ACCA P4 45 Days revision plan-1

- 格式:pdf

- 大小:168.98 KB

- 文档页数:6

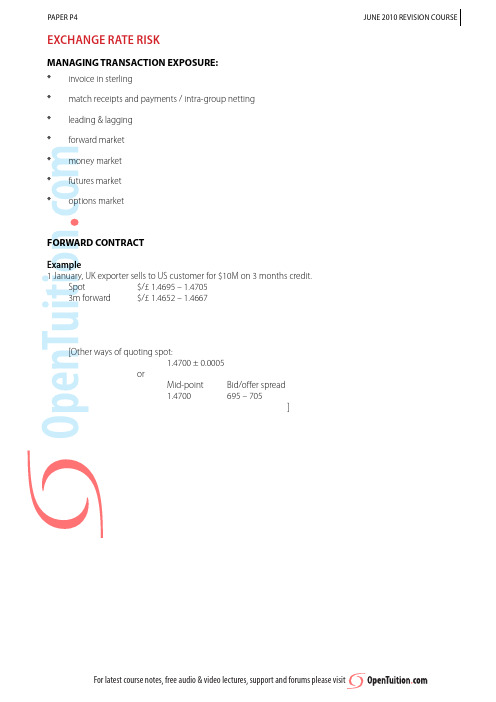

MANAGING TRANSACTION EXPOSURE:* invoice in sterling* match receipts and payments / intra-group netting* leading & lagging* forward market* money market* futures market* options marketFORWARD CONTRACTExample1 January, UK exporter sells to US customer for $10M on 3 months credit.Spot $/£ 1.4695 – 1.47053m forward $/£ 1.4652 – 1.4667[Other ways of quoting spot:1.4700 ± 0.0005orMid-point Bid/offer spread7051.4700–695]MONEY MARKETExampleUK company to receive $100K in 3 months time.Current 3 months interest rates:US Prime 2.7% (p.a.) UK LIBOR 1.8% (p.a.) Current exchange rate $1.47 to £How can company hedge against exchange rate risk?[Note: to get quarterly interest rate, divide annual rate by four. No need to allow for compounding effect.]FoRwARd CoNTRACTAnswer to example:Receive $, so use $ sell rate:$10M ÷ 1.4667 = £6,818,027[Exchange rate fixed now for conversion in 3 months time]MoNEy MARKETAnswer to example:0675.%]£67,571£67,875A UK company will receive $2.5M from an American customer in 3 months time at the end of February. Futures: $/£ contracts (£62500)December 1.5830 $/£March 1.5896 $/£Current spot rate: 1.5842 - 1.5852demonstrate how a futures hedge would work.(assume spot in February is 1.6005 – 1.6015)Step 1As a reference point, convert at the current spot rate (this is only necessary if required to calculate hedging ef-ficiency later): $2.5M ÷ 1.5852 = £1,577,088Step 2Write down what futures deal will be started “today”Month: March (this means that deal must finish by the end of March – choosefirst month after date of transaction)(check the contract currency £62,500. Decide whether transactionis buying or selling the contract currency – here receive $’s, so sell $’s, so buy £’s. Same deal in futures is buy futures)$2.5M÷1.5896÷£62500(transaction)(todays futuresprice)(contract size)= 25 contracts (nearest whole number of contracts)Buy 25 March futures contractsTodayDate of transaction End of future (end February )(end March)1.5896 1.60221.58471.60100.0049(1/4)0.00121 month4 months[Assume that the basis risk falls to zero over the life of the future]Step 4Illustration of what happens in February (date of transaction)Transaction – convert at spot $2.5M ÷ 1.6015£1,561,037Profit on futures=$ 19688 ÷ 1.6015 =£12,293TOTAL RECEIPT£1,573,33025contracts£62500sizesell buy ××−(..1602215896)Step 5 (IF REQUIRED)Hedging efficiency =Profit on one transactionLoss on other transact t ion100%=12,2931,577,088-1,561,037100%=××76.6%Philadelphia SE £/$ option £31,250 (cents per £)Strike Calls PutsPrice Oct Nov Dec Oct Nov Dec1.540 4.40– 5.12–0.370.881.550 3.40 3.83 4.39–0.56 1.161.5602.493.09 3.73–0.81 1.491.570 1.612.473.120.11 1.06 1.881.5800.88 1.882.840.38 1.47 2.091.5900.68 1.402.570.88 2.00 2.33A UK company will receive $5M from a US customer in December.Spot rate is 1.5848 and the company is concerned that the $ might weaken. Show how traded £/$ currency options can be used to hedge the risk at 1.580Step 1: Show Options dealStrike: 1.580 (from question, otherwise choose any strike to illustrate)Month:D ecemberPUT/CALL CALL (transaction is receiving $’s so need to sell $’s, i.e. buy £’s/£’s are the contract currency)Contracts $5M÷ 1.580÷31250= 101 contracts (transaction)strike(contract size)Step 2: Calculate premium:101×31250×0.0284=$89637.5contracts contract size from tablePremium calculated in $’s and payable immediately, so convert at current spot rate.89637.5 ÷ 1.5848 = £56,561Step 3: Illustrate what happens on date of transaction.If not then given spot in December, then invent one for illustration.E.g. If spot in December is 1.62Transaction – convert at spot:£3,086,420$5M ÷ 1.62Exercise options:101 × 31250 × (1.62 – 1.58)= $126250 ÷ 1.62 = £77,932£3,164,352Or alternativelyExercise option:£$101 contracts of £31,250 converts to3,156,250from (at 1.50)4,986,875Actually receive $5M, soextra13,125Must be converted at spot(13125 ÷1.62)8,102Neteffect£3,164,352$5,000,000First method is better (what happens in practice)CoMpARISoN oF METHodSForward contracts, money market hedges, and futures all effectively ‘fix’the exchange rate(a) forward contracts– Can be tailored to exact requirements(b) money market– C an be tailored. More easily adjusted where daily exposure to FX changes.May be cheaper for a very (very) large company.(c) futures– More flexible, but cannot be exactly tailored.Transaction costs are cheaper for very large firms.OPTIONS Protect from adverse fluctuations but allow benefit from favourable movements.Best if treasurer is fairly certain that FX rates will move in his favour.INTEREST RATE RISKCan be managed by:* F orward rate agreements (FRA’s)* I nterest rate guarantees* I nterest rate futures* I nterest rate optionsFORWARD RATE AGREEMENTSContract with bank on borrowing rate which will apply at certain time for a stated period on a stated sum. Works as follows:Company pays interest at whatever the actual rate isSettles with bank the difference between actual rate & rate agreedINTEREST RATE GUARANTEESContract with bank to fix a maximum borrowing rate in exchange for an up-front fee. (Interest rate option; interest rate cap).ExampleMight obtain IRG from bank that interest rate will not exceed 14%. If rates turn out to be lower, company pays actual rate.If rates turn out to be higher, company pays actual rate, but bank pays over the difference above 14%.INTEREST RATE FUTURESIf paying interest, then SELL futures (because higher interest rates mean lower futures prices – selling now gives profit if interest rates increase).ExampleIt is now 1 November.On 31 January, UK company will need a £250M loan for 5 months at fixed interest. On 1 November, interest rates are 6.1% p.a. The company is charged a premium for risk of 1%.On 1 November: 3 months interest rate contracts (£1M)D ecember 93.10March 92.90Demonstrate how futures can be used to hedge against interest rate movements. (For example, if future rates not given, make up rates to illustrate.Eg. assume interest rate increases by 2%)INTEREST RATE FUTURES – ANSwERStep 1 C alculate interest at current rate as a reference point (only needed if hedging efficiency is required later).£250M × (6.1% + 1%) × 5/12 = £7,395,833Step 2 Show futures deal starting on first 1 November Month: March (First month end after date of transaction)Buy/Sell: Sell (Sell now, buy later – always sell if borrowing money)Contracts: £250M÷ £1M= 417 contracts length ofloancontractsize(3 month futures)Sell 417 £1m March futures Step 3Show interest rate and futures price at start of loan. If not given futures price then estimate.Now (1 Nov)Start of loan (31 Jan)End of future (31 March)March futures 92.9091.50Interest rate(general rate - ignore premium)93.9091.90[100 – 6.1][100 – 8.1]Basis Risk (1.00)(2⁄5)(0.40)02 months5 monthsOn 31 JanuaryInterest rate 8.1%[Company pays 8.1%+1%=9.1%]March futures 91.50Step 4Illustrate what happens at start of loan (31 January)Interest on loan (actual rate)£250M × (8.1% + 1%) × 5⁄12 = 9,479,167(PAY)Profit on futures1,459,500(REC)£8,019,667417192909150400M (××£.-.)Step 5Calculate hedging efficiency (only if required)Hedging efficiency =Profit on one transactionLoss s on other transaction ×=10014595002083334%,,,,×−10094791677395833%(,,,,)=70%Step 6 Calculate Effective Interest Rate (Only if required)Net amount to pay8019667250000000100125,,,,%××p.a.=7.7%INTEREST RATE OPTIONSOption to buy (call) or sell (put) an interest rate future at a fixed price.If we are worried that interest rates will rise → futures prices will fall → buy a ‘put’option. We can then buy the fu-tures at a lower price & immediately sell at the option price → make a profit to compensate for the higher interest payable.[Do not have to exercise the option, therefore still get benefit if interest rates fall]Example3 months sterling options - £500,000 (points of 100%)Strike price Calls PutsDec Mar Jun Dec Mar Jun93250.180.350.460.140.250.4293500.070.220.330.280.370.5493750.020.130.230.480.530.693 months sterling futures - £500,000 (points of 100%,)Dec 93.80Mar 93.40Jun 93.00It is now end of November. We wish to borrow £3M in March for 6 months.Interest is currently 6.5%.We wish to hedge against the interest rate rising above 6.5%.what will happen if interest rates rise by 1% and futures move by 0.95% using an option hedge at 9350.INTEREST RATE OPTIONS – ANSwERStep 1 Show options deal Month March Strike: 93.50 (equivalent to 6.5%) Put/Call PUT (always PUT!)Contracts: Length of loan£3M÷ £0.5M =12 contractscontract sizeStep 2Calculate Premium Payable12 ××= £5,550fromsize(Payable immediately)037.(3 months futures)Step 3Write down interest rate and futures price at start of loan.Interest 7.5%(6.5 +1)March Futures 92.45(93.40 – 0.95)(If futures price not given, then need to calculate in normal way)Step 4Illustrate what happens at start of loan Loan interest (at actual rate)£3M × 7.5% × 6⁄12 = 112,500(PAY)Exercise option(SELL FUTURES at strike;need to BUY FUTURES at current price to have something to sell!)1293509245400××−£0.5M contractssize(..)15,750(REC)96,750(at start of loan)Premium5,550(immediately)102,300Step 5Effective Interest rate:1023003000000100126,,,%××=6.82%Step 6Theoretical maximum interest rate.Strike 93.50 6.5%Premium 0.37%6.87%At other strikes:93.25 6.75%93.75 6.25%Premium0.25%Premium0.53%7.00%6.78%INTEREST RATE SwAPSExampleCompany X and company Y can borrow as follows:Fixed FloatingX 5% LIBORY 6% LIBOR + ½%Company X’s income fluctuates with interest rates, whilst Y’s does not. They both wish to borrow the same amount.Suggest a solution.EXCHANGE RATES - PREDICTING FUTURE SPOT RATESPurchasing power parityS S h h c b 1011=×++()()ExampleCurrent spot rate$/£ 1.52Inflation:US 4% p.a.;UK 2% p.a.What will be the spot rate in 1 and 2 years time?Answer:Spot rate in 1 years time =×=152104102155....in 2 years time =×=1521041021582.(..).GENERAL POINTS ABOUT RAISING DEBT FINANCE* Effect on gearing (mkt values if possible)* Effect on interest cover* Length of loan (match to life project)* Issue costs / arrangement fee* If borrowed in different currencyEffect of exchange rates onpayments– Interest– Payments of principal* Fixed / floating interest* Tax allowable? (Interest payments)* Credit rating of the company* Security to offer* Constraints on level of debt from Articles of Association or other loan agreement * Forecast cash flows to service and repay the debtCOMPANY PERSPECTIVE:Irredeemable debt:Cost to company:I(1-t)P 0 [not given](same as k d × (I – t) where k d is investors required yield)Example 1X plc has irredeemable debt with a coupon rate of 5%. Debt is currently trading at 70%. Corporation Tax is 33%.(i) What is return to investors?(ii) What is after tax cost of debt?==Redeemable debt:Cost to company = IRR of relevant cash flows by the company (net of tax where appropriate)Example 2Y plc has in issue 8% debentures redeemable in 4 years time at par.The current market value is 94p.c.Corporation Tax is 25%(i) What is kd (return to investors)?(ii) What is the cost of debt to the company?CONVERTIBLE DEBENTURES:Advantages To Company:* c an offer a lower rate of interest because of conversion potential* w ill not have to redeem if conversion is attractiveAdvantages To Investors:* fixed income / low risk, with potential for equity share if company’s prospects are good.FINDING COST OF DEBT FOR CONVERTIBLES(a) decide whether convertibles are likely to be converted or redeemed.If converted then ‘redemption price’should be value of shares at conversion(b) calculate IRR in normal way.Example8% debentures redeemable at par or convertible at conversion ratio of 25 at conversion price of $4, in 5 years time. MV of debentures: $95MV of shares: $3.90Dividends growing at 5% p.a.What is cost of debt to the company?WARRANTS:Give the holder to buy a specified number of shares at a specified price. Usually issued with debt, but can be de-tached and traded separately.Advantages To Company:* c an reduce the coupon required on related loan stock* p rovide a means of generating equity funds in future without immediate dilution of earningsAdvantages To Investors:* no income⇒ all profits are capital gains ⇒ may be tax saving (CGT allowance)* p otential for high profit on relatively low outlay.BANK LOANS(Usually) Less attractive form of debt financedue to • higher interest rate.• more likely to be floating rate.But: • may be more flexible• may give company credibility (checks on credit worthiness)• lower issue costs – good if ‘small’amountCALCULATION OF COST OF DEBT:Since repayable at ‘par’(i.e. no premium on redemption)Cost= k(1– t)dIf floating interest rate, use maximum forecast rate (if given) or (otherwise) current interest rate. But: potential for discussion.hedging)(riskINTEREST YIELD l REDEMPTION YIELDIn respect of traded debt & Government Securities, the newspaper quote the Interest Yield and Redemption Yield:Price Interest Yield Redemption Yield7% Govt. Stock 2007957.37%8.17%‘now’is 2000INTEREST YIELD:Int MVREDEMPTION YIELD:IRR of flows to investori.e.Int. Yield ignores redemption premium / loss.Red. Yield includes it.[in both cases – yields to investor. Before tax] Example8% Govt. Stock 2002 M.V:. 105 (‘now’is 2000)What are Int. Yld. & Red Yld.?YIELD CURVEThe yield curve shows the relationship between cost of debt (or redemption yield – only difference is the tax relief) and the term (period) to maturity (redemption) of that debt.debtUsually the curve is upward sloping to reflect the premium that investors want if investing long term. (normal yield curve)Sometimes, short term interest rates go higher than longer term rates (inverse yield curve). This happens if the market believes that interest rates will fall in the future.The shape of the yield curve indicates investors expectations about future interest rates:Upward sloping – they expect interest rates to riseDownward sloping – they expect interest rates to fallEUROMARKETSUsed for borrowing in foreign currency (eg: for funding investment in foreign currency) BANK BORROWINGEUROCURRENCY LOANS – short to medium termEUROCREDIT LOANS – medium to long termIn both cases – borrowing from bank(s)– low issue cost– usually floating rate interestISSUE OF BONDS / DEBENTURESEURONOTES – short to medium termEUROBONDS – medium to long termIn both cases – higher issue costs– longer time to arrangeinterest– lowerBonds may be made more attractive by being convertible or having warrants.If the company knows the share price, the dividend just paid, and can estimate future growth, then:k eD gPg =++1()calculates investors required return.As the company must provide what the shareholders want, the investors required return (ke ) is the cost of equityto the company.Since dividends are paid after charging corporation tax, ignore tax in the calculation of ke ExampleMV of equity is £1.20 (cum div.) per share. Dividend about to be paid 6p per share. Dividend growth: 14% p.a.Corp. Tax: 33%;Calculate(i) ke(ii) Cost of equity(iii) MV per share (ex div) in 2 years time.Equity(given) k DgP ge =++1()(shareholders required return = cost of equity)Debt(not given) k=I Pd(irredeemable)or IRR of flows (redeemable)(debt lenders required return)Cost of debt = k(1-T)or I(1-T) Pd[](assuming debt interest tax allowable) (irredeemable) or IRR of after tax flows (redeemable)Weighted average(given) WACC VV v kVV vk Tee d ede dd=+++−[][]()1[But strictly the formula for WACC is only correct for irredeemable debt. If debt is redeemable then‘kd(1 – T)’should be replaced by the IRR of the after-tax cash flows]Dividend growth rate(not given) Growth in dividends:Depending on the information given,Either:g1or: g = rbb = rate of retentionr = rate of return on re-investment (kein a perfect world!)ExampleA company is financed as follows:Equity: 5M $0.10 shares quoted at $0.37 ex div.Debt: $2M 8% loan stock quoted at 95 pc ex int, redeemable at par in 5 years timeThe company has paid dividends over the past 5 years as follows (current years dividend first): $250,000; $240,000; $220,000; $218,000; $200,000Calculate the WACC of company(Corporation Tax is 30%)Capital Asset Pricing Model(given) k=E=r+[E-r]e(r)f(r)fmi iβ(same formula for kd, using β of debt, but usually in exam assume debt is risk free, therefore β= 0,and kd = rf)ExampleCompany is financed as follows:Equity: 10M $0.50 shares, quoted at $1.20.Debt: $6M 9% irredeemable debenture (unquoted) The β of a share in the company is 0.85The market return is 20%, risk free rate is 12% Corporation Tax is 30%; Ignore Income Tax. Calculate:(a) the market value of debentures(b) the WACC of the companyModigliani & Miller (Summary)* Debt borrowing is cheaper than equity borrowing because less risky for investors (therefore require lower return) and debt interest gets tax relief.* Higher gearing results in more risk to shareholders (because of higher fixed interest payments). Therefore higher cost of equity (because shareholders want higher returns)*M odigliani and Millers model predicts how the shareholders required return will react to changes in gearing.k k T k k V V e e i e i d de=+−−()()1* Key assumptions:Rational investors Perfect information No transaction costs Debt is risk-free Irredeemable debtInvestors indifferent between personal & corporate gearing Debt interest gets full tax relief No personal taxesIgnores fear of bankruptcy Ignores agency costsExampleA is currently financed $8M from equity and $4M from debt. The cost of equity is currently 20%.They raise more debt and the gearing ratio changes to 80% (debt to equity)Risk free rate is 4%, Corporation Tax is 25%, default risk premium is 2%What is the current WACC?What will be the new WACC?COST OF CAPITAL (4) - AnSWerCurrent position: Cost of equity = k e = 20%Cost of debt = kd (1 – t ) = 6% × 0.75 = 4.5%WACC = ()()%.%.%81220412451483×+×=With current gearing:200756481375225%.(%) ..=+−=−k k k k e i e i e e i =1618.%With new gearing:k e = 16.18% + 0.75(16.18% – 6%) 0.8 = 16.18% + 6.11% = 22.29% New WACC = (22.29% × 50%) + (4.5% × 50%) = 13.4%CORPORATE DIVIDEND POLICYWhich is better:* p ayment of dividend nowor* r etention of earnings to reinvest to give capital gainsResidual theory:If a company can identify projects with positive NPV’s; it should invest in them. Dividends are only paid once the company runs out of these projects (a residual amount)Dividend irrelevancy (M&M)* M&M argued that only project cashflows and risk affect firm values & hence share price. Timing of dividends paid out is irrelevant.* I n a perfect world, if no dividends were paid one year because of investment opportunities, shareholders could create their own income by:(i) selling some sharesor(ii) borrowing against security of shareholdingPRACTICAL POINTS FOR COMPANY WHEN DECIDING ON DIVIDEND PAYOUT * a vailability of cash* availability of profits* signalling* d ividend policy of competition* profitability of current investment opportunities* ‘clientele effect’ALTERNATIVES TO CASH DIVIDENDSScrip dividends- Extra shares instead of cashShare Buy Back- Buy back shares at Pand cancel themNPV’sProforma:0123456 Sales receipts x x x x xCosts(x)(x)(x)(x)(x)Net operating flow x x x x xTax on operating flows(x)(x)(x)(x)(x) Capital Expenditure(x)Scrap proceeds xTax saved on Cap. Allowances x x x x x Working Capital(x)(x)(x)x x x(x)x x x x x x Discount factors x x x x x x x Present value(x)x x x x x x-show referenced workingsN.P.V.NPV POINTsINFLATION* I nflate flows and then discount at money (actual) cost of capital* I f long project and only one rate of inflation, then discount current price flows at real cost of capital.1r+=+ + 1 1ihr = real rate; i = nominal value (money rate); h = inflation rateTAXATION* W atch for timing assumptions - if not told then state assumption* S how tax saving on capital allowances (tax allowable depreciation) separately from tax on ‘profits’. OVERSEAS TRADE* I f evaluated from point of view of overseas subsidiary* c alculate NPV in foreign currency* I f evaluating from point of UK owner- calculate remittances in foreign currency- convert to £’s (maybe use formula to predict future exchange rates)- calculate NPV in £’s.DIsCOUNTING WITH INFLATIONTwo approaches:1. Inflate cash flows and then discount at actual (nominal) Cost of CapitalFlows before inflation Inflationat 5%Actual (nominal)cash flowsDiscountfactor at 15%Presentvalue at 15%0(50,000)(50,000)(50,000) 120,000x 1.05=21,000x0.870=18,270 230,000x(1.05)2=33,075x0.756=25,005 340,000x(1.05)3=46,305x0.658=30,469NPV$23,744 2. Discount current price flows at effective (real) Cost of Capital.1+r=1+h1+i=1.151.05=1.095r = 9.5% (say 10%)df @ 10%PV @ 10% 0(50,000)(50,000)120,0000.90918,180230,0000.82624,780340,0000.75130.040NPV$23,000In exam:• Either approach is accepted• For short project with different inflation rates, use approach 1• For long project with single inflation rate use approach 2• Always discount using tables at nearest %CAPM FORMULAE (r i ) = R f + βi (E (r m ) – R f )[given]Example 1If there is a market premium for risk of 12% and the risk free rate is 6%, what is the required return on a share with an equity beta of 1.5?Answer:Required return = 6% + 1.5 × 12% = 24%Example 2If market return is 12% and the risk rate is 5%, what is the required rate of return, k d , on debt which has a debt beta of 0.3? What is the cost of debt to the company if tax rate is 30%?Answer:Required return = 5% + 0.3 (12% – 5%) = 7.1%Cost of debt = k d (1 – t) = 7.1% × 0.7 = 4.97%[In words, β measures the systematic risk of an investment relative to the market (stock exchange) as a whole. β of 1.2 means that the investment is 1.2 times as risky (volatile) as the market. Or that fluctuations in returns will be 1.2 times as great.]ASSET BETA’SEquity β gives cost of equity Debt β gives cost of debtAsset β gives cost of capital for an ungeared version of the companyβββa ee d e d e d dv v v T v T v v T =+−+−+−[][](())()(())111[If debt β is missing, assume zero – almost certain to be the case in the exam)ExampleT has equity β of 1.2 and debt β of 0.2.R m = 12%; R f = 5%; tax = 33%T has £2M of equity and £0.5M of debt.Calculate T’s WACC.Calculate T’s WACC if it were all equity funded. Answer:Currently: k e = 5% + 1.2 (12% – 5%) = 13.4% k d = 5% + 0.2 (12% – 5%) = 6.4%WACC =+×++××−=220513405205641033..%...%(.)11.58% If all equity funded:βββa ee d e d e d d v v v T v T v v T =+−+−+−=[][](())()(())111 1......222033502033520335×++×+=1.0565WACC = k e = 5% + 1.0565 (12% – 5%) = 12.4%COMBINING β FACTORSTo find overall β of several investments, calculate the weighted average.ExampleCompany has MV of £50M and a β of 0.8. It is considering a project which will cost £10M, has NPV of £3M and a β of 0.6.What will β of company be if it undertakes the project having raised new finance to do so?Answer:M.V.βCurrent500.8Project (10 +3)130.663New β =×+×=506308136306..0.76α VALUESIn a perfect world, the return actually given by a share would equal the return required given by the CAPM formula. In practice the actual return might be different.α value is the difference between the two.ExampleICI currently gives a return of 19%It has β of 1.4Risk free rate = 10%.Market return = 16%.What is the α for ICI?[Obviously, we would not expect α to stay constant]Answer:Theoretical return = 10% +1.4(16% –10%)18.4%=Actual return = 19%α = 19% – 18.4%= +0.6%LIMITATIONS OF CAPM.* A ssumes investors have well-diversified portfolios* P erfect capital market- rational investors- perfect information- no transaction costs- investors can invest/borrow at same rate of interest* Single-period model* E stimates of risk free returnmarket returnβ factorARBITRAGE PRICING THEORY* a ssumes expected return on share depends on several independent factors * r= α + β1 (factor 1) + β2 (factor2) + .jfour suggested factors:(a) level of industrial activity(b) inflation rates(c) spread between long and short term interest rates(d) spread between yield of low and high risk corporate bondsSHOULD COMPANIES DIVERSIFY?No (in theory!) because shareholders can diversify themselves.BUT: m ay be profitable where:(a) shareholders are not diversified (small family companies)(b) company has opportunities not open to shareholders (China?)(c) diversification reduces risk of bankruptcy and therefore adds value.(d) Other synergistic gains or competitive advantages not open to separate companies.CAPITAL ASSET PRICING MODELSUMMARY* I f shareholders are well-diversified then they are only concerned with the systematic risk of investments.* T herefore (for large quoted companies where we assume shareholders overall are well-diversified) it is the systematic risk that determines the required return (and therefore the Cost of Equity)* W hen appraising new investments, it is the systematic risk of the investment that that should therefore de-termine the appraisal rate.* S ystematic risk is usually measured relative to the risk of the market (stock exchange as a whole) and quoted as a β factor.(β of 0.8 means investment is 80% as risky as the market)。

acca p4公式【1.ACCA P4考试简介】ACCA(Association of Chartered Certified Accountants,特许公认会计师公会)是全球知名的财务和会计专业资格认证。

P4是ACCA专业阶段考试中的一门,全称为“Applied Knowledge in Financial Management”(财务管理应用知识)。

该课程主要考察考生对财务管理领域各种工具、方法和实务的理解和应用能力。

【2.ACCA P4公式概述】在ACCA P4考试中,涉及众多财务管理相关的公式。

这些公式既包括基本的财务比率、现金流量和利润分配等,也包括复杂的估值、风险管理和企业战略等领域。

掌握这些公式对于考生在考试中取得优异成绩至关重要。

【3.重要公式及其应用】以下是ACCA P4考试中一些重要公式及其应用:1.财务比率:包括流动比率、速动比率、负债比率、权益比率、利润率、毛利率、净利润率等。

2.现金流量:包括经营现金流、投资现金流、筹资现金流等。

3.估值模型:包括市盈率(P/E)估值、市净率(P/B)估值、企业价值(EV)估值等。

4.风险管理:包括风险价值(VaR)、预期损失(ES)等。

5.企业战略:包括市占率、竞争力分析等。

【4.公式记忆与实践技巧】1.制定学习计划:合理安排时间,逐步掌握各个公式及其应用。

2.制作公式手册:将常用公式整理成手册,便于随时查阅。

3.做练习题:通过大量练习题巩固公式,提高实际应用能力。

4.参加模拟考试:模拟真实考试环境,检验自己的学习成果。

【5.结论与建议】ACCA P4考试对考生的财务管理知识体系提出了较高要求。

要想在考试中取得好成绩,熟练掌握相关公式是关键。

通过制定学习计划、制作公式手册、做练习题和参加模拟考试等方法,相信大家一定能掌握这些公式,并在考试中发挥出色。

祝各位考试顺利!请注意,以上内容仅供参考,实际考试要求可能会有所不同。

P4AdvancedFinancialManagement2008年9月份,我去曼彻斯特商学院的香港分校上MBA有幸见到了P4的考官BobRyan,他正好要给我上Financialanalysis的课程,课程共计4天,内容与P4的非常相近。

由于我在中新国际财经讲授3.7和P4也有三年了,这么好的机会是绝对不能错过的,也就尽一切可能向BobRyan询问一些关于P4考试相关的内容。

BobRyan非常的慷慨,有问必答,还给我copy了许多资料,绝对够我消化好几个月了。

BobRyan当前在英国各大商学院的财务管理和公司理财这系列的学科里赫赫有名,担任了许多大学商学院的教授,同时他也曾经担任英国另一个会计师组织ACA(ICAEW)一门paper的考官长达10多年,出题非常有经验。

2007年3.7的老考官ScottGoddard退休,新的科目P4就由BobRyan担任。

现在的P4与3.7的出题思路有很大的不同,ScottGoddard担任3.7考官长达20年之久,他的出题思路已经被广大讲师说熟知,而当前的P4,BobRyan刻意避免原来3.7的出题思路,而形成自己的出题风格。

BobRyan的题目读起来没有3.7那样直接,所以考生往往不太适应,有时候不知道他想要考那些东西。

但他出的题目更贴近实际,如果真正了解他的用意,那么题目就能比较容易的被求解出来,对学员ACCA读完后的财务工作的实际运用也很有帮助。

我们作为ACCA讲师,一项关键任务就是帮助学生了解考官的出题思路,并以一种比较快捷的方法解出题目的答案。

通过我在香港那几天的上课以及与BobRyan的沟通,基本上了解P4新的出题方向,下面就是我对P4考点新动向的一个总结:1.Costofcapital(WACC)Costofdebt(Kd)的计算以前3.7里计算Bond的Kd,只要算这个Bond的post-taxcashflow的IRR就可以。

而P4里算Kd,可能会出现两个和两个以上的Bond,所以更侧重于用Interestyieldcurve和公司的creditspread来计算。

中公财经培训网:/

做好ACCA备考对于ACCA考试非常的重要。

下面中公财经小编就P4阶段的备考,给大家详细的介绍一下。

具体情况如下所示;

P4考官的出题套路很难找。

套用考官自己的一句话,他从不根据历年真题来决定每次Exam要考什么知识点。

因为他认为P4是很tough的一门课,他不希望学生是投机取巧通过,而希望大家踏踏实实通过P4,他要求全大纲覆盖式的复习P4。

那我们对P4就只能依赖ACCA考试“非常注重实际应用,专注考核学生在在仿真的情境下解决问题的能力”,这个角度去做预测。

其实,企业战略高层所涉及的财务管理的专业能力,主要包括三大块内容:

(1)项目的投融资分析;

(2)公司收购与拆分;

(3)汇率或利润风险的管理。

对P4历年真题的研究发现,考官出题是比较偏实务的以上这三块内容要是抓住了,70%的分数就到手了。

另外,不要错认为P4是考计算的课程,P4考试55%是计算,45%是论述,论述中优缺点和assumption的出现的频率尤其高,考官认为P4计算部分比较难,顺利通过P4考试应该好好背论述题,那些才是easy mark。

他说当你WACC算不出来的时候,甚至可以猜一个%,用于NPV的discount,你依然可以得到大部分的分数,得分不在于数字的正确性,而在于解决问题的逻辑。

ACCA的P阶段选修课选择小技巧本文由高顿ACCA整理发布,转载请注明出处ACCA的选修课程包括有:P4-高级财务管理、P5-高级业绩管理、P6-高级税法和P7-高级审计。

其中,P6-高级税法即将在2010年12月起取消中国税法的考试。

因此,不建议您在此客观阶段选读这门课程。

在其它三门选修课中,P5-高级业绩管理则相对较容易,并且许多知识点与前面的课程联系较大,所以建议您可以考虑选读这门课程。

对于接下来的2门课程,您该如何做出正确的选择,从而顺利的通过考试呢?高顿财经的老师为您提供一些建议供参考:1: P7高级审计。

这门课程偏重于会计师事务所各类审计计划和报告,考试注重写作。

建议具有相关经验和擅长写作的同学可以考虑先选修这门课程,取得ACCA的qualification 后,如果需要也可再选修P4课程以进一步提高自身的能力。

P7的优势:在我国许多外资企业都希望把公司的审计和其他业务交给大型国际会计师事务所,而根据ACCA官方条例,大型国际会计师事务所的合伙人必须是ACCA的会员,并且必须是已经通过P6或P7的考试。

ACCA会员如果没有学习并通过P7的考试,即便将来有意向发展个人事业,开设自己的国际会计师事务所,还是需要回到课堂重新学习并通过该门课程考试。

2:ACCA课程中的P4-高级财务管理,此课程包含的知识点具有较强的实用性,例如:公司新项目投资评估、公司并购估值、公司财务或业务战略重组以及公司外汇及信用风险管理等,因此在此科目考试中各类计算占主要部分。

建议擅长计算的同学可优先报选读P4,在取得ACCA的qualification之后,您如果需要也可再选修P7课程,可以进一步提高自身的能力。

更多ACCA资讯请关注高顿ACCA官网:。

ACCA P4重点难点一:A Role of senior financial adviser in the multinational organisation 跨国公司中高级财务管理人员的职能1. The role and responsibility of senior financial executive/advisor 高级财务总监(咨询师)的功能和职责2. Financial strategy formulation 财务战略的形成3. Ethical and governance issues 商业道德和公司治理问题4. Management of international trade and finance 国际贸易和国际金融管理5. Strategic business and financial planning for multinational organisations 跨国公司商业战略和财务计划6. Dividend policy in multinationals and transfer pricing 跨国公司股利政策和转移定价A部分对财务管理实务中常用的知识点的考查,考查的面更广,包括behavioral finance 、free trade areas、customs unions和WTO;更为重要的是,相较于以前对知识点内容的考查,现在有一个趋势,是要求学员运用综合分析能力,对知识点进行灵活运用,这一点在第一道必选题中体现得特别明显。

所以要求学员不仅仅要记住内容,更重要的是会应用,要有分析框架、要有逻辑分析能力。

ACCA P4重点难点二:B Advanced investment appraisal 高级投资决策1. Discounted cash flow techniques 折现投资评价技术2. Application of option pricing theory in investment decisions 期权定价理论在投资决策中的应用3. Impact of financing on investment decisions and adjusted present values 融资对投资决策的影响和APV4. Valuation and the use of free cash flows 使用自由现金流进行估价5. International investment and financing decisions 国际投资和融资决策B部分高级投资决策是非常重要的内容,其中BSOP模型以及real option;Overseas NPV计算、APV、项目评估(流动性和风险角度),折现率的选择和计算(去杠杆和再杠杆方法的运用),债券投资(定价和估值、债券久期);投资决策中的国际投资项目评估、APV、FCFE、FEFF等内容都是非常重要的考核点。

ACCA P4最新备考经验分享这篇文章提供给大家一些考前的各种补充,希望各种准备程度的考生都能从中获益。

首先先重点说考试的结构,考试分为Section A和Section B两个部分,其中Section A为一道必答题,分值为50分;Section B包含3道题目,每道题分值25分,所以是从给出的三道题目中选择两道回答!是从给出的三道题目中选择两道回答!是从给出的三道题目中选择两道回答!重要的事情说三遍,因为前两天有一个已经第二次考P4的人居然和小编诉苦说做不完四道题目为什么这么多T^T,我能说什么呢,小编有的时候真的是不能放心(心塞)。

从P4之前2014年的改革之后,P4的主要内容分为四部:第一部分Investment,第二部分Merger& Acquisition,第三部分是Risk Management,剩余的知识统称为Others。

大家要根据自己在这几个模块中的能力来估算自己能否通过P4的考试。

在P4的考试中,题目分数的分配非常合理,50分文字,50分论述,所以对于中国学生来说,只要在擅长的计算部分可以多拿分,那么较为薄弱的论述部分压力就会大大减少。

所以大家要合理根据考试的内容安排自己最后所要重点关注复习的部分,争取保证能拿分的点至少要到60%~70%左右。

对于P4的考试技巧,答题上相信大家一路走来答题的方法已经不用我多说,每个考生都有自己非常独到的做题方法,方法怎么样不重要,重要的是适合你的答题节奏和思路就好。

所以这里还是要说一些最基本的方法:1.读题要先看Requirement,带着问题再去读题目可以帮助你快速识别重点信息,加快做题效率;2.答题结构,这点也是非常重要的,整洁有条理的答案其实是你通过P阶段考试最为重要的而又常常不被人注意的关键,在答题时如果计算类题目的workings一定不能只写计算过程,必须携带必要的文字叙述;。

acca阶段划分

ACCA 考试分为四个阶段,每个阶段都需要通过相应的考试才能进入下一阶段:

1. 知识课程(F1-F3):这是 ACCA 考试的第一阶段,主要涉及基础的财务和管理知识,包括财务会计、管理会计、商业法等。

这一阶段的考试主要测试学生对基本概念和原理的理解。

2. 技能课程(F4-F9):这是 ACCA 考试的第二阶段,主要涉及更深入的财务和管理技能,包括财务报告、审计、税务、财务管理等。

这一阶段的考试主要测试学生在实际工作中应用知识的能力。

3. 核心课程(P1-P3):这是 ACCA 考试的第三阶段,主要涉及战略管理和领导能力,包括公司治理、风险管理、战略财务管理等。

这一阶段的考试主要测试学生在复杂的商业环境中做出决策和管理的能力。

4. 选修课程(P4-P7):这是 ACCA 考试的最后一个阶段,学生可以选择自己感兴趣的领域进行深入学习,包括高级财务管理、高级审计与认证业务、高级税务等。

通过完成这四个阶段的考试,学生可以获得 ACCA 资格证书,并成为全球认可的专业会计师。

每个阶段的考试都需要学生具备相应的知识和技能,并且需要进行系统的学习和准备。