会计专业英语011 (1)

- 格式:pdf

- 大小:1.38 MB

- 文档页数:40

会计专业英语-CAL-FENGHAI.-(YICAI)-Company One1一、words and phrases1.残值 scrip value2.分期付款 installment3.concern 企业4.reversing entry 转回分录5.找零 change6.报销 turn over7.past due 过期8.inflation 通货膨胀9.on account 赊账10.miscellaneous expense 其他费用11.charge 收费12.汇票 draft13.权益 equity14.accrual basis 应计制15.retained earnings 留存收益16.trad-in 易新,以旧换新17.in transit 在途18.collection 托收款项19.资产 asset20.proceeds 现值21.报销 turn over22.dishonor 拒付23.utility expenses 水电费24.outlay 花费25.IOU 欠条26.Going-concern concept 持续经营27.运费 freight二、Multiple-choice question1.Which of the following does not describe accounting( C )A. Language of businessB. Useful ofr decision makingC. Is an end rathe than a means to an end.ed by business, government, nonprofit organizations, and individuals.2.An objective of financial reporting is to ( B )A. Assess the adequacy of internal control.B.Provide information useful for investor decisions.C.Evaluate management results compared with standards.D.Provide information on compliance with established procedures.3.Which of the following statements is(are) correct( B )A.Accumulated depreciation represents a cash fund being accumulated for the replacement of plant assets.B.A company may use different depreciation methods in its financial statements and its income tax return.C.The cost of a machine includes the cost of repairing damage to the machine during the installation process.D.The use of an accelerated depreciation method causes an asset to wear out more quickly than does use of the unit-of-product method.4. Which of the following is(are) correct about a company’s balance sheet( B )A.It displays sources and uses of cash for the period.B.It is an expansion of the basic accounting equationC.It is not sometimes referred to as a statement of financial position.D.It is unnecessary if both an income statement and statement of cash flows are availabe.5.Objectives of financial reporting to external investors and creditors include preparing information about all of the following except. ( A )rmation used to determine which products to poducermation about economic resources, claims to those resources, and changes in both resources and claims.rmation that is useful in assessing the amount, timing, and uncertainty of future cash flows.rmation that is useful in making ivestment and credit decisions.6.Each of the following measures strengthens internal control over cash receipts except. ( C )A.The use of a petty cash fund.B.Preparation of a daily listing of all checks received through the mail.C.The use of cash registers.D.The deposit of cash receipts in the bank on a daily basis.7.The primary purpose for using an inventory flow assumption is to. ( A )A.Offset against revenue an appropriate cost of goods sold.B.Parallel the physical flow of units of merchandise.C.Minimize income taxes.D.Maximize the reported amount of net income.8.In general terms, financial assets appear in the balance sheet at. ( B )A.Current valueB.Face valueC.CostD.Estimated future sales value.9.If the going-concem assumption is no longer valid for a company except. ( C )nd held as an ivestment would be valued at its liquidation value.B.All prepaid assets would be completely written off immediately.C.Total contributed capital and retained earnings would remain unchanged.D.The allowance for uncollectible accounts would be eliminated.10.Which of the following explains the debit and credit rules relating to the recording of revenue and expenses( C )A.Expenses appear on the left side of the balance sheet and are recorded by debits;revenue appears on the right side of the balance sheet and is reoorded by credits.B. Expenses appear on the left side of the income statement and are recorded by debits; Revenue appears on the right side of the income statement and is recorded by credits.C.The effects of revenue and expenses on owners’ equity.D.The realization principle and the matching principle.11.Which of the following statements is(are) correct( B )A.Accumulated depreciation represents a cash fund being accumulated for the replacement of plant assets.B.The cost of a machine do not includes the cost of repairing damage to the machine during the installation prcess.C.A company may use same depreciation methods in its finacial statements and its income tax return.D.The use of an accelerated depreciation method causes an asset to wear out more quickly than does use of the straight-line method.12.A set of financial statements ( B ) except.A.Is intended to assist users in evaluating the financial position, profitability, and future prospects of an entity.B.Is intended to assist the Intemal Revenue Service in detemining the amount of income taxes owed by a business organization.C.Includes notes disclosing information necessary for the proper interpretation of the statements.D.Is intended to assist investors and creditors in making decisions inventory the allocation of economic resources.13.The primary purpose for using an inventory flow assumption is to. ( B )A.Parallel the physical flow of units of merchandise.B.Offset against revenue an appropriate cost of goods soldC.Minimize income taxes.D.Maximize the reported amount of net income.14.Indicate all correct answers. In the accounting cycle. ( D )A.Transactions are posted before they are journalized.B.A trial balance is prepared after journal entries haven’t been posted.C.The Retained Earnings account is not shown as an up-to-date figure in the trial balance.D.Joumal entries are posted to appropriate ledger accounts.15.According to text, Objectives of Financial Reporting by Business Enterprises. ( D )A.Extemal users have the ability to prescribe information they want.rmation is always based on exact measures.C.Financial reporting is usually based on industries or the economy as a whole.D.Financial accounting does not directly measure the value of a business enterprise.16.Indicate all correct answers. Dividends except ( A )A.Decrease owners’ equity.B.Decrease net incomeC.Are recorded by debiting the Cash accountD.Are a business expense17.Which of the following practices contributes to efficient cash management ( C )A.Never borrow money-maintain a cash balance sufficient to make all necessary payments.B.Record all cash receipts and cash payments at the end of the month when reconciling the bank statements.C.Prepare monthly forecasts of planned cash receipts, payments, and anticipated cash balances up to a year in advance.D.Pay each bill as soon as the invoice arrives.18.Which of the following would you expect to find in a correctly prepared income statement ( A )A.Revenues earned during the period.B.Cash balance at the end of the period.C.Contributions by the owner during the period.D.Expenses incurred during the next period to earn revenues.19.Which of the following are important factors in ensuring the integrity of accounting information ( D )A.Institutional factors, such as standards for preparing information.B.Professional organizations, such as the American Institute of CPAs.petence’ judgment’ and ethical behavior of individual accountants’D.All of the above.三、Practices11.On Jan.1, 2000, Mark Co, acquired equipment to use in its operations. The equipment has an estimated useful life of 10 years and an estimated salvage value of $5,000. The depreciation applicable to this equipment was $40,000 for 2000, calculated under the sum-of –the-years’–digits method. Required: Determine the acquisition cost of the equipment. ( C )A.$210,000B.$250,000C.$225.000D.$200,0002. On Jan.2, 2002, Mark Co, acquired equipment to use in its operations. The equipment has an estimated useful life of 10 years and an estimated salvage value of $5,000. The depreciation applicable to this equipment was $24,000 for 2004, calculated under the sum-of –the-years’–digits method (4%). Required: Determine the acquisition cost of the equipment. ( C )A.$220,000B.$250,000C.$224.000D.$200,0003. October 1, 2005, Coast Financial Ioaned Bart Corporation $3000,000, receiving in exchange a nine-month, 12 percent note receivable. Coast ends its fiscal year on December 31 and makes adjusting entries to accrue interest earned on all notes receivable. The interest earned on the note receivable from Bart Corporation during 2006 will amount to. ( A )A.$9,000B.$18,000C.$27.000D.$36,000Question: What is the reconciled balance ( B )A.$4,187B.$4,085C.$4,090D.$4,000Required: Choose the reconciled balance. ( D )A.$3,220B.$3,250C.$3,200D.$3,225Required:Calculate the cost of goods available for sale(C)A.$475,000B.$474,000C.$470,000D.$473,000Required: Calculate the cost of goods sold ( D )A.$225,000B.$254,000C.$250,000D.$253,0008.At the end of the current year, the accounts receivable account has a debit balance of $60,000 and net sales for the year total $100,000. The allowance account before adjunstment has adebit balance of a $500, and uncollectible accounts expense is estimated at 1% of net sales. Question: The entry for the above bad debts is ( A )A.Dr. Bad Debt Accts. $1,500B.Dr. Bad Debt Accts. $500Cr. Allowance Doubtful Accts. $1,500 Cr. Allowance Doubtful Accts. $500C. Dr. Bad Debt Accts. $1,000D. Dr. Bad Debt Accts. $1,500Cr. Accts Rec. $1,000 Cr. Accts Rec. $1,5009.The balance sheet items to The Oven Bakery(arranged in alphabetical order)were as follows at August 1,2005.(You are to compute the missing figure for retained earnings.)(4%)REQUIRED:Find Retained earnings at August 1 2005(D)A.$420,000B.$44,000C.$40,000D.$48,000Practices2Sue began a public accounting practice and completed these transactions during first month of the current year.Required: Choose the entries to record the following transactons.1.Invested $50,000 cash in a public accounting practice begun this day. ( A )A.Dr. Cash $50,000B.Dr. Capital Stock $50,000Cr. Capital Stock $50,000 Cr. Cash $50,0002.Paid cash for three monts’ office rent in advance $900(B)A.Dr. Rent Exp. $900B.Dr. Prepaid Rent $900Cr. Cash $900 Cr. Cash $9003.Paid the premium on two insurance policies, $300. ( )A.Dr. Prepaid Insurance $300B.Dr. Insurance Exp $300Cr. Cash $300 Cr. Cash $300pleted accounting work for Sun Bank on credit $1000. ( A )A.Dr. Accts Rec $1000B.Dr. Cash $1000Cr.Accounting Revenue $1000 Cr.Accounting Revenue $10005.Paid the monthly utility bills of the accounting office $300 ( A )A.Dr Utility Exp $300B.Dr office Exp $300Cr. Cash $300 Cr. Cash $300Linda began a public accounting practice and completed these transactons during first month of the current year.Required: Choose the entries to record the following transactons.6.Invested $20,000 cash in a public accounting practice begun this day. ( A )A.Dr Cash $20,00B.Dr Capital Stock $20,000Cr. Capital Stock $20,000 Cr. Cash $20,007.Paid cash for three months’ office rent in advance $1200.( B )A.Dr. Rent Exp $1200B.Dr. Prepaid Rent $1200Cr. Cash $1200 Cr. Cash $12008.Purchased offfice supplies $100 and office equipment $2,000 on credit. ( B )A.Dr. Office Equipment $2,000B.Dr.Office Equipment $2,000Office Supplies $100 Office Supplies $100Cr. Accts Rec. $2,100 Cr.Accts Pay. $2,100pleted accounting work for Jack Hall and collected $2000 cash therefore. ( B )A.Dr. Accts Rec $2000B.Dr. Cash $2000Cr.Accounting Revenue $2000 Cr.Accounting Revenue $200010.Purchase additional office equipment on credit $2500.( A )A.Dr.Office equipment $2500B.Dr. Office equipment $2500Cr.Accts Pay $2500 Cr.Accts Rec $2500四、Translation:1)The mechanics of double-entry accounting are such that every transaction is recorded in the debit side of one or more accounts and in the credit side of one or more accounts with equal debits and credits. Such form of combination is called accounting entry. Where there are only two accounts affected. 2)the debit and credit amounts are equal. If more than two accounts are affceted, the total of the debit entries must equal the total of the credit entries. The double-entry accounting is used by virtually every business organization, regardless of whether the company’s accounting records are maintained manually or by computer.1.The mechanics of double-entry accounting.( B )A.会计两次记账的制度B.复式记账机制C.会计的重复记账体制2.the debit and credit amounts are equal. ( A )A.借方金额与贷方金额是相等的B.借出金额与贷款金额是相等的C.借入金额与贷款金额是相等的Most accounting methods are based on the assumption that the business enterprise will have a long life. Experience indicates that.1)inspite of numerous business failures, companies have a fairly highcontinuance rate. Accountants do not believe that business firms will last indefinitely, but they do expect them to last long enouthto 2)fulfill their objectives and commitments.3.in spite of numerous business failures, companies have a fairly high continuance rate. ( B )A.可惜有许多企业失败,但公司仍有较高的持续经营比率。

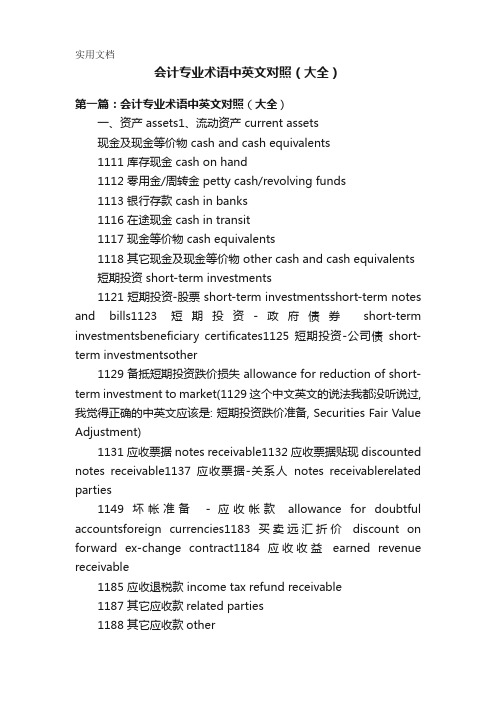

会计专业术语中英文对照(大全)第一篇:会计专业术语中英文对照(大全)一、资产 assets1、流动资产 current assets现金及现金等价物 cash and cash equivalents1111 库存现金 cash on hand1112 零用金/周转金 petty cash/revolving funds1113 银行存款 cash in banks1116 在途现金 cash in transit1117 现金等价物 cash equivalents1118 其它现金及现金等价物 other cash and cash equivalents 短期投资 short-term investments1121 短期投资-股票 short-term investmentsshort-term notes and bills1123 短期投资-政府债券short-term investmentsbeneficiary certificates1125 短期投资-公司债short-term investmentsother1129 备抵短期投资跌价损失 allowance for reduction of short-term investment to market(1129这个中文英文的说法我都没听说过,我觉得正确的中英文应该是: 短期投资跌价准备, Securities Fair Value Adjustment)1131 应收票据 notes receivable1132 应收票据贴现 discounted notes receivable1137 应收票据-关系人notes receivablerelated parties1149 坏帐准备-应收帐款allowance for doubtful accountsforeign currencies1183 买卖远汇折价discount on forward ex-change contract1184 应收收益earned revenue receivable1185 应收退税款 income tax refund receivable1187 其它应收款related parties1188 其它应收款other1189 坏帐准备other receivables121~122 存货 inventories1211 商品存货 merchandise inventory1212 寄销商品 consigned goods1213 在途商品 goods in transit1219 存货跌价准备 allowance to reduce inventory to market 1221 制成品 finished goods1222 寄销制成品 consigned finished goods1223 副产品 by-products1224 在制品 work in process1225 委外加工 work in processother2、基金及长期投资 funds and long-term investments基金 funds1311 偿债基金 redemption fund(or sinking fund)1312 改良及扩充基金 fund for improvement and expansion1313 意外损失准备基金 contingency fund1314 退休基金 pension fund1318 其它基金 other funds长期投资 long-term investments1321 长期股权投资 long-term equity investments1322 长期债券投资 long-term bond investments1323 长期不动产投资 long-term real estate investments1324 人寿保险现金解约价值cash surrender value of life insurance1328 其它长期投资 other long-term investments 1329 备抵长期投资跌价损失 allowance for excess of cost over market value of long-term investments3、固定资产property , plant, and equipment土地 land1411 土地 land1418 土地-重估增值 landrevaluation increments1429 累积折旧-土地改良物 accumulated depreciationbuildings144~146 机(器)具及设备 machinery and equipment1441 机(器)具 machinery1448 机(器)具-重估增值 machinerymachinery151 租赁资产 leased assets1511 租赁资产 leased assets1519 累积折旧-租赁资产accumulated depreciationleasehold improvements156 未完工程及预付购置设备款construction in progress and prepayments forequipment1561 未完工程 construction in progress1562 预付购置设备款 prepayment for equipment158 杂项固定资产miscellaneous property, plant, and equipment1581 杂项固定资产miscellaneous property, plant, and equipment1588 杂项固定资产-重估增值miscellaneous property, plant, and equipmentmiscellaneous property, plant, and equipment递耗资产 depletable assets161 递耗资产 depletable assets1611 天然资源 natural resources1618 天然资源-重估增值natural resources-revaluation increments1619 累积折耗-天然资源accumulated depletionother 其它资产 other assets181 递延资产 deferred assets1811 债券发行成本 deferred bond issuance costs1812 长期预付租金 long-term prepaid rent1813 长期预付保险费 long-term prepaid insurance1814 递延所得税资产 deferred income tax assets1815 预付退休金 prepaid pension cost1818 其它递延资产 other deferred assets182 闲置资产 idle assets1821 闲置资产 idle assets184 长期应收票据及款项与催收帐款long-term notes , accounts and overdue receivables1841 长期应收票据 long-term notes receivable1842 长期应收帐款 long-term accounts receivable1843 催收帐款 overdue receivables1847 长期应收票据及款项与催收帐款-关系人 long-term notes, accounts and overdue receivables-related parties1848 其它长期应收款项 other long-term receivables1849 备抵呆帐-长期应收票据及款项与催收帐款allowance for uncollectible accountsincremental value from revaluation 1859 累积折旧-出租资产 accumulated depreciationrestricted 1888 杂项资产-其它 miscellaneous assets-other第二篇:会计专业术语中英文对照流动资产: CURRENT ASSETS:货币资金 Cash结算备付金 Provision of settlement fund拆出资金 Funds lent交易性金融资产 Financial assets held for trading应收票据 Notes receivable应收账款 Accounts receivable预付款项 Advances to suppliers应收保费 Insurance premiums receivable应收分保账款 Cession premiums receivable应收分保合同准备金 Provision of cession receivable应收利息 Interests receivable其他应收款 Other receivable买入返售金融资产 Recoursable financial assets acquired存货Inventories其中:原材料 Raw material库存商品 Stock goods一年内到期的非流动资产 Non-current assets maturing within one year其他流动资产 Other current assets流动资产合计 TOTAL CURRENT ASSETS非流动资产:NON-CURRENT ASSETS发放贷款及垫款 Loans and payments on behalf可供出售金融资产 Available-for-sale financial assets持有至到期投资 Held-to-maturity investments长期应收款 Long-term receivables长期股权投资 Long-term equity investments投资性房地产 Investment real estates固定资产原价 Fixed assets original cost减:累计折旧 Less:Accumulated depreciation固定资产净值 Fixed assets--net value减:固定资产减值准备 Less:Fixed assets impairment provision 固定资产净额 Fixed assets--net book value在建工程 Construction in progress工程物资 Construction supplies固定资产清理 Fixed assets pending disposal生产性生物资产 Bearer biological assets油气资产 Oil and natural gas assets无形资产 Intangibel assets开发支出 Research and development costs商誉 Goodwill长期待摊费用 Long-term deferred expenses递延所得税资产 Deferred tax assets其他非流动资产 Other non-current assets其中:特准储备物资Physical assets reserve specificallyauthorized非流动资产合计 TOTAL NON-CURRENT ASSETS流动负债:CURRENT LIABILITIES:短期借款 Short-term borrowings向中央银行借款 Borrowings from central bank吸收存款及同业存放 Deposits from customers and interbank 拆入资金 Deposit funds交易性金融负债 Financial assets held for liabilities应付票据 Notes payable应付账款 Accounts payable预收款项 Advances from customers卖出回购金融资产款 Funds from sales of financial assets with repurchasement agreement应付手续费及佣金Handling charges and commissions payable应付职工薪酬 Employee benefits payable其中:应付工资 Including:Accrued payroll应付福利费 Welfare benefits payable其中:职工奖励及福利基金 Including:Staff and workers' bonus and selfare应交税费 Taxes and surcharges payable其中:应交税金 Including:Taxes payable应付利息 Interests payable其他应付款 Other payables应付分保账款 Cession insurance premiums payable保险合同准备金 Provision for insurance contracts代理买卖证券款 Funds received as agent of stock exchange代理承销证券款 Funds received as stock underwrite一年内到期的非流动负债Non-current liabilities maturing within one year其他流动负债 Other current liablities流动负债合计 TOTAL CURRENT LIABILITIES:非流动负债:NON-CURRENT LIABILITIES:长期借款Long-term loans应付债券 Debentures payable长期应付款 Long-term payables专项应付款 Specific payable预计负债 Accrued liabilities递延所得税负债 Deferred tax liabilities其他非流动负债 Other non-current liablities其中:特准储备基金 Authorized reserve fund非流动负债合计 TOTAL NON-CURRENT LIABILITIES:负债合计 TOTAL LIABILITIES所有者权益(或股东权益):OWNERS'(OWNER'S)/SHAREHOLDERS' EQUITY实收资本(股本)Registered capital国家资本 National capital集体资本 Collective capital法人资本 Legal person's capital其中:国有法人资本Including:State-owned legal person's capital集体法人资本Collective legal person“s capital个人资本Personal capital外商资本 Foreign businessmen's capital减:已归还投资 Less:Returned investment实收资本(或股本)净额 Registered capital--net book value资本公积 Capital surplus减:库存股 Treasury stock专项储备 Special reserve盈余公积 Surplus reserve其中:法定公积金Including:Statutory accumulation reserve任意公积金 Discretionary accumulation储备基金 Reserved funds企业发展基金 Enterprise expension funds利润归还投资 Profits capitalised on retum of investments一般风险准备 Provision for normal risks未分配利润 Undistributed profits外币报表折算差额 Exchange differences on translating foreign operations归属于母公司所有者权益合计 Total owners' equity belongs to parent company少数股东权益 Minority interest所有者权益合计 TOTAL OWNERS' EQUITY负债及所有者权益总计 TOTAL LIABILITIES & OWNERS' EQUITY一、营业总收入 OVERALL SALES其中:营业收入 Including:Sales from operations其中:主营业务收入 Including:sales of main operations其他业务收入 Income from other operations利息收入 Interest income已赚保费 Insurance premiums earned手续费及佣金收入 Handling charges and commissions income二、营业总成本 OVERALL COSTS其中:营业成本 Including: Cost of operations其中:主营业务成本 Including:Cost of main operations其他业务成本 cost of other operations利息支出 Interest expenses手续费及佣金支出Handling charges and commissions expenses退保金 Refund of insurance premiums赔付支出净额 Net payments for insurance claims提取保险合同准备金净额 Net provision for insurance contracts 保单红利支出 Commissions on insurance policies分保费用 Cession charges营业税金及附加 Sales tax and additions销售费用 Selling and distribution expenses管理费用 General and administrative expenses其中:业务招待费 business entertainment研究与开发费research and development财务费用Financial expenses其中:利息支出 Interest expense利息收入 Interest income汇兑净损失(净收益以“-”号填列)Gain or loss on foreign exchange transactions(less exchange gain)资产减值损失 Impairment loss on assets其他other加:公允价值变动收益(损失以“-”号填列)Plus: Gain or loss from changes in fair values(loss expressed with ”-“)投资收益(损失以“-”号填列)Investment income(loss expressed with ”-“)其中:对联营企业和合营企业的投资收益 Including: Investment income from joint ventures and affiliates(loss express ed with ”-“)汇兑收益(损失以“-”号填列)Gain or loss on foreign exchange transactions s(loss expressed with ”-“)三、营业利润(亏损以“-”号填列)PROFIT FROM OPERATIONS加:营业外收入 Plus: Non-operating profit 其中:非流动资产处置利得 Gains from disposal of non-current assets非货币性资产交换利得Gains from exchange of non-monetary assets政府补助 Government grant income债务重组利得 Gains from debt restructuring减:营业外支出 Less:Non-operating expenses其中:非流动资产处置损失Including:Losses from disposal ofnon-current assets非货币性资产交换损失Losses from exchange of non-monetary assets债务重组损失 Losses from debt restructuring四、利润总额(亏损总额以“-”号填列)PROFIT BEFORE TAX(LOSS EXPRESSED WITH ”-“)减:所得税费用 Less: Income tax expenses五、净利润(净亏损以“-”号填列)NET PROFIT(LOSS EXPRESSED WITH ”-")归属于母公司所有者的净利润Net profit belonging to parent company少数股东损益 Minority interest六、每股收益: EARNINGS PER SHARE(EPS)基本每股收益 Basic EPS稀释每股收益 Diluted EPS七、其他综合收益 OTHER CONSOLIDATED INCOME八、综合收益总额 TOTAL CONSOLIDATED INCOME归属于母公司所有者的综合收益总额Consolidated income belonging to parent company归属于少数股东的综合收益总额Consolidated income belonging to Minority shareholders九、补充资料 SUPPLEMENTARY INFORMATION营业总收入中:出口产品销售收入 Including overall sales:sales income of export products营业总成本中:出口产品销售成本 Including overall costs:sales cost of export products第三篇:模具常用专业术语中英文对照塑料模具常用专业术语中英文对照模胚(架): mold base三板模(细水口):3-plate mold二板模(大水口):2-plate 定位圈(法栏)locating ring 浇口套(唧嘴)sprue bushing热流道: hot runner,hot manifold面板:cavity adaptor plate 水口板:runner stripper plate 上模板(A板):cavity plate 下模板(B板):core plate 上内模(型腔\母模\凹模):cavity insert下内模(型芯\公模\凸模):core insert 推板:stripper plate 模脚(方铁)spacer plate 顶针板:ejector retainner plate托板(顶针底板): support plat垃圾钉:stop pin撑头: support pillar底板:coreadaptor plate 推杆:push bar 顶针: ejector pin 司筒:ejector sleeve司筒针:ejector pin 回针:push bake pin 导柱:leader pin/guide pin 导套:bushing/guide bushing中托司(顶针板导套):shoulder guide bushing中托边(顶针板导柱):guide pin滑块(行位): slide 波子弹弓(定位珠):ball catch 耐磨板/油板:wedge wear 压条:plate斜导边(斜导柱):angle pin压座/铲鸡:wedge斜顶:angle from pin 斜顶杆:angle ejector rod 缩呵:movable core,return core core puller尼龙拉勾(扣机):nylonlatch lock栓打螺丝:S.H.S.B 镶针:pin喉塞: pipe plug锁模块:lock plate挡板:stop plate螺丝: screw推板:stripper plate斜顶:lifterplate塑胶管:plastic tube快速接头:jiffy quick connector plug/sockermold内模管位:core/cavity inter-lockflash(塑件)毛边电极(铜公):copper electrode五金模具常用专业术语中英文对照cutting die, blanking die冲裁模progressive die, follow(-on)die 连续模compound die复合模punched hole冲孔panel board镶块to cutedges=side cut=side scrap切边to bending折弯to pull, to stretch拉伸Line streching, line pulling线拉伸engraving, to engrave刻印 top plate上托板(顶板)top block 上垫脚punch set上模座punch pad上垫板punch holder上夹板stripper pad脱料背板up stripper上脱料板die pad下垫板die holder下夹板die set下模座bottom block下垫脚bottom plate 底板(下托板)stripping plate 脱料板(表里打)outer stripper外脱料板inner stripper内脱料板lower stripper 下脱料板上模座upper die set 成型公 form punch脱料板stripper 垫板subplate/backup plate下模座die plate垫脚parallel托板mounting plate 顶料销kick off初始管位first start pin 带肩螺丝shoulder screw两用销lifter pin弹簧护套spring cage 拔牙螺丝jack screw侧冲组件 cam sectionbites导导正装置 guide equipment 尺rail漏废料孔 slug hole限位块stop block送料板rail plate刀口trim line挡块stopper倒角chamfer入子insert 浮块lifter 销钉dowel 护套bushing压块keeper尖角sharp--angle整形公restrike forming 靠块heel 普通弹簧coil springpunch 对正块alignmentblock镶件insert止挡板stop plate闭合高度shuthight 插针pilot pin挂台head 上夹板/固定座顶杆lifter bolt扣位pocket of head导柱guide post导套guide bushing油嘴oil nipple接刀口mismatch/cookieholder/retainer下模座lower die set成刑母公formingdie码模槽mounting slot 球锁紧固定座ball-lock起吊孔handing hole垫片shim/wear-plate键槽key slot沉孔counter hole导正块thrustblock 第四篇:音乐专业术语中英文对照Accordion 手风琴Aftertouch 触后Alto 女低音Amplitude 振幅Amplitude Modulation(AM)调幅Analogue 模拟的Anticipation 先现音Arpeggio 琶音,分解和弦Attack 起音Audio 音频Augmented 增音程,增和弦Ballade 叙事曲Band 波段,大乐队Banjo 班卓琴(美国民间乐器)Bank 音色库Baritone 男中音Barline 小节线Baroque 巴罗克Bass 贝司Bassoon 大管(巴松)Brass 铜管总称Cassette 卡座Cello 大提琴Channel 音色通道Choir 人声合唱Chord 和弦Chorus 合唱效果器Clarinet 单簧管Clef 谱号Combination 组合音色Compressor 压缩效果器Concerto 协奏曲Console 调音台Contrabass 低音提琴Ctrl 控制器Cymbal 镲,钹Decay 衰减Delay 延迟效果器Digital 数码的Diminished 减音程,减和弦Distorted 失真效果器Dolby NR 杜比降噪 Dominant 属音(和弦)Dot 附点Drum 鼓Duration 音符的时值Echo 回声,反射Effector 效果器Encore 返场加演曲目English Horn 英国管Enhance 增益Envelope 包络EQ(Equalizer)均衡器Exciter 激励器External 外置的,外部设备的Fade in 淡入Fade out 淡出Fantasia 幻想曲Filter 滤波器Flange 凸缘效果器Flat 降号Flute 长笛French Horn 圆号(法国号)Frequency 频率Frequency Modulation(FM)调频Fret 吉它指板Fretless Bass 无品贝司Grace Note 装饰音Grand Piano 三角钢琴Graphic 图解式的Guitar 吉它Harmonica 口琴Harmony 和声,和声学Harp 竖琴Harpsichord 古钢琴Instrument 乐器Intermezzo 间奏曲Internal 内置的,内部的Interval 音程Inversion 转位Key 调Keyboard 键盘Leading-note 导音LFO 低频震荡器 Loop 循环反复Lyric 歌词Major 大调的March 进行曲Measure 小节Metronome 节拍器Minor 小调的Modulation 调制Mordent 波音Monitor 监听Mono 单声道Multiple 多重,多轨Mute 静音Nocturne 夜曲Normalize 最大化波形Note 音符Nylon 尼龙弦吉它Oboe 双簧管Octave 八度Opera 歌剧Orchestral 交响乐团Organ 管风琴Overdrive 过载效果器Overture 序曲Pad 铺垫和弦Pan 相位Pattern 模板Pedal 踏板Percussion 打击乐Phase 相位调整Phones 耳机Piccolo 短笛Pitch 音高Pitch Bend 音高的滑动(推弦)Pizz String 弦乐器拨弦Playback 回放Polyphony 复调,复音数Prelude 前奏曲Quantize 量化Quartet 四重奏(唱)Quintet 五重奏(唱)Realtime 实时的 Recorder 竖笛Relative key 关系调Release 释音Renaissance 文艺复兴Reverb 混响Reverse 颠倒位置Rhapsody 狂想曲Sample 采样器Sample rate 采样率Sampler 采样器Sawtooth 锯齿波Sax 萨克斯Scale 音阶Score 谱面Serenade 小夜曲Sequencer 音序器Sharp 升号Sine 正弦波Sitar 西他(印度乐器)SMPTE 音视频同步码Solo 独奏Sonata 奏鸣曲Soprano 女高音Spectrum 频谱Square 方型波Staff 五线谱Steel 钢弦吉它Stereo 立体声Strings 弦乐器Subdominant 下属音(和弦)Suspension 延留音Sustain 延音(踏板)Symphony 交响曲Synth 合成的Synthesizer 合成器Tab 吉它六线谱Tape 磁带Tempo 速度Tenor 男高音Timpani 定音鼓Tonica 主和弦Track 音轨 Transpose 移调Tremolo 颤音Trembone 长号Trio 三重奏(唱)Trumpet 小号Tuba 大号Turn 调音Velocity 触键力度Vibrato 颤音,振动Viola 中提琴Violin 小提琴Voice 声部Volume 音量Wah 哇音效果器Xylophone 木琴第五篇:物探专业术语中英文对照lunar tide太阴潮 solar tide太阳潮 turbulence湍流spectrum of turbulence湍流谱turbulent diffusion湍流扩散turbulent dissipation湍流耗散turbulent exchange湍流交换turbulent mixing湍流混合 twilight曙暮光 wind shear风切变 yield function产额函数zonal circulation纬向环流zonal wind纬向风airglow气辉MST radarMST雷达,对流层、平流层、中层大气探测雷达。

会计英文词汇大全A (1)account 账户,报表A (2)accounting postulate 会计假设A (3)accounting valuation 会计计价A (4)accountability concept 经营责任概念A (5)accountancy 会计职业A (6)accountant 会计师A (7)accounting 会计A (8)agency cost 代理成本A (9)accounting bases 会计基础A (10)accounting manual 会计手册A (11)accounting period 会计期间A (12)accounting policies 会计方针A (13)accounting rate of return 会计报酬率A (14)accounting reference date 会计参照日A (15)accounting reference period 会计参照期间A (16)accrual concept 应计概念A (17)accrual expenses 应计费用A (18)acid test ratio 速动比率(酸性测试比率)A (19)acquisition 收购A (20)acquisition accounting 收购会计A (21)adjusting events 调整事项A (22)administrative expenses 行政管理费A (23)amortization 摊销A (24)analytical review 分析性复核A (25)annual equivalent cost 年度等量成本法A (26)annual report and accounts 年度报告和报表A (27)appraisal cost 检验成本A (28)appropriation account 盈余分配账户A (29)articles of association 公司章程细则A (30)assets 资产A (31)assets cover 资产担保A (32)asset value per share 每股资产价值A (33)associated company 联营公司A (34)attainable standard 可达标准A (35)attributable profit 可归属利润A (36)audit 审计A (37)audit report 审计报告A (38)auditing standards 审计准则A (39)authorized share capital 额定股本A (40)available hours 可用小时A (41)avoidable costs 可避免成本B (42)back-to-back loan 易币贷款B (43)backflush accounting 倒退成本计算B (44)bad debts 坏帐B (45)bad debts ratio 坏帐比率B (46)bank charges 银行手续费B (47)bank overdraft 银行透支B (48)bank reconciliation 银行存款调节表B (49)bank statement 银行对账单B (50)bankruptcy 破产B (51)basis of apportionment 分摊基础B (52)batch 批量B (53)batch costing 分批成本计算B (54)beta factor B (市场)风险因素BB (55)bill 账单B (56)bill of exchange 汇票B (57)bill of lading 提单B (58)bill of materials 用料预计单B (59)bill payable 应付票据B (60)bill receivable 应收票据B (61)bin card 存货记录卡B (62)bonus 红利B (63)book-keeping 薄记B (64)Boston classification 波士顿分类B (65)breakeven chart 保本图B (66)breakeven point 保本点B (67)breaking-down time 复位时间B (68)budget 预算B (69)budget center 预算中心B (70)budget cost allowance 预算成本折让B (71)budget manual 预算手册B (72)budget period 预算期间B (73)budgetary control 预算控制B (74)budgeted capacity 预算生产能力B (75)business center 经营中心B (76)business entity 营业个体B (77)business unit 经营单位B (78)by-product 副产品C (79)called-up share capital 催缴股本C (80)capacity 生产能力C (81)capacity ratios 生产能力比率C (82)capital 资本C (83)capital assets pricing model 资本资产计价模式C (84)capital commitment 承诺资本C (85)capital employed 已运用的资本C (86)capital expenditure 资本支出C (87)capital expenditure authorization 资本支出核准C (88)capital expenditure control 资本支出控制C (89)capital expenditure proposal 资本支出申请C (90)capital funding planning 资本基金筹集计划C (91)capital gain 资本收益C (92)capital investment appraisal 资本投资评估C (93)capital maintenance 资本保全C (94)capital resource planning 资本资源计划C (95)capital surplus 资本盈余C (96)capital turnover 资本周转率C (97)card 记录卡C (98)cash 现金C (99)cash account 现金账户C (100)cash book 现金账薄C (101)cash cow 金牛产品C (102)cash flow 现金流量C (103)cash flow budget 现金流量预算C (104)cash flow statement 现金流量表C (105)cash ledger 现金分类账C (106)cash limit 现金限额C (107)CCA 现时成本会计C (108)center 中心C (109)changeover time 变更时间C (110)chartered entity 特许经济个体C (111)cheque 支票C (112)cheque register 支票登记薄C (113)classification 分类C (114)clock card 工时卡C (115)code 代码C (116)commitment accounting 承诺确认会计C (117)common cost 共同成本C (118)company limited by guarantee 有限担保责任公司C (119)company limited by shares 股份有限公司C (120)competitive position 竞争能力状况C (121)concept 概念C (122)conglomerate 跨行业企业C (123)consistency concept 一致性概念C (124)consolidated accounts 合并报表C (125)consolidation accounting 合并会计C (126)consortium 财团C (127)contingency plan 应急计划C (128)contingent liabilities 或有负债C (129)continuous operation 连续生产C (130)contra 抵消C (131)contract cost 合同成本C (132)contract costing 合同成本计算C (133)contribution centre 贡献中心C (134)contribution chart 贡献图C (135)control 控制C (136)control account 控制账户C (137)control limits 控制限度C (138)controllability concept 可控制概念C (139)controllable cost 可控制成本C (140)conversion cost 加工成本C (141)convertible loan stock 可转换为股票的贷款C (142)corporate appraisal 公司评估C (143)corporate planning 公司计划C (144)corporate social reporting 公司社会报告C (145)cost 成本C (146)cost account 成本账户C (147)cost accounting 成本会计C (148)cost accounting manual 成本手册C (149)cost adjustment 成本调整C (150)cost allocation 成本分配C (151)cost apportionment 成本分摊C (152)cost attribution 成本归属C (153)cost audit 成本审计C (154)cost benefit analysis 成本效益分析C (155)cost center 成本中心C (156)cost driver 成本动因C (157)cost of capital 资本成本C (158)cost of goods sold 销货成本C (159)cost of non-conformance 非相符成本C (160)cost of sales 销售成本C (161)cost reduction 成本降低C (162)cost structure 成本结构C (163)cost unit 成本单位C (164)cost-volume-profit analysis(CVP) 本量利分析C (165)costing 成本计算C (166)credit note 贷项通知C (167)credit report 信贷报告书C (168)creditor 债权人C (169)creditor days ratio 应付账款天数率C (170)creditors ledger 应付账款分类账C (171)critical event 关键事项C (172)critical path 关键路线C (173)cumulative preference shares 累积优先股C (174)current asset 流动资产C (175)current cost accounting 现时成本会计C (176)current liabilities 流动负债C (177)current purchasing power accounting 现时购买力会计C (178)current ratio 流动比率C (179)cut-off 截止C (180)CVP 本量利分析C (181)cycle time 周转时间D (182)debenture 债券D (183)debit note 借项通知D (184)debit capacity 举债能力D (185)debt ratio 债务比率D (186)debtor 债务人;应收账款D (187)debtor days ratio 应收账款天数率D (188)debtors ledger 应收账款分类账D (189)debtor' age analysis 应收账款账龄分析D (190)decision driven costs 决策连动成本D (191)decision tree 决策树D (192)defects 次品D (193)deferred expenditure 递延支出D (194)deferred shares 递延股份D (195)deferred taxation 递延税款D (196)delivery note 交货单D (197)departmental accounts 部门报表D (198)departmental budget 部门预算D (199)depreciation 折旧D (200)dispatch note 发运单D (201)development cost 开发成本D (202)differential cost 差别成本D (203)direct cost 直接成本D (204)direct debit 直接借项D (205)direct hours yield 直接小时产出率D (206)direct labour cost percentage rate 直接人工成本百分比D (207)direct labour hour rate 直接人工小时率D (208)directs on indirect work 间接工作事项上的工时D (209)discount rate 贴现率D (210)discounted cash flow 现金流量贴现D (211)discretionary cost 酌量成本D (212)distribution cost 摊销成本D (213)diversions 移用D (214)diverted hours 移用小时D (215)diverted hours ratio 移用工时比率D (216)dividend 股利D (217)dividend cover 股利产出率D (218)dividend per share 每股股利D (219)dog 疲软产品D (220)double entry accounting 复式会计D (221)double-entry book-keeping 复式薄记D (222)doubtful debts 可疑债务D (223)down time 停工时间D (224)dynamic programming 动态规划E (225)earning per share 每股盈利E (226)earning ratio 市盈率E (227)economic order quantity(EOQ) 经济订购批量E (228)efficient market hypothesis 有效市场假设E (229)efficiency ration 效率性比率E (230)element of cost 成本要素E (231)entity 经济个体E (232)environmental audit 环境审计E (233)environmental impact assessment 环境影响评价E (234)EOQ 经济订购批量E (235)equity 权益E (236)equity method of accounting 权益法会计计算E (237)equity share capital 权益股本E (238)equivalent units 当量E (239)event 事项E (240)exceptional items 例外事项E (241)expected value 期望值E (242)expenditure 支出E (243)expenses 费用E (244)external audit 外部审计E (245)external failure cost 外部损失成本E (246)extraordinary items 非常事项F (247)factory goods 让售商品F (248)factoring 应收帐款让售F (249)fair value 公允价值F (250)feedback 反馈F (251)FIFO 先近先出法F (252)final accounts 年终报表F (253)finance lease 融资租赁F (254)financial accounting 财务会计F (255)financial accounts calendar adjustment 财务报表的日历时间调整F (256)financial management 财务管理F (257)financial planning 财务计划F (258)financial statement 财务报表F (259)finished goods 完成品F (260)fixed asset 固定资产F (261)fixed overhead 固定制造费用F (262)fixed asset turnover 固定资产周转率F (263)fixed assets register 固定资产登记薄F (264)fixed cost 固定成本F (265)flexed budget 变动限额预算F (266)flexible budget 弹性预算F (267)float time 浮动时间F (268)floating charge 流动抵押F (269)flow of funds statement 资金流量表F (270)forecasting 预测F (271)founder's shares 发起人股份F (272)full capacity 满负荷生产能力F (273)function costing 职能成本计算F (274)functional budget 职能预算F (275)fund accounting 基金会计F (276)fundamental accounting concept 基础会计概念F (277)fungible assets 可互换资产F (278)futuristic planning 远景计划G (279)gap analysis 间距分析G (280)gearing 举债经营比率(杠杆)G (281)goal congruence 目标一致性G (282)going concern concept 持续经营概念G (283)goods received note 商品收讫单G (284)goodwill 商誉G (285)gross dividend yield 总股息产出率G (286)gross margin 总边际G (287)gross profit 毛利润G (288)gross profit percentage 毛利润百分比G (289)group 企业集团G (290)group accounts 集团报表H (291)high-geared 高结合杠杆(比例)H (292)hire purchase 租购H (293)historical cost 历史成本H (294)historical cost accounting 历史成本会计H (295)hours 小时H (296)hurdle rate 最低可接受的报酬率I (297)ideal standard 理想标准I (298)idle capacity ration 闲置生产能力比率I (299)idle time 闲置时间I (300)impersonal accounts 非记名账户I (301)imprest system 定额备用制度I (302)income and expenditure account 收益和支出报表I (303)incomplete records 不完善记录I (304)incremental cost 增量成本I (305)incremental yield 增量产出率I (306)indirect cost 间接成本I (307)indirect hours 间接小时I (308)insolvency 无力偿付I (309)intangible asset 无形资产I (310)integrated accounts 综合报表I (311)interdependency concept 关联性概念I (312)interest cover 利息保障倍数I (313)interlocking accounts 连锁报表I (314)internal audit 内部审计I (315)internal check 内部牵制I (316)internal control system 内部控制体系I (317)internal failure cost 内部损失成本I (318)internal rate of return(IRR) 内含报酬率I (319)inventory 存货I (320)investment 投资I (321)investment center 投资中心I (322)invoice register 发票登记薄I (323)issued share capital 已发行股本J (324)job 定单J (325)job card 工作卡J (326)job costing 工作成本计算J (327)job sheet 工作单J (328)joint cost 联合成本J (329)joint products 联产品J (330)joint stock company 股份公司J (331)joint venture 合资经营J (332)journal 日记账J (333)just-in-time(JIT) 适时制度J (334)just-in-time production 适时生产J (335)just-in-time purchasing 适时购买K (336)key factor 关键因素L (337)labour 人工L (338)labour transfer note 人工转移单L (339)leaning curve 学习曲线L (340)ledger 分类账户L (341)length of order book 定单平均周期L (342)letter of credit 信用证L (343)leverage 举债经营比率L (344)liabilities 负债L (345)life cycle costing 寿命周期成本计算L (346)LIFO 后近先出法L (347)limited liability company 有限责任公司L (348)limiting factor 限制因素L (349)line-item budget 明细支出预算L (350)liner programming 线性规划L (351)liquid assets 变现资产L (352)liquidation 清算L (353)liquidity ratios 易变现比率L (354)loan 贷款L (355)loan capital 借入资本L (356)long range planning 长期计划L (357)lost time record 虚耗时间记录L (358)low geared 低结合杠杆(比例)L (359)lower of cost or net realizable value concept 成本或可变净价孰低概念M (360)machine hour rate 机器小时率M (361)machine time record 机器时间记录M (362)managed cost 管理成本M (363)management accounting 管理会计M (364)management accounting concept 管理会计概念M (365)management accounting guides 管理会计指导方针M (366)management audit 管理审计M (367)management buy-out 管理性购买产权M (368)management by exception 例外管理原则M (369)margin 边际M (370)margin of safety ration 安全边际比率M (371)margin cost 边际成本M (372)margin costing 边际成本计算M (373)mark-down 降低标价M (374)mark-up 提高标价M (375)market risk premium 市场分险补偿M (376)market share 市场份额M (377)marketing cost 营销成本M (378)matching concept 配比概念M (379)materiality concept 重要性概念M (380)materials requisition 领料单M (381)materials returned note 退料单M (382)materials transfer note 材料转移单M (383)memorandum of association 公司设立细则M (384)merger 兼并M (385)merger accounting 兼并会计M (386)minority interest 少数股权M (387)mixed cost 混合成本N (388)net assets 净资产N (389)net book value 净账面价值N (390)net liquid funds 净可变现资金N (391)net margin 净边际N (392)net present value(NPV) 净现值N (393)net profit 净利润N (394)net realizable value 可变现净值N (395)net worth 资产净值N (396)network analysis 网络分析N (397)noise 干捞N (398)nominal account 名义账户N (399)nominal share capital 名义股本N (400)nominal holding 代理持有股份N (401)non-adjusting events 非调整事项N (402)non-financial performance measurement 非财务业绩计量N (403)non-integrated accounts 非综合报表N (404)non-liner programming 非线性规划N (405)non-voting shares 无表决权的股份N (406)notional cost 名义成本N (407)number of days stock 存货周转天数N (408)number of weeks stock 存货周转周数O (409)objective classification 客体分类O (410)obsolescence 陈旧O (411)off balance sheet finance 资产负债表外筹资O (412)offer for sale 标价出售O (413)operating budget 经营预算O (414)operating lease 经营租赁O (415)operating statement 营业报表O (416)operation time 操作时间O (417)operational control 经营控制O (418)operational gearing 经营杠杆O (419)operating plans 经营计划O (420)opportunity cost 机会成本O (421)order 定单O (422)ordinary shares 普通股O (423)out-of-date cheque 过期支票O (424)over capitalization 过分资本化O (425)overhead 制造费用O (426)overhead absorption rate 制造费用分配率O (427)overhead cost 制造费用O (428)overtrading 超过营业资金的经营P (429)paid cheque 已付支票P (430)paid-up share capital 认定股本P (431)parent company 母公司P (432)pareto distribution 帕累托分布P (433)participating preference shares 参与优先股P (434)partnership 合伙P (435)payable ledger 应付款项账户P (436)payback 回收期P (437)payments and receipts account 收入和支出报表P (438)payments withheld 保留款额P (439)payroll 工资单P (440)payroll analysis 工资分析P (441)percentage profit on turnover 利润对营业额比率P (442)period cost 期间成本P (443)perpetual inventory 永续盘存P (444)personal account 记名账户P (445)PEPT 项目评审法P (446)petty cash account 备用金账户P (447)petty cash voucher 备用金凭证P (448)physical inventory 实地盘存P (449)planning 计划P (450)planning horizon 计划时限P (451)planning period 计划期间P (452)policy cost 政策成本P (453)position audit 状况审计P (454)post balance sheet events 资产负债表编后事项P (455)practical capacity 实际生产能力P (456)pre-acquisition losses 购置前损失P (457)pre-acquisition profits 购置前利润P (458)preference shares 优先股P (459)preference creditors 优先债权人P (460)preferred creditors 优先债权人P (461)prepayments 预付款项P (462)present value 现值P (463)prevention cost 预防成本P (464)price ratio 市盈率P (465)prime cost 主要成本P (466)prime entry-books of 原始分录登记薄P (467)principal budget factor 主要预算因素P (468)prior charge capital 优先股P (469)prior year adjustments 以前年度调整P (470)priority base budgeting 优先顺序体制的预算P (471)private company 私人公司P (472)pro-forma invoice 预开发票P (473)problem child 问号产品P (474)process costing 分步成本计算P (475)process time 加工时间P (476)product cost 产品成本P (477)Product life cycle 产品寿命周期P (478)production cost 生产成本P (479)production cost of sales 售货成本P (480)production volume ratio 生产业务量比率P (481)profit center 利润中心P (482)profit per employee 每员工利润P (483)profit retained for the year 年度利润留存P (484)profit to turnover ratio 利润对营业额比率P (485)profit-volume graph 利量图P (486)profitability index 盈利指数P (487)programming 规划P (488)project evaluation and review technique 项目评审法P (489)projection 预计P (490)promissory note 本票P (491)prospectus 募债说明书P (492)provisions for liabilities and charges 偿债和费用准备P (493)prudent concept 稳健性概念P (494)public company 公开公司P (495)purchase order 订购单P (496)purchase requisition 请购单P (497)purchase ledger 采购账户Q (498)quality related costs 质量有关成本Q (499)queuing time 排队时间R (500)rate 率R (501)ratio 比率R (502)ration pyramid 比率金字塔R (503)raw material 原材料R (504)receipts and payments account 收入和支付报表R (505)receivable ledger 应收款项账户R (506)redeemable shares 可赎回股份R (507)redemption 赎回R (508)registered share capital 注册资本R (509)rejects 废品R (510)relevancy concept 相关性概念R (511)relevant costs 相关成本R (512)relevant range 相关范围R (513)reliability concept 可靠性概念R (514)replacement price 重置价格R (515)report 报表R (516)reporting 报告R (517)research cost, applied 应用性研究成本R (518)research cost, pure or basic 理论或基础研究成本R (519)reserves 留存收益R (520)residual income 剩余收益R (521)responsibility center 责任中心R (522)retention money 保留款额R (523)return on capital employed 运用资本报酬率R (524)returns 退回R (525)revenue 收入R (526)revenue center 收入中心R (527)revenue expenditure 收益支出R (528)revenue investment 收入性投资R (529)right issue 认股权发行R (530)rolling budget 滚动预算R (531)rolling forecast 滚动预测S (532)sales ledger 销售分类账S (533)sales order 销售定单S (534)sales per employee 每员工销售额S (535)scrap 废料S (536)scrip issue 红股发行S (537)secured creditors 有担保的债权人S (538)segmental reporting 分部报告S (539)selling cost 销售成本S (540)semi-fixed cost 半固定成本S (541)semi-variable cost 半变动成本S (542)sensitivity analysis 敏感性分析S (543)service cost center 服务成本中心S (544)service costing 服务成本计算S (545)set-up time 安装时间S (546)shadow prices 影子价格S (547)share 股票S (548)share capital 股份资本S (549)share option scheme 购股权证方案S (550)share premium 股票溢价S (551)sight draft 即期汇票S (552)single-entry book-keeping 单式薄记S (553)sinking fund 偿债基金S (554)slack time 松弛时间S (555)social responsibility cost 社会责任成本S (556)sole trader 独资经营者S (557)source and application of funds statement 资金来源和运用表S (558)special order costing 特殊定单成本计算S (559)staff costs 职工成本S (560)statement of account 营业账单S (561)statement of affairs 财务状况表S (562)statutory body 法定实体S (563)stock 存货S (564)stock control 存货控制S (565)stock turnover 存货周转率S (566)stocktaking 盘点存货S (567)stores requisition 领料申请单S (568)strategic business unit 战略性经营单位S (569)strategic management accounting 战略管理会计S (570)strategic planning 战略计划S (571)strategy 战略S (572)subjective classification 主体分类S (573)subscribed share capital 已认购的股本S (574)subsidiary undertaking 子公司S (575)sunk cost 沉没成本S (576)supply estimate 预算估计S (577)supply expenditure 预算支出S (578)suspense account 暂记账户S (579)SWOT analysis 长处和短处,机会和威胁分析S (580)system 制度,体系T (581)tactical planning 策略计划T (582)tactics 策略T (583)take-over 接收T (584)tangible asset 有形资产T (585)tangible fixed asset statement 有形固定资产表T (586)target cost 目标成本T (587)terotechnology 设备综合工程学T (588)throughput accounting 生产量会计T (589)time 时间T (590)time sheet 时间记录表T (591)total assets 总资产T (592)total quality management 全面质量管理T (593)total stocks 存货总计T (594)trade creditors 购货客户(应付账款)T (595)trade debtors 销货客户(应收账款)T (596)trading profit and loss account 营业损益表T (597)transfer price 转让价格T (598)transit time 中转时间T (599)treasurership 财务长制度T (600)trail balance 试算平衡表T (601)turnover 营业额U (602)uncalled share capital 未催缴股本U (603)under capitalization 不足资本化U (604)under or over-absorbed overhead 少吸收或多吸收的制造费用U (605)uniform accounting 统一会计U (606)uniform costing 统一成本计算U (607)unissued share capital 未发行股本V (608)value 价值V (609)value added 增值V (610)value analysis 价值分析V (611)value for money audit 经济效益审计V (612)vote 表决V (613)voucher 凭证W (614)waiting time 等候时间W (615)waste 废品(料)W (616)wasting asset 递耗资产W (617)weighted average cost of capital 资本的加权平均成本W (618)weighted average price 加权平均价格W (619)with resource 有追索权W (620)without recourse 无追索权W (621)working capital 营运资本W (622)write-down 减值Z (623)zero base budgeting 零基预算Z (624)zero coupon bond 无息债券Z (625)Z score 破产预测计分法。

会计专业英语知识点作为一门重要的商科专业,会计在各行各业中都扮演着重要的角色。

对于学习会计的学生来说,掌握好会计专业的英语知识点是非常必要的。

本文将介绍一些与会计专业相关的英语知识点,以帮助学生在学习和实践中更好地应用。

一、会计基础术语1. Assets(资产):在会计中,资产指的是公司拥有的具有现金价值的资源,包括现金、存货、房地产等。

2. Liabilities(负债):负债是指公司对外的债务或应付款项,在会计中包括借款、应付账款等。

3. Equity(所有者权益):也被称为净资产或股东权益,表示公司的所有者对于其资产净值的权益。

4. Revenue(收入):收入是指公司通过销售产品或提供服务而获得的资金流入。

5. Expenses(费用):费用是指公司为经营活动而发生的支出,包括租金、工资、税金等。

6. Balance Sheet(资产负债表):资产负债表是一份会计报表,以资产、负债和所有者权益的形式显示公司的财务状况。

二、会计报表1. Income Statement(利润表):利润表显示了公司在一定期间内的收入、费用和净利润。

2. Cash Flow Statement(现金流量表):现金流量表反映了公司在一定期间内现金收入、现金支出以及现金净增加额。

3. Statement of Retained Earnings(留存收益表):留存收益表展示了公司在一定期间内的净利润和分红情况。

4. Statement of Changes in Equity(权益变动表):权益变动表展示了公司在一段时间内所有者权益的变化情况,包括净利润、股东投资等。

三、审计和税务1. Audit(审计):审计是对公司财务报表和财务记录的全面审核和检查。

2. Taxation(税务):税务是指涉及支付税款和申报纳税义务的活动,包括个人所得税、企业所得税等。

3. Tax Return(纳税申报表):纳税申报表是个人或企业向税务机关报告收入和纳税情况的文件。

会计专业英语习题答案Chapter. 11-1As in many ethics issues, there is no one right answer. The local newspaper reported on this issue in these terms: "The company covered up the first report, and the local newspaper uncovered the company's secret. The company was forced to not locate here (Collier County). It became patently clear that doing the least that is legally allowed is not enough."1-21. B2. B3. E4. F5. B6. F7. X 8. E 9. X 10. B1-3a. $96,500 ($25,000 + $71,500)b. $67,750 ($82,750 – $15,000)c. $19,500 ($37,000 – $17,500)1-4a. $275,000 ($475,000 – $200,000)b. $310,000 ($275,000 + $75,000 – $40,000)c. $233,000 ($275,000 – $15,000 – $27,000)d. $465,000 ($275,000 + $125,000 + $65,000)e. Net income: $45,000 ($425,000 – $105,000 – $275,000) 1-5a. owner's equityb.liabilityc.assetd.assete.owner'sequity f. asset1-6a. Increases assets and increases owner’s equity.b. Increases assets and increases owner’s equity.c. Decreases assets and decreases owner’s equity.d. Increases assets and increases liabilities.e. Increases assets and decreases assets.1-71. increase2. decrease3.increase4. decrease1-8a. (1) Sale of catering services for cash, $25,000.(2) Purchase of land for cash, $10,000.(3) Payment of expenses, $16,000.(4) Purchase of supplies on account, $800.(5) Withdrawal of cash by owner, $2,000.(6) Payment of cash to creditors, $10,600.(7) Recognition of cost of supplies used, $1,400.b. $13,600 ($18,000 – $4,400)c. $5,600 ($64,100 – $58,500)d. $7,600 ($25,000 – $16,000 – $1,400)e. $5,600 ($7,600 – $2,000)1-9It would be incorrect to say that the business had incurred a net loss of $21,750. The excess of the withdrawals over the net income for the period is a decrease in the amount of owner’s equity in the business.1-10Balance sheet items: 1, 3, 4, 8, 9, 101-11Income statement items: 2, 5, 6, 71-12MADRAS COMPANYStatement of Owner’s EquityFor the Month Ended April 30, 2006Leo Perkins, capital, April 1, 2006 ...... $297,200 Net income for the month ................ $73,000Less withdrawals ........................... 12,000Increase in owner’s equity................ 61,000 Leo Perkins, capital, April 30, 2006 .... $358,2001-13HERCULES SERVICESIncome StatementFor the Month Ended November 30, 2006Fees earned ................................ $232,120 Operating expenses:Wages expense .......................... $100,100Rent expense ............................. 35,000Supplies expense ........................ 4,550Miscellaneous expense.................. 3,150Total operating expenses ............. 142,800 Net income .................................. $89,3201-14Balance sheet: b, c, e, f, h, i, j, l, m, n, oIncome statement: a, d, g, k1-151. b–investing activity2.a–operating activity3. c–financing activity4.a–operating activity1-16a. 2003: $10,209 ($30,011 – $19,802)2002: $8,312 ($26,394 – $18,082)b. 2003: 0.52 ($10,209 ÷ $19,802)2002: 0.46 ($8,312 ÷ $18,082)c. The ratio of liabilities to stockholders’ equity increased from2002 to 2003, indicating an increase in risk for creditors.However, the assets of The Home Depot are more than sufficient to satisfy creditor claims.Chapter. 22-1AccountAccount NumberAccounts Payable 21Accounts Receivable 12Cash 11Corey Krum, Capital 31Corey Krum, Drawing 32Fees Earned 41Land 13Miscellaneous Expense 53Supplies Expense 52Wages Expense 512-2Balance Sheet Accounts Income Statement Accounts1. Assets11 Cash12 Accounts Receivable13 Supplies14 Prepaid Insurance15Equipment2. Liabilities21 Accounts Payable22Unearned Rent3. Owner's Equity31 Millard Fillmore, Capital32 Millard Fillmore, Drawing4. Revenue41Fees Earned5. Expenses51 Wages Expense52 Rent Expense53 Supplies Expense59 Miscellaneous Expense2-3a. andb.Account Debited Account Credited Transaction T ype Effect Type Effect(1) asset + owner's equity +(2) asset + asset –(3) asset + asset –liability +(4) expense + asset –(5) asset + revenue +(6) liability –asset –(7) asset + asset –(8) drawing + asset –(9) expense + asset –Ex. 2–4(1) Cash...................................... 40,000Ira Janke, Capital ................... 40,000 (2) Supplies ................................. 1,800Cash................................... 1,800 (3) Equipment ............................... 24,000Accounts Payable ................... 15,000Cash................................... 9,000 (4) Operating Expenses ................... 3,050Cash................................... 3,050 (5) Accounts Receivable .................. 12,000Service Revenue ..................... 12,000 (6) Accounts Payable ...................... 7,500Cash................................... 7,500 (7) Cash...................................... 9,500Accounts Receivable ............... 9,500 (8) Ira Janke, Drawing ..................... 5,000Cash................................... 5,000 (9) Operating Expenses ................... 1,050Supplies .............................. 1,0502-51. debit and credit (c)2. debit and credit (c)3. debit and credit (c)4. credit only (b)5. debit only (a)6. debit only (a)7. debit only (a)2-6a. Liability—credit f. Revenue—creditb. Asset—debit g. Asset—debitc. Asset—debit h. Expense—debitd. Owner's equity i. Asset—debit(Cindy Yost, Capital)—credit j. Expense—debite. Owner's equity(Cindy Yost, Drawing)—debit2-7a. credit g. debitb. credit h. debitc. debit i. debitd. credit j. credite. debit k. debitf. credit l. credit2-8a. Debit (negative) balance of $1,500 ($10,500 – $4,000– $8,000). Such a negative balance means that the liabilities of Seth’s business exceed the assets.b. Y es. The balance sheet prepared at December 31will balance, with Seth Fite, Capital, being reported in the owner’s equity section as a negative $1,500.2-9a. T he increase of $28,750 in the cash accountdoes not indicate earnings of that amount.Earnings will represent the net change in allassets and liabilities from operatingtransactions.b. $7,550 ($36,300 – $28,750)2-10a. $40,550 ($7,850 + $41,850 – $9,150)b. $63,000 ($61,000 + $17,500 – $15,500)c. $20,800 ($40,500 – $57,700 + $38,000)2-112005Aug.1 Rent Expense ........................... 1,500Cash................................... 1,5002 Advertising Expense (700)Cash (700)4 Supplies ................................. 1,050Cash................................... 1,0506 Office Equipment ....................... 7,500Accounts Payable ................... 7,5008 Cash...................................... 3,600Accounts Receivable ............... 3,60012 Accounts Payable ...................... 1,150Cash................................... 1,15020 Gayle McCall, Drawing ................ 1,000Cash................................... 1,00025 Miscellaneous Expense (500)Cash (500)30 Utilities Expense (195)Cash (195)31 Accounts Receivable .................. 10,150Fees Earned ......................... 10,15031 Utilities Expense (380)Cash (380)2-12a.JOURNAL Page 43Post.Date Description Ref. Debit Credit 2006Oct.27 Supplies .......................... 15 1,320Accounts Payable ............ 21 1,320Purchased supplies on account.b.,c.,d.Supplies 15Post.BalanceDate Item Ref. Dr. Cr.Dr. Cr.2006Oct. 1 Balance ................ ✓...... ...... 585 ......27 .......................... 43 1,320 ...... 1,905 ...... Accounts Payable 21 2006Oct. 1 Balance ................ ✓...... ...... ..... 6,15027 .......................... 43 ...... 1,320 ..... 7,4702-13Inequality of trial balance totals would be caused by errors described in (b) and (d).2-14ESCALADE CO.Trial BalanceDecember 31, 2006Cash ........................................... 13,375 Accounts Receivable .......................... 24,600Prepaid Insurance .............................. 8,000 Equipment ...................................... 75,000 Accounts Payable .............................. 11,180 Unearned Rent ................................. 4,250 Erin Capelli, Capital ........................... 82,420 Erin Capelli, Drawing .......................... 10,000Service Revenue ................................ 83,750 Wages Expense ................................ 42,000 Advertising Expense ........................... 7,200 Miscellaneous Expense ....................... 1,425 181,600 181,6002-15a. Gerald Owen, Drawing ................ 15,000Wages Expense ..................... 15,000b. Prepaid Rent ............................ 4,500Cash................................... 4,5002-16题目的资料不全, 答案略.2-17a. KMART CORPORATIONIncome StatementFor the Years Ending January 31, 2000 and 1999(in millions)Increase (Decrease)2000 1999 Amount Percent1. Sales .......................... $37,028 $35,925 .......................... $ 1,1033.1%2. Cost of sales ................ (29,658)(28,111) ......................... 1,5475.5%3. Selling, general, and admin.expenses ..................... (7,415) (6,514) 901 13.8%4. Operating income (loss)before taxes ................. $ (45) $1,300$(1,345)(103.5%)b. The horizontal analysis of Kmart Corporation revealsdeteriorating operating results from 1999 to 2000.While sales increased by $1,103 million, a 3.1%increase, cost of sales increased by $1,547 million, a5.5% increase. Selling, general, and administrativeexpenses also increased by $901 million, a 13.8%increase. The end result was that operating incomedecreased by $1,345 million, over a 100% decrease,and created a $45 million loss in 2000. Little over ayear later, Kmart filed for bankruptcy protection. It hasnow emerged from bankruptcy, hoping to return toprofitability.3-11. Accrued expense (accrued liability)2. Deferred expense (prepaid expense)3. Deferred revenue (unearned revenue)4. Accrued revenue (accrued asset)5. Accrued expense (accrued liability)6. Accrued expense (accrued liability)7. Deferred expense (prepaid expense)8. Deferred revenue (unearned revenue)3-2Supplies Expense (801)Supplies (801)3-3$1,067 ($118 + $949)3-4a. Insurance expense (or expenses) will be understated.Net income will be overstated.b. Prepaid insurance (or assets) will be overstated.Owner’s equity will be overstated.3-5a.Insurance Expense ............................ 1,215Prepaid Insurance ...................... 1,215 b.Insurance Expense ............................ 1,215Prepaid Insurance ...................... 1,2153-6Unearned Fees ................................... 9,570Fees Earned ............................ 9,5703-7a.Salary Expense ................................ 9,360Salaries Payable ........................ 9,360 b.Salary Expense ................................ 12,480Salaries Payable ........................ 12,480 3-8$59,850 ($63,000 – $3,150)3-9$195,816,000 ($128,776,000 + $67,040,000)3-10Error (a) Error (b)Over- Under- Over-Under-stated stated stated stated1. Revenue for the year would be $ 0 $6,900 $ 0 $ 02. Expenses for the year would be 0 0 0 3,7403. Net income for the year would be 0 6,900 3,740 04. Assets at December 31 would be 0 0 0 05. Liabilities at December 31 would be 6,900 0 0 3,7406. Own er’s equity at December 31would be ......................... 0 6,900 3,740 03-11$175,840 ($172,680 + $6,900 – $3,740)3-12a.Accounts Receivable .......................... 11,500Fees Earned ............................ 11,500b. No. If the cash basis of accounting is used, revenuesare recognized only when the cash is received.Therefore, earned but unbilled revenues would not berecognized in the accounts, and no adjusting entrywould be necessary.3-13a. Fees earned (or revenues) will be understated. Netincome will be understated.b. Accounts (fees) receivable (or assets) will beunderstated. Owner’s equity will be understated.3-14Depreciation Expense ........................... 5,200Accumulated Depreciation ............ 5,200 3-15a. $204,600 ($318,500 – $113,900)b. No. Depreciation is an allocation of the cost of theequipment to the periods benefiting from its use. Itdoes not necessarily relate to value or loss of value.3-16a. $2,268,000,000 ($5,891,000,000 – $3,623,000,000)b. No. Depreciation is an allocation method, not avaluation method. That is, depreciation allocates thecost of a fixed asset over its useful life. Depreciationdoes not attempt to measure market values, whichmay vary significantly from year to year.3-17a.Depreciation Expense ......................... 7,500Accumulated Depreciation ............ 7,500 b. (1) D epreciation expense would be understated. Netincome would be overstated.(2) A ccumulated depreciation would be understated,and total assets would be overstated. Owner’sequity would be overstated.3-181.Accounts Receivable (4)Fees Earned (4)2.Supplies Expense (3)Supplies (3)3.Insurance Expense (8)Prepaid Insurance (8)4.Depreciation Expense (5)Accumulated Depreciation—Equipment 5 5.Wages Expense (1)Wages Payable (1)3-19a. Dell Computer CorporationAmount Percent Net sales $35,404,000 100.0Cost of goods sold (29,055,000) 82.1Operating expenses (3,505,000) 9.9Operating income (loss) $2,844,000 8.0b. Gateway Inc.Amount Percent Net sales $4,171,325 100.0Cost of goods sold (3,605,120) 86.4Operating expenses (1,077,447) 25.8Operating income (loss) $(511,242)(12.2)c. Dell is more profitable than Gateway. Specifically,Dell’s cost of goods sold of 82.1% is significantly less(4.3%) than Gateway’s cost of goods sold of 86.4%.In addition, Gateway’s operating expenses are over one-fourth of sales, while Dell’s operating expenses are 9.9% of sales. The result is that Dell generates an operating income of 8.0% of sales, while Gateway generates a loss of 12.2% of sales. Obviously, Gateway must improve its operations if it is to remain in business and remain competitive with Dell.4-1e, c, g, b, f, a, d4-2a. Income statement: 3, 8, 9b. Balance sheet: 1, 2, 4, 5, 6, 7, 104-3a. Asset: 1, 4, 5, 6, 10b. Liability: 9, 12c. Revenue: 2, 7d. Expense: 3, 8, 114-41. f2. c3. b4. h5. g6. j7. a8. i9. d10. e4–5ITHACA SERVICES CO.Work SheetFor the Year Ended January 31, 2006AdjustedTrial Balance Adjustments TrialBalanceAccount Title Dr. Cr. Dr. Cr. Dr. Cr.1 Cash 8 8 12 Accounts Receivable50 (a) 7 57 23 Supplies 8 (b) 5 3 34 Prepaid Insurance 12 (c) 6 6 45 Land 50 50 56 Equipment 32 32 67 Accum. Depr.—Equip. 2 (d) 5 7 78 Accounts Payable 26 26 89 Wages Payable 0 (e) 1 1 910 Terry Dagley, Capital 112 112 1011 Terry Dagley, Drawing8 8 1112 Fees Earned 60 (a) 7 67 1213 Wages Expense 16 (e) 1 17 1314 Rent Expense 8 8 1415 Insurance Expense 0 (c) 6 6 1516 Utilities Expense 6 6 1617 Depreciation Expense0 (d) 5 5 1718 Supplies Expense 0 (b) 5 5 1819 Miscellaneous Expense 2 2 120 Totals 200 200 24 24213 213 20ContinueITHACA SERVICES CO.Work SheetFor the Year Ended January 31, 2006Adjusted Income BalanceTrial Balance StatementSheetAccount Title Dr. Cr. Dr. Cr. Dr. Cr.1 Cash 8 8 12 Accounts Receivable57 57 23 Supplies 3 3 34 Prepaid Insurance 6 6 45 Land 50 50 56 Equipment 32 32 67 Accum. Depr.—Equip. 7 7 78 Accounts Payable 26 26 89 Wages Payable 1 1 910 Terry Dagley, Capital 112 112 1011 Terry Dagley, Drawing8 8 1112 Fees Earned 67 67 1213 Wages Expense 17 17 1314 Rent Expense 8 8 1415 Insurance Expense 6 6 1516 Utilities Expense 6 6 1617 Depreciation Expense5 5 1718 Supplies Expense 5 5 1819 Miscellaneous Expense 2 2 120 Totals 213 213 49 67 164 146 2021 Net income (loss) 18 18 2122 67 67 164 164 224-6ITHACA SERVICES CO.Income StatementFor the Year Ended January 31, 2006Fees earned .................................... $67Expenses:Wages expense ............................ $17Rent expense (8)Insurance expense (6)Utilities expense (6)Depreciation expense (5)Supplies expense (5)Miscellaneous expense (2)Total expenses ...........................49Net income ...................................... $18ITHACA SERVICES CO.Statement of Owner’s EquityFor the Year Ended January 31, 2006 Terry Dagley, capital, February 1, 2005 .... $112 Net income for the year ....................... $18 Less withdrawals . (8)Increase in owner’s equity....................10Terry Dagley, capital, January 31, 2006 ... $122ITHACA SERVICES CO.Balance SheetJanuary 31, 2006Assets LiabilitiesCurrent assets: Current liabilities:Cash ............... $ 8 Accounts payable $26 Accounts receivable 57 .. Wages payable 1 Supplies ........... 3 Total liabilities . $ 27 Prepaid insurance 6Total current assets $ 74Property, plant, and Owner’s Equityequipment: Terry Dagley, capital (12)Land ............... $50Equipment ........ $32Less accum. depr. 7 25Total property, plant,and equipment 75 Total liabilities andTotal assets ......... $149 owner’s equity .. $1494-72006Jan.31 Accounts Receivable (7)Fees Earned (7)31 Supplies Expense (5)Supplies (5)31 Insurance Expense (6)Prepaid Insurance (6)31 Depreciation Expense (5)Accumulated Depreciation—Equipment 531 Wages Expense (1)Wages Payable (1)4-82006Jan.31 Fees Earned (67)Income Summary (67)31 Income Summary (49)Wages Expense (17)Rent Expense (8)Insurance Expense (6)Utilities Expense (6)Depreciation Expense (5)Supplies Expense (5)Miscellaneous Expense (2)31 Income Summary (18)Terry Dagley, Capital (18)31 Terry Dagley, Capital (8)Terry Dagley, Drawing (8)4-9SIROCCO SERVICES CO.Income StatementFor the Year Ended March 31, 2006Service revenue ................................$103,850Operating expenses:Wages expense ............................ $56,800Rent expense ............................... 21,270Utilities expense ............................ 11,500Depreciation expense ..................... 8,000Insurance expense ......................... 4,100Supplies expense .......................... 3,100Miscellaneous expense .................... 2,250Total operating expenses ....... 107,020Net loss ..........................................$ (3,170)4-10SYNTHESIS SYSTEMS CO.Statement of Owner’s EquityFor the Year Ended October 31, 2006 Suzanne Jacob, capital, November 1, 2005$173,750Net income for year ........................... $44,250 Less withdrawals ............................... 12,000 Increase in owner’s equity....................32,250Suzanne Jacob, capital, October 31, 2006 $206,0004-11a. Current asset: 1, 3, 5, 6b. Property, plant, and equipment: 2, 44-12Since current liabilities are usually due within one year, $165,000 ($13,750 × 12 months) would be reported as a current liability on the balance sheet. The remainder of $335,000 ($500,000 – $165,000) would be reported as a long-term liability on the balance sheet.4-13TUDOR CO.Balance SheetApril 30, 2006AssetsLiabilitiesCurrent assetsCurrent liabilities:Cash $31,500Accounts payable ........... $9,500Accounts receivable 21,850 Salaries payable1,750Supplies ............ 1,800 Unearned fees ............... Prepaid insurance 7,200 Total liabilitiesPrepaid rent ....... 4,800Total current assets $67,150 Owner’s E Property, plant, and equipment: Vernon Posey,capital 114,200Equipment ....... $80,600Less accumulated depreciation 21,100 59,500Total liabilities andTotal assets $126,650 owner’s equity ...............4-14Accounts Receivable ............................ 4,100Fees Earned ......................... 4,100 Supplies Expense ...................... 1,300Supplies .............................. 1,300 Insurance Expense ..................... 2,000Prepaid Insurance ................... 2,000 Depreciation Expense ................. 2,800Accumulated Depreciation—Equipment 2,800 Wages Expense ........................ 1,000Wages Payable ...................... 1,000 Unearned Rent .......................... 2,500Rent Revenue ........................ 2,5004-15c. Depreciation Expense—Equipmentg. Fees Earnedi. Salaries Expensel. Supplies Expense4-16The income summary account is used to close the revenue and expense accounts, and it aids in detectingand correcting errors. The $450,750 represents expense account balances, and the $712,500 represents revenue account balances that have been closed.4-17a.Income Summary ............................. 167,550Sue Alewine, Capital ................... 167,550 Sue Alewine, Capital ............................ 25,000Sue Alewine, Drawing ................. 25,000b. $284,900 ($142,350 + $167,550 – $25,000)4-18a. Accounts Receivableb. Accumulated Depreciationc. Cashe. Equipmentf. Estella Hall, Capitali. Suppliesk. Wages Payable4-19a. 2002 2001Working capital ($143,034)($159,453)Current ratio 0.81 0.80b. 7 Eleven has negative working capital as of December31, 2002 and 2001. In addition, the current ratio is below one at the end of both years. While the working capital and current ratios have improved from 2001 to 2002, creditors would likely be concerned about the ability of 7 Eleven to meet its short-term credit obligations. This concern would warrant further investigation to determine whether this is a temporaryissue (for example, an end-of-the-periodphenomenon) and the company’s plans to address itsworking capital shortcomings.4-20a. (1) Sales Salaries Expense ................ 6,480Salaries Payable ........................ 6,480(2) Accounts Receivable ................... 10,250Fees Earned ............................. 10,250b. (1) Salaries Payable ........................ 6,480Sales Salaries Expense ................ 6,480(2) Fees Earned ............................. 10,250Accounts Receivable ................... 10,2504-21a. (1) Payment (last payday in year)(2) Adjusting (accrual of wages at end of year)(3) Closing(4) Reversing(5) Payment (first payday in following year)b. (1) W ages Expense ........................ 45,000Cash ...................................... 45,000(2) Wages Expense ......................... 18,000Wages Payable .......................... 18,000(3) Income Summary .......................1,120,800Wages Expense ......................... 1,120,800(4) Wages Payable .......................... 18,000Wages Expense ......................... 18,000(5) Wages Expense ......................... 43,000Cash ...................................... 43,000 Chapter6(找不到答案,自己处理了哦)Ex. 8–1a. Inappropriate. Since Fridley has a large number ofcredit sales supported by promissory notes, a notesreceivable ledger should be maintained. Failure tomaintain a subsidiary ledger when there are asignificant number of notes receivable transactionsviolates the internal control procedure that mandates proofs and security. Maintaining a notes receivable ledger will allow Fridley to operate more efficiently and will increase the chance that Fridley will detect accounting errors related to the notes receivable. (The total of the accounts in the notes receivable ledger must match the balance of notes receivable in the general ledger.)b. Inappropriate. The procedure of proper separation ofduties is violated. The accounts receivable clerk is responsible for too many related operations. The clerk also has both custody of assets (cash receipts) and accounting responsibilities for those assets.c. Appropriate. The functions of maintaining theaccounts receivable account in the general ledger should be performed by someone other than the accounts receivable clerk.d. Appropriate. Salespersons should not be responsiblefor approving credit.e. Appropriate. A promissory note is a formal creditinstrument that is frequently used for credit periods over 45 days.Ex. 8–2-aa.Customer Due Date Number of DaysPast DueJanzen Industries August 29 93 days (2 + 30+ 31 + 30)Kuehn Company September 3 88 days (27 + 31+ 30)Mauer Inc. October 21 40 days (10 +30)Pollack Company November 23 7 daysSimrill Company December 3 Not past dueEx. 8–3Nov.30 Uncollectible Accounts Expense ..... 53,315*Allowances for Doubtful Accounts 53, *$60,495 – $7,180 = $53,315Ex. 8–4Estimated Uncollectible AccountsAge Interval Balance Percent AmountNot past due .............. $450,000 2% $9,0001–30 days past due...... 110,000 4 4,40031–60 days past due .... 51,000 6 3,06061–90 days past due .... 12,500 20 2,50091–180 days past due .. 7,500 60 4,500Over 180 days past due 5,500 80 4,400 Total .................... $636,500 $27,860Ex. 8–52006Dec. 31 Uncollectible Accounts Expense ..... 29,435*.A llowance for Doubtful Accounts 29,435 *$27,860 + $1,575 = $29,435Ex. 8–6a. $17,875 c. $35,750b. $13,600 d. $41,450Ex. 8–7a.Allowance for Doubtful Accounts ........... 7,130Accounts Receivable .................. 7,130b.Uncollectible Accounts Expense ............ 7,130Accounts Receivable .................. 7,130Ex. 8–8Feb.20 Accounts Receivable—Darlene Brogan 12,100 Sales .................................. 12,10020 Cost of Merchandise Sold ............ 7,260Merchandise Inventory .............. 7,260May30 Cash...................................... 6,000Accounts Receivable—Darlene Brogan 6,030 Allowance for Doubtful Accounts .... 6,100Accounts Receivable—Darlene Brogan 6,1Aug. 3Accounts Receivable—Darlene Brogan 6,100 Allowance for Doubtful Accounts . 6,1003 Cash...................................... 6,100Accounts Receivable—Darlene Brogan 6,1$223,900 [$212,800 + $112,350 –($4,050,000 × 21/2%)]Ex. 8–10Due Date Interesta. Aug. 31 $120b. Dec. 28 480c. Nov. 30 250d. May 5 150e. July 19 100Ex. 8–11a. August 8b. $24,480c. (1) N otes Receivable .......................... 24,000Accounts Rec.—Magpie Interior Decorators 24,(2) C ash......................................... 24,480Notes Receivable ....................... 24,000Interest Revenue (480)1. Sale on account.2. Cost of merchandise sold for the sale on account.3. A sales return or allowance.4. Cost of merchandise returned.5. Note received from customer on account.6. Note dishonored and charged maturity value of note tocustomer’s account receivable.7. Payment received from customer for dishonored noteplus interest earned after due date.Ex. 8–132005Dec.13 Notes Receivable ....................... 25,000Accounts Receivable—Visage Co. 25,31 Interest Receivable ..................... 75*Interest Revenue (75)31 Interest Revenue (75)Income Summary (75)2006。