Prediction_Markets

- 格式:ppt

- 大小:102.50 KB

- 文档页数:3

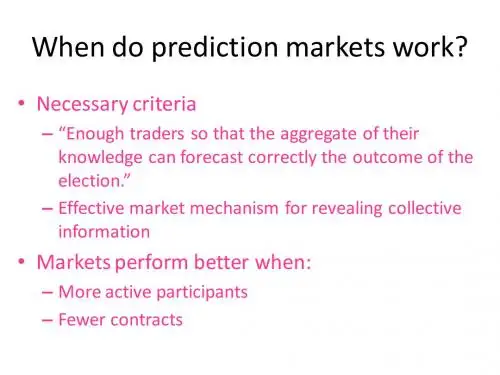

prediction的作用

近来,越来越多的企业和团体开始重视技术创新,致力于加速新型产品的研发、改善企业的运营,其中预测技术颇受青睐。

预测技术即将机器学习技术结合运用于数据、产品的分析与预测领域,它通过提取数据动态而不断更新的特点,可以迅捷简单地分析出大量定向、有效、值得信赖的预测数据,已成为互联网企业组建运营等方面的实用利器。

预测技术在互联网行业已经得到大量的应用,例如社交活动的预测,能够有效

的提供社交活动的参与度和热度分析,使企业在活动策划时能够快速制定有效的营销方案;另外,预测技术还能够帮助企业预测网站的用户访问量,大大改善网站的运营,有效避免网站出现过多的并发,使用户体验更加友好。

此外,预测技术还能有效识别网络营销、网络攻击等行为,帮助企业及时进行防护,避免因攻击行为而带来的财务损失。

显而易见,预测技术在互联网行业具有不可替代的作用,它不仅可以提高企业

的数据开发能力,还能有效分析用户行为,准确预测用户喜好,提升产品研发能力,并且为企业带来更多的营销机会,提升品牌和社会知名度。

综上所述,预测技术是互联网行业发展的重要部分,其重要性实不容忽视。

stata中predict用法Stata中的predict命令是用来生成模型预测值或残差值的。

在进行统计分析时,我们经常需要用到这些值来评估模型的拟合效果或者进行进一步的分析。

本文将介绍predict命令的基本用法和一些常见的选项。

1. 基本语法predict命令的基本语法如下:predict [options] newvar [if] [in], [noinv]其中,newvar是要生成的新变量的名称,if和in是用来限定样本范围的条件,noinv表示不反转二元哑变量。

例如,我们可以使用以下命令生成一个新变量yhat,它是根据模型预测得到的y的值:regress y x1 x2predict yhat2. 常用选项predict命令有多种选项可以控制预测值或残差值的生成方式。

以下是一些常见的选项:(1)residuals:生成残差如果我们想得到模型的残差值,可以在predict命令后面加上residuals选项,如下所示:regress y x1 x2predict res, residuals这样就可以生成一个新变量res,它是根据模型计算得到的y的残差值。

(2)standardized:生成标准化预测值或残差值如果我们希望得到标准化的预测值或残差值,可以在predict命令后面加上standardized选项,如下所示:regress y x1 x2predict yhat_std, standardized这样就可以生成一个新变量yhat_std,它是根据模型计算得到的y的标准化预测值。

(3)xb:生成线性预测值如果我们想得到线性预测值,可以在predict命令后面加上xb 选项,如下所示:regress y x1 x2predict yhat_lin, xb这样就可以生成一个新变量yhat_lin,它是根据模型计算得到的线性预测值。

(4)stdp:生成标准化的完全预测偏差如果我们希望得到标准化的完全预测偏差,可以在predict命令后面加上stdp选项,如下所示:regress y x1 x2predict yhat_stdp, stdp这样就可以生成一个新变量yhat_stdp,它是根据模型计算得到的标准化的完全预测偏差。

![健康经济学(巴塔查里亚 曹乾)课后判断题 答案 (9)[2页]](https://imgs-1438308264.cos.ap-hongkong.myqcloud.com/6c201da7e518964bce847ca9.webp)

10Adverse Selection in Real MarketsComprehension QuestionsIndicate whether the statement is true,false,or unclear,and justify your answer. Be sure to cite evidence from the chapter and state any additional assumptions you may need.1.One of the major predictions of the Rothschild-Stiglitz model is a positivecorrelation between risk and insurance coverage.This has never been ob-served in practice due to the confounding influence of moral hazard.FALSE.This is a prediction of the Rothschild-Stiglitz model,but it has been confirmed in several contexts,including Dutch families seeking supplemen-tal private insurance(van de Ven and van Vliet1995)and young graduates joining the American workforce(Cardon and Hendel2001).2.On average,observed mortality rates are higher for people who buy life in-surance than for people who do not.This is best taken as evidence in favor of adverse selection in life insurance markets.TRUE.He(2009)finds that this is the case,although other studies of life insurance come to opposite conclusions.3.In some markets,adverse selection develops over time as customers learnabout their own risk levels.TRUE.This makes sense,because adverse selection relies on asymmetric in-formation.This phenomenon is in evidence in the Israeli car insurance mar-ket(Cohen2005).12|Health Economics Answer Key4.Although afirm prediction of Akerlof’s model,the adverse selection deathspiral has never been observed in practice.FALSE.Cutler and Reber(1998)find evidence of an adverse selection death spiral at Harvard,and evidence of other death spirals has been observed in insurance markets in New Jersey and California.5.Ex post risk is typically much lower than ex ante risk because uncertainty islargely eliminated by the purchase of an insurance contract.FALSE.Ex-post risk is greater than ex-ante risk due to moral hazard.Having health insurance encourages people to take more risks and consume more health care.6.Cawley and Philipson(1999)find that in life insurance markets,there isa bulk discount(that is,people buying larger policies pay lower per unitprices).They conclude that thisfinding is inconsistent with the Rothschild-Stiglitz model.TRUE.The Rothschild-Stiglitz model predicts bulk markups in markets with asymmetric information.7.Consider an HIV patient who recently started HAART therapy and whosehealth is improving rapidly as a result.Viatical settlementfirms will offer him more money for his life insurance policy than they would have before he started HAART because his health outlook is much better.FALSE.If he is healthier,his life insurance policy is less valuable to viatical firms.8.The fact that high-risk customers are usually less risk-averse than low-riskcustomers helps counteract adverse selection.TRUE.If low-risk customers are more risk averse and tend to demand more insurance,this is an example of advantageous selection that counteracts ad-verse selection.c Bhattacharya,Hyde&Tu20132。

金融预测模型的使用教程金融预测模型是一种通过数据分析和统计方法,对金融市场的未来走势进行预测的工具。

在金融领域,预测模型的应用十分广泛,可以帮助机构和个人做出更明智的投资决策。

本教程将介绍金融预测模型的基本原理和常用方法,以及如何运用这些模型进行金融预测。

一、金融预测模型简介金融预测模型是一种用来预测金融市场变化的数学和统计模型。

其基本原理是通过分析历史数据和相关变量,建立一个数学模型,然后利用这个模型来预测未来的市场走势。

早期的金融预测模型主要基于经验和直觉,随着数据分析和计算机技术的发展,现代金融预测模型变得更加精确和可靠。

二、常用的金融预测模型1. 时间序列模型:时间序列模型是基于历史数据的统计模型,通过分析过去的数据来预测未来的走势。

常见的时间序列模型包括ARIMA模型、GARCH模型等。

ARIMA模型是一种常用的自回归移动平均模型,适用于具有平稳性和可预测趋势的时间序列数据。

GARCH模型用于分析资产收益率的波动性,可以预测风险。

2. 神经网络模型:神经网络模型是一种模仿人脑神经系统工作方式的模型。

它通过输入历史数据和相关变量,训练神经网络来预测未来的市场走势。

常见的神经网络模型包括前馈神经网络和循环神经网络。

前馈神经网络适合处理非时序数据,而循环神经网络适合处理时间序列数据。

3. 支持向量机模型:支持向量机模型是一种基于统计学习理论的模型,可以用于分类和回归问题。

在金融预测中,支持向量机模型常用于预测股票价格和汇率等连续性变量。

它通过训练一个分类器或回归器来寻找最佳的划分边界或拟合曲线。

4. 回归模型:回归模型是一种用来建立变量之间关系的模型,可以用于预测一个变量的值。

在金融预测中,回归模型常用于预测股票价格和市场指数等连续性变量。

常见的回归模型包括线性回归模型和多元回归模型。

线性回归模型假设变量之间服从线性关系,而多元回归模型考虑了多个变量对因变量的影响。

三、使用金融预测模型的步骤1. 收集和准备数据:首先,收集与预测目标相关的历史数据和其他相关变量。