普华永道——金融保险 (PWC-Vivian, Contact020930)

- 格式:xls

- 大小:41.50 KB

- 文档页数:2

普华永道会计师事务所公司介绍普华永道(Price Waterhouse Coopers)是四大国际会计师事务所之一,主要服务领域包括审计、税务、人力资源、交易、危机管理等。

普华永道通过制定解决方案及提供实用性意见,不断为客户及股东提升价值。

普华永道致力于提供切合各行业所需要的审计、税务及谘询服务,以提升客户的价值。

普华永道在154 个国家和地区超过161,000 人的专业团队所组成的全球网络内,对22个行业进行专业研究,分享其思维成果,行业经验和解决方案,并为客户开拓新视野及提供实用的建议。

主要业务:1、保证及企业咨询服务。

具体包括:财务报表审计、石油行业价值证分析、全球扩展及私有化、内部控制服务、内部审计服务、风险管理、外包服务等;2、商业程序外包。

具体包括:财务及会计、应用流程、采购、人力资源、不动产管理等;3、财务咨询服务。

具体包括:企业重组服务、致力于有形及无形资产评估等的公司价值咨询服务等;4、全球人力资源。

具体包括:全球人力资源解决方案、人力资源咨询支持等;5、管理咨询服务。

具体包括:公司战略、技术战略、组织战略、经营战略、改造战略等。

客户中25%为大型企业,30%为中型企业,45%为小客户、私人企业、非营利组织、公共机构。

主要国际客户有埃克森、IBM、日本电报电话公司、强生公司、高盛集团、美国电报电话公司、英国电信、戴尔电脑、福特汽车、雪佛莱、康柏电脑和诺基亚等。

主要中国客户有江苏五星电器有限公司、中国建设银行、中国银行、中国石油、中钢集团、中国铝业、中煤集团、中国联通、中国国家开发银行、华能国际、大唐电力、Chevron、民生银行、中国人寿、东方资产管理公司、中国邮政、中国交通建设集团、新浪网、网易、搜狐、东方航空、京东网上商城等。

普华永道中国大陆、香港、台湾及新加坡事务所已根据各地适用的法律协作运营。

整体而言,员工总数逾14,000人,其中包括逾620名合伙人。

分布于以下城市:北京、香港、上海、新加坡、台北、重庆、中坜、大连、广州、杭州、新竹、高雄、澳门、南京、宁波、青岛、深圳、苏州、台中、台南、天津、厦门及西安。

普华永道会计师事务所普华永道会计师事务所(Price Waterhouse Coopers 或PWC,香港称作罗兵咸永道,俗称水记或水房,台湾的PWC称为资诚)是世界最大的专业服务机构。

它是普华(Price Waterhouse)和永道(Coopers&Lybrand)于1998年合并而成。

普华永道和毕马威(KPMG)、安永(Ernst&Young)以及德勤(DeloitteToucheTohmatsu)合称为四大国际会计师事务所。

一.历史沿革关于普华(Price Waterhouse)1849年,普里斯(Samuel Price)在伦敦开始了其会计师生涯。

1865年,普里斯与威廉•豪里兰德(William Holyland)及埃德温•华特豪斯(Edwin Waterhouse)建立了合伙制的会计师事务所,豪里兰德在此之后很快退出。

1874年,该事务所被命名为普里斯•华特豪斯公司(Price, Waterhouse&Co.)。

到19世纪晚期,普华作为一家会计师事务所已经取得了广泛的认可。

为了应对英国和美国之间快速发展的贸易关系,在1890年,普华在纽约开办了一家分所。

美国分所在此之后进行了高速扩张。

同时,原有的英国事务所也在不列颠帝国内部的主要国家不断开办新的事务所。

在每个国家都建立了独立的关系,这样就给予了当地合伙人扩张本地业务的强烈冲劲。

这样,普华在全世界的扩张不是通过国际范围的合并重组,而是通过建立合作关系的联盟完成的。

关于永道(Coopers&Lybrand)与普华一样,永道同样可以起源于19世纪。

在1854年,威廉•库珀(William Cooper)在伦敦建立了自己的会计师事务所。

七年后,库珀的其他三个兄弟也加入了这家事务所,于是便改称“库珀兄弟会计师事务所”(Cooper Brothers)。

在1898年,罗伯•H•蒙哥马利(Rober H. Montgomery), 威廉•M•莱布兰德(William M. Lybrand),小亚当•A•罗斯(Adam A. Ross)和他的兄弟爱德华•罗斯在美国成立了莱布兰德-罗斯兄弟-蒙哥马利会计师事务所(Lybrand,Ross Brothers and Montgomery)。

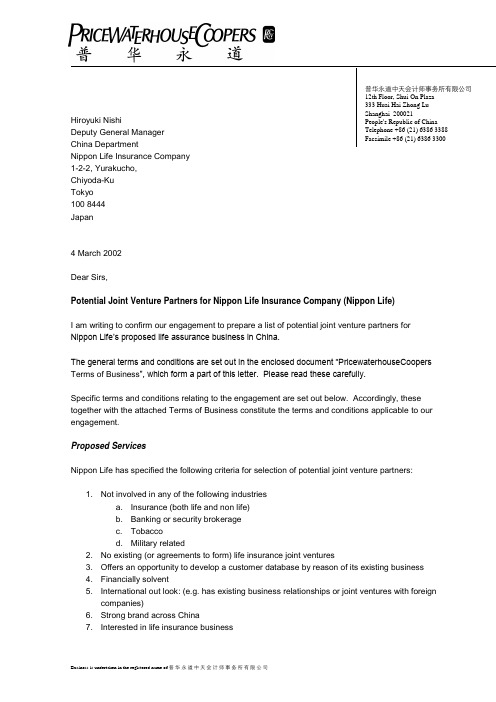

普华永道中天会计师事务所有限公司 12th Floor, Shui On Plaza 333 Huai Hai Zhong Lu Shanghai 200021 People's Republic of China Telephone +86 (21) 6386 3388 Facsimile +86 (21) 6386 3300Hiroyuki NishiDeputy General ManagerChina DepartmentNippon Life Insurance Company1-2-2, Yurakucho,Chiyoda-KuTokyo100 8444Japan4 March 2002Dear Sirs,Potential Joint Venture Partners for Nippon Life Insurance Company (Nippon Life)I am writing to confirm our engagement to prepare a list of potential joint venture partners for Nippon Life’s proposed life assurance business in China.The general terms and conditions are set out in the enclosed document “PricewaterhouseCoopers Terms of Business ”, which form a part of this letter. Please read these carefully.Specific terms and conditions relating to the engagement are set out below. Accordingly, these together with the attached Terms of Business constitute the terms and conditions applicable to our engagement.Proposed ServicesNippon Life has specified the following criteria for selection of potential joint venture partners:1. Not involved in any of the following industriesa. Insurance (both life and non life)b. Banking or security brokeragec. Tobaccod. Military related2. No existing (or agreements to form) life insurance joint ventures3. Offers an opportunity to develop a customer database by reason of its existing business4. Financially solvent5. International out look: (e.g. has existing business relationships or joint ventures with foreigncompanies)6. Strong brand across China7. Interested in life insurance businessWe will perform the following work•First, using our knowledge of companies in China, we will conduct a general company search and screening out the companies based on the criteria 1 to 2 above to produce along list of companies.•Second, from the long list of companies, we will research and sort out a list of 20 companies (10 state owned and 10 non-state owned) that satisfy criteria 4 to 6 above. We will include in this list the companies already selected by Nippon Life. This list will not bebased on a review of all likely companies in China but will be derived from our knowledge of the market. The list will not therefore be exhaustive nor will it necessarily include the 20 best companies meeting the criteria 4 to 6 above.•Third, we will make an assessment of the 20 listed companies’ scores, on a scale of 1 to 10, against each of the criteria 4 to 6 above. This assessment will be based on publiclyavailable information and discussion, where possible, with the company management.Specifically, we will rely on such information for our assessment of financial solvency and this analysis will necessarily be high level and will not be a substitute for appropriate duediligence which would be undertaken before entering into any form of commitments withthe company concerned.•We will make direct contact with the company and attempt to gauge their interest in a life insurance joint venture with a foreign company. We will not reveal the identity or nationality of Nippon Life. Accordingly, any expression of interest may not be continued if furtherdiscussions take place. We will estimate their interest, from the conversation with them, as “strong”, “neutral”,“slightly” or “not interested”.•We will list all 20 companies in our report with the results of our assessment, including whether or not each is interested in a life insurance joint venture.Your responsibilityThe overall definition and scope of the work to be performed is your responsibility. You bear final responsibility for the adequacy of the scope of the work for your purposes.ReportWe will provide a report in the form of a tabular summary of our analysis together with commentary as necessary. Our report will be provided in English. We will provide a draft of our report for your comments.TimetableWe will provide our draft report 5 weeks after signature of this engagement letter and the payment of the initial fee (see below).MeetingsAll meetings in connection with this assignment between Nippon Life and us will take place in Shanghai.Our TeamOur team will be led by David Campbell, who will have overall responsibility for the project. Saito Tsuyoshi will be responsible for liaison with you during the course of the project. The team members will be Ying Xiao, Freddy Zhou, Ma Lei and Connie Gu.FeesOur fee will be US$30,000inclusive of all associated taxes. We will charge out-of-pocket expenses in addition. Out of pocket expenses will not exceed US$3000.We anticipate the need to purchase financial information on some of the list of 20 companies. Such purchases will be made only with prior agreement with Nippon Life to meet the cost, which will be in addition to our fees and out of pocket expenses.If the scope changes due to conditions outside our control, or a requirement for additional work arises, creating a variance in the estimated fee, we will notify you immediately to discuss and agree this with you. Prior to commencing any additional piece of work, which is not currently included in the scope of this assignment, we will provide and agree with you a revised scope and fee estimate.Fees will be payable as followsOn signature of engagement letter US$10,000On delivery of draft report US$10,000On completion of the assignment US$10,000 plus expensesFees and expenses will be due and payable on presentation. In the event of early cancellation of the project by Nippon Life, the full fee of US$30,000 plus expenses will become due immediately.Non-exclusivityNippon Life acknowledges that PricewaterhouseCoopers are not by reason of this engagement prevented or restricted from working on behalf of any other entity in relation to the business of Nippon Life. We will take steps to ensure that confidential information communicated to us in the course of this engagement will be maintained confidentially.Reliance and limitation on adviceWe will rely on publicly available data. We will take reasonable steps to verify the consistency, completeness and accuracy of the data but these steps will not be sufficient to completely confirm the accuracy of the data. Accordingly we take no responsibility for the accuracy or completeness of the information on which our assessment is based.It is the responsibility of Nippon Life to ensure it understands and takes into account the effect of this, and any other significant limitations and uncertainties, in any use to which it puts our Services and deliverables. We take no responsibility for any decisions which Nippon Life or third parties may take based on its use of our Services and deliverables for this engagement.Third PartiesOur work will be conducted for the sole use and benefit of Nippon Life. Unless required by law, no copy of or extract from our deliverables is to be distributed to third parties without our prior written consent. Third party recipients may not further distribute the deliverables without our prior written consent. No oral or written reference to the content of the deliverables may be made by Nippon Life or by any third party recipients to any other parties without our prior consent. We may at our discretion grant or withhold our consent under this paragraph or grant it subject to conditions.IndemnityAs a condition of our engagement we require Nippon Life to indemnify PricewaterhouseCoopers, its partners and employees for any claims or loss whatsoever which arise from or in relation to information provided to us by Nippon Life which may be incomplete, false, misleading or in any way inaccurate.We also draw your attention to section 7.7 of the Terms of Business attached which requires Nippon Life to indemnify PricewaterhouseCoopers, its partners and employees for any claims or losses whatsoever incurred as a result of a claim by a third party in connection with the provision of the Services or in connection with any use by you of any Deliverables provided by PwC under this contract.LiabilityIn accordance with Section 7.2 of the Terms of Business attached, the liability of PricewaterhouseCoopers, its partners and staff for loss or damage arising from or in relation to this engagement, whether arising from breach of contract, tort or otherwise, shall be limited to a reimbursement of the fees charged.Acceptance of terms of agreementShould you be in agreement with the scope, timetable and fees set out in this letter, please sign this letter and return it to us as confirmation of the engagement and acceptance of our standard Terms of Business which are also attached.Yours sincerely,____________________________________David CampbellPartner PricewaterhouseCoopersSigned for and on behalf of Nippon Life as confirmation of agreement with the scope and the terms and conditions set out in this letter.Name:______________________________ Signature:_______________________________ The signatory warrants that he or she has the authority to sign for and on behalf of Nippon Life.Position:______________________________Date:_________________________________。

四大指什么公司

金融方面的四大指的是四大会计师事务所,即普华永道(PwC)、德勤(DTT)、毕马威(KPMG)、安永(EY)。

1.普华永道(PwC):

由原来的普华国际会计公司(Price Waterhouse)和永道国际会计公司(Coopers & Lybrand)于1998年7月1日合并而成。

2.德勤(DTT):

德勤总部位于美国纽约,早在1917年,德勤已认识到中国的商机。

在上海成立办事处,成为首家在这个动感及繁荣的大城市开设分支机构的外国会计师事务所。

3.毕马威(KPMG):

毕马威(KPMG)是一家网络遍布全球的专业服务机构,专门提供审计、税务和咨询等服务。

毕马威国际合作组织(“毕马威国际”)瑞士实体由各地独立成员组成,但各成员在法律上均属分立和不同的个体。

现毕马威中国在北京、上海、沈阳、南京、杭州、福州、厦门、青岛、广州、深圳、成都、重庆、天津、佛山、香港特别行政区和澳门特别行政区共设有十六家机构(包括毕马威企业咨询(中国)有限公司)。

4.安永(EY):

安永早于1973年在香港设立办事处,1981年成为最早获中国政府批准在北京设立办事处的国际专业服务公司。

1992年,安永在北京成立安永华明会计师事务所。

目前,安永在中国拥有超过6500名专业人员,北京、香港、上海、广州、深圳、大连、武汉、成都、苏州、沈阳及澳门均设有分所。

四大会计师事务所组织结构四大会计师事务所是指世界上四家最大、最著名的会计师事务所,它们分别是普华永道、德勤、安永和毕马威。

这些会计师事务所在全球范围内提供各种专业服务,包括审计、税务、咨询和企业风险管理等。

它们的组织结构如下:一、普华永道(PwC)普华永道是全球最大的会计师事务所之一,总部位于英国伦敦。

普华永道的组织结构由全球董事会、全球执行委员会以及各个地区和行业的负责人组成。

全球董事会负责制定公司的发展战略和政策,全球执行委员会则负责执行和监督各项业务。

普华永道的服务范围包括审计、税务、咨询和企业风险管理等,通过各个业务线的合作,为客户提供全方位的专业服务。

二、德勤(Deloitte)德勤是全球第二大的会计师事务所,总部位于美国纽约。

德勤的组织结构分为全球董事会、全球执行委员会、各个国家和地区的管理层以及各个业务线的负责人。

全球董事会负责制定公司的战略和政策,全球执行委员会则负责执行和监督各项业务。

德勤的服务范围包括审计、税务、咨询和风险管理等,通过全球网络和专业团队的协作,为客户提供高质量的专业服务。

三、安永(EY)安永是全球第三大的会计师事务所,总部位于英国伦敦。

安永的组织结构由全球合伙人大会、全球执行委员会以及各个地区和行业的负责人组成。

全球合伙人大会负责制定公司的策略和政策,全球执行委员会则负责执行和监督各项业务。

安永的服务范围包括审计、税务、咨询和企业风险管理等,通过全球一体化的工作方式,为客户提供创新的专业服务。

四、毕马威(KPMG)毕马威是全球第四大的会计师事务所,总部位于荷兰阿姆斯特丹。

毕马威的组织结构由全球合伙人大会、全球执行委员会以及各个国家和地区的管理层组成。

全球合伙人大会负责制定公司的战略和政策,全球执行委员会则负责执行和监督各项业务。

毕马威的服务范围包括审计、税务、咨询和风险管理等,通过跨国团队的合作,为客户提供高效的专业服务。

总结起来,四大会计师事务所在全球范围内拥有庞大的组织结构和专业团队,能够为各类企业提供全方位的专业服务。

目录应届生求职网简介 (2)第一章、普华永道(Pwc)简介 (5)1.1普华永道概况 (5)1.2普华永道企业文化 (6)1.3普华永道生涯管理 (6)1.4普华永道与中国 (8)第二章、普华永道(Pwc)笔试资料 (9)2.1普华永道2010校园招聘笔试资料 (9)2.1.1普华永道2010笔试总结 (9)2.1.2在清华大学考场的普华永道笔试经历 (11)2.1.3在上海财大考场的普华永道笔试,充满血泪啊 (12)2.1.4普华永道2010完整笔经倾情奉献 (14)2.1.5普华永道上海外贸学院笔经 (14)2.1.6普华永道笔经,攒人品,有详细tips (14)2.1.7北京普华永道笔经&tips (16)2.1.8普华永道上海笔试归来 (17)2.1.9曲折的普华永道笔试 (18)2.1.10普华永道笔经分享,很详细 (20)2.1.11普华永道济南超详细笔经攒rp~~ (21)2.1.12普华永道笔试准备 SHL+托福作文 (22)2.2普华永道2008-2009校园招聘笔试资料 (22)2.2.1 普华永道笔试作文题库分类 (22)2.2.2普华永道清华详细笔经 (23)2.2.3普华永道天津详细笔经(天大考点) (24)2.2.4积累人品,普华永道北京林大笔经 (25)2.2.5上海普华永道笔经新鲜出炉 (26)2.2.6普华永道青岛笔经总结 (26)2.2.7语言推理技巧,很有用 (27)第三章、普华永道(Pwc)面试资料 (33)3.1普华永道2010校园招聘群面(AC面)面经 (33)3.1.1普华永道北京所AC面面经 (33)3.1.2普华永道上海所AC面面经 (35)3.1.3普华永道广州所AC面面经 (37)3.1.4伴着武汉的大雪,一起分享 PwC的 AC经历 (37)3.1.5上海所Audit AC面面经 (39)3.1.6普华永道AC面总结望能帮助后来人 (40)3.1.7【回报贴】北京所assurance AC面新鲜面经 (41)3.1.8普华永道AC面经验分享,攒RP! (42)3.1.9普华永道上海所Advisory valuation AC面经 (43)3.1.10 PwC AC面经,攒rp啊!! (43)3.2普华永道2009校园招聘群面(AC面)面经 (45)3.2.1我的普华AC面经,非常详细 (45)第一章、普华永道(Pwc)简介1.1普华永道概况普华永道官方网站公司介绍普华永道()是全球最具规模的专业服务机构之一。

中国四大会计师事务所的名称中国四大会计师事务所,分别是普华永道、德勤、安永和毕马威。

这四家会计师事务所在中国具有较高的知名度和影响力,为国内外客户提供全方位的专业服务。

普华永道(PwC)是全球领先的专业服务机构之一,总部位于伦敦。

普华永道在中国的历史可以追溯到1913年,如今已经成为中国市场的重要参与者和合作伙伴。

普华永道的服务范围广泛,包括审计、税务、咨询等领域,为客户提供专业的解决方案和战略建议。

德勤(Deloitte)是全球四大会计师事务所之一,总部位于纽约。

德勤在中国的历史可以追溯到1917年,如今已经在中国建立了全国性的服务网络。

德勤以其专业的团队和全球化的资源,为中国企业提供包括审计、咨询、税务、风险管理等多领域的综合服务。

安永(EY)是全球四大会计师事务所之一,总部位于伦敦。

安永在中国的历史可以追溯到1917年,如今已经在中国拥有20多个办公室和上万名员工。

安永以其专业的团队和全球一体化的服务模式,为中国企业提供审计、咨询、税务等全方位的专业服务。

毕马威(KPMG)是全球四大会计师事务所之一,总部位于阿姆斯特丹。

毕马威在中国的历史可以追溯到1898年,如今已经在中国拥有多个办公室和上千名员工。

毕马威以其专业的团队和全球化的服务网络,为中国企业提供审计、税务、咨询等多领域的专业服务。

四大会计师事务所作为全球专业服务机构的代表,在中国市场扮演着重要的角色。

无论是国内企业还是跨国公司,都可以从这些会计师事务所的专业服务中受益。

审计是这四大会计师事务所的核心业务之一,通过对企业财务报表的审查,确保其真实、准确和合规。

税务咨询是另一个重要的服务领域,帮助企业合理规划税务策略,降低税务风险。

此外,这些会计师事务所还提供咨询服务,包括战略咨询、财务咨询、风险管理等,为企业提供全方位的解决方案。

四大会计师事务所在中国的发展与中国经济的快速增长密切相关。

随着中国经济的不断发展,企业对于财务报表的准确性和透明度要求越来越高,这就为会计师事务所提供了更多的机会和挑战。

普华永道主要(zhǔyào)服务项目及企业(qǐyè)普华永道提供咨询(zīxún)、审计和税务服务,主要(zhǔyào)服务项目(xiàngmù)包括:1. 审计服务财务报告审计、精算服务、合规性报告、萨班斯-奥克斯利法案合规、国际财务报告准则、内部审计、公司财务报告提升、可持续性报告、独立控制和系统流程审计等;2. 税务服务中国税务、信托和私人客户服务、国际税务、个人税务管理、兼并与收购、合规服务和转让定价等;3. 咨询服务我们的咨询服务致力为客户解决策略性以至日常营运的问题,并为客户实践他们的商业战略,服务内容涉及:战略、运营、风险、法务鉴证、人才与转变、科技、财务和估值等,在内部审计、风险管理、公司治理、内部控制和合规管理、信息安全和技术风险管理等方面提供专业广泛的解决方法。

普华永道主要的服务(fúwù)客户包括:房地产业(fánɡ dì chǎn yè):中国国际贸易中心、远洋地产控股(kònɡ ɡǔ)有限公司、首创置业股份(gǔfèn)有限公司、北京北辰(běichén)实业股份有限公司、领汇房地产投资信托基金、上海世茂股份有限公司、和记黄埔有限公司、合生创展集团有限公司、嘉里建设有限公司、新世界中国地产有限公司、广州富力地产股份有限公司、越秀投资有限公司、新世界发展有限公司、凯德置地集团、碧桂园集团、太古地产有限公司、广西阳光股份有限公司、嘉华国际集团有限公司金融机构服务:中国工商银行、中国农业银行、中国建设银行、中国银行、交通银行国家开发银行、中国进出口银行、北京银行、上海浦东发展银行、汇丰银行、德意志银行、法国巴黎银行、花旗银行、美洲银行、荷兰银行、瑞信、高盛集团、摩根大通集团、国泰君安证券股份有限公司、申银万国证券股份有限公司、中国国际金融有限公司、香港交易及结算所有限公司、博时基金管理有限公司、宝盈基金管理有限公司、长盛基金管理有限公司、国泰基金管理有限公司、嘉实基金管理公司、华夏基金管理有限公司、中国人寿保险股份有限公司、中国再保险公司、新华人寿保险股份有限公司、华泰保险集团股份有限公司、美国国际集团、瑞士苏黎世保险公司、慕尼黑再保险公司、大众汽车金融(中国)有限公司科技、通讯(tōngxùn)信息、娱乐及媒体行业:中国联通股份(gǔfèn)有限公司、中国网通集团(jítuán)(香港)有限公司(yǒu xiàn ɡōnɡ sī)、完美(wánměi)时空有限责任公司、中国民航信息网络股份有限公司、海湾安全技术有限公司、上海盛大网络发展有限公司、上海第九城市信息技术有限公司、网易公司、新浪公司、搜狐公司、TOM在线有限公司、晶澳太阳能有限公司、如家酒店连锁、携程旅行网、IBM中国有限公司、诺基亚(中国)投资有限公司、三星(中国)投资有限公司、爱立信(中国)通信有限公司、索尼爱立信移动通信产品(中国)有限公司、乐金电子中国有限公司、诺基亚西门子通信有限公司、AT&T(中国)有限公司、麦肯光明广告有限公司、索尼(中国)有限公司能源及公共事业:中国石油天然气股份有限公司、中国中煤能源股份有限公司、壳牌、雪佛龙、埃克森美孚公司、中国铝业股份有限公司、五矿资源有限公司、华能国际电力股份有限公司、大唐国际发电股份有限公司、中电控股有限公司、中国电力国际发展有限公司、广东电力发展股份有限公司、中国中钢集团公司私募基金(jījīn):Affinity集团(jítuán)、贝恩资本(zīběn)、凯雷投资(tóu zī)集团、CVC资本(zīběn)、TPG集团华平投资集团、Cerberus美林证券、摩根士丹利、老虎基金、红杉资本、蓝山投资、弘毅投资、鼎辉投资、新天域资本、中信资本、九鼎投资、今日资本集团、渤海产业投资基金、崇德投资、中国平安信托投资有限公司零售及消费品行业:宝洁(中国)有限公司、欧莱雅(中国)有限公司、历峰集团(Richemont)、安海斯-布希公司、乐购、可口可乐、沃尔玛(中国)投资有限公司、和记黄埔有限公司、太古股份有限公司、思捷环球控股有限公司、利丰投资有限公司、百丽国际控股有限公司、联想集团有限公司、苏宁电器、青岛啤酒股份有限公司、恒安国际集团有限公司、中国动向 (集团)有限公司、李宁有限公司、统一企业中国控股有限公司、新世界百货中国有限公司、中国旺旺控股有限公司运输(yùnshū)和物流业:德国铁路(tiělù)公司、加拿大太平洋铁路公司(ɡōnɡ sī)、敦豪快递(kuài dì)服务公司荷皇天(huánɡ tiān)地有限公司、日本邮船株式会社、长荣海运股份有限公司、香港泛亚班拿有限公司、丹沙货运、美商恒运国际货运有限公司、美国总统轮船公司、中国远洋控股股份有限公司、中海集装箱运输股份有限公司、广深铁路股份有限公司、大秦铁路股份有限公司、中国外运股份有限公司、北京首都国际机场股份有限公司、厦门国际港务股份有限公司、天津港股份有限公司、上海国际机场股份有限公司、深圳高速公路股份有限公司、中外运航运有限公司、招商局国际有限公司中远太平洋有限公司、越秀交通有限公司、东方海外(国际)有限公司保昌控股有限公司、新创建集团有限公司、内容总结(1)普华永道主要服务项目及企业普华永道提供咨询、审计和税务服务,主要服务项目包括:审计服务财务报告审计、精算服务、合规性报告、萨班斯-奥克斯利法案合规、国际财务报告准则、内部审计、公司财务报告提升、可持续性报告、独立控制和系统流程审计等。

四大会计事务所是哪四个

四大会计事务所是指全球最大的四家专业服务网络,它们提供审计、税务和咨询服务。

这四家公司因其规模、影响力和全球业务范围而闻名,它们分别是:

1. 普华永道(PwC,PricewaterhouseCoopers):普华永道是一家总部位于伦敦的国际性专业服务网络,由普华(Price Waterhouse)和永道(Coopers & Lybrand)于1998年合并而成。

普华永道在全球范围内拥有广泛的客户群,并提供包括审计、税务和咨询服务在内的多种专业服务。

2. 德勤(Deloitte):德勤是一家总部位于美国纽约的全球性专业服务网络,提供审计、税务、管理咨询、财务咨询、风险咨询、人力资源咨询和财务咨询服务。

德勤在全球范围内拥有众多分支机构,服务于各种规模的企业。

3. 安永(EY,Ernst & Young):安永是一家总部位于英国伦敦的全球性专业服务公司,由恩斯特·惠尼(Ernst & Whinney)和亚瑟·杨(Arthur Young)于1989年合并而成。

安永提供广泛的服务,包括审计、税务、交易和咨询服务。

4. 毕马威(KPMG):毕马威是一家总部位于荷兰阿姆斯特丹的全球性专业服务网络,由毕马威(Klynveld Main Goerdeler)和Peat Marwick于1987年合并而成。

毕马威提供审计、税务和咨询服务,其客户包括许多跨国公司和公共部门组织。

这四大会计事务所因其在全球范围内的广泛影响力和专业服务能力,

常被简称为“四大”。

它们在会计、审计和咨询行业中占据着领导地位,对全球经济和商业环境有着重要的影响。