2013年6月CFA+Level+I+重点习题集答案+FSA

- 格式:pdf

- 大小:36.71 KB

- 文档页数:6

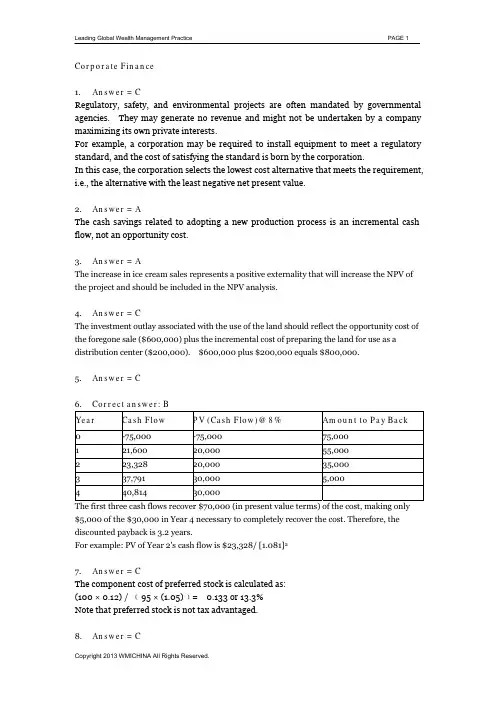

FSA1.Answer = CManagement must highlight any favorable and unfavorable trends and identify significant eventsand uncertainties that affect the company’s liquidity, capital resources and results of operations inthe management discussion and analysis (MD&A).2.Answer = BProxy statements are prepared and distributed to shareholders on matters that are to be put to avote at shareholder meetings.3.Answer = BFor a publicly traded firm in the United States, the auditor must express an opinion as to whetherthe company’s internal control system is in accordance with the Public Company AccountingOversight Board, under the Sarbanes–Oxley Act. This is done either as a final paragraph in theauditor’s report or as a separate opinion.4.Answer = B5.Answer = CThe company should have made an adjusting entry to reduce the Unearned revenue account (aliability) by $5,000 and increase Revenue, (and hence net income and retained earnings) by$5,000. As the company failed to make the adjusting entry the liabilities are overstated and owners’equity is understated.6.Answer = CTotal assets = liabilities + owner’s equity. Owner’s equity = $5,250– 2,200= 3,050. Ownersequity = contributed capital + ending retained earnings. Ending retained earnings = 3,050–1,400= 1,650. Ending retained earnings = beginning retained earnings + net income – dividends.1,650= 800 + net income – 200; Net income = $1,0507.Answer = APercentCompletedCosts Incurred/Total Costs Anticipated x 100Gross Profit % Complete x Anticipated Profit - Profit Already RecognizedYear 1Year 2Costs Incurred 3,117,500 3,117,500+2,582,500=5,700,000 Percent Complete 3,117,500/7,250,000 = 43.0% 5,700,000/7,600,000 = 75.0%Gross Profit 43.0% x (10,000,000 -7,250,000) = 1,182,500 75.0% x (10,000,000- 7,600,000) – 1,182,500 = 617,5008.Answer = BUnder the installment method, the portion of the total profit that is recognized in each period isdetermined by the percentage of the total sales price for which the seller has received cash. For Company A: 2/10 x 4 = $0.8 million. Note, cost recovery method could be used in this case, but the reported profit would be $0.9.Answer = AWhether securities are classified as held for trading or available for sale, they are measured at their fair value on the balance sheet, but all gains/losses on held for trading securities are reported on the income statements. The unrealized gains/losses on available for sale securities are reported in equity. However, this treatment is the same for both IFRS and U.S. GAAP reporting.10.Answer = CCFO = net income + depreciation + loss on sale of equipment + decrease in accounts receivable – increase in inventories + increase in accounts payable. (The loss on sale of equipment is added back when calculating CFO. It would have been deducted in the calculation of net income but the loss is not the cash impact of the transaction (the proceeds received, if any, would be the cash effect) and cash flows related to equipment transactions are investing activities, not operating activities. CFO = 45.8 + 18.2 +1.6 + 4.2 – 3.4 +2.5 = $68.9 million $68.9 – $7.3 = $61.6 million free cash flow to equity.11.Answer = ACredit analysis is concerned with a company’s debt-paying ability. Returns to creditors are normally paid in cash, so the company’s ability to generate cash internally is the most important factor in credit analysis.12.Answer = BEquipment sale 1 results in a gain of $20,000, sale 2 results in a gain of $30,000, and sale 3 results in a loss of $10,000. The net gain is $40,000. The amount that would be deducted from net income to determine cash flow from operations is equal to the net gain of $40,000.13.Answer = BSlowing down the rate or payments to suppliers is the simplest way to increase reported operating cash flow.14.Answer = AThe current ratio includes inventory but the quick ratio does not. (Current ratio is higher than quick ratio and quick ratio is higher than cash ratio.) The quick ratio includes accounts receivable but the cash ratio does not. The denominator for all three ratios is current liabilities, which are the same proportion for both companies. The difference in ratios is therefore created by inventory and accounts receivable. Company 1 has the higher percentage of inventory because the difference between the current ratio and quick ratio is greater for that company. Company 2 had the higher percentage of accounts receivable because the difference between the quick ratio and the cash ratio is greater for Company 2.15.Answer = CAny time the current ratio is above 1, equal changes in a current asset and a current liability will result in an increase in the current ratio: if current assets = 550 and current liabilities are 275, current ratio = 550/275 = 2.0. After the bank borrowing has been paid, the ratio becomes (550-150)/ (275-150) = 3.2. Had the ratio initially been below 1, current assets = 250 and current liabilities are 275, current ratio = 250/275 = 0.91, the equal change in current assets and liabilities would decrease the current ratio: 100/125=0.80.16.Answer = AThe recording of a warranty expense will create a warranty liability and the resulting increase in current liabilities will decrease the current ratio.17.Answer = ADiluted EPS is calculated using the treasury stock method that considers what would be the effect if the options or warrants had been exercised. Only options or warrants that are in-the-money are included, as out-of-the-money options would not be exercised. Therefore only the warrants are dilutive: their exercise price is below the average market price of the stock.Using the treasury stock method, the number of new shares issued on exercise is reduced by the number of shares that could be purchased with the cash received upon exercise of the warrants: 20,000($30) = $600,000 in proceeds.$600,000 / $40 = 15,000 shares treasury stock. Incremental shares using the treasury stock method = 20,000 – 15,000 = 5,000.18.Answer = CDuring a period of rising prices, ending inventory under LIFO will be lower than that of FIFO and cost of goods sold higher; therefore, inventory turnover (COGS/average inventory) will be higher.19.Answer = AThe equipment is impaired. NBV = $550,000 which is greater than the sum of the undiscounted cash flows 5 yrs x $80,000 = $400,000. The company’s future ROA will increase. Once the asset is written down, there will be lower depreciation charges, which will increase net income, and a lower carrying value of assets, which decreases total assets. Both factors would increase any future ROA.20.Answer = CIntangible assets with indefinite lives need to be tested for impairment at least annually. PP&E and intangibles with finite lives are tested only if there has been a significant change or other indication of impairment.21.Answer = CLong-lived assets that will be disposed of other than by sale, such as a spin-off, an exchange for other assets, or abandonment, are classified as held for use until disposal and continue to be depreciated until that time.22.Answer = BIFRS recommends the effective interest method for the amortization of bond discounts/premiums.The bond is issued for 0.9228x50 million= 46.140.Interest expense=46.140x5%=2.307million23.Answer = CThe book value of the bonds on 1 January 2011 is equal to the present value of the remaining coupon payments and principal discounted at the market rate at time of issue (3% per period).Coupon = 0.08 × ½ × 5,000,000 = 200,000; there are 4 years remaining or 8 coupon paymentsBook value = 200,000 PVAnnuity (n=8, i=3%) + 5,000,000 PV (n=8, i=3%) = 1,403,938 + 3,947,046 = 5,350,984Using a financial calculator: PMT = 200,000; FV = 5,000,000; I% =3%; N = 8;Compute PV = 5,350,984Because the market interest rate when the bonds are bought back (8%) is equal to the coupon rate, the company can buy back the bonds at par, $5,000,000Cost of repurchase $5,000,000Book value 5,350,984Gain on retirement 350,984On the cash flow statement the gain would be deducted from net income in calculating the cash from operations under the indirect method, and the cash paid to repurchase the bonds would be a cash outflow in the financing section.24.Answer = CThe pension expense would be the sum of the expense for the defined contribution plan and the defined benefit plan (retirement benefit obligation): 1,525 + 728 = 2,253.25.Answer = BNet income $800,000Add back book depreciation 70,000Deduct tax allowed depreciation (90,000)Deduct Dividend income (120,000)Add back Fine 100,000Add back book R&D 50,000Deduct tax allowed R&D (20,000)Taxable income 790,000Current taxes payable 35% x $790,000=276,50026.Answer = AAccounting Purposes TaxPurposes Revaluation surplus (10,000 – 6,800) =3,200 no revaluation allowed Depreciation, straight-line 20 years 5 years remaining2009 start of year balanceafter revaluation 10,000 5,000 Depreciation 2009 500 1,000Net balance end of 2009 9,500 4,000Less revaluation surplus (3,200) _____Carrying value for purposes ofdeferred taxes 6,300 4,000 Deferred tax liability = 0.30 x (6,300 – 4,000) = 690Only the portion of the difference between the tax base and the carrying amount that is not the result of the revaluation is recognized as giving rise to a deferred tax liability. The portion arisingfrom the revaluation surplus is used to reduce the revaluation surplus in equity.27.Answer = AThe present value of the operating leases should be added to both the total debt and the total assets.To estimate the present value it is appropriate to estimate the number of years of lease payments reflected in the 2016 and thereafter figure. Based on the constant expense shown in the first 5 years, there are 9 (1,260/140) more payments for a total of 14 payments.Adjusted debt to total assets=(2,125+1,134)/(4,500+1,134)=57.8%14 N, 140 PMT, 10 I/Y, 0 FV, CPT PV*(1+10%)28.Answer = BIt is a sales type lease: the lease period covers more than 75% of its useful life (5/6=83.3%) and the asset is on its books at less than the present value of the lease payments ($199,635) (PMT = $50,000, N=5, i=8%). The firm must have acquired or manufactured the asset if it is recorded at less than the present value of the lease payments.29.Answer = BThe present value of the lease is $360,477.62. (n = 5, I = 12%, PMT = $100,000) 12% of the originalPV is $43,257.31 and represents the interest component of the payment in the first year. The difference between the annual payment and the interest is the amortization of the lease obligation included in cash flow from financing. $100,000 – 43,257.31 = $56,742.69. Depreciation is $360,477.62 / 5 or $72,095.52 so the total reduction in pretax income would be interest plus depreciation or $115,352.83. Cash flow from operations would be reduced by the amount of the interest only because the depreciation would be added back to determine cash flow from operations.30.Answer = AYear StartingBalanceInterestExpense@12%LeasePaymentPrincipalReductionEndingBalance1 10,000 0 2,000 2,000 8,0002 8,00096031.Answer = CA ratio of operating cash flow to net income below 1.0 (not above 1.0) can be a warning sign of low quality earnings.32.Answer = BThe “fraud triangle” requires incentives (e.g. debt covenants), opportunities, and management’s ability to rationalize (temporary economic conditions). Adding independent members to the Board of Directors should improve corporate governance and hence decrease the opportunity for fraud.33.Answer = AUS GAAP requires that interest paid be classified as an operating cash flow; IFRS allows interest paid to be classified as either an operating or financing activity.34.Answer = BThe company is recognizing revenue for sales on shipment while the risks and rewards of ownership have not yet been transferred to the wholesalers. The motivation behind the activity is most likely the pressure to meet the expectations of investment analysts to meet ever increasing sales growth forecasts.。