intermediate acct test bank chap19-21spr2010

- 格式:pdf

- 大小:117.21 KB

- 文档页数:29

附录SWIFT的使用第一节SWIFT的基本内容环球银行间金融电讯协会(Society of Worldwide Inter-bank Financial Telecommunication,SWIFT)。

1973年5月,由15个国家的239家银行在比利时共同创办了一个国际间非盈利性国际合作组织“环球银行间金融电讯协会”。

它的环球计算机数据通讯网在荷兰、美国和香港设有运行中心,在各会员国设有地区处理站,现有会员银行2281个,分会员银行3098个,参加用户1954个,用户总数7333个。

年处理电讯信息11亿多条(2000年统计数据),平均日处理信息500万多条,年信息处理量的平均增长速度为16.26%,其总部设在比利时,受比利时法律管辖。

二、SWIFT特点及其服务种类标准化的SWIFT电讯分为10大类:客户汇款与支票、银行头寸调拨、外汇买卖和存放款、托收、证券、贵金属和银团贷款、跟单信用证和保函、旅行支票、银行账务和SWIFT系统电报。

此外,SWIFT还提供金融衍生工具业务,例如利率掉期和远期外汇等。

每一类电讯根据业务内容分为若干格式,每种格式又由若干项目组成,根据业务要求选择相应的项目。

SWIFT电讯传递安全可靠,每份SWIFT电讯的发妥和收妥均得到自动证实,例如SWIFT 操作中心收到银行终端发出的电讯时,如果确认无误,将一份拷贝发回终端,并引述发电全文,加注ACK(收妥证实)。

如果发回的拷贝加注NAK,则表示该电讯未发妥,拷贝末尾注明未发妥原因。

电脑对收发电信号进行严格控制,自动完成编押和核押工作。

SWIFT密押的组成根据电文中的货币名称、金额、日期、电文中每一个字符作为编押依据,在每份电讯最后写上自动核押(SAC,SYSTEM AUTHENTIFICATION CORRECT)。

SWIFT的电路速度是普通电传的48-192倍,每份电讯的费用则只有普通邮件的2/3左右。

SWIFT的操作详细规定请参考《SWIFT操作指南》一书。

考试注意事项整个试卷共120题,听力部分有30道题,长度约25分钟,该部分结束后立即开始语法词汇部分,然后是填充部分和阅读部分。

这三部分时间统用,共80分钟。

听力录音长度约21分钟,共30题,其中10题有惩罚措施:做对得1分,做错扣0.5分。

因此建议:不要做没有把握的题。

阅读部分中第111-120题亦有惩罚措施:做对得1分;做错扣1分。

请先下载听力试题的声音文件(MP3格式。

按鼠标右键,用―目标另存为...‖将声音文件下载到硬盘上,然后用相关软件播放。

试题的标准答案附在最后。

请自己核对答案。

最终成绩的换算表:Part I Listening Comprehension (听力理解每个正确答案乘以 1Part II Grammar and Vocabulary (语法、词汇每个正确答案乘以 0.6Part III Cloze (填充每个正确答案乘以 0.8Part IV Reading Comprehension (阅读理解每个正确答案乘以 1四项换算后的成绩之和为总分。

满分为100分。

录取等级参考标准如下:高级班:65分以上中级班:50-64分准中级班:35-49分基础班:20-34分Part I Listening ComprehensionSection ADirections :In this section, you will hear 10 short statements. The statements will be spoken just once. They will not be written out for you, and you must listen carefully in order to understand what the speaker says.When you hear a statement, you will have a period of 15 to 20 seconds to read the four sentences in your test book and decide which one is closest in meaning to the statement you have heard. Then, on your answer sheet, find the number of the problem and mark your answer by drawing with a pencil a short bar across the corresponding letter in the brackets.Listen to the following example:You will hear:You will read:[A] He's been living in Beijing for a long time.[B] He used to live in Beijing.[C] He's gone to Beijing for a short visit.[D] He should stay longer in Beijing,Sentence [B] "He used to live in Beijing" is closest in meaning to the statement "He is no longer living in Beijing." Therefore you should choose answer [B].1. [A] Tom is riding a bike.[B] The bike is upside down.[C] Tom is repairing the bike.[D] Tom is cleaning his bike.2. [A] Professor Graff doesn't usually write on the blackboard.[B] Students are rarely bored in Professor Grafts class.[C] The professor uses graphs when she lectures.[D] Students in the graphic arts course don't take notes.3. [A] They are with them.[B] It is with them.[C] They are with her.[D] He is with her.4. [A] I passed the test because I studied hard.[B] I won't do well on the test if I don't study.[C] I failed the test because I didn't study enough.[D] I'll study hard so I can pass the test.5. [A] How long is the school term?[B] Why did you turn over the stool?[C] I wish I know how to get to the dormitory.[D] I want the term to end soon.6. [A] The boat owner must be rich.[B] This man must be the owner.[C] Those men are both rich.[D] The boat has a monkey on it.7. [A] Alice answered Jean's question.[B] Alice allowed Jean to respond.[C] Jean's response was questionable.[D] Alice accepted the answer.8.[A] Bob bought a new pair of sandals.[B] Bob's sandals were fixed.[C] The shoemaker only made sandals.[D] The shoemaker wore sandals.9.[A] We have to go to a party after work.[B] We are going to have a party when the house has been painted.[C] We went to a huge party after the house was painted.[D] We'll go to the party if the house is painted.10. [A] They read about the invention in the news report.[B] The inventor wrote an interesting news report.[C] A reporter asked the inventor some questions.[D] The reporter was watching the news.Section BDirections:In this section you will hear 10 short conversations between two speakers. At the end of each conversation, a question will be asked about what was said. You will hear the question only once. When you have heard the question, you will have a period of 15 to 20 seconds to read the four possible answers marked [A], [B], [C] and [D] and decide which is the best answer. Mark your answer on the answer sheet by drawing with a pencil a short bar across the corresponding letter in the brackets.Example :You will hear:'You will read:[A] At the office.[B] On his way to work.[C] Home in bed.[D] Away on vacation.From the conversation, we know that Bill is sick and will have to stay in bed until Monday. The best answer, then, is [C] "Home in bed." Therefore, you should choose answer [C].11. [A] On the steps.[B] By the window.[C] At s store.[D]In a bank.12. [A] It's almost time for lunch.[B] Only a few strawberries will be eaten at lunch.[C] There are just enough strawberries for lunch.[D] There won't be many people for lunch.13.[A] No one knows how Mary gets to work.[B] It's surprising that Mary could repair the record player.[C] She threw the old records away.[D] She doesn't think the record player works.14. [A] In a railroad station.[B] In a bus terminal.[C] In a restaurant.[D] In a hotel room.15. [A] At the information desk.[B] On the platform.[C] On the train.[D] Near the stairs.16. [A] Eighteen.[B] Nineteen.[C] Twenty.[D] Twenty-eight.17. [A] He gave homework.[B] He prepared a test.[C] He opened the book to page 20.[D] He went to the cinema.18. [A] He doesn't understand the question.[B] He will definitely not lend her the money.[C] He will lend her the money.[D] He might lend her the money.19. [A] She lost her money.[B] The price of postage went up.[C] She didn't know where the post office.[D] The post office was closed today.20. [A] Zero.[B] One.[C]Two.[D] Three.Section CDirections :In this section you will hear several brief talks and/or conversations. You will hear them once only. After each one, you will hear some questions. You will hear each question once only. After you hear the question, you will have 1 5 to 20 seconds to choose the best answer from the four choices given. Mark your answer on the answer sheet by drawing with a pencil a short bar across the corresponding letter in the brackets.21. [A] A person's character.[B] A person's voice characteristics.[C] A person's health.[D] A person's profession.22. [A] The strength of the speaker.[B] The force of air that comes from the lungs.[C] The weight of the speaker.[D] The height of the speaker.23. [A] The highness or lowness of sounds.[B] The loudness of sounds.[C] The force of sounds.[D] The speed of sounds.24. [A] The Student Activities Office will open.[B] Seniors will measure their heads.[C] Students will order new school hats.[D] Seniors will graduate.25. [A] All students[B] All seniors[C] All graduating seniors[D] All faculty26. [A] What kind of ceremony there will be[B] How to order the graduation outfit[C] How much to pay for the clothes[D] Where to go for graduation27. [A] Rent them[B] Buy them[C] Clean them[D] Measure them28. [A] Michael Jackson.[B] Muhammad Ali[C] A very famous actor.[D] A very famous and powerful president.29. [A] He was a gold medal winner in Olympics.[B] He is the younger brother of Michael Jackson.[C] He had some influence on the president of the U.S.[D] He is quite popular with the American young people today.30. [A] They usually don't live long.[B] They usually are quickly forgotten by the public.[C] They don't know where to hide themselves.[D] They are usually very fat.Part II Grammatical Structure and Vocabulary(30 minutesSection ADirections :There are 10 sentences in this section. Beneath each sentence there are 4 words or phrases marked [A], [B], [C] and [D]. Choose the one word or phrase that best completes the sentence. Mark your answer on the answer sheet by drawing with a pencil a short bar across the corresponding letter in the brackets.Example: I have been to the Great Wall three times ___ 1979.[A] from[B] after[C] for[D] sinceThe sentence should read, "I have been to the Great Wall three times since 1979." Therefore you should choose [D].31. Those foreign visitors look very ____.[A] smartly[B] wildly[C] like friends[D] friendly32.It ____ every day so far this month.[A] is raining[B] rains[C] has rained[D] rained33. James has just arrived, but I didn't know he ____ until yesterday.[A] will come[B] was coming[C] had been coming[D] came34. She ought to ___ my letter a week ago. But she was busy with her work.[A] have answered[B] answering[C] answer[D] be answered35. The house ____ windows are broken is unoccupied.[A] its[B] whose[C] which[D] those36. _____ of gold in California caused many people to travel west in hope of becoming rich.[A] The discovering[B] To discover[C] The discovery[D] On discovering37. _____ the Wright brothers successfully flew their airplane.[A] The century was beginning[B] It was the beginning of the century[C] At the beginning of the century[D] The beginning of the century38. After a brief visit to New Orleans,____.[A] returning to New York and beginning to write his greatest poetry did Walt . Whitman.[B] Walt Whitman returned to New York and began to write his greatest poetry.[C] Walt Whitman was writing his greatest poetry when he returned to New York.[D] having returned to New York Walt Whitman wrote his greatest poetry.39. We wish that you ____ such a lot of work , because we know that you would have enjoyed theparty.[A] hadn't had[B] hadn't[C] didn't have had[D] hadn't have40. Since your roommate is visiting her family this weekend, why_____ you have dinner with ustonight[A] will[B] won't[C]do[D] don'tSection BDirections :There are 10 sentences in this section. Each sentence has four parts underlined. The four underlined parts are marked [A], [B], [C] and [D]. Identify the one underlined part that is wrong. Mark your answer on the answer sheet by drawing with a pencil a short bar across the corresponding letter in the brackets.Example:A number of foreign visitors were taken to the industrial exhibition which they sawA B C Dmany new products.Answer [C] is wrong because the sentence should read, "A number of foreign visitors were taken to the industrial exhibition where they saw many new products." So you should choose[C].41. Thomas is most excellent in the family.A B C D42. By 1642 all towns in the colony of Massachusetts was required by law to have schools.A B C D43. Both moths and butterflies have a keen sense of sight, smell, and tasting.A B C D44.The plane took off after holding up for hours by fog.A B C D45. Smith sold most of his belongings. He has hardly nothing left in the house.A B C D46. The reason why I decided to come here is because this university has a goodA B CDepartment of English.D47.If he would have finished his paper a little sooner, he would have graduated this term.A B C D48. Most experts agree that there have never been such an exciting series ofA B Cbreakthroughs in the search for a cancer cure as we have seen recently.D49. If one does not have respect for himself, you cannot expect others to respect him.A B C D50. The South is mostly Democrat politically, when the North has both DemocratsA B C Dand Republicans.Section CDirections:There are 20 sentences in this section. Each sentence has a word or phrase underlined. There are four words or phrases beneath each sentence. Choose the one word or phrase which would best keep the meaning of the original sentence if it were substituted for the underlined part. Mark your choice on the answer sheet by drawing with a pencil a short bar across the corresponding letter in the brackets.Example: The initial step is often the most difficult.[A] quickest[B] longest[C] last[D] firstThe best answer is [D] because "first" has the same meaning as "initial" in the sentence. Therefore you should choose [D].51. The initial talks were the base of the later agreement.[A] first[B] quickest[C] last[D] longest52. She is quiet and pious at church in the morning but gossips all afternoon.[A]gentle[B] smiling[C]joyful[D] devout53. The weatherman said, "It will be chilly this afternoon."[A] wet[B] turbid[C] hot[D] cold54. He walked to his bedroom cautiously because he heard strange sounds in it.[A] happily[B] carefully[C] curiously[D] noisily55. Apparently she never got my letter after all.[A] Evidently[B] Disappointedly[C] Luckily[D] Anxiously56. Placing tags on ducks and geese as they migrate is one method of studying the behavior of birds.[A] sleep for winter[B] move from one place to another[C] flee their enemies[D] search for food57. In September, 1835, Darwin's vessel arrived at the Galapagos Islands.[A] assistant[B] cargo[C] ship[D] gun58. Movie studios often boost a new star with guest appearances on television talk shows.[A] attack[B] watch[C] denounce[D] promote59. When products advertise extensively on television, they are often ridiculously overpriced.[A] inexpensive[B] costly[C] valueless[D] overabundant60. John and his brother have entirely different temperaments.[A] likings[B] dispositions[C] tastes[D] objectives61. Seeds are contained in the center of fleshy fruit such as apples and pears.[A] core[B] focus[C] nucleus[D] median62. One of the responsibilities of a forest ranger is to drive slowly through the area in search of animals in distress.[A] cruise[B] tiptoe[C] skid[D] mare63. Mrs. Palmer was offended by the clerk's mean remark.[A] tasty[B] nasty[C] misty[D] musty64. Most recipients of the peace prize are given the award in person, but sometimes the award is givenposthumously.[A] when the person is out of the country[B] after the person has died[C] to political prisoners[D] by mail65. Seeing the Grand Canyon from the air is a sight to behold.[A] hold upon[B] remember[C] anticipate[D] gaze upon66: Mythical creatures have been a part of the folklore of many cultures throughout the centuries.[A] Appealing[B] Magical[C] Legendary[D] Fighting67. Everyone would like a panacea for health problems.[A] protection against[B] advice for[C] a cure-all for[D] a decrease in68. In the fall it is gratifying to see stalks of wheat ready for harvest.[A] terrifying[B] satisfying[C] surprising[D] relaxing69. A bad winter storm can paralyse an urban area.[A] immobilise[B] evacuate[C] isolate[D] stabilise70. Even though he was obese, Oliver Hardy gained fame as a comedian.[A] dying[B] crazy[C] unhappy[D]fatPart III ClozeDirections: For each blank in the following passage, choose the best answer from the choices in the column on the right. Then, on your answer sheet, find the number of the question and draw a short bar across the corresponding letter.There is a lot of luck in the drilling foroil. The [71] may just miss the oil although it is near;[72], it may strike oil at a fairly high[73]. When the drill goes down, itbrings [74] soil. The sample of soil from various depths areexamined for traces of [75]. If they are disappointed at one place, thedrillers go to [76]. Great sums ofmoney [77] spent, for example in the deserts of Egypt, in ‗prospecting‘ for oil. Sometimes[78] is found. When you buy a few gallons of petrol for our cars, we pay not only the [79] of the petrol, but also part of the cost if the search that 71.[A] time[B] man[C] drill[D] plan72. [A] at last[B] in the end[C] as a result[D] on the other hand73. [A] level[B] time[C] place[D] price74. [A] down[B] up[C] on[D] in75. [A] sand[B] water[C] oil[D] gas76. [A] another[B] the other[C] others[D] one another77. [A] are[B] is[C] has been[D] have been78. [A] a little[B] little[C] a few[D] few79. [A] amount[B] price[C] cost[D] drilling北京语言大学出国人员培训部/入学考试样题/2013is [ 80 ] going on.When the crude oil is obtained from the field, it is taken to the refineries.[ 81 ].The commonestform of treatment is [ 82 ]. When the oil is heated, the first vapours[ 83 ] are cooled and become the finest petrol. Petrol has a lowboiling[ 84 ]; if a little is poured into the hand, it soon vaporizes.Gas that comes off the [ 85 ] lateris condensed into paraffin. [ 86 ] the lubricating oils of variousgrades are produced. What [ 87 ] is heavy oil that is used as fuel.There are four main areas ofthe world [ 88 ] deposits of oil appear.The first is [ 89 ] of the Middle East.Another is thearea [ 90 ] North and South America, and the third, between Asia and Australia. The fourth area is the part near the North Pole. 80. [A] often[B] frequently[C] busily[D] always81. [A] to be treated[B] to treat[C] for treatment[D] for treating82. [A] heated[B] to be heated[C] to heat[D] heating83. [A] to rise[B] rises[C] rising[D] risen84. [A] level[B] place[C] point[D] degree85. [A] ground[B] air[C] oil[D] water86. [A] Then[B] Last of all[C] Afterwards[D] Lately87. [A] remains[B] remain[C] remained[D] remaining88. [A] there[B] which[C] that[D] where89. [A] the one[B] one[C] that[D] this90. [A] between[B] among[C] above[D] belowPart IV Reading Comprehension(40 minutesDirections:In this part there are passages followed by questions or unfinished statements, each with four suggested answers. Choose the one you think is the best answer. Mark your choice on the answer sheet by drawing with a pencil a short bar across the corresponding letter in the brackets. Questions 91-94 are based on the following passage:The fiddler crab is a living clock. It indicates the time of day by the color of its skin, which is dark by day and pale by night. The crab's changing skin color follows a regular 24-hour cycle that exactly matches the daily rhythm of the sun.Does the crab actually keep time, or does its skin simply respond to the sun's rays, changing color according to the amount of light that strikes it? To find out, biologists kept crabs in a dark room for two months. Even without daylight the crab's skin color continued to change precisely on schedule.This characteristic probably evolved in response to the rhythm of the sun, to help protect the crab from sunlight and enemies. After millions of years it has become completely regulated inside the living body of the crab.The biologists noticed that once each day the color of the fiddler crab is especially dark, and that each day this occurs fifty minutes later than on the day before. From this they discovered that each crab follows not only the rhythm of the sun but also that of the tides. The crab's period of greatest darkening is precisely the time of low tide on the beach where it was caught!91. The fiddler crab is like a clock because it changes color[A] in a regular 24-hour rhythm.[B] in response to the sun's rays.[C] at low tide.[D] every fifty minutes.92. The crab's changing color[A] tells the crab what time it is.[B] protects the crab from the sunlight and enemies.[C] keeps the crab warm.[D] is of no real use.93. When the fiddler crabs were kept in the dark, they[A] did not change color.[B] changed color more quickly.[C] changed color more slowly.[D] changed color on the same schedule.94. The best title for the passage is[A] The Rhythmic Cycles of the Sun and Tide[B] Discoveries in Biology[C] A Scientific Study[D] A living ClockThere is another example of the revolution in railway signaling and safety measures which can also be attributed to the widespread introduction of electricity in the last decade of the nineteenth century. The track circuit, patented by one William Robinson as far back as 1872, was based on a simple principle. A section of track is insulated at the rail joints from the adjoining sections, and an electrically-operated switch or relay is maintained in the closed position by a low-voltage current passing continually through the rails. The effect of the entry of a train on the insulated section is to short-circuit this current through its wheels and axles with the result that the switch opens. It will be appreciated that should the current fail or should an accidental short-circuit take place, the device will behave as if a train were on the section. However, it will obey the essential requirement of every safety device that in the event of failure the danger signal is given.95. What does the paragraph preceding this one probably discuss?[A] Another one of Robinson's inventions[B] A twentieth-century safety device[C] An electrically-operated safety device[D] Railroading in the mid-nineteenth century96. In the last sentence in the passage, what does the word "it" refer to?[A] An accidental short-circuit[B] A danger signal[C] A safety device[D] A train97. Which of the following statements is TRUE?[A] Railway signaling improved with the American Revolution.[B] The last century saw great progress in railway signaling device.[C] The track circuit is a simple application of a complex principle.[D] The widespread introduction of electricity took place around 1910.98. If a short-circuit takes place, what will happen to the section containing the safety device?[A] A fire will start.[B] A danger signal will be given.[C] A train will derail.[D] The electrically operated switch will close.99. What is the result when a train passed over a section with a low-voltage current?[A] It will derail.[B] A switch opens.[C] A danger signal is given.[D] It will shock the crew.100. What is the topic of this passage?[A] The development of electrical safety devices[B] The inventions of William Robinson[C] The danger of railroad accidents[D] The operation of an electrical safety device for trainsLife near the shore everywhere is affected by the tides, which come and go twice each day in a cycle of about twelve-and-a-half hours —just different enough from the daily cycle of the sun so that there can be no regular relationship between the shore being alternately wet and dry and alternately light and dark. The extent of the tides varies greatly, from as little as one foot in inland seas like the Mediterranean, to fifty feet or so in the Bay of Fundy in Nova Scotia. In some parts of the world, one of the two daily tides rises higher and falls lower than the other; and tides at the time of new moon and full moon are generally greater than at other times. The extent of the intertidal zone thus varies from day to day as well as from place to place.The kinds of organisms living in the region between the tidal limits depend very much on whether the shore is rocky, sandy, or muddy. Rocky shores have the most obviously rich faunas, because of the firm anchorage for both animals and plants, and because of the small pools left by the retreating seas. Sandy shores, especially when exposed to surf (as they usually are, have the fewest kinds of animals.101. Which of the following factors does not affect the extent of the tides?[A] Place[B] Time[C] The moon[D] The composition of the shore soil102. The time span between tides[A] varies as much as the extent of the tides.[B] is a more constant phenomenon than the extent of the tides.[C] is shorter in inland seas.[D] and the extent of tides depend upon each other.103. The two tides in a given day[A] may vary in extent.[B] never vary in extent.[C] always vary in extent.[D] only vary in extent at the time of a new moon or a full moon.104. The composition of the intertidal soil affect[A] the nature of tides.[B] the temperature of the water in that area.[C] the amount of animals and plants living in that area.[D] the level of pollution in that area.105. Muddy shores[A] have poorer faunas than do sandy shores.[B] have richer faunas than do rocky shores.[C] have poorer faunas than do rocky shores, but richer faunas than do sandy shores.[D] have no faunas at all.106. The smallest tides occur in[A] open seas.[B] inland.[C] bays.[D] deeper seas.Reading is the key to school success and, like any skill, it takes practice. A child learns to walk by practising until he no longer has to think about how to put one foot in front of the other. A great athlete practices until he can play quickly, accurately, without thinking. Tennis players call that "being in the zone." Educators call it "automaticity."A child learns to read by sounding out the letters and decoding the words. With practice, he stumbles less and less, reading by the phrase. With automaticity, he doesn't have to think about decoding the words, so he can concentrate on the meaning of the text.It can begin as early as first grade. In a recent study of children in Illinois schools, Alan Rossman of Northwestern University found automatic readers in the first grade who were reading almost three times as fast as the other children and scoring twice as high on comprehension tests. At fifth grade, the automatic readers were reading twice as fast as the others, and still outscoring them on accuracy, comprehension and vocabulary."It's not I.Q. but the amount of time a child spends reading that is the key to automaticity," according to Rossman. Any child who spends at least 3.5 to 4 hours a week reading books, magazines or newspapers will in all likelihood reach automaticity. At home, where the average child spends 25 hours a week watching television, it can happen by turning off the set just one night in favour of reading.You can test your child by giving him a paragraph or two to read aloud - something unfamiliar but appropriate to his age. If he reads aloud with expression, with a sense ofthe meaning of the sentences, he probably is an automatic reader. If he reads haltingly, one word at a time, without expression or meaning, he needs more practice.107. The first paragraph tells us____.[A] what automaticity is[B] how accuracy is acquired[C] how a child learns to walk[D] how an athlete is trained108. An automatic reader[A] sounds out the letters[B] concentrates on meaning[C] has a high I.Q.[D] pays much attention to the structures of sentences109. The Illinois study shows that the automatic reader's high speed[A] costs him a lot of work[B] affects his comprehension[C] leads to his future success[D] doesn't affect his comprehension110. A bright child[A] also needs practice to be an automatic reader[B] always achieves great success in comprehension tests[C] becomes an automatic reader after learning how to read[D] is a born automatic readerQuestions 111 - 116 are based on the following passage:The Triumph of Unreason?Neoclassical economics is built on the assumption that humans are rational beings who have a clear idea of their best interests and strive to extract maximum benefit (or―utility‖, in economist-speak from any situation. Neoclassical economics assumes that the process of decision-making is rational. But that contradicts growing evidence that decision-making draws on the emotions—even when reason is clearly involved.The role of emotions in decisions makes perfect sense. For situations met frequently in the past, such as obtaining food and mates, and confronting or fleeing from threats, the neural mechanisms required to weigh up the pros and cons will have been honed by evolution to produce an optimal outcome. Since emotion is the mechanism by which animals are prodded towards such outcomes, evolutionary and economic theory predict the same practical consequences for utility in these cases. But does this still apply when the ancestral machinery has to respond to the stimuli of urban modernity?One of the people who thinks that it does not is George Loewenstein, an economist at Carnegie Mellon University, in Pittsburgh. In particular, he suspects that modern shopping has subverted the decision-making machinery in a way that encourages people to run up debt. To prove the point he has teamed up with two psychologists, Brian Knutson of Stanford University and Drazen Prelec of the Massachusetts Institute of Technology, to look at what happens in the brain when it is deciding what to buy.。

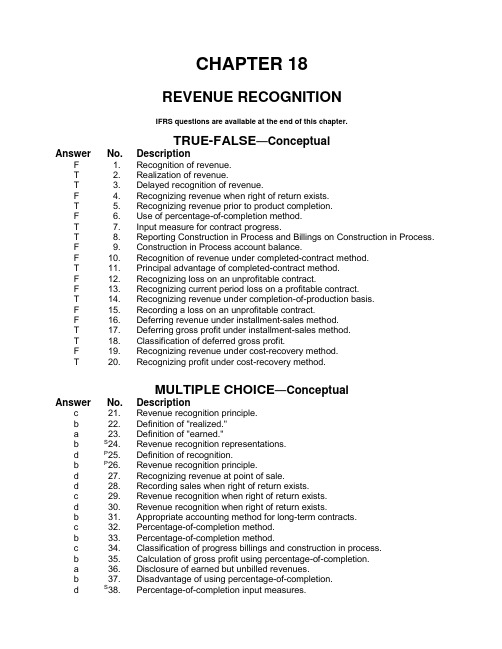

CHAPTER 18REVENUE RECOGNITIONIFRS questions are available at the end of this chapter.TRUE-FALSE—ConceptualAnswer No. DescriptionF 1. Recognition of revenue.T 2. Realization of revenue.T 3. Delayed recognition of revenue.F 4. Recognizing revenue when right of return exists.T 5. Recognizing revenue prior to product completion.F 6. Use of percentage-of-completion method.T 7. Input measure for contract progress.T 8. Reporting Construction in Process and Billings on Construction in Process.F 9. Construction in Process account balance.F 10. Recognition of revenue under completed-contract method.T 11. Principal advantage of completed-contract method.F 12. Recognizing loss on an unprofitable contract.F 13. Recognizing current period loss on a profitable contract.T 14. Recognizing revenue under completion-of-production basis.F 15. Recording a loss on an unprofitable contract.F 16. Deferring revenue under installment-sales method.T 17. Deferring gross profit under installment-sales method.T 18. Classification of deferred gross profit.F 19. Recognizing revenue under cost-recovery method.T 20. Recognizing profit under cost-recovery method.MULTIPLE CHOICE—ConceptualAnswer No. Descriptionc 21. Revenue recognition principle.b 22. Definition of "realized."a 23. Definition of "earned."b S24. Revenue recognition representations.d P25. Definition of recognition.b P26. Revenue recognition principle.d 27. Recognizing revenue at point of sale.d 28. Recording sales when right of return exists.c 29. Revenue recognition when right of return exists.d 30. Revenue recognition when right of return exists.b 31. Appropriate accounting method for long-term contracts.c 32. Percentage-of-completion method.b 33. Percentage-of-completion method.c 34. Classification of progress billings and construction in process.b 35. Calculation of gross profit using percentage-of-completion.a 36. Disclosure of earned but unbilled revenues.b 37. Disadvantage of using percentage-of-completion.d S38. Percentage-of-completion input measures.18 - 2Test Bank for Intermediate Accounting, Fourteenth EditionMULTIPLE CHOICE—Conceptual (cont.)Answer No. Descriptiona S39. Advantage of completed-contract methodc 40. Revenue, cost, and gross profit under the completed-contract method.a 41. Loss recognition on a long-term contract.c 42. Accounting for long-term contract losses.d 43. Criteria for revenue recognition of completion of production.a 44. Completion-of-production basis.d S45. Revenue recognition of completion of production.b S46. Treatment of estimated contract cost increase.c 47. Presentation of deferred gross profit.c 48. Appropriate use of the installment-sales method.b 49. Valuing repossessed assets.b 50. Gross profit deferred under the installment-sales method.c S51. Income realization on installment sales.d P52. Conservative revenue recognition method.b 53. Income recognition under the cost-recovery method.b 54. Income recognition under the cost-recovery method.d 55. Cost recovery basis of revenue recognition.b 56. Deposit method of revenue recognition.d 57. Cost recovery method.b *58. Types of franchising arrangements.d *59. Accounting for consignment sales.d *60. Allocation of initial franchise fee.a *61. Recognition of continuing franchise fees.b *62. Future bargain purchase option.a *63. Option to purchase franchisee's business agreement.d *64. Revenue recognition by the consignor.P These questions also appear in the Problem-Solving Survival Guide.S These questions also appear in the Study Guide.*This topic is dealt with in an Appendix to the chapter.MULTIPLE CHOICE—ComputationalAnswer No. Descriptionc 65. Computation of total revenue and accounts receivable.d 66. Computation of total construction expenses.b 67. Computation of costs and profits in excess of billings balance.c 68. Computation of total revenue and construction expenses.b 69. Gross profit recognized under percentage-of-completion.c 70. Computation of construction in process amount.c 71. Percentage-of-completion method.c 72. Percentage-of-completion method.b 73. Determine cash collected on long-term construction contract.d 74. Determine gross profit using percentage-of-completion.c 75. Gross profit to be recognized using percentage-of-completion.b 76. Gross profit to be recognized using percentage-of-completion.c 77. Profit to be recognized using completed-contract method.a 78. Gross profit to be recognized using percentage-of-completion.Revenue Recognition 18 - 3 MULTIPLE CHOICE—Computational (cont.)Answer No. Descriptionb 79. Profit to be recognized using completed-contract method.a 80. Gross profit to be recognized using percentage-of-completion.c 81. Gross profit to be recognized using completed-contract method.b 82. Computation of construction costs incurred.c 83. Gross profit recognized under percentage-of-completion.a 84. Computation of construction in process amount.b 85. Loss recognized using completed-contract method.c 86. Revenue recognition using completed-contract method.c 87. Reporting a current liability with completed-contract-method.a 88. Reporting inventory under completed-contract method.d 89. Gain recognized on repossession—installment sale.b 90. Calculate loss on repossessed merchandise.a 91. Calculate loss on repossessed merchandise.b 92. Interest recognized on installment sales.b 93. Calculation of deferred gross profit amount.b 94. Computation of realized gross profit amount.d 95. Computation of loss on repossession.d 96. Calculation of gross profit rate.a 97. Computation of net income from installment sales.d 98. Computation of realized and deferred gross profit.a 99. Calculation of gross profit rate.d 100. Computation of net income from installment sales.a 101. Computation of realized and deferred gross profit.c 102. Computation of realized gross profit amount.b 103. Computation of realized gross profit-cost recovery method.a 104. Revenue recognized under the cost-recovery method.d *105. Cancellation of franchise agreement.c *106. Accounting for initial and annual continuing franchise fees.b *107. Franchise fee with a bargain purchase option.d *108. Sales on consignment.a *109. Reporting inventory on consignment.MULTIPLE CHOICE—CPA AdaptedAnswer No. Descriptiona 110. FASB's definition of "recognition."b 111. Determine contract costs incurred during year.d 112. Gross profit to be recognized using percentage-of-completion.d 113. Profit to be recognized using completed-contract method.c 114. Revenue recognized under completed-production method.b 115. Determine balance of installment accounts receivable.c 116. Calculate deferred gross profit—installment sales.c 117. Calculate deferred gross profit—installment sales.c 118. Balance of deferred gross profit—installment sales.c 119. Reporting deferred gross profit—installment sales.a 120. Effect of collections received on service contracts.18 - 4Test Bank for Intermediate Accounting, Fourteenth EditionEXERCISESItem DescriptionE18-121 Revenue recognition (essay).E18-122 Revenue recognition (essay).E18-123 Long-term contracts (essay).E18-124 Journal entries—percentage-of-completion.E18-125 Percentage-of-completion method.E18-126 Percentage-of-completion method.E18-127 Percentage-of-completion and completed-contract methods. E18-128 Installment sales.E18-129 Installment sales.E18-130 Installment sales.*E18-131 Franchises.PROBLEMSItem DescriptionP18-132 Long-term construction project accounting.P18-133 Accounting for long-term construction contracts.P18-134 Long-term contract accounting—completed-contract.P18-135 Installment sales.CHAPTER LEARNING OBJECTIVES1. Apply the revenue recognition principle.2. Describe accounting issues for revenue recognition at point of sale.3. Apply the percentage-of-completion method for long-term contracts.4. Apply the completed-contract method for long-term contracts.5. Identify the proper accounting for losses on long-term contracts.6. Describe the installment-sales method of accounting.7. Explain the cost-recovery method of accounting.*8. Explain revenue recognition for franchises and consignment sales.Revenue Recognition 18 - 5 SUMMARY OF LEARNING OBJECTIVES BY QUESTIONSNote: TF = True-FalseMC = Multiple ChoiceE = ExerciseP = ProblemTest Bank for Intermediate Accounting, Fourteenth Edition18 - 6TRUE-FALSE—Conceptual1. Companies should recognize revenue when it is realized and when cash is received.2. Revenues are realized when a company exchanges goods and services for cash or claimsto cash.3. Delayed recognition of revenue is appropriate if the sale does not represent substantialcompletion of the earnings process.4. If a company sells its product but gives the buyer the right to return it, the company shouldnot recognize revenue until the sale is collected.5. Companies can recognize revenue prior to completion and delivery of the product undercertain circumstances.6. Companies must use the percentage-of-completion method when estimates of progresstoward completion are reasonably dependable.7. The most popular input measure used to determine the progress toward completion is thecost-to-cost basis.8. If the difference between the Construction in Process and the Billings on Construction inProcess account balances is a debit, the difference is reported as a current asset.9. The Construction in Process account includes only construction costs under thepercentage-of-completion method.10. Under the completed-contract method, companies recognize revenue and costs only whenthe contract is completed.11. The principal advantage of the completed-contract method is that reported revenue reflectsfinal results rather than estimates.12. Companies must recognize a loss on an unprofitable contract under the percentage-of-completion method but not the completed-contract method.13. A loss in the current period on a profitable contract must be recognized under both thepercentage-of-completion and completed-contract method.14. Under the completion-of-production basis, companies recognize revenue when agricul-tural crops are harvested since the sales price is reasonably assured and no significant costs are involved in product distribution.15. The provision for a loss on an unprofitable contract may be combined with the Constructionin Process account balance under percentage-of-completion but not completed-contract.16. Under the installment-sales method, companies defer revenue and income recognition untilthe period of cash collection.Revenue Recognition 18 - 7 17. The installment-sales method defers only the gross profit instead of both the sales priceand cost of goods sold.18. Deferred gross profit is generally treated as an unearned revenue and classified as acurrent liability.19. Under the cost-recovery method, a company recognizes no revenue or profit until cashpayments by the buyer exceed the cost of the merchandise sold.20. Companies recognize profit under the cost-recovery method only when cash collectionsexceed the total cost of the goods sold.MULTIPLE CHOICE—Conceptual21. The revenue recognition principle provides that revenue is recognized whena. it is realized.b. it is realizable.c. it is realized or realizable and it is earned.d. none of these.22. When goods or services are exchanged for cash or claims to cash (receivables), revenuesarea. earned.b. realized.c. recognized.d. all of these.23. When the entity has substantially accomplished what it must do to be entitled to thebenefits represented by the revenues, revenues area. earned.b. realized.c. recognized.d. all of these.Test Bank for Intermediate Accounting, Fourteenth Edition18 - 8S24. Which of the following is not an accurate representation concerning revenue recognition?a. Revenue from selling products is recognized at the date of sale, usually interpreted tomean the date of delivery to customers.b. Revenue from services rendered is recognized when cash is received or when serviceshave been performed.c. Revenue from permitting others to use enterprise assets is recognized as time passesor as the assets are used.d. Revenue from disposing of assets other than products is recognized at the date of sale. P25. The process of formally recording or incorporating an item in the financial statements of an entity isa. allocation.b. articulation.c. realization.d. recognition.P26. Dot Point, Inc. is a retailer of washers and dryers and offers a three-year service contract on each appliance sold. Although Dot Point sells the appliances on an installment basis, all service contracts are cash sales at the time of purchase by the buyer. Collections received for service contracts should be recorded asa. service revenue.b. deferred service revenue.c. a reduction in installment accounts receivable.d. a direct addition to retained earnings.27. Which of the following is not a reason why revenue is recognized at time of sale?a. Realization has occurred.b. The sale is the critical event.c. Title legally passes from seller to buyer.d. All of these are reasons to recognize revenue at time of sale.28. An alternative available when the seller is exposed to continued risks of ownership throughreturn of the product isa. recording the sale, and accounting for returns as they occur in future periods.b. not recording a sale until all return privileges have expired.c. recording the sale, but reducing sales by an estimate of future returns.d. all of these.29. A sale should not be recognized as revenue by the seller at the time of sale ifa. payment was made by check.b. the selling price is less than the normal selling price.c. the buyer has a right to return the product and the amount of future returns cannot bereasonably estimated.d. none of these.Revenue Recognition 18 - 9 30. The FASB concluded that if a company sells its product but gives the buyer the right toreturn the product, revenue from the sales transaction shall be recognized at the time of sale only if all of six conditions have been met. Which of the following is not one of these six conditions?a. The amount of future returns can be reasonably estimated.b. The seller's price is substantially fixed or determinable at time of sale.c. The buyer's obligation to the seller would not be changed in the event of theft ordamage of the product.d. The buyer is obligated to pay the seller upon resale of the product.31. In selecting an accounting method for a newly contracted long-term construction project,the principal factor to be considered should bea. the terms of payment in the contract.b. the degree to which a reliable estimate of the costs to complete and extent of progresstoward completion is practicable.c. the method commonly used by the contractor to account for other long-term construc-tion contracts.d. the inherent nature of the contractor's technical facilities used in construction.32. The percentage-of-completion method must be used when certain conditions exist. Whichof the following is not one of those necessary conditions?a. Estimates of progress toward completion, revenues, and costs are reasonablydependable.b. The contractor can be expected to perform the contractual obligation.c. The buyer can be expected to satisfy some of the obligations under the contract.d. The contract clearly specifies the enforceable rights of the parties, the consideration tobe exchanged, and the manner and terms of settlement.33. When work to be done and costs to be incurred on a long-term contract can be estimateddependably, which of the following methods of revenue recognition is preferable?a. Installment-sales methodb. Percentage-of-completion methodc. Completed-contract methodd. None of these34. How should the balances of progress billings and construction in process be shown atreporting dates prior to the completion of a long-term contract?a. Progress billings as deferred income, construction in progress as a deferred expense.b. Progress billings as income, construction in process as inventory.c. Net, as a current asset if debit balance, and current liability if credit balance.d. Net, as income from construction if credit balance, and loss from construction if debitbalance.35. In accounting for a long-term construction-type contract using the percentage-of-completion method, the gross profit recognized during the first year would be the estimated total gross profit from the contract, multiplied by the percentage of the costs incurred during the year to thea. total costs incurred to date.b. total estimated cost.c. unbilled portion of the contract price.d. total contract price.18 - 10Test Bank for Intermediate Accounting, Fourteenth Edition36. How should earned but unbilled revenues at the balance sheet date on a long-termconstruction contract be disclosed if the percentage-of-completion method of revenue recognition is used?a. As construction in process in the current asset section of the balance sheet.b. As construction in process in the noncurrent asset section of the balance sheet.c. As a receivable in the noncurrent asset section of the balance sheet.d. In a note to the financial statements until the customer is formally billed for the portionof work completed.37. The principal disadvantage of using the percentage-of-completion method of recognizingrevenue from long-term contracts is that ita. is unacceptable for income tax purposes.b. gives results based upon estimates which may be subject to considerable uncertainty.c. is likely to assign a small amount of revenue to a period during which much revenuewas actually earned.d. none of these.S38. One of the more popular input measures used to determine the progress toward completion in the percentage-of-completion method isa. revenue-percentage basis.b. cost-percentage basis.c. progress completion basis.d. cost-to-cost basis.S39. The principal advantage of the completed-contract method is thata. reported revenue is based on final results rather than estimates of unperformed work.b. it reflects current performance when the period of a contract extends into more thanone accounting period.c. it is not necessary to recognize revenue at the point of sale.d. a greater amount of gross profit and net income is reported than is the case when thepercentage-of-completion method is used.40. Under the completed-contract methoda. revenue, cost, and gross profit are recognized during the production cycle.b. revenue and cost are recognized during the production cycle, but gross profitrecognition is deferred until the contract is completed.c. revenue, cost, and gross profit are recognized at the time the contract is completed.d. none of these.41. Cost estimates on a long-term contract may indicate that a loss will result on completion ofthe entire contract. In this case, the entire expected loss should bea. recognized in the current period, regardless of whether the percentage-of-completion orcompleted-contract method is employed.b. recognized in the current period under the percentage-of-completion method, but thecompleted-contract method should defer recognition of the loss to the time when thecontract is completed.c. recognized in the current period under the completed-contract method, but thepercentage-of-completion method should defer the loss until the contract is completed.d. deferred and recognized when the contract is completed, regardless of whether thepercentage-of-completion or completed-contract method is employed.42. Cost estimates at the end of the second year indicate a loss will result on completion of theentire contract. Which of the following statements is correct?a. Under the completed-contract method, the loss is not recognized until the year theconstruction is completed.b. Under the percentage-of-completion method, the gross profit recognized in the firstyear must not be changed.c. Under the completed-contract method, when the billings exceed the accumulated costs,the amount of the estimated loss is reported as a current liability.d. Under the completed-contract method, when the Construction in Process balanceexceeds the billings, the estimated loss is added to the accumulated costs.43. The criteria for recognition of revenue at the completion of production of precious metalsand farm products includea. an established market with quoted prices.b. low additional costs of completion and selling.c. units are interchangeable.d. all of these.44. In certain cases, revenue is recognized at the completion of production even though nosale has been made. Which of the following statements is not true?a. Examples involve precious metals or farm equipment.b. The products possess immediate marketability at quoted prices.c. No significant costs are involved in selling the product.d. All of these statements are true.S45. For which of the following products is it appropriate to recognize revenue at the completion of production even though no sale has been made?a. Automobilesb. Large appliancesc. Single family residential unitsd. Precious metalsS46. When there is a significant increase in the estimated total contract costs but the increase does not eliminate all profit on the contract, which of the following is correct?a. Under both the percentage-of-completion and the completed-contract methods, theestimated cost increase requires a current period adjustment of excess gross profitrecognized on the project in prior periods.b. Under the percentage-of-completion method only, the estimated cost increase requiresa current period adjustment of excess gross profit recognized on the project in priorperiods.c. Under the completed-contract method only, the estimated cost increase requires acurrent period adjustment of excess gross profit recognized on the project in priorperiods.d. No current period adjustment is required.47. Deferred gross profit on installment sales is generally treated as a(n)a. deduction from installment accounts receivable.b. deduction from installment sales.c. unearned revenue and classified as a current liability.d. deduction from gross profit on sales.48. The installment-sales method of recognizing profit for accounting purposes is acceptable ifa. collections in the year of sale do not exceed 30% of the total sales price.b. an unrealized profit account is credited.c. collection of the sales price is not reasonably assured.d. the method is consistently used for all sales of similar merchandise.49. The method most commonly used to report defaults and repossessions isa. provide no basis for the repossessed asset thereby recognizing a loss.b. record the repossessed merchandise at fair value, recording a gain or loss if appropriate.c. record the repossessed merchandise at book value, recording no gain or loss.d. none of these.50. Under the installment-sales method,a. revenue, costs, and gross profit are recognized proportionate to the cash that isreceived from the sale of the product.b. gross profit is deferred proportionate to cash uncollected from sale of the product, buttotal revenues and costs are recognized at the point of sale.c. gross profit is not recognized until the amount of cash received exceeds the cost of theitem sold.d. revenues and costs are recognized proportionate to the cash received from the sale ofthe product, but gross profit is deferred until all cash is received.S51. The realization of income on installment sales transactions involvesa. recognition of the difference between the cash collected on installment sales and thecash expenses incurred.b. deferring the net income related to installment sales and recognizing the income ascash is collected.c. deferring gross profit while recognizing operating or financial expenses in the periodincurred.d. deferring gross profit and all additional expenses related to installment sales until cashis ultimately collected.P52. A manufacturer of large equipment sells on an installment basis to customers with questionable credit ratings. Which of the following methods of revenue recognition is least likely to overstate the amount of gross profit reported?a. At the time of completion of the equipment (completion of production method)b. At the date of delivery (sales method)c. The installment-sales methodd. The cost–recovery method53. A seller is properly using the cost-recovery method for a sale. Interest will be earned on thefuture payments. Which of the following statements is not correct?a. After all costs have been recovered, any additional cash collections are included inincome.b. Interest revenue may be recognized before all costs have been recovered.c. The deferred gross profit is offset against the related receivable on the balance sheet.d. Subsequent income statements report the gross profit as a separate item of revenuewhen it is recognized as earned.54. Under the cost-recovery method of revenue recognition,a. income is recognized on a proportionate basis as the cash is received on the sale ofthe product.b. income is recognized when the cash received from the sale of the product is greaterthan the cost of the product.c. income is recognized immediately.d. none of these.55. Winser, Inc. is engaged in extensive exploration for water in Utah. If, upon discovery ofwater, Winser does not recognize any revenue from water sales until the sales exceed the costs of exploration, the basis of revenue recognition being employed is thea. production basis.b. cash (or collection) basis.c. sales (or accrual) basis.d. cost recovery basis.56. The deposit method of revenue recognition is used whena. the product can be marketed at quoted prices and units are interchangeable.b. cash is received before the sales transaction is complete.c. the contract is short-term or the percentage-of-completion method can’t be used.d. there are no significant costs of distribution.57. The cost-recovery methoda. is prohibited under current GAAP due to its conservative nature.b. requires a company to defer profit recognition until all cash payments are received fromthe buyer.c. is used by sellers when there is a reasonable basis for estimating collectibility.d. recognizes total revenue and total cost of goods sold in the period of sale.*58. Types of franchising arrangements include all of the following excepta. service sponsor-retailer.b. wholesaler-service sponsor.c. manufacturer-wholesaler.d. wholesaler-retailer.*59. In consignment sales, the consigneea. records the merchandise as an asset on its books.b. records a liability for the merchandise held on consignment.c. recognizes revenue when it ships merchandise to the consignor.d. p repares an “account report” for the consignor which shows sales, expenses, and cashreceipts.*60. Some of the initial franchise fee may be allocated toa. continuing franchise fees.b. interest revenue on the future installments.c. options to purchase the franchisee's business.d. All of these may reduce the amount of the initial franchise fee that is recognized asrevenue.。

Name: __________________________Section: 501University of Texas at ArlingtonMid-Term 3Acct 5311- Spring 2008Chandra SubramaniamTHIS EXAM IS 80 MINUTES LONG.This exam consists of 3 problems. The first problem uses the multiple choice format. Please use your Scantron sheet for this section. Answer the remaining problems in the space provided in this exam. Please make sure that you have ten (10) pages including this cover page.There are 100 total possible points. Allocate an appropriate amount of time to each question. The only materials you are permitted to use on this exam are (1) a calculator, (2) a pencil with eraser or pen.Be sure to note the relevant dates referred to in each question.Point AllocationProblem 1 (40)Problem 2 (40)Problem 3 (20)Total Possible points 100GOOD LUCK!Multiple Choice ( 2 points each)1. Cotton Hotel Corporation recently purchased Holiday Hotel and the land on which it islocated with the plan to tear down the Holiday Hotel and build a new luxury hotel on the site. The cost of the Holiday Hotel should bea. depreciated over the period from acquisition to the date the hotel is scheduled to betorn down.b. written off as an extraordinary loss in the year the hotel is torn down.c. capitalized as part of the cost of the land.d. capitalized as part of the cost of the new hotel.2. If a corporation purchases a lot and building and subsequently tears down the buildingand uses the property as a parking lot, the proper accounting treatment of the cost of the building would depend ona. the significance of the cost allocated to the building in relation to the combined costof the lot and building.b. the length of time for which the building was held prior to its demolition.c. the contemplated future use of the parking lot.d. the intention of management for the property when the building was acquired.3. Assets that qualify for interest cost capitalization includea. assets under construction for a company's own use.b. assets that are ready for their intended use in the earnings of the company.c. assets that are not currently being used because of excess capacity.d. All of these assets qualify for interest cost capitalization.4. Which of the following statements is true regarding capitalization of interest?a. Interest cost capitalized in connection with the purchase of land to be used as abuilding site should be debited to the land account and not to the building account.b. The amount of interest cost capitalized during the period should not exceed theactual interest cost incurred.c. When excess borrowed funds not immediately needed for construction aretemporarily invested, any interest earned should be offset against interest costincurred when determining the amount of interest cost to be capitalized.d. The minimum amount of interest to be capitalized is determined by multiplying aweighted average interest rate by the amount of average accumulated expenditureson qualifying assets during the period.5. The King-Kong Corporation exchanges one plant asset for a similar plant asset andgives cash in the exchange. The exchange is not expected to cause a material change in the future cash flows for either entity. If a gain on the disposal of the old asset is indicated, the gain willa. be reported in the Other Revenues and Gains section of the income statement.b. effectively reduce the amount to be recorded as the cost of the new asset.c. effectively increase the amount to be recorded as the cost of the new asset.d. be credited directly to the owner's capital account.6. An improvement made to a machine increased its fair market value and its productioncapacity by 25% without extending the machine's useful life. The cost of the improvement should bea. expensed.b. debited to accumulated depreciation.c. capitalized in the machine account.d. allocated between accumulated depreciation and the machine account.7. Tyson Chandler Company purchased equipment for $10,000. Sales tax on the purchasewas $500. Other costs incurred were freight charges of $200, warranty costs of one year for $350, and installation costs of $225. What is the cost of the equipment?a. $10,000b. $10,500c. $10,925d. $11,2758. Ben Gordon Corporation constructed a building at a cost of $10,000,000. Averageaccumulated expenditures were $4,000,000, actual interest was $600,000, and avoidable interest was $300,000. If the salvage value is $800,000, and the useful life is40 years, depreciation expense for the first full year using the straight-line method isa. $237,500.b. $245,000.c. $257,500.d. $337,500.9. Quayle Company acquired machinery on January 1, 2002 which it depreciated under thestraight-line method with an estimated life of fifteen years and no salvage value. On January 1, 2007, Quayle estimated that the remaining life of this machinery was six years with no salvage value. How should this change be accounted for by Quayle?a. As a prior period adjustmentb. As the cumulative effect of a change in accounting principle in 2007c. By setting future annual depreciation equal to one-sixth of the book value on January1, 2007d. By continuing to depreciate the machinery over the original fifteen year life10. George Martin Corporation purchased a depreciable asset for $300,000 on January 1,2005. The estimated salvage value is $30,000, and the estimated useful life is 9 years.The straight-line method is used for depreciation. In 2008, George Martin changed its estimates to a total useful life of 5 years with a salvage value of $50,000. What is 2008 depreciation expense?a. $30,000b. $50,000c. $80,000d. $90,000was estimated to have a useful life of 10 years with an estimated salvage value of $42,000. During 2007, it became apparent that the machine would become uneconomical after December 31, 2011, and that the machine would have no scrap value. Accumulated depreciation on this machine as of December 31, 2006, was $177,000. What should be the charge for depreciation in 2007 under generally accepted accounting principles?a. $106,200b. $114,600c. $123,000d. $143,25012. Klein Co. purchased machinery on January 2, 2001, for $440,000. The straight-linemethod is used and useful life is estimated to be 10 years, with a $40,000 salvage value.At the beginning of 2007 Klein spent $96,000 to overhaul the machinery. After the overhaul, Klein estimated that the useful life would be extended 4 years (14 years total), and the salvage value would be $20,000. The depreciation expense for 2007 should bea. $28,250.b. $34,500.c. $40,000.d. $37,000.13. In January, 2007, Miley Corporation purchased a mineral mine for $3,400,000 withremovable ore estimated by geological surveys at 2,000,000 tons. The property has an estimated value of $200,000 after the ore has been extracted. The company incurred $1,000,000 of development costs preparing the mine for production. During 2007, 500,000 tons were removed and 400,000 tons were sold. What is the amount of depletion that Miley should expense for 2007?a. $640,000b. $800,000c. $840,000d. $1,120,00014. A plant asset with a five-year estimated useful life and no residual value is sold at theend of the second year of its useful life. How would using the sum-of-the-years'-digits method of depreciation instead of the double-declining balance method of depreciation affect a gain or loss on the sale of the plant asset?Gain Lossa. Decrease Decreaseb. Decrease Increasec. Increase Decreased. Increase Increaseestimated useful life of five years and a salvage value of $80,000. The machine is being depreciated from the date of acquisition by the 150% declining-balance method. For the year ended December 31, 2007, Gant should record depreciation expense on this machine ofa. $120,000.b. $80,000.c. $60,000.d. $48,000.16. Mack Co. takes a full year's depreciation expense in the year of an asset's acquisitionand no depreciation expense in the year of disposition. Data relating to one of Mack's depreciable assets at December 31, 2007 are as follows:Acquisition year 2005Cost $140,000Residual value 20,000Accumulated depreciation 96,000Estimated useful life 5 yearsUsing the same depreciation method as used in 2005, 2006, and 2007, how much depreciation expense should Mack record in 2008 for this asset?a. $16,000b. $24,000c. $28,000d. $32,00017. Wriglee, Inc. went to court this year and successfully defended its patent from infringe-ment by a competitor. The cost of this defense should be charged toa. patents and amortized over the legal life of the patent.b. legal fees and amortized over 5 years or less.c. expenses of the period.d. patents and amortized over the remaining useful life of the patent.18. A loss on impairment of an intangible asset is the difference between the asset’sa. carrying amount and the expected future net cash flows.b. carrying amount and its fair value.c. fair value and the expected future net cash flows.d. book value and its fair value.19. If a company constructs a laboratory building to be used as a research and developmentfacility, the cost of the laboratory building is matched against earnings asa. research and development expense in the period(s) of construction.b. depreciation deducted as part of research and development costs.c. depreciation or immediate write-off depending on company policy.d. an expense at such time as productive research and development has beenobtained from the facility.20. Blue Sky Company’s 12/31/08 balance sheet reports assets of $5,000,000 and liabilitiesof $2,000,000. All of Blue Sky’s assets’ book values approximate their fair value, except for land, which has a fair value that is $300,000 greater than its book value. On 12/31/08, Horace Wimp Corporation paid $5,100,000 to acquire Blue Sky. What amount of goodwill should Horace Wimp record as a result of this purchase?a. $ -0-b. $100,000c. $1,800,000d. $2,100,000Problem 2 (40 points)Part A. Two independent companies, Mintz Co. and Pine Co., are in the home building business. They agree to exchange their equipment for the other. An appraiser was hired, and from her report and the companies' records, the following information was obtained:Mintz's Equipment Pine's Equipment Cost $392,000 $220,000Accumulated Depreciation 200,000 100,000Fair value based upon appraisal 240,000 210,000The exchange was made, and based on the difference in appraised fair values, Pine paid $30,000 to Mintz. The exchange lacked commercial substance. (20 points)a. Determine the amount of pre-tax gain or loss Mintz should recognize on this exchangeb. Determine the amount at which the new equipment should be reported in Mintz's booksc. Determine the amount of pre-tax gain or loss Pine should recognize on this exchanged) Determine the amount at which the new equipment should be reported in Pine's books Part B. On June 1, 2004, Wordcrafters contracted with Favre Construction to have a new building constructed for $5,000,000 on land owned by Wordcrafters. The payments made byWordcrafters to Favre Constructions are shown in the schedule below.Date AmountJuly 30, 2004 $1,200,000Jan 30, 2005 1,500,000May 30, 2005 1,300,000July 30, 2005 1,000,000Aug 30, 2005 500,000Total Payments $5,500,000Construction was completed and the building was ready for occupancy on September 30, 2005. Wordcrafters borrowed $2 million on June 1, 2004 at 10% expressly for the construction of the new building. They had the following debt outstanding at May 31, 2005, and 2006, the end of its fiscal year.14.5%, 5-year note payable of $2,000,000, dated April 1, 2001, with interest payable annually on April 1.12%, 10-year bond issue of $3,000,000 sold at June 30, 1997, with interest payable annually on June 30.Required:a. Compute the avoidable interest on Wordcraft ers’ new building for fiscal year 2005. (5points)b. Prepare the adjusting journal on May 31, 2005 to account for the interest expense. (5 points)c. Compute the avoidable interest on Wordcrafters’ new building for fiscal year 2006. (5points)d. Determine the cost of the building reported in Wordcrafters books on May 31, 2006. (5 points)Problem 3 (20 points)Wardell Company purchased a minicomputer on January 1, 2001, at a cost of $40,000. The computer was depreciated using the 200% declining balance method over an estimated five-year life with an estimated residual value of $4,000. The company’s fiscal year ends on December 31.a) Prepare the journal entry required for depreciation in 2002b) On July 1, 2003, the estimate of useful life was changed to a total of 8 years (from thedate of the original purchase), and the estimate of residual value was changed to$900.Prepare the appropriate journal entries required for depreciation in 2003 to reflect the revised estimate.c) On March 31, 2004 Wardell spent $15,000 on the minicomputer to improve itsperformance (consider this a betterment). Prepare the appropriate journal entries for the year 2004 including the adjusting journal entry required for depreciation.d) On April 31, 2006 Wardell sold the minicomputer for $20,000. Prepare the appropriatejournal entries on this date.Multiple choice1. c2. d3. a4. b5. b6. c7. c8. a9. c 10. c11. b 12. b 13. c 14. b 15. c 16. a 17. d 18. b 19. b 20. cProblem 2Part Aa) For Mintz BV = $192,000, FMV = $240,000 Gain = $48,000 and Mintz receives cashhence a portion of the asset sold and a portion traded.Portion sold = Cash/Cash+ FMV of new asset = $30,000/($30,000+210,000) = 12.5%Gain recognized = 12.5% * $48,000 = $6,000b) New equipment value = FMV –– 42,000 = $168,000.c)portion is traded. Gain recognized = 0.d) – 90,000 = $150,000Part Ba. 1,200,000 * 10/10 = $1,200,0001,500,000 * 4/10 = 600,0001,300,000 * 0/10 = 04,000,000 WAAE 1,800,000Avoidable or Capitalized interest = 1,800,000*10%*10/12 = $150,000b. 2,000,000*14.5% = 290,0002,000,000*10% = 200,0003,000,000*12% = 360,000850,000 (actual interest)CIP 150,000 or CIP $150,000Interest Expense 700,000 Interest Exp 700,000Cash 471,666 Int pay/Cash $850,000Interest Payable 378,334c. 4,150,000 *4/4 = 4,150,0001,000,000 *2/4 = 500,000500,000 *1/4 = 125,0005,650,000 WAAE 4,775,0002,000,000*10%*4/12 = 66,6672,775,000*13%*4/12 = 120,2504,775,000 186,917Avoidable interest = $186,917d. 5,650,000+186,917=$5,836,917Alternatively using 12 months windows.a) 1,200,000 * 10/12 = $1,000,0001,500,000 * 4/12 = 500,0001,300,000 * 0/12 = 04,000,000 WAAE 1,500,000Avoidable or Capitalized interest = 1,500,000*10% = $150,000b) The answer is exactly the samec) 4,150,000 *4/12 = 1,383,3331,000,000 *2/12 = 166,667500,000 *1/12 = 41,6675,650,000 WAAE 1,591,6671591667*10% = 159,167Avoidable interest = $159,167d) 5,650,000+159,167=$5,809,167Problem 3a) On December 31, 2002,Depreciation Exp $9,600A/D $9,600b) Now for the 2003 depreciationDepreciation exp $4,800A/D $4,800c) On 3/31/2004Equipment $15,000Cash $15,000New book value following the betterment (40,000 – 30,400) +15,000 = $24,600 with 5 more years to go and salvage = 900 using DDBOn 12/31/2004Depreciation Exp $9,840A/D $9,840d) Depreciation for 2005 = $5904 ((2/5)*(24,600 – 9840))Depreciation for 2006 = $1181 ((2/5)*(24,600 – 15,744))*(4/12) 4/31/2006Acc. Depr $47,325Cash 20,000Asset $55,000Gain 12,325。