201112 FINANCIAL AID REFUND CHECK SCHEDULE

- 格式:pdf

- 大小:73.09 KB

- 文档页数:2

财务结账校验产品设计流程英文回答:The process of designing a financial closingverification product involves several steps to ensure accuracy and efficiency. Here is a breakdown of the process:1. Define the objectives: The first step is to clearly define the objectives of the financial closing verification product. This involves understanding the specific requirements and goals of the organization. For example,the product may need to verify the accuracy of financial statements, detect fraudulent activities, or ensure compliance with regulations.2. Gather requirements: Once the objectives are defined, the next step is to gather the requirements for the product. This includes identifying the data sources, the types of checks and validations needed, and any specific rules or criteria that need to be applied. For example, the productmay need to check for duplicate transactions, validate account balances, or verify the accuracy of tax calculations.3. Design the system: With the requirements in hand, the next step is to design the system architecture and user interface. This involves determining the technology stack, database structure, and the user interface design. For example, the system may be designed as a web-based application with a responsive user interface and a relational database.4. Develop the product: Once the system design is finalized, the development of the product can begin. This involves writing the code, integrating with external systems, and conducting thorough testing to ensure the product functions as intended. For example, the product may be developed using programming languages such as Python or Java, and it may need to integrate with accounting software or data warehouses.5. Test and validate: After the product is developed,it needs to be thoroughly tested and validated. This includes conducting unit tests, integration tests, and user acceptance tests to ensure all requirements are met and the product functions correctly. For example, the product maybe tested by creating test scenarios and comparing the expected results with the actual results.6. Deploy and monitor: Once the product is tested and validated, it can be deployed in the production environment. This involves setting up the necessary infrastructure, migrating data, and training users on how to use the product. Additionally, monitoring tools should be put in place to track the performance and usage of the product.For example, the product may be deployed on a cloud-based server and monitored using tools like Splunk or New Relic.7. Continuous improvement: The process of designing a financial closing verification product does not end with deployment. It is important to continuously monitor and improve the product based on user feedback and changing requirements. This involves collecting user feedback, analyzing metrics, and implementing updates andenhancements to the product. For example, based on user feedback, the product may be enhanced to include additional validation checks or improve the user interface.中文回答:财务结账校验产品设计流程涉及多个步骤,以确保准确性和效率。

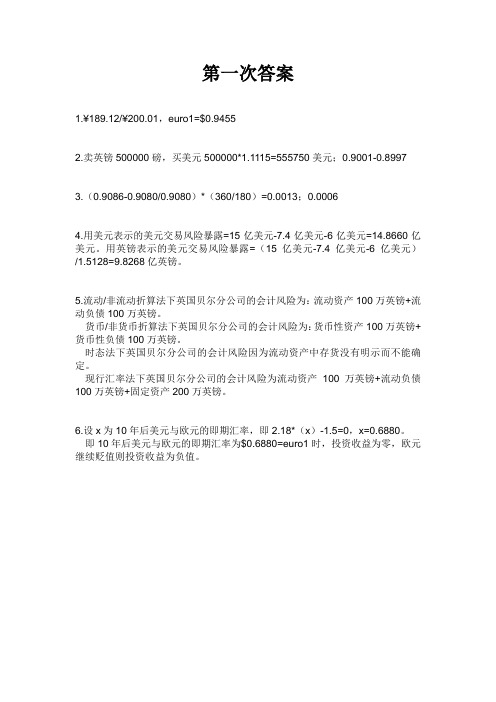

1.¥189.12/¥200.01,euro1=$0.94552.卖英镑500000磅,买美元500000*1.1115=555750美元;0.9001-0.89973.(0.9086-0.9080/0.9080)*(360/180)=0.0013;0.00064.用美元表示的美元交易风险暴露=15亿美元-7.4亿美元-6亿美元=14.8660亿美元。

用英镑表示的美元交易风险暴露=(15亿美元-7.4亿美元-6亿美元)/1.5128=9.8268亿英镑。

5.流动/非流动折算法下英国贝尔分公司的会计风险为:流动资产100万英镑+流动负债100万英镑。

货币/非货币折算法下英国贝尔分公司的会计风险为:货币性资产100万英镑+货币性负债100万英镑。

时态法下英国贝尔分公司的会计风险因为流动资产中存货没有明示而不能确定。

现行汇率法下英国贝尔分公司的会计风险为流动资产100万英镑+流动负债100万英镑+固定资产200万英镑。

6.设x为10年后美元与欧元的即期汇率,即2.18*(x)-1.5=0,x=0.6880。

即10年后美元与欧元的即期汇率为$0.6880=euro1时,投资收益为零,欧元继续贬值则投资收益为负值。

1.国际企业的资金来源:(1)来自于公司内部:1)母公司或子公司本身的未分配利润和公司集团内部积存的折旧基金。

2)公司集团内部相互提供的资金。

主要有各子公司向母公司上缴的利润及划拨的资金,母公司向子公司输送的资金及子公司之间相互提供的资金。

(2)来自于母公司所在国的金融市场。

(3)来自于子公司所在国的金融市场。

(4)来自于国际金融市场:1)向第三国或国际金融机构借款。

2)向国际资本市场融资。

与国内公司相比,其优势在于:(1)资金来源更加广泛。

(2)融资方式更加多样化。

(3)国际融资风险较大。

2.企业国际股票融资的程序包括发行前的准备、起草招股说明书和进行核实、香港联交所或美国证券交易委员会(SEC)的审查和批准过程和股票发行四个步骤。

The University of Hong Kong2011 Financial ReportTreasurer’s Report1Governance of the University6Independent Auditor’s Report8Consolidated Statement of Comprehensive Income10Statement of Comprehensive Income11Consolidated Balance Sheet12Balance Sheet13Consolidated Statement of Cash Flows14Consolidated Statement of Changes in Fund Balances16Notes to the Consolidated Financial Statements17The University of Hong KongOVERVIEWThe financial year 2010-11 was the second year of the last Triennium of the three-year structure curriculum. The Group’s consolidated financial results recorded a surplus of $1,518 million which was largely attributed to the continued recovery of the investment asset value since the global financial crises that took off from September 2008 and partly to the receipt of the matching grant under the fifth Government Matching Grant Scheme introduced in June 2010, from which the University was able to reach the upper limit of $220 million set for each institution. While approaching to the year 2012 when the four-year curriculum structure takes place, the University requires substantial resources to prepare for the double cohort of students in all spheres including the preparation for the curriculum reform and the provision of additional space and infrastructure for teaching and learning. At the same time, the University is also investing in initiatives to further the University vision in alignment with its strategic direction. The University has thus been working on tight financial resources.In preparing the consolidated financial statements, the Group has adopted certain new/revised Hong Kong Accounting Standards (“HKAS”) and Hong Kong Financial Reporting Standards (“HKFRS”) (Collectively “HKFRSs”) issued by the Hong Kong Institute of Certified Public Accountants which are effective and relevant to the Group’s operation.RESULTS FOR THE YEARThe Group’s consolidated results for the year ended 30 June 2011are summarized as follows:20112010$ million$ millionIncome6,4246,110Expenditure(6,172)(5,984)Interest and Investment Gain1,255705Surplus for the year before Share of Surplus of Associates and Jointly Controlled Entities 1,507831Share of Surplus of Associates and Jointly Controlled Entities1111Surplus for the year1,518842The consolidated income for the year 2010-11 has increased by $314 million. This was mainly attributable to the increase in government subvention for the Fifth Matching Grant Scheme introduced in June 2010.2011 Financial ReportOn the consolidated expenditure, a total of $6,172 million was incurred for the year (2009-10: $5,984 million), of which $4,734 million (2009-10: $4,641 million) was spent on teaching/learning and research activities of the Group. If the total depreciation and amortization charges of $333 million (2009-10: $280 million) were excluded, the expenditure incurred for the year was approximately 2.5 per cent higher than that of the previous year.INVESTMENTSThe Group’s total investment funds, comprising the General Endowment Fund, General Funds and Specific Funds, amounted to $13,500 million on average in 2011 (2009-10: $12,800 million), an increase of $700 million from 2010. The increase in investment fund size was mainly due to increase in investment asset price and additional donations and grants received during the year.The Group continues to adopt a prudent, disciplined, diversified and long-term approach to its investments. The Group recorded an overall investment gain of $1,255 million for the year, as compared with $705 million in 2010.The investment portfolio securities, being valued at fair value on a consistent basis, generated an overall positive return of 10.4 per cent for the year (2009-10: 6.3 per cent).RESEARCH GRANTS In addition to funding the basic research infrastructure through the block grant, the UGC also provides earmarked grants through the Research Grants Council (“RGC”), partly by direct allocations to the eight institutions to be used as research grants to staff, and partly by awards for competitive bids by individual principal investigators or institutions. The amounts of research grants received and receivable by the University through direct allocations were $14 million (2009-10: $14 million). During the year, the University has been awarded grants totalling $224 million (2009-10: $216 million) through the RGC competitive bids exercise, $74 million of the grants, representing 50% of the General Research Grant would be released to the University in August of the following financial year pursuant to the latest disbursement arrangement of the RGC. The University also received a transfer of $8 million (2009-10: $11 million) from other tertiary institutions for joint research projects. On the related research expenditure side, a total of $215 million was incurred for the year (2009-10: $196 million).DONATIONSDuring the year under review, donations totalling $1,033 million (2009-10: $895 million) were received, of which $127 million (2009-10: $131 million) was for research, $241 million (2009-10: $207 million) for capital building and alterations, additions & improvements projects, $47 million (2009-10: $81 million) for scholarships, bursaries, prizes and loans, and $502 million (2009-10: $397 million) for various purposes, in addition to the $116 million (2009-10: $79 million) for endowments.For accounting purpose, donations and benefactions of $698 million (2009-10: $819 million) was recorded as income in the Consolidated Statement of Comprehensive Income while $116 million (2009-10: $79 million) was recorded as endowment under reserve movement. CAPITAL BUILDING AND ALTERATIONS, ADDITIONS & IMPROVEMENTS PROJECTSIn 2010-11, the University received funding of $966 million (2009-10: $574 million) comprising government subventions of $725 million (2009-10: $367 million) and donations of $241 million (2009-10: $207 million) for its capital programmes covering building projects and other alterations, additions and improvements works. This income was recorded as deferred income in the financial statements. In terms of expenditure, a total of $1,101 million was incurred for the year (2009-10: $536 million), of which $1,053 million (2009-10: $488 million) was spent on capital projects and capitalised as either as construction in progress or building upon completion, and another $48 million (2009-10: $48 million) was expensed in the Income and Expenditure account.The University, under the strategic steering of the Campus Development and Planning Committee, is continuing to plan for the physical development of the campus to meet the projected increase in demand for space as a result of the change to the curriculum structure and the resulting increase in student and staff numbers as well as for the continuing provision of facility and accommodation consistent with the strategic aim to develop the University to the highest level of academic excellence.Construction for the Centennial Campus has been progressing as scheduled. It includes the construction of three academic buildings atop a podium housing central classrooms and learning common facilities with an overall net operable floor area of approximately 42,000 square metres. The project is expected to achieve practical completion in March 2012 to be followed by internal fitting-out and furnishing. It is anticipated that the Centennial Campus will be ready for moving-in by the faculties in mid 2012, and be ready for the in-take of the double cohort of students in the academic year 2012-13. Construction works under the University Street project have been on-going with works being completed in phases. Phase I includes works within the site boundary of the Centennial Campus and is expected to be completed concurrently with the Centennial Campus by the middle of 2012. Phase 2 is being completed in stages with the new canteen at Haking Wong Building started its operation in December 2010 and major renovation works at Composite Building completed and handed over to the Student Union for occupation in July 2011. Other remaining works including phase 3 that extend the University Street to the Sun Yat-Sen Plaza are on-going. The entire project is expected to be substantially completed by 2012.The University of Hong Kong2011 Financial ReportThe Lung Wah Street Student Residence project in Kennedy Town will provide an additional 1,800 residential places for both undergraduate and postgraduate students. The construction of the foundation was completed in 2010 and the superstructure works also commenced in the 4th quarter of the same year. The project is planned to be completed in the latter half of 2012.The project for the construction of Hong Kong Jockey Club Building for Interdisciplinary Research was completed in June 2011 with user departments starting to move-in from the second half of the year. It will provide an additional floor space of about 8,000 square metres with advanced technologies and facilities to cultivate a multi-disciplinary environment for fundamental human research.HKU SCHOOL OF PROFESSIONAL AND CONTINUING EDUCATIONThe School’s enrolment levels consolidated in 2010/11 with 87,797 students enrolled on courses, representing a full-time student equivalent load of some 21,982. Total income for the year increased by 2.7 per cent when compared with the previous year while the expenses increased by 2.9 per cent. A net surplus of $55 million was recorded in the School’s consolidated statement of comprehensive income (2009/10: $54 million), after an annual contribution of $26 million was made to the University (2009/10: $26 million). With its commitments to provide the best in professional and continuing education services in Hong Kong and the region, the School will continue to invest surplus funds generated to develop new programmes and to improve learning and other facilities in the School.In addition to the School’s own Community College, the full-time sub-degree programme activities of the School include the HKU SPACE Po Leung Kuk Community College which is jointly controlled by the School and Po Leung Kuk. A range of new full-time programmes has been offered by the College at its campus in Leighton Road, Causeway Bay and this helped to ensure its continued success in student recruitment.While the current levels of demand appear unlikely to diminish, the continuing education/lifelong learning sector in Hong Kong remains highly competitive. The School is committed to responding to community demand in the dynamic environment of lifelong learning in fulfilment of the University’s mission statement.FINANCIAL OUTLOOKWith the end of the financial year 2010-11, the University has entered into the last year of the triennium before transiting to the four-year structure curriculum. As the year 2012 approaches, full heed has been given to prepare for the new curriculum structure and to receive the double cohorts of students. The year 2011 marks the Centenary of the University. The University is conscious of the competitive environment both locally and globally. With academic excellence underpinning the University’s strategic development, the University is prepared to invest in initiatives that steer the University to further institutional advancement. Given the marginal rate of Government funding for the extra year of the new curriculum, the uncertain future economic outlook arising from the Euro debt and confidence crises surrounding the financial markets and the persistence of the extremely low interest rate environment which impacts upon the University income sources particularly from investment and fund-raising activities, the University has to be more cautious and prudent in financial management to facilitate the long-term growth of the University during this difficult period.Paul M.Y. ChowTreasurerHong Kong, 25 October 2011The University of Hong Kong2011 Financial ReportThe following statement is given to assist readers of the Consolidated Financial Statements to understand the governance structure of the University.SUMMARY OF THE UNIVERSITY’S STRUCTURE OF GOVERNANCEThe University’s structure of governance comprises a Court, a Council and a Senate whose respective constitutions, powers and duties shall be prescribed by the University Ordinance and statutes.The Court is the University’s supreme advisory body and comprises representatives of the University and other stakeholders. The Court offers a means whereby the wider interests of the communities served by the University can be represented and it provides a public forum where members of the Court can raise matters about the University.The Council is the University’s supreme governing body and is responsible for the University’s finances and investments, the management of estate and buildings, staff appointments and terms and conditions of service, and drafting of Statutes.The Senate is the principal academic authority of the University. The Vice-Chancellor chairs the Senate which comprises mainly academic staff and students. Decisions of the Senate on academic matters which have financial or resource implications are subject to approval by the Council. Conversely, decisions by the Council which have academic implications are subject to consultation with the Senate, which is normally the initiating body in such matters.The University follows international best practice in regularly reviewing its governance (as well as management) structure. A Fit for Purposes governance structure was adopted from 2003 following a review pursuant to the recommendation of the University Grants Committee’s Higher Education Review (2002). The “Five Year Review of Fit for Purpose” was conducted and the report had been considered by the Council in 2009 which re-affirmed the Council as the de facto supreme governing body of the University and operates to the trustee model. A Guide and Code of Practice for Members of the Council has also been published to help enhance the transparency and accountability of the governing body and conform to the highest standard of corporate governance.The Council, the supreme governing body of the University, now comprises 16 lay members and 8 University members (both staff and students).The Council met 12 times during 2010-11 and has several Committees including a Finance Committee, an Audit Committee, a Human Resources Policy Committee, a Campus Development and Planning Committee and a Nomination Committee. These committees are formally constituted with terms of reference and they comprise mainly lay members of the Council, one of whom is the Chair.The F inance Committee met 3 times during 2010-11. The Committee advises the Council on all matters within the jurisdiction of the Council which have financial implications and performs the functions laid upon the Committee by the Statutes (Financial procedures), and by the Council’s Budgetary Control Regulations. The Finance Committee appoints an Investments Sub-Committee to oversee and advise on the University’s investment strategy and controls. The Investments Sub-Committee meets regularly and reports significant investment matters to the Finance Committee. The Audit Committee met 4 times during 2010-11. The Committee reviews the effectiveness of the University’s financial and other control systems, satisfies itself that satisfactory arrangements are in place to promote efficiency and effectiveness and advises the Council on risk management and the effectiveness of accounting procedures. It reviews the external auditor’s report and the scope and effectiveness of the internal auditor’s work and advises Council on the appointment of the external auditor. Whilst senior executives attend meetings of the Audit Committee as necessary, they are not members of the Committee and the Committee does meet with the internal and external auditors on their own for independent discussions.The Human Resources Policy Committee dealt with most policy-related matters in circulation and held 5 meetings during 2010-11. The Committee reviews matters on human resource policy such as staff recruitment, retention and development, performance management, workforce planning, succession planning, terms and conditions of service and remuneration strategies, and to advise the Council thereon. It reviews and determines the salaries and terms and conditions of service of officers whose salaries fall outside any pre-determined salary scale/range, and to consider and decide any severance payment for such staff.The Campus Development and Planning Committee met 4 times during 2010-11. The Committee advises the Council on matters relating to the physical development and planning of the University campuses and keep under review operational policies, standards and procedures in connection with University building works and facilities management.The Nominations Committee considers nominations for lay vacancies in the Council membership under the relevant ordinance. In addition, the Senate is the principal academic authority of the University and comprises 51 members who are mainly academic staff while there are also student representatives. Under the Statutes, the Senate is responsible for regulating and directing the academic work of the University in teaching, examining and research, for the award of all Degrees, Diplomas, Certificates and other academic distinction of the University and for the discipline of the students of the University and for the enforcement of such discipline.The University of Hong Kong2011 Financial ReportWe have audited the consolidated financial statements of The University of Hong Kong (the “University”) and its subsidiaries (together, the “Group”) set out on pages 10 to 95, which comprise the consolidated and University balance sheets as at 30 June 2011, and the consolidated and University statement of comprehensive income, the consolidated statement of changes in fund balances and the consolidated statement of cash flows for the year then ended, and a summary of significant accounting policies and other explanatory information.R E S P O N S I B I L I T Y O F T H E C O U N C I L O F T H E UNIVERSITY FOR THE CONSOLIDATED FINANCIAL STATEMENTSThe Council of the University is responsible for the preparation of consolidated financial statements that give a true and fair view in accordance with Hong Kong Financial Reporting Standards issued by the Hong Kong Institute of Certified Public Accountants, and for such internal control as the Council of the University determine is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.AUDITOR’S RESPONSIBILITYOur responsibility is to express an opinion on these consolidated financial statements based on our audit and to report our opinion solely to you, as a body, in accordance with the Statutes of the University and for no other purpose. We do not assume responsibility towards or accept liability to any other person for the contents of this report.We conducted our audit in accordance with Hong Kong Standards on Auditing issued by the Hong Kong Institute of Certified Public Accountants. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements arefree from material misstatement.The University of Hong KongAn audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation of consolidated financial statements that give a true and fair view in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the Council of the University, as well as evaluating the overall presentation of the consolidated financial statements.We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.OPINIONIn our opinion, the consolidated financial statements give a true and fair view of the state of affairs of the University and of the Group as at 30 June 2011, and of the results of the University and the Group and the cash flows of the Group for the year then ended in accordance with Hong Kong Financial Reporting Standards.PricewaterhouseCoopers Certified Public Accountants Hong Kong, 25 October 20112011 Financial Report(Expressed in thousands of Hong Kong dollars)(Note20112010IncomeGovernment Subventions23,091,3682,794,812Tuition, Programmes and Other Fees 31,930,6961,839,605Donations and Benefactions 4698,577818,782Auxiliary Services 5224,155203,304Other Income6479,371454,115 6,424,1676,110,618Expenditure 7Learning and Research Instruction and Research 4,205,5324,080,340Library 194,150196,525Central Computing Facilities 125,538156,390Other Academic Services 208,536207,791Institutional Support Management and General 400,395368,177Premises and Related Expenses 707,066679,054Student and General Education Services 222,216202,622Other Activities108,94193,332 6,172,3745,984,231Interest and Investment Gain 81,255,602704,845Surplus from Operations 1,507,395831,232Share of Losses of Associates 13(9)(10)Share of Surplus of Jointly Controlled Entities1410,98211,380Surplus for the Year1,518,368842,602Other Comprehensive LossRelease of Deferred Capital Funds 25(47,449)(23,786)Exchange Differences2,295– (45,154)(23,786)Total Comprehensive Income for the Year1,473,214818,816The University of Hong Kong(Expressed in thousands of Hong Kong dollars)Note20112010IncomeGovernment Subventions23,089,6932,793,696Tuition, Programmes and Other Fees 31,102,5501,033,821Donations and Benefactions 4694,611794,149Auxiliary Services 5218,516198,318Other Income6465,265457,661 5,570,6355,277,645Expenditure 7Learning and Research Instruction and Research 3,873,5833,756,084Library 195,731198,632Central Computing Facilities 103,183135,887Other Academic Services 63,42561,591Institutional Support Management and General 232,838215,304Premises and Related Expenses 585,260549,481Student and General Education Services 217,672202,596Other Activities81,81271,859 5,353,5045,191,434Interest and Investment Gain 81,250,060700,990Surplus for the Year1,467,191787,201Other Comprehensive LossRelease of Deferred Capital Funds 25(47,449)(23,786) Total Comprehensive Income for the Year1,419,742763,4152011 Financial Report(Expressed in thousands of Hong Kong dollars)Note20112010ASSETSNon-Current AssetsProperty, Plant and Equipment 116,312,9715,414,233Intangible Assets1230,962–Interest in Associates13664673Interest in Jointly Controlled Entities 14(i)56,55044,414Available-for-Sale Financial Assets 151,4311,431Held-to-Maturity Investments16904,9311,199,945Financial Assets at Fair Value through Profit or Loss 178,704,1876,738,102Loans Receivable1810,37117,169 16,022,06713,415,967 Current AssetsHeld-to-Maturity Investments16427,869255,996Financial Assets at Fair Value through Profit or Loss 175,738631Loans Receivable 18185,772188,202Inventories5,7914,833Accounts Receivable and Prepayments 19584,116337,291Amount due from Jointly Controlled Entities14(i)11,23019,258Bank Deposits with Original Maturity over Three Months 1,156,6503,037,145Cash and Cash Equivalents 202,853,6751,248,458 5,230,8415,091,814 TOTAL ASSETS21,252,90818,507,781FUNDSDeferred Capital Funds 252,132,9211,223,118Restricted Funds 96,274,0505,990,153Other Funds 109,516,4968,248,163 TOTAL FUNDS17,923,46715,461,434 LIABILITIESNon-Current LiabilitiesAccounts Payable and Accruals 2399,903–Employee Benefit Accruals 21138,292205,113Loans and Borrowings 22244,087264,787 482,282469,900 Current LiabilitiesAccounts Payable and Accruals231,549,4681,362,844Amount due to a Jointly Controlled Entity 14(i)431424Employee Benefit Accruals 21519,846439,247Loans and Borrowings 22129,841131,857Deferred Income 24647,573642,075 2,847,1592,576,447 TOTAL LIABILITIES3,329,4413,046,347 TOTAL FUNDS AND LIABILITIES 21,252,90818,507,781 NET CURRENT ASSETS2,383,6822,515,367 TOTAL ASSETS LESS CURRENT LIABILITIES18,405,74915,931,334L.C. TSUI PAUL M.Y. CHOWP.B.L. LAMVice-ChancellorTreasurer Director of FinanceHong Kong, 25 October 2011The University of Hong Kong(Expressed in thousands of Hong Kong dollars)Note20112010ASSETSNon-Current AssetsProperty, Plant and Equipment 115,547,0434,660,261Intangible Assets1223,824–Available-for-Sale Financial Assets 15234234Held-to-Maturity Investments16904,9311,199,945Financial Assets at Fair Value through Profit or Loss 178,704,1876,738,102Loan to a Jointly Controlled Entity 2,2013,200Loans Receivable18256,444283,017 15,438,86412,884,759Current AssetsHeld-to-Maturity Investments 16427,869235,996Loans Receivable 18207,681210,111Inventories 4,8934,123Accounts Receivable and Prepayments 19569,902304,390Bank Deposits with Original Maturity over Three Months 826,3672,583,364Cash and Cash Equivalents202,617,5641,199,878 4,654,2764,537,862 TOTAL ASSETS 20,093,14017,422,621FUNDSDeferred Capital Funds 252,132,9211,223,118Restricted Funds 96,274,8705,990,973Other Funds 108,645,3657,430,504 TOTAL FUNDS17,053,15614,644,595LIABILITIESNon-Current LiabilitiesAccounts Payable and Accruals 2399,903–Employee Benefit Accruals 21138,292205,113Loans and Borrowings22244,087264,787 482,282469,900Current LiabilitiesAccounts Payable and Accruals231,308,5771,140,068Amount due to a Jointly Controlled Entity 431424Employee Benefit Accruals 21472,162394,416Loans and Borrowings 22129,841131,857Deferred Income24646,691641,361 2,557,7022,308,126 TOTAL LIABILITIES3,039,9842,778,026 TOTAL FUNDS AND LIABILITIES 20,093,14017,422,621 NET CURRENT ASSETS2,096,5742,229,736 TOTAL ASSETS LESS CURRENT LIABILITIES17,535,43815,114,495L.C. TSUIPAUL M.Y. CHOWP.B.L. LAMVice-ChancellorTreasurer Director of FinanceHong Kong, 25 October 20112011 Financial Report(Expressed in thousands of Hong Kong dollars)20112010Cash Flows from Operating Activities Surplus for the Year 1,518,368842,602Adjustments for:Depreciation of Property, Plant and Equipment 325,566280,474(Gain)/Loss on Disposal of Property,Plant and Equipment(44)111Amortisation of Intangible Assets7,740–Gain on Disposal of a Subsidiary and an Associate–(1,822)Share of Losses of Associates910Share of Surplus of Jointly Controlled Entities(10,982)(11,380)Amortised cost on loans from HKSAR Government 241–Interest Expenses 3,7093,965Donation in-kind(306,457)(700)Interest and Investment Gain (1,255,602)(704,845)Operating Surplus before Working Capital Changes282,548408,415Decrease in Amount Due from Jointly Controlled Entities8,02810,138Increase in Amount Due to a Jointly Controlled Entity7424Decrease in Staff Loans Receivable10,4841,882Decrease/(Increase) in Student Loans Receivable 431(20)Increase in Other Loans Receivable (1,687)(563)Increase in Inventories(958)(998)Increase in Accounts Receivable and Prepayments (244,880)(111,283)Increase/(Decrease) in Accounts Payable and Accruals173,682(2,243)Increase in Employee Benefit Accruals 13,7787,708Increase in Deferred Income 5,49866,976Cash Generated from Operations 246,931380,436Loan Interest Income Received2,9733,440 Net Cash Generated from Operating Activities 249,904383,876Cash Flows from Investing ActivitiesPurchase of Property, Plant and Equipment (1,113,340)(664,337)Proceeds from Sale of Property,Plant and Equipment1,551976Acquisition of Intangible Assets(38,702)–Decrease in Loan to a Jointly Controlled Entity999–Payment for Purchase of Investments (3,370,519)(2,436,244)Proceeds from Disposals of Investments 2,831,2792,871,210Decrease/(Increase) in Bank Deposits 1,880,495(1,844,008)Interest and Investment Income Received 249,367186,372Net Cash Generated from/(Used in)Investing Activities441,130(1,886,031)。

IFRS12 International Financial Reporting Standard12Disclosure of Interests in Other EntitiesIn May2011the International Accounting Standards Board(IASB)issued IFRS12Disclosure of Interests in Other Entities.IFRS12replaced the disclosure requirements in IAS27Consolidated and Separate Financial Statements,IAS28Investments in Associates and IAS31Interests in Joint Ventures.In June2012,IFRS12was amended by Consolidated Financial Statements,Joint Arrangements and Disclosure of Interests in Other Entities:Transition Guidance(Amendments to IFRS10,IFRS11and IFRS12).These amendments provided additional transition relief in IFRS12,limiting the requirement to present adjusted comparative information to only the annual period immediately preceding the first annual period for which IFRS12is applied.Furthermore, for disclosures related to unconsolidated structured entities,the amendments removed the requirement to present comparative information for periods before IFRS12is first applied.Other IFRSs have made minor consequential amendments to IFRS12,including Investment Entities(Amendments to IFRS10,IFRS12and IAS27)(issued October2012).IFRS Foundation A505IFRS12C ONTENTSfrom paragraph INTRODUCTION IN1 INTERNATIONAL FINANCIAL REPORTING STANDARD12 DISCLOSURE OF INTERESTS IN OTHER ENTITIESOBJECTIVE1 Meeting the objective2 SCOPE5 SIGNIFICANT JUDGEMENTS AND ASSUMPTIONS7 Investment entity status9A INTERESTS IN SUBSIDIARIES10 The interest that non-controlling interests have in the group’s activities andcash flows12 The nature and extent of significant restrictions13 Nature of the risks associated with an entity’s interests in consolidatedstructured entities14 Consequences of changes in a parent’s ownership interest in a subsidiarythat do not result in a loss of control18 Consequences of losing control of a subsidiary during the reporting period19 INTERESTS IN UNCONSOLIDATED SUBSIDIARIES(INVESTMENT ENTITIES)19A INTERESTS IN JOINT ARRANGEMENTS AND ASSOCIATES20 Nature,extent and financial effects of an entity’s interests in jointarrangements and associates21 Risks associated with an entity’s interests in joint ventures and associates23 INTERESTS IN UNCONSOLIDATED STRUCTURED ENTITIES24 Nature of interests26 Nature of risks29 APPENDICESA Defined termsB Application guidanceC Effective date and transitionD Amendments to other IFRSsFOR THE ACCOMPANYING DOCUMENTS LISTED BELOW,SEE PART B OF THIS EDITIONAPPROVAL BY THE BOARD OF IFRS12ISSUED IN MAY2011APPROVAL BY THE BOARD OF CONSOLIDATED FINANCIAL STATEMENTS,JOINT ARRANGEMENTS AND DISCLOSURE OF INTERESTS IN OTHERENTITIES:TRANSITION GUIDANCE(AMENDMENTS TO IFRS10,IFRS11ANDIFRS12)ISSUED IN JUNE2012APPROVAL BY THE BOARD OF INVESTMENT ENTITIES(AMENDMENTS TOIFRS10,IFRS12AND IAS27)ISSUED IN OCTOBER2012A506IFRS FoundationIFRS12 BASIS FOR CONCLUSIONSIFRS Foundation A507IFRS12International Financial Reporting Standard12Disclosure of Interests in Other Entities (IFRS12)is set out in paragraphs1–31and Appendices A–D.All the paragraphs have equal authority.Paragraphs in bold type state the main principles.Terms defined in Appendix A are in italics the first time they appear in the IFRS.Definitions of other terms are given in the Glossary for International Financial Reporting Standards.IFRS12 should be read in the context of its objective and the Basis for Conclusions,the Preface to International Financial Reporting Standards and the Conceptual Framework for Financial Reporting.IAS8Accounting Policies,Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies in the absence of explicit guidance.A508IFRS FoundationIFRS12 IntroductionIN1IFRS12Disclosure of Interests in Other Entities applies to entities that have an interest in a subsidiary,a joint arrangement,an associate or an unconsolidatedstructured entity.IN2The IFRS is effective for annual periods beginning on or after1January2013.Earlier application is permitted.Reasons for issuing the IFRSIN3Users of financial statements have consistently requested improvements to the disclosure of a reporting entity’s interests in other entities to help identify theprofit or loss and cash flows available to the reporting entity and determine thevalue of a current or future investment in the reporting entity.IN4They highlighted the need for better information about the subsidiaries that are consolidated,as well as an entity’s interests in joint arrangements and associatesthat are not consolidated but with which the entity has a special relationship.IN5The global financial crisis that started in2007also highlighted a lack of transparency about the risks to which a reporting entity was exposed from itsinvolvement with structured entities,including those that it had sponsored.IN6In response to input received from users and others,including the G20leaders and the Financial Stability Board,the Board decided to address in IFRS12theneed for improved disclosure of a reporting entity’s interests in other entitieswhen the reporting entity has a special relationship with those other entities.IN7The Board identified an opportunity to integrate and make consistent the disclosure requirements for subsidiaries,joint arrangements,associates andunconsolidated structured entities and present those requirements in a singleIFRS.The Board observed that the disclosure requirements of IAS27Consolidatedand Separate Financial Statements,IAS28Investments in Associates and IAS31Interestsin Joint Ventures overlapped in many areas.In addition,many commented thatthe disclosure requirements for interests in unconsolidated structured entitiesshould not be located in a consolidation standard.Therefore,the Boardconcluded that a combined disclosure standard for interests in other entitieswould make it easier to understand and apply the disclosure requirements forsubsidiaries,joint ventures,associates and unconsolidated structured entities. Main features of the IFRSIN8The IFRS requires an entity to disclose information that enables users of financial statements to evaluate:(a)the nature of,and risks associated with,its interests in other entities;and(b)the effects of those interests on its financial position,financialperformance and cash flows.IFRS Foundation A509IFRS12General requirementsIN9The IFRS establishes disclosure objectives according to which an entity discloses information that enables users of its financial statements(a)to understand:(i)the significant judgements and assumptions(and changes tothose judgements and assumptions)made in determining thenature of its interest in another entity or arrangement(iecontrol,joint control or significant influence),and indetermining the type of joint arrangement in which it has aninterest;and(ii)the interest that non-controlling interests have in the group’sactivities and cash flows;and(b)to evaluate:(i)the nature and extent of significant restrictions on its ability toaccess or use assets,and settle liabilities,of the group;(ii)the nature of,and changes in,the risks associated with itsinterests in consolidated structured entities;(iii)the nature and extent of its interests in unconsolidatedstructured entities,and the nature of,and changes in,the risksassociated with those interests;(iv)the nature,extent and financial effects of its interests in jointarrangements and associates,and the nature of the risksassociated with those interests;(v)the consequences of changes in a parent’s ownership interest in asubsidiary that do not result in a loss of control;and(vi)the consequences of losing control of a subsidiary during thereporting period.IN10The IFRS specifies minimum disclosures that an entity must provide.If the minimum disclosures required by the IFRS are not sufficient to meet thedisclosure objective,an entity discloses whatever additional information isnecessary to meet that objective.IN11The IFRS requires an entity to consider the level of detail necessary to satisfy the disclosure objective and how much emphasis to place on each of therequirements in the IFRS.An entity shall aggregate or disaggregate disclosuresso that useful information is not obscured by either the inclusion of a largeamount of insignificant detail or the aggregation of items that have differentcharacteristics.IN12Investment Entities(Amendments to IFRS10,IFRS12and IAS27),issued in October 2012,introduced an exception to the principle in IFRS10Consolidated FinancialStatements that all subsidiaries shall be consolidated.The amendments define aninvestment entity and require a parent that is an investment entity to measureits investment in particular subsidiaries at fair value through profit or loss inaccordance with IFRS9Financial Instruments(or IAS39Financial Instruments: A510IFRS FoundationIFRS12Recognition and Measurement,if IFRS9has not yet been adopted)instead of consolidating those subsidiaries in its consolidated and separate financial statements.Consequently,the amendments also introduced new disclosure requirements for investment entities in this IFRS and IAS27Separate Financial Statements.IFRS Foundation A511IFRS12International Financial Reporting Standard12Disclosure of Interests in Other EntitiesObjective1The objective of this IFRS is to require an entity to disclose information that enables users of its financial statements to evaluate:(a)the nature of,and risks associated with,its interests in otherentities;and(b)the effects of those interests on its financial position,financialperformance and cash flows.Meeting the objective2To meet the objective in paragraph1,an entity shall disclose:(a)the significant judgements and assumptions it has made in determining:(i)the nature of its interest in another entity or arrangement;(ii)the type of joint arrangement in which it has an interest(paragraphs7–9);(iii)that it meets the definition of an investment entity,if applicable(paragraph9A);and(b)information about its interests in:(i)subsidiaries(paragraphs10–19);(ii)joint arrangements and associates(paragraphs20–23);and(iii)structured entities that are not controlled by the entity(unconsolidated structured entities)(paragraphs24–31).3If the disclosures required by this IFRS,together with disclosures required by other IFRSs,do not meet the objective in paragraph1,an entity shall disclosewhatever additional information is necessary to meet that objective.4An entity shall consider the level of detail necessary to satisfy the disclosure objective and how much emphasis to place on each of the requirements in thisIFRS.It shall aggregate or disaggregate disclosures so that useful information isnot obscured by either the inclusion of a large amount of insignificant detail orthe aggregation of items that have different characteristics(see paragraphsB2–B6).Scope5This IFRS shall be applied by an entity that has an interest in any of the following:(a)subsidiaries(b)joint arrangements(ie joint operations or joint ventures)A512IFRS FoundationIFRS12(c)associates(d)unconsolidated structured entities.6This IFRS does not apply to:(a)post-employment benefit plans or other long-term employee benefitplans to which IAS19Employee Benefits applies.(b)an entity’s separate financial statements to which IAS27SeparateFinancial Statements applies.However,if an entity has interests inunconsolidated structured entities and prepares separate financialstatements as its only financial statements,it shall apply therequirements in paragraphs24–31when preparing those separatefinancial statements.(c)an interest held by an entity that participates in,but does not have jointcontrol of,a joint arrangement unless that interest results in significantinfluence over the arrangement or is an interest in a structured entity.(d)an interest in another entity that is accounted for in accordance withIFRS9Financial Instruments.However,an entity shall apply this IFRS:(i)when that interest is an interest in an associate or a joint venturethat,in accordance with IAS28Investments in Associates and JointVentures,is measured at fair value through profit or loss;or(ii)when that interest is an interest in an unconsolidated structuredentity.Significant judgements and assumptions7An entity shall disclose information about significant judgements and assumptions it has made(and changes to those judgements andassumptions)in determining:(a)that it has control of another entity,ie an investee as described inparagraphs5and6of IFRS10Consolidated Financial Statements;(b)that it has joint control of an arrangement or significant influenceover another entity;and(c)the type of joint arrangement(ie joint operation or joint venture)when the arrangement has been structured through a separate vehicle.8The significant judgements and assumptions disclosed in accordance with paragraph7include those made by the entity when changes in facts andcircumstances are such that the conclusion about whether it has control,jointcontrol or significant influence changes during the reporting period.9To comply with paragraph7,an entity shall disclose,for example,significant judgements and assumptions made in determining that:(a)it does not control another entity even though it holds more than half ofthe voting rights of the other entity.(b)it controls another entity even though it holds less than half of thevoting rights of the other entity.IFRS Foundation A513IFRS12(c)it is an agent or a principal(see paragraphs B58–B72of IFRS10).(d)it does not have significant influence even though it holds20per cent ormore of the voting rights of another entity.(e)it has significant influence even though it holds less than20per cent ofthe voting rights of another entity.Investment entity status9A When a parent determines that it is an investment entity in accordance with paragraph27of IFRS10,the investment entity shall discloseinformation about significant judgements and assumptions it has made indetermining that it is an investment entity.If the investment entity does nothave one or more of the typical characteristics of an investment entity(seeparagraph28of IFRS10),it shall disclose its reasons for concluding that it isnevertheless an investment entity.9B When an entity becomes,or ceases to be,an investment entity,it shall disclose the change of investment entity status and the reasons for the change.Inaddition,an entity that becomes an investment entity shall disclose the effect ofthe change of status on the financial statements for the period presented,including:(a)the total fair value,as of the date of change of status,of the subsidiariesthat cease to be consolidated;(b)the total gain or loss,if any,calculated in accordance withparagraph B101of IFRS10;and(c)the line item(s)in profit or loss in which the gain or loss is recognised(ifnot presented separately).Interests in subsidiaries10An entity shall disclose information that enables users of its consolidated financial statements(a)to understand:(i)the composition of the group;and(ii)the interest that non-controlling interests have in thegroup’s activities and cash flows(paragraph12);and(b)to evaluate:(i)the nature and extent of significant restrictions on itsability to access or use assets,and settle liabilities,of thegroup(paragraph13);(ii)the nature of,and changes in,the risks associated with itsinterests in consolidated structured entities(paragraphs14–17);(iii)the consequences of changes in its ownership interest in asubsidiary that do not result in a loss of control(paragraph18);andA514IFRS FoundationIFRS12(iv)the consequences of losing control of a subsidiary duringthe reporting period(paragraph19).11When the financial statements of a subsidiary used in the preparation of consolidated financial statements are as of a date or for a period that is differentfrom that of the consolidated financial statements(see paragraphs B92and B93of IFRS10),an entity shall disclose:(a)the date of the end of the reporting period of the financial statements ofthat subsidiary;and(b)the reason for using a different date or period.The interest that non-controlling interests have in thegroup’s activities and cash flows12An entity shall disclose for each of its subsidiaries that have non-controlling interests that are material to the reporting entity:(a)the name of the subsidiary.(b)the principal place of business(and country of incorporation if differentfrom the principal place of business)of the subsidiary.(c)the proportion of ownership interests held by non-controlling interests.(d)the proportion of voting rights held by non-controlling interests,ifdifferent from the proportion of ownership interests held.(e)the profit or loss allocated to non-controlling interests of the subsidiaryduring the reporting period.(f)accumulated non-controlling interests of the subsidiary at the end of thereporting period.(g)summarised financial information about the subsidiary(seeparagraph B10).The nature and extent of significant restrictions13An entity shall disclose:(a)significant restrictions(eg statutory,contractual and regulatoryrestrictions)on its ability to access or use the assets and settle theliabilities of the group,such as:(i)those that restrict the ability of a parent or its subsidiaries totransfer cash or other assets to(or from)other entities within thegroup.(ii)guarantees or other requirements that may restrict dividendsand other capital distributions being paid,or loans and advancesbeing made or repaid,to(or from)other entities within thegroup.(b)the nature and extent to which protective rights of non-controllinginterests can significantly restrict the entity’s ability to access or use theassets and settle the liabilities of the group(such as when a parent isobliged to settle liabilities of a subsidiary before settling its ownIFRS Foundation A515IFRS12liabilities,or approval of non-controlling interests is required either toaccess the assets or to settle the liabilities of a subsidiary).(c)the carrying amounts in the consolidated financial statements of theassets and liabilities to which those restrictions apply.Nature of the risks associated with an entity’s interestsin consolidated structured entities14An entity shall disclose the terms of any contractual arrangements that could require the parent or its subsidiaries to provide financial support to aconsolidated structured entity,including events or circumstances that couldexpose the reporting entity to a loss(eg liquidity arrangements or credit ratingtriggers associated with obligations to purchase assets of the structured entity orprovide financial support).15If during the reporting period a parent or any of its subsidiaries has,without having a contractual obligation to do so,provided financial or other support to aconsolidated structured entity(eg purchasing assets of or instruments issued bythe structured entity),the entity shall disclose:(a)the type and amount of support provided,including situations in whichthe parent or its subsidiaries assisted the structured entity in obtainingfinancial support;and(b)the reasons for providing the support.16If during the reporting period a parent or any of its subsidiaries has,without having a contractual obligation to do so,provided financial or other support to apreviously unconsolidated structured entity and that provision of supportresulted in the entity controlling the structured entity,the entity shall disclosean explanation of the relevant factors in reaching that decision.17An entity shall disclose any current intentions to provide financial or other support to a consolidated structured entity,including intentions to assist thestructured entity in obtaining financial support.Consequences of changes in a parent’s ownershipinterest in a subsidiary that do not result in a loss ofcontrol18An entity shall present a schedule that shows the effects on the equity attributable to owners of the parent of any changes in its ownership interest in asubsidiary that do not result in a loss of control.Consequences of losing control of a subsidiary duringthe reporting period19An entity shall disclose the gain or loss,if any,calculated in accordance with paragraph25of IFRS10,and:(a)the portion of that gain or loss attributable to measuring any investmentretained in the former subsidiary at its fair value at the date whencontrol is lost;andA516IFRS FoundationIFRS12(b)the line item(s)in profit or loss in which the gain or loss is recognised(ifnot presented separately).Interests in unconsolidated subsidiaries(investment entities)19A An investment entity that,in accordance with IFRS10,is required to apply the exception to consolidation and instead account for its investment in a subsidiaryat fair value through profit or loss shall disclose that fact.19B For each unconsolidated subsidiary,an investment entity shall disclose:(a)the subsidiary’s name;(b)the principal place of business(and country of incorporation if differentfrom the principal place of business)of the subsidiary;and(c)the proportion of ownership interest held by the investment entity and,if different,the proportion of voting rights held.19C If an investment entity is the parent of another investment entity,the parent shall also provide the disclosures in19B(a)–(c)for investments that arecontrolled by its investment entity subsidiary.The disclosure may be providedby including,in the financial statements of the parent,the financial statementsof the subsidiary(or subsidiaries)that contain the above information.19D An investment entity shall disclose:(a)the nature and extent of any significant restrictions(eg resulting fromborrowing arrangements,regulatory requirements or contractualarrangements)on the ability of an unconsolidated subsidiary to transferfunds to the investment entity in the form of cash dividends or to repayloans or advances made to the unconsolidated subsidiary by theinvestment entity;and(b)any current commitments or intentions to provide financial or othersupport to an unconsolidated subsidiary,including commitments orintentions to assist the subsidiary in obtaining financial support.19E If,during the reporting period,an investment entity or any of its subsidiaries has,without having a contractual obligation to do so,provided financial orother support to an unconsolidated subsidiary(eg purchasing assets of,orinstruments issued by,the subsidiary or assisting the subsidiary in obtainingfinancial support),the entity shall disclose:(a)the type and amount of support provided to each unconsolidatedsubsidiary;and(b)the reasons for providing the support.19F An investment entity shall disclose the terms of any contractual arrangements that could require the entity or its unconsolidated subsidiaries to providefinancial support to an unconsolidated,controlled,structured entity,includingevents or circumstances that could expose the reporting entity to a loss(egliquidity arrangements or credit rating triggers associated with obligations topurchase assets of the structured entity or to provide financial support).IFRS Foundation A517IFRS1219G If during the reporting period an investment entity or any of its unconsolidated subsidiaries has,without having a contractual obligation to do so,providedfinancial or other support to an unconsolidated,structured entity that theinvestment entity did not control,and if that provision of support resulted inthe investment entity controlling the structured entity,the investment entityshall disclose an explanation of the relevant factors in reaching the decision toprovide that support.Interests in joint arrangements and associates20An entity shall disclose information that enables users of its financial statements to evaluate:(a)the nature,extent and financial effects of its interests in jointarrangements and associates,including the nature and effects of itscontractual relationship with the other investors with joint control of,or significant influence over,joint arrangements and associates(paragraphs21and22);and(b)the nature of,and changes in,the risks associated with its interestsin joint ventures and associates(paragraph23).Nature,extent and financial effects of an entity’sinterests in joint arrangements and associates21An entity shall disclose:(a)for each joint arrangement and associate that is material to thereporting entity:(i)the name of the joint arrangement or associate.(ii)the nature of the entity’s relationship with the joint arrangementor associate(by,for example,describing the nature of theactivities of the joint arrangement or associate and whether theyare strategic to the entity’s activities).(iii)the principal place of business(and country of incorporation,ifapplicable and different from the principal place of business)ofthe joint arrangement or associate.(iv)the proportion of ownership interest or participating share heldby the entity and,if different,the proportion of voting rightsheld(if applicable).(b)for each joint venture and associate that is material to the reportingentity:(i)whether the investment in the joint venture or associate ismeasured using the equity method or at fair value.(ii)summarised financial information about the joint venture orassociate as specified in paragraphs B12and B13.A518IFRS FoundationIFRS12(iii)if the joint venture or associate is accounted for using the equitymethod,the fair value of its investment in the joint venture orassociate,if there is a quoted market price for the investment.(c)financial information as specified in paragraph B16about the entity’sinvestments in joint ventures and associates that are not individuallymaterial:(i)in aggregate for all individually immaterial joint ventures and,separately,(ii)in aggregate for all individually immaterial associates.21A An investment entity need not provide the disclosures required by paragraphs21(b)–21(c).22An entity shall also disclose:(a)the nature and extent of any significant restrictions(eg resulting fromborrowing arrangements,regulatory requirements or contractualarrangements between investors with joint control of or significantinfluence over a joint venture or an associate)on the ability of jointventures or associates to transfer funds to the entity in the form of cashdividends,or to repay loans or advances made by the entity.(b)when the financial statements of a joint venture or associate used inapplying the equity method are as of a date or for a period that isdifferent from that of the entity:(i)the date of the end of the reporting period of the financialstatements of that joint venture or associate;and(ii)the reason for using a different date or period.(c)the unrecognised share of losses of a joint venture or associate,both forthe reporting period and cumulatively,if the entity has stoppedrecognising its share of losses of the joint venture or associate whenapplying the equity method.Risks associated with an entity’s interests in jointventures and associates23An entity shall disclose:(a)commitments that it has relating to its joint ventures separately fromthe amount of other commitments as specified in paragraphs B18–B20.(b)in accordance with IAS37Provisions,Contingent Liabilities and ContingentAssets,unless the probability of loss is remote,contingent liabilitiesincurred relating to its interests in joint ventures or associates(includingits share of contingent liabilities incurred jointly with other investorswith joint control of,or significant influence over,the joint ventures orassociates),separately from the amount of other contingent liabilities.IFRS Foundation A519。