公司财务原理与资本运作(公司金融) 部分课后答案(原书第10版)

- 格式:pdf

- 大小:904.44 KB

- 文档页数:20

Chapter 1Goal OF FirmN0.2, 3, 4, 5, 10.2. Not-for-Profit Firm Goals Suppose you were the financial manager of a not-for-profit business (anot-for-profit hospital, perhaps). What kinds of goals do you think would be appropriate?答:所有者权益的市场价值的最大化。

3.Goal of the Firm Evaluate the following statement: Managers should not focus on the current stock value because doing so will lead to an overemphasis on short-term profits at the expense of long-term profits.答:错误;因为现在的股票价值已经反应了短期和长期的的风险、时间以及未来现金流量。

4. Ethics and Firm Goals Can the goal of maximizing the value of the stock conflict with other goals, such as avoiding unethical or illegal behavior? In particular, do you think subjects like customer and employee safety, the environment, and the general good of society fit in this framework, or are they essentially ignored? Think of some specific scenarios to illustrate your answer.答:有两种极端。

公司理财课后习题参考答案ANSWS第1章习题答案1.在投资活动上,固定资产投资大量增加,增加金额为387270117(万元)2.在筹资活动上,非流动负债减少,流动负债大大增加,增加金额为29990109(万元)3.在营运资本表现上,2022年初的营运资本20220220(万元)2022年末的营运资本21129988(万元)营运资本不仅大大减少,而且已经转为负数。

这与流动负债大大增加,而且主要用于固定资产的形成直接相关。

第2章习题答案1.PV200(P/A,3%,10)(P/F,3%,2)1608.11(元)2.5000012500(P/A,10%,n)(P/A,10%,n)50000/125004查表,(P/A,10%,5)3.7908(P/A,10%,6)4.3553n543.7908(65)(43.7908)插值计算:n5654.35533.79084.35533.7908n5.37最后一次取款的时间为5.37年。

3.租入设备的年金现值14762(元),低于买价。

租入好。

4.乙方案的现值9.942万元,低于甲方案。

乙方案好。

5.40001000(P/F,3%,2)1750(P/F,3%,6)F(P/F,3%,10)F2140.12第五年末应还款2140.12万元。

6.(1)债券价值4(P/A,5%,6)100(P/F,5%,6)20.3074.6294.92(元)(2)2022年7月1日债券价值4(P/A,6%,4)100(P/F,6%,4)13.8679.2193.07(元)(3)4(P/F,i/2,1)104(P/F,i/2,2)97i12%时,4(P/F,6%,1)104(P/F,6%,2)3.7792.5696.33i10%时,4(P/F,5%,1)104(P/F,5%,2)3.8194.3398.14利用内插法:(i10%)/(12%10%)(98.1497)/(98.1496.33)解得i11.26%7.第三种状态估价不正确,应为12.79元。

《公司金融》课后习题参考答案各大重点财经学府专业教材期末考试考研辅导资料第一章导论第二章财务报表分析与财务计划第三章货币时间价值与净现值第四章资本预算方法第五章投资组合理论第六章资本结构第七章负债企业的估值方法第八章权益融资第九章债务融资与租赁第十章股利与股利政策第十一章期权与公司金融第十二章营运资本管理与短期融资第一章导论1.治理即公司治理(corporate governance),它解决了企业与股东、债权人等利益相关者之间及其相互之间的利益关系。

融资(financing),是公司金融学三大研究问题的核心,它解决了公司如何选择不同的融资形式并形成一定的资本结构,实现企业股东价值最大化。

估值(valuation),即企业对投资项目的评估,也包括对企业价值的评估,它解决了企业的融资如何进行分配即投资的问题。

只有公司治理规范的公司,其投资、融资决策才是基于股东价值最大化的正确决策。

这三个问题是相互联系、紧密相关的,公司金融学的其他问题都可以归纳入这三者的范畴之中。

2.对于上市公司而言,股东价值最大化观点隐含着一个前提:即股票市场充分有效,股票价格总能迅速准确地反映公司的价值。

于是,公司的经营目标就可以直接量化为使股票的市场价格最大化。

若股票价格受到企业经营状况以外的多种因素影响,那么价值确认体系就存在偏差。

因此,以股东价值最大化为目标必须克服许多公司不可控的影响股价的因素。

第二章财务报表分析与财务计划1.资产负债表;利润表;所有者权益变动表;现金流量表。

资产= 负债+ 所有者权益2.我国的利润表采用“多步式”格式,分为营业收入、营业利润、利润总额、净利润、每股收益、其他综合收益和综合收益总额等七个盈利项目。

3.直接法是按现金收入和支出的主要类别直接反映企业经营活动产生的现金流量,一般以利润表中的营业收入为起算点,调整与经营活动有关项目的增减变化,然后计算出经营活动现金流量。

间接法是以净利润为起算点,调整不涉及现金的收入、费用、营业外收支以及应收应付等项目的增减变动,据此计算并列示经营活动现金流量。

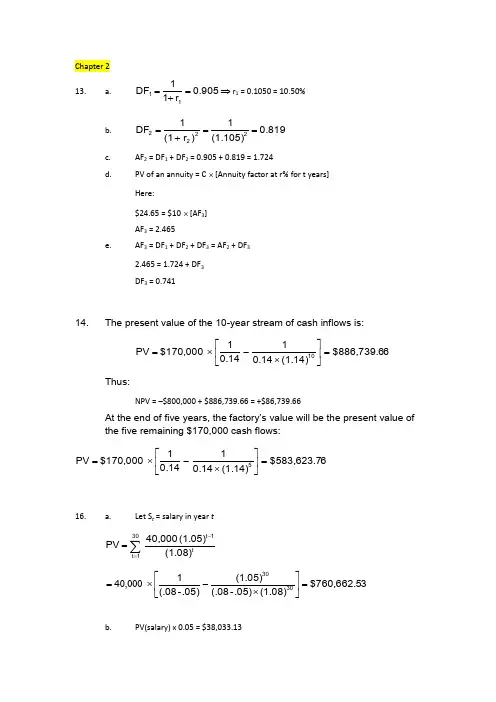

公司财务,第十版,课后答案CHAPTER 2FINANCIAL STATEMENTS AND CASH FLOWAnswers to Concepts Review and Critical Thinking Questions1.True. Every asset can be converted to cash at some price. However, when we are referring to a liquidasset, the added assumption that the asset can be quickly converted to cash at or near market value is important.2.The recognition and matching principles in financial accounting call for revenues, and the costsassociated with producing those revenues, to be “booked” when the revenue pro cess is essentially complete, not necessarily when the cash is collected or bills are paid. Note that this way is not necessarily correct; it’s the way accountants have chosen to do it.3.The bottom line number shows the change in the cash balance on the balance sheet. As such, it is nota useful number for analyzing a company.4. The major difference is the treatment of interest expense. The accounting statement of cash flowstreats interest as an operating cash flow, while the financial cash flows treat interest as a financing cash flow. The logic of the accounting statement of cash flows is that since interest appears on the income statement, which shows the operations for the period, it is an operating cash flow. In reality, interest is a financing e xpense, which results from the company’s choice of debt and equity. We will have more to say about this in a later chapter. When comparing the two cash flow statements, the financial statement of cash flows is a more appropriate measureof the company’s pe rformance because of its treatment of interest.5.Market values can never be negative. Imagine a share of stock selling for –$20. This would meanthat if you placed an order for 100 shares, you would get the stock along with a check for $2,000.How many shares do you want to buy? More generally, because of corporate and individual bankruptcy laws, net worth for a person or a corporation cannot be negative, implying that liabilities cannot exceed assets in market value.6.For a successful company that is rapidly expanding, for example, capital outlays will be large,possibly leading to negative cash flow from assets. In general, what matters is whether the money is spent wisely, not whether cash flow from assets is positive or negative.7.It’s probably not a good sign for an established company to have negative cash flow from operations,but it would be fairly ordinary for a start-up, so it depends.8.For example, if a company were to become more efficient in inventory management, the amount ofinventory needed would decline. The same might be true if the company becomes better at collecting its receivables. In general, anything that leads to a decline in ending NWC relative to beginning would have this effect. Negative net capital spending would mean more long-lived assets were liquidated than purchased.9.If a company raises more money from selling stock than it pays in dividends in a particular period,its cash flow to stockholders will be negative. If a company borrows more than it pays in interest and principal, its cash flowto creditors will be negative.10.The adjustments discussed were purely accounting changes; they had no cash flow or market valueconsequences unless the new accounting information caused stockholders to revalue the derivatives. Solutions to Questions and ProblemsNOTE: All end-of-chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability constraints, when these intermediate steps are included in this solutions manual, rounding may appear to have occurred. However, the final answer for each problem is found without rounding during any step in the problem.Basic1.To find owners’ equity, we must construct a balance sheet as follows:Balance SheetCA $ 5,700 CL $ 4,400NFA 27,000 LTD 12,900OE ??TA $32,700 TL & OE $32,700We know that total liabilities and owners’ equity (TL & OE) must equal total assets of $32,700. We also know that TL & OE is equal to current liabilities plus long-term debt plus owner’s equity, so owner’s equity is:O E = $32,700 –12,900 – 4,400 = $15,400N WC = CA – CL = $5,700 – 4,400 = $1,3002. The income statement for the company is:Income StatementSales $387,000Costs 175,000Depreciation 40,000EBIT $172,000Interest 21,000EBT $151,000Taxes 52,850Net income $ 98,150One equation for net income is:Net income = Dividends + Addition to retained earningsRearranging, we get:Addition to retained earnings = Net income – DividendsAddition to retained earnings = $98,150 – 30,000Addition to retained earnings = $68,1503.To find the book value of current assets, we use: NWC = CA – CL. Rearranging to solve for currentassets, we get:CA = NWC + CL = $800,000 + 2,400,000 = $3,200,000The market value of current assets and net fixed assets is given, so:Book value CA = $3,200,000 Market value CA = $2,600,000 Book value NFA = $5,200,000 Market value NFA = $6,500,000 Book value assets = $8,400,000 Market value assets = $9,100,0004.Taxes = 0.15($50,000) + 0.25($25,000) + 0.34($25,000) + 0.39($273,000 – 100,000)Taxes = $89,720The average tax rate is the total tax paid divided by net income, so:Average tax rate = $89,720 / $273,000Average tax rate = 32.86%The marginal tax rate is the tax rate on the next $1 ofearnings, so the marginal tax rate = 39%.5.To calculate OCF, we first need the income statement:Income StatementSales $18,700Costs 10,300Depreciation 1,900EBIT $6,500Interest 1,250Taxable income $5,250Taxes 2,100Net income $3,150OCF = EBIT + Depreciation – TaxesOCF = $6,500 + 1,900 – 2,100OCF = $6,300/doc/a95a227710a6f524cdbf8525.ht ml capital spending = NFA end– NFA beg + Depreciation Net capital spending = $1,690,000 – 1,420,000 + 145,000Net capital spending = $415,0007.The long-term debt account will increase by $35 million, the amount of the new long-term debt issue.Since the company sold 10 million new shares of stock with a $1 par value, the common stock account will increase by $10 million. The capital surplus account will increase by $48 million, the value of the new stock sold above its par value. Since the company had a net income of $9 million, and paid $2 million in dividends, the addition to retained earnings was $7 million, which will increase the accumulated retained earnings account. So, the new long-term debt and stockholders’ equity portion of the balance sheet will be:Long-term debt $ 100,000,000Total long-term debt $ 100,000,000Shareholders equityPreferred stock $ 4,000,000Common stock ($1 par value) 25,000,000Accumulated retained earnings 142,000,000Capital surplus 93,000,000Total equity $ 264,000,000Total Liabilities & Equity $ 364,000,0008.Cash flow to creditors = Interest paid – Net new borrowingCash flow to creditors = $127,000 – (LTD end– LTD beg)Cash flow to creditors = $127,000 – ($1,520,000 – 1,450,000) Cash flow to creditors = $127,000 – 70,000Cash flow to creditors = $57,0009. Cash flow to stockholders = Dividends paid –Net new equityCash flow to stockholders = $275,000 –[(Common end + APIS end) – (Common beg + APIS beg)]Cash flow to stockholders = $275,000 –[($525,000 + 3,700,000) – ($490,000 + 3,400,000)]Cash flow to stockholders = $275,000 –($4,225,000 –3,890,000)Cash flow to stockholders = –$60,000Note, APIS is the additional paid-in surplus.10. Cash flow from assets = Cash flow to creditors + Cash flow to stockholders= $57,000 – 60,000= –$3,000Cash flow from assets = OCF – Change in NWC – Net capital spending–$3,000 = OCF – (–$87,000) – 945,000OCF = $855,000Operating cash flow = –$3,000 – 87,000 + 945,000Operating cash flow = $855,000Intermediate11. a.The accounting statement of cash flows explains the change in cash during the year. Theaccounting statement of cash flows will be:Statement of cash flowsOperationsNet income $95Depreciation 90Changes in other current assets (5)Accounts payable 10Total cash flow from operations $190Investing activitiesAcquisition of fixed assets $(110)Total cash flow from investing activities $(110)Financing activitiesProceeds of long-term debt $5Dividends (75)Total cash flow from financing activities ($70)Change in cash (on balance sheet) $10b.Change in NWC = NWC end– NWC beg= (CA end– CL end) – (CA beg– CL beg)= [($65 + 170) – 125] – [($55 + 165) – 115)= $110 – 105= $5c.To find the cash flow generated by the firm’s assets, we need the operating cash flow, and thecapital spending. So, calculating each of these, we find:Operating cash flowNet income $95Depreciation 90Operating cash flow $185Note that we can calculate OCF in this manner since there are no taxes.Capital spendingEnding fixed assets $390Beginning fixed assets (370)Depreciation 90Capital spending $110Now we can calculate the cash flow generated by the firm’s assets, which is:Cash flow from assetsOperating cash flow $185Capital spending (110)Change in NWC (5)Cash flow from assets $ 7012.With the information provided, the cash flows from the firm are the capital spending and the changein net working capital, so:Cash flows from the firmCapital spending $(21,000)Additions to NWC (1,900)Cash flows from the firm $(22,900)And the cash flows to the investors of the firm are:Cash flows to investors of the firmSale of long-term debt (17,000)Sale of common stock (4,000)Dividends paid 14,500Cash flows to investors of the firm $(6,500)13. a. The interest expense for the company is the amount of debt times the interest rate on the debt.So, the income statement for the company is:Income StatementSales $1,060,000Cost of goods sold 525,000Selling costs 215,000Depreciation 130,000EBIT $190,000Interest 56,000Taxable income $134,000Taxes 46,900Net income $ 87,100b. And the operating cash flow is:OCF = EBIT + Depreciation – TaxesOCF = $190,000 + 130,000 – 46,900OCF = $273,10014.To find the OCF, we first calculate net income.Income StatementSales $185,000Costs 98,000Depreciation 16,500Other expenses 6,700EBIT $63,800Interest 9,000Taxable income $54,800Taxes 19,180Net income $35,620Dividends $9,500Additions to RE $26,120a.OCF = EBIT + Depreciation – TaxesOCF = $63,800 + 16,500 – 19,180OCF = $61,120b.CFC = Interest – Net new LTDCFC = $9,000 – (–$7,100)CFC = $16,100Note that the net new long-term debt is negative because the company repaid part of its long-term debt.c.CFS = Dividends – Net new equityCFS = $9,500 – 7,550CFS = $1,950d.We know that CFA = CFC + CFS, so:CFA = $16,100 + 1,950 = $18,050CFA is also equal to OCF – Net capital spending – Change in NWC. We already know OCF.Net capital spending is equal to:Net capital spending = Increase in NFA + DepreciationNet capital spending = $26,100 + 16,500Net capital spending = $42,600Now we can use:CFA = OCF – Net capital spending – Change in NWC$18,050 = $61,120 – 42,600 – Change in NWC.Solving for the change in NWC gives $470, meaning the company increased its NWC by $470.15.The solution to this question works the income statement backwards. Starting at the bottom:Net income = Dividends + Addition to ret. earningsNet income = $1,570 + 4,900Net income = $6,470Now, looking at the income statement:EBT –(EBT × Tax rate) = Net incomeRecognize that EBT × tax rate is simply the calculation for taxes. Solving this for EBT yields:EBT = NI / (1– Tax rate)EBT = $6,470 / (1 – .35)EBT = $9,953.85Now we can calculate:EBIT = EBT + InterestEBIT = $9,953.85 + 1,840EBIT = $11,793.85The last step is to use:EBIT = Sales – Costs – Depreciation$11,793.85 = $41,000 – 26,400 – DepreciationDepreciation = $2,806.1516.The market value of shareholders’ equity cannot be negative. A negative market value in this casewould imply that the company would pay you to own the stock. The market value of shareholders’ equity can be stated as: Shareholders’ equity = Max [(TA – TL), 0]. So, if TA is $12,400, equity is equal to $1,500, and if TA is $9,600, equity is equal to $0. We should note here that while the market value of equity cannot be negative, the book value of share holders’ equity can be negative. 17. a. Taxes Growth = 0.15($50,000) + 0.25($25,000) + 0.34($86,000 – 75,000) = $17,490Taxes Income = 0.15($50,000) + 0.25($25,000) + 0.34($25,000) + 0.39($235,000)+ 0.34($8,600,000 – 335,000)= $2,924,000b. Each firm has a marginal tax rate of 34% on the next $10,000 of taxable income, despite theirdifferent average tax rates, so both firms will pay an additional $3,400 in taxes.18.Income StatementSales $630,000COGS 470,000A&S expenses 95,000Depreciation 140,000EBIT ($75,000)Interest 70,000Taxable income ($145,000)Taxes (35%) 0/doc/a95a227710a6f524cdbf8525.ht ml income ($145,000)b.OCF = EBIT + Depreciation – TaxesOCF = ($75,000) + 140,000 – 0OCF = $65,000/doc/a95a227710a6f524cdbf8525.ht ml income was negative because of the tax deductibility of depreciation and interest expense.However, the actual cash flow from operations was positive because depreciation is a non-cash expense and interest is a financing expense, not an operating expense.19. A firm can still pay out dividends if net income is negative; it just has to be sure there is sufficientcash flow to make the dividend payments.Change in NWC = Net capital spending = Net new equity = 0. (Given)Cash flow from assets = OCF – Change in NWC – Net capitalspendingCash flow from assets = $65,000 – 0 – 0 = $65,000Cash flow to stockholders = Dividends – Net new equityCash flow to stockholders = $34,000 – 0 = $34,000Cash flow to creditors = Cash flow from assets – Cash flow to stockholdersCash flow to creditors = $65,000 – 34,000Cash flow to creditors = $31,000Cash flow to creditors is also:Cash flow to creditors = Interest – Net new LTDSo:Net new LTD = Interest – Cash flow to creditorsNet new LTD = $70,000 – 31,000Net new LTD = $39,00020. a.The income statement is:Income StatementSales $19,900Cost of good sold 14,200Depreciation 2,700EBIT $ 3,000Interest 670Taxable income $ 2,330Taxes 932Net income $1,398b.OCF = EBIT + Depreciation – TaxesOCF = $3,000 + 2,700 – 932OCF = $4,768c.Change in NWC = NWC end– NWC beg= (CA end– CL end) – (CA beg– CL beg)= ($5,135 – 2,535) – ($4,420 – 2,470)= $2,600 – 1,950 = $650Net capital spending = NFA end– NFA beg + Depreciation = $16,770 – 15,340 + 2,700= $4,130CFA = OCF – Change in NWC – Net capital spending= $4,768 – 650 – 4,130= –$12The cash flow from assets can be positive or negative, since it represents whether the firm raised funds or distributed funds on a net basis. In this problem, even though net income and OCF are positive, the firm invested heavily in both fixed assets and net working capital; it had to raise a net $12 in funds from its stockholders and creditors to make these investments.d.Cash flow to creditors = Interest – Net new LTD= $670 – 0= $670Cash flow to stockholders = Cash flow from assets – Cash flow to creditors= –$12 – 670= –$682We can also calculate the cash flow to stockholders as:Cash flow to stockholders = Dividends – Net new equitySolving for net new equity, we get:Net new equity = $650 – (–682)= $1,332The firm had positive earnings in an accounting sense (NI > 0) and had positive cash flow from operations. The firm invested $650 in new net working capital and $4,130 in new fixed assets.The firm had to raise $12 from its stakeholders to support this new investment. It accomplished this by raising $1,332 in theform of new equity. After paying out $650 of this in the form of dividends to shareholders and $670 in the form of interest to creditors, $12 was left to meet the firm’s cash flow needs for investment.21. a.Total assets 2011 = $936 + 4,176 = $5,112Total liabilities 2011 = $382 + 2,160 = $2,542Owners’ equity 2011 = $5,112 – 2,542 = $2,570Total assets 2012 = $1,015 + 4,896 = $5,911Total liabilities 2012 = $416 + 2,477 = $2,893Owners’ equity 2012 = $5,911 – 2,893 = $3,018b.NWC 2011 = CA11 – CL11 = $936 – 382 = $554NWC 2012 = CA12 – CL12 = $1,015 – 416 = $599Change in NWC = NWC12 – NWC11 = $599 – 554 = $45c.We can calculate net capital spending as:Net capital spending = Net fixed assets 2012 –Net fixed assets 2011 + DepreciationNet capital spending = $4,896 – 4,176 + 1,150Net capital spending = $1,870So, the company had a net capital spending cash flow of $1,870. We also know that net capital spending is:Net capital spending = Fixed assets bought –Fixed assets sold$1,870 = $2,160 – Fixed assets soldFixed assets sold = $2,160 – 1,870 = $290To calculate the cash flow from assets, we must first calculate the operating cash flow. The operating cash flow is calculated as follows (you can also prepare a traditional income statement): EBIT = Sales – Costs – DepreciationEBIT = $12,380 – 5,776 – 1,150EBIT = $5,454EBT = EBIT – InterestEBT = $5,454 – 314EBT = $5,140Taxes = EBT ? .40Taxes = $5,140 ? .40Taxes = $2,056OCF = EBIT + Depreciation – TaxesOCF = $5,454 + 1,150 – 2,056OCF = $4,548Cash flow from assets = OCF – Change in NWC – Net capital spending.Cash flow from assets = $4,548 – 45 – 1,870Cash flow from assets = $2,633/doc/a95a227710a6f524cdbf8525.ht ml new borrowing = LTD12 – LTD11Net new borrowing = $2,477 – 2,160Net new borrowing = $317Cash flow to creditors = Interest – Net new LTDCash flow to creditors = $314 – 317Cash flow to creditors = –$3Net new borrowing = $317 = Debt issued – Debt retiredDebt retired = $432 – 317 = $11522.Balance sheet as of Dec. 31, 2011Cash $4,109 Accounts payable $4,316 Accounts receivable 5,439 Notes payable 794 Inventory 9,670 Current liabilities $5,110 Current assets $19,218Long-term debt $13,460 Net fixed assets $34,455 Owners' equity 35,103 Total assets $53,673 Total liab. & equity $53,673 Balance sheet as of Dec. 31, 2012Cash $5,203 Accounts payable $4,185Accounts receivable 6,127 Notes payable 746Inventory 9,938 Current liabilities $4,931Current assets $21,268Long-term debt $16,050 Net fixed assets $35,277 Owners' equity 35,564Total assets Total liab. & equity2011 Income Statement 2012 Income Statement Sales $7,835.00Sales $8,409.00 COGS 2,696.00COGS 3,060.00 Other expenses 639.00Other expenses 534.00 Depreciation 1,125.00Depreciation 1,126.00 EBIT $3,375.00EBIT $3,689.00 Interest 525.00Interest 603.00 EBT $2,850.00EBT $3,086.00 Taxes 969.00Taxes 1,049.24 Net income $1,881.00Net income $2,036.76 Dividends $956.00Dividends $1,051.00 Additions to RE 925.00Additions to RE 985.76 23.OCF = EBIT + Depreciation –TaxesOCF = $3,689 + 1,126 – 1,049.24OCF = $3,765.76Change in NWC = NWC end– NWC beg = (CA – CL) end– (CA – CL) begChange in NWC = ($21,268 – 4,931) – ($19,218 – 5,110)Change in NWC = $2,229Net capital spending = NFA end– NFA beg+ DepreciationNet capital spending = $35,277 – 34,455 + 1,126Net capital spending = $1,948Cash flow from assets = OCF – Change in NWC – Net capital spendingCash flow from assets = $3,765.76 – 2,229 – 1,948Cash flow from assets = –$411.24Cash flow to creditors = Interest – Net new LTDNet new LTD = LTD end– LTD begCash flow to creditors = $603 – ($16,050 – 13,460)Cash flow to creditors = –$1,987Net new equity = Common stock end– Common stock beg Common stock + Retained earnings = Total owners’ equity Net new equity = (OE – RE) end– (OE – RE) begNet new equity = OE end– OE beg + RE beg– RE endRE end= RE beg+ Additions to RENet new equity = OE end–OE beg+ RE beg–(RE beg + Additions to RE)= OE end– OE beg– Additions to RENet new equity = $35,564 – 35,103 – 985.76 = –$524.76Cash flow to stockholders = Dividends – Net new equityCash flow to stockholders = $1,051– (–$524.76)Cash flow to stockholders = $1,575.76As a check, cash flow from assets is –$411.24Cash flow from assets = Cash flow from creditors + Cash flow to stockholdersCash flow from assets = –$1,987 + 1,575.76Cash flow from assets = –$411.24Challenge24.We will begin by calculating the operating cash flow. First, we need the EBIT, which can becalculated as:EBIT = Net income + Current taxes + Deferred taxes + InterestEBIT = $173 + 98 + 19 + 48EBIT = $338Now we can calculate the operating cash flow as:Operating cash flowEarnings before interest and taxes $338Depreciation 94Current taxes (98)Operating cash flow $334The cash flow from assets is found in the investing activities portion of the accounting statement of cash flows, so: Cash flow from assetsAcquisition of fixed assets $215Sale of fixed assets (23)Capital spending $192The net working capital cash flows are all found in the operations cash flow section of the accounting statement of cash flows. However, instead of calculating the net working capital cash flows as the change in net working capital, we must calculate each item individually. Doing so, we find:Net working capital cash flowCash $14Accounts receivable 18Inventories (22)Accounts payable (17)Accrued expenses 9Notes payable (6)Other (3)NWC cash flow ($7)Except for the interest expense and notes payable, the cash flow to creditors is found in the financing activities of the accounting statement of cash flows. The interest expense from the income statement is given, so:Cash flow to creditorsInterest $48Retirement of debt 162Debt service $210Proceeds from sale of long-term debt (116)Total $94And we can find the cash flow to stockholders in the financing section of the accounting statement of cash flows. The cash flow to stockholders was:Cash flow to stockholdersDividends $ 86Repurchase of stock 13Cash to stockholders $ 99Proceeds from new stock issue (44)Total $ 55/doc/a95a227710a6f524cdbf8525.ht ml capital spending = NFA end– NFA beg + Depreciation = (NFA end– NFA beg) + (Depreciation + AD beg) – AD beg = (NFA end– NFA beg)+ AD end– AD beg= (NFA end + AD end) – (NFA beg + AD beg) = FA end– FA beg26. a.The tax bubble causes average tax rates to catch up to marginal tax rates, thus eliminating thetax advantage of low marginal rates for high income corporations.b.Assuming a taxable income of $335,000, the taxes will be:Taxes = 0.15($50K) + 0.25($25K) + 0.34($25K) + 0.39($235K) = $113.9KAverage tax rate = $113.9K / $335K = 34%The marginal tax rate on the next dollar of income is 34 percent.For corporate taxable income levels of $335K to $10M,average tax rates are equal to marginal tax rates.Taxes = 0.34($10M) + 0.35($5M) + 0.38($3.333M) = $6,416,667Average tax rate = $6,416,667 / $18,333,334 = 35%The marginal tax rate on the next dollar of income is 35 percent. For corporate taxable income levels over $18,333,334, average tax rates are again equal to marginal tax rates.c.Taxes = 0.34($200K) = $68K = 0.15($50K) + 0.25($25K) +0.34($25K) + X($100K);X($100K) = $68K – 22.25K = $45.75KX = $45.75K / $100KX = 45.75%。

《公司金融》课后习题参考答案各大重点财经学府专业教材期末考试考研辅导资料第一章导论第二章财务报表分析与财务计划第三章货币时间价值与净现值第四章资本预算方法第五章投资组合理论第六章资本结构第七章负债企业的估值方法第八章权益融资第九章债务融资与租赁第十章股利与股利政策第十一章期权与公司金融第十二章营运资本管理与短期融资第一章导论1.治理即公司治理(corporate governance),它解决了企业与股东、债权人等利益相关者之间及其相互之间的利益关系。

融资(financing),是公司金融学三大研究问题的核心,它解决了公司如何选择不同的融资形式并形成一定的资本结构,实现企业股东价值最大化。

估值(valuation),即企业对投资项目的评估,也包括对企业价值的评估,它解决了企业的融资如何进行分配即投资的问题。

只有公司治理规范的公司,其投资、融资决策才是基于股东价值最大化的正确决策。

这三个问题是相互联系、紧密相关的,公司金融学的其他问题都可以归纳入这三者的范畴之中。

2.对于上市公司而言,股东价值最大化观点隐含着一个前提:即股票市场充分有效,股票价格总能迅速准确地反映公司的价值。

于是,公司的经营目标就可以直接量化为使股票的市场价格最大化。

若股票价格受到企业经营状况以外的多种因素影响,那么价值确认体系就存在偏差。

因此,以股东价值最大化为目标必须克服许多公司不可控的影响股价的因素。

第二章财务报表分析与财务计划1.资产负债表;利润表;所有者权益变动表;现金流量表。

资产= 负债+ 所有者权益2.我国的利润表采用“多步式”格式,分为营业收入、营业利润、利润总额、净利润、每股收益、其他综合收益和综合收益总额等七个盈利项目。

3.直接法是按现金收入和支出的主要类别直接反映企业经营活动产生的现金流量,一般以利润表中的营业收入为起算点,调整与经营活动有关项目的增减变化,然后计算出经营活动现金流量。

间接法是以净利润为起算点,调整不涉及现金的收入、费用、营业外收支以及应收应付等项目的增减变动,据此计算并列示经营活动现金流量。

财务会计第十版答案财务会计第十版答案【篇一:财务会计学第10、11、12章课后习题参考答案】>教材练习题解析1.20x?年。

提取的盈余公积金;200x10%=20(万元)可供分配利润=200—20=180(万元)应支付优先股股利=5 000x6%=300(万元)则实际支付优先股股利=180(万元) .未分派的优先股股利=300—180=120(万元)20x8年。

提取的盈余公积金=2 875x10%=287.5(万元)可供分配利润=2 875—287.5=2 587.5(万元)补付20x7年优先股股利=120(万元)20x8年优先股股利=5 000x6%=300(万元)剩余可供分配利润=2 587.5—120—300=2167.5(万元)优先股剩余股利=0.070 5x5 000—300=52.5(万元)优先股股利总额=120+300+52.5=472.5(万元)2.20x6年1月1日。

公司预计支付股份应负担的费用=loxl000x200=2 000000(元) 不作会计处理。

20x6年12月31 h。

公司预计:支付股份:应负担的费用=2 000 000x(1—10%) =1 800 000(元)借:管理费用 600 000贷:资本公积——其他资本公积 600 00020x7年工2月31日。

公司预计支付股份应负担的费用=2 000 000x(1—8%)=1 840000(元) 20x7年累计应负担妁费用=1 840000x2/3x1 226 667(元) 20x7年应负担的费用=1 226 667—600 000=626 667(元) 借:管理费用 626 667贷:资本公积——其他资本公积 626 66720x8年12月31日。

公司实际支付股份应负担的费用昌loxl000x(200—3—3—1)=1 930 000(元)20x8年应负担的费用=1 930000-226 667=703 333(元)借:管理费用 703 333贷:资本公积——其他资本公积 703 33320x9年1月1日。

第十章财务控制与评价思考练习一、单项选择题1.A 2.D 3.D 4.B 5.A 6.A7.B 8.C 9.C 10.D 11.D 12.B二、多项选择题1.AC2.ACD 3.ABD 4.BCD 5.BCD 6.ACD7.ABC 8.AD 9.BD 10.CD 11.AC 12.ABC三、判断题1-5.√×√√√ 6-10.×××√× 11-15 ××√××四、计算题1.(1)填列表格如下:单位:万元项目总资产息税前利润息税前利润率剩余收益甲投资中心500 40乙投资中心 1000 86追加投资前 1000 150 8% -10追加投资后86/1000×100%=8.6%86-1000×10%=-14追加投资前 1500 205 15% +50追加投资后205/1500×100%=13.67% 205-1500×10%=55(2)决策如下:由于甲投资中心追加投资后将降低剩余收益,故不应追加投资;乙投资中心追加投资后可提高剩余收益,故可追加投资。

2.(1)①该投资中心的投资报酬率=(150000-100000-8000-25000)/100000=17%②公司规定该中心的最低报酬率=8%+1.5×(10%-8%)=11%③剩余收益=17000-100000×11%=6000(元)(2)追加投资后的指标计算如下:①投资报酬率=[150000-100000-8000-25000]+9000]/(100000+60000)=26000/160000=16.25%②剩余收益=26000-160000×11%=8400(元)由于追加投资后的投资报酬率低于变动前的,故根据投资报酬率决策,该项目不可行;追加投资后的剩余收益高于变动前的,故根据剩余收益决策,该项目是可行的。

第一章Corporate finance(公司财务)是金融学的分支学科,用于考察公司如何有效地利用各种融资渠道,获得最低成本的资金来源,并形成合适的资本结构(capital structure);还包括企业投资、利润分配、运营资金管理及财务分析等方面。

它会涉及到现代公司制度中的一些诸如委托-代理结构的金融安排等深层次的问题。

为什么说公司理财研究的就是如下三个问题:(1) 公司应该投资于什么样的长期资产?涉及资产负债表的左边。

我们使用“资本预算(capital budgeting)”和“资本性支出”这些专业术语描述这些长期固定资产的投资和管理过程。

(2) 公司如何筹集资本性支出所需的资金呢?涉及资产负债表的右边。

回答这一问题又涉及到资本结构(Capital structure),它表示公司短期及长期负债与股东权益的比例。

(3) 公司应该如何管理它在经营中的现金流量?涉及资产负债表的上方。

首先,经营中的现金流入量和现金流出量在时间上不对等。

此外,经营中现金流量的数额和时间都具有不确定性,难于确切掌握。

财务经理必须致力于管理现金流量的缺口。

从资产负债表的角度看,现金流量的短期管理与净营运资本(net working capital)有关。

净营运资本定义为短期资本与短期负债之差。

从财务管理的角度看,短期现金流量问题是由于现金流量和现金流量之间不对等所引起的,属于短期理财问题。

资本结构公司可以事先发行比股权多的债权,筹集所需的资金;可以考虑改变二者的比例,买回它的一些债权。

融资决策在原先投资决策前就可以独立设定。

这些发行债权和股权的决策影响到公司的资本结构。

资金主管负责处理现金流量、投资预算和制定财务计划。

财务主管负责会计工作职能,包括税收、成本核算、财务会计和信息系统。

现金流量的时点公司投资的价值取决于现金流量的时点。

一个最重要的假设是任何人都偏好早一点收到现金流量。

今天收到的一美元比明天收到的一美元更有价值。

CHAPTER 18VALUATION AND CAPITAL BUDGETING FOR THE LEVERED FIRM Answers to Concepts Review and Critical Thinking Questions1.APV is equal to the NPV of the project (i.e. the value of the project for an unlevered firm) plus theNPV of financing side effects.2. The WACC is based on a target debt level while the APV is based on the amount of debt.3.FTE uses levered cash flow and other methods use unlevered cash flow.4.The WACC method does not explicitly include the interest cash flows, but it does implicitly includethe interest cost in the WACC. If he insists that the interest payments are explicitly shown, you should use the FTE method.5. You can estimate the unlevered beta from a levered beta. The unlevered beta is the beta of the assetsof the firm; as such, it is a measure of the business risk. Note that the unlevered beta will always be lower than the levered beta (assuming the betas are positive). The difference is due to the leverage of the company. Thus, the second risk factor measured by a levered beta is the financial risk of the company.Solutions to Questions and ProblemsNOTE: All end-of-chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability constraints, when these intermediate steps are included in this solutions manual, rounding may appear to have occurred. However, the final answer for each problem is found without rounding during any step in the problem.Basic1. a.The maximum price that the company should be willing to pay for the fleet of cars with all-equity funding is the price that makes the NPV of the transaction equal to zero. The NPV equation for the project is:NPV = –Purchase Price + PV[(1 –t C )(EBTD)] + PV(Depreciation Tax Shield)If we let P equal the purchase price of the fleet, then the NPV is:NPV = –P + (1 – .35)($175,000)PVIFA13%,5 + (.35)(P/5)PVIFA13%,5Setting the NPV equal to zero and solving for the purchase price, we find:0 = –P + (1 – .35)($175,000)PVIFA13%,5 + (.35)(P/5)PVIFA13%,5P = $400,085.06 + (P)(.35/5)PVIFA13%,5P = $400,085.06 + .2462P.7538P = $400,085.06P = $530,761.93b.The adjusted present value (APV) of a project equals the net present value of the project if itwere funded completely by equity plus the net present value of any financing side effects. In this case, the NPV of financing side effects equals the after-tax present value of the cash flows resulting from the firm’s debt, so:APV = NPV(All-Equity) + NPV(Financing Side Effects)So, the NPV of each part of the APV equation is:NPV(All-Equity)NPV = –Purchase Price + PV[(1 – t C )(EBTD)] + PV(Depreciation Tax Shield)The company paid $480,000 for the fleet of cars. Because this fleet will be fully depreciated over five years using the straight-line method, annual depreciation expense equals:Depreciation = $480,000/5Depreciation = $96,000So, the NPV of an all-equity project is:NPV = –$480,000 + (1 – .35)($175,000)PVIFA13%,5 + (.35)($96,000)PVIFA13%,5NPV = $38,264.03NPV(Financing Side Effects)The net present value of financing side effects equals the after-tax present value of cash flows resulting from the firm’s debt, so:NPV = Proceeds – Aftertax PV(Interest Payments) – PV(Principal Payments)Given a known level of debt, debt cash flows should be discounted at the pre-tax cost of debt R B. So, the NPV of the financing side effects are:NPV = $390,000 – (1 – .35)(.08)($390,000)PVIFA8%,5– $390,000/1.085NPV = $43,600.39So, the APV of the project is:APV = NPV(All-Equity) + NPV(Financing Side Effects)APV = $38,264.03 + 43,600.39APV = $81,864.422.The adjusted present value (APV) of a project equals the net present value of the project if it werefunded completely by equity plus the net present value of any financing side effects. In this case, the NPV of financing side effects equals the after-tax present value of the cash flows resulting from the firm’s debt, so:APV = NPV(All-Equity) + NPV(Financing Side Effects)So, the NPV of each part of the APV equation is:NPV(All-Equity)NPV = –Purchase Price + PV[(1 –t C)(EBTD)] + PV(Depreciation Tax Shield)Since the initial investment of $1.7 million will be fully depreciated over four years using thestraight-line method, annual depreciation expense is:Depreciation = $1,700,000/4Depreciation = $425,000NPV = –$1,700,000 + (1 – .30)($595,000)PVIFA13%,4 + (.30)($425,000)PVIFA9.5%,4NPV (All-equity) = –$52,561.35NPV(Financing Side Effects)The net present value of financing side effects equals the aftertax present value of cash flowsresulting from the firm’s debt. So, the NPV of the financing side effects are:NPV = Proceeds(Net of flotation) – Aftertax PV(Interest Payments) – PV(Principal Payments) + PV(Flotation Cost Tax Shield)Given a known level of debt, debt cash flows should be discounted at the pre-tax cost of debt, R B.Since the flotation costs will be amortized over the life of the loan, the annual flotation costs that will be expensed each year are:Annual flotation expense = $45,000/4Annual flotation expense = $11,250NPV = ($1,700,000 – 45,000) – (1 – .30)(.095)($1,700,000)PVIFA9.5%,4– $1,700,000/1.0954 + .30($11,250) PVIFA9.5%,4NPV = $121,072.23So, the APV of the project is:APV = NPV(All-Equity) + NPV(Financing Side Effects)APV = –$52,561.35 + 121,072.23APV = $68,510.883. a.In order to value a firm’s equity using the flow-to-equity approach, discount the cash flowsavailable to equity holders at the cost of the firm’s levered equity. The cash flows to equity holders will be the firm’s net income. Remembering that the company has three stores, we find:Sales $3,900,000COGS 2,010,000G & A costs 1,215,000Interest 123,000EBT $ 552,000Taxes 220,800NI $ 331,200Since this cash flow will remain the same forever, the present value of cash flows available tothe firm’s equity holders is a perpetuity. We can discount at the levered cost of equity, so, thevalue of the company’s equity is:PV(Flow-to-equity) = $331,200 / .19PV(Flow-to-equity) = $1,743,157.89b.The value of a firm is equal to the sum of the market values of its debt and equity, or:V L = B + SWe calculated the value of the company’s equity in part a, so now we need to calculate the value of debt. The company has a debt-to-equity ratio of .40, which can be written algebraically as:B / S = .40We can substitute the value of equity and solve for the value of debt, doing so, we find:B / $1,743,157.89 = .40B = $697,263.16So, the value of the company is:V = $1,743,157.89 + 697,263.16V = $2,440,421.054. a.In order to determine the cost of the firm’s debt, we need to find the yield to maturity on itscurrent bonds. With semiannual coupon payments, the yield to maturity of the company’s bonds is:$1,080 = $35 (PVIFA R%,40) + $1,000(PVIF R%,40)R = .03145, or 3.145%Since the coupon payments are semiannual, the YTM on the bonds is:YTM = 3.145%× 2YTM = 6.29%b.We can use the Capital Asset Pricing Model to find the return on unlevered equity. Accordingto the Capital Asset Pricing Model:R0 = R F+ βUnlevered(R M–R F)R0 = 4% + .85(11% – 4%)R0 = 9.95%Now we can find the cost of levered equity. According to Modigliani-Miller Proposition II with corporate taxesR S = R0 + (B/S)(R0–R B)(1 –t C)R S = .0995 + (.40)(.0995 – .0629)(1 – .34)R S = .1092, or 10.92%c.In a world with corporate taxes, a firm’s weighted average cost of capital is equal to:R WACC = [B / (B + S)](1 –t C)R B + [S / (B + S)]R SThe problem does not provide either the debt-value ratio or equity-value ratio. However, the firm’s debt-equity ratio is:B/S = .40Solving for B:B = .4SSubstituting this in the debt-value ratio, we get:B/V = .4S / (.4S + S)B/V = .4 / 1.4B/V = .29And the equity-value ratio is one minus the debt-value ratio, or:S/V = 1 – .29S/V = .71So, the WACC for the company is:R WACC = .29(1 – .34)(.0629) + .71(.1092)R WACC = .0898, or 8.98%5. a.The equity beta of a firm financed entirely by equity is equal to its unlevered beta. Since eachfirm has an unlevered beta of 1.10, we can find the equity beta for each. Doing so, we find:North PoleβEquity = [1 + (1 –t C)(B/S)]βUnleveredβEquity = [1 + (1 – .35)($2,900,000/$3,800,000](1.10)βEquity = 1.65South PoleβEquity = [1 + (1 –t C)(B/S)]βUnleveredβEquity = [1 + (1 – .35)($3,800,000/$2,900,000](1.10)βEquity = 2.04b.We can use the Capital Asset Pricing Model to find the required return on each firm’s equity.Doing so, we find:North Pole:R S = R F+ βEquity(R M–R F)R S = 3.20% + 1.65(10.90% – 3.20%)R S = 15.87%South Pole:R S = R F+ βEquity(R M–R F)R S = 3.20% + 2.04(10.90% – 3.20%)R S = 18.88%6. a.If flotation costs are not taken into account, the net present value of a loan equals:NPV Loan = Gross Proceeds – Aftertax present value of interest and principal paymentsNPV Loan = $5,850,000 – .08($5,850,000)(1 – .40)PVIFA8%,10– $5,850,000/1.0810NPV Loan = $1,256,127.24b.The flotation costs of the loan will be:Flotation costs = $5,850,000(.025)Flotation costs = $146,250So, the annual flotation expense will be:Annual flotation expense = $146,250 / 10Annual flotation expense = $14,625If flotation costs are taken into account, the net present value of a loan equals:NPV Loan = Proceeds net of flotation costs – Aftertax present value of interest and principalpayments + Present value of the flotation cost tax shieldNPV Loan = ($5,850,000 – 146,250) – .08($5,850,000)(1 – .40)(PVIFA8%,10)– $5,850,000/1.0810 + $14,625(.40)(PVIFA8%,10)NPV Loan = $1,149,131.217.First we need to find the aftertax value of the revenues minus expenses. The aftertax value is:Aftertax revenue = $3,200,000(1 – .40)Aftertax revenue = $1,920,000Next, we need to find the depreciation tax shield. The depreciation tax shield each year is:Depreciation tax shield = Depreciation(t C)Depreciation tax shield = ($11,400,000 / 6)(.40)Depreciation tax shield = $760,000Now we can find the NPV of the project, which is:NPV = Initial cost + PV of depreciation tax shield + PV of aftertax revenueTo find the present value of the depreciation tax shield, we should discount at the risk-free rate, and we need to discount the aftertax revenues at the cost of equity, so:NPV = –$11,400,000 + $760,000(PVIFA3.5%,6) + $1,920,000(PVIFA11%,6)NPV = $772,332.978.Whether the company issues stock or issues equity to finance the project is irrelevant. Thecompany’s optimal capital structure determines the WACC. In a world with corporate taxes, a firm’s weighted average cost of capital equals:R WACC = [B / (B + S)](1 –t C)R B + [S / (B + S)]R SR WACC = .80(1 – .34)(.069) + .20(.1080)R WACC = .0580, or 5.80%Now we can use the weighted average cost of capital to discount NEC’s unlevered cash flows. Doing so, we find the NPV of the project is:NPV = –$45,000,000 + $3,100,000 / .0580NPV = $8,418,803.429. a.The company has a capital structure with three parts: long-term debt, short-term debt, andequity. Since interest payments on both long-term and short-term debt are tax-deductible, multiply the pretax costs by (1 –t C) to determine the aftertax costs to be used in the weighted average cost of capital calculation. The WACC using the book value weights is:R WACC = (X STD)(R STD)(1 –t C) + (X LTD)(R LTD)(1 –t C) + (X Equity)(R Equity)R WACC = ($10 / $19)(.041)(1 – .35) + ($3 / $19)(.072)(1 – .35) + ($6 / $19)(.138)R WACC = .0650, or 6.50%ing the market value weights, the company’s WACC is:R WACC = (X STD)(R STD)(1 –t C) + (X LTD)(R LTD)(1 –t C) + (X Equity)(R Equity)R WACC = ($11 / $40)(.041)(1 – .35) + ($10 / $40)(.072)(1 – .35) + ($26 / $40)(.138)R WACC = .1005, or 10.05%ing the target debt-equity ratio, the target debt-value ratio for the company is:B/S = .60B = .6SSubstituting this in the debt-value ratio, we get:B/V = .6S / (.6S + S)B/V = .6 / 1.6B/V = .375And the equity-value ratio is one minus the debt-value ratio, or:S/V = 1 – .375S/V = .625We can use the ratio of short-term debt to long-term debt in a similar manner to find the short-term debt to total debt and long-term debt to total debt. Using the short-term debt to long-term debt ratio, we get:STD/LTD = .20STD = .2LTDSubstituting this in the short-term debt to total debt ratio, we get:STD/B = .2LTD / (.2LTD + LTD)STD/B = .2 / 1.2STD/B = .167And the long-term debt to total debt ratio is one minus the short-term debt to total debt ratio, or: LTD/B = 1 – .167LTD/B = .833Now we can find the short-term debt to value ratio and long-term debt to value ratio bymultiplying the respective ratio by the debt-value ratio. So:STD/V = (STD/B)(B/V)STD/V = .167(.375)STD/V = .063And the long-term debt to value ratio is:LTD/V = (LTD/B)(B/V)LTD/V = .833(.375)LTD/V = .313So, using the target capital structure weights, the company’s WACC is:R WACC = (X STD)(R STD)(1 –t C) + (X LTD)(R LTD)(1 – t C) + (X Equity)(R Equity)R WACC = (.063)(.041)(1 – .35) + (.313)(.072)(1 – .35) + (.625)(.138)R WACC = .1025, or 10.25%d.The differences in the WACCs are due to the different weighting schemes. The company’sWACC will most closely resemble the WACC calculated using target weights since futureprojects will be financed at the target ratio. Therefore, the WACC computed with targetweights should be used for project evaluation.Intermediate10.The adjusted present value of a project equals the net present value of the project under all-equityfinancing plus the net present value of any financing side effects. In the joint venture’s case, the NPV of financing side effects equals the aftertax present value of cash flows resulting from the firms’ debt. So, the APV is:APV = NPV(All-Equity) + NPV(Financing Side Effects)The NPV for an all-equity firm is:NPV(All-Equity)NPV = –Initial Investment + PV[(1 –t C)(EBITD)] + PV(Depreciation Tax Shield)Since the initial investment will be fully depreciated over five years using the straight-line method, annual depreciation expense is:Annual depreciation = $80,000,000/5Annual depreciation = $16,000,000NPV = –$80,000,000 + (1 – .35)($12,100,000)PVIFA13%,20 + (.35)($16,000,000)PVIFA13%,5NPV = –$5,053,833.77NPV(Financing Side Effects)The NPV of financing side effects equals the after-tax present value of cash flows resulting from the firm’s debt. The coupon rate on the debt is relevant to determine the interest payments, but the resulting cash flows should still be discounted at the pretax cost of debt. So, the NPV of the financing effects is:NPV = Proceeds – Aftertax PV(Interest Payments) – PV(Principal Repayments)NPV = $25,000,000 – (1 – .35)(.05)($25,000,000)PVIFA8.5%,15– $25,000,000/1.08515NPV = $10,899,310.51So, the APV of the project is:APV = NPV(All-Equity) + NPV(Financing Side Effects)APV = –$5,053,833.77 + $10,899,310.51APV = $5,845,476.7311.If the company had to issue debt under the terms it would normally receive, the interest rate on thedebt would increase to the company’s normal cost of debt. The NPV of an all-equity project would remain unchanged, but the NPV of the financing side effects would change. The NPV of the financing side effects would be:NPV = Proceeds – Aftertax PV(Interest Payments) – PV(Principal Repayments)NPV = $25,000,000 – (1 – .35)(.085)($25,000,000)PVIFA8.5%,15– $25,000,000/1.08515NPV = $6,176,275.95Using the NPV of an all-equity project from the previous problem, the new APV of the project would be:APV = NPV(All-Equity) + NPV(Financing Side Effects)APV = –$5,053,833.77 + $6,176,275.95APV = $1,122,442.18The gain to the company from issuing subsidized debt is the difference between the two APVs, so: Gain from subsidized debt = $5,845,476.73 – 1,122,442.18Gain from subsidized debt = $4,723,034.55Most of the value of the project is in the form of the subsidized interest rate on the debt issue.12.The adjusted present value of a project equals the net present value of the project under all-equityfinancing plus the net present value of any financing side effects. First, we need to calculate the unlevered cost of equity. According to Modigliani-Miller Proposition II with corporate taxes:R S = R0 + (B/S)(R0–R B)(1 –t C).16 = R0 + (.50)(R0– .09)(1 – .40)R0 = .1438 or 14.38%Now we can find the NPV of an all-equity project, which is:NPV = PV(Unlevered Cash Flows)NPV = –$18,000,000 + $5,700,000/1.1438 + $9,500,000/(1.1438)2 + $8,800,000/1.14383NPV = $124,086.62Next, we need to find the net present value of financing side effects. This is equal the aftertax present value of cash flows resulting from the firm’s debt. So:NPV = Proceeds – Aftertax PV(Interest Payments) – PV(Principal Payments)Each year, an equal principal payment will be made, which will reduce the interest accrued during the year. Given a known level of debt, debt cash flows should be discounted at the pre-tax cost of debt, so the NPV of the financing effects is:NPV = $9,300,000 – (1 – .40)(.09)($9,300,000) / 1.09 – $3,100,000/1.09– (1 – .40)(.09)($6,200,000)/1.092– $3,100,000/1.092– (1 – .40)(.09)($3,100,000)/1.093– $3,100,000/1.093NPV = $581,194.61So, the APV of project is:APV = NPV(All-equity) + NPV(Financing side effects)APV = $124,086.62 + 581,194.61APV = $705,281.2313. a.To calculate the NPV of the project, we first need to find the company’s WACC. In a worldwith corporate taxes, a firm’s weighted average cost of capital equals:R WACC = [B / (B + S)](1 –t C)R B + [S / (B + S)]R SThe market value of the company’s equity is:Market value of equity = 4,500,000($25)Market value of equity = $112,500,000So, the debt-value ratio and equity-value ratio are:Debt-value = $55,000,000 / ($55,000,000 + 112,500,000)Debt-value = .3284Equity-value = $112,500,000 / ($55,000,000 + 112,500,000)Equity-value = .6716Since the CEO believes its current capital structure is optimal, these values can be used as the target w eights in the firm’s weighted average cost of capital calculation. The yield to maturity of the company’s debt is its pretax cost of debt. To find the company’s cost of equity, we need to calculate the stock beta. The stock beta can be calculated as:β = σS,M / σ2Mβ = .0415 / .202β = 1.04Now we can use the Capital Asset Pricing Model to determine the cost of equity. The Capital Asset Pricing Model is:R S = R F+ β(R M–R F)R S = 3.4% + 1.04(7.50%)R S = 11.18%Now, we can calculate the company’s WACC, which is:R WACC = [B / (B + S)](1 –t C)R B + [S / (B + S)]R SR WACC = .3284(1 – .35)(.065) + .6716(.1118)R WACC = .0890, or 8.90%Finally, we can use the WACC to discount the unlevered cash flows, which gives us an NPV of: NPV = –$42,000,000 + $11,800,000(PVIFA8.90%,5)NPV = $4,020,681.28b.The weighted average cost of capital used in part a will not change if the firm chooses to fundthe project entirely with debt. The weighted average cost of capital is based on optimal capital structure weights. Since the current capital structure is optimal, all-debt funding for the project simply implies that the firm will have to use more equity in the future to bring the capital structure back towards the target.14.We have four companies with comparable operations, so the industry average beta can be used as thebeta for this project. So, the average unlevered beta is:βUnlevered = (1.15 + 1.08 + 1.30 + 1.25) / 4βUnlevered = 1.20A debt-to-value ratio of .40 means that the equity-to-value ratio is .60. This implies a debt-equityratio of .67{=.40/.60}. Since the project will be levered, we need to calculate the levered beta, which is:βLevered = [1 + (1 –t C)(Debt/Equity)]βUnleveredβLevered = [1 + (1 – .34)(.67)]1.20βLevered = 1.72Now we can use the Capital Asset Pricing Model to determine the cost of equity. The Capital Asset Pricing Model is:R S = R F+ β(R M–R F)R S = 3.8% + 1.72(7.00%)R S = 15.85%Now, we can calculate the company’s WACC, which is:R WACC = [B / (B + S)](1 –t C)R B + [S / (B + S)]R SR WACC = .40(1 – .35)(.068) + .60(.1585)R WACC = .1130, or 11.30%Finally, we can use the WACC to discount the unlevered cash flows, which gives us an NPV of: NPV = –$4,500,000 + $675,000(PVIFA11.30%,20)NPV = $770,604.48Challenge15. a.The company is currently an all-equity firm, so the value as an all-equity firm equals thepresent value of aftertax cash flows, discounted at the cost of the firm’s unlevered cost of equity. So, the current value of the company is:V U = [(Pretax earnings)(1 –t C)] / R0V U = [($21,000,000)(1 – .35)] / .16V U = $85,312,500The price per share is the total value of the company divided by the shares outstanding, or:Price per share = $85,312,500 / 1,300,000Price per share = $65.63b.The adjusted present value of a firm equals its value under all-equity financing plus the netpresent value of any financing side effects. In this case, the NPV of financing side effects equals the aftertax present value of cash flows resulting from the firm’s debt. Given a known level of debt, debt cash flows can be discounted at the pretax cost of debt, so the NPV of the financing effects are:NPV = Proceeds – Aftertax PV(Interest Payments)NPV = $30,000,000 – (1 – .35)(.09)($30,000,000) / .09NPV = $10,500,000So, the value of the company after the recapitalization using the APV approach is:V = $85,312,500 + 10,500,000V = $95,812,500Since the company has not yet issued the debt, this is also the value of equity after the announcement. So, the new price per share will be:New share price = $95,812,500 / 1,300,000New share price = $73.70c.The company will use the entire proceeds to repurchase equity. Using the share price wecalculated in part b, the number of shares repurchased will be:Shares repurchased = $30,000,000 / $73.70Shares repurchased = 407,045And the new number of shares outstanding will be:New shares outstanding = 1,300,000 – 407,045New shares outstanding = 892,955The value of the company increased, but part of that increase will be funded by the new debt.The value of equity after recapitalization is the total value of the company minus the value of debt, or:New value of equity = $95,812,500 – 30,000,000New value of equity = $65,812,500So, the price per share of the company after recapitalization will be:New share price = $65,812,500 / 892,955New share price = $73.70The price per share is unchanged.d.In order to value a firm’s equity using the flow-to-equity approach, we must discount the cashflows available to equity holders at the cost of the firm’s levered equity. According to Modigliani-Miller Proposition II with corporate taxes, the required return of levered equity is: R S = R0 + (B/S)(R0–R B)(1 –t C)R S = .16 + ($30,000,000 / $65,812,500)(.16 – .09)(1 – .35)R S = .1807, or 18.07%After the recapitalization, the net income of the company will be:EBIT $21,000,000Interest 2,700,000EBT $18,300,000Taxes 6,405,000Net income $11,895,000The firm pays all of its earnings as dividends, so the entire net income is available toshareholders. Using the flow-to-equity approach, the value of the equity is:S = Cash flows available to equity holders / R SS = $11,895,000 / .1807S = $65,812,50016. a.If the company were financed entirely by equity, the value of the firm would be equal to thepresent value of its unlevered after-tax earnings, discounted at its unlevered cost of capital.First, we need to find the company’s unlevered cash flows, which are:Sales $17,500,000Variable costs 10,500,000EBT $7,000,000Tax 2,800,000Net income $4,200,000So, the value of the unlevered company is:V U = $4,200,000 / .13V U = $32,307,692.31b.According to Modigliani-Miller Proposition II with corporate taxes, the value of levered equityis:R S = R0 + (B/S)(R0–R B)(1 –t C)R S = .13 + (.35)(.13 – .07)(1 – .40)R S = .1426 or 14.26%c.In a world with corporate taxes, a firm’s weighted average cost of capital equals:R WACC = [B / (B + S)](1 –t C)R B + [S / (B + S)]R SSo we need the debt-value and equity-value ratios for the company. The debt-equity ratio forthe company is:B/S = .35B = .35SSubstituting this in the debt-value ratio, we get:B/V = .35S / (.35S + S)B/V = .35 / 1.35B/V = .26And the equity-value ratio is one minus the debt-value ratio, or:S/V = 1 – .26S/V = .74So, using the capital structure weights, the company’s WACC is:R WACC = [B / (B + S)](1 –t C)R B + [S / (B + S)]R SR WACC = .26(1 – .40)(.07) + .74(.1426)R WACC = .1165, or 11.65%We can use the weighted average cost of capital to discount the firm’s unlevered aftertax earnings to value the company. Doing so, we find:V L = $4,200,000 / .1165V L = $36,045,772.41Now we can use the debt-value ratio and equity-value ratio to find the value of debt and equity, which are:B = V L(Debt-value)B = $36,045,772.41(.26)B = $9,345,200.25S = V L(Equity-value)S = $36,045,772.41(.74)S = $26,700,572.16d.In order to value a firm’s equity using the flow-to-equity approach, we can discount the cashflows available to equity holders at the cost of the firm’s levered equity. First, we need to calculate the levered cash flows available to shareholders, which are:Sales $17,500,000Variable costs 10,500,000EBIT $7,000,000Interest 654,164EBT $6,345,836Tax 2,538,334Net income $3,807,502So, the value of equity with the flow-to-equity method is:S = Cash flows available to equity holders / R SS = $3,807,502 / .1426S = $26,700,572.1617. a.Since the company is currently an all-equity firm, its value equals the present value of itsunlevered after-tax earnings, discounted at its unlevered cost of capital. The cash flows to shareholders for the unlevered firm are:EBIT $118,000Tax 47,200Net income $70,800So, the value of the company is:V U = $70,800 / .14V U = $505,714.29b.The adjusted present value of a firm equals its value under all-equity financing plus the netpresent value of any financing side effects. In this case, the NPV of financing side effects equals the after-tax present value of cash flows resulting from debt. Given a known level of debt, debt cash flows should be discounted at the pre-tax cost of debt, so:NPV = Proceeds – Aftertax PV(Interest payments)NPV = $235,000 – (1 – .40)(.08)($235,000) / .08NPV = $94,000So, using the APV method, the value of the company is:APV = V U + NPV(Financing side effects)APV = $505,714.29 + 94,000APV = $599,714.29The value of the debt is given, so the value of equity is the value of the company minus the value of the debt, or:S = V–BS = $599,714.29 – 235,000S = $364,714.29c.According to Modigliani-Miller Proposition II with corporate taxes, the required return oflevered equity is:R S = R0 + (B/S)(R0–R B)(1 –t C)R S = .14 + ($235,000 / $364,714.29)(.14 – .08)(1 – .40)R S = .1632, or 16.32%d.In order to value a firm’s equity using the flow-to-equity approach, we can discount the cashflows available to equity holders at the cost of the firm’s levered equity. First, we need to calculate the levered cash flows available to shareholders, which are:EBIT $118,000Interest 18,800EBT $99,200Tax 39,680Net income $59,520。

公司理财学原理第十章习题答案二、单选题1、下列在确定公司利润分配政策时应考虑的因素中,不属于股东因素的是( D )。

A.规避风险B.稳定股利收入C.防止公司控制权旁落D.公司未来的投资机会2、( A )的依据是股利无关论。

A.剩余股利政策B.固定股利政策C.固定股利支付率政策D.低正常股利加额外股利政策3、剩余股利政策的优点是( C )。

A.有利于树立良好的形象B.有利于投资者安排收入和支出C.有利于企业价值的长期最大化D.体现投资风险与收益的对等4、某公司2005年度净利润为4000万元,预计2006年投资所需的资金为2000万元,假设目标资金结构是负债资金占60%,企业按照15%的比例计提盈余公积金,公司采用剩余股利政策发放股利,则2005年度企业可向投资者支付的股利为(B)万元。

A.2600B.3200C.2800D.22005、( B )适用于经营比较稳定或正处于成长期、信誉一般的公司。

A.剩余股利政策B.固定股利政策C.固定股利支付率政策D.低正常股利加额外股利政策6、( D )既可以在一定程度上维持股利的稳定性,又有利于企业的资本结构达到目标资本结构,使灵活性与稳定性较好的结合。

A.剩余股利政策B.固定股利政策C.固定股利支付率政策D.低正常股利加额外股利政策7、上市公司发放现金股利的原因不包括(D)。

A.投资者偏好B.减少代理成本C.传递公司的未来信息D.减少公司所得税负担8、( B )是确定在什么时候持有股票的股东可以获得股利的日期A.股利宣告日B.股权登记日C.除息日D.股利支付日9、某公司现有发行在外的普通股200万股,每股面值1元,资本公积300万元,未分配利润800万元,股票市价10元,若按10%的比例发放股票股利并按市价折算,公司报表中资本公积的数额将会增加( A )万元。

A.180B.280C.480D.30010、在下列股利政策中,股利与利润之间保持固定比例关系,体现风险投资与风险收益对等关系的是( C )A.剩余股利政策B.固定股利政策C.固定股利支付率政策D.低正常股利加额外股利政策11、某公司2006年末已发行在外的普通股为2000万股,拟发放10%的股票股利,并按发放股票股利后的股数支付现金股利,股利分配前的每股市价为20元,每股净资产为5元,若股利分配不改变市净率,并要求股利分配后每股市价达到18元。

公司金融作业题说明:公司财务原理 (原书第10版)+第22章(原书第12版)第4章24.DCF 和自由现金流混合肥料科学公司(CSI )从事的是将波士顿的城市污水转化为肥料的任务。

业务本身盈利不高,但是为了把CSI 留在这个行业中,城市委员会(MDC )同意支付任何必要的补贴,是CSI 的账面股权收益率能够达到10%。

预期年末CSI 将支付每股4美元的股利,再投资比例为40%,增长率为4%。

a .假设CSI 继续保持目前的增长趋势,以100美元的价格购买公司股票,预期长期收益率是多少?100美元中有多少是增长机会的现值的贡献?b .现在MDC 宣布了一项计划,需要CSI 处理剑桥市的城市污水。

因此,CSI 要在未来五年中逐步扩建工厂。

这就意味着在未来的五年中,CSI 必须要将80%的盈利进行再投资。

从第六年开始,它将能够恢复60%的股利支付率。

MDC 的计划一宣布,以及随后对CSI 的影响公布后,CSI 的股价将是多少?24.a. Here we can apply the standard growing perpetuity formula with DIV 1 = $4, g = 0.04 and P 0 = $100:8.0%.080.040$100$4g P DIV r 01==+=+=The $4 dividend is 60 percent of earnings. Thus:EPS 1 = 4/0.6 = $6.67Also:PVGO rEPS P 10+=PVGO 0.08$6.67$100+=PVGO = $16.63b.DIV 1 will decrease to: 0.20 ⨯ 6.67 = $1.33However, by plowing back 80 percent of earnings, CSI will grow by 8 percent per year for five years. Thus:Year 1 2 3 4 5 6 7, 8 . . . DIV t 1.33 1.44 1.55 1.68 1.81 5.88 Continued growth at EPS t6.677.207.788.409.079.804 percentNote that DIV 6 increases sharply as the firm switches back to a 60 percent payout policy. Forecasted stock price in year 5 is:$147.0400.085.88g r DIV P 65=-=-=Therefore, CSI’s stock price will increase to:$106.211.081471.811.081.681.081.551.081.441.081.33P 54320=+++++=第9章6.可分散风险很多投资项目都有可分散风险。

“可分散”在这里的含义是什么?项目的估值应该如何考虑可分散风险?应该完全忽略可分散风险吗?6.可分散风险是指与公司、行业或投资相关的风险。

这是一个固有的风险也称为非系统性风险。

投资者可以通过不同的投资来分散这种风险风险较小的证券。

许多投资项目都暴露在多种风险之下,意味着投资的风险项目可以减少。

项目价值评估的目的并没有充分考虑可分散的风险。

它不应该完全被企业忽视,因为它是一个影响项目的风险。

它没有被记录下来计算一个项目所需的回报率或资本成本。

换句话说,如果风险是分散的,项目的资本成本不会改变。

而计算所需的收益率,考虑系统的风险度量,即beta 。

9.判断正误 a .公司资本成本对所有项目来说,都是正确的贴现率,因为有些项目的高风险可以被其他项目的低风险所抵消。

(False )b .较迟发生的现金流比近期发生的现金流风险高,因此,长期项目需要更高的风险调整贴现率。

(False)c .与快速收益项目相比,在贴现率中加入修正因素低估长期项目。

(True)11.资本成本奥克弗洛基房地产公司的普通股总市值为6百万美元,其负债总价值为4百万美元。

公司财务主管估计,目前股票贝塔为1.5,预期市场风险溢价为4%(6%?),国库券利率为4%。

假设为简化起见,奥克弗洛基的负债无风险,公司不需要纳税。

a . 公司股票要求的收益率是多少?b . 估计公司资本成本c . 公司当前业务拓展项目的贴现率是多少?d . 假设公司想进行多样化,生产玫瑰色眼镜,无负债光学制造商的贝塔为1.2。

估计奥克弗洛基新项目的要求收益率。

11. a.r equity = r f + β ⨯ (r m – r f ) = 0.04 + (1.5 ⨯ 0.06) = 0.13 = 13%b. ⎪⎭⎫ ⎝⎛⨯+⎪⎭⎫ ⎝⎛⨯=+=0.13$10million $6million 0.04$10million $4million r V E r V D r equity debt assetsrassets = 0.094 = 9.4%c. 资金成本取决于被评估项目的风险。

如果项目的风险类似于公司其他资产的风险,那么合适的回报率就是公司的资本成本。

在这里,适当的贴现率是9.4%。

d.r equity = r f + β ⨯ (r m – r f ) = 0.04 + (1.2 ⨯ 0.06) = 0.112 = 11.2%⎪⎭⎫ ⎝⎛⨯+⎪⎭⎫ ⎝⎛⨯=+=0.112$10million $6million 0.04$10million $4million r V E r V D r equity debt assetsr assets = 0.0832 = 8.32%16.资产贝塔什么类型的公司需要估计行业资产贝塔?如何估计?描述具体步骤。

从事投资组合的金融分析师或投资者可能会使用行业betas 。

为了计算行业beta ,我们将构建一系列行业投资组合,并评估该组合产生的回报与历史市场走势之间的关系。

第10章14.敏感性分析Rustic Welt 公司正在考虑用更现代的设备取代老式贴边机。

新设备的成本9百万美元(已有老设备无残值)。

新机器的好处是预期会使单位生产成本从8美元降为4美元。

但是,如下表所示,在未来的销售量、新机器的性能方面存在某些不确定性:(P213)假设贴现率为12%,公司不需要纳税。

对设备更换决策进行敏感性分析。

14. If Rustic replaces now rather than in one year, several things happen:i. It incurs the equivalent annual cost of the $9 million capital investment.ii.It reduces manufacturing costs.For example, for the “Expected” case, analyzing “Sales” we have (all dollar figures in millions):i.The economic life of the new machine is expected to be 10 years, so the equivalentannual cost of the new machine is:$9/5.6502 = $1.59ii.The reduction in manufacturing costs is:0.5 $4 = $2.00Thus, the equivalent annual cost savings is:–$1.59 + $2.00 = $0.41Continuing the analysis for the other cases, we find:Equivalent Annual Cost Savings (Millions)Pessimistic Expected OptimisticSales 0.01 0.41 1.21 Manufacturing Cost -0.59 0.41 0.91Economic Life 0.03 0.41 0.60第11章1.经济租金判断正误-HJ(P238 利润超出资本成本的部分就是经济租金)a.赚取到资本机会成本的公司,也在获取经济租金F(一个赚取资本的机会成本的公司正在赚取经济租金。

这种说法是错误的。

经济租金是指超过资本成本的利润。

这就意味着,额外的资本成本和高于资本的机会成本是众所周知的。

) b.投资正NPV项目的公司预期得到经济租金T(经济租金是指超过资本成本的利润。

一个积极的净现值收益风险可以在未来获得更多的利润。

这将带来额外的利润,被称为经济租金。

)c.财务经理应该尽力确定公司能够获得经济租金的领域,因为在这个领域才有可能发现NPV为正的项目T(财务经理应该设法确定他们的公司可以赚取经济租金的领域,因为很可能会发现正的npv项目。

这句话是正确的。

经济租金是指超过资本成本的利润。

能够赚取经济租金的风险投资肯定会导致正净现值的情况。

额外的利润是经济租金,只有积极的净现值投资才有可能。

)d.经济租金是经营性资本设备的等价年度成本F(经济租金是相当于营运资本设备的年成本。

这个声明是错误的。

经济租金是指超过资本成本的利润。

经济租金与运营资本设备成本无关。

)10.经济租金由于购买了一项关键专利,你公司现在是北美独家生产barkelgassers(BG)的厂家。

购买每年生产200 000BG的生产设备,需要立即发生资本支出25百万美元。

每单位BG的生产成本估计为65美元。

BG市场经理非常自信,所有200 000单位的BG都能够以每单位100美元的价格售出,直到5年后专利到期。

之后,市场经理没有给出关于销售价格的线索。

BG项目的NPV是多少?假设实际资本成本为9%。

为了简单起见,还有以下假设:●制造BG的技术不变。

资本成本和生产成本的实际价值不变。

●竞争对手了解这项技术,专利一到期,就能够马上进入,也就是第六年●如果你公司立即投资,12个月后将满负荷生产,即第一年●没有税●BG生产设备将使用12年,使用期结束时无残值。

合理假设在第六年对手进入市场后,会迅速的让价格降低到经济租金为0,且资本成本9%为行业普遍的资本成本。

那么,从第六年开始,NPV为0.因题目中未提供通胀数据,方便起见,假设通胀通胀为0那么,也就是说,第1至第4年相对于9%资本成本的超额收益,减去建设周期周期中的资本成本,就是项目NPV第1至第4年超额收益为 200000 * (100 - 35)- 25000000 * 9% = 1075000折现到投资时刻=1075000/((1+9%)^2) +1075000/((1+9%)^3)+ 1075000/((1+9%)^4)+ 1075000/((1+9%)^5) = 3195137建设周期中资金成本 = 25000000 * 9% = 2250000折现到投资时刻 = 2250000 / (1+9%) = 2064220那么,项目 NPV = 3195137– 2064220 = 1130917第12章-HJ9.激励假设工厂和部门经理的报酬只有固定工资,没有其他激励或奖金。