中美会计准则对比(中英文对照)

- 格式:pdf

- 大小:468.04 KB

- 文档页数:48

中国会计准则和美国会计准则差异有哪些?想考美国注会(U.S.CPA)的同学们对中美会计准则的差异非常关注,如下内容为大家揭秘:中美两国会计准则差异。

一、中美会计准则的实质性差别rulebasedvsprinciplebased美国会计准则的模式为规则导向,更容易导致机会主义和盈余管理。

目前的USGAAP共168号(新旧放在一起)不是按要素制定的,是一种救火式的准则,哪里出了问题,立马会有相应的准则制定出来。

中国会计准则的模式为原则导向,强调实质重于形式,采购谨慎性原则、减少方法的选择、充分披露,以此来克服机会主义的盈余管理。

财政部自2006年颁布新的会计准则以来,陆续颁布了“新会计准则应用指南”以及3个解释公告。

其中,在3号解释公告里提出了综合收益的(comprehensiveincome)概念。

(Tips:如何理解comprehensiveincome?如可供出售金融资产,持有时其价值变动计入资本公积,一旦出售,就会进利润表,以综合收益的形式反映。

comprehensiveincome就是用来反映未来利润的。

新准则修订了资产的定义:经济利益很可能流入企业,金额可以可靠计量,淡化了“过去交易”,主要也是为了配合“未来”交易,如亏损合同等)。

可以这样总结,会计准则未来的发展趋势是:一是从损益满计观向资本保全管转变,反映自从萨班斯法案以来国际财务界重视资产计价的趋势(典型地,如捐赠收入,债务重组收益进利润表,不再进资本公积。

目前资本公积科目得到了净化,只含“股本溢价”和“其它”两个明细);二是资产计价将存在两种模式:成本模式(costvalue)和公允价值模式(fairvalue);三是反映未来信息的新趋势(典型地,comprehensiveincome)。

二、美国会计准则总体介绍(一)制定美国公认会计准则的组织证券交易委员会(SecuritiesandExchangeCommission,SEC);美国注册会计师协会(AmericanInstituteofCertifiedPublicAccountingStandardsBoard,AICPA);财务会计准则委员会(FinancialAccountingStandardsBoard,FASB);政府会计准则委员会(GovermentalAccountingStandardsBoard,GASB)。

中美的会计准则制度差异英语作文Differences in Accounting Standards between China and the United StatesIntroductionThe accounting standards followed by different countries vary considerably due to differences in legal, economic, and cultural factors. China and the United States have distinct accounting frameworks, with China following the Chinese Accounting Standards (CAS) and the United States following the Generally Accepted Accounting Principles (GAAP). This essay will analyze the key differences between the accounting standards of China and the United States and discuss the implications of these differences on financial reporting and decision-making.Comparison of Accounting Standards1. Legal Framework: China has a civil law system that governs its accounting standards, while the United States has a common law system. This difference influences the accounting standards in terms of legal requirements, enforcement mechanisms, and the role of regulators.2. Disclosure Requirements: The CAS in China focus on protecting the interests of stakeholders, including investors,regulators, and creditors. On the other hand, the GAAP in the United States emphasize transparency and comparability in financial reporting.3. Valuation of Assets: The CAS in China allow for more subjective judgment in the valuation of assets, leading to potential differences in the reported value of assets compared to the GAAP in the United States, which require more conservative valuation methods.4. Revenue Recognition: The CAS in China allow for more flexibility in revenue recognition, which may lead to the recognition of revenue earlier than under the GAAP in the United States, where strict criteria must be met for revenue recognition.Implications of Differences in Accounting Standards1. Financial Reporting: The differences in accounting standards between China and the United States can result in inconsistencies in financial reporting, making it challenging for investors and analysts to compare the financial performance of companies across borders.2. Cost of Capital: The differences in accounting standards can impact the cost of capital for companies operating in China and the United States. Investors may perceive higher risks injurisdictions with less stringent accounting standards, leading to higher capital costs.3. Regulatory Compliance: Companies operating in both China and the United States face the challenge of complying with two different sets of accounting standards, which can be time-consuming and costly.ConclusionIn conclusion, the differences in accounting standards between China and the United States have significant implications for financial reporting and decision-making. Companies operating in both countries must navigate these differences to ensure compliance with regulatory requirements and provide accurate and transparent financial information to stakeholders. It is essential for regulators, standard-setters, and practitioners to work towards greater convergence of accounting standards to promote transparency, comparability, and efficiency in the global capital markets.。

中国会计准则与美国会计制度比较引言:在全球化的背景下,国际间的贸易、投资和合作日益频繁,不同国家的会计准则和制度成为企业跨境经营的重要考虑因素。

中国作为世界上最大的发展中国家,其会计准则与美国会计制度有着显著的差异。

本文将对中国会计准则与美国会计制度进行比较,以了解两者之间的异同和影响。

一、会计准则的体系中国会计准则:中国会计准则以《中华人民共和国企业会计准则》为核心,由财政部颁布并得到相关监管机构的认可。

同时,中国还制定了一系列行业特定会计准则和企业类型的会计准则。

美国会计制度:美国的会计准则主要由美国财务会计准则委员会(FASB)颁布,其准则以《美国通用会计准则》(US GAAP)为基础。

此外,美国还存在行业特定会计准则,如金融业会计准则和保险业会计准则。

比较分析:中国的会计准则体系相对较为复杂,由于不同行业、企业类型和财政部门的不同规定,会计准则相对分散。

而美国的会计准则更为统一,US GAAP成为了金融报告的主要依据。

这意味着在跨国业务中,与美国企业合作的中国企业需要适应或转变会计准则的要求。

二、会计报告标准中国会计准则:中国会计准则要求企业编制财务报表包括资产负债表、利润表、现金流量表和所有者权益变动表。

此外,中国的会计报告标准还要求企业披露必要的附注信息,以提供更详尽的财务信息。

美国会计制度:美国的会计报告标准同样要求企业编制资产负债表、利润表和现金流量表,但与中国不同的是,美国的会计报告标准更加详细和严格。

US GAAP要求企业进行更广泛的披露,包括管理层讨论与分析、业务风险和前景、股东权益变动等。

比较分析:美国的会计报告标准更加规范和详细,使投资者和利益相关者能够更全面地了解企业的财务状况和经营情况。

相比之下,中国的会计报告标准虽然也要求附注信息的披露,但相对较少。

中国企业与美国企业进行合作时,需要适应美国会计报告标准的要求,以满足国际投资者和监管机构的需求。

三、会计处理原则中国会计准则:中国的会计处理原则以审慎性原则为基础,侧重于保守估计和风险防范。

美国和中国的会计准则制度的对比英语作文Title: A Comparative Analysis of US GAAP and Chinese Accounting StandardsThe financial reporting landscape across global economies is shaped by the accounting standards adopted by each nation. Among these, the United States Generally Accepted Accounting Principles (US GAAP) and the Chinese Accounting Standards (CAS) stand out as two significant frameworks. This essay aims to compare and contrast the key features of US GAAP and CAS, highlighting their similarities and differences in approach to financial reporting.1. Overview of US GAAP and CASUS GAAP: Developed by the Financial Accounting Standards Board (FASB), US GAAP is a comprehensive set of accounting rules widely used in the United States for preparing and reporting financial statements.CAS: Established by the Ministry of Finance of China, CAS is designed to align with international financial reporting standards while maintaining specific provisions tailored to the Chinese economic environment.2. Convergence and International AlignmentUS GAAP: Has historically been more independent, though recent efforts have been made to converge with International Financial Reporting Standards (IFRS).CAS: Has shown a strong commitment to convergence with IFRS, aiming to enhance comparability and transparency in financial reporting.3. Key Differences in Accounting TreatmentRevenue Recognition: US GAAP provides more detailed guidance on revenue recognition, while CAS follows a principles-based approach similar to IFRS.Inventory Valuation: Under US GAAP, companies can choose between different inventory costing methods, whereas CAS mandates the use of historical cost or market price, whichever is lower.Intangible Assets: US GAAP has stringent criteria for capitalization of intangible assets, while CAS allows for greater flexibility in this area.4. Disclosure RequirementsUS GAAP: Emphasizes extensive disclosures to provide users with a comprehensive understanding of the company's financial health.CAS: While also requiring disclosure of relevant information, may have less detailed requirements compared to US GAAP.5. Regulatory Oversight and EnforcementUS GAAP: Enforced by the Securities and Exchange Commission (SEC) and subject to rigorous auditing standards.CAS: Monitored by the Chinese regulatory authorities, with increasing emphasis on compliance and enforcement in recent years.The comparison between US GAAP and CAS reveals both commonalities and distinctions in their approaches to financial reporting. While both systems strive for accuracy and transparency, they reflect the unique contexts of their respective economies. As the world becomes increasingly interconnected, the trend towards convergence of accounting standards continues, with the potential to simplifycross-border financial analysis and investment decisions. However, it is crucial to recognize the nuances and adapt accordingly when navigating the financial statements prepared under these distinct accounting regimes.。

中美会计准则比较中美会计准则比较中国会计准则和美国会计准则差异有哪些?想考美国注会〔U.S.CPA〕的同学们对中美会计准则的差异特别关注,如下内容为大家揭秘:中美两国会计准则差异。

一、中美会计准则的实质性差异rulebasedvsprinciplebased美国会计准则的模式为规则导向,更简单导致机会主义和盈余管理。

目前的USGAAP共168号〔新旧放在一起〕不是按要素制定的,是一种救火式的准则,哪里出了问题,立马会有相应的准则制定出来。

中国会计准则的模式为原则导向,强调实质重于形式,选购谨慎性原则、削减方法的选择、充分披露,以此来克服机会主义的盈余管理。

财政部自2006年公布新的会计准则以来,陆续公布了"新会计准则应用指南'以及3个解释公告。

其中,在3号解释公告里提出了综合收益的〔comprehensiveincome〕概念。

〔Tips:如何理解comprehensiveincome?如可供出售金融资产,持有时其价值变动计入资本公积,一旦出售,就会进利润表,以综合收益的形式反映。

comprehensiveincome就是用来反映将来利润的。

新准则修订了资产的定义:经济利益很可能流入企业,金额可以可靠计量,淡化了"过去交易',主要也是为了协作"将来'交易,如亏损合同等〕。

可以这样总结,会计准则将来的进展趋势是:一是从损益满计观向资本保全管转变,反映自从萨班斯法案以来国际财务界重视资产计价的趋势〔典型地,如捐赠收入,债务重组收益进利润表,不再进资本公积。

目前资本公积科目得到了净化,只含"股本溢价'和"其它'两个明细〕;二是资产计价将存在两种模式:本钱模式〔costvalue〕和公允价值模式〔fairvalue〕;三是反映将来信息的新趋势〔典型地,comprehensiveincome〕。

二、美国会计准则总体介绍〔一〕制定美国公认会计准则的组织证券交易委员会〔SecuritiesandExchangeCommission,SEC〕;美国注册会计师协会〔AmericanInstituteofCertifiedPublicAccountingStandardsBoard,AICPA〕;财务会计准则委员会〔FinancialAccountingStandardsBoard,FASB〕;政府会计准则委员会〔GovermentalAccountingStandardsBoard,GASB〕。

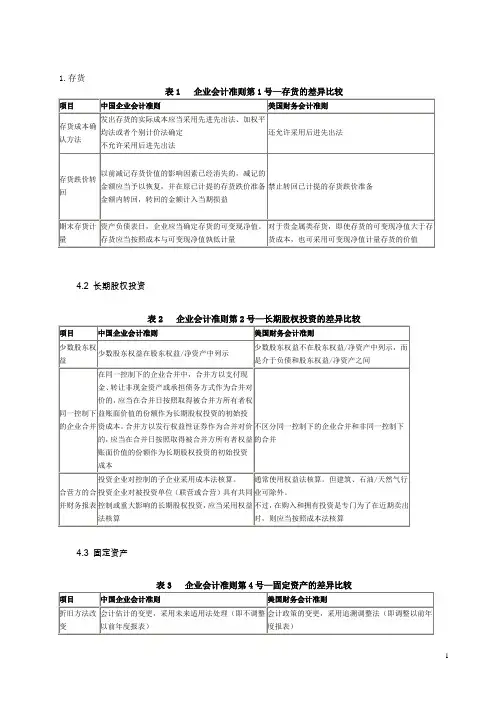

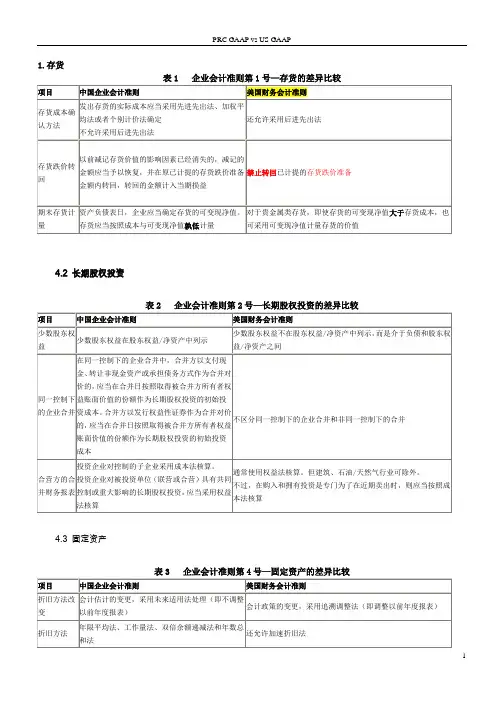

1.存货

表1 企业会计准则第1号—存货的差异比较

4.2 长期股权投资

表2 企业会计准则第2号—长期股权投资的差异比较

4.3 固定资产

表3 企业会计准则第4号—固定资产的差异比较

4.4 无形资产

4.5 非货币性资产交换

4.6 雇员薪酬、福利、奖励(职工薪酬、企业年金基金、股份支付)

4.7 收入

表7 企业会计准则第14号—收入的差异比较

4.8 建造合同

表8 企业会计准则第15号—建造合同的差异比较

4.9 政府补助

表9 企业会计准则第16号—政府补助的差异比较

4.10 所得税

4.11 企业合并

表11 企业会计准则第20号—企业合并的差异比较

4.12 金融工具

4.13 会计政策、会计估计变更和差错更正

表13 企业会计准则第28号—会计政策、会计估计变更和会计差错更正的差异比较

4.14 财务报表列报

表14 企业会计准则第30号—财务报表列报的差异比较

4.15 中期财务报告

表15 企业会计准则第29号—中期财务报告的差异比较

4.16 关联方披露

表16 企业会计准则第36号—关联方披露的差异比较。

中美的会计准则制度差异英语作文Accounting standards and systems play a crucial role in the financial reporting and decision-making processes of businesses around the world. In this regard, the differences between the accounting standards and systems of China and the United States are of particular interest. This article will explore the key differences between the accounting standards and systems of China and the United States, and their implications for businesses operating in these two countries.One of the key differences between the accounting standards of China and the United States is the underlying principles upon which they are based. In the United States, accounting standards are predominantly based on the principles of Generally Accepted Accounting Principles (GAAP), which emphasize the principles of relevance, reliability, comparability, and consistency. In contrast, China has its own set of accounting standards known as Chinese Accounting Standards (CAS), which are based on a mix of international accounting standards and Chinese regulatory requirements.Another key difference between the accounting standards of China and the United States is the level of detail and guidance provided in the standards. In general, US GAAP provides moredetailed guidance on accounting treatments and disclosures for various transactions, while CAS tends to be less prescriptive and allows for more flexibility in accounting treatments. This difference in detail and guidance can lead to differences in financial reporting practices and results between companies in China and the United States.Furthermore, the regulatory environment surrounding accounting standards and systems in China and the United States also differs. In the United States, accounting standards are set by independent standard-setting bodies such as the Financial Accounting Standards Board (FASB) and the Securities and Exchange Commission (SEC), which are overseen by the Public Company Accounting Oversight Board (PCAOB). In China, accounting standards are set and regulated by the Ministry of Finance (MOF) and the China Securities Regulatory Commission (CSRC), which have a more direct role in setting and enforcing accounting standards.The differences in accounting standards and systems between China and the United States have implications for businesses operating in these two countries. For multinational companies with operations in both China and the United States, the differences in accounting standards can pose challenges infinancial reporting and compliance. Companies may need to reconcile their financial statements prepared under different accounting standards, which can be time-consuming and costly.In addition, the differences in accounting standards can also impact investors and other stakeholders who rely on financial information to make informed decisions. Investors may need to be aware of the differences in accounting standards between China and the United States when evaluating the financial performance and position of companies operating in these two countries. The differences in accounting standards can also impact the comparability of financial information across companies and countries, which can make it difficult for investors to make meaningful comparisons.Overall, the differences in accounting standards and systems between China and the United States highlight the complexity and challenges of financial reporting in a globalized economy. Businesses operating in these two countries need to be aware of the differences in accounting standards and ensure compliance with the relevant requirements. By understanding the key differences between the accounting standards and systems of China and the United States, businesses can navigate thechallenges and opportunities of operating in these two important markets.。

中美的会计准则制度的对比英语作文A Comparison of Accounting Standards and Systems between China and the United StatesIntroductionIn today's global economy, accounting standards play a crucial role in ensuring the transparency and reliability of financial reporting. China and the United States, as two of the world's largest economies, have their own unique accounting systems and standards. In this paper, we will compare the accounting standards and systems of China and the United States, highlighting the key similarities and differences between the two countries.Accounting Standards in ChinaIn China, the accounting standards are issued by the Ministry of Finance (MoF) and are known as Chinese Accounting Standards (CAS). CAS are based on a mix of international accounting standards (IAS/IFRS) and local regulations. The standards are compulsory for all enterprises in China, including foreign-invested enterprises and listed companies. CAS are aimed at improving the quality and transparency of financialreporting, enhancing the comparability of financial statements, and facilitating the development of the capital markets.One of the key characteristics of CAS is that they are more rules-based than principle-based. This means that the standards provide detailed guidelines and specific rules for financial reporting, leaving less room for interpretation. In addition, Chinese accounting standards place a strong emphasis on prudence and conservatism, which can sometimes lead to more conservative financial reporting practices.Accounting Standards in the United StatesIn the United States, accounting standards are issued by the Financial Accounting Standards Board (FASB) and are known as Generally Accepted Accounting Principles (GAAP). GAAP are considered the gold standard of accounting in the United States and are widely recognized and accepted by investors, regulators, and other stakeholders. GAAP are based on a principles-based approach, which focuses on conceptual frameworks and broad accounting principles rather than detailed rules.One of the key characteristics of GAAP is their flexibility and adaptability. GAAP allows for professional judgment and interpretation in financial reporting, which can result in more subjective accounting practices. In addition, GAAP also place astrong emphasis on fair value accounting, which values assets and liabilities at their current market prices.Comparison of Accounting SystemsWhen comparing the accounting systems of China and the United States, several key differences emerge. One of the main differences is the level of government involvement in setting accounting standards. In China, the government plays a more active role in regulating and enforcing accounting standards, while in the United States, the FASB operates independently of the government.Another difference is the level of enforcement and compliance with accounting standards. In China, there have been concerns about the quality and reliability of financial reporting, with instances of fraud and misrepresentation. In contrast, the United States has a strong regulatory framework and enforcement mechanisms to ensure compliance with GAAP.ConclusionIn conclusion, while both China and the United States have their own unique accounting standards and systems, they share a common goal of enhancing transparency and reliability in financial reporting. The differences between the two countries liein the approach to setting standards, the level of government involvement, and the emphasis on rules-based versus principles-based accounting. By understanding these differences, companies operating in both countries can navigate the complex landscape of global accounting standards and comply with the regulatory requirements of each jurisdiction.。

1.存货

表1 企业会计准则第1号—存货的差异比较

4.2 长期股权投资

表2 企业会计准则第2号—长期股权投资的差异比较

4.3 固定资产

表3 企业会计准则第4号—固定资产的差异比较

4.4 无形资产

表4 企业会计准则第6号—无形资产的差异比较

4.5 非货币性资产交换

4.6 雇员薪酬、福利、奖励(职工薪酬、企业年金基金、股份支付)

表6 企业会计准则第9/10/11号—雇员薪酬、福利、奖励差异的比较

4.7 收入

表7 企业会计准则第14号—收入的差异比较

4.8 建造合同

表8 企业会计准则第15号—建造合同的差异比较

4.9 政府补助

4.10 所得税

表10 企业会计准则第18号—所得税的差异比较

4.11 企业合并

表11 企业会计准则第20号—企业合并的差异比较

4.12 金融工具

表12 企业会计准则第22/23/24/37号—金融工具确认、计量、转移、套期保值及列报的差异比较

4.13 会计政策、会计估计变更和差错更正

4.14 财务报表列报

表14 企业会计准则第30号—财务报表列报的差异比较

4.15 中期财务报告

4.16 关联方披露。

中美会计准则对比1.目标和原则中国会计准则的主要目标是提供企业财务信息,以帮助用户了解企业的财务状况、经营成果和现金流量,并做出相应决策。

美国会计准则的主要目标是提供投资者和债权人关于企业财务状况和经营结果的准确和全面的信息。

2.框架和指南中国会计准则遵循国际会计准则理事会(IASB)的国际财务报告准则(IFRS),在其框架和指南上与国际接轨。

美国会计准则主要遵循美国公认会计准则(GAAP),并由美国财务会计准则委员会(FASB)制定。

3.会计政策中国会计准则允许企业根据实际情况进行会计政策的选择,但必须在财务报表中明确披露相关信息。

美国会计准则也允许会计政策的选择,但有一些具体要求,例如,企业必须在会计政策一致性原则下进行分析和披露。

4.资产计量中国会计准则强调成本基础计量,即资产和负债以其获取或产生时的历史成本计量。

美国会计准则也支持成本基础计量,但它还允许一些资产按照公允价值计量,特别是在金融工具和投资方面。

5.准确认可信度中国会计准则对准确认可信度要求较高。

在确认收入和费用时,必须满足一系列条件,例如确认是基于已发生的经济利益,交易是可量度和可计量的。

美国会计准则也对准确认可信度有所要求,但更加灵活和宽松。

6.报表要求中国会计准则规定了财务报表的具体要求,包括资产负债表、利润表和现金流量表。

美国会计准则也制定了相似的报表要求,但它还有一些额外的要求,例如综合收益表和股东权益变动表。

以上仅是中美会计准则的一些主要对比。

由于两国的法律、经济和文化差异,这些准则之间还存在许多其他差异。

企业和会计师必须根据其所在的国家和商业环境来遵循适用的会计准则,并确保按照相应的规定进行财务报告。

美国会计准则与中国会计准则具体差异-列表对比1.存货表1 企业会计准则第1号—存货的差异比较项目中国企业会计准则美国财务会计准则存货成本确认方法发出存货的实际成本应当采用先进先出法、加权平均法或者个别计价法确定不允许采用后进先出法还允许采用后进先出法存货跌价转回以前减记存货价值的影响因素已经消失的,减记的金额应当予以恢复,并在原已计提的存货跌价准备金额内转回,转回的金额计入当期损益禁止转回已计提的存货跌价准备期末存货计量资产负债表日,企业应当确定存货的可变现净值。

存货应当按照成本与可变现净值孰低计量对于贵金属类存货,即使存货的可变现净值大于存货成本,也可采用可变现净值计量存货的价值4.2 长期股权投资表2 企业会计准则第2号—长期股权投资的差异比较项目中国企业会计准则美国财务会计准则少数股东权益少数股东权益在股东权益/净资产中列示少数股东权益不在股东权益/净资产中列示,而是介于负债和股东权益/净资产之间同一控制下的企业合并在同一控制下的企业合并中,合并方以支付现金、转让非现金资产或承担债务方式作为合并对价的,应当在合并日按照取得被合并方所有者权益账面价值的份额作为长期股权投资的初始投资成本。

合并方以发行权益性证券作为合并对价的,应当在合并日按照取得被合并方所有者权益账面价值的份额作为长期股权投资的初始投资成本不区分同一控制下的企业合并和非同一控制下的合并合营方的合并财务报表投资企业对控制的子企业采用成本法核算。

投资企业对被投资单位(联营或合营)具有共同控制或重大影响的长期股权投资,应当采用权益法核算通常使用权益法核算。

但建筑、石油/天然气行业可除外。

不过,在购入和拥有投资是专门为了在近期卖出时,则应当按照成本法核算项目中国企业会计准则美国财务会计准则研究和开发费用所有研发项目研究阶段的支出全部计入当期费用。

开发阶段支出如果符合特定标准(使用或出售的意图、技术可行、市场存在、资源支持)则予以资本化,确认为无形资产通常所有研究和开发支出全部作为当期费用(除部分用于网站开发及内部使用的软件开发成本可以资本化)。