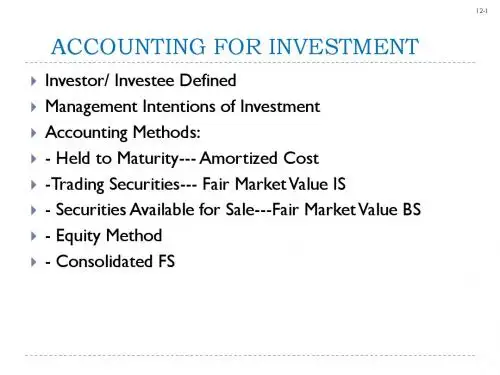

CH12-Investments

- 格式:ppt

- 大小:2.21 MB

- 文档页数:64

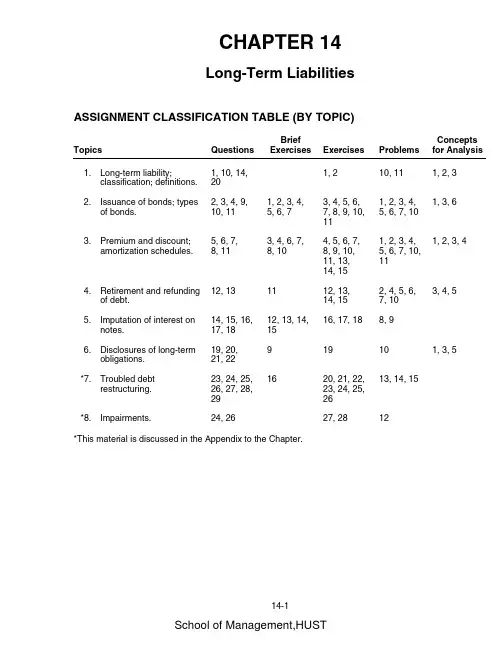

CHAPTER 14Long-Term Liabilities ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)Topics QuestionsBriefExercises Exercises ProblemsConceptsfor Analysis1.Long-term liability;classification; definitions.1, 10, 14,201, 210, 111, 2, 32.Issuance of bonds; typesof bonds.2, 3, 4, 9,10, 111, 2, 3, 4,5, 6, 73, 4, 5, 6,7, 8, 9, 10,111, 2, 3, 4,5, 6, 7, 101, 3, 63.Premium and discount;amortization schedules.5, 6, 7,8, 113, 4, 6, 7,8, 104, 5, 6, 7,8, 9, 10,11, 13,14, 151, 2, 3, 4,5, 6, 7, 10,111, 2, 3, 44.Retirement and refundingof debt.12, 131112, 13,14, 152, 4, 5, 6,7, 103, 4, 55.Imputation of interest onnotes.14, 15, 16,17, 1812, 13, 14,1516, 17, 188, 96.Disclosures of long-termobligations.19, 20,21, 22919101, 3, 5*7.Troubled debtrestructuring.23, 24, 25,26, 27, 28,291620, 21, 22,23, 24, 25,2613, 14, 15*8.Impairments.24, 2627, 2812 *This material is discussed in the Appendix to the Chapter.ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)Learning Objectives BriefExercises Exercises Problems1.Describe the formal proceduresassociated with issuing long-term debt.2.Identify various types of bond issues.1, 23.Describe the accounting valuationfor bonds at date of issuance.1, 2, 3, 4, 5,6, 7, 83, 4, 5, 6, 7, 8,9, 10, 11, 12,13, 14, 151, 2, 3, 4, 5,6, 7, 104.Apply the methods of bond discountand amortization.2, 3, 4, 5,6, 7, 8, 103, 4, 5, 6, 7, 8,9, 10, 12, 13,14, 151, 2, 3, 4, 5,6, 7, 10, 115.Describe the accounting for theextinguishment of debt.1112, 13, 14, 152, 4, 5, 6,7, 106.Explain the accounting for long-termnotes payable.12, 13, 14, 1516, 17, 188, 97.Explain the reporting of off-balance sheetfinancing arrangements.8.Indicate how to present and analyzelong-term debt.9194, 10*9.Describe the accounting for a loanimpairment.1627, 2812*10.Describe the accounting for debt restructuring.20, 21, 22,23, 24, 25,2613, 14, 15ASSIGNMENT CHARACTERISTICS TABLEItem Description Level ofDifficultyTime(minutes)E14-1Classification of liabilities.Simple15–20 E14-2Classification.Simple15–20 E14-3Entries for bond transactions.Simple15–20 E14-4Entries for bond transactions—straight-line.Simple15–20 E14-5Entries for bond transactions—effective-interest.Simple15–20 E14-6Amortization schedule—straight-line.Simple15–20 E14-7Amortization schedule—effective-interest.Simple15–20 E14-8Determine proper amounts in account balances.Moderate15–20 E14-9Entries and questions for bond transactions.Moderate20–30 E14-10Entries for bond transactions.Moderate15–20 E14-11Information related to various bond issues.Simple20–30 E14-12Entry for retirement of bond; bond issue costs.Simple15–20 E14-13Entries for retirement and issuance of bonds.Simple15–20 E14-14Entries for retirement and issuance of bonds.Simple12–16 E14-15Entries for retirement and issuance of bonds.Simple10–15 E14-16Entries for zero-interest-bearing debt.Simple15–20 E14-17Imputation of interest.Simple15–20 E14-18Imputation of interest with right.Moderate15–20 E14-19Long-term debt disclosure.Simple10–15 *E14-20Settlement of debt.Moderate15–20 *E14-21Term modification without gain—debtor’s entries.Moderate20–30 *E14-22Term modification without gain—creditor’s entries.Moderate25–30 *E14-23Term modification with gain—debtor’s entries.Moderate25–30 *E14-24Term modification with gain—creditor’s entries.Moderate20–30 *E14-25Debtor/creditor entries for settlement of troubled debt.Simple15–20 *E14-26Debtor/creditor entries for modification of troubled debt.Moderate20–25 *E14-27Impairments.Moderate15–25 *E14-28Impairments.Moderate15–25P14-1Analysis of amortization schedule and interest entries.Simple15–20 P14-2Issuance and retirement of bonds.Moderate25–30 P14-3Negative amortization.Moderate20–30 P14-4Issuance and retirement of bonds; income statementpresentation.Simple15–20 P14-5Comprehensive bond problem.Moderate50–65 P14-6Issuance of bonds between interest dates, straight-line,retirement.Moderate20–25P14-7Entries for life cycle of bonds.Moderate20–25 P14-8Entries for zero-interest-bearing note.Simple15–25 P14-9Entries for zero-interest-bearing note; payablein installments.Moderate20–25P14-10Comprehensive problem; issuance, classification,reporting.Moderate20–25P14-11Effective-interest method.Moderate40–50 *P14-12Loan impairment entries.Moderate30–40ASSIGNMENT CHARACTERISTICS TABLE (Continued)Item Description Level ofDifficultyTime(minutes)*P14-13Debtor/creditor entries for continuation of troubled debt.Moderate15–25 *P14-14Restructure of note under different circumstances.Moderate30–45 *P14-15Debtor/creditor entries for continuation of troubled debtwith new effective-interest.Complex40–50CA14-1Bond theory: balance sheet presentations, interest rate,premium.Moderate25–30CA14-2Various long-term liability conceptual issues.Moderate10–15 CA14-3Bond theory: price, presentation, and retirement.Moderate15–25 CA14-4Bond theory: amortization and gain or loss recognition.Simple20–25 CA14-5Off-balance-sheet financing.Moderate20–30 CA14-6Bond issue, ethics Moderate23–30ANSWERS TO QUESTIONS1.(a)Funds might be obtained through long-term debt from the issuance of bonds, and from thesigning of long-term notes and mortgages.(b)A bond indenture is a contractual agreement (signed by the issuer of bonds) between the bondissuer and the bondholders. The bond indenture contains covenants or restrictions for the protection of the bondholders.(c)A mortgage is a document which describes the security for a loan, indicates the conditionsunder which the mortgage becomes effective (that is, conditions of default), and describes the rights of the mortgagee under default relative to the security. The mortgage accompaniesa formal promissory note and becomes effective only upon default of the note.2.If the entire bond matures on a single date, the bonds are referred to as term bonds. Mortgagebonds are secured by real estate. Collateral trust bonds are secured by the securities of other corporations. Debenture bonds are unsecured. The interest payments for income bonds depend on the existence of operating income in the issuing company. Callable bonds may be called and retired by the issuer prior to maturity. Registered bonds are issued in the name of the owner and require surrender of the certificate and issuance of a new certificate to complete the sale. A bearer or coupon bond is not recorded in the name of the owner and may be transferred from one investor to another by mere delivery. Convertible bonds can be converted into other securities of the issuing corporation for a specified time after issuance. Commodity-backed bonds (also called asset-linked bonds) are redeemable in measures of a commodity. Deep-discount bonds (also called zero-interest bonds) are sold at a discount which provides the buyer’s total interest payoff at maturity.3.(a)Yield rate—the rate of interest actually earned by the bondholders; it is synonymous with theeffective and market rates.(b)Nominal rate—the rate set by the party issuing the bonds and expressed as a percentage ofthe par value; it is synonymous with the stated rate.(c)Stated rate—synonymous with nominal rate.(d)Market rate—synonymous with yield rate and effective rate.(e)Effective rate—synonymous with market rate and yield rate.4.(a)Maturity value—the face value of the bonds; the amount which is payable upon maturity.(b)Face value—synonymous with par value and maturity value.(c)Market value—the amount realizable upon sale.(d)Par value—synonymous with maturity and face value.5. A discount on bonds payable results when investors demand a rate of interest higher than the ratestated on the bonds. The investors are not satisfied with the nominal interest rate because they can earn a greater rate on alternative investments of equal risk. They refuse to pay par for the bonds and cannot change the nominal rate. However, by lowering the amount paid for the bonds, investors can alter the effective rate of interest.A premium on bonds payable results from the opposite conditions. That is, when investors aresatisfied with a rate of interest lower than the rate stated on the bonds, they are willing to pay more than the face value of the bonds in order to acquire them, thus reducing their effective rate of interest below the stated rate.6.Discount (premium) on bonds payable should be reported in the balance sheet as a directdeduction from (addition to) the face amount of the bond. Both are liability valuation accounts.Questions Chapter 14 (Continued)7.Bond discount and bond premium may be amortized on a straight-line basis or on an effective-interest basis. The profession recommends the effective-interest method but permits the straight-line method when the results obtained are not materially different from the effective-interest method. The straight-line method results in an even or average allocation of the total interest over the life of the notes or bonds. The effective-interest method results in an increasing or decreasing amount of interest each period. This is because interest is based on the carrying amount of the bond issuance at the beginning of each period. The straight-line method results in a constant dollar amount of interest and an increasing or decreasing rate of interest over the life of the bonds.The effective-interest method results in an increasing or decreasing dollar amount of interest anda constant rate of interest over the life of the bonds.8.The annual interest expense will decrease each period throughout the life of the bonds. Under theeffective-interest method the interest expense each period is equal to the effective or yield interest rate times the book value of the bonds at the beginning of each interest period. When bonds are sold at a premium, their book value declines to face value over their life; therefore, the interest expense declines also.9.Bond issuance costs according to APB Opinion No. 21 should be debited to a deferred chargeaccount for Unamortized Bond Issue Costs and amortized over the life of the issue, separately from but in a manner similar to that used for discount on bonds. The FASB in SFAC No. 3 takes the position that debt issue costs can be treated as either an expense of the period in which the bonds are issued or a reduction of the related debt liability.10.Treasury bonds should be shown on the balance sheet as a deduction from the bonds payable.11.The call feature of a bond issue grants the issuer the privilege of purchasing, after a certain date ata stated price, outstanding bonds for the purpose of reducing indebtedness or taking advantage oflower interest rates. The call feature does not affect the amortization of bond discount or premium;because early redemption is not a certainty, life to maturity date should be used for amortization purposes.12.It is sometimes desirable to reduce bond indebtedness in order to take advantage of lower pre-vailing interest rates. Also the company may not want to make a very large cash outlay all at once when the bonds mature.Bond indebtedness may be reduced by either issuing bonds callable after a certain date and then calling some or all of them, or by purchasing bonds on the open market and then retiring them.When a portion of bonds outstanding is going to be retired, it is necessary for the accountant to make sure any corresponding discount or premium is properly amortized.13.Gains or losses from extinguishment of debt should be aggregated and reported in income.For extinguishment of debt transactions disclosure is required of the following items:1. A description of the transactions, including the sources of any funds used to extinguish debt ifit is practicable to identify the sources.2.The income tax effect in the period of extinguishment.3.The per share amount of the aggregate gain or loss net of related tax effect.14.The entire arrangement must be evaluated and an appropriate interest rate imputed. This is doneby (1) determining the fair value of the property, goods, or services exchanged or (2) determining the market value of the note, whichever is more clearly determinable.Questions Chapter 14 (Continued)15.If a note is issued for cash, the present value is assumed to be the cash proceeds. If a note isissued for noncash consideration, the present value of the note should be measured by the fair value of the property, goods, or services or by an amount that reasonably approximates the market value of the note (whichever is more clearly determinable).16.When a debt instrument is exchanged in a bargained transaction entered into at arm’s-length, thestated interest rate is presumed to be fair unless: (1) no interest rate is stated, or (2) the stated interest rate is unreasonable, or (3) the stated face amount of the debt instrument is materially different from the current sales price for the same or similar items or from the current market value of the debt instrument.17.Imputed interest is the interest factor (a rate or amount) assumed or assigned which is differentfrom the stated interest factor. It is necessary to impute an interest rate when the stated interest rate is presumed to be unfair. The imputed interest rate is used to establish the present value of the debt instrument by discounting, at that imputed rate, all future payments on the debt instrument. In imputing interest, the objective is to approximate the rate which would have resulted if an independent borrower and an independent lender had negotiated a similar transaction under comparable terms and conditions with the option to pay the cash price upon purchase or to givea note for the amount of the purchase which bears the prevailing rate of interest to maturity. In orderto accomplish that objective, consideration must be given to (1) the credit standing of the issuer,(2) restrictive covenants, (3) collateral, (4) payment and other items pertaining to the debt, (5) theexisting prime interest rate, and (6) the prevailing rates for similar instruments of issuers with similar credit ratings.18. A fixed-rate mortgage is a note that requires payment of interest by the mortgagor at a rate thatdoes not change during the life of the note. A variable-rate mortgage is a note that features an interest rate that fluctuates with the market rate; the variable rate generally is adjusted periodically as specified in the terms of the note and is usually limited in the amount of each change in the rate up or down and in the total change that can be made in the rate.19.FASB Statement No. 47 requires disclosure at the balance sheet date of future payments forsinking fund requirements and the maturity amounts of long-term debt during each of the next five years.20.Off-balance-sheet-financing is an attempt to borrow monies in such a way that the obligations arenot recorded. Reasons for off-balance sheet financing are:1.Many believe removing debt enhances the quality of the balance sheet and permits credit to beobtained more readily and at less cost.2.Loan covenants are less likely to be violated.3.The asset side of the balance sheet is understated because fair value is not used for manyassets. As a result, not reporting certain debt transactions offsets the nonrecognition of fair values on certain assets.21.Forms of off-balance-sheet financing include (1) investments in non-consolidated subsidiaries forwhich the parent is liable for the subsidiary debt; (2) use of special purpose entities (SPEs), which are used to borrow money for special projects (resulting in take-or-pay contracts; (3) operating leases, which when structured carefully give the company the benefits of ownership without reporting the liability for the lease payments.22.In take-or-pay contracts, the outside party agrees to make specified minimum payments even if itdoes not take possession of the contracted goods or services. In through-put contracts, the outside party agrees to pay specified amounts in return for processing or transportation services rendered by the debtor, which is usually the owner of a manufacturing or transportation facility.Questions Chapter 14 (Continued)*23.Two different types of situations result with troubled debt: (1) Impairments, and (2) Restructurings.Restructurings can be further classified into:a.Settlements.b.Modification of terms.When a debtor company runs into financial difficulty, creditors may recognize an impairment ona loan extended to that company. Subsequently, the creditor may modify the terms of the loan, orsettles it on terms unfavorable to the creditor. In unusual cases, the creditor forces the debtor into bankruptcy in order to ensure the highest possible collection on the loan.*24.A loan is considered impaired when it is probable that the creditor will be unable to collect all amounts due (both principal and interest) according to the contractual terms of the loan. If a loan is considered impaired, the loss due to impairment should be measured as the difference between the investment in the loan and the expected future cash flows discounted at the loan’s historical effective-interest rate. The loss is recorded on the books of the creditor. The debtor would not be aware of the entry made by the creditor and would not make an entry until settlement or ifa modification of items resulted.*25.A transfer of noncash assets (real estate, receivables, or other assets) or the issuance of the debtor’s stock can be used to settle a debt obligation in a troubled debt restructuring. In these situations, the noncash assets or equity interest given should be accounted for at their fair market value. The debtor is required to determine the excess of the carrying amount of the payable over the fair value of the assets or equity transferred (gain). Likewise, the creditor is required to determine the excess of the receivable over the fair value of those same assets or equity interests transferred (loss). The debtor recognizes a gain equal to the amount of the excess and the creditor normally would charge the excess (loss) against Allowance for Doubtful Accounts. In addition, the debtor recognizes a gain or loss on disposition of assets to the extent that the fair value of those assets differs from their carrying amount (book value).*26.(a)The creditor will grant concessions in a troubled debt situation because it appears to be the more likely way to maximize recovery of the investment.(b)The creditor might grant any one or a combination of the following concessions:1.Reduce the face amount of the debt.2.Accept noncash assets or equity interests in lieu of cash in settlement.3.Reduce the stated interest rate.4.Extend the maturity date of the face amount of the debt.5.Reduce or defer any accrued interest.(c)A loan is impaired when there is a reduction in the likelihood of collecting the interest andprincipal payments as originally scheduled. An impairment should be recorded by a creditor when it is “probable” that the payment will not be collected as scheduled. Debtors do not record impairments.*27.When a loan is restructured, the creditor should calculate the loss due to restructuring by sub-tracting the present value of the restructured cash flows from the carrying value of the loan.Interest revenue is calculated at the original effective rate applied towards the new carrying value.The debtor will record a gain only if the undiscounted restructured cash flows are less than the carrying value of the loan. If a gain is recognized, subsequent payments will be all principal. There is no interest component. If the undiscounted cash flows exceed the carrying amount, no gain is recognized, and a new imputed interest rate must be calculated in order to recognize interest expense in subsequent periods.Questions Chapter 14 (Continued)*28.“Accounting symmetry” between the entries recorded by the debtor and the creditor in a troubled debt restructuring means that there is a correspondence or agreement between the entries recorded by each party. Impairments are nonsymmetrical because, while the creditor recordsa loss, the debtor makes no entry at all. Troubled debt restructurings are nonsymmetrical becausecreditors calculate their loss using the discounted present value of future cash flows, while debtors calculate their gain using the undiscounted cash flows. The FASB chose to accept this nonsymmetric treatment rather than address debtor accounting because it feared that expansion of the scope of FASB Statement No. 114 would further delay its issuance.*29.A transaction would be recorded as a troubled debt restructuring by only the debtor if the amount for which the liability is settled is less than its carrying amount on the debtor’s books, but equal to or greater than the carrying amount on the creditor’s books. In addition to the situation created by the use of discounted versus undiscounted cash flows by creditors and debtors, this situation can occur when a debtor or creditor has been substituted for one of the parties to the original transaction.SOLUTIONS TO BRIEF EXERCISESBRIEF EXERCISE 14-1Present value of the principal$300,000 X .37689$113,067Present value of the interest payments$13,500 X 12.46221 168,240 Issue price$281,307BRIEF EXERCISE 14-2(a)Cash...................................................................................200,000Bonds Payable.....................................................200,000 (b)Interest Expense............................................................10,000Cash ($200,000 X 10% X 6/12).........................10,000 (c)Interest Expense............................................................10,000Interest Payable...................................................10,000 BRIEF EXERCISE 14-3(a)Cash ($200,000 X 98%).................................................196,000Discount on Bonds Payable......................................4,000Bonds Payable.....................................................200,000 (b)Interest Expense............................................................10,000Cash ($200,000 X 10% X 6/12).........................10,000 (c)Interest Expense............................................................10,000Interest Payable...................................................10,000 Interest Expense (800)Discount on Bonds Payable (800)($4,000 X 1/5 = $800)BRIEF EXERCISE 14-4(a)Cash ($200,000 X 103%)...............................................206,000Bonds Payable.....................................................200,000Premium on Bonds Payable............................6,000 (b)Interest Expense.............................................................10,000Cash ($200,000 X 10% X 6/12).........................10,000 (c)Interest Expense.............................................................10,000Interest Payable...................................................10,000 Premium on Bonds Payable.......................................1,200Interest Expense ($6,000 X 1/5 = $1,200).....1,200 BRIEF EXERCISE 14-5(a)Cash....................................................................................510,000Bonds Payable.....................................................500,000Interest Expense..................................................10,000($500,000 X 6% X 4/12 = $10,000)(b)Interest Expense.............................................................15,000Cash ($500,000 X 6% X 6/12 = $15,000)........15,000 (c)Interest Expense.............................................................15,000Interest Payable...................................................15,000 BRIEF EXERCISE 14-6(a)Cash....................................................................................372,816Discount on Bonds Payable.......................................27,184Bonds Payable.....................................................400,000 (b)Interest Expense.............................................................14,913Cash.........................................................................14,000Discount on Bonds Payable (913)($372,816 X 8% X 6/12 = $14,913)($400,000 X 7% X 6/12 = $14,000)BRIEF EXERCISE 14-6 (Continued)(c)Interest Expense............................................................14,949Interest Payable...................................................14,000Discount on Bonds Payable (949)($373,729 X 8% X 6/12 = $14,949)BRIEF EXERCISE 14-7(a)Cash...................................................................................429,757Bonds Payable.....................................................400,000Premium on Bonds Payable............................29,757(b)Interest Expense............................................................12,893Premium on Bonds Payable......................................1,107Cash........................................................................14,000($429,757 X 6% X 6/12 = $12,893)($400,000 X 7% X 6/12 = $14,000)(c)Interest Expense............................................................12,860Premium on Bonds Payable......................................1,140Interest Payable...................................................14,000($428,650 X 6% X 6/12 = $12,860)BRIEF EXERCISE 14-8Interest Expense........................................................................4,298Premium on Bonds Payable (369)Interest Payable...............................................................4,667 ($429,757 X 6% X 2/12 = $4,298)($400,000 X 7% X 2/12 = $4,667)BRIEF EXERCISE 14-9Current liabilities$80,000 Bond Interest PayableLong-term liabilities$2,000,000 Bonds Payable, due January 1, 2016 98,000 Less: Discount on Bonds Payable$1,902,000 BRIEF EXERCISE 14-10Bond Issue Expense..................................................................18,000 Unamortized Bond Issue Costs..................................18,000 ($180,000 X 1/10)BRIEF EXERCISE 14-11Bonds Payable............................................................................600,000Premium on Bonds Payable...................................................15,000 Unamortized Bond Issue Costs..................................5,250 Cash.....................................................................................594,000 Gain on Redemption of Bonds....................................15,750 BRIEF EXERCISE 14-12(a)Cash....................................................................................100,000Notes Payable.......................................................100,000 (b)Interest Expense.............................................................11,000Cash ($100,000 X 11% = $11,000)...................11,000 BRIEF EXERCISE 14-13(a)Cash....................................................................................31,776Discount on Notes Payable........................................18,224Notes Payable.......................................................50,000BRIEF EXERCISE 14-13 (Continued)(b)Interest Expense............................................................3,813Discount on Notes Payable.............................3,813($31,776 X 12%)BRIEF EXERCISE 14-14(a)Computer..........................................................................39,369Discount on Notes Payable........................................10,631Notes Payable......................................................50,000 (b)Interest Expense............................................................4,724Cash........................................................................2,500Discount on Notes Payable.............................2,224($39,369 X 12% = $4,724)($50,000 X 5% = $2,500)BRIEF EXERCISE 14-15 Cash...............................................................................................50,000Discount on Notes Payable....................................................18,224 Notes Payable...................................................................50,000 Unearned Revenue.........................................................18,224 [$50,000 – ($50,000 X .63552) = $18,224]*BRIEF EXERCISE 14-16Toni Braxton (Debtor): No EntryNational American Bank (Creditor):Bad Debt Expense..........................................................225,000Allowance for Doubtful Accounts....................225,000。

Active internal arc protection for low and medium voltage switchgear—UFES™ Ultra-FastEarthing Switch• Protects operators and investments • Minimizes downtime and damage on equipment• Reduces costs related to arc fault impactsCB2T1CTUFES PSEUFES protection zoneHSO 2HSO 1CB1PSE TripUFES QRU100REA101CBCBCBLight sensorOptolink (Trip)2B RO CH U R E TITLE B R O CH U R E SU BTITL EThe active arc fault protection device for switchgearThe occurance of an arc fault, the most serious fault within a switchgear system, is mostly associated with extremely high thermal and mechanical stresses in the area concerned. An active arc fault protection system based on the know-how gained from decades of experience with the ABB vacuum interrupter and I S -limiter technology now effectively helps to avoid these negative effects if a fault should occur.The Ultra-Fast Earthing Switch of type UFES is a combination of devices consisting of an elec-tronic device and the corresponding primary switching elements which initiate a 3-phase short-circuit to earth in the event of a fault. The extremely short switching time of the primary switching element, less than 1.5 ms, in conjunc-tion with the rapid and reliable detection of the fault, ensures that an arc fault is extinguished almost immediately after it arises. With a total extinguishing time of less than 4 ms after detec-tion, an active protection concept with the Ultra- Fast Earthing Switch enables switchgear installa-tions to achieve the highest possible level of pro-tection for persons and equipment.—01 UFES applica-tion (example)—02 Energy release of arc faults and the thermal effects—UFESS 3 – Speed, Safety, SavingsAvoidance of the severe effects of an arc fault, such as:• Extreme pressure• Temperature rise up to 20,000 °C• Burning / vaporization of metal and insulating material• Release of particles and hot gases • Intensive light / high acoustic stress—01—02Greatly increased operator safety ... by effective prevention of hazardous situationsMinimized damage of electrical equipment and direct environment ... due to ultra-fast arc fault mitigation Drastic reduction in downtimes & repair costs… to avoid significant economic lossesApplication of active protection concepts for pressure sensitive environment... e.g. where gas ducts are not applicableEpoxy resin insulation Fixed contactCeramicinsulatorMovingcontact pinRupture jointCylinderMovingcontact systemMicro gasgenerator Short-circuit current IDC componentArcing time with UFESFinal clearing of fault current byupstream circuit-breaker - 80 ms + Zeit xReaching time for tripping criteriatOverpressure in barPressure curve with UFES (4 ms)Reaching time for tripping criteriaPressure curvewithout UFESt1.61.21.0Piston* 40.5 kV on requestElectrical maximum characterstics for each voltage category(Different types available)—UFES primary switching element type U1A RTI CL E O R CH A P TER TITL E3—03 The Ultra-FastEarthing Switch elimi-nates the arc fault inless than 4 ms afterdetection (grey area)—04 Example pressurecurves, with and withoutUFES, in a compartmentof an air-insulatedmedium voltageswitchgear systemwith an internal arcfault current of 130 kA(peak) / 50 kA (rms)—05 Primary switchingelement for one phase—UFESUltra-Fast Earthing Switch—05—04—03UFESApplicationsSelection of retrofit solutionsParticularly for older, non-IAC qualified switch-gear systems, the Ultra-Fast Earthing Switch allows the highest degree of protection for equipment and operator safety to be achieved. A variety of solutions are available for retrofitting of existing switchgear systems.ABB Service Box (up to 24 kV)Universally usable ABB UFES Service Box for retrofitting of air-insulated switchgear • Non-proprietary application• Maximum installation flexibility to suit the space availableABB withdrawable solutionsThe UFES primary switching elements, installed in ABB withdrawable assembly or truck design, provides a simple opportunity to upgrade exist-ing switchgear systems with active arc fault protection• The contact with the busbars is established via the isolating contacts of the withdrawable assembly• The optimum Plug & Play solution when vacant panels are available• Similar solutions are also available for other switchgear types with trucks *New ABB switchgearAlso for new ABB switchgear, the integration of UFES is a useful supplement in order to protect this investment against the impacts of an internal arc, and in addition, to increase the operator safety to a maximum. For switchgear of type UniGear ZS1 for example, the following technical solutions are available:• UFES installation in a top box with direct connection to the busbar• UFES installation in the cable connection compartment• Separate panel with UFES draw-out unit UFES componentsThe Ultra-Fast Earthing Switch can also beprovided as a loose OEM component. There are different types of UFES kits available.* on request—07—06—06 ABB Service Box, top mounted —07 ABB with-drawable solutionABB arc protection system REA• Optical detection via line or lens sensors • Overcurrent detection • Selective protection• Circuit-breaker failure protectionUFES electronics type QRU1• Alternative electronic detection and tripping unit• 3 current inputs• 9 optical inputs for light detection by lens sensors• Complete solution for simple protection zones • For large protection zones expandable up to 159 lens sensors with ABB arc guard type TVOC-2• Self monitoring• Testing mode for functional check • DIP switch configuration • Fast fault localizationUFESActive protection for switchgear—01 —03—02—04—01 UFES electronics type QRU100—02 UFES primary switchingelement type U1—03 REA system —04 UFES electronics type QRU1UFES electronics type QRU100• Standard electronic tripping unit for the combi-nation with ABB arc protection system REA • 2 Optolink inputs for connection of the REA101 relay• 2 High-speed inputs (HSI)• Self monitoring• Optolink supervision• Testing mode for functional check • DIP switch configuration• Ideal for extension of existing ABB arc protec-tion systems• Alternative: Fault detection by non-ABB system (Compatibility verification required!)UFES primary switching element type U1• Ultra-fast operating mechanism with micro gas generator• Vacuum interrupter • Compact design• Versatile in installation • Long service lifeUFES certified by:D E A B B 2459 18 g b (09.18-0000-A M C )© Copyright 2018 ABB. All rights reserved.Specifications subject to change without notice.Additional informationWe reserve the right to make technical changes or modify the contents of this document without prior notice. With regard to purchase orders, the agreed particulars shall prevail. ABB AG does not accept any responsibility whatso-ever for potential errors or possible lack of information in this document.We reserve all rights in this document and in the subject matter and illustra-tions contained therein. Any reproduc-tion, disclosure to third parties orutilization of its contents – in whole or in parts – is forbidden without prior written consent of ABB AG.—ABB AGOberhausener Strasse 3340472 Ratingen GermanyPhone: +49 2102 12-0Fax: +49 2102 12-17 /mediumvoltage。

CHAPTER 25 CAPITAL BUDGETING AND MANAGERIAL DECISIONSSP refers to the Serial ProblemES refers to Excel SimulationsAdditional Information on Related Assignment MaterialConnectAvailable on the instructor’s course-specific website) repeats all numerical Quick Studies, all Exercises and Problems Set A. Connect also provides algorithmic versions for Quick Study, Exercises and Problems. It allows instructors to monitor, promote, and assess student learning. It can be used in practice, homework, or exam mode.Connect InsightThe first and only analytics tool of its kind, Connect Insight is a series of visual data displays that are each framed by an intuitive question and provide at-a-glance information regarding how an instructor’s class is performing. Connect Insight is available through Connect titles.The Serial Problem (SP) for Success Systems continues in this chapter.General LedgerAssignable within Connect, General Ledger (GL) problems offer students the ability to see how transactions post from the general journal all the way through the financial statements. Critical thinking and analysis components are added to each GL problem to ensure understanding of the entire process. GL problems are auto-graded and provide instant feedback to the student.Excel SimulationsAssignable within Connect, Excel Simulations allow students to practice their Excel skills—such as basic formulas and formatting—within the context of accounting. These questions feature animated, narrated Help and Show Me tutorials (when enabled). Excel Simulations are auto-graded and provide instant feedback to the student. Synopsis of Chapter RevisionNEW opener—Simply Gum and entrepreneurial assignment.Added exhibit and discussion of capital budgeting process.Added exhibit and discussion of cash inflows and outflows in capital budgeting.Added lists of strengths and weaknesses, with revised discussion, of payback period.Added list of weaknesses of accounting rate of return method.New art showing timeline of NPV calculation.Added discussion of outsourcing in make or buy decisions.Added discussion of capital rationing.Added financial calculator and Excel steps for many calculations.Revised discussion of relevant costs and benefits.Revised Sustainability section on capital budgeting for solar investments and Simply Gum example.Added two Quick Studies on capital budgeting for solar investments.Added Appendix and end of chapter assignments on product pricing.Chapter OutlineNotes Section 1 Capital BudgetingI.Capital budgeting is a process of analyzing alternative long-terminvestments and deciding which assets to acquired or sellA.An objective of capital budgeting decisions is to earn a satisfactoryrate of return.B.The process begins with department or plant managers submittingproposals for new investment in property, plant, and equipment. Acapital budget committee evaluates the proposals and recommendsfor approval or rejection. Finally, board of directors approvescapital expenditures for the year.C.Such decisions require careful analysis because they are difficultand risky.1.Difficult because of need to make predictions of events thatwill occur well into the future.2.Risky because: Outcome is uncertain, large amounts of moneyare involved, a long-term commitment is required, and thedecision may be difficult or impossible to reverse.II.Methods Not Using Time Value of Money Investments areexpected to produce net cash outflows; Net Cash flows equal cashinflows minus cash outflows. Simple analysis methods do not considerthe time value of money.A.Payback Period1.Payback period is the expected amount of time to recover theinitial investment amount.2.Evaluating Payback Period: managers prefer investments withshorter payback periods.a.Shorter payback period reduces risk of an unprofitableinvestment over the long run.pany’s risk due to potentially inaccurate long-termpredictions of future cash flows is reduced.3.To compute payback period, exclude all non-cash revenue andexpenses from computation. Depreciation is a non-cashexpense, so it is not included.a.When annual cash flows are even in amount:Payback Period = Cost of InvestmentAnnual net cash flowsb.When annual cash flows are unequal, payback period iscomputed using the cumulative total of net cash flows(starting with the negative cash flow resulting from theinitial investment); when cumulative net cash flowchanges from positive to negative, the investment is fullyrecovered. (see Exhibit 25.5)4.Payback period has two strengths: it uses cash flows, notincome and it is easy to use.Chapter OutlineNotes5.Payback period has three major weaknesses: it does not reflectdifferences in the timing of net cash flows within the paybackperiod; it ignores all cash flows occurring after the point offully recovered costs; and it ignores the time value of money.B.Accounting Rate of Return1.The percentage accounting return on annual averageinvestment.2.Called “accounting” return because it is based on net incomeinstead of on cash flows.puted as:after tax net incomeaverage annual investment4.Accrual basis after-tax net income is used.pute the average investment:a.If straight-line deprecation is used then:Annual average = (Beg. Book Value + End. Book value)Investment 2where ending book value = salvage value if there is oneb.If the depreciation method is other than straight linemethod then the general formula is:Annual = sum of individual year’s average book valueAve. Invest number of years of the planned investment6.Accounting Rate of Return = After-tax net incomeAverage investment amount7.Risk of an investment should be considered.a.Investment’s return is satisfactory only when related toreturns from other investments with similar lives and risk.b.Capital investment with least risk and highest return forthe longest time is often identified as best; analysis can bechallenging because different investments often yielddifferent rankings depending on measure used.8.Evaluating Accounting Rate of Return – should never be theonly consideration in capital budgeting decisions. Three majorweaknesses:a.It ignores the time value of moneyb.It focuses on income, not cash flows.c.If income varies from year to year, the project mightappear desirable in some years and not in others.Chapter OutlineNotes III.Methods Using Time Value of Money Net present value andinternal rate of return methods consider time value of money. Present Value (see also Appendix B near end of textbook) Present Value (NPV) analysis applies the time value ofmoney to cash inflows and cash outflows so management canevaluate a project’s benefits and cost at one point in time.2.NPV is computed by discounting the future net cash flowsfrom the investment at the required rate of return, and thensubtract the initial amount invested.a.The required rate of return also called the hurdle rate orthe cost of capital that the company must pay to its long-term creditors and shareholders.b.Each annual net cash flow is multiplied by the relatedpresent value of 1 factor or discount factor. (Obtain fromTable B.1 in Appendix B.)i.Discount factors assume that net cash flows arereceived at the end of each year.ii.R ate of return required by the company and number ofyears until cash flow is received are used to determinediscount factors.c.Initial amount invested includes all costs incurred to getasset in proper location and ready to use. Present Value Decision Rule Present Value = PV of cash flows – Amount Investedb.If the NPV is greater than or equal to $0, then asset isexpected to recover its cost and provide a return at least ashigh as that required; invest.c.If NPV is negative, do not invest4.NPV analysis can be used when comparing several investmentopportunities; if investment opportunities have same cost andsame risk, the one with highest NPV is preferred.5.When annual net cash flows are equal in amount, NPVcalculation can be simplified.a.Individual annual present value of $1 factors can besummed, and the total multiplied by annual net cash flowto get total present value of net cash flows.b.To simplify the computation, the present value of anannuity of $1 table may be usedc.Calculator with compound interest function or aspreadsheet program can also be used.6.NPV analysis can also be applied when net cash flows areunequal. (Use procedures and decision-rules above.)7.If salvage value is expected at end of useful life, treat as anadditional net cash flow received at end the of asset’s life.Chapter OutlineNotes8.Accelerated depreciation methods do not change basics ofNPV analysis, but can change results; using accelerateddepreciation for tax reporting affects net present value ofasset’s cash flowsa.Accelerated depreciation produces larger depreciationdeductions in early years of asset’s life and smaller ones inlater years; large net cash inflows are produced in earlyyears and smaller ones in later years.b.Early cash flows are more valuable than later ones; assuch, being able to use accelerated depreciation for taxreporting makes investment more desirable.paring positive NPV projects is of limited value forcomparison purposes if initial investment differs substantiallyacross projects.10.W hen a company can’t fund all positive net present valueprojects , they can be compared using the profitability index:a.Profitability Index = Net present value of cash flowsCost of investmentb. A higher profitability index makes the project moredesirable.11.NPVs should be computed using different discount rates; thegreater the risk, the higher the discount rate.12.Capital rationing – hard rationing is imposed by externalforces and soft rationing is internally imposed bymanagement. Profitability index can be used to select the bestof several competing projects.13.Inflation – net cash flows can be adjusted for inflation byusing future value computations.B.Internal Rate of Return1.IRR is a rate used to evaluate acceptability of an investment; itequals the rate that yields a NPV of zero for an investment.2.T otal present value of project’s net cash flows is computedusing the IRR as the discount rate, and subtracting the initialinvestment from total present value to get a zero NPV.3.Two step process in computing IRR (equal cash flows)a.Step 1: Compute the present value factor for the projectby dividing the amount invested by annual net cash flows.b.Step 2: Find discount rate (IRR) yielding the PV factor.i. A present value of an annuity table (Appendix B) canbe used to determine the discount rate that relates tothis present value factor given the life of the project.ii.If the present value factor in the table does not exactlyequal the one computed, Excel and many calculatorsuse built-in functions can be used.Chapter Outline4.When cash flows are unequal, trial and error must be used;select any reasonable discount rate and compute the NPV.a.If amount is positive, recompute NPV using higherNotes discount rate; if amount is negative, recompute NPV usinglower discount rate.b.Continue steps until two consecutive computations resultin NPVs that have different signs (positive and negative);IRR lies between these two discount rates; value can beestimated.c.Spreadsheet software and calculators can also be used tocompute the IRR. (See Appendix 25A)pare IRR with hurdle rate (or minimum acceptable rate ofreturn); if IRR exceeds hurdle rate, invest.6.If evaluating multiple projects, rank by extent to which IRRexceeds hurdle rate.7.IRR is not subject to limitations of NPV when comparingprojects with different amounts invested; IRR is expressed aspercent rather than an absolute dollar value using NPV.parison of Capital Budgeting Methods (see Exhibit 25.12)1.Payback period and accounting rate of return do not considertime value of money; NPV and IRR do.2.Payback period method is simple; sometimes used whenlimited cash to invest and a number of projects to choosefrom. Gives manager an estimate of how soon the initialinvestment can be recovered.3.Accounting rate of return is a percent computed using accrualincome instead of cash flows, and is an average rate for theentire investment period; annual returns are not reflected. Present Value (NPV):a.Considers all estimated cash flows of project; can beapplied to equal and unequal cash flows.b.Can reflect changes in level of risk over life of project.parisons of projects of unequal sizes is more difficult5.Internal Rate of Return (IRR):a.Considers all estimated cash flows of project.b.Readily computed when cash flows are equal, but requirestrial and error estimation when cash flows are unequal.c.Allows comparisons of projects with different investmentamounts.d.Does not reflect changes in risk over life of project.Chapter OutlineNotes Section 2—Managerial DecisionsEmphasis is on use of quantitative measures to make important short-termdecisions. Costs and other factors relevant to decision must be identified.I.Decisions and InformationA.Decision Making1.Five steps involved in managerial decision making.a.Define the decision taskb.Identify alternative courses of action.c.Collect relevant information and evaluate each alternative.d.Select the preferred course of action.e.Analyze and assess the decision.2.Both managerial and financial accounting information playimportant role in making decisionsa.Accounting system provides primarily financialinformation such as performance reports and budgetanalyses.b.Non-financial information is also relevant, such asenvironmental effects, political sensitivities, and socialresponsibility.B.Relevant Costs and Benefits1.Managers should focus on relevant benefits which exceedrelevant costs.a.Relevant costs are the incremental costs, or differentialcosts which are the additional costs incurred if a companypursues a certain course of action.b.Relevant benefits are the additional or incrementalrevenue generated by selecting a certain course of actionover another. Three types of costs:i.Sunk cost arises from a past decision; cannot beavoided or changed, and not relevant to futuredecisions.ii.Out-of-pocket cost requires future outlay of cash andresults from result of management’s decisions; isrelevant.iii.Opportunity cost is a potential benefit lost by takingspecific action when two or more alternative choicesare available; consideration is important.Chapter OutlineNotes II.Managerial Decision Scenarios consider each decision taskdiscussed below independent from the others.A. Additional Business1.Effect on net income must be considered when decidingwhether to accept or reject an order; reject if loss results.2.Historical costs are not relevant to this decision.3.Incremental or additional costs (also called differential costs)are additional costs incurred if company pursues certaincourse of action; relevant to this decision.4.Minimum acceptable price per unit can be determined bydividing incremental cost by the number of units in the order.5.Incremental costs of additional volume are relevant.6.If additional volume approaches or exceeds existing availablecapacity of factory, incremental costs required to expandcapacity may quickly exceed incremental revenue.7.Accepting order may cause existing sales to decline; thecontribution margin lost from the decline in sales is anopportunity cost and is relevant (if future cash flows overseveral time periods are affected, net present value should becomputed).8.Note – Allocated overhead costs, which are historical costs,should not automatically be considered; only incremental coststo be incurred are relevant.9.Key point: management must not blindly use historical costs,especially allocated to overhead costs. Instead the accountingsystem needs to provide incremental cost information if theadditional business is accepted.B.Make or Buy1.When determining whether to make or buy a component of aproduct, only incremental costs are relevant.2.Only incremental (additional) overhead costs are relevant; anincremental overhead rate should be determined.3.If the incremental costs of making the component exceed thepurchase price paid to buy the component, decision rule wouldbe to buy. Process of buying from an external supplier iscalled outsourcing. Several other factors should beconsidered.a.Product quality.b.Timeliness of delivery (especially in JIT settings).c.Reactions of customers and suppliers.d.Other intangibles (employee morale and workload).e.Must also consider if making the part will requireincremental fixed costs to expand plant capacity.Chapter OutlineNotesC.Scrap or Rework1.Costs already incurred in manufacturing units of product notmeeting quality are sunk costs and are irrelevant in anydecision on whether to sell to substandard units as scrap orrework to meet quality standards.2.Incremental revenues, incremental costs of reworking defects,and opportunity costs (the contribution margin lost if sales ofother units are given up) are all relevant.D.Sell or Process Further1.Partially completed products can be sold as is or they can beprocessed further and then sold as other products.pute incremental revenue from further processing(amount of revenue after further processing less revenue fromselling the products as partially completed)pute incremental cost from further processing.4.Process further and sell if incremental revenue from furtherprocessing exceeds related incremental costs.E.Sales Mix Selection1.When more than one product is sold, some are likely to bemore profitable than others; management should concentratesales efforts on more profitable products.2.If production facilities or other factors are limited, an increasein production and sale of one product usually requiresreduction in production and sale of others.3.The most profitable combination, or sales mix, of productsshould be determined. To identify the best sales mix,management focuses on the contribution margin per unit ofscarce resource. The scarce resource could be the machinesused to make the products.4.Determine the contribution margin of each product, thefacilities required to produce these products and anyconstraints on facilities and markets for the products.5.If demand is unlimited and the products use the same inputsthen the product with the highest contribution margin shouldbe produced.6.If demand is unlimited but the products use different inputsthen determine contribution margin per unit of the constraint(the factor that limits capacity, such as machine timerequired); produce the product with the highest contributionmargin per unit of the constraint.7.If demand is limited then the company should first produce themost profitable product, up to the point of the total demand.The remaining capacity should be used to produce the nextmost profitable product.Chapter OutlineNotesF.Segment Elimination1.If segment, division, or store is performing poorly,management must consider eliminating it.2.It is not sufficient to base the decision on net income (loss) orits contribution to overhead.3.Need to consider avoidable and unavoidable expenses:a.Avoidable (or escapable) expenses are costs or expensesthat would not be incurred if the segment is eliminated.b.Unavoidable (or inescapable) expenses are costs orexpenses that would continue even if the segment iseliminated.4.Decision rule – Segment is candidate for elimination if itsrevenues are less than its avoidable expenses.5.Should also assess impact of elimination on other segments.a.An unprofitable segment might contribute to anothersegment’s revenue and expensesb. A profitable segment might be eliminated if its space,assets and staff can be more profitably used by anothersegment or new segment.G.Keep or Replace Equipment1.Must decide whether the reduction in variable manufacturingcosts over its life is greater than the net purchase price of thenew equipment. purchase price is the cost of the new equipment lessany trade in allowance given or cash receipt for the oldequipment.b.Book value of the old equipment is not used. It is a sunkcost.III.Decision Analysis−Break-Even Time (BET) −A variation of thepayback period method – overcomes the limitation of not using thetime value of moneyA.The future cash flows are restated in terms of their present values;B.The payback period is computed using these present valuesC.Break-even time (BET) is useful measure; managers know whento expect cash flows to yield net positive returns.D.If BET is less than estimated life of investment, positive netpresent value can be expected from investment.E.To compare and rank alternative investment projects, choose theproject with the lowest break-even time.IV.Product Pricing –companies often use cost-plus pricing as a startingpoint in determining selling prices. Many factors determine price.Chapter OutlineNotesA.Target costing – used when competition is high and they havelittle control in setting prices.Target cost = expected selling price – desired profitB.Other Pricing methods – alternatives include approaches based oneither product costs or variable costs. Companies must adjusttheir desired markup percentage upward to ensure that the sellingprice covers all costs.C.Variable cost method – the markup percentage is determined as:Markup % = (Target profit + Fixed OH + Fixed S&A) / Totalvariable costs.D.Selling price = (direct materials + direct labor + OH + sellingcosts + administrative costs) = total cost + markup.Chapter 25 Alternate Demo ProblemA company is planning to buy a new machine at a cost of $200,000. The machine is expected to last for 10 years and have no salvage value at the end of its useful life. Straight-line depreciation will be used. The company expects to save 10,000 hours of direct labor each year because of the new machine, as well as $4,000 each year in other operating costs.Management’s best estimate is that on average the hourly rate for the labor saved will be $5.50. With the exception of the initial purchase, assume all cash flows take place at the end of the year, and a tax rate of 40%.Required:1. Calculate the payback period on the investment in new machinery.2. Calculate the rate of return on the average investment.3. Calculate the net present value of the investment and profitability index:(a) Ignoring income taxes, using a discount rate of 10%.(b) Including the effect of taxes, using a 10% discount rate.Chapter 25 Alternate Demo Problem: Solution1. First, calculate annual net cash flow:Determine increase in after-tax net income:Labor savings: 10,000 hours @ $5.50 per hour $55,000Other operating savings 4,000Annual cash savings before tax 59,000Less: annual depreciation expense 20,000Increase in net income before tax 39,000Less: Increase in annual income tax @ 40% 15,600Increase in net income after tax $23,400 Then, add back depreciation expense (noncash):Increase in net income after tax $23,400Plus annual depreciation expense 20,000Annual net cash flow $43,400 Payback period equals cost of new machine divided by annual net cash flow or $200,000 / $43,400 = 4.6 years.2. The rate of return on average investment equals the increase in net income aftertax divided by the amount of the average investment.The average investment would be $200,000 / 2, or $100,000.Rate of return on average investment = $23,400 / $100,000 = 23.4%3(a) There is a cash savings of $59,000 each year for 10 years if income taxes are ignored. The present value factor for a 10-year annuity at 10% is 6.1446.Present value of cash savings ($59,000 x 6.1446) $362,531 Present value of investment 200,000 Net present value (positive) $162,531 Profitability Index = Net Present Value = $ 162,531 = .813Cost of Investment $ 200,0003(b) There is a cash savings of only $43,400 each year for 10 years if income taxes are considered.Present value of cash savings ($43,400 x 6.1446) $266,676 Present value of investment 200,000 Net present value (positive) $ 66,676 Profitability Index = Net Present Value = $ 66,676 = .333Cost of Investment $ 200,000。