成本管理会计练习chap06

- 格式:doc

- 大小:38.50 KB

- 文档页数:1

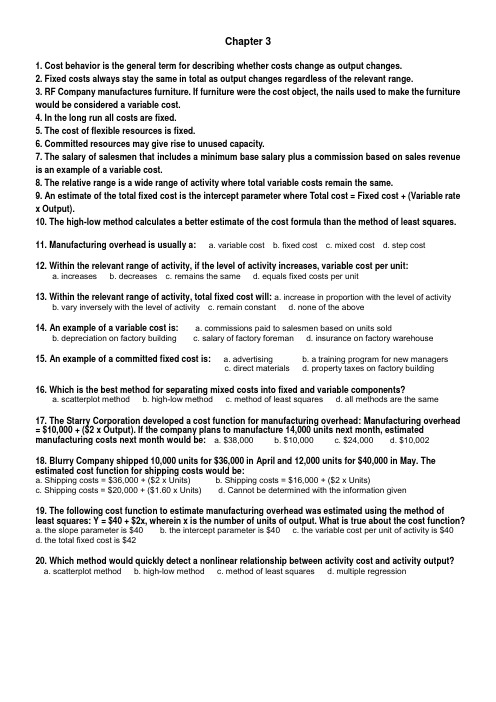

Chapter 31. Cost behavior is the general term for describing whether costs change as output change s.2. Fixed costs always stay the same in total as output change s regardless of the relevant range.3. RF Company manufactures furniture. If furniture were the cost object, the nails used to make the furniture would be considered a variable cost.4. In the long run all costs are fixed.5. The cost of flexible resource s is fixed.6. Committed resource s may give rise to unused capacity.7. The salary of salesmen that include s a minimum base salary plus a commission ba sed on sales revenue is an example of a variable cost.8. The relative range is a wide range of activity where total variable costs remain the same.9. An estimate of the total fixed cost is the intercept parameter where Total cost = Fixed cost + (Variable rate x Output).10. The high-low method calculates a better estimate of the cost formula than the method of least square s.11. Manufacturing overhead is usually a: a. variable cost b. fixed cost c. mixed cost d. step cost12. Within the relevant range of activity, if the level of activity increases, variable cost per unit:a. increasesb. decreasesc. remains the samed. equals fixed costs per unit13. Within the relevant range of activity, total fixed cost will: a. increase in proportion with the level of activityb. vary inversely with the level of activityc. remain constantd. none of the above14. An example of a variable cost is: a. commissions paid to salesmen based on units soldb. depreciation on factory buildingc. salary of factory foremand. insurance on factory warehouse15. An example of a committed fixed cost is: a. advertising b. a training program for new man agersc. direct materialsd. property taxes on factory building16. Which is the be st method for separating mixed costs into fixed and variable components?a. scatterplot methodb. high-low methodc. method of least squaresd. all methods are the same17. The Starry Corporation developed a cost function for manufacturing overhead: Manufacturing overhead = $10,000 + ($2 x Output). If the company plans to manufacture 14,000 units next month, estimated manufacturing costs next month would be: a. $38,000 b. $10,000 c. $24,000 d. $10,00218. Blurry Company shipped 10,000 units for $36,000 in April and 12,000 units for $40,000 in May. The estimated cost function for shipping costs would be:a. Shipping costs = $36,000 + ($2 x Units)b. Shipping costs = $16,000 + ($2 x Units)c. Shipping costs = $20,000 + ($1.60 x Units)d. Cannot be determined with the information given19. The following cost function to estimate manufacturing overhead was estimated using the method ofleast squares: Y = $40 + $2x, wherein x is the number of units of output. What is true about the cost function?a. the slope parameter is $40b. the intercept parameter is $40c. the variable cost per unit of activity is $40d. the total fixed cost is $4220. Which method would quickly detect a nonlinear relationship between activity cost and activity output?a. scatterplot methodb. high-low methodc. method of least squaresd. multiple regression。

成本管理会计试题库(含答案)一、单选题(共40题,每题1分,共40分)1、应列入企业成本、费用的支出项目主要有()。

A、报销差旅费B、支付违约金C、购建生产用设备D、对外投资支出正确答案:A2、在下列指标中,可据以判断企业经营安全程度的指标是()。

A、保本作业率B、贡献毛益C、保本量D、保本额正确答案:A3、下列各项中不属于现金流入量的是()。

A、营业收入B、固定资产投资C、固定资产残值D、流动资金回收正确答案:B4、在简化的分批法下,累计间接费用分配率()。

A、既是各批产品之间,也是完工产品与在产品之间分配间接费用的依据B、只是在各批产品之间分配间接费用的依据C、只是在各批在产品之间分配间接费用的依据D、只是完工产品与在产品之间分配间接费用的依据正确答案:A5、当企业利用剩余生产能力选择生产新产品,而且每种新产品都没有专属成本时,应以()作为选择标准。

A、产销量B、成本C、销售价格D、贡献毛益总额正确答案:D6、采用简化的分批法,在产品完工之前,产品成本明细账()。

A、只登记间接费用,不登记直接费用B、不登记任何费用C、只登记原材料费用D、只登记直接费用和生产工时正确答案:D7、在采用评价指标分析长期投资决策项目财务上的可行性时,如(),投资项目一般可以接受。

A、净现值小于零B、净现值率小于零C、设定的折现率大于内含报酬率D、设定的折现率小于内含报酬率正确答案:D8、下列各项中不属于现金流入的是()A、流动资金回收B、固定资产残值C、营业收入D、固定资产投资正确答案:D9、采用逐步结转分步法,各步骤期末在产品是指()。

A、库存半成品B、广义在产品C、自制半成品D、狭义在产品正确答案:D10、下列各项中,属于无关成本的是()。

A、沉没成本B、增量成本C、专属固定成本D、机会成本正确答案:A11、在进行成本性态分析时,历史资料分析法中最为简便易行的方法是()。

A、散布图法B、高低点法C、回归直线法D、直接分析法正确答案:B12、半成品立即出售或继续加工的决策,一般可将继续加工后预期可增加的收入与进一步加工需追加的成本进行比较,若前者()后者,说明进一步加工的方案较优。

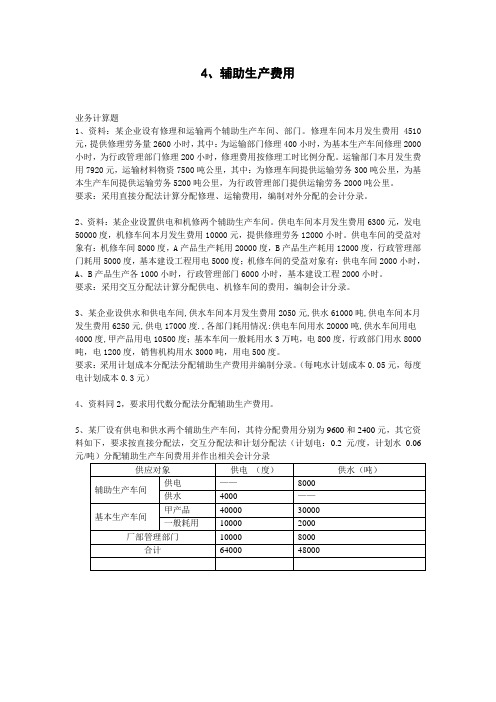

4、辅助生产费用业务计算题1、资料:某企业设有修理和运输两个辅助生产车间、部门。

修理车间本月发生费用4510元,提供修理劳务量2600小时,其中:为运输部门修理400小时,为基本生产车间修理2000小时,为行政管理部门修理200小时,修理费用按修理工时比例分配。

运输部门本月发生费用7920元,运输材料物资7500吨公里,其中:为修理车间提供运输劳务300吨公里,为基本生产车间提供运输劳务5200吨公里,为行政管理部门提供运输劳务2000吨公里。

要求:采用直接分配法计算分配修理、运输费用,编制对外分配的会计分录。

2、资料:某企业设置供电和机修两个辅助生产车间。

供电车间本月发生费用6300元,发电50000度,机修车间本月发生费用10000元,提供修理劳务12000小时。

供电车间的受益对象有:机修车间8000度,A产品生产耗用20000度,B产品生产耗用12000度,行政管理部门耗用5000度,基本建设工程用电5000度;机修车间的受益对象有:供电车间2000小时,A、B产品生产各1000小时,行政管理部门6000小时,基本建设工程2000小时。

要求:采用交互分配法计算分配供电、机修车间的费用,编制会计分录。

3、某企业设供水和供电车间,供水车间本月发生费用2050元,供水61000吨,供电车间本月发生费用6250元,供电17000度.,各部门耗用情况:供电车间用水20000吨,供水车间用电4000度,甲产品用电10500度;基本车间一般耗用水3万吨,电800度,行政部门用水8000吨,电1200度,销售机构用水3000吨,用电500度。

要求:采用计划成本分配法分配辅助生产费用并编制分录。

(每吨水计划成本0.05元,每度电计划成本0.3元)4、资料同2,要求用代数分配法分配辅助生产费用。

5、某厂设有供电和供水两个辅助生产车间,其待分配费用分别为9600和2400元,其它资料如下,要求按直接分配法,交互分配法和计划分配法(计划电:0.2元/度,计划水0.06元/吨)分配辅助生产车间费用并作出相关会计分录5、制造费用的核算一、名词解释1、制造费用2、生产工时比例法3、生产工资比例法4、机器工时比例法5、按年度计划分配率分配法二、问答题1、什么是制造费用?制造费用一般应包括哪些项目?2、季节性生产企业分配制造费用为什么适宜采用按年度计划分配率分配法?3、说明按年度计划分配率分配法的特点、适用范围和优缺点。

(精编)成本管理会计相关练习题成本管理会计练习题一、名词解释1.经济订货批量2.概率预算3.内部转移价格4.零基预算5.分批成本法6.约当产量比例法7.机会成本8.成本还原9.安全边际10.变动成本计算法11.财务预算12.经济附加值13.直接成本14.产品成本15.直接分配法16.标准成本17.剩余收益18.平行结转分步法19.约当产量比例法二、单项选择题1.下列各项中,其计算结果不等于变动成本率的是()。

A.1-边际贡献率B.1-达到保本点的作业率C.单位变动成本/单价*100% D.变动成本/销售收入*100%2.在变动成本计算法下,产品成本中不包括()。

A.直接材料B.直接人工C.变动制造费用D.固定制造费用3.已知某产品的销售利润率为16%,安全边际率为40%,边际贡献率为()。

A.40% B.6.4%C.2.5% D.56%4.以下说法不正确的是()。

A.没有期初、期末存货的情况下,按完全成本计算法计算的损益与按变动成本计算法计算的损益相等B.没有期初存货、但有期末存货的情况下,按完全成本计算法计算的损益小于按变动成本计算法计算的损益C.在有期初存货、但没有期末存货的情况下,按完全成本计算法计算的损益小于按变动成本计算法计算的损益D.即使期初存货与期末存货数量相等,按完全成本计算法计算的损益与按变动成本计算法计算的损益也不一定相等5.如果所制定的标准成本符合企业的实际情况,且成本差异不大,()。

A.每月的成本差异按标准成本的比例在销售成本、产成品和在产品之间分摊B.每月将成本差异全部结转到销售成本中去C.成本差异累积到年终时,按比例分摊到销售成本、产成品和在产品成本D.成本差异累积到年终时,全部结转到销售成本上去6.在生产设备最优利用的决策中,关键是计算分析不同类型设备之间产品加工批量的()。

A.最优生产批量B.生产准备成本C.储存成本D.成本平衡点7.产品或劳务处于完全的市场竞争条件下,并有客观的市价可供采用,各责任中心之间转让的产品或劳务应()。

成本管理会计练习chap08Chapter 81. Managers use budgeting as a planning tool rather than asa control tool.2. Control involves identifying objectives and identifying actions needed to achieve the objectives.3. A continuous budget requires managers to continuously update the budget to include new information.4. The usual starting point in budgeting is to make forecasts of sales.5. The budgeted income statement is an operating budget.6. The production budget is usually prepared before the direct labor budget.7. The overhead budget includes direct materials and direct labor.8. An ideal budgetary system creates goal incongruence.9. Managers should be responsible for controllable costs.10. The performance evaluation of managers should be based solely on financial measures from the budget.11. What is an advantage of budgeting? a. budgets do not force managers to plan b. budgets provide information that can be used for decision making c. budgets promote independence and secrecy d. budgets do not provide a basis for control12. Budgets are both planning and control tools. Which of the following is a planning tool activity?a. identifying objectivesb. comparing actual results with planned amountsc. taking corrective action if neededd. all of the above are planning tool activities13. The master budget includes: a. the income statement budget b. the production budgetc. the sales budgetd. all of the above14. Which budget allows management to prepare performance reports that compare actual and budgeted costs for the actual level of activity? a. static budget b. master budget c. flexible budget d. income statement budget15. Which of the following a key feature of a budgeting system that encourages positive behavior?a. frequent feedback on performanceb. participative budgetingc. realistic standardsd. all of the above16. A potential problem of participative budgeting would be:a. budgets would be unrealisticb. creation of budgetary slackc. increase goal congruenced. no monetary or non-monetary incentive17. Natural Company plans to sell 40,000 boxes of teabags during January. The company has 6,000 boxes on hand on January 1 and requires 15% of the next months’ sales on hand at the end of the month. Budgeted sales for the month of February and March, are 35,000 and 45,000 boxes, respectively. Budgeted production for January would be: a. 40,000 boxes b. 35,000 boxes c. 39,250 boxes d. 40,750 boxes18. The Sage Company has budgeted production for the next two months as follows: first month, 20,000 and second month, 22,000. Three pounds of direct materials are required to produce one unit of the product. Direct materials on hand were 6,000pounds. Direct materials at the end of each month should equal 10% of next month’s production needs. Budgeted purchases of direct materials would be:a. 60,600 lbsb. 60,000 lbsc. 66,600 lbsd. 59,400 lbs19. Thomville Company makes collections on sales according to the following schedule:50% in the month of sale 40% in the month following sale 10% in the second month following salea. $45,000b. $50,000c. $49,500d. $51,50020. Stevie Company has a cash balance of $10,500 on May 1. The company is planning to maintain a minimum cash balance of $5,000. During May, expected cash receipts are $50,000 and expected cash disbursements are $60,000. During May, the company will need to borrow: a. $0 b. $4,500 c. $5,000 d. $5,500。

《成本管理会计》习题返回主页第一章总论一、名词解释1、成本计算2、管理会计3、预测4、决策5、战略管理会计二、单项选择1、在传统管理会计阶段,管理会计的内容主要包括()。

A、预算和控制B、预测和决策C、日常控制D、业绩评价2、20世纪50年代起,所谓“管理中心在经营,经营的重心在决策”,正是适应生产力迅速发展而提出的()。

A、预测分析法B、企业管理的指导方针C、经营决策方法D、控制、规划方略3、在电脑一体化制造的经营环境中,产品成本的构成内容体现为()。

A、由生产制造作业引起的成本比重会下降,由管理作业引起的成本比重会大幅度上升。

B、由管理作业引起的成本会下降,由生产制造作业引起的成本比重会上升。

C、期间费用会上升。

D、直接材料成本会下降。

4、下列说法正确的是()。

A、管理会计就是内部会计。

B、管理会计就是决策会计。

C、管理会计的实质是会计与管理的直接结合。

D、管理会计就是预测、决策的一系列分析方法。

5、在下列各项中,管理会计与财务会计之间不存在区别的是()。

A、工作程序B、作用时效C、最终奋斗目标D、信息特征三、判断1、从成本管理会计的发展历程看,成本会计的重点已从产品成本计算扩展到利用不同的成本信息进行企业内部管理()。

2、现代管理科学的发展与管理会计的发展没有什么必然的联系()。

3、行为科学主要是利用心理学、社会学等原理,来研究人们行为以及产生人的各种行为的客观原因和主观动机的一门科学()。

4、我国制造成本计算法的特点是把企业的全部成本费用划分为制造成本(生产成本)和期间费用两部分,企业产品成本核算到制造成本为止()。

5、在市场经济条件下,筹集资金、购买设备和原材料、劳动力使用等,企业并没有完全的自主权()。

四、简述1、我国成本会计现状及存在的问题?2、简述现代成本管理会计的发展趋势及方向?第二章成本概念及成本核算程序一、名词解释1、生产成本2、成本性态3、变动成本4、固定成本5、产品成本计算方法二、单项选择1、下列项目中,属于变动生产成本的是()。

第 7 章 生产费用在完工产品和在产品之间分配的核算一.单项选择题1.月末在产品数量较大且各月末在产品数量变化较大,产品中各成本项目费用的比重相差不多 的产品,其在产品成本计算应采用 ( ) 。

A .定额成本法 B. 定额比例法 固定成本法正确的定额资料的企业, 月末在产品数量变化较大的产 。

定额比例法 固定成本法3. 采用约当产量法, 原材料费用按完工产品和月末在产品数量分配时应具备的条件是 ( )A.原材料是陆续投入的 B. 原材料是生产开始时一次投入的C. 原材料在产品成本中所占比重大D.原材料按定额投入4. 在定额管理基础较好, 消耗定额准确、稳定, 而且月初、月末在产品数量变化不大的条件下,在产品成本计算应采用( ) 。

A.定额成本法B. 定额比例法C. 约当产量法D.固定成本法5. 分配加工费用时所采用的在产品的完工率是指产品 ( )与完工产品工时定额的比率。

A .所在工序的工时定额 B .前面各工序工时定额与所在工序工时定额之半 的合计数 C .所在工序的累计工时定额 D .所在工序的工时定额之半6. 如果某种产品的月末在产品数量较大, 各月在产品数量变化也较大, 产品成本中各项费用的 比重相差不大,生产费用在完工产品与月末在产品之间分配,应采用的方法是( )。

A .不计在产品成本法B .约当产量比例法C .在产品按完工产品计算方法 D. 定额比例法7. 某企业产品经过两道工序, 各工序的工时定额分别为 30 小时和 40 小时, 则第二道工序的完工 率为( )。

A . 68% B. 69%C .70%8. 下列方法中不属于完工产品与月末在产品之间分配费用的方法是( ) A.约当产量比例法 BC.年度计划分配率分配法D.分配计算完工产品和月末在产品成本, 必须具备下列条件.原材料在生产开始时一次投料D.各项消耗定额比较准确、稳定10.某产品经过两道工序加工完成。

第一道工序月末在产品数量为C. 约当产量法D.2. 定额基础管理较好, 各种产品有健全、 品,在产品成本的计算应采用 ( )A. 定额成本法B.C. 约当产量法D.71%.不计算在产品成本法 定额比例法9. 按完工产品和月末在产品数量比例,( )。

《成本管理会计》习题返回主页第一章总论一、名词解释1、成本计算2、管理会计3、预测4、决策5、战略管理会计二、单项选择1、在传统管理会计阶段,管理会计的内容主要包括()。

A、预算和控制B、预测和决策C、日常控制D、业绩评价2、20世纪50年代起,所谓“管理中心在经营,经营的重心在决策”,正是适应生产力迅速发展而提出的()。

A、预测分析法B、企业管理的指导方针C、经营决策方法D、控制、规划方略3、在电脑一体化制造的经营环境中,产品成本的构成内容体现为()。

A、由生产制造作业引起的成本比重会下降,由管理作业引起的成本比重会大幅度上升。

B、由管理作业引起的成本会下降,由生产制造作业引起的成本比重会上升。

C、期间费用会上升。

D、直接材料成本会下降。

4、下列说法正确的是()。

A、管理会计就是内部会计。

B、管理会计就是决策会计。

C、管理会计的实质是会计与管理的直接结合。

D、管理会计就是预测、决策的一系列分析方法。

5、在下列各项中,管理会计与财务会计之间不存在区别的是()。

A、工作程序B、作用时效C、最终奋斗目标D、信息特征三、判断1、从成本管理会计的发展历程看,成本会计的重点已从产品成本计算扩展到利用不同的成本信息进行企业内部管理()。

2、现代管理科学的发展与管理会计的发展没有什么必然的联系()。

3、行为科学主要是利用心理学、社会学等原理,来研究人们行为以及产生人的各种行为的客观原因和主观动机的一门科学()。

4、我国制造成本计算法的特点是把企业的全部成本费用划分为制造成本(生产成本)和期间费用两部分,企业产品成本核算到制造成本为止()。

5、在市场经济条件下,筹集资金、购买设备和原材料、劳动力使用等,企业并没有完全的自主权()。

四、简述1、我国成本会计现状及存在的问题2、简述现代成本管理会计的发展趋势及方向第二章成本概念及成本核算程序一、名词解释1、生产成本2、成本性态3、变动成本4、固定成本5、产品成本计算方法二、单项选择1、下列项目中,属于变动生产成本的是()。

第一章第一章成本会计流程(二)判断题(正确的划√错误的划×)1.成本的经济实质,是企业在生产经营过程中所耗费的资金的总和。

()2.在实际工作中,确定成本的开支范围应以成本的经济实质为理论依据。

()3.成本预测和计划是成本会计的最基本的任务。

()4.成本会计的对象,概括的讲,就是产品的生产成本。

()5.以已经发生的各项费用为依据,为经济管理提供真实的、可以验证的成本信息资料,是成本会计反映职能的基本方面。

()6.制定和修订定额,只是为了进行成本审核,与成本计算没有关系。

()7.为了正确计算产品成本,应该也可能绝对正确地划分完工产品与在产品的费用界限。

()8.产品成本项目就是计入产品成本的费用按经济内容分类核算的项目。

()9.生产工资和福利费是产品成本项目。

()10.直接生产费用既可能是直接计入费用,也可能是间接计入费用。

()11.为了尽可能地符合实际情况,厂内价格应该在年度内经常变动。

()12.“基本生产成本”科目应该按成本计算对象设置明细分类账,账内按成本项目分设专栏或专行。

()13.企业生产经营的原始记录,是进行成本预测、编制成本计划、进行成本核算的依据。

()14.生产设备的折旧费用计入制造费用,因此它属于间接生产费用。

()(三)单项选择题1.成本会计的任务主要决定于()。

A、企业经营管理的要求。

B、成本核算C、成本控制D、成本决策2.产品成本是指企业生产一定种类、一定数量的产品所支出的各项()。

A、生产费用之和B、生产经营管理费用总和C、经营管理费用总和D、料、工、费及经营费用总和3.成本会计最基本的任务和中心环节是()。

A、进行成本预测,编制成本计划B、审核和控制各项费用的支出C、进行成本核算,提供实际成本的核算资料D、参与企业的生产经营决策4.成本的经济实质是()。

A、生产经营过程中所耗费生产资料转移价值的货币表现。

B、劳动者为自己劳动所创造价值的货币表现C、劳动者为社会劳动所创造价值的货币表现D、企业在生产经营过程中所耗费的资金的总和5.下列各项中,属于产品生产成本项目的是()。

Chapter 6

1. Process costing accumulates costs by processing departments rather than by jobs.

2. In parallel processing, each unit must pass through one process before they can be worked on in later processes.

3. The same equivalent units figure is used for both materials and conversion costs in process costing.

4. The output of process costing are homogeneous products.

5. When computing the cost per equivalent unit, it is not necessary to consider the percentage completion of the units in beginning inventory under the weighted-average method.

6. Equivalent production expresses all activity of the period in terms of partially completed units.

7. When units pass through more than one process, the units transferred from Department 1 equals the units completed in Department 2.

8. When units pass through more than one process, and the units transferred are transferred from Department 1 to 2, the entry to record this transfer involves a debit to Work in Process.

9. Department 3, the last processing department, receives goods produced in previous departments. The costs transferred into Department 3 are treated as materials costs added at the end of the process.

10. The FIFO method is more useful for cost control when the costs of manufacturing inputs fluctuate from period to period.

11. Process costing would be most appropriate for which of the following?

a. oil refining

b. custom furniture

c. t-shirt printing

d. food catering

12. The cost of production report: a. provides information about the physical units processed by the department

b. provides information about the manufacturing costs incurred by the department

c. both a and c

d. none of the above

13. Which method considers the percentage of completion of ending work-in-process inventory?

a. weighted average

b. FIFO

c. both weighted average and FIFO

d. percentage of completion is not calculated for ending work-in-process inventory

14. The cost of units finished at the last department will flow from work in process to:

a. cost of goods sold

b. finished goods

c. work in process

d. sales

15. Assuming the balance in beginning work-in-process inventory was zero and the ending working process inventory is 25% complete with respect to conversion costs. The number of equivalent units of production with respect to conversion costs under the weighted average method would be: a. less than the units started in the period

b. less than the units completed

c. the same as the units started

d. the same as the units completed

16. The Lockhart Company uses the weighted average method. The beginning work in process consists of 10,000 units (100% completed as to materials and 50% complete as to conversion costs). The number of units completed was 100,000. The ending work in process consists of 15,000 units (100% complete as to materials and 20% complete as to conversion costs). The equivalent units of production for conversion costs was:

a. 150,000

b. 110,000

c. 103,000

d. 108,000

17. The Lockhart Company uses the weighted average method. The beginning work in process consists of 10,000 units (100% completed as to materials and 50% complete as to conversion costs). The number of units completed was 100,000. The ending work in process consists of 15,000 units (100% complete as to materials and 20% complete as to conversion costs). The units started during the period was:

a. 95,000

b. 100,000

c. 105,000

d. 115,000

18. Dino Manufacturers uses the weighted average method in its costing system. The following information

19. Dino Manufacturers uses the weighted average method in its costing system. The following information

20. Garcia Company uses the weighted average method in its costing system. For the month of May in the Assembly Department, the equivalent units for conversion costs amounted to 35,000. There were 5,000 units in beginning work-in-process that were 50% complete. During the month, 33,000 units were started and 31,400 were completed and transferred. The ending work in process:

a. consist of 3,600 units

b. consist of 6,600 units

c. consist of 5,000 units

d. consist of 7,000 units。