Financial_Instruments10_questions

- 格式:doc

- 大小:56.50 KB

- 文档页数:6

Examination Problems for Fundamentals of Financial Management 2004-2005 (Paper B)overall goal in mind.A. Financial managementB. Profit maximizationC. Agency theoryD. Social responsibility2.A major disadvantage of the corporate form of organization is the ( ).A. double taxation of dividendsB. inability of the firm to raise large sums of additional capitalC. limited liability of shareholdersD. limited life of the corporate form.3. Interest paid (earned) on both the original principal borrowed (lent) and previous interest earned is often referred to as ( ).A. present valueB. simple interestC. future valueD. compound interest4. If the intrinsic value of a share of common stock is less than its market value, which of the following is the most reasonable conclusion?A. The stock has a low level of risk.B. The stock offers a high dividend payout ratio.C. The market is undervaluing the stock.D. The market is overvaluing the stock.5. A 250 face value share of preferred stock, pays a 20 annual dividend and investors require a 7% return on this investment. If the security is currently selling for 276, what is the difference (overvaluation) between its intrinsic and market value (rounded to the nearest whole dollar)?A. approximately 26B. approximately 10C. approximately 6D. approximately 16. Felton Farm Supplies, Inc., has an 8 percent return on total assets of 300,000 and a net profit margin of 5 percent. What are its sales?A. 3,750,000B. 480,000C. 300,000D. 1,500,0007. A company can improve (lower) its debt-to-total asset ratio by doing which of the following?A. Borrow more.B. Shift short-term to long-term debt.C. Shift long-term to short-term debt.D. isssue common stock.8. The DuPont Approach breaks down the earning power on shareholders' book value (ROE) as follows: ROE = ( ).A. Net profit margin × Total asset turnover × Equity multiplierB. Total asset turnover × Gross profit margin × Debt ratioC. Total asset turnover × Net profit marginD. Total asset turnover × Gross profit margin × Equity multiplier9. Which of the following items concerns financing decision? ( )A. sales forecastingB. bond issuingC. receivables collectionD. investment project selection10. Which of the following items is the function of a treasurer? ( )A. cost accountingB. internal controlC. capital budgetingD. general ledger11. For financial instruments, ( ) is judged in relation to the ability to sell a significant volume of securities in a short period of time without significant price concession.A. maturityB. marketabilityC. defaultD. inflation12. ( ) is the value at some future time of a present amount of money, or a series of payments, evaluated at a given interest rate.A. future valueB. present valueC. intrinsic valueD. market value13.Ellesmere Corporation issues 1 million $1 par value bonds. The stated interest rate is 6% per year and the interest is paid twice a year. What is the real interest rate of the bond? ( )A. 6%B.3%C. 12%D. (1+6%/2)2-114. Assume that dividends of a common stock will be maintained at D forever, and the required return of the stockholder is r, the par value of the stock is m, the value of the stock is ( )A. mB. m+DC. m+D/rD. D/r15. Which of the following items has the most risk? ( )A. treasury billB. corporate bondC. preferred stockD. common stock16. ( ) equals the gross profit divided by net sales of a firm.A. gross profit marginB. net profit marginC. return on investmentD. return on equity17. ( A ) is the ratios that measure a firm’s ability to meet short-term obligationsA. liquidity ratiosB. leverage ratios c. coverage ratios D. activity ratios18. ( A ) is the result of Net Profi t Margin × total asset turnover × (total assets/shareholders’ equity)A. Return on equityB. return on investmentC. current ratioD. quick ratio19. Government tax law adjustment is ( A ) to a firm.A. general economic riskB. inflation and deflation riskC. firm-specific riskD. international risk20 ( A ) equals the gross profit divided by net sales of a firm.A. gross profit marginB. net profit marginC. return on investmentD. return on equity II. Statement judgement (10 Points) (Please write your answer in the following1. Until around the first half of the 1900s, financial managers primarily raised funds and managed their firm’s cash positions. ( )2. In general, the higher the marketability of a security, the greater the yield necessary to attract investors ( )3. Discount Rate is the interest rate used to convert future values to present values. ( )4. The expected return of a portfolio is simply a weighted average of the expected return of the securities comprising that portfolio ( )5. The type of analysis varies according to the specific interests of the party involved ( )6. In a sole proprietorship, the owner is personally responsible for all financial obligations of thefirm. ( )7. When a stock goes "ex-rights, " its market price theoretically declines. ( )8. The market price of a particular bond is much greater today than it was yesterday. The calculated yield to maturity (YTM) based on today's market price would, therefore, be greater than the calculated YTM based on yesterday's market price. ( )9. A short average collection period assures us that accounts receivable are being efficiently managed. ( )10. Simple interest is interest that is paid on only the original amount borrowed (lent) ( )III. Questions (10 points) (Please write your answer on the answer paper)1. The method of depreciation does not alter the total amount deducted from income during the life of an asset. What does it alter and why is that important? (5 )2. What is primary and secondary market? (5)IV. Problems (60 Points) (Please write your answer on the answer paper)1. you need to have $100000 at the end of 10 years. To accumulate this sum, you have decided to save a certain amount at the end of each next 10 years and deposit it in the bank. The bank pays 8% interest compounded annually for long-term deposit. How much will you have to save each year? (PVIF(8%,10)=0.463, PVIFA(8%,10)=0.671, FVIF(8%,10)=2.159, FVIFA(8%,10)=14.487)2.Just today, Bird Seed Company’s common stock paid a $1.50 annual dividend per share and hada closing price of $24. Assume that the market’s required return for this investment is 12% and that dividends are expected to grow at a constant rate forever.a. calculate the implied growth rate in dividends.b. what is expected dividend yield and capital gains yield?3. The data for various companies in the same industry are as follows: (amounts are in millionDetermine the total asset turnover, net profit margin, and write your computation result in the table.4. You expect to deposit the following cash flows at the end of years 1 through 5, 1,000; 4,000; 9,000; 5,000; and 2,000 respectively. Alternatively, you could deposit a single amount today at the beginning of year 1 (end of year 0). How much is the single deposit needed to be today if you can earn 10% compounded annually? (10/ )5.Stock A has an expected growth rate of 16% for the first 3 years and 8% thereafter. Each share of stock just received an annual 3.24 dividend per share. The appropriate discount rate is 15%.What is the value of the common stock under this scenario? (10/ )6. The following common stocks are available for investment:COMMON STOCK (TICKER SYMBOL) BETANanyang Business Systems (NBS) 1.40Yunnan Garden Supply, Inc. (YUWHO) .80Bird Nest Soups Company (SLURP) .60! (WACHO) 1.80Park City Cola Company (BURP) 1.05Oldies Records, Ltd. (SHABOOM) .90a. If you invest 20 percent of your funds in each of the first four securities, and 10 percent in each of the last two, what is the beta of your portfolio? (5/ )b. If the risk-free rate is 8 percent and the expected return on the market portfolio is 14 percent, what will be the portfolio's expected return? (5/ )Solutions (B)1. Depreciation changes the timing of tax payments. The longer these payments can be delayed, the better off the business is.2. A primary market is a “new issues” market. Here, funds raised through the sale of new securities flow from ultimate savers to the ultimate investors in real assetsIn a secondary market, existing securities are bought and sold. Transactions in these already existing securities do not provide additional funds to finance capital investmentIV. Problems (60 Points) (Please write your answer on the answer paper)1. Answer:100000=A FVIF(8%,10)=14.487A A=100000/14.487=69032. Answer:a. 24=1.5(1+g)/(0.12-g), g=0.054b. dividend yield=0.12-g=0.066, capital gains yield=0.0541. (10/ ) Many different methods to lead to a correct solution.PV of this mixed flows problem = 1,000(PVIF10%,1) + 4,000(PVIF10%,2) + 9,000(PVIF10%,3) + 5,000(PVIF10%,4) + 2,000(PVIF10%,5) = 15,633.62.5. (1) Determine the annual dividends.D0 = $3.24 (this has been paid already)D1 = D0(1+g1)1 = $3.24(1.16)1 =3.76D2 = D0(1+g1)2 = $3.24(1.16)2 =4.36D3 = D0(1+g1)3 = $3.24(1.16)3 =5.06D4 = D3(1+g2)1 = $5.06(1.08)1 =5.46P3 = 5.46 / (.15 - .08) = $78 [CG Model](2) Determine the PV of cash flows.PV(D1) = D1(PVIF15%, 1) = 3.76 (.870) = 3.27PV(D2) = D2(PVIF15%, 2) = 4.36 (.756) = 3.30PV(D3) = D3(PVIF15%, 3) = 5.06 (.658) = 3.33PV(P3) = P3(PVIF15%, 3) = 78 (.658) = 51.32(3) Calculate the intrinsic value by summing all the cash flow present values.V = 3.27 + 3.30 + 3.33 + 51.326. a) (5/) The beta of a portfolio is simply a weighted average of the betas of the individual securities that make up the portfolio.TICKER SYMBOL BETA PROPORTION WEIGHTED BETANBS 1.40 .2 .280YUWHO .80 .2 .160SLURP .60 .2 .120W ACHO 1.80 .2 .360BURP 1.05 .1 .105SHABOOM .90 .1 .0901.0 1.115The portfolio beta is 1.115.b) (5/ ) Expected portfolio return=.08 + (.14 - .08)(1.115)= .08 + .0669 = .1469 or 14.69%。

财务会计英文影印版第十版课后练习题含答案简介本文档为《财务会计英文影印版第十版》的课后练习题及答案。

该书是一本介绍财务会计的教材,涵盖了财务会计理论和实践,适用于财务会计初学者。

练习题Chapter 11.1 Expln the difference between management accounting and financial accounting.1.2 Expln the purpose of financial statements.1.3 Expln the role of the audit committee.1.4 Expln the difference between the balance sheet and the income statement.Chapter 22.1 Expln the difference between revenue and profit.2.2 Expln the difference between cash basis accounting and accrual basis accounting.2.3 Expln the purpose of the statement of cash flows.Chapter 33.1 Expln the difference between current and non-current assets.3.2 Expln the difference between current and non-current liabilities.3.3 Expln the difference between financing activities and investing activities.Chapter 44.1 Expln the purpose of the double-entry accounting system.4.2 Expln the difference between debits and credits.4.3 Expln the purpose of the trial balance.Chapter 55.1 Expln the difference between the cost of goods sold and operating expenses.5.2 Expln the purpose of the income statement.5.3 Expln the difference between gross profit and net profit.答案Chapter 11.1 Management accounting is concerned with providing information for internal decision-making, while financial accounting is concerned with providing information to external users.1.2 The purpose of financial statements is to provide information about an entity’s financial performance, financial position, and cash flows.1.3 The audit committee is responsible for overseeing the financial reporting process and ensuring the integrity of financial statements.1.4 The balance sheet shows an entity’s financial position at a specific point in time, while the income statement shows an entity’s financial performance over a period of time.Chapter 22.1 Revenue represents the amounts earned from the sale of goods or services, while profit represents the difference between revenue and expenses.2.2 Cash basis accounting recognizes revenue and expenses when cash is received or pd, while accrual basis accounting recognizes revenue and expenses when they are earned or incurred, regardless of when cash is received or pd.2.3 The statement of cash flows is used to show the inflows and outflows of cash from operating, investing, and financing activities.Chapter 33.1 Current assets are expected to be converted to cash within one year, while non-current assets are expected to be held for more than one year.3.2 Current liabilities are expected to be pd within one year, while non-current liabilities are expected to be pd after one year.3.3 Financing activities involve obtning funds from external sources and paying dividends to shareholders, while investing activities involve acquiring and disposing of property, plant, and equipment, and other long-term investments.Chapter 44.1 The double-entry accounting system ensures that everytransaction is recorded in two accounts, with equal debits and credits,in order to mntn the equality of debits and credits in the accounting equation.4.2 Debits are used to record increases in assets and expenses and decreases in liabilities and equity, while credits are used to record increases in liabilities and equity and decreases in assets and expenses.4.3 The trial balance is a list of all the accounts in the ledgerwith their balances, used to ensure that the total of the debits equals the total of the credits.Chapter 55.1 The cost of goods sold represents the cost of the goods or services sold by a company, while operating expenses represent the other costs of running a business.5.2 The income statement shows a company’s revenue, expenses, andnet income or loss for a period of time.5.3 Gross profit represents revenue minus the cost of goods sold, while net profit represents gross profit minus operating expenses.结论本文档为《财务会计英文影印版第十版》课后练习题及答案,涵盖了财务会计的基本理论和实践。

投资学课后题及答案Chapter 1 The Investment Environment 1.What is a real asset?Real assets are used to produce goods and services. Real assets consist of land, labor, and buildings. These generate income to the economy and determine both the material wealth and productive capacity of the economy. Additionally, real assets appear on only one side of the balance sheet.2.What is a financial asset?Financial assets are claims on real assets and income from them. Financial assets consist of stocks and bonds. These contribute indirectly to the productive capacity of the economy. Additionally, financial assets appear on both sides of the balance sheet.3.What is consumption timing and why is it important? Consumption timing allows flexibility between earnings and spending. Therefore, when we are younger and we can consume more than we earn by borrowing money to by homes and automobiles. As we age, we can invest to so that we can retire someday and live off of our prior earnings. Financial assets4.What is allocation of risk and why is it important?Allocation of risk is creating assets with various degrees of risk. This enables firms to raise capital and also gives investors a choice of assets with various risk levels from which to choose5.What is separation of ownership and why is it important?The separation of ownership and management is important. Unlike a sole proprietorship where the owners are the managers, owners of corporations are stockholders. Stockholders elect the broad of directors that hires the management team. The objective that all owners can agree to is for management tomaximize the value of the firm (share price).6.What are the three sectors of the economy and what is theirprimary need?A. Firms are typically net borrowers as they seek to expand the firm and require resources to take on valuable projects.B. Households are typically net savers as they seek to use consumption timing to plan for longer-term financial requirements such as educating their children and investing for retirement. As such, they are interested in risk and after tax returns of investments.C. Governments are typically net borrowers but their needs depend on the current relationship between tax receipts and expenditures7.List and explain four important functions that financialintermediates perform.Financial intermediaries connect borrowers and lenders. Financial intermediaries are able to sell their own securities and invest in the liabilities of other firms. As such they can:A. pool resources to spread management costs over an larger base which reduces costs to an individual investor.B. diversify investments by being able to invest in more securities.C. develop expertise through the increased volume of business that they do.D. achieve economies of scale by being spread research costs over the pool.]8.What is securitization and why is it important?Securitization allows borrowers to enter capital markets directly. Loans are arranged into pass-through securities (such as mortgage pool) and investors can invest in securities backed bythose pools9.List and briefly explain five ways an investor can globallydiversityA primary market transaction is where securities are initially issued. Thus, the issuing firm receives the money and delivers the securities. The secondary market is where existing securities are traded. Thus, the firm that originally issued the securities receives no proceeds from the transaction. The individual selling the securities receives the money and delivers the securities while the individual buying the securities delivers the money 10.The four types of markets where trading takes place are listed below.A. Direct search markets. In direct search markets buyers and sellers must find each other. These markets are characterized by sporadic trading and low-priced non-standard goods such as refrigerator or sofas.B. Brokered markets. In markets that have active trading, brokers find it profitable to offer search services to buyers and seller. One example of this is real estate.C. Dealer market. In dealer markets, the dealers specialize by buying and selling for their own account. Dealers profit from the difference between their buying price and selling price (bid-ask spread). The OTC market is a dealer market.D. Auction market. In an auction market, such as the NYSE, all tradersconverge in one place to buy or sell an asset. Auction markets require heavy trading to make them efficient.11.The five ways for investors to globally diversify portfolio arelisted and discussed below.A.Investors can purchase American Depository Receipts (ADR=s) whichare a certificate that is denominated in dollars and represents a claim ona bundle of stock.B.Investors can purchase directly purchase foreign securities offered forsale in dollars.C.Investors can purchase international mutual funds that invest ininternational securities.D.Investors can purchase derivatives on foreign securities.E.Investors can purchase World Equity Benchmark Shares (WEBS) whichuse the same structure as an ADR but allow an investor to tradeportfolios of foreign stocks in a selected country.Chapter 2 Financial Instruments1.The price quotations of Treasury bonds in the Wall Street Journalshow an ask price of 101:12 and a bid price of 101:07.A. As a buyer of the bond what is the dollar price you expect to pay?B. As a seller of the bond what is the dollar price you expect to receive?A. You would pay the ask price of the dealer, 10112/32 or 101.375% of$10,000, or $10,137.50.B. You would receive the bid price of the dealer, 1017/32 or 101.21875% of$10,000, or $10,121.875.2.An investor is considering the purchase of either a municipal or acorporate bond that pay before tax rates of return of 6.92% and9.67%, respectively. If the investor is in the 25% marginal taxbracket, his or her after tax rates of return on the municipal and corporate bonds would be_________ and _________, respectively.Corporate bonds are taxable, therefore the after tax return would ber c=0.0967(1-0.25) =0.0725 or 7.25%. Since municipal bonds are free of federal tax the after tax return is equal to the before tax rate of return r m=0.0692(1-0) =6.92%.3. A 6.25% 25-year municipal bond is currently priced to yield8.7%. For a taxpayer in the 25% marginal tax bracket, this bondwould offer an equivalent taxable yield of __________.The equivalent taxable yield is the yield divided by the quantity one minus the tax rate or r m/ (1-t). Therefore, 0.087/0.75=11.6%.4.If three stocks comprise an index and the returns on the threestocks during a given period were 17%, -13%, and 6%, what would be the geometric return of the index?To compute a geometric average, add one to each of the returns and multiply each of the terms to find the geometric sum. To find the geometric average, the geometric sum is raised to 1/n and then one is subtracted. Therefore, the geometric mean is [(1.17) (0.87) (1.06)]1/3-1=2.566%.5.In order for you to be indifferent between the after tax returns ona corporate bond paying 8.15% and a tax-exempt municipalbond paying 6.32%, what would you tax bracket need to be? For you to be indifferent, the after tax returns would need to be equal. Since only the corporate bond is taxed, r c(1-t)= r m. Therefore,0.0632=0.0815(1-t), (1-t) =0.77546, and t=0.2245 or 22.45%.6. A $1,000 face value bond pays annual coupon payments of $65and is currently priced at $967. The current yield of the bond is __________.The current yield is annual interest divided by the current price ($65/$967) = 6.72%./doc/e714998860.html,pare the after tax return to a corporation that buys a share ofpreferred stock at the beginning of the year for $65, receives a dividend of $4.50 during the year, and sells the stock at the end of the year for $65. The corporation is in the 30% tax bracket.Answer the questions below based on the information given in the following table.Stock Price Number of shares outstandingStock A $35 2,000Stock B $82 4,500Stock C $21 1,600The total before tax income is the $4.50 dividend. Since the firm can exclude 70% of the dividend from tax, the firm must pay tax on 30% of the dividend, or ($4.50×0.30) =$1.35. Since the firm is in the 30% tax bracket the taxliability is $1.35×0.30=0.405. Therefore, the firm nets (aftertax)$4.50-0.41=4.09. Since the firm experienced no capital gain (or loss), the after tax return is $4.09/$65 = 0.06292 or 6.29%.8.The price-weighted index constructed with the three stocks is__________.A price weighted index is constructed by adding the prices of the securities and dividing by the number of securities in the index ($35 + $82 + $21)/3 = $46.9.The value-weighted index constructed with the three stocksusing a divisor of 1,000 is __________.A value-weighted index is computed by first computing the market value of each stock (price time the number of shares outstanding). Once each market value is computed, add the market values together and divide by the divisor. In this case it is [($35×2,000) + ($82×4,500) +($21×1,600)]/1,000 = 472.60.10.Assume that the return on stocks A, B, and C (above) during theyear were 18%, -6%, and 30%, respectively.A.The return of the price-weighted index would be__________.B.The return of the value-weighted index would be__________.C.The arithmetic return of the equally weighted index wouldbe__________.A. To compute the return of the price-weighted index you need to find the new prices of the stocks and then compute the average as follows:Stock A = [$35×(1.18)] = $41.30Stock A = [$82×(0.94)] = $77.08Stock A = [$21×(1.30)] = $27.30Average = (41.30 + 77.08 +27.30)/3 = $48.56.The change in the index value (return) is (48.56 - 46)/46 =5.565%.B. To compute the return of the value-weighted index you need to use the new prices to find the new value of the index. The return will be the change in the value of the index. In this case the new value is [($41.30×2,000) + ($77.08×4,500) + ($27.30×1,600)]/1,000 = 473.14. The old value is [($35×2,000) + ($82×4,500) + ($21×1,600)]/1,000 = 472.60. Therefore, the return is (473.14 – 472.60)/472.60 = 0.11%.C. The return of an equally weighted index is the sum of the return of eachsecurity in the index divided by the number of securities or [18% + (-6%) + 30%]/3 = 14%.Chapter 3 Security Markets1.Assume you purchased 400 shares of IBM common stock onmargin at $85 per share from your broker. If the initial margin is 60%, how much did you borrow from the broker?If you bought 400 shares@ $85/share, the cost is 400*$85=$34,000. Of this you invested $34,000*0.6=20,400 and borrowed$34,000*(1-0.6)=$13,600.2.You sold short 350 shares of common stock at $42 per share. Theinitial margin is 60%. Your initial investment was___________.If you sold short 350 share@ $42/share the proceeds are350*$42=$14,700. With a margin of 60% you must invest$14,700*0.6=$8,820.3.You purchased 1,000 shares of Cisco common stock on margin at$18 per share. Assume the initial margin is 50% and themaintenance margin is 30%. Below what stock price level would you get a margin call? Assume the stock pays no dividend; ignore interest on margin.If you purchased 1,000 shares@ $18/share the cost is$18*1,000=$18,000. Of this you must invest 50% and can borrow 50%.Therefore, the loan amount is $18,000*0.5=$9,000. Margin= [1,000P-$9,000]/1,000P.Therefore, 0.30 = (1,00P-$9,000)/1,000P; 300P=1,000P-$9,000;-700P=-$9,000; P=$12.864.You purchased 600 shares of common stock on margin at $27 pershare. Assume the initial margin is 50% and the stock pays nodividend. What would the maintenance margin be if a margin call is made at a stock price of $22? Ignore interest on margin.If you purchased 600 shares@ $27/share the cost is $27*600=$16,200.Therefore, you invest 50% and borrowed the other 50% of the amount.The loan amount is 16,200*0.5=%8,100.Margin = [600*$22-$8,100]/ 600*$22; Margin = 0.386 or 38.6%.5.You purchased 200 shares of common stock on margin at $35 pershare. Assume the initial margin is 50% and the stock pays no dividend. What would your rate of return be if you sell thestock at price of $45.50 per share? Ignore interest on margin.The initial investment is 200*$35*0.50=$3,500. The change in value of the stock is ($45.50-$35)*200 = $2,100. Therefore, the return =$2,000/$3,500 = 60%.6.Assume you sell short 100 shares of common stock at $30 pershare, with initial margin at 50% and the stock pays no dividend.What would your rate of return if you repurchase the stock at $37/share? The stock paid no dividends during the period, and you did not remove any money from the account before making the offsetting transaction.The profit on the stock is = ($30-$37)*100 = -$700. The initial investment is $100*0.30*0.5=1,500. Therefore, the return is -$700/$1,500 = -46.67%.7.You sold short 200 shares of common stock at $30 per share. Theinitial margin at 50%. At what stock price would you receive a margin call if the maintenance margin is 35%.The amount in your account is 200*$50*1.5 = $15,000 and you owe 200 shares of stock. Therefore your net equity is $15,000-200P.Margin = net equity/amount you owe or 0.35 = ($15,000 -200P)/200P.Rearranging, $70 = $15,000 –200P; 270P=$15,000; P = $55.55.8.Assume you sold short 100 shares of common stock at $25 pershare. The initial margin at 50%. What would be themaintenance margin if a margin call is made at a stock price of $30?The amount your account is $25*100*1.5 = $3,750 and you owe 100 shares of stock. Therefore your net equity is $3,750-100P.Margin = net equity/amount you owe or 0.35 = ($3,750-100*$30)/100*$30=25%..Rearranging, $70 = $15,000 –200P; 270P=$15,000; P = $55.55.9.You want to purchase AMAT stock at $42 from your broker usingas little of your own money as possible. If initial margin is 50% and you have $2,700 to invest, how many shares can you buy?The margin is 50% or = 0.5 = ($42Q - $2,700)/$42Q. Therefore, $21Q = $42Q - $2,700.Rearranging, -$21Q = -$2,700; Q = 128.54. Since you can only buy whole shares, you can buy 128 shares. Alternatively, you can buy[$2,700*2]/$42 = 128. 57 shares.10.You buy 150 shares of Citicorp for $25 per share and depositinitial margin of 50%. The next day Citicorp's price drop to $20 per share. What is your actual margin?The actual margin (AT) is AM = [150*$20-0.5*150*25]/[150*$20] =0.375 or 37.5%.Chapter 4 Mutual Funds and Other Investment Companies1. A mutual fund had NAV per share of $14.25 on January 1, 2003.On December 31 of the same year the fund's NAV was $14.87.Income distributions were $0.59 and the fund had capitalgain distributions of $1.36. Without considering taxes and transactions costs, what rate of return did an investor receive on the fund last year?The return is calculated by finding the change in value of the investment divided by the price. The change in value is the capital gain (whether realized or not) plus the sum of all distributions. Therefore,Return= ($14.87 -14.25 + 0.59 + 1.36)/ $14.25 = 18.04%.2. A mutual fund had NAV per share of $16.25 on January 1, 2003.On December 31 of the same year the fund's rate of return was14.2%. Income distributions were $1.02 and the fund had capitalgain distributions of $0.63. Without considering taxes and transactions costs, what ending NAV would you calculate?The return is equals the capital gain plus the all distributions divided by the investment. Therefore, 0.142 = (P - $16.25 + 1.02 + 0.63)/$16.25;P = $16.9075.3. A mutual fund had year-end assets of $316,000,000 andliabilities of $42,000,000. If the fund's NVA was $28.64, how many shares must have been held in the fund?The number of shares equals the assets minus the liabilities divided by the NAV. Therefore, ($316,000,000 - $42,000,000)/$28.64 =9,567,039.106 shares.4. A mutual fund had year-end assets of $750,000,000 andliabilities of $8,000,000. There were 40,750,000 shares in thefund at year end. What was the mutual fund's Net Asset Value?NAV equals assets minus liabilities divided by the number of shares.Therefore, ($750,000,000 – 8,000,000)/40,750,000 = $18.21.5. A mutual fund had average daily assets of $1.8 billion on 2003.The fund sold $625 million worth of stock and purchased $900 million worth of stock during the year. The fund's turnover ratio is ___________.Turnover is the value of securities sold divided by the average assets of the fund. Therefore, 625,000,000/1,800,000,000 = 34.7%.6.You purchased shares of a mutual fund at a price of $18 per shareat the beginning of the year and paid a front-end load of 5.75%.If the securities in which the fund invested increased in value by 12% during the year, and the fund's expense ratio was 0.75%, your return of you sold the fund at the end of the year would be _______.Since the fund has a front-end load, only (1-load) (or 0.9425) times NAV(18) is actually invested and growing. The money invested will grow at12% minus the 0.75% fees (or 11.25%). Therefore, [($18)(0.9425)(1.12-0.075) - $18]/$18 = 4.85% return.7.Apex fund has a NAV of 16.12 and a front load of 5.62%. What isthe offer price?The offer price equals NAV divided by one minus load. Therefore, $16.12 / (1 – 0.0562) = $17.08.8.Exponential growth fund has an offer price of 14.77 and a load of6%. What is the NAV?The offer price times on minus load equals NAV. Therefore, NAV equals $14.77 (0.94) = $13.889. A fund owns only three stocks with prices and quantities shownbelow. The fund has 50,000 shares outstanding. If the fund has $47,000 in liabilities, its NAV is________.Stock Price Number of shares outstandingStock A $35 2,000Stock B $82 4,500Stock C $21 1,600The value of assets is [($35?2,000) + ($82?4,500) + ($21?1.600)] = $472,600. Since NAV is asset minus liabilities divided by the number of shares outstanding, NAV = ($472,600 - $47,000)/50,000 = $8.5110.You have decided to invest $10,000 in the Pinnacle fund. Overthe long haul, the Pinnacle fund is expected to earn a return of10.25% on the portfolio (gross of fees). However, Pinnacle fundoffers several classes of funds. Therefore, you can choose to paya front load of 5% and escape 12-b1 fees or you can avoid theload fee by paying 12-b1 fees of 0.75%. If you investmenthorizon is 16 years, which should you choose?Since both strategies have a claim on the same portfolio ofsecurities, you need to compute you expected terminal wealth under each strategy.The terminal wealth in the no-load fund would be the initial investment ($10,000) times one plus the net rate of return (return minus 12-b1 fee) or 1.095 raised to the N number of years (16). Therefore, 10,00(1.095)16 = $42,719.48.The terminal wealth in the front-end load fund would be the initialinvestment in the portfolio ($10,000) (1-load) times on plus the rate of return or 1.1025 raised to the N number of years (16). Therefore,9,500(1.1025)16= $45,266.94.In this case, you would be better off with the load-end fund.———大猫。

高二英语金融理财单选题40题1.Which one is not a financial instrument?A.stockB.bondC.bookD.option答案:C。

book 不是金融工具,stock 是股票,bond 是债券,option 是期权,都属于金融工具。

2.If you want to invest in a company, you can buy its _____.A.sharesB.booksC.pensD.papers答案:A。

如果你想投资一家公司,可以买它的股票(shares)。

books 是书,pens 是笔,papers 是纸,都与投资公司无关。

3.A bond is a kind of _____.A.debt instrumentB.equity instrumentC.stationeryD.food答案:A。

债券是一种债务工具((debt instrument)。

equity instrument 是权益工具,stationery 是文具,food 是食物。

4.Which of the following is not a characteristic of stocks?A.High riskB.Low returnC.LiquidityD.Part ownership of a company答案:B。

股票的特点通常有高风险((High risk)、流动性((Liquidity)以及代表对公司的部分所有权((Part ownership of a company),而不是低回报(Low return)。

5.An option gives the holder the right to _____.A.buy or sell an assetB.read a bookC.eat an appleD.write a letter答案:A。

期权给予持有者买入或卖出一项资产的权利。

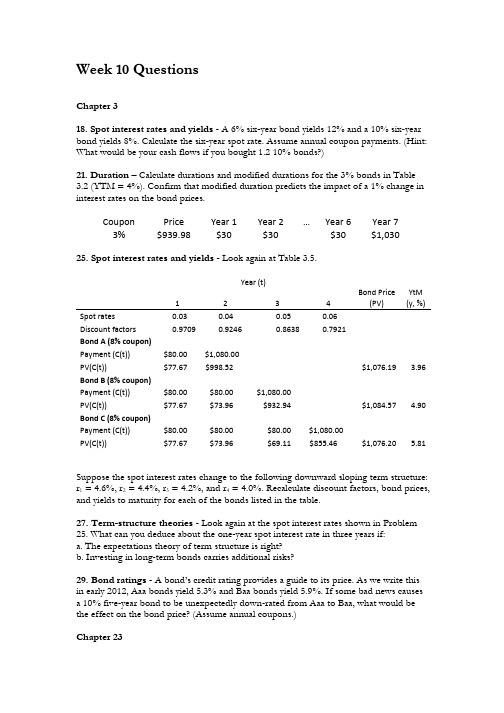

Week 10 QuestionsChapter 318. Spot interest rates and yields - A 6% six-year bond yields 12% and a 10% six-year bond yields 8%. Calculate the six-year spot rate. Assume annual coupon payments. (Hint: What would be your cash flows if you bought 1.2 10% bonds?)21. Duration –Calculate durations and modified durations for the 3% bonds in Table 3.2 (YTM = 4%). Confirm that modified duration predicts the impact of a 1% change in interest rates on the bond prices.Coupon Price Year 1 Year 2 … Year 6 Year 7 3% $939.98 $30 $30 $30 $1,03025. Spot interest rates and yields - Look again at Table 3.5.Year (t)12 3 4 Bond Price (PV)YtM (y, %)Spot rates 0.03 0.04 0.05 0.06 Discount factors 0.97090.92460.86380.7921Bond A (8% coupon)Payment (C(t)) $80.00 $1,080.00 PV(C(t))$77.67$998.52$1,076.19 3.96Bond B (8% coupon)Payment (C(t)) $80.00 $80.00 $1,080.00 PV(C(t))$77.67$73.96$932.94$1,084.57 4.90Bond C (8% coupon)Payment (C(t)) $80.00 $80.00 $80.00 $1,080.00 PV(C(t))$77.67$73.96$69.11$855.46$1,076.20 5.81Suppose the spot interest rates change to the following downward sloping term structure: r 1 = 4.6%, r 2 = 4.4%, r 3 = 4.2%, and r 4 = 4.0%. Recalculate discount factors, bond prices, and yields to maturity for each of the bonds listed in the table.27. Term-structure theories - Look again at the spot interest rates shown in Problem 25. What can you deduce about theone-year spot interest rate in three years if: a. The expectations theory of term structure is right? b. Investing in long-term bonds carries additional risks?29. Bond ratings - A bond’s credit rating provides a guide to its price. As we write this in early 2012, Aaa bonds yield 5.3% and Baa bonds yield 5.9%. If some bad news causes a 10% five-year bond to be unexpectedly down-rated from Aaa to Baa, what would be the effect on the bond price? (Assume annual coupons.)Chapter 239. Default Options - Company A has issued a single zero-coupon bond maturing in 10 years. Company B has issued a coupon bond maturing in 10 years. Explain why it is more complicated to value B’s debt than A’s.。

公司财务,第十版,课后答案CHAPTER 2FINANCIAL STATEMENTS AND CASH FLOWAnswers to Concepts Review and Critical Thinking Questions1.True. Every asset can be converted to cash at some price. However, when we are referring to a liquidasset, the added assumption that the asset can be quickly converted to cash at or near market value is important.2.The recognition and matching principles in financial accounting call for revenues, and the costsassociated with producing those revenues, to be “booked” when the revenue pro cess is essentially complete, not necessarily when the cash is collected or bills are paid. Note that this way is not necessarily correct; it’s the way accountants have chosen to do it.3.The bottom line number shows the change in the cash balance on the balance sheet. As such, it is nota useful number for analyzing a company.4. The major difference is the treatment of interest expense. The accounting statement of cash flowstreats interest as an operating cash flow, while the financial cash flows treat interest as a financing cash flow. The logic of the accounting statement of cash flows is that since interest appears on the income statement, which shows the operations for the period, it is an operating cash flow. In reality, interest is a financing e xpense, which results from the company’s choice of debt and equity. We will have more to say about this in a later chapter. When comparing the two cash flow statements, the financial statement of cash flows is a more appropriate measureof the company’s pe rformance because of its treatment of interest.5.Market values can never be negative. Imagine a share of stock selling for –$20. This would meanthat if you placed an order for 100 shares, you would get the stock along with a check for $2,000.How many shares do you want to buy? More generally, because of corporate and individual bankruptcy laws, net worth for a person or a corporation cannot be negative, implying that liabilities cannot exceed assets in market value.6.For a successful company that is rapidly expanding, for example, capital outlays will be large,possibly leading to negative cash flow from assets. In general, what matters is whether the money is spent wisely, not whether cash flow from assets is positive or negative.7.It’s probably not a good sign for an established company to have negative cash flow from operations,but it would be fairly ordinary for a start-up, so it depends.8.For example, if a company were to become more efficient in inventory management, the amount ofinventory needed would decline. The same might be true if the company becomes better at collecting its receivables. In general, anything that leads to a decline in ending NWC relative to beginning would have this effect. Negative net capital spending would mean more long-lived assets were liquidated than purchased.9.If a company raises more money from selling stock than it pays in dividends in a particular period,its cash flow to stockholders will be negative. If a company borrows more than it pays in interest and principal, its cash flowto creditors will be negative.10.The adjustments discussed were purely accounting changes; they had no cash flow or market valueconsequences unless the new accounting information caused stockholders to revalue the derivatives. Solutions to Questions and ProblemsNOTE: All end-of-chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability constraints, when these intermediate steps are included in this solutions manual, rounding may appear to have occurred. However, the final answer for each problem is found without rounding during any step in the problem.Basic1.To find owners’ equity, we must construct a balance sheet as follows:Balance SheetCA $ 5,700 CL $ 4,400NFA 27,000 LTD 12,900OE ??TA $32,700 TL & OE $32,700We know that total liabilities and owners’ equity (TL & OE) must equal total assets of $32,700. We also know that TL & OE is equal to current liabilities plus long-term debt plus owner’s equity, so owner’s equity is:O E = $32,700 –12,900 – 4,400 = $15,400N WC = CA – CL = $5,700 – 4,400 = $1,3002. The income statement for the company is:Income StatementSales $387,000Costs 175,000Depreciation 40,000EBIT $172,000Interest 21,000EBT $151,000Taxes 52,850Net income $ 98,150One equation for net income is:Net income = Dividends + Addition to retained earningsRearranging, we get:Addition to retained earnings = Net income – DividendsAddition to retained earnings = $98,150 – 30,000Addition to retained earnings = $68,1503.To find the book value of current assets, we use: NWC = CA – CL. Rearranging to solve for currentassets, we get:CA = NWC + CL = $800,000 + 2,400,000 = $3,200,000The market value of current assets and net fixed assets is given, so:Book value CA = $3,200,000 Market value CA = $2,600,000 Book value NFA = $5,200,000 Market value NFA = $6,500,000 Book value assets = $8,400,000 Market value assets = $9,100,0004.Taxes = 0.15($50,000) + 0.25($25,000) + 0.34($25,000) + 0.39($273,000 – 100,000)Taxes = $89,720The average tax rate is the total tax paid divided by net income, so:Average tax rate = $89,720 / $273,000Average tax rate = 32.86%The marginal tax rate is the tax rate on the next $1 ofearnings, so the marginal tax rate = 39%.5.To calculate OCF, we first need the income statement:Income StatementSales $18,700Costs 10,300Depreciation 1,900EBIT $6,500Interest 1,250Taxable income $5,250Taxes 2,100Net income $3,150OCF = EBIT + Depreciation – TaxesOCF = $6,500 + 1,900 – 2,100OCF = $6,300/doc/a95a227710a6f524cdbf8525.ht ml capital spending = NFA end– NFA beg + Depreciation Net capital spending = $1,690,000 – 1,420,000 + 145,000Net capital spending = $415,0007.The long-term debt account will increase by $35 million, the amount of the new long-term debt issue.Since the company sold 10 million new shares of stock with a $1 par value, the common stock account will increase by $10 million. The capital surplus account will increase by $48 million, the value of the new stock sold above its par value. Since the company had a net income of $9 million, and paid $2 million in dividends, the addition to retained earnings was $7 million, which will increase the accumulated retained earnings account. So, the new long-term debt and stockholders’ equity portion of the balance sheet will be:Long-term debt $ 100,000,000Total long-term debt $ 100,000,000Shareholders equityPreferred stock $ 4,000,000Common stock ($1 par value) 25,000,000Accumulated retained earnings 142,000,000Capital surplus 93,000,000Total equity $ 264,000,000Total Liabilities & Equity $ 364,000,0008.Cash flow to creditors = Interest paid – Net new borrowingCash flow to creditors = $127,000 – (LTD end– LTD beg)Cash flow to creditors = $127,000 – ($1,520,000 – 1,450,000) Cash flow to creditors = $127,000 – 70,000Cash flow to creditors = $57,0009. Cash flow to stockholders = Dividends paid –Net new equityCash flow to stockholders = $275,000 –[(Common end + APIS end) – (Common beg + APIS beg)]Cash flow to stockholders = $275,000 –[($525,000 + 3,700,000) – ($490,000 + 3,400,000)]Cash flow to stockholders = $275,000 –($4,225,000 –3,890,000)Cash flow to stockholders = –$60,000Note, APIS is the additional paid-in surplus.10. Cash flow from assets = Cash flow to creditors + Cash flow to stockholders= $57,000 – 60,000= –$3,000Cash flow from assets = OCF – Change in NWC – Net capital spending–$3,000 = OCF – (–$87,000) – 945,000OCF = $855,000Operating cash flow = –$3,000 – 87,000 + 945,000Operating cash flow = $855,000Intermediate11. a.The accounting statement of cash flows explains the change in cash during the year. Theaccounting statement of cash flows will be:Statement of cash flowsOperationsNet income $95Depreciation 90Changes in other current assets (5)Accounts payable 10Total cash flow from operations $190Investing activitiesAcquisition of fixed assets $(110)Total cash flow from investing activities $(110)Financing activitiesProceeds of long-term debt $5Dividends (75)Total cash flow from financing activities ($70)Change in cash (on balance sheet) $10b.Change in NWC = NWC end– NWC beg= (CA end– CL end) – (CA beg– CL beg)= [($65 + 170) – 125] – [($55 + 165) – 115)= $110 – 105= $5c.To find the cash flow generated by the firm’s assets, we need the operating cash flow, and thecapital spending. So, calculating each of these, we find:Operating cash flowNet income $95Depreciation 90Operating cash flow $185Note that we can calculate OCF in this manner since there are no taxes.Capital spendingEnding fixed assets $390Beginning fixed assets (370)Depreciation 90Capital spending $110Now we can calculate the cash flow generated by the firm’s assets, which is:Cash flow from assetsOperating cash flow $185Capital spending (110)Change in NWC (5)Cash flow from assets $ 7012.With the information provided, the cash flows from the firm are the capital spending and the changein net working capital, so:Cash flows from the firmCapital spending $(21,000)Additions to NWC (1,900)Cash flows from the firm $(22,900)And the cash flows to the investors of the firm are:Cash flows to investors of the firmSale of long-term debt (17,000)Sale of common stock (4,000)Dividends paid 14,500Cash flows to investors of the firm $(6,500)13. a. The interest expense for the company is the amount of debt times the interest rate on the debt.So, the income statement for the company is:Income StatementSales $1,060,000Cost of goods sold 525,000Selling costs 215,000Depreciation 130,000EBIT $190,000Interest 56,000Taxable income $134,000Taxes 46,900Net income $ 87,100b. And the operating cash flow is:OCF = EBIT + Depreciation – TaxesOCF = $190,000 + 130,000 – 46,900OCF = $273,10014.To find the OCF, we first calculate net income.Income StatementSales $185,000Costs 98,000Depreciation 16,500Other expenses 6,700EBIT $63,800Interest 9,000Taxable income $54,800Taxes 19,180Net income $35,620Dividends $9,500Additions to RE $26,120a.OCF = EBIT + Depreciation – TaxesOCF = $63,800 + 16,500 – 19,180OCF = $61,120b.CFC = Interest – Net new LTDCFC = $9,000 – (–$7,100)CFC = $16,100Note that the net new long-term debt is negative because the company repaid part of its long-term debt.c.CFS = Dividends – Net new equityCFS = $9,500 – 7,550CFS = $1,950d.We know that CFA = CFC + CFS, so:CFA = $16,100 + 1,950 = $18,050CFA is also equal to OCF – Net capital spending – Change in NWC. We already know OCF.Net capital spending is equal to:Net capital spending = Increase in NFA + DepreciationNet capital spending = $26,100 + 16,500Net capital spending = $42,600Now we can use:CFA = OCF – Net capital spending – Change in NWC$18,050 = $61,120 – 42,600 – Change in NWC.Solving for the change in NWC gives $470, meaning the company increased its NWC by $470.15.The solution to this question works the income statement backwards. Starting at the bottom:Net income = Dividends + Addition to ret. earningsNet income = $1,570 + 4,900Net income = $6,470Now, looking at the income statement:EBT –(EBT × Tax rate) = Net incomeRecognize that EBT × tax rate is simply the calculation for taxes. Solving this for EBT yields:EBT = NI / (1– Tax rate)EBT = $6,470 / (1 – .35)EBT = $9,953.85Now we can calculate:EBIT = EBT + InterestEBIT = $9,953.85 + 1,840EBIT = $11,793.85The last step is to use:EBIT = Sales – Costs – Depreciation$11,793.85 = $41,000 – 26,400 – DepreciationDepreciation = $2,806.1516.The market value of shareholders’ equity cannot be negative. A negative market value in this casewould imply that the company would pay you to own the stock. The market value of shareholders’ equity can be stated as: Shareholders’ equity = Max [(TA – TL), 0]. So, if TA is $12,400, equity is equal to $1,500, and if TA is $9,600, equity is equal to $0. We should note here that while the market value of equity cannot be negative, the book value of share holders’ equity can be negative. 17. a. Taxes Growth = 0.15($50,000) + 0.25($25,000) + 0.34($86,000 – 75,000) = $17,490Taxes Income = 0.15($50,000) + 0.25($25,000) + 0.34($25,000) + 0.39($235,000)+ 0.34($8,600,000 – 335,000)= $2,924,000b. Each firm has a marginal tax rate of 34% on the next $10,000 of taxable income, despite theirdifferent average tax rates, so both firms will pay an additional $3,400 in taxes.18.Income StatementSales $630,000COGS 470,000A&S expenses 95,000Depreciation 140,000EBIT ($75,000)Interest 70,000Taxable income ($145,000)Taxes (35%) 0/doc/a95a227710a6f524cdbf8525.ht ml income ($145,000)b.OCF = EBIT + Depreciation – TaxesOCF = ($75,000) + 140,000 – 0OCF = $65,000/doc/a95a227710a6f524cdbf8525.ht ml income was negative because of the tax deductibility of depreciation and interest expense.However, the actual cash flow from operations was positive because depreciation is a non-cash expense and interest is a financing expense, not an operating expense.19. A firm can still pay out dividends if net income is negative; it just has to be sure there is sufficientcash flow to make the dividend payments.Change in NWC = Net capital spending = Net new equity = 0. (Given)Cash flow from assets = OCF – Change in NWC – Net capitalspendingCash flow from assets = $65,000 – 0 – 0 = $65,000Cash flow to stockholders = Dividends – Net new equityCash flow to stockholders = $34,000 – 0 = $34,000Cash flow to creditors = Cash flow from assets – Cash flow to stockholdersCash flow to creditors = $65,000 – 34,000Cash flow to creditors = $31,000Cash flow to creditors is also:Cash flow to creditors = Interest – Net new LTDSo:Net new LTD = Interest – Cash flow to creditorsNet new LTD = $70,000 – 31,000Net new LTD = $39,00020. a.The income statement is:Income StatementSales $19,900Cost of good sold 14,200Depreciation 2,700EBIT $ 3,000Interest 670Taxable income $ 2,330Taxes 932Net income $1,398b.OCF = EBIT + Depreciation – TaxesOCF = $3,000 + 2,700 – 932OCF = $4,768c.Change in NWC = NWC end– NWC beg= (CA end– CL end) – (CA beg– CL beg)= ($5,135 – 2,535) – ($4,420 – 2,470)= $2,600 – 1,950 = $650Net capital spending = NFA end– NFA beg + Depreciation = $16,770 – 15,340 + 2,700= $4,130CFA = OCF – Change in NWC – Net capital spending= $4,768 – 650 – 4,130= –$12The cash flow from assets can be positive or negative, since it represents whether the firm raised funds or distributed funds on a net basis. In this problem, even though net income and OCF are positive, the firm invested heavily in both fixed assets and net working capital; it had to raise a net $12 in funds from its stockholders and creditors to make these investments.d.Cash flow to creditors = Interest – Net new LTD= $670 – 0= $670Cash flow to stockholders = Cash flow from assets – Cash flow to creditors= –$12 – 670= –$682We can also calculate the cash flow to stockholders as:Cash flow to stockholders = Dividends – Net new equitySolving for net new equity, we get:Net new equity = $650 – (–682)= $1,332The firm had positive earnings in an accounting sense (NI > 0) and had positive cash flow from operations. The firm invested $650 in new net working capital and $4,130 in new fixed assets.The firm had to raise $12 from its stakeholders to support this new investment. It accomplished this by raising $1,332 in theform of new equity. After paying out $650 of this in the form of dividends to shareholders and $670 in the form of interest to creditors, $12 was left to meet the firm’s cash flow needs for investment.21. a.Total assets 2011 = $936 + 4,176 = $5,112Total liabilities 2011 = $382 + 2,160 = $2,542Owners’ equity 2011 = $5,112 – 2,542 = $2,570Total assets 2012 = $1,015 + 4,896 = $5,911Total liabilities 2012 = $416 + 2,477 = $2,893Owners’ equity 2012 = $5,911 – 2,893 = $3,018b.NWC 2011 = CA11 – CL11 = $936 – 382 = $554NWC 2012 = CA12 – CL12 = $1,015 – 416 = $599Change in NWC = NWC12 – NWC11 = $599 – 554 = $45c.We can calculate net capital spending as:Net capital spending = Net fixed assets 2012 –Net fixed assets 2011 + DepreciationNet capital spending = $4,896 – 4,176 + 1,150Net capital spending = $1,870So, the company had a net capital spending cash flow of $1,870. We also know that net capital spending is:Net capital spending = Fixed assets bought –Fixed assets sold$1,870 = $2,160 – Fixed assets soldFixed assets sold = $2,160 – 1,870 = $290To calculate the cash flow from assets, we must first calculate the operating cash flow. The operating cash flow is calculated as follows (you can also prepare a traditional income statement): EBIT = Sales – Costs – DepreciationEBIT = $12,380 – 5,776 – 1,150EBIT = $5,454EBT = EBIT – InterestEBT = $5,454 – 314EBT = $5,140Taxes = EBT ? .40Taxes = $5,140 ? .40Taxes = $2,056OCF = EBIT + Depreciation – TaxesOCF = $5,454 + 1,150 – 2,056OCF = $4,548Cash flow from assets = OCF – Change in NWC – Net capital spending.Cash flow from assets = $4,548 – 45 – 1,870Cash flow from assets = $2,633/doc/a95a227710a6f524cdbf8525.ht ml new borrowing = LTD12 – LTD11Net new borrowing = $2,477 – 2,160Net new borrowing = $317Cash flow to creditors = Interest – Net new LTDCash flow to creditors = $314 – 317Cash flow to creditors = –$3Net new borrowing = $317 = Debt issued – Debt retiredDebt retired = $432 – 317 = $11522.Balance sheet as of Dec. 31, 2011Cash $4,109 Accounts payable $4,316 Accounts receivable 5,439 Notes payable 794 Inventory 9,670 Current liabilities $5,110 Current assets $19,218Long-term debt $13,460 Net fixed assets $34,455 Owners' equity 35,103 Total assets $53,673 Total liab. & equity $53,673 Balance sheet as of Dec. 31, 2012Cash $5,203 Accounts payable $4,185Accounts receivable 6,127 Notes payable 746Inventory 9,938 Current liabilities $4,931Current assets $21,268Long-term debt $16,050 Net fixed assets $35,277 Owners' equity 35,564Total assets Total liab. & equity2011 Income Statement 2012 Income Statement Sales $7,835.00Sales $8,409.00 COGS 2,696.00COGS 3,060.00 Other expenses 639.00Other expenses 534.00 Depreciation 1,125.00Depreciation 1,126.00 EBIT $3,375.00EBIT $3,689.00 Interest 525.00Interest 603.00 EBT $2,850.00EBT $3,086.00 Taxes 969.00Taxes 1,049.24 Net income $1,881.00Net income $2,036.76 Dividends $956.00Dividends $1,051.00 Additions to RE 925.00Additions to RE 985.76 23.OCF = EBIT + Depreciation –TaxesOCF = $3,689 + 1,126 – 1,049.24OCF = $3,765.76Change in NWC = NWC end– NWC beg = (CA – CL) end– (CA – CL) begChange in NWC = ($21,268 – 4,931) – ($19,218 – 5,110)Change in NWC = $2,229Net capital spending = NFA end– NFA beg+ DepreciationNet capital spending = $35,277 – 34,455 + 1,126Net capital spending = $1,948Cash flow from assets = OCF – Change in NWC – Net capital spendingCash flow from assets = $3,765.76 – 2,229 – 1,948Cash flow from assets = –$411.24Cash flow to creditors = Interest – Net new LTDNet new LTD = LTD end– LTD begCash flow to creditors = $603 – ($16,050 – 13,460)Cash flow to creditors = –$1,987Net new equity = Common stock end– Common stock beg Common stock + Retained earnings = Total owners’ equity Net new equity = (OE – RE) end– (OE – RE) begNet new equity = OE end– OE beg + RE beg– RE endRE end= RE beg+ Additions to RENet new equity = OE end–OE beg+ RE beg–(RE beg + Additions to RE)= OE end– OE beg– Additions to RENet new equity = $35,564 – 35,103 – 985.76 = –$524.76Cash flow to stockholders = Dividends – Net new equityCash flow to stockholders = $1,051– (–$524.76)Cash flow to stockholders = $1,575.76As a check, cash flow from assets is –$411.24Cash flow from assets = Cash flow from creditors + Cash flow to stockholdersCash flow from assets = –$1,987 + 1,575.76Cash flow from assets = –$411.24Challenge24.We will begin by calculating the operating cash flow. First, we need the EBIT, which can becalculated as:EBIT = Net income + Current taxes + Deferred taxes + InterestEBIT = $173 + 98 + 19 + 48EBIT = $338Now we can calculate the operating cash flow as:Operating cash flowEarnings before interest and taxes $338Depreciation 94Current taxes (98)Operating cash flow $334The cash flow from assets is found in the investing activities portion of the accounting statement of cash flows, so: Cash flow from assetsAcquisition of fixed assets $215Sale of fixed assets (23)Capital spending $192The net working capital cash flows are all found in the operations cash flow section of the accounting statement of cash flows. However, instead of calculating the net working capital cash flows as the change in net working capital, we must calculate each item individually. Doing so, we find:Net working capital cash flowCash $14Accounts receivable 18Inventories (22)Accounts payable (17)Accrued expenses 9Notes payable (6)Other (3)NWC cash flow ($7)Except for the interest expense and notes payable, the cash flow to creditors is found in the financing activities of the accounting statement of cash flows. The interest expense from the income statement is given, so:Cash flow to creditorsInterest $48Retirement of debt 162Debt service $210Proceeds from sale of long-term debt (116)Total $94And we can find the cash flow to stockholders in the financing section of the accounting statement of cash flows. The cash flow to stockholders was:Cash flow to stockholdersDividends $ 86Repurchase of stock 13Cash to stockholders $ 99Proceeds from new stock issue (44)Total $ 55/doc/a95a227710a6f524cdbf8525.ht ml capital spending = NFA end– NFA beg + Depreciation = (NFA end– NFA beg) + (Depreciation + AD beg) – AD beg = (NFA end– NFA beg)+ AD end– AD beg= (NFA end + AD end) – (NFA beg + AD beg) = FA end– FA beg26. a.The tax bubble causes average tax rates to catch up to marginal tax rates, thus eliminating thetax advantage of low marginal rates for high income corporations.b.Assuming a taxable income of $335,000, the taxes will be:Taxes = 0.15($50K) + 0.25($25K) + 0.34($25K) + 0.39($235K) = $113.9KAverage tax rate = $113.9K / $335K = 34%The marginal tax rate on the next dollar of income is 34 percent.For corporate taxable income levels of $335K to $10M,average tax rates are equal to marginal tax rates.Taxes = 0.34($10M) + 0.35($5M) + 0.38($3.333M) = $6,416,667Average tax rate = $6,416,667 / $18,333,334 = 35%The marginal tax rate on the next dollar of income is 35 percent. For corporate taxable income levels over $18,333,334, average tax rates are again equal to marginal tax rates.c.Taxes = 0.34($200K) = $68K = 0.15($50K) + 0.25($25K) +0.34($25K) + X($100K);X($100K) = $68K – 22.25K = $45.75KX = $45.75K / $100KX = 45.75%。

CorporateFinance10ESolutionManual课后习题解答Chap001Chapter 01 - Introduction to Corporate FinanceSolutions ManualCorporate FinanceRoss, Westerfield, and Jaffe10th editionXX/XX/2013Prepared by:Joe SmoliraBelmont UniversityCHAPTER 1INTRODUCTION TO CORPORATE FINANCEAnswers to Concept Questions1. In the corporate form of ownership, the shareholders are the owners of the firm. The shareholderselect the directors of the corporation, who in turn appoint the firm’s management. This separation of ownership from control in the corporate form of organization is what causes agency problems to exist. Management may act in its own or someone else’s best interests, rather than those of the shareholders. If such events occur, they may contradict the goal of maximizing the share price of the equity of the firm.2.Such organizations frequently pursue social or political missions, so many different goals areconceivable. One goal that is often cited is revenue minimization; i.e., provide whatever goods and services are offered at the lowest possible cost to society. A better approach might be to observe that even a not-for-profit business hasequity. Thus, one answer is that the appropriate goal is to maximize the value of the equity.3.Presumably, the current stock value reflects the risk, timing, and magnitude of all future cash flows,both short-term and long-term. If this is correct, then the statement is false.4.An argument can be made either way. At the one extreme, we could argue that in a market economy,all of these things are priced. There is thus an optimal level of, for example, ethical and/or illegal behavior, and the framework of stock valuation explicitly includes these. At the other extreme, we could argue that these are non-economic phenomena and are best handled through the political process.A classic (and highly relevant) thought question that illustrates this debate goes something like this: “A firm has estimated that the cost of improving the safety of one of its products is $30 million. However, the firm believes that improving the safety of the product will only save $20 million in product liability claims. What should the firm do?”5.The goal will be the same, but the best course of action toward that goal may be different because ofdiffering social, political, and economic institutions.6.The goal of management should be to maximize the share price for the current shareholders. Ifmanagement believes that it can improve the profitability of the firm so that the share price will exceed $35, then they should fight the offer from the outside company. If management believes that this bidder or other unidentified bidders will actually pay more than $35 per share to acquire the company, then they should still fight the offer. However, if the currentmanagement cannot increase the value of the firm beyond the bid price, and no other higher bids come in, then management is not acting in the interests of the shareholders by fighting the offer. Since current managers often lose their jobs when the corporation is acquired, poorly monitored managers have an incentive to fight corporate takeovers in situations such as this.7.We would expect agency problems to be less severe in other countries, primarily due to the relativelysmall percentage of individual ownership. Fewer individual owners should reduce the number of diverse opinions concerning corporate goals. The high percentage of institutional ownership might lead to a higher degree of agreement between owners and managers on decisions concerning risky projects. In addition, institutions may be better able to implement effective monitoring mechanisms on managers than can individual owners, based on the institutions’ deeper resources and experiences with their own management.8.The increase in institutional ownership of stock in the United States and the growing activism ofthese large shareholder groups may lead to a reduction in agency problems for U.S. corporations anda more efficient market for corporate control. However, this may not always be the case. If themanagers of the mutual fund or pension plan are not concerned with the interests of the investors, the agency problem could potentially remain the same, or even increase since there is the possibility of agency problems between the fund and its investors.9. How much is too much? Who is worth more, Larry Ellsion or Tiger Woods? The simplest answer isthat there is a market for executives just as there is for all types of labor. Executive compensation is the price that clears the market. The same is true for athletes and performers. Having said that, one aspect of executive compensation deserves comment.A primary reason executive compensation has grown so dramatically is that companies have increasingly moved to stock-based compensation.Such movement is obviously consistent with the attempt to better align stockholder and management interests. In recent years, stock prices have soared, so management has cleaned up. It is sometimes argued that much of this reward is simply due to rising stock prices in general, not managerial performance. Perhaps in the future, executive compensation will be designed to reward only differential performance, i.e., stock price increases in excess of general market increases.10. Maximizing the current share price is the same as maximizing the future share price at any futureperiod. The value of a share of stock depends on all of the future cash flows of company. Another way to look at this is that, barring large cash payments to shareholders, the expected price of the stock must be higher in the future than it is today. Who would buy a stock for $100 today when the share price in one year is expected to be $80?。

(一)名词解释(1)Presentment: A draft must be duly presented for payment if it is a sight bill or dully presented for acceptance first and then presented for payment at maturity if it is a time bill.(2) Acceptance: Acceptance of a draft is a signification by the drawee of his assent to the order given by the drawer.(3) Protest : A written statement under seal drawn up and signed by a notary public or other authorized person for the purpose of giving evidence that a bill of exchange has been presented by him for acceptance or for payment but dishonored(4) Endorsement: It is an act of negotiation.prerequisites for a valid endorsement:It should be normally effected on the back of a draft and signed by the endorserIt must be made for the whole amount of the draft. (5) Definition of International payments and settlements .International payments and settlements are financial activities conducted among different countries in which payments are effected or funds are transferred from one country to another in order to settle accounts , debts, claims, etc, emerged in the course of political economic or cultural contacts among then.(6) Definition of collection 托收的定義----is an arrangement where by the goods are shipped and a relevant bill of exchange is drawn by the seller on the buyer, and/or shipping documents are forwarded to the seller's bank with clear instructions for collection through one of its correspondent bank located in the domicile of the buyer.(7)D/P(documents against payments)The collecting bank may release the documents only against full and immediate payment ,insofar as national ,federal or local laws or regulations do not prevent it.(8)D/A(documents against acceptance)The presenting bank may release the documents to the buyer against the buyer’s acceptance of a draft, drawn payable 30-180days after sight ordue on a definite date.(9)议付二、简答(1) Evolution of International Payments and Settlementsa: From Cash Settlement to Non-Cash Settlementb: From Direct Payment Made between International Traders to Payment effected through a Financial Intermediary(從貨商之間支接支付到通過金融中介進行支付)c: From payments under Simple Price Terms to Payments under More Complex price Terms(從使用简单贸易术语支付到使用复杂贸易术语支付)(2) Four kinds of endorsementsa: Blank Endorsement An endorsement in blank is one that shows an endorser's signature only and specifies no endorseeb: Special endorsement. A special endorsement is one that specifies an endorsee to whom or whose order the draft is to be paid, in addition to the signature of on endorser. For example, "Pay Hhn Smths"c: Restrictive endorsement: An endorsement is restrictive when it prohibits further transfer of the draft.For example "Pay John Smiths only" d: Conditional endorsement: A conditional endorsement is a special endorsement adding some word there to that create a condition bound to be merit before the special endorsee in entitled to receive payment.The endorsement is liable only if the condition is fulfilled(3)票据的性质1、流通转让性(negotiability)2、无因性(non-causative nature)3、要式性(requisite in form)4、提示性(presentment)5、返还性(returnability)6、设权性(Right Establishing)7、文义性(Word Meaning)三、填空题Chapter 2(1)Before the sixth century B.C. , goods were exchanged between traders in different countries on a (barter) basis.(2)A (coin) ended the barter transactions.(3)The shipment of gold or silver across national boundaries was both (expensive) and risky.(4)Nostro account means (our) account.(5)(Vostro) account means your account.(6)To Bank of China, a RMB account held by Bank of England is called (vostro) account(7)If a British bank has an account in Paris with a French bank, it will refer to that account as (nostro) account(8)Control documents are lists of (specimen of Authorized signatured), (Telegraphic Test Keys), (Terms and Conditions)and (SWIFT Authentic Key).Chapter 4(1)International remittance happens when a client (payer) asks his bank to send a sum of moner to a <beneficiary> abroad by one of the transfer methods at his option.(2)A (payment orde r,mail advice, or debit advice)is an authenticated order in writing addressed by one bank to anther instructing the latter to pay a sum oertain in moner to a specified person or a beneficiary named thereon.(3)Telegraphic transfer is often used when (the remittance amount is large) and (the transfer of funds is subject to a time limit). The only means of authenticating a cable transfer is the (test key).(4)Under D/D, upon receipt of the draft, the beneficiary can either present is for payment at the counter of the drawee bank or (sell it to his own bank for crediting his account).(5)The whole procedure virtually is done by entries over banking accounts, where the buyer's bank (remitting bank) <debits> his account and <credits> the account of the correspondent bank.(6)In time of war, one can transfer funds out of the enemy country bymeans of the (demand draft) in virtue of its negotiability.(7)The remitting bank under D/D is generally reluctant to stop payment on a draft issued by itself for this would mean an (act of dishonor) on its part which will have an unfacorable effect on its credit-worthiness.(8)A large number of international remittances are carried out by telecommunications (swiftness, r eliability, safety) and (inexpensiveness) are major advantages of transactions among member banks by means of SWIFT messages.(9)If the paying bank maintains the remitting bank's account, the reimbursementmay be effected by (debiting remitting banks nostro account)(10)Any methods of transfer may be used to transfer the payment before (delivery of the goods) from the ......Chapter 5(1)If the collecting bank is not located near the importer, it would send the documents to a (presenting bank) in the importer's city(2)In a documentary collection the bank, acting as the exporter's agent, regulates the tming and sequence of the exchange of goods for value by holding the (title documents) until the importer either ((pays the draft) or (accepts the obligation to do so ).(3)The clean collection method lacks the protection of the documentary collection. It is generally used in countries where a draft is needed for (legal) purposesor because it is required by (t he exchange control authorities )(4)Under documents againse acceptance, after acceptance, after acceptance, the buyer gains possession of the goods before (the payment is made) and is able to dispose of the goods as he wishes.(5)Collections serve as a conpromise between (open account) and (advance payment) in settlement of international transactions concluled by the implrter and the exporter.(6) (Inward collection) is a banking business in which a bank acting as the collecting bank receives the draft with or without shipping documents attached as well as the instructions from a bank abroad and endeavors to collect the payment or obtain the acceptance from the importers.(7)Collection bill purchased inbolves great risk for (the remitting bank) for lack of bank's guarantee, so they are seldom willing wo do so .(8)The collecting bank authorizing the release of title documents on (trust receipt) must realize that this financing requires a great degree of confidence in the reputation ,honesty , and integrity of the customer acting as trustee.(9)Under(D/P at sight), the seller issres a draft. The collecting bank presents the draft to the buyers. When the buyer sees it he must pay the money at once, then he can get the shipping documents.(10) The remitting bank sends (documents, draft and collection order) to the collecting/presenting bank in the importer's country that notifies the importer.Chapter 7(1)When the beneficiary presents the documents to his bank,he must follow the "3C principle" in his documentation, the "3C" represent (completeness, correctness, c onsistenly).(2)The credit is legally quite independent of the (underlying transaction)(3)If a letter of credit is issued by air mail, it ought wo be authenticated by (authorized signatures) and when issued by cable/telex it is authenticated by (test key).(4)The documents of the credit must (comply with ) the terms and conditions of the letter of credit on the one hand and they must ( comply with ) with each other on the other hand(5)The currency in which the credit is to be issued should be indicated as shown in the ( Iso currency code )汇票的要义EXCHANGEfor USD5461.50 21st, August, 1995On 23rd October of this FIRST OF Exchange(Second of Exchange being unpaid)pay to Johnson & Smith Inc.or orderthe sum of FIVE THOUSAND FOUR HUNDRED AND SIXTY ONE US DOLLARS AND FIFTY CENTSDrawn against shipment of wool from Australia to New YorkTO Irving Trust Company, New York For George Thomas Inc., New YorkSignature Experiment One Financial Instruments1.Please answer, fill the blanks in or make choice of the following questions. Exchange for GBP1,250.00 Beijing, 1 April, 200X At 90 days after sight pay to the order of DEF Co.the sum of Pounds one thousand two hundred and fifty onlyTo XYZ Bank, For ABC Co., Beijing London Signature__________Refer to the above bill you may understand that a bill of exchange is an unconditional order in writing addressed by ___ ABC Co.___ to _ XYZ Bank ___ signed by __ ABC Co._______giving it requiring __ XYZ Bank ___ to whom it is addressed to pay_ At 90 days after sight _____ the sum of __ GBP1,250.00__ to __ the order of DEF Co.___.The holder of this bill is _ DEF Co.__who must firstly present it to _ XYZ Bank _for Acceptance_. At maturity, the holder must present it again for__Payment___.2. Fill in the following blank forms to draw four bills of exchange. Each bill includes the requisite items as follows:date:23 July., 200Xamount: USD35,461.50tenor: on 31 Oct., 2000 fixeddrawer: George Anderson Inc., New Yorkdrawee: Irving Trust Company, New Yorkpayee: Brown and Thomas Inc. or orderdrawn against shipment of cotton from Australia to St. LouisEXCHANGE for _ USD35,461.50___ _ New York _,_23 July.,200x_ on 31 Oct., 2000 fixed _____pay this first Bill of Exchange(Second of same tenor and date unpaid) to the order of ___ Brown and Thomas Inc. or order ___________________________________________________________________the sum of __Thirty-five Thousand Four Hundred and Sixty-one and 50/1000 US Dollars_______________________________________________________________________________________________________________________Drawn__ against shipment of cotton from Australia to St. Louis _______________________________________________________________________________________To__ Irving Trust Company _______ For__ George Anderson Inc.________ New York _____________ ____ New York _____3. Please answer, fill the blanks in or make choice of the following questions. Exchange for GBP5,000.00 London, 1 April, 200XAt 60 days after sight pay to the order of Bank of Australiathe sum of Pounds five thousand onlyTo The Importing Co. For The Exporting Co.Melbourne LondonSignature__________(1)refer to the above bill, the holder i.e. _ Bank of Australia has the right of __transferring__ it to _another______ person, or the right of presentment for ___acceptance___ and/or _____payment_______ to the Importing Co. Melbourne. If the latter refuses to pay, the holder has the right of ___recourse___against _the other parties thereto_.。