高速铁路基础设施组件制造行业研究报告 - High Speed Rail Infrastructure Component Manufacturing - 2010

- 格式:pdf

- 大小:362.21 KB

- 文档页数:7

2023年高速铁路行业市场调研报告随着我国高速铁路建设的不断发展,高速铁路行业已成为一个正处于高速发展阶段的新兴产业。

本文将分析高速铁路行业的市场情况,包括产业链结构、行业规模、市场竞争格局和未来发展趋势等方面。

一、产业链结构高速铁路行业产业链包括铁路建设、铁路装备、铁路运营、铁路配套服务等环节。

其中,铁路建设是整个产业链的基石,同时也是产业链中投入最大、风险最高的环节。

铁路装备主要包括高速列车、信号设备、通信设备、供电设备等。

铁路运营则包括车站建设、行车调度、售票等各方面。

铁路配套服务包括餐饮、旅游、物流、安全等。

这样的产业链结构形成了高速铁路建设、运营等完整的产业体系。

二、行业规模根据2019年中国铁路总公司的数据,截至2018年底,全国铁路运营里程已达13.7万公里,其中高速铁路里程已经达到2.9万公里,占比21.2%。

高速铁路的建设水平已经处于世界领先地位。

同时,中国高速铁路的线路密度也远高于其他国家,2018年中国高速铁路密度为每万平方公里7.65公里,比第二名日本高出约2.3倍。

作为中国铁路战略的重要组成部分,高速铁路行业规模不断扩大,预计到2025年,高速铁路里程将再次增加至3.5万公里以及以上,投资总额逾2000亿元。

三、市场竞争格局目前中国高速铁路行业主要的竞争者是中国中车、中国南车、北京动车组等国内厂商以及西门子、阿尔斯通等国际企业。

在高速列车制造方面,中国中车和中国南车两家企业独占鳌头,占据了中国高速铁路列车制造市场的超过90%的份额。

在信号设备、通信设备、供电设备等铁路装备领域,一些专业的外资企业则占据优势地位。

同时,在高铁运营商方面,中国铁路总公司是唯一的经营单位,还没有其他竞争者加入进来。

需要指出的是,随着国内高铁列车制造技术的不断提高和产业化程度的加深,国内外厂商竞争也将更加激烈。

四、未来发展趋势高速铁路作为我国重点建设项目之一,在未来有着广阔的发展空间和市场需求。

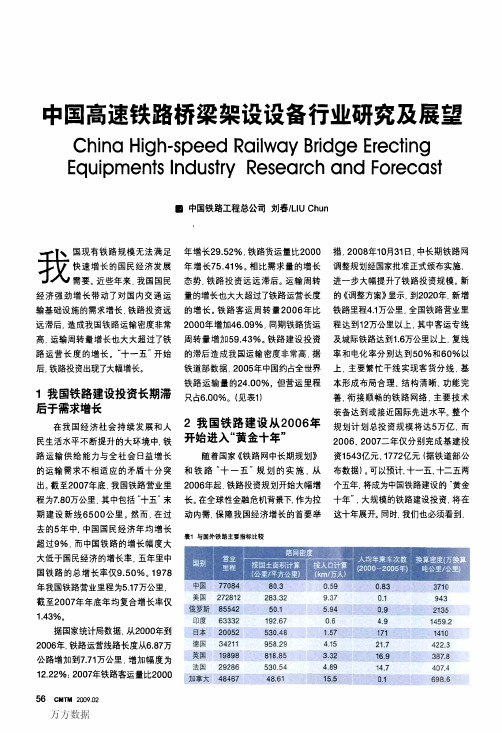

中国高速铁路桥梁架设设备行业研究及展望ChinaHigh-・speedRailwayBridgeErectingEquipmentsIndustryResearchandForecast—rT\我国现有铁路规模无法满足快速增长的国民经济发展需要。

近些年来.我国国民经济强劲增长带动了对国内交通运输基础设施的需求增长,铁路投资远远滞后.造成我国铁路运输密度非常高,运输周转量增长也大大超过了铁路运营长度的增长。

“十一五”开始后,铁路投资出现了大幅增长。

1我国铁路建设投资长期滞后于需求增长在我国经济社会持续发展和人民生活水平不断提升的大环境中.铁路运输供给能力与全社会日益增长的运输需求不相适应的矛盾十分突出。

截至2007年底.我国铁路营业里程为7.80万公里,其中包括“十五”末期建设新线6500公里。

然而,在过去的5年中,中国国民经济年均增长超过9%,而中国铁路的增长幅度大大低于国民经济的增长率.五年里中国铁路的总增长率仅9.50%。

1978年我国铁路营业里程为5.17万公里.截至2007年年底年均复合增长率仅1.43%。

据国家统计局数据.从2000年到2006年,铁路运营线路长度从6.87万公路增加到7.71万公里.增加幅度为12.22%:2007年铁路客运量E匕200056CMTM2009.02■中国铁路工程总公司刘春/LIUChun年增长29.52%,铁路货运量Lt,2000年增长75.41%。

相比需求量的增长态势,铁路投资远远滞后。

运输周转量的增长也大大超过了铁路运营长度的增长。

铁路客运周转量2006年比2000年增7]1146.09%.同期铁路货运周转量增力1159.43%。

铁路建设投资的滞后造成我国运输密度非常高.据铁道部数据.2005年中国约占全世界铁路运输量的24.00%,但营运里程只占6.00%。

(见表1)2我国铁路建设从2006年开始进入“黄金十年”随着国家《铁路网中长期规划》和铁路”十一五”规划的实施.从2006年起,铁路投资规划开始大幅增长。

掌握高铁基础设施英文作文英文:As a transportation enthusiast, I have always been fascinated by high-speed rail infrastructure. High-speed rail, also known as bullet train, is a type of passenger rail transport that operates significantly faster than traditional rail traffic. It is an important part of modern transportation systems, providing a fast, convenient, and efficient way for people to travel between cities.One of the key elements of high-speed rail infrastructure is the tracks. High-speed rail tracks are specially designed and constructed to support the high speeds and heavy loads of the trains. They are made ofhigh-quality materials such as concrete and steel, and are laid to very precise standards to ensure a smooth and stable ride for passengers.In addition to the tracks, high-speed railinfrastructure also includes stations, signaling systems, and power supply systems. The stations are designed to accommodate the high volume of passengers and provide easy access to the trains. The signaling systems are crucial for ensuring the safe and efficient operation of the trains, while the power supply systems provide the electricity needed to propel the trains at high speeds.High-speed rail infrastructure is not only importantfor passenger transportation, but also for the economy and the environment. It can help reduce traffic congestion, air pollution, and carbon emissions by providing an alternative to car and air travel. For example, in China, the high-speed rail network has significantly reduced travel times between major cities, making it easier for people to commute for work and for leisure.Overall, high-speed rail infrastructure plays a crucial role in shaping the way people travel and the development of cities and regions. It not only provides a fast and efficient mode of transportation, but also brings economic and environmental benefits to society.中文:作为一个交通运输爱好者,我一直对高铁基础设施感到着迷。

2023年铁路基础设施行业市场调研报告铁路基础设施行业市场调研报告一、调研背景随着我国经济社会的发展,铁路作为重要的交通工具之一,在物流及人员运输方面的作用越来越凸显。

铁路基础设施作为铁路运输体系中的重要组成部分,对于保障铁路运营的安全高效至关重要。

本次调研旨在深入了解我国铁路基础设施行业的发展现状、面临的挑战及未来发展方向,为该行业未来的发展提供有力支撑。

二、调研目的1、了解我国铁路基础设施行业的市场发展情况。

2、深入探讨行业面临的困难与挑战,为行业未来的发展提供参考。

3、分析行业未来的发展趋势,给企业如何在该行业发展提供指导。

三、调研方法本次调研采用文献资料调查及问卷调查相结合的方式进行。

文献资料调查:主要查阅铁路基础设施行业的相关资料,包括政策法规、管理规定、技术标准、市场调研报告、学术论文等。

问卷调查:以铁路基础设施相关企业为对象,采用问卷的方式收集数据。

四、调研结果1、市场现状目前,我国铁路基础设施建设总体健康发展,随着中国高铁的发展,铁路基础设施将更好地为铁路运输服务。

铁路基础设施行业拥有一大批专业技术人才,各种技术手段不断提升,使得铁路基础设施行业的发展在技术水平、市场需求等方面得到极大的提升。

2、行业挑战(1)外部环境:铁路基础设施行业与技术水平、管理、投资等多方面紧密联系,随着经济发展、社会进步及新型疫情等外部环境的变化,会给行业带来一定的影响。

(2)内部管理:部分企业在内部管理、品牌建设、研发创新等方面存在不足,需要加强。

3、行业未来发展趋势(1)企业数字化转型:以智能制造、大数据及互联网+等技术为代表的数字化转型将进一步推动行业革新与升级。

(2)产业链协同发展:铁路基础设施行业与其他工业领域、科技研发领域、管理领域等将进一步协同发展,促进产业链的形成。

(3)市场化趋势:以市场为导向的铁路基础设施行业将进一步加强市场开拓与营销能力,实现市场化发展。

五、结论与建议1、铁路基础设施行业在新的历史条件下必须加快转型升级,推动数字化转型,提高信息化和智能化水平,优化业务流程。

《高速铁路产业发展政策研究》篇一一、引言随着科技的进步和国民经济的持续发展,高速铁路作为现代交通的重要组成部分,其发展速度和水平已经成为衡量一个国家现代化程度的重要标志。

中国的高速铁路产业在近年来取得了长足的进步,这背后离不开政府的支持和政策的引导。

因此,本文将围绕高速铁路产业发展政策展开深入研究,分析其现状、问题及未来发展趋势。

二、高速铁路产业发展现状我国高速铁路网络已覆盖全国主要城市,总里程位居世界前列。

政府通过实施一系列政策措施,如加大投资、优化审批流程、鼓励技术创新等,推动了高速铁路产业的快速发展。

产业规模持续扩大,技术不断更新,服务质量显著提高。

三、高速铁路产业发展政策分析1. 政策支持政府出台了一系列支持高速铁路产业发展的政策,包括财政支持、税收优惠、土地使用优惠等,以促进产业发展。

此外,政府还加大了对高铁技术研究的投入,推动产业创新。

2. 基础设施建设政策政府重视高速铁路基础设施建设,通过实施“八纵八横”等高铁网络规划,加大资金投入,加快高铁线路建设。

同时,政府还鼓励企业参与高铁建设,通过PPP模式等吸引社会资本投入。

3. 产业协同发展政策高速铁路产业与相关产业协同发展,如旅游业、物流业、制造业等。

政府通过政策引导,促进产业间的协同发展,提高产业链的整体竞争力。

四、政策实施中存在的问题及挑战1. 政策执行力度不够部分地区在执行高速铁路产业发展政策时存在力度不够的问题,导致政策效果未能充分发挥。

2. 资金投入不足尽管政府加大了对高速铁路产业的投资,但仍存在资金投入不足的问题,尤其是对于一些中西部地区的高铁建设项目。

3. 技术创新压力增大随着高速铁路技术的不断发展,技术创新压力逐渐增大。

政府需加大技术研发支持力度,推动产业持续创新。

五、政策建议及未来发展趋势1. 加强政策执行力度政府应加强政策执行力度,确保各项政策措施落到实处,发挥政策效果。

同时,应建立完善的政策评估机制,对政策实施效果进行定期评估和调整。

高速铁路行业分析报告高速铁路行业分析报告一、定义高速铁路是在新一代铁路技术和设施和基础设施上的高速列车,快速地连接城市,提供高品质的乘客服务,并利用先进的技术设施来确保舒适和安全的旅行。

二、分类特点高速铁路可以分为两种类型:传统的高速旅客列车和高速动车。

高速旅客列车的速度可以超过300公里/小时,可以在1小时内连接两个城市。

旅客列车专门用于长途旅行,通常只有两到三个车站,并且旅客在列车上可以享受丰盛的餐饮和娱乐设施。

高速动车通常停靠更多的车站,并提供更多的旅游设施。

这种车辆的速度通常不到300公里/小时,但它们被设计用于城市之间更短的距离,因此它们更便宜和更高效地代替了地方。

三、产业链高速铁路产业链主要有四部分:1、装备制造包括高速铁路的轨道、车辆、控制系统和供电系统的制造商。

对于高速铁路的发展,装备制造商非常关键,能自主发展和生产高速铁路的厂家具有很强的市场竞争力。

2、服务方包括运营商、维护公司和物流公司。

运营商的任务是为乘客提供舒适、安全和高效的高速铁路服务。

维护公司有责任维持高速铁路在正常运行的条件下。

物流公司负责确保能够快速地处理旅客和货物。

3、投资方包括政府、银行和投资机构。

政府为高速铁路的建设提供资金支持,银行和投资机构提供融资。

4、旅客方无论是个人还是公司客户,他们都是高速铁路供应链的主要组成部分,对高速铁路行业的发展有着重要的影响。

四、发展历程中国高速铁路的发展可以追溯到1997年,当时中国开始建立自己的高速铁路系统。

2008年北京奥运会举办之前,中国高速铁路的里程只有1,428公里。

高速铁路在中国的发展呈指数增长,2008年之后,中国的高速铁路行业取得了巨大的进步。

2019年,中国高速铁路累计里程达到了3.5万公里,超过全世界其它国家的总和,成为全球高速铁路行业的领导者。

五、行业政策文件高速铁路行业政策文件包括:1、《高速铁路建设规划》规定了高速铁路的建设标准和路线规划,着重于建设快速、高效、安全的高速铁路。

高速铁路行业分析报告高速铁路行业分析报告一、定义高速铁路是指在轨道交通系统中,设计时速大于或等于200公里/小时,运营时速大于或等于250公里/小时的特种铁路运输方式。

二、分类特点高速铁路可分为城市轨道交通、旅客专线、干线高速铁路、跨境铁路等,其分类特点包括:运营速度快、运营效率高、载客能力大、安全性高、维护成本低等。

三、产业链高速铁路产业链主要包括原材料及零部件、制造商、系统集成商、运营商、维护服务商等,其中系统集成商为核心产业链环节。

四、发展历程我国高速铁路的发展历程可分为三个阶段:试验性发展阶段、规模化建设阶段、高品质发展阶段。

自2007年我国首次实现商业运营以来,高速铁路取得了长足的发展。

五、行业政策文件及其主要内容行业政策文件主要包括国家规划、法律法规、标准规范等,其中《中长期铁路网规划》是高速铁路发展的宏观规划文件,在未来的发展中将起到重要指导作用。

六、经济环境高速铁路行业在我国的经济环境中具有重要地位,其所带来的经济效益包括人员流动异地就业、物资网络便利快捷、经济交流增进等。

七、社会环境高速铁路行业对我国社会环境产生的影响包括人员流动异地就业、城市化进程加快、环保科技创新等。

八、技术环境高速铁路行业在技术环境方面的发展主要体现在高速铁路系统集成技术和高速列车运行技术的不断提升。

九、发展驱动因素高速铁路行业的发展驱动因素包括政策引领、投资支持、科技突破、市场需求等。

十、行业现状高速铁路行业在我国的现状主要表现在高速铁路建设规模壮大、运行效率不断提升、技术创新推进等方面。

十一、行业痛点高速铁路行业在发展过程中存在的痛点主要包括运营成本较高、票价较高、盈利能力受限等方面。

十二、行业发展建议加大投资力度、推进技术创新、降低运营成本、增强服务水平等是高速铁路行业发展的重要建议。

十三、行业发展趋势前景高速铁路行业未来的发展趋势主要体现在高速铁路网络覆盖全国、技术创新不断推进、服务水平不断提高等。

高铁配套件生产项目可行性研究报告申请报告【摘要】本报告对高铁配套件生产项目进行了可行性研究。

通过市场调研和竞争对手分析,发现高铁配套件市场需求旺盛且竞争激烈,项目具有较高的发展前景。

本报告同时进行了技术可行性、经济可行性、社会可行性和环境可行性的评估,认为项目在这些方面均具备可行性。

最后,提出了进一步开展该项目的建议和措施。

【关键词】高铁配套件;可行性研究一、项目背景与目标高铁的飞速发展和普及使得配套件市场需求不断增长。

本项目旨在利用自身技术优势,开展高铁配套件的生产,以满足市场需求并获得经济效益。

二、市场调研与竞争对手分析1.市场调研通过对高铁市场的调研,发现高铁配套件具有较大的市场需求。

近年来,高铁建设迅猛发展,高铁线路不断延伸,对高铁配套件提出了更高的要求。

2.竞争对手分析当前市场上已存在一些高铁配套件生产企业,其中一部分具有一定的规模和技术实力,竞争激烈。

但是,市场需求较大,增长空间仍然存在。

三、技术可行性分析1.技术储备公司已具备高铁配套件生产的基本工艺和设备,可适应该生产项目的要求。

2.技术进步性公司可以通过技术创新和研发,提高产品品质和技术水平,以满足市场需求。

3.技术风险技术风险存在,但可以通过加强技术研发和引入优秀人才来缓解。

四、经济可行性分析1.投资成本项目需要一定的投资成本,包括设备采购、人员培训和生产场地等方面。

2.预期收益通过市场需求和竞争对手分析,预期项目可以获得一定的市场份额和收益。

五、社会可行性分析1.就业机会项目的实施将提供大量的就业机会,带动当地经济发展,减少就业压力。

2.市场繁荣项目的推进将带动整个高铁行业的发展,推动市场的繁荣和产业链的扩展。

六、环境可行性分析项目生产过程中存在一定的环境影响,需在生产中采取相应的环保措施,减少对环境的负面影响。

七、项目建议和措施1.加强研发力量,提升产品技术水平。

2.充分发挥自身优势,通过品牌效应提升竞争力。

3.关注市场动态,及时调整市场策略。

China High-Speed RailwayAs the economic grow, intercity travel demand has increased dramatically in the Greater China Area. Traditional railways can hardly satisfy the passenger and freight travel demand, high speed rail is hence proposed and constructed after 1990s. This study aims to integrate current development of both rail-based and Maglev high speed trains in this area. From 1997, Taiwan kicked-off its high speed rail construction by importing the technology of Japanese Shinkansen. The Taiwan High Speed Rail is a 15-billion US dollars project. To save the cost of construction and management, the BOT model was applied. Though not totally satisfied, this project is still successful and ready to operate in the 4th quarter of 2007. China is preparing its high speed rail services by upgrading current networks. The capacity and operating speed are all increased after 5-times system upgrade. The 6th upgrade will be initiated in 2006. By then, trains will run at a speed of 200km/h in a total distance of 1,400km in 7 different routes. From the white paper published by the Ministry of Railway in China, there will be totally 8 rail-based High Speed Train services. Four of them are North-South bound, and four of them are East-West bound. 5 of the 8 High Speed Rails are now under construction, the first line will be finished in 2009, and the 2nd one will be in 2010. By 2020, there will be totally 12,000 kilometers high speed rail services in China. The 250 billion US dollars construction cost still leaves some uncertainties for all these projects. Finally, the future of the Maglev system in China is not so bright as rail-based. Shanghai airport line could be the first, also the last Maglev project in China if the approved Shanghai-Hangzhou line cannot raise enough 4.4 billion dollars to build it.Steel rail compositionSteel rail is composed of iron, carbon, manganese, and silicon, and contains impurities such as phosphorous, sulphur, gases, and slag. The proportions of these substances may be altered to achieve different properties, such as increased resistance to wear on curves.The standard configuration for North American rail resembles an upside down T. The three parts of T-rail are called the base, web, and head. The flat base enabled such rail to be spiked directly to wooden crossties; later, rail was placed on the now-standard steel tie plate. While the proportions and precise shape of rail are subject to constant analysis and refinement, the basic T-section has been standard since the mid-19th century.WeightThe most common way of describing rail is in terms of its weight per linear yard (the historic British unit of length), which is a function of its cross section. In the late 19th century, rail was produced in a range of sections weighing between 40 and 80 lbs. per yard. Weights increased over time, so that rail rolled today weighs between 112 and 145 lbs. (The Pennsylvania Railroad's 155-lb. section, used for a time after World War II, was the heaviest used in the U.S.)Jointed rail segmentsThe length of standard rails has historically been related to the length of the cars used to transport them. From an early range of 15-20 feet, rail length increased with car size until a standard of 39 feet (easily accommodated by the once-common 40-foot car) was reached. Even with the advent of today's longer cars, 39 feet has remained the standard for rail owing to limitations in steel mills and ease of handling.The joints in rail — its weakest points — can make for a rough ride, and are expensive to maintain. Individual rails are joined with steel pieces called joint (or angle) bars, which are held in place by four or six bolts. Today, the six-bolt type, once reserved for heavy-duty applications, is standard. The bolts in a joint bar are faced alternately outward and inward to guard against the remote possibility that a derailed car's wheel would shear them all off, causing the rails to part. Transition between rails of two different weights is achieved with special angle bars. In territory where the rails serve as conductors for signal systems, bond wires must be used at the joints to maintain the circuit.Welded railThe troublesome nature of rail joints prompted the most easily recognized advance in rail technology: the adoption of continuous welded rail (CWR).From its early use on a handful of roads in the 1940's, welded rail has come to be preferred for almost all applications. It is produced by welding standard 39-foot (or newer 78-foot) segments together into quarter-mile lengths at dedicated plants.The rails are transported to where they're needed in special trains, which are pulled slowly out from under the rail when it is to be unloaded. When in place, CWR is often field-welded into even greater lengths. Much jointed track survives because of the long lifespan of even moderately used rail, and because the specialized equipment needed for CWR installation is not economical for short distances.Managing the expansion and contraction that comes with temperature change is important with CWR. To avoid expanding and potential buckling when in service, welded rail is laid when temperatures are high (or is artificially heated). Rail anchors clipped on at the ties keep the rail from getting shorter as it contracts with falling temperatures. Thus constrained, it shrinks in cross section (height and width), but not in length. Because it's in tension, welded rail is treated with care during trackwork in cold weather.Maintaining and reusing railUnder heavy traffic, rails get worn down, although their life can be extended by grinding the head back to the proper contour.Rail no longer suited for main-line use may still have some light-duty life in it and is often relaid on branches, spurs, or in yards. Main-track reduction projects are also sources of such "relay" rail.When rail wear is uneven at a given location (such as a curve), rail may be transposed from one side to another to get maximum use out of it.中国高速铁路随着经济的增长,城市间的旅行需要在中国地区飞速增长。

高速铁路产业发展与推广研究报告一、引言高速铁路产业在现代交通领域的快速发展,成为国家经济发展的重要支撑。

本报告将对高速铁路产业发展与推广进行研究和分析。

二、高速铁路产业的背景1. 高速铁路产业起源高速铁路产业起源于西方发达国家,随着技术的不断进步,逐渐向全球范围推广。

2. 高速铁路发展的动力高速铁路的快速、安全、方便的优势,为其发展提供了坚实的动力。

三、高速铁路产业的成果1. 基础设施建设高速铁路产业的发展推动了基础设施建设的进展,提高了国家的交通运输效率。

2. 技术创新高速铁路产业的发展促进了相关技术的创新和发展,提升了国家的科技实力。

3. 经济效益高速铁路产业为国家带来了巨大的经济效益,推动了相关产业链的发展。

四、高速铁路产业的发展模式1. 投资与政策支持高速铁路产业的发展需要大量的投资和政策的支持,才能够实现良好的发展态势。

2. 技术与人才支持高速铁路产业发展需依靠先进技术和高素质人才的支持,才能获得长期发展。

3. 合作与竞争高速铁路产业的发展离不开国际间的合作和国内企业之间的竞争,形成良性循环。

五、高速铁路产业的推广国内现状1. 高铁网络建设中国高铁网络建设迅猛发展,已经形成了较为完善的运输体系。

2. 技术创新与标准制定国内高速铁路产业在技术创新和标准制定方面取得了突破,走在了世界前列。

3. 国内市场的发展高速铁路产业的快速发展推动了国内市场需求的增长,带动了相关产业的发展。

六、高速铁路产业的推广国际现状1. 高速铁路产业的国际影响力中国的高速铁路产业在国际上具有较大的影响力,成为许多国家学习的对象。

2. 国际市场的拓展中国高速铁路产业积极拓展国际市场,扩大了在国际竞争中的份额。

3. 技术转让与合作中国高速铁路产业积极推动技术转让与国际合作,提升了世界各国的铁路建设水平。

七、高速铁路产业的挑战1. 资金压力高速铁路产业的发展需要巨额的资金投入,对国家财政提出了很大的压力。

2. 技术壁垒高速铁路产业的技术壁垒较高,需要依靠科研机构和企业不断进行技术创新和突破。

高速铁路基础设施组件制造行业研究报告- High Speed Rail Infrastructure Component Manufacturing - 2010.6.【报告名称】:高速铁路基础设施组件制造行业研究报告- High Speed Rail Infrastructure Component Manufacturing - 2010.6.【报告页数】:166【报告来源】:SBI Energy【报告日期】:2010.6.【报告价格】:电子版RMB ¥500.00【订购联系人】报告快速购买通道,请联系admin@【报告摘要】: All4report [报告汇] is an industrial focused team, providing most up-to-date industrial analysis, marketing research reports, consulting reports across sectors. It provides free & sharing-base platform for exchange industrial information & trends.OVERVIEWDuring 2010, many nations will increase their roll out of high-speed rail (HSR) initiatives to make them a more integral part of their overall transportation infrastructure. Several countries in Europe that lack an HSR system have expressed their commitment to begin construction by the end of the year. Many Asian nations, too, have already begun HSR development projects that will be completed by 2015 or 2020. Manufacturers of a multitude of HSR components required to construct this complex transportation system stand waiting in the wings to capitalize on the potential need for their supply of goods and services. This SBI Energy report analyzes the market opportunities that global HSR manufacturers are eager to embrace through the next decade. We examine the critical trends driving HSR growth by region and forecast the value of this growth by each of the manufactured HSR components.Finally, we look at the socioeconomic and consumer-based trends affecting the HSR industry, such as the development of next-generation HSR products, safety issues, and long-term effects of HSR on a transportation economy.SBI Energy estimates that the global HSR manufacturing industry has amassed a total value of more than $244 billion (USD) for the five-year period of 2005 to 2009. Our sizing of the market takes into account sales of the pre-fabricated components required to construct several types of HSR systems, including Maglev and TGV, and incremental HSR added on to established railway routes. Our analysis of the market value is divided among these HSR systems and also comprises the sectors that produce the following HSR materials:•Rail bed: The rail bed encompasses the iron and steel rails and associated hardwarefor HSR tracks. In Maglev systems, the rail bed includes the guideway and suspension systems.•Railroad: This sector includes the manufacturing of railway coaches, bogies, coupling devices, wheels, brakes, and other components required to construct an HSR train.•Stations: The production of new HSR train facilities and terminals or the upgrading of established stations to accommodate an HSR railroad.高速铁路基础设施组件制造行业研究报告- High Speed Rail Infrastructure Component Manufacturing - 2010.6. 【报告目录】:Table of ContentsHigh Speed Rail Infrastructure Component ManufacturingChapter 1: Executive Summary (1)Table 1-1: Accumulated Market Value of HSR Manufacturing Sectorsby Type of HSR System, 2005 to 2009 (in $ millions) (2)Figure 1-1: Share of Miles of HSR Track Currently Installed, Under Construction, or Planned Construction, 2005 to 2009, Total Globaland Asian Countries (3)Energy Conservation Drives HSR Development (3)Table 1-2: Transportation Capital Stock by Mode, 1999, 2008 and2009 (in $ billions) (4)Demand for Freight Transportation Will Grow (5)Table 1-3: Commercial Freight Activity in the U.S. by TransportationMode, 2002 vs. 2009 (5)Transportation Effects of HSR (6)Figure 1-2: Total U.S. Railroad Stations and Amtrak’s Share of theTotal, 1995 to 2009 (7)U.S. Maglev Deployment Program Takes Off (7)Table 1-4: Projected Costs Per Mile of Maglev and Light-Rail Projects Worldwide (in $ millions) (8)Figure 1-3: Projected Country Share of HSR Miles by Type of HSRSystem, 2014 (9)United States Progresses to HSR Future (10)U.S. Imports of HSR Components Decline (11)Table 1-5: U.S. Shipment Value of HSR Manufacturing Components,2005 vs. 2009 (in $ millions) (12)Table 1-6: U.S. Shipment Value of HSR Manufacturing Components,2005 to 2009 (in $ millions) (13)Table 1-7: Projected Total of Newly Constructed Miles of HSR Tracks Installed, by HSR System in 2014 (14)China Develops Largest HSR Network (15)China Poised to Play Role in U.S. HSR Manufacturing (15)Europe Accelerates HSR Manufacturing (16)HSR Challenges Ahead (17)HSR Manufacturers Address Safety (19)Table 1-8: U.S. Transportation Fatalities by Mode of Transportation,2005 to 2009 (19)Chapter 2: Introduction and Overview (21)Report Scope (22)Methodology (22)HSR Background (23)高速铁路基础设施组件制造行业研究报告- High Speed Rail Infrastructure Component Manufacturing - 2010.6. Terminology (24)Maglev Technology Options (25)The German Technology (25)Japanese High-Speed Maglev Technology (25)Table 2-1: Planned Maglev HSR Manufacturing Projects in the U.S.and Germany (26)Transrapid International (TRI) Maglev System (26)Maglev 2000 System (27)U.S. Maglev Technology (28)Maglev Compared with Other Transportation Modes (29)Potential Maglev Disadvantages (30)Chapter 3: Global Activities in HSR Manufacturing (33)Energy Conservation Drives HSR Development (33)Table 3-1: U.S. Energy Consumption by Transportation Mode,2005 to 2009 (in Trillions BTUs) (34)Figure 3-1: Index of U.S. Ton-Miles of Freight by Mode ofTransportation, 1995 to 2009 (35)Table 3-2: Transportation Capital Stock by Mode, 1999, 2008 and2009 (in $ billions) (36)Table 3-3: Transportation System Mileage within the U.S. by Mode,2004 to 2009 (37)Table 3-4: Total Class-1 Rail Replaced or Added in the U.S.,1999 to 2009 (in thousands tons) (38)Demand for Freight Transportation Will Grow (38)Table 3-5: Commercial Freight Activity in the U.S. by TransportationMode, 2002 vs. 2009 (39)Figure 3-2: Total Rail Replaced or Added in the U.S., 1999 to 2009(in thousands of tons) (40)Figure 3-3: Share of Commercial Freight Activity in the U.S. by Modeof Transportation, 2002 vs. 2009 (41)Transportation Effects of HSR (42)Figure 3-4: Total U.S. Railroad Stations and Amtrak’s Share of theTotal, 1995 to 2009 (43)Table 3-6: Number of U.S. Stations Serviced by Amtrak and OtherClass 1 Rails, 1995 to 2009 (44)Table 3-7: Transit Passenger Miles by Type of Transportation Service,2005 to 2009 (in millions) (45)U.S. Maglev Deployment Program Takes Off (45)Table 3-8: Projected Costs Per Mile of Maglev and Light-Rail Projects Worldwide (in $ millions) (46)Table 3-9: Comparison of Capital Costs of TGV vs. Maglev HSRSystems (47)高速铁路基础设施组件制造行业研究报告- High Speed Rail Infrastructure Component Manufacturing - 2010.6. Table 3-10: Estimated Capital Costs of European HSR System(in $ millions) (47)Table 3-11: Estimated Capital Costs of U.S. Maglev HSR Systemvs. U.S. Metroliner Incremental HSR System (48)Figure 3-5: HSR Construction Costs Per Mile for Several Global HSRProjects (in $ millions) (49)United States Progresses to HSR Future (50)Baltimore-Washington Maglev Project (53)Pittsburgh Maglev Project (54)Las Vegas–Anaheim Maglev Project (55)China Develops Largest HSR Network (55)China Poised to Play Role in U.S. HSR Manufacturing (56)Japan Keeps Pace with HSR Development (58)Europe Accelerates HSR Manufacturing (59)Germany and U.K. Forge Maglev Projects (61)Spain Extends HSR Network (62)Chapter 4: The Global HSR Manufacturing Market (63)Table 4-1: Accumulated Market Value of HSR Manufacturing Sectorsby Type of HSR System, 2005 to 2009 (in $ millions) (63)Table 4-2: Length of HSR Track by Region Installed, UnderConstruction, and Planned, 2005 to 2009 (in miles) (65)Figure 4-1: Share of Miles of HSR Track Currently Installed, Under Construction, or Planned Construction, 2005 to 2009, Total Globaland Asian Countries (66)Table 4-3: Miles of HSR Track Installed Through 2009 by Type ofHSR System and Region (67)Figure 4-2: Share of Miles of HSR Track Currently Installed, Under Construction, or Planned Construction, 2005 to 2009, U.S. and Europe (68)Table 4-4: Share of Miles of HSR Tracks Installed by Type of HSRSystem and Region, 2005 to 2009 (69)Figure 4-3: Projected Country Share of HSR Miles by Type of HSRSystem, 2014 (70)Table 4-5: Market Value of HSR Manufacturing by Region,2005 to 2009 (in $ millions) (72)Figure 4-4: Market Share of HSR Manufacturing Sectors by HSRSystem Technology, 2009 (73)Figure 4-5: Projected Share of Market Value of HSR ManufacturingSectors in 2014, by HSR System Technology (75)Table 4-6: Projected Total of Newly Constructed Miles of HSR Tracks Installed, by HSR System in 2014 (76)Table 4-7: Projected Accumulated Market Value of HSR高速铁路基础设施组件制造行业研究报告- High Speed Rail Infrastructure Component Manufacturing - 2010.6. Manufacturing by Type of HSR System, 2010 to 2014(in $ millions) (77)Table 4-8: Market Value of Maglev HSR Manufacturing by Region,2005 to 2009 (in $ millions) (78)Table 4-9: Market Value of TGV HSR Manufacturing, 2005 to 2009,by Region (in $ millions) (79)Table 4-10: Projected Market Value of TGV Manufacturing,2010 to 2014, by Region (in $ millions) (80)Figure 4-6: Share of Maglev HSR Manufacturing by Region,2010 vs. 2014 (81)Figure 4-7: Share of TGV HSR Manufacturing by Region,2010 vs. 2014 (81)Table 4-11: Projected Market Value of Maglev HSR Manufacturingby Region, 2010 to 2014 (in $ Millions) (82)Table 4-12: Market Value of TGV HSR Manufacturing Sectors,2005 to 2009, by Region (in $ millions) (83)Table 4-13: Market Value of Maglev HSR Manufacturing,2005 to 2009, by Region (in $ millions) (84)Table 4-14: Accumulated Market Value of HSR Manufacturing byType of HSR System and Manufacturing Sector, 2010 to 2014(in $ millions) (84)Table 4-15: Projected Market Value of TGV Manufacturing,2010 to 2014, by Region and Manufacturing Sector (in $ millions) (85)Table 4-16: Projected Market Value of Maglev Manufacturing,2010 to 2014, by Region and Manufacturing Sector (in $ millions) (86)Table 4-17: CAGR of TGV HSR Manufacturing by Sector,2005 to 2014 (87)Table 4-18: CAGR of Maglev HSR Manufacturing by Sector andRegion, 2005 to 2014 (88)Figure 4-8: CAGR of HSR Manufacturing Sectors, 2005 to 2014 (89)Projected Growth of HSR Components (89)Figure 4-9: Projected CAGR of Market Value of HSR Components,2010 to 2014 (90)Table 4-19: Projected Global Market Value of Railroad Components,2010 to 2014 (91)Table 4-20: Projected Global Market Value of Rail Bed Components,2010 to 2014 (91)Table 4-21: Projected Global Market Value of HSR StationComponents, 2010 to 2014 (92)Table 4-22: Projected Global Market Value of HSR TechnologyComponents, 2010 to 2014 (92)U.S. Import and Export Value of HSR Manufacturing (92)Figure 4-10: Share of Imports and Exports Conducted by Rail高速铁路基础设施组件制造行业研究报告- High Speed Rail Infrastructure Component Manufacturing - 2010.6. between NAFTA Countries, 1995 to 2009 (93)U.S. Imports of HSR Components Decline (93)Table 4-23: U.S. Shipment Value of HSR Manufacturing Components,2005 vs. 2009 (in $ millions) (94)Table 4-24: U.S. Shipment Value of HSR Manufacturing Components,2005 to 2009 (in $ millions) (95)Table 4-25: Share of U.S. Shipment Value of HSR Manufacturing Components, 2005 vs. 2009 (96)Figure 4-11: Share of U.S. Imports by Country of Iron Rails Used forHSR Manufacturing, 2009 (97)Table 4-26: U.S. Import Value of HSR Manufacturing Components,2005 vs. 2009 (in $ thousands) (98)Table 4-27: U.S. Imports by Country of Electromagnetic CouplingsUsed in HSR Manufacturing (in $ thousands) (99)Figure 4-12: Share of U.S. Exports by Country of Iron Rails Usedfor HSR Manufacturing, 2009 (100)Table 4-28: U.S. Export Value of HSR Manufacturing Components,2005 vs. 2009 (in $ thousands) (101)Chapter 5: Competitive Profiles (103)Bombardier, Inc. (104)Overview and Performance (104)Figure 5-1: Bombardier Revenues and Year-over-Year PercentChange, 2006 to 2010 (105)GE Technology Infrastructure (107)Overview and Performance (107)Table 5-1: General Electric Co. Infrastructure Division Revenues,2004 to 2009 (e) (in $Billions) (108)Figure 5-2: Share of General Electric Revenue for 2009, by GEBusiness Unit (in $ billions) (108)Research & Development (109)Alstom (110)Overview and Performance (110)Table 5-2: Alstom Revenues by Business Unit, 2008 vs. 2009 (111)Figure 5-3: Alstom’s Share of Revenue by Business Segment,2008 vs. 2009 (112)Research & Development (112)Siemens Mobility (114)Overview and Performance (114)Table 5-3: Siemens Revenues, 2008 to 2009, by Business Unit(in $ billions) (116)Significant Developments (117)Kawasaki Heavy Industries (118)高速铁路基础设施组件制造行业研究报告- High Speed Rail Infrastructure Component Manufacturing - 2010.6. Overview and Performance (118)Outlook (119)Figure 5-4: Kawasaki Heavy Industries Revenues andYear-Over-Year Percent Change, 2005 to 2009 (121)HSR Component Manufacturers (121)Wabtec Corp. (121)National Railway Equipment Co. (122)New York Air Brake Corp. (122)ORX (123)Ronsco (123)Liaoning MEC Group Co. (123)ZTR Control Systems (123)Talgo (124)Koni-Enidine (124)Chapter 6: High-Speed Rail Manufacturing Challenges (127)Critical Challenge One: Securing HSR Funding (128)Laying of Legislative HSR Foundation (129)Figure 6-1: Share of Miles Traveled to Home, Work, School,Recreation, Shopping, and Other Reasons in the U.S. byMode of Transportation, 2009 (132)HSR Lobbying Activity Escalates in the U.S. (133)Critical Challenge Two: HSR Manufacturers Address Safety (137)Table 6-1: Top Speeds, Weights and Acceleration Statistics by Typeof HSR (138)Track Sharing Approved (138)Table 6-2: U.S. Transportation Fatalities by Mode of Transportation,2005 to 2009 (140)Table 6-3: U.S. Transportation Accidents by Mode of Transportation,2005 to 2009 (141)Maglev Safety Issues Differ from TGV (142)Asia Challenges U.S. on HSR Safety (142)Japan Advises on Safety in U.S. (143)Critical Challenge Three: Innovations Help Differentiate HSR Systems (144)Innovation Occurring in Train Controls (145)U.S. HSR Control Systems (147)Figure 6-2: Causes of Train Accidents in the U.S., 2007 (148)Appendix (i)。