bma9e13 Agency Problems, Management Compensation, and The Measurement of Performance Principles of C

- 格式:ppt

- 大小:651.50 KB

- 文档页数:24

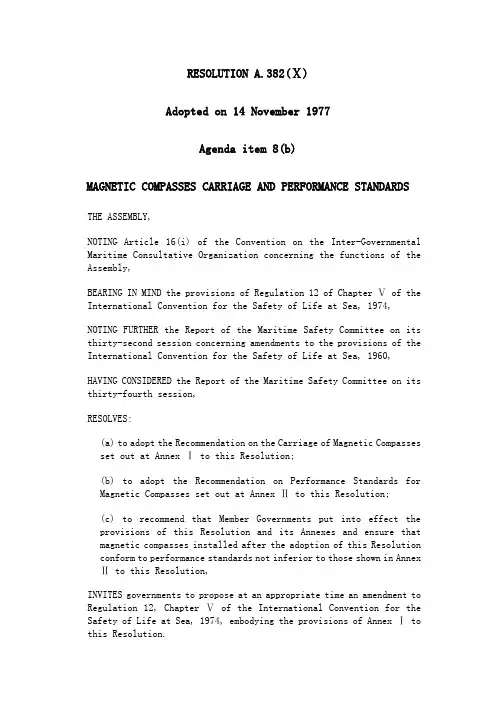

RESOLUTION A.382(Ⅹ)Adopted on 14 November 1977Agenda item 8(b)MAGNETIC COMPASSES CARRIAGE AND PERFORMANCE STANDARDS THE ASSEMBLY,NOTING Article 16(i) of the Convention on the Inter-Governmental Maritime Consultative Organization concerning the functions of the Assembly,BEARING IN MIND the provisions of Regulation 12 of Chapter Ⅴ of the International Convention for the Safety of Life at Sea, 1974,NOTING FURTHER the Report of the Maritime Safety Committee on its thirty-second session concerning amendments to the provisions of the International Convention for the Safety of Life at Sea, 1960,HAVING CONSIDERED the Report of the Maritime Safety Committee on its thirty-fourth session,RESOLVES:(a) to adopt the Recommendation on the Carriage of Magnetic Compassesset out at Annex Ⅰ to this Resolution;(b) to adopt the Recommendation on Performance Standards forMagnetic Compasses set out at Annex Ⅱ to this Resolution;(c) to recommend that Member Governments put into effect theprovisions of this Resolution and its Annexes and ensure that magnetic compasses installed after the adoption of this Resolution conform to performance standards not inferior to those shown in Annex Ⅱ to this Resolution,INVITES governments to propose at an appropriate time an amendment to Regulation 12, Chapter Ⅴ of the International Convention for the Safety of Life at Sea, 1974, embodying the provisions of Annex Ⅰ to this Resolution.ANNEX ⅠRECOMMENDATION ON THE CARRIAGE OF MAGNETIC COMPASSES Member Governments are recommended to ensure that:1. All ships are fitted with:(a) a standard magnetic compass, as defined in Annex Ⅱ,(b) a steering magnetic compass, as defined in Annex Ⅱ, unless theheading information provided by the standard compass, required under sub-paragraph (a), is made available and clearly readable by the helmsman at the main steering position;(c) adequate means of communication between the standard compassposition and the normal navigation control position to the satisfaction of the Administration.2. A spare magnetic compass, interchangeable with the standard compass, is carried, unless the steering compass mentioned in sub-paragraph 1(b) or gyro-compass is fitted.3. Each magnetic compass is properly compensated and its table or curve of residual deviations is available on board in the vicinity of the compass at all times.Note: The Administration, if it considers it unreasonable or unnecessary to require a standard magnetic compass, may exempt any ship from these requirements if the nature of the voyage, the ship's proximity to land or the type of ship does not warrant a standard compass, provided that a suitable steering compass will in all cases be required.ANNEX ⅡRECOMMENDATION ON PERFORMANCE STANDARDS FOR MAGNETICCOMPASSES1. Definitions1.1 A magnetic compass is an instrument designed to seek a certaindirection in azimuth and to hold that direction permanently, and which depends, for its directional properties, upon the magnetism of the earth.1.2 The standard compass is a magnetic compass used for navigation,mounted in a suitable binnacle containing the required correcting devices and equipped with a suitable azimuth reading device.1.3 The steering compass is a magnetic compass used for steeringpurposes mounted in a suitable binnacle containing the required correcting devices.Note: If the transmitted image of a sector of the standard compass card of at least 15˚to each side of the lubber mark is clearly readable for steering purposes at the main steering position, both in daylight and artificial light according to 7.1, the standard compass can also be regarded as the steering compass.2. Compass Card2.1 The compass card should be graduated in 360 single degrees. Anumerical indication should be provided every ten degrees, starting from North (000˚) clockwise to 360˚. The cardinal points should be indicated by the capital letters N, E, S and W. The North point may instead be indicated by a suitable emblem.2.2 The directional error of the card, composed of inaccuracies ingraduation, eccentricity of the card on its pivot and inaccuracy of orientation of the card on the magnetic system should not exceed 0.5˚on any heading.2.3 The card of the steering compass should clearly be readable bothin daylight and artificial light at a distance of 1.4 m. The use ofa magnifying glass is permitted.3. Materials3.1 The magnets used in the directional system and the correctormagnets for correcting the permanent magnetic fields of the shipshould have a high coercivity of at least 11.2.3.2 Material used for correcting induced fields should have a lowremanence and coercivity.3.3 All other materials used in the magnetic compass and in thebinnacle should be non-magnetic, so far as reasonable and pracicable and such that the deviation of the card caused by these materialsshould not exceed ( -->)˚, where H is the horizontal component of the magnetic flux density in (micro Tesia) at the place of the compass.4. PerformanceThe magnetic compass equipment should operate satisfactorily and remain usable under the operational and environmental conditions likely to be experienced on board ships in which it is installed.5. Constructional Error5.1 With the compass rotating at a uniform speed of 1.5˚ per secondand temperature of the compass of 20℃± 3℃ the deflection of thecard should not exceed ( -->)˚, if the diameter of the card is less than 200 ㎜. If the diametter of the compass card is 200 ㎜ ormore, the deflection of the card should not exceed ( -->)˚; H being defined as in sub-paragraph 3.3.5.2 The error due to friction should not exceed ( -->)˚ at atemperature of 20℃± 3℃; H being defined as in sub-paragraph 3.3.5.3 With a horizontal component of the magnetic field of 18 the halfperiod of the card should be at least 12 seconds, after an initial deflection of 40˚. The time taken to return finally to within ±1˚ of the magnetic meridian should not exceed 60 seconds after an initial deflection of 90˚. Aperiodic compasses shall comply with the latter requirements only.6. Correcting Devices6.1 The binnacle should be provided with devices for correctingsemicircular and quadrantal deviation due to:(a) the horizontal components of the ship's permanent magnetism;(b) heeling error;(c) the horizontal component of the induced horizontal magnetism;(d) the horizontal component of the induced vertical magnetism.6.2 The correcting devices provided in sub-paragraph 6.1 shouldensure that no serious changes of deviation occur under the influence of the conditions described in paragraph 4 and particularly considerable alteration of magnetic latitude. Sextantal and deviations of higher order should be negligible.7. Construction7.1 Primary and emergency illumination should be installed so thatthe card may be read at all times. Facilities for dimming should be provided.7.2 With the exception of the illumination, no electrical powersupply should be necessary for operating the magnetic compass.7.3 In the case where an electrical reproduction of the indicationof the standard compass is regarded as a steering compass, the transmitting system should be provided with both primary and emergency electrical power supply.7.4 Equipment should be constructed and installed in such a way thatit is easily accessible for correcting and maintenance purposes.7.5 The compass, binnacle and azimuth reading device should be markedto the satisfaction of the Administration.7.6 The standard compass should be suspended in gimbals so that itsverge ring remains horizontal when the binnacle is tilted up to 40˚in any direction, and so that the compass cannot be dislodged under any condition of sea or weather. Steering compasses suspended in gimbals should meet the same requirements. If they are not suspended In gimbals they should have a freedom of the card of at least 30˚in all directions7.7 Material used for the manufacture of magnetic compasses shouldbe of sufficient strength and be to the satisfaction of the Administration.8. Positioning8.1 The magnetic compass equipment should be installed Ifpracticable and reasonable on the ship's centreline. The main lubber mark should indicate the ship's heading with an accuracy of ± O.5˚.8.2 The standard compass should be installed so that from ifsposition the view is as uninterrupted as possible, for the purpose of taking horizontal and celestial bearings. The steering compass should be clearly readable by the helmsman at the main steering position.8.3 The magnetic compasses should be installed as far as possiblefrom magnetic material. The minimum distances of the standard compass from any magnetic material which is part of the ship's structure should be to the satisfaction of the Administration. The following diagram gives general guidelines to indicate the minimum desirable distances from the standard compass. The minimum desirable distances for the steering compass may be reduced to 65 per cent of the values given by the diagram provided that no distance is less than 1m. If there is only a steering compass the minimum distances for the standard compass should be applied as far as practicable.DiagramMinimum desirable distances from the Standard CompassUninterrupted fixed magnetic materialEnd parts of flued magnetic material such as top edges of walls, partitions and bulkheads, extremities of flames, girders, stanchions, beams. pillars and similar steel parts. Magnetic materialsubject to movement at sea such as davits. ventilators, steel doors, etc. Large masses of magnetic material with variable fields such as funnels.8.4 The distance of the magnetic compass from electrical or magneticequipment should be at least equal to the safe distance specified for the equipment and be to the satisfaction of the Administration.。

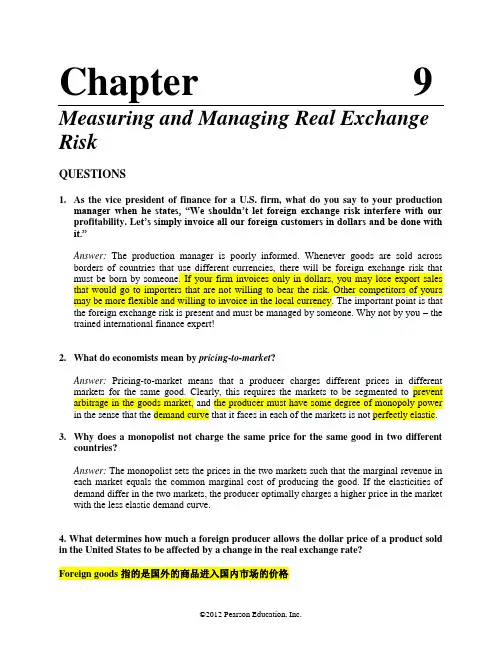

Chapter 9 Measuring and Managing Real Exchange RiskQUESTIONS1.As the vice president of finance for a U.S. firm, what do you say to your productionmanager when he states, “We shouldn’t let foreign exchange risk interfere with our profitability. Le t’s simply invoice all our foreign customers in dollars and be done with it.”Answer: The production manager is poorly informed. Whenever goods are sold across borders of countries that use different currencies, there will be foreign exchange risk that must be born by someone. If your firm invoices only in dollars, you may lose export sales that would go to importers that are not willing to bear the risk. Other competitors of yours may be more flexible and willing to invoice in the local currency. The important point is that the foreign exchange risk is present and must be managed by someone. Why not by you – the trained international finance expert!2.What do economists mean by pricing-to-market?Answer: Pricing-to-market means that a producer charges different prices in different markets for the same good. Clearly, this requires the markets to be segmented to prevent arbitrage in the goods market, and the producer must have some degree of monopoly power in the sense that the demand curve that it faces in each of the markets is not perfectly elastic.3.Why does a monopolist not charge the same price for the same good in two differentcountries?Answer: The monopolist sets the prices in the two markets such that the marginal revenue in each market equals the common marginal cost of producing the good. If the elasticities of demand differ in the two markets, the producer optimally charges a higher price in the market with the less elastic demand curve.4. What determines how much a foreign producer allows the dollar price of a product sold in the United States to be affected by a change in the real exchange rate?Foreign goods 指的是国外的商品进入国内市场的价格Chapter 9: Measuring and Managing Real Exchange Risk2Answer: Pricing-to-market interacts with changes in the real exchange rate to prevent the full pass-through of the change in the exchange rate to the change in the price of the good. If the real exchange rate moves in a favorable direction for the monopolist, the foreign price of the good could be allowed to fall one-for-one with the appreciation of the foreign currency. But, while the monopolist will allow the price to fall to allow the sale of more goods, the monopolist will not let the price fall one-for-one with the exchange rate because the monopolist has the opportunity to take enhanced profitability on all sales. Conversely, if the real exchange rate moves in an unfavorable direction for the monopolist, the foreign price of the good will be allowed to rise to decrease the amount sold, but the monopolist will also accept some reduced profitability on all sales.5.Why is the pass-through from changes in exchange rates to changes in the prices of products not one-for-one?Answer: Imperfect pass-through ultimately reflects imperfections in the competitiveness of goods markets. If markets were perfectly competitive, pass-through would be full. For additional discussion, see the answer to Question 5. These are really the same question.6.Given that real exchange rates fluctuate, when would be the best time to enter the market of a foreign country as an exporter to that market?Answer: Firms often introduce new products in foreign markets when the foreign currencies are strong in real terms. Doing so allows the new entrant to the market to set a comparatively low foreign currency price for a product so that it can better compete and become an established player in the market. This strategy allows the exporter to develop loyal customers who will then potentially tolerate increases in the foreign currency price that the exporter feels compelled to introduce when the foreign currency eventually depreciates relative to the exporter’s currency.7.You have been asked to evaluate possible sites for an Asian production facility that will manufacture your firm’s products and sell them to the Asian market. What real exchange rate considerations should you entertain in your evaluation?Answer: You must be aware of the strength or weakness of the real exchange rates in the various countries. Because your firm will be exporting from the country in which the plant is located, your profits will be hurt by a future real appreciation (相当于home currency 增值)of the currency of that country relative to the currencies of countries to which you export. Your costs would rise with no corresponding benefit in sales. Thus, if the potential production country currency is currently severely undervalued on foreign exchange markets, this country may appear to be a low cost production center, but it is likely that this cost advantage will be eroded by a real appreciation in the future.Chapter 9: Measuring and Managing Real Exchange Risk 3Chapter 10Exchange Rate Determination andForecastingQUESTIONS1. What is the difference between the ex ante and the ex post real interest rate?Answer: The ex post interest rate corrects the nominal interest rate with the realized or ex post rate of inflation; whereas the ex-ante (or expected) real interest rate corrects the nominal interest rate for expected inflation.As a lender, you care about the real return on your investment, which is the return thatmeasures your increase in purchasing power between two periods of time. If you invest $1,you sacrifice where P(t) is the price level. In 1 year, you get back 1 + i P(t+1), where i is the nominal rate of interest. We calculate the real return by dividing the real amount you get back by the real amount that you invest. Thus, if r ep is the ex post real rate of return and ex post real interest rate, we have ()ep 1 + i 1 + i P(t+1)1 + r = = 1P(t+1)P(t)P(t)⎛⎫ ⎪⎝⎭⎛⎫⎛⎫ ⎪ ⎪⎝⎭⎝⎭Notice that the real rate of interest depends on the realization of the rate of inflation because P(t + 1)/P(t) = 1 + π(t + 1), where π(t + 1) is the rate of inflation between time t and t + 1. For simplicity, we drop the time notation and simply writeep (1 + i)1 + r = (1 + π) If we subtract 1 from each side, we haveep (1 + i)(1 + π)i - πr = -= (1 + π)(1 + π)(1 + π)which is often approximated asr ep = i – πChapter 9: Measuring and Managing Real Exchange Risk4The approximation involves ignoring the term (1 + π) in the denominator, which is close to 1 if inflation is not too high. Thus, the ex post real interest rate equals the nominal interest rate minus the actual rate of inflation.Because the inflation rate is uncertain at the time an investment is made, the lender cannot know with certainty the real rate of return on the loan. By taking the expected value of both sides of the equation, conditional on the information set at the time of the loan, we derive the lender’s expected real rate of return, which is also called the expected real interest rate, or the ex ante real interest rate, which we denote r e:e epr = E[r] = i(t) - E[π(t+1)]t t2.Suppose that the international parity conditions all hold and a country has a highernominal interest rate than the United States. Characterize the country’s inflation rate compared to the United States, the country’s expected exchange rate change versus the dollar, the country’s currency forward premium (or discount) versus the dollar, and the country’s real interest rate compared to the U.S. real interest rate.Answer: When all the parity conditions hold, real interest rates are equalized across countries, so the country’s real interest rate should equal that of the United States. The country’s higher nominal interest rate therefore must reflect a higher expected rate of inflation relative to the United States. Since the parity conditions hold, a higher expected rate of inflation implies that country’s currency should be expected to depreciate relative to the dollar, and the currency will trade at a forward discount relative to the dollar.3.How do fundamental analysis and technical analysis differ?Answer: Fundamental analysis typically uses formal economic models of exchange rate determination and macroeconomic fundamental data such as money supplies, inflation rates, productivity growth rates, and the current account of the balance of payments to predict exchange rates.Technical analysis uses only past exchange rate data, and perhaps some other financial data, such as the volume of currency trade, to predict future exchange rates.4.Would technical analysis be useful if the international parity conditions held? Why orwhy not?Answer: If the parity conditions held, technical analysis would not be useful in the sense of providing profitable trading information or information about expected exchange rates that could not be obtained elsewhere. If the parity conditions held, the best predictor of the future exchange rate would be the forward rate, and exchange rate forecasts based on other indicators would not lead to systematic profits on currency speculation.Chapter 9: Measuring and Managing Real Exchange Risk 5 5.Describe three statistics you should obtain from a currency-forecasting service in orderto judge the quality of its currency forecasts.Answer: Three important statistics are the Root Mean Squared Error (RMSE) or Mean Absolute Deviation of its forecasting record, which would provide information on accuracy;the percentage of times they were on the correct side of the forward rate, which would provide useful information on the profitability, and a risk–return statistic (such as the Sharpe ratio), which would provide a characterization of the profitability of using their forecasts in a real time trading strategy.6.Does a large increase in the domestic money supply always lead to a depreciation of thecurrency?Answer: Most theories of the determination of exchange rates would predict that a large increase in the money supply would imply a depreciation of the currency, definitely in the long run, and especially as economists say when “everything else is equal.” However, it is possible that the change in the money supply is accompanied by an increase in real income that increases the demand for money and thus offsets the money supply’s effect on the exchange rate.7.Is a current account deficit always associated with a strong real exchange rate (that is,one that is overvalued compared to the PPP prediction)?Answer: Not necessarily. It is best to view the current account and the real exchange rate as being determined in an equilibrium that depends on many forces, such as movements in net foreign assets, government spending, productivity growth, and the expectations and risk tolerances of domestic and foreign investors.8.Describe how three macroeconomic fundamentals affect exchange rates.Answer: According to the monetary exchange rate model, the domestic currency weakens (strengthens) if the domestic (foreign) money supply increases today or if news arrives that leads people to believe that the future domestic (foreign) money supply will increase. The domestic currency also weakens if domestic real income falls, if foreign real income rises, or if news arrives that causes people to expect lower domestic real growth or faster foreign real growth. Finally, according to the equilibrium theory regarding the real exchange rate and the current account, an increase in government spending or a decrease in taxes that causes a budget deficit should increase the real exchange rate (and hence likely also the nominal exchange rate). This is because an increase in government spending increases aggregate demand in the economy, which causes the real interest rate to rise. The rise in the interest rate reduces investment and encourages private saving.Chapter 9: Measuring and Managing Real Exchange Risk69.Which simple statistical model yields some of the best exchange rate predictionsavailable? What does this imply for the value of models of exchange rate determination to multinational businesses?Answer: It is surprisingly difficult to beat the forecasts of the random walk model. This model uses the current exchange rate as the predictor of the future exchange rate. If this model provided the best forecast, the unbiasedness hypothesis (which says the forward rate is the best predictor) would be violated. If there were a forward premium on the foreign currency, the forward rate would be above the expected future spot rate, and you would want to sell the foreign currency in the forward market.10.What is chartism?Answer: Chartists graphically record the actual trading history of an exchange rate and then try to infer possible future trends based on that information alone.11.What is an x% filter rule?Answer: An x% rule states that you should go long in the foreign currency (buy) after the foreign currency has appreciated relative to the domestic currency by x% above its most recent trough (or support level) and that you should go short in the foreign currency (sell) whenever the currency falls x% below its most recent peak (or resistance level). Common x% filter rules are 1% or 2%.12.What is a moving-average crossover rule?Answer: Moving-average crossover rules use moving averages of the exchange rate to indicate trade directions. An n-day moving average is just the sample average of the last n trading days, including the current rate. A (y, z) moving-average crossover rule uses averages over a short period (y days) and over a long period (z days). The strategy states that you should go long (short) in the foreign currency when the short-term moving average crosses the long-term moving average from below (above). Common rules use 1 and 5 days (1, 5), 1 and 20 days (1, 20), and 5 and 20 days (5, 20).13.Have currency traders been successful in exploiting their exchange rate forecasts?Answer: While there exists scant empirical evidence on the forecasting ability of exchange rate forecasting services, the number of active currency traders, mostly organized as hedge funds, has grown considerably over the past decade. Because many of these currency traders report returns to various indices, we can analyze their performance. If such funds fail to forecast exchange rates, they should not consistently produce high returns! Pojarliev and Levich (2008) conducted a study on the returns earned by currency managers reporting to theChapter 9: Measuring and Managing Real Exchange Risk 7 Barclay Currency Traders Index (BCTI) between January 1990 and December 2006. All of these returns are reported net of fees. Hedge funds typically charge a fixed fee of 2% and a variable fee of 20% on the performance over a benchmark (which can be zero or the Treasury bill return). The study first tries to establish what techniques the currency managers use: Do they use the carry strategy, do they follow trends, or do they trade based on fundamentals?To do so, the investigators use historical data to create returns to carry-trade, trend-following, and fundamental strategies for the major currencies, and they use regression analysis to investigate whether the returns of the various managers correlate with these benchmark returns. The majority of the funds (and the average index) appear to follow trend-following strategies; many also show positive carry exposure, but there is not much of a link with the return on fundamental strategies. Recent academic research has shown that the returns to simplistic trend following strategies are no longer statistically significant, but currency traders may follow more sophisticated strategies. The average excess return earned over 34 different managers with relatively long track records between 2001 and 2006 is 5.45%, and the average (annual) Sharpe ratio is 0.47, which is higher than the Sharpe ratio generated by the equity market. Pojarliev and Levich also check whether the managers outperform the benchmark returns. Deutsche Bank, among others, has introduced easily tradable funds that mimic the simple strategies represented by the benchmarks. For an investor, it would make little sense to pay the heavy fees hedge funds charge for exposure to an index that can be bought for a small fixed fee. Pojarliev and Levich find that only eight of the 34 managers significantly outperform a combination of benchmark indices that best describes their investment style.14.Are devaluations of pegged exchange rates totally unexpected?Answer: While there is a debate about their predictability, some theories suggest that devaluations may be partially predictable. These models argue that growing budget deficits, fast money growth, and rising wages and prices usually precede devaluations. Increases in nominal interest rates typically reflect a combination of the probability and magnitude of a possible devaluation.15.Construct a list of a country’s economic statistics you would assemble to help determinethe probability of a devaluation of its currency within the coming year.Answer: Based on theoretical and empirical work, the following economic variables should prove useful predictors: PPP-based measures of currency overvaluation, current account balances and monetary growth rates. In addition, if liquid financial markets exist, information about forward rates or interest rates, currency option prices, and so on may prove useful in terms of forecasting devaluations.PROBLEMSChapter 9: Measuring and Managing Real Exchange Risk81.Suppose the 1-year nominal interest rate in Zooropa is 9%, and Zooropa’s expectedinflation rate is 4%. What is the real interest rate in Zooropa?Answer: The expected real interest rate is approximately 9% - 4% = 5%. The correct computation is: (1 + 0.09) / (1 + 0.04) – 1 = 0.0481 or 4.81%.2.You were recently hired by the Doolittle Corporation corporate treasury to helpoversee its expansion into Europe. Blake Francis, the CFO, wants to hire a foreign exchange forecasting company. Blake has asked you to evaluate three different companies, and he has obtained information on their past performances. Out of a total of 50 forecasts for the $/€ rate, the companies reported the number of times they correctly forecast appreciations and depreciations:There are a total of 35 dollar appreciations (down periods) and 15 dollar depreciations (up periods) in the sample. Blake wants to know two things:a.Can anything be said about the companies’ forecasting ability with the availabledata?Answer: Yes, one can compute the number of correct “directional” forecasts. Morrissey has the highest correct proportion with 25 out of 50 correct, whereas the other firms have less than 50% correct. However, note that the dollar over this period was relatively strong and appreciations (down forecasts for the $/€ rate) dominate. Hence, forecasts in the down period may be more useful (see footnote 3 in the chapter). If we look at correct conditional forecasts, we see that Morrissey is correct 20/35 or 57.14% of the time when the dollar appreciates, but only 5/15 or 33.33% of the time when the dollar depreciates. According to the Henriksson–Merton test, the sum of these two proportions should be over 1 for a firm to have market timing ability. However, the sum in this case is only 90.47%. While Morrissey obviously dominates Pixie Land Exchange, it is not clear that it is better than FOREX Cures. The proportions of correct conditional forecasts of FOREX Cures are 12/35 (34.29%) and 12/15 (80%) for a sum of 114.29%. Consequently, only FOREX Cures shows directional forecasting ability.b.What additional information should Blake try to obtain in order to form a betterjudgment?Chapter 9: Measuring and Managing Real Exchange Risk 9 Answer: Directional forecasting ability in the foreign exchange market is not particularly useful if the forecasts are to be used in speculative strategies. To this end, it would have been more useful to know whether the forecasting firms were on the correct side of the forward rate. Ideally, a full record of forecasts would be obtained. Then, accuracy statistics (like the RMSE) and profitability statistics (like the Sharpe ratio) could be computed.3.Web Problem: Go to /currency/big-mac-index. Oanda reports the lastavailable Big Mac index but then updates the exchange rates on a regular basis to compare them with the PPP-based exchange rates. What are currently the most under-valued and over-valued exchange rates? How would you use this information in forecasting exchange rates?On June 6, 2011, the most overvalued currency versus the dollar was the Norwegian kroner (NOK). The actual exchange rate was NOK5.3407/USD and the implied PPP rate was 12.1.The dollar would have to strengthen by 126.56% if the current exchange rate were to go to the implied PPP rate. The most undervalued currency versus the dollar was the Ukrainian hryvnia (UAH). The actual exchange rate was UAH8.0544/USD and the implied PPP rate was 3.88. The dollar would have to weaken by 51.83% if the current exchange rate were to go to the implied PPP rate. If there is a tendency for large PPP deviations to correct themselves, one would forecast that the NOK was going to weaken versus the dollar and the UAH was going to strengthen versus the dollar. One might even want to speculate that the NOK would weaken relative to the UAH. You could borrow NOK, convert to dollars, convert to UAH, and invest the UAH money market.。

自《国家中长期教育改革和发展规划纲要(2010—2020年)》提出教育管理体制实行“管办评分离”以来,政府、高校、社会等多元主体参与的必要性及其合法地位在高等教育评估领域中逐渐明确[1]。

认证制度作为教育行业的一种自律行为和质量保障方法,已成为第三方评估的重要形式和手段。

该制度首创于美国,经过一百多年的发展,已形成了一套较为成熟的机制[2]。

目前已知的、具有全球影响力的国际认证机构包括:新闻与大众传播教育协会(A s s o c i a t i o nf o rE d u c a t i o ni nJ o u r n a -li s m a n dM a s sC o m m u n i c a t i o n ,简称A E J M C)、国际商学院促进协会(T h e A s s o c i a t i o n t o A d v a n c e C o lle g i a t eS c h o o ls o fB u s i n e s s ,简称A A C S B )以及美国工程和技术认定委员会(A c c r e d i t a t i o n B o a r d f o rE n g i n e e r i n g a n d T e c h n o lo g y ,简称A B E T )等。

本文选取全球知名的A A C S B 商科认证体系作为研究对象,重点分析作为该系统核心构成的认证标准及其变革演进情况,以及这些变化背后反映的有关商科教育和管理的价值取向与理念转变。

研究结论可为我国相关部门更好地应对第三方评估机制构建中出现的问题提供启示。

一、第三方评估与国际认证(一)第三方评估的定位与意义詹姆斯·罗西瑙(J a m e sN .R o s e n a u )等人在《没有政府的治理》(G o v e r n a n c eW i t h o u tG o v e r n m e n t )一书中提出“没有政府治理的公共服务与公共生活是否可能”的问题。