九 07年美国次贷危机(American subprime mortgage crisis in nine and 07)

- 格式:doc

- 大小:66.50 KB

- 文档页数:19

九 07年美国次贷危机(American subprime mortgage crisis in

nine and 07)

07 U.S. subprime mortgage crisis 2008-05-19 17:38

Subprime mortgage crisis in 07 years

First, the definition of subprime mortgage crisis in the United

States

The subprime mortgage crisis in the United States refers to the

financial market crisis caused by the insolvency of the debtor

in the real estate market. It refers to a storm that happened

in the United States due to the bankruptcy of the subprime

mortgage institutions, the closure of the investment fund and

the violent volatility of the stock market. It has led to a

looming shortage of liquidity in the world's major financial

markets. The subprime mortgage crisis in the United States

began to emerge gradually in the spring of 2006. August 2007

swept the world's major financial markets such as the United

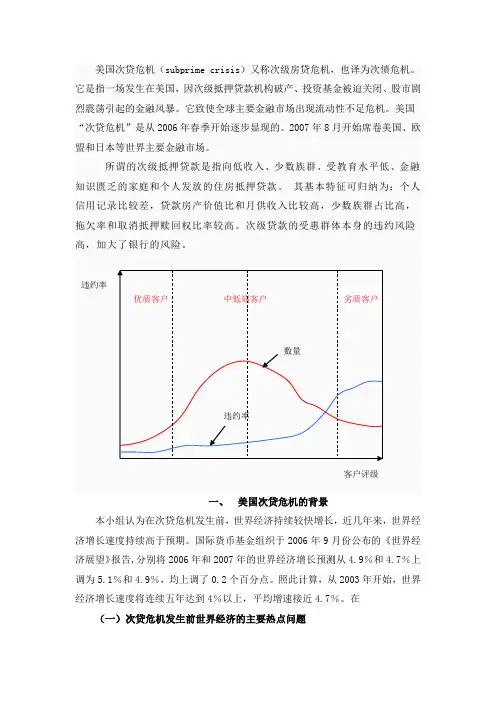

States, the European Union and japan. The subprime mortgage

loan is relative to the mortgage loan with better credit

condition. Through the form of mortgage, to low-income, no or

lack of sufficient repayment ability to prove, or other heavy

debt, credit conditions more "second" housing buyers loans. The

mortgage loan of American real estate market can be divided into

3 levels: high quality loan market, "ALT-A" loan market and

secondary loan market. High quality loan market faces high

credit level, reasonable debt burden and little risk, and the

mortgage interest rate is relatively low. Secondary market

refers to the low credit score, lack of proof of income, heavy debt of customers, such as the low income class and new

immigrants in the United states. The "ALT-A" loan market is a

gray area between the two, refers to the credit record is good,

but lack or no fixed income, deposits, assets and other

legitimate documents of the client. Subprime markets and ALT-A

lending markets are high-risk markets, mortgage rates are

higher than high-quality loans, subprime lending crisis is the

risk caused by this part of the market.

Two, the causes of the subprime mortgage crisis:

The direct cause of the U.S. subprime mortgage market turmoil

is the rising interest rates in the United States and the

continued cooling of the housing market. Subprime mortgages are

loans provided by some lending institutions to borrowers with

poor credit and low income.

Interest increases, resulting in increased repayment pressure,

many users who have bad credit feel the pressure of repayment,

the possibility of default, the impact of the recovery of bank

loans caused crisis.

The US subprime mortgage market usually adopts the fixed

interest rate and floating interest rate combination of

repayment, namely: property buyers in the purchase in the first

few years of fixed rate loans, followed by floating rate loans.

In the 5 years before 2006, the U.S. subprime mortgage market

grew rapidly due to the continued prosperity of the US housing

market and the low level of interest rates in the United States

in the past few years.

With the cooling of the housing market in the United States,

especially the short-term interest rate, the repayment

interest rate of the subprime mortgage loans has also risen

sharply, and the repayment burden of the buyers has been greatly

aggravated. At the same time, the continued cooling of the

housing market also makes it difficult for homebuyers to sell

their homes or refinance through mortgage housing. This

situation directly leads to a large number of subprime mortgage

borrowers can not repay the loan on time, and then lead to the

"subprime mortgage crisis"".

Three, the impact of the U.S. subprime mortgage crisis:

1, the impact of subprime mortgage crisis on the United states:

How broad will the impact of the sub prime crisis in the United

States be? This is the current world economic and financial

circles pay close attention to the problem.

From its direct influence:

First of all, the impact is a large number of low-income buyers.

Unable to repay their loans, they will face the difficult

situation of housing being repossessed by banks.

Secondly, more secondary mortgage institutions will be forced

to apply for bankruptcy protection because they can not accept

loans and suffer serious losses.

Finally, because many US and European investment funds have