).3.(4points)Test the hypotheses H o:v=5vs H a:v=5,where v is the degrees offreedom of the conditional Student t distribution.Draw your conclusion.[Hint:you may use the usual t-ratio test.]A;t-ratio=6.684?5=2.62>1.96.Thus,reject H o:v=5.4.(5points)To better understand the leverage e?ect,use the?tted EGARCH(1,1)modelto calculate the ratioσ2t( =?3)2t ,where t denotes the iid sequence of the innovationsde?ned in class.A:From the?tetd volatility equation,we haveσ2t=exp(?0.06316)(σ2t?1).989exp(0.1033| t?1|?0.0564 t?1). Therefore,σ2t( =?3)σ2t( =3)=exp(?0.0564(?3))exp(?0.0564(3))=exp(0.0564×6)=1.403.5.(4points)Used the?tted EGARCH model and T=2519as the forecast origin.Whatare the1-step ahead forecasts of log return and volatility?A:Forecast of log return is0.0492and forecast of volatility is1.184.6.(4points)Write down the mean equation of the?tted GARCH-M model for the data.A:r t=0.058+0.00629σ2t+a t.7.(3points)Based on the GARCH-M model,is the risk premium statistically signi?cant?Why?A:No,the t-ratio is0.453with p-value=0.65(two-sided).5。

《金融时间序列模型》期末考试试卷(1)课程代码及课序号:学号:姓名:成绩:班级:课序号:任课教师:一判断题:得分如果下面说法正确则在括号内添入T,否则添入F,每个2分,共20分。

( )1、某项投资分为4个周期,每个周期的收益率不同,用R" i=l,…,4表示,y4R那么该项投资与投资期4个周期,每个周期收益率都是二的投资是等价的。

4( )2、如果&满足一个GARCH(2, 1)模型,那么&平方后满足一个ARMA(2, 2)模型。

( )3、如果以t分布作为对照分布画出的Q-Q图是直线说明该组数据服从t分布。

(根据t分布计算理论上的分位数标在纵轴上,根据数据计算出的样本分位数画在横轴上) ( )4、使用JB检验判断数据的分布是否是正态分布,如果检验的p —值等于0. 78,说明该组数据不服从正态分布。

( )5、自回归过程% = 0. 1Y- -1.4Y T + 0. 7丫3 +&的偏自相关系数等于0。

( )6、Q检验的缺陷是经常把不是白噪声的残差误认为是白噪声过程。

( )7、如果某银行宣布该银行1 —天内,99%置信水平下,风险价值等于30 (百万),说明该银行有1%的可能性1天内的损失会小于30 (百万)。

( )8、假设半年支付利率一次,周期利率5% (以半年为一个周期),那么年简单收益率是10%,年复利收益率是10. 25%,年连续复利收益率9. 89%( )9、对某模型的残差的平方进行检验,发现存在自相关,所以应该对残差建立ARCH类模型。

( )10、对MA⑴模型Y t=0. 4+e t +0. 6e t-i的3 一步预测值等于0. 4。

二选择题:得分可能有多个选项是正确的,把正确选项前的标号填入括号中,每题3分,共15分1、下面是对几个时间序列做单位根检验的结果,哪些序列是1(1)的,把标号写在括号中A AR 模型B MA 模型C ARMA-ARCH 模型D ARCH 模型3、Yt = 0. 9+(pY t -i +(p 2Y - +£如果pi = 10/21,那么cp 等于多少? (A 2. 5BC -D -2.(A 3.95MB 4.88MC 0.395MD 4.95M得分2、偏自相关函数是拖尾的模型包括4、 下面是几个模型,写出满足平稳条件模型的标号( )A Yt 二0. 1+1. 3 Yt-i -0.3 Yt-2 +讯B Yt 二0. 75 Yt-i - 0. 125 Y t -2 +&C Yt= 0. 44Y t -i+8t +1. 98t -iD Y t =£t +0. 7gt -i+0. 03gt-25、 假设某只股票的年收益率是10%,年波动率是30%,初始投资10M (M 表示货币单位是百万),5%显著水平下,1 —年内的VaR 等于三简答题:(每个5分,共20分)1、用AIC 准则来定阶,假设自回归部分滞后阶数Q 的上界为2,滑动平均部分滞后阶数q2、同学A 建立了一个消费模型,用C 表示消费,I 表示收入。