Conceptual Framework Overview

Objectives of Financial Reporting Qualitative Elements Characteristics of Financial of Information Statements Accounting Recognition and Measurement Concepts Assumptions Principles Constraints

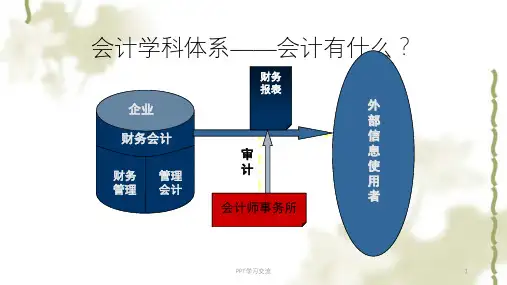

财务报告概念框架内容

财务报告目标 基本假设 财务报告信息质量特征 财务报表要素 财务报表要素的确认 财务报表要素的计量 财务报告

美国注册会计师协会(AICPA) 在1992年发布第69号审计准则,将 GAAP划分为若干层次:

Generally Accepted Accounting Principles (GAAP)

Continued

Hierarchy of Sources of GAAP

D. Widely accepted practices and pronouncements representing prevalent practice in a particular industry or applications to specific circumstances. E. Other accounting literature.

Conceptual Framework

The fundamentals are the underlying concepts of accounting, concepts that guide the selection of events to be accounted for, the measurement of those events, and the means of summarizing and communicating them to interested parties. (Scope and Implications