公司理财原版题库Chap029

- 格式:rtf

- 大小:127.99 KB

- 文档页数:18

公司理财考试题目参考答案一、辨析简答题任选5小题; 每小题12分;共60分1.古人云:“车到山前必有路”;从公司理财的角度如何辩证地认识这句话呢答:车沿着路走;即使到了山前仍然可以找到出路;尽管从远处可能看不到出路在哪..从公司理财的角度而言;一方面;作为市场中的微观主体;企业要按照市场和财务的原理合理规划企业的发展之路;并坚信在这条“路”前进不止;一定能实现企业的目标;另一方面;微观企业也应认识到宏观环境的复杂多变;认真分析握宏观环境;主动适应宏观环境;唯于是;才能在企业发展的十字路口找到适合企业发展的康庄大道..2.有人认为“企业家就是在风险条件下做出合理的决策”;对此;你有何评论答:这句话道出了风险与收益的辩证关系;企业决策所面临的风险无处不在;不同的决策对应着不同的风险;不同的风险也意味着不同收益..作为市场中的逐利者;企业家决策时的目标毫无疑问是追求企业收益或者说企业价值最大化;但与此同时也面临着不同决策所包涵风险的制约;并考虑企业自身承担风险的能力..因此;企业的决策过程;就是一个在既定风险水平约束下;如何实现企业收益最大化的求解过程..3.中国的中小企业融资难是其规模问题还是所有制问题为什么答:企业规模和所有制尤其是产权结构都会成为影响中小企业融资的主要因素;但从远来看;中小企业融资难主要是规模问题..首先;所有制会影响中小企业的融资;在实务中;我们发现;产权结构清晰、责任明确的中小企业往往更易获得银行等金融机构的资金;而产权结构模糊的个体企业和集体企业则难以获得;其次;规模也会影响中小企业融资;规模较大的企业;往往能够提供更多的抵押物;并获得银行等金融机构较高的评级;因此更易从银行等金融机构获得资金支持;规模较小的企业则难以获得这样的便利..从长远来看;随着中国经济市场化改革进程的深入;企业的产权结构日前明晰;企业的规模将成为影响中小企业融资的主要因素;因此;通过互助贷款协议等方式实现企业规模的虚拟放大是破解中小企业融资难的主要途径..4.如何理解“资本结构体现了公司治理结构”呢答:资本结构包括股权和债权两个方面;公司治理结构主要体现公司权力的安排..首先;公司的股权结构影响公司的权力安排;不同的股权在股东会上拥有不同份量的投票权;进而影响董事会和监事会;以及经理层的人事和权力安排;以维护自身利益;其次;公司的债务也会影响公司的权力安排;负债是公司发展的助跑器;但与此同时;负债还本付息的压力;以及债务人对企业发展的期望;都会成为影响企业治理层和管理层决策的重要因素;进而影响公司的决策导向和权力安排..5.许多人认为中国国有企业的负债比率过高; 请从财务杠杆的角度; 评述这种说法..答:企业负债比率越高;财务杠杆越大..由于债务的利息成本可以在税前扣除;对于高盈利的企业;高财务杠杆会让企业充分享受债务所带来的节税效益;使企业快速扩张;但对于低盈利或者亏损的企业;高财务杠杆会加速企业的破产..中国国有企业的高负债比率主要有以下几个原因:一是由于垄断地位;国有企业的盈利较高;高财务杠杆能加速其扩张;二是国有企业高杠杆的风险由其出资人——国家承担;在企业风险机制尚未健全之前;企业决策者往往表现的更加激进;三是国有企业由于其规模和政策上的优势;更易获得债务资金..6.资本预算与经营预算、财务预算如何有机地融合在一起答:资本预算是对某一项目投入、产出的整体预算;进而评估项目是否可靠;经营预算和财务预算是对具体项目在某一特定时期的经营状况及其财务表现的预算..经营预算和财务预算是资本预算编制的基础;资本预算又对财务预算的编制产生影响..为将三者有机整合起来;一方面;在编制资本预算之前;应对企业的经营和财务状况进行充分的预算;并编制详实的经营预算和财务预算;也确保资本预算及其决策的科学性;另一方面;在编制财务预算时;应充分考虑资本预算和经营预算的相关数据和信息;以确保财务预算的准确性..7.营运资本净额为零时一种理想还是梦想答:营运资本净额是指企业组织的流动资产总额与流动负债总额之间的差额..营运资本为零时;企业的流动资产总额等于流动负债总额;企业的长期资产由长期负债和股东权益提供;企业的资产负债结构最为合理..在实务中;由于经营的季节性和不确定性;企业营运资本净额往往不为零;并呈现一定的波动性;但营运资本为零仍然可以成为企业追求的目标;从这个角度而言;营运资本为零是一种理想..二、讨论分析题第1、2小题每题12分; 第3小题16分;共40分1.Tomas 公司是一家小型游艇贸易商..2001年度卖出一艘价值100;000元的游艇..该游艇的成本总额为80;000元.. Tomas 公司已经支付了购买该游艇的货款80;000元;但是;在年底还没有从顾客手中收到这100;000的货款..问题:1Tomas 公司能否得到价值补偿2会计学与公司理财学有何差异答:1Tomas 公司能否得到价值补偿取决于其在100000元货款最终收回前80000元成本所发生的资金成本;以及最终收回该货款的可能性..一方面;如果在100000元货款最终收回前;80000元成本所发生的资金成本大于20000元;其价值得到了补偿;反之;不能得到补偿;另一方面;如果最终无法收回100000元货款;其价值也得不到补偿..2会计学与公司理财学的差异:①货币时间价值..会计学往往根据权责发生责确认收入和成本;而无论收入和成本是实现;而公司理财学往往根据现金流入或流出确认收入或成本;考虑了资金的时间价值;②收益和风险的均衡..会计学往往在风险出现时或出现迹象时;才考虑风险对会计确认的影响;而公司理财学在决策时即考虑风险因素;以及由此对决策的影响..2.股评专家经常告诉股民;“某只股票的价值被市场低估;具有投资价值;投资者可以介入”;可是;投资者购买了这只股票后;却被长期“套牢”;更谈不上获利..于是;投资者大骂股评专家被人收买;为“庄家”说话..问题:1股评专家说“某只股票的价值被市场低估”的依据是什么2股票内在价值与市场价格之间的关系如何如何正确看待这种关系答:1其依据是股票的内在价值;主要根据该公司过往财务报表数据、股票市场和行业相关的数据;运用股票估价模型计算而来..2两者的关系:在完全有效的市场中;股票的内在价值等于其市场价格;但在现实经济生活中;由于信息的不对称性;完全有效的市场并不存在;股票的市场价格往往围绕其内在价值上下波动..股票市场价格和内在价值的波动关系;一方面使得股票市场中大量投机的存在;甚至有些所谓“专家”利用其获取信息上的优势;为“庄家”大放厥词;干扰普通股民的判断;获取非法暴利;另一方面;我们也应看到;股票市场价格围绕内在价值上下波动;也有利于市场价格真实的反映股票的内在价值;并实现两者之间的动态平衡..3.西方公司理财的融资优先次序Pecking Order理论认为:公司首先选择的融资方式是内部融资留存收益融资;其次是债务融资;再次是优先股融资;接下来是混合证券融资如可转换债券融资;最后才是普通股融资..1中国上市公司为何热衷于配股2这种热衷于配股的行为又如何得以实现答:1配股是根据公司发展需要;依照相关程序;向原股东进一步发行、筹集资金的行为..中国上市公司热衷于配股的主要原因:一是有利于扩大公司股本规模;降低公司的资产负债率;二是配股比单纯的增发股票条件更为宽松;发行费用也较低;有利于弥补上市公司其他融资渠道受阻时的资金缺口;三是配股在正常情况下;发行的价格按发行配股公告时折价10%到25%;因此会拉低高价股票;为股票价格的后续上涨留下空间..2配股是上市公司再融资方式的一种;其实现步骤如下:①上市公司制定配股方案;并报证券监管部门审批通过后;发布配股公选;②上市公司原有股东在规定的时间内确认购买数量并缴款;③原有股东股票到账;上市公司收到股票价款..。

公司理财试题及答案解析一、单项选择题(每题2分,共20分)1. 公司理财的主要目标是()。

A. 利润最大化B. 股东财富最大化C. 企业价值最大化D. 市场份额最大化答案:B解析:公司理财的主要目标是股东财富最大化,即通过合理配置资源、降低成本、提高效率等方式,使股东的财富得到最大化的增长。

2. 公司理财的基本原则包括()。

A. 风险与收益相匹配B. 资金的时间价值C. 投资组合多元化D. 以上都是答案:D解析:公司理财的基本原则包括风险与收益相匹配、资金的时间价值和投资组合多元化。

这些原则有助于公司在风险可控的前提下,实现资金的有效配置和收益最大化。

3. 以下哪项不是公司理财的主要活动?()A. 投资决策B. 融资决策C. 营运资金管理D. 人力资源管理答案:D解析:公司理财的主要活动包括投资决策、融资决策和营运资金管理。

人力资源管理虽然对公司运营至关重要,但它不属于公司理财的范畴。

4. 以下哪项不是公司理财中的风险类型?()A. 市场风险B. 信用风险C. 操作风险D. 人力资源风险答案:D解析:公司理财中的风险类型包括市场风险、信用风险和操作风险。

人力资源风险虽然对公司运营有影响,但它不属于公司理财中的风险类型。

5. 以下哪项不是公司理财中的投资决策?()A. 资本预算B. 证券投资C. 营运资金管理D. 项目评估答案:C解析:公司理财中的投资决策包括资本预算、证券投资和项目评估。

营运资金管理属于公司理财中的融资决策范畴。

6. 以下哪项不是公司理财中的融资决策?()A. 股权融资B. 债务融资C. 营运资金管理D. 资本结构决策答案:C解析:公司理财中的融资决策包括股权融资、债务融资和资本结构决策。

营运资金管理属于公司理财中的投资决策范畴。

7. 以下哪项不是公司理财中的营运资金管理?()A. 现金管理B. 存货管理C. 应收账款管理D. 人力资源管理答案:D解析:公司理财中的营运资金管理包括现金管理、存货管理和应收账款管理。

公司理财试题及答案一、选择题1. 下列哪个不是公司理财的基本目标?A. 增加现金流入B. 最大化利润C. 降低风险D. 提高市场份额答案:D2. 公司理财的基本原则包括以下哪些?A. 高收益原则B. 高流动性原则C. 长期经营原则D. 分散投资原则答案:BCD3. 公司现金流量分析的主要目的是什么?A. 评估公司现金收入和支出的状况B. 分析公司的盈利能力C. 了解公司的资产负债状况D. 预测公司未来的发展趋势答案:A二、简答题1. 请简要解释公司风险管理的概念和重要性。

答案:公司风险管理是指对公司面临的各种风险进行识别、评估、控制和监测的过程。

它的重要性体现在以下几个方面:- 风险管理有助于公司降低风险,防范损失,保障公司的可持续发展。

- 通过全面分析风险,公司可以制定有效的风险应对策略,提高决策的准确性和有效性。

- 风险管理可以增加公司的竞争力,提高投资者、合作伙伴和顾客的信任度。

2. 请列举一些常见的公司理财工具,并简要说明其特点。

答案:常见的公司理财工具包括:- 现金管理工具:如短期存款、货币市场基金等。

这些工具具有流动性高、风险低的特点,适合用于短期的现金周转和备付金管理。

- 债券:公司可以通过发行债券融资,债券具有固定收益、期限确定等特点,适合用于长期资金的筹集。

- 股票:公司可以通过发行股票融资,股票具有股东权益和股东收益的特点,适合用于扩大股东基础和提高公司声誉。

- 衍生品:如期货、期权等。

衍生品具有杠杆效应和价格波动性高的特点,可以用于套期保值和投机交易。

三、案例分析某公司在进行资金投资决策时,面临着以下两个项目:项目A:投资额为100万元,预期年收益为10万元,投资期限为5年,风险评估为中等。

项目B:投资额为80万元,预期年收益为8万元,投资期限为3年,风险评估为低。

请根据公司理财的原则,帮助公司选择投资项目并给出理由。

答案:根据公司理财的原则,首先应该考虑的是投资的风险。

项目A和项目B的风险评估分别为中等和低,因此项目B在风险控制方面更为有利。

习题一1.5.1 单项选择题1 .不能偿还到期债务是威胁企业生存的()。

A .外在原因B .内在原因C .直接原因D .间接原因2.下列属于有关竞争环境的原则的是()。

A .净增效益原则B .比较优势原则C .期权原则D .自利行为原则3.属于信号传递原则进一步运用的原则是指()A .自利行为原则B .比较优势原则C . 引导原则D .期权原则4 .从公司当局可控因素来看,影响报酬率和风险的财务活动是()。

A .筹资活动B .投资活动C .营运活动D .分配活动5 .自利行为原则的依据是()。

A .理性的经济人假设B .商业交易至少有两方、交易是“零和博弈”,以及各方都是自利的C .分工理论D .投资组合理论6 .下列关于“有价值创意原则”的表述中,错误的是()。

A .任何一项创新的优势都是暂时的B .新的创意可能会减少现有项目的价值或者使它变得毫无意义C .金融资产投资活动是“有价值创意原则”的主要应用领域D .成功的筹资很少能使企业取得非凡的获利能力7 .通货膨胀时期,企业应优先考虑的资金来源是()A .长期负债B .流动负债C .发行新股D .留存收益8.股东和经营者发生冲突的根本原因在于()。

A .具体行为目标不一致B .掌握的信息不一致C .利益动机不同D ,在企业中的地位不同9 .双方交易原则没有提到的是()。

A .每一笔交易都至少存在两方,双方都会遵循自利行为原则B .在财务决策时要正确预见对方的反映C .在财务交易时要考虑税收的影响D .在财务交易时要以“自我为中心”10.企业价值最大化目标强调的是企业的()。

A .预计获利能力B .现有生产能力C .潜在销售能力D .实际获利能力11.债权人为了防止其利益受伤害,通常采取的措施不包括()。

A .寻求立法保护B .规定资金的用途C .提前收回借款D .不允许发行新股12.理性的投资者应以公司的行为作为判断未来收益状况的依据是基于()的要求。

《公司理财》试题及答案第一章公司理财概述一、单选题1、在筹资理财阶段,公司理财的重点内容是(b)。

A资金的有效使用B如何筹集所需资金C研究投资组合d国际融资II。

填空1、在内部控制理财阶段,公司理财的重点内容是如何有效地(运用资金)。

2.西方经济学家和企业家过去把(利润最大化)作为公司的经营目标和财务目标。

3.现代公司的财务目标是股东财富最大化。

4、公司资产价值增加,生产经营能力提高,意味着公司具有持久的、强大的获利能力和(偿债能力)。

5.本公司的融资渠道主要分为两类:一类是募集(自有资金),另一类是募集(借入资金)。

3、简短回答问题1、为什么以股东财富最大化作为公司理财目标?(1)考虑到了货币时间价值和风险价值;(2)体现了对公司资产保值增值的要求;(3)有利于克服公司经营上的短期行为,促使公司理财当局从长远战略角度进行财务决策,不断增加公司财富。

2、公司理财的具体内容是什么?(1)筹资决策;(2)投资决策;(3)股利分配决策。

第二章财务报表分析一、单项选择题1.资产负债表为(b)。

a动态报表b静态报表c动态与静态相结合的报表d既不是动态报表也不是静态报表2、下列负债中属于长期负债的是(d)。

A应付账款B应付税款C预计负债D应付债券3。

公司最具流动性的资产是(a)。

a货币资金b短期投资c应收账款d存货4、下列各项费用中属于财务费用的是(c)。

A广告费B劳动保险费C利息费D坏账损失5。

反映公司收入与职业比例关系的财务指标为(b)。

a资产负债率b资产利润率c销售利润率d成本费用利润率二、多项选择题1.资产负债表中与财务状况计量直接相关的会计要素为(ABC)。

a资产b负债c所有者权益d成本费用e收入利润2、与利润表中经营成果的计量有直接联系的会计要素有(bcd)。

资产B收入C成本和费用D利润E所有者权益iii填写空白1、资产的实质是(经济资源)。

2.公司所有者权益金额为(资产)减去(负债)后的余额。

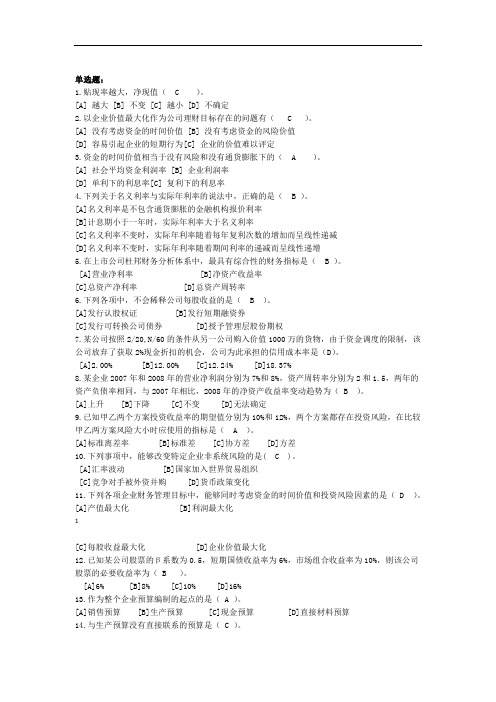

单选题:1.贴现率越大,净现值( C )。

[A] 越大 [B] 不变 [C] 越小 [D] 不确定2.以企业价值最大化作为公司理财目标存在的问题有( C )。

[A] 没有考虑资金的时间价值 [B] 没有考虑资金的风险价值[D] 容易引起企业的短期行为[C] 企业的价值难以评定3.资金的时间价值相当于没有风险和没有通货膨胀下的( A )。

[A] 社会平均资金利润率 [B] 企业利润率[D] 单利下的利息率[C] 复利下的利息率4.下列关于名义利率与实际年利率的说法中,正确的是( B )。

[A]名义利率是不包含通货膨胀的金融机构报价利率[B]计息期小于一年时,实际年利率大于名义利率[C]名义利率不变时,实际年利率随着每年复利次数的增加而呈线性递减[D]名义利率不变时,实际年利率随着期间利率的递减而呈线性递增5.在上市公司杜邦财务分析体系中,最具有综合性的财务指标是( B )。

[A]营业净利率 [B]净资产收益率[C]总资产净利率 [D]总资产周转率6.下列各项中,不会稀释公司每股收益的是( B )。

[A]发行认股权证 [B]发行短期融资券[C]发行可转换公司债券 [D]授予管理层股份期权7.某公司按照2/20,N/60的条件从另一公司购入价值1000万的货物,由于资金调度的限制,该公司放弃了获取2%现金折扣的机会,公司为此承担的信用成本率是(D)。

[A]2.00% [B]12.00% [C]12.24% [D]18.37%8.某企业2007年和2008年的营业净利润分别为7%和8%,资产周转率分别为2和1.5,两年的资产负债率相同,与2007年相比,2008年的净资产收益率变动趋势为( B )。

[A]上升 [B]下降 [C]不变 [D]无法确定9.已知甲乙两个方案投资收益率的期望值分别为10%和12%,两个方案都存在投资风险,在比较甲乙两方案风险大小时应使用的指标是( A )。

[A]标准离差率 [B]标准差 [C]协方差 [D]方差10.下列事项中,能够改变特定企业非系统风险的是( C )。

《公司理财》考试范围:第3~7章,第13章,第16~19章,其中第16章和18章为较重点章节。

书上例题比较重要,大家记得多多动手练练。

PS:书中课后例题不出,大家可以当习题练练~考试题型:1.单选题10分 2.判断题10分 3.证明题10分 4.计算分析题60分 5.论述题10分注:第13章没有答案第一章1.在所有权形式的公司中,股东是公司的所有者。

股东选举公司的董事会,董事会任命该公司的管理层。

企业的所有权和控制权分离的组织形式是导致的代理关系存在的主要原因。

管理者可能追求自身或别人的利益最大化,而不是股东的利益最大化。

在这种环境下,他们可能因为目标不一致而存在代理问题。

2.非营利公司经常追求社会或政治任务等各种目标。

非营利公司财务管理的目标是获取并有效使用资金以最大限度地实现组织的社会使命。

3.这句话是不正确的。

管理者实施财务管理的目标就是最大化现有股票的每股价值,当前的股票价值反映了短期和长期的风险、时间以及未来现金流量。

4.有两种结论。

一种极端,在市场经济中所有的东西都被定价。

因此所有目标都有一个最优水平,包括避免不道德或非法的行为,股票价值最大化。

另一种极端,我们可以认为这是非经济现象,最好的处理方式是通过政治手段。

一个经典的思考问题给出了这种争论的答案:公司估计提高某种产品安全性的成本是30美元万。

然而,该公司认为提高产品的安全性只会节省20美元万。

请问公司应该怎么做呢”5.财务管理的目标都是相同的,但实现目标的最好方式可能是不同的,因为不同的国家有不同的社会、政治环境和经济制度。

6.管理层的目标是最大化股东现有股票的每股价值。

如果管理层认为能提高公司利润,使股价超过35美元,那么他们应该展开对恶意收购的斗争。

如果管理层认为该投标人或其它未知的投标人将支付超过每股35美元的价格收购公司,那么他们也应该展开斗争。

然而,如果管理层不能增加企业的价值,并且没有其他更高的投标价格,那么管理层不是在为股东的最大化权益行事。

一、公司理财基本技能单选题1、有甲、乙两台设备可供选用,甲设备的年使用费比乙设备低2000元,但价格高于乙设备8000元。

若资本成本为10%,甲设备的使用期应长于(D)年,选用甲设备才是有利的A、4B、5C、4.6D、5.42、(F/A,10%,11)=18.531普通年金现值系数的倒数称为(D)A、复利现值系数B、普通年金终值系数C、偿债基金系数D、资本回收系数3、关于风险报酬正确的表述是(D )A、风险报酬是必要投资报酬B、风险报酬是投资者的风险态度C、风险报酬是无风险报酬加通胀贴补D、风险报酬率=风险报酬斜率×风险程度4、以资本利润率最大化作为公司理财目标,存在的缺陷是(D )A、不能反映资本的获利水平B、不能用于不同资本规模的企业间比较C、不能用于同一企业的不同期间比较D、没有考虑风险因素与时间价值5、(F./A,10%,9)=13.579 已知,则10年、10%的即付年金终值系数为(A )。

A、17.531B、15.937C、14.579D、12.5796、下列风险因素中,( D)可以引起实质性风险A、偷工减料引起产品事故B、新产品设计错误C、信用考核不严谨而出现贷款拖欠D、食物质量对人体的危害7、我国企业应采用的较为合理的财务目标是( C)A、利润最大化B、每股利润最大化C、企业价值最大化D、资本利润率最大化8、当一年内复利m次时,其名义利率r与实际利率i之间的关系是(A)A、 i=(1+r/m)m-1B、 i=(1+r/m)-1C、i=(1+r/m)-m-1D、i=1-(1+r/m)9、某公司向银行借款100万元,借款期限2年,借款利率6%,每半年付息1次,该笔借款的实际利率为(A )A、6.09%B、6%C、6.21%D、5.80%10、企业投资可以分为广义投资和狭义投资,狭义的投资仅指(D)A、固定资产投资B、证券投资C、对内投资D、对外投资12、企业财务管理是企业经济管理工作的一个组成部分,区别于其他经济管理工作的特点在于它是一种(C)A、劳动要素的管理B、物资设备的管理C、资金的管理D、使用价值的管理13、x.y方案的标准离差是1.5,方案的标准离差是1.4,如两方案的期望值相同,则两方案的风险关系为(A)A、x>yB、x<YC、无法确定D、x=y14、我国企业财务管理的最优目标是(D)A、总产值最大化B、利润最大化C、股东财富最大化D、企业价值最大化15、注册资本由等额股份构成并通过发行股票筹集资本的是(D )A、独资企业B、合资企业C、合伙企业D、股份有限公司16、以资本利润率最大化作为公司理财目标,存在的缺陷是( D)A、不能反映资本的获利水平B、不能用于不同资本规模的企业间比较C、不能用于同一企业的不同期间比较D、没有考虑风险因素与时间价值17、与债券信用等级有关的利率因素是(C)A、通货膨胀附加率B、到期风险附加率C、违约风险附加率D、纯粹利率18、现代企业财务管理的最优目标是( C)A、利润最大化B、风险最小化C、企业价值最大化D、资本最大化19、一项500万元的借款,借款期5年,年利率为8%,若每年半年复利一次,年实际利率会高出名义利率( C)A、4%B、0.24%C、0.16%D、0.80%20、关于风险报酬正确的表述是(D )A、风险报酬是必要投资报酬B、风险报酬是投资者的风险态度C、风险报酬是无风险报酬加通胀贴补D、风险报酬率=风险报酬斜率×风险程度21、一项投资的利率为10%,期限7年,其投资回收系数为(C )A、0.513B、4.868C、0.21D、1.6122、一定时期内每期期末等额收付的年金是(A )A、普通年金B、预付年金C、递延年金D、永续年金23、企业与政府间的财务关系体现为(B )A、债权债务关系B、强制和无偿的分配关系C、资金结算关系D、风险收益对等关系24、表示资金时间价值的利息率是(C )。

(完整版)公司理财-罗斯课后习题答案-CAL-FENGHAI-(2020YEAR-YICAI)_JINGBIAN第一章1.在所有权形式的公司中,股东是公司的所有者。

股东选举公司的董事会,董事会任命该公司的管理层。

企业的所有权和控制权分离的组织形式是导致的代理关系存在的主要原因。

管理者可能追求自身或别人的利益最大化,而不是股东的利益最大化。

在这种环境下,他们可能因为目标不一致而存在代理问题。

2.非营利公司经常追求社会或政治任务等各种目标。

非营利公司财务管理的目标是获取并有效使用资金以最大限度地实现组织的社会使命。

3.这句话是不正确的。

管理者实施财务管理的目标就是最大化现有股票的每股价值,当前的股票价值反映了短期和长期的风险、时间以及未来现金流量。

4.有两种结论。

一种极端,在市场经济中所有的东西都被定价。

因此所有目标都有一个最优水平,包括避免不道德或非法的行为,股票价值最大化。

另一种极端,我们可以认为这是非经济现象,最好的处理方式是通过政治手段。

一个经典的思考问题给出了这种争论的答案:公司估计提高某种产品安全性的成本是30美元万。

然而,该公司认为提高产品的安全性只会节省20美元万。

请问公司应该怎么做呢?”5.财务管理的目标都是相同的,但实现目标的最好方式可能是不同的,因为不同的国家有不同的社会、政治环境和经济制度。

6.管理层的目标是最大化股东现有股票的每股价值。

如果管理层认为能提高公司利润,使股价超过35美元,那么他们应该展开对恶意收购的斗争。

如果管理层认为该投标人或其它未知的投标人将支付超过每股35美元的价格收购公司,那么他们也应该展开斗争。

然而,如果管理层不能增加企业的价值,并且没有其他更高的投标价格,那么管理层不是在为股东的最大化权益行事。

现在的管理层经常在公司面临这些恶意收购的情况时迷失自己的方向。

7.其他国家的代理问题并不严重,主要取决于其他国家的私人投资者占比重较小。

较少的私人投资者能减少不同的企业目标。

Chapter 2: Accounting Statements and Cash Flow2.10AssetsCurrent assetsCash $ 4,000Accounts receivable 8,000Total current assets $ 12,000Fixed assetsMachinery $ 34,000Patents 82,000Total fixed assets $116,000Total assets $128,000Liabilities and equityCurrent liabilitiesAccounts payable $ 6,000Taxes payable 2,000Total current liabilities $ 8,000Long-term liabilitiesBonds payable $7,000Stockholders equityCommon stock ($100 par) $ 88,000Capital surplus 19,000Retained earnings 6,000Total stockholders equity $113,000Total liabilities and equity $128,0002.11One year ago TodayLong-term debt $50,000,000 $50,000,000Preferred stock 30,000,000 30,000,000Common stock 100,000,000 110,000,000Retained earnings 20,000,000 22,000,000Total $200,000,000 $212,000,0002.12Total Cash Flow ofthe Stancil CompanyCash flows from the firmCapital spending $(1,000)Additions to working capital (4,000)Total $(5,000)Cash flows to investors of the firmShort-term debt $(6,000)Long-term debt (20,000)Equity (Dividend - Financing) 21,000Total $(5,000)[Note: This table isn’t the Statement of Cash Flows, which is only covered in Appendix 2B, since the latter has th e change in cash (on the balance sheet) as a final entry.]2.13 a. The changes in net working capital can be computed from:Sources of net working capitalNet income $100Depreciation 50Increases in long-term debt 75Total sources $225Uses of net working capitalDividends $50Increases in fixed assets* 150Total uses $200Additions to net working capital $25*Includes $50 of depreciation.b.Cash flow from the firmOperating cash flow $150Capital spending (150)Additions to net working capital (25)Total $(25)Cash flow to the investorsDebt $(75)Equity 50Total $(25)Chapter 3: Financial Markets and Net Present Value: First Principles of Finance (Advanced)3.14 $120,000 - ($150,000 - $100,000) (1.1) = $65,0003.15 $40,000 + ($50,000 - $20,000) (1.12) = $73,6003.16 a. ($7 million + $3 million) (1.10) = $11.0 millionb.i. They could spend $10 million by borrowing $5 million today.ii. They will have to spend $5.5 million [= $11 million - ($5 million x 1.1)] at t=1.Chapter 4: Net Present Valuea. $1,000 ⨯ 1.0510 = $1,628.89b. $1,000 ⨯ 1.0710 = $1,967.15c. $1,000 ⨯ 1.0520 = $2,653.30d. Interest compounds on the interest already earned. Therefore, the interest earned inSince this bond has no interim coupon payments, its present value is simply the present value of the $1,000 that will be received in 25 years. Note: As will be discussed in the next chapter, the present value of the payments associated with a bond is the price of that bond.PV = $1,000 /1.125 = $92.30PV = $1,500,000 / 1.0827 = $187,780.23a. At a discount rate of zero, the future value and present value are always the same. Remember, FV =PV (1 + r) t. If r = 0, then the formula reduces to FV = PV. Therefore, the values of the options are $10,000 and $20,000, respectively. You should choose the second option.b. Option one: $10,000 / 1.1 = $9,090.91Option two: $20,000 / 1.15 = $12,418.43Choose the second option.c. Option one: $10,000 / 1.2 = $8,333.33Option two: $20,000 / 1.25 = $8,037.55Choose the first option.d. You are indifferent at the rate that equates the PVs of the two alternatives. You know that rate mustfall between 10% and 20% because the option you would choose differs at these rates. Let r be thediscount rate that makes you indifferent between the options.$10,000 / (1 + r) = $20,000 / (1 + r)5(1 + r)4 = $20,000 / $10,000 = 21 + r = 1.18921r = 0.18921 = 18.921%The $1,000 that you place in the account at the end of the first year will earn interest for six years. The $1,000 that you place in the account at the end of the second year will earn interest for five years, etc. Thus, the account will have a balance of$1,000 (1.12)6 + $1,000 (1.12)5 + $1,000 (1.12)4 + $1,000 (1.12)3= $6,714.61PV = $5,000,000 / 1.1210 = $1,609,866.18a. $1.000 (1.08)3 = $1,259.71b. $1,000 [1 + (0.08 / 2)]2 ⨯ 3 = $1,000 (1.04)6 = $1,265.32c. $1,000 [1 + (0.08 / 12)]12 ⨯ 3 = $1,000 (1.00667)36 = $1,270.24d. $1,000 e0.08 ⨯ 3 = $1,271.25e. The future value increases because of the compounding. The account is earning interest on interest. Essentially, the interest is added to the account balance at the e nd of every compounding period. During the next period, the account earns interest on the new balance. When the compounding period shortens, the balance that earns interest is rising faster.The price of the consol bond is the present value of the coupon payments. Apply the perpetuity formula to find the present value. PV = $120 / 0.15 = $800a. $1,000 / 0.1 = $10,000b. $500 / 0.1 = $5,000 is the value one year from now of the perpetual stream. Thus, the value of theperpetuity is $5,000 / 1.1 = $4,545.45.c. $2,420 / 0.1 = $24,200 is the value two years from now of the perpetual stream. Thus, the value of the perpetuity is $24,200 / 1.12 = $20,000.pply the NPV technique. Since the inflows are an annuity you can use the present value of an annuity factor.ANPV = -$6,200 + $1,200 81.0= -$6,200 + $1,200 (5.3349)= $201.88Yes, you should buy the asset.Use an annuity factor to compute the value two years from today of the twenty payments. Remember, the annuity formula gives you the value of the stream one year before the first payment. Hence, the annuity factor will give you the value at the end of year two of the stream of payments.A= $2,000 (9.8181)Value at the end of year two = $2,000 20.008= $19,636.20The present value is simply that amount discounted back two years.PV = $19,636.20 / 1.082 = $16,834.88The easiest way to do this problem is to use the annuity factor. The annuity factor must be equal to $12,800 / $2,000 = 6.4; remember PV =C A T r. The annuity factors are in the appendix to the text. To use the factor table to solve this problem, scan across the row labeled 10 years until you find 6.4. It is close to the factor for 9%, 6.4177. Thus, the rate you will receive on this note is slightly more than 9%.You can find a more precise answer by interpolating between nine and ten percent.[ 10% ⎤[6.1446 ⎤a ⎡r ⎥bc ⎡6.4 ⎪ d⎣9%⎦⎣6.4177 ⎦By interpolating, you are presuming that the ratio of a to b is equal to the ratio of c to d.(9 - r ) / (9 - 10) = (6.4177 - 6.4 ) / (6.4177 - 6.1446)r = 9.0648%The exact value could be obtained by solving the annuity formula for the interest rate. Sophisticated calculators can compute the rate directly as 9.0626%.[Note: A standard financial calculator’s TVM keys can solve for this rate. With annuity flows, the IRR key on “advanced” financial c alculators is unnecessary.]a. The annuity amount can be computed by first calculating the PV of the $25,000 which youThat amount is $17,824.65 [= $25,000 / 1.075]. Next compute the annuity which has the same present value.A$17,824.65 = C 507.0$17,824.65 = C (4.1002)C = $4,347.26Thus, putting $4,347.26 into the 7% account each year will provide $25,000 five years from today.b. The lump sum payment must be the present value of the $25,000, i.e., $25,000 / 1.075 =$17,824.65The formula for future value of any annuity can be used to solve the problem (see footnote 11 of the text).Option one: This cash flow is an annuity due. To value it, you must use the after-tax amounts. Theafter-tax payment is $160,000 (1 - 0.28) = $115,200. Value all except the first payment using the standard annuity formula, then add back the first payment of $115,200 to obtain the value of this option.AValue = $115,200 + $115,200 30.010= $115,200 + $115,200 (9.4269)= $1,201,178.88Option two: This option is valued similarly. You are able to have $446,000 now; this is already on an after-tax basis. You will receive an annuity of $101,055 for each of the next thirty years. Those payments are taxable when you receive them, so your after-tax payment is $72,759.60 [= $101,055 (1 - 0.28)].AValue = $446,000 + $72,759.60 30.010= $446,000 + $72,759.60 (9.4269)= $1,131,897.47Since option one has a higher PV, you should choose it.et r be the rate of interest you must earn.$10,000(1 + r)12 = $80,000(1 + r)12= 8r = 0.18921 = 18.921%First compute the present value of all the payments you must make for your children’s educati on. The value as of one year before matriculation of one child’s education isA= $21,000 (2.8550) = $59,955.$21,000 415.0This is the value of the elder child’s education fourteen years from now. It is the value of the younger child’s education sixteen years from today. The present value of these isPV = $59,955 / 1.1514 + $59,955 / 1.1516= $14,880.44You want to make fifteen equal payments into an account that yields 15% so that the present value of the equal payments is $14,880.44.A= $14,880.44 / 5.8474 = $2,544.80Payment = $14,880.44 / 15.015This problem applies the growing annuity formula. The first payment is$50,000(1.04)2(0.02) = $1,081.60.PV = $1,081.60 [1 / (0.08 - 0.04) - {1 / (0.08 - 0.04)}{1.04 / 1.08}40]= $21,064.28This is the present value of the payments, so the value forty years from today is$21,064.28 (1.0840) = $457,611.46se the discount factors to discount the individual cash flows. Then compute the NPV of the project. NoticeYou can still use the factor tables to compute their PV. Essentially, they form cash flows that are a six year annuity less a two year annuity. Thus, the appropriate annuity factor to use with them is 2.6198 (= 4.3553 - 1.7355).Year Cash Flow Factor PV0.9091 $636.371$70020.8264 743.769003 1,000 ⎤4 1,000 ⎥ 2.6198 2,619.805 1,000 ⎥6 1,000 ⎦7 1,250 0.5132 641.508 1,375 0.4665 641.44Total $5,282.87NPV = -$5,000 + $5,282.87= $282.87Purchase the machine.Chapter 5: How to Value Bonds and StocksThe amount of the semi-annual interest payment is $40 (=$1,000 ⨯ 0.08 / 2). There are a total of 40 periods;i.e., two half years in each of the twenty years in the term to maturity. The annuity factor tables can be usedto price these bonds. The appropriate discount rate to use is the semi-annual rate. That rate is simply the annual rate divided by two. Thus, for part b the rate to be used is 5% and for part c is it 3%.A+F/(1+r)40PV=C Tra. $40 (19.7928) + $1,000 / 1.0440 = $1,000Notice that whenever the coupon rate and the market rate are the same, the bond is priced at par.b. $40 (17.1591) + $1,000 / 1.0540 = $828.41Notice that whenever the coupon rate is below the market rate, the bond is priced below par.c. $40 (23.1148) + $1,000 / 1.0340 = $1,231.15Notice that whenever the coupon rate is above the market rate, the bond is priced above par.a. The semi-annual interest rate is $60 / $1,000 = 0.06. Thus, the effective annual rate is 1.062 - 1 =0.1236 = 12.36%.A+ $1,000 / 1.0612b. Price = $30 12.006= $748.48A+ $1,000 / 1.0412c. Price = $30 1204.0= $906.15Note: In parts b and c we are implicitly assuming that the yield curve is flat. That is, the yield in year 5applies for year 6 as well.rice = $2 (0.72) / 1.15 + $4 (0.72) / 1.152 + $50 / 1.153= $36.31The number of shares you own = $100,000 / $36.31 = 2,754 sharesPrice = $1.15 (1.18) / 1.12 + $1.15 (1.182) / 1.122 + $1.152 (1.182) / 1.123+ {$1.152 (1.182)(1.06) / (0.12 - 0.06)} / 1.123= $26.95[Insert before last sentence of question: Assume that dividends are a fixed proportion of earnings.] Dividend one year from now = $5 (1 - 0.10) = $4.50Price = $5 + $4.50 / {0.14 - (-0.10)}= $23.75Since the current $5 dividend has not yet been paid, it is still included in the stock price.Chapter 6: Some Alternative Investment Rulesa. Payback period of Project A = 1 + ($7,500 - $4,000) / $3,500 = 2 yearsPayback period of Project B = 2 + ($5,000 - $2,500 -$1,200) / $3,000 = 2.43 yearsProject A should be chosen.b. NPV A = -$7,500 + $4,000 / 1.15 + $3,500 / 1.152 + $1,500 / 1.153 = -$388.96NPV B = -$5,000 + $2,500 / 1.15 + $1,200 / 1.152 + $3,000 / 1.153 = $53.83Project B should be chosen.a. Average Investment:($16,000 + $12,000 + $8,000 + $4,000 + 0) / 5 = $8,000Average accounting return:$4,500 / $8,000 = 0.5625 = 56.25%b. 1. AAR does not consider the timing of the cash flows, hence it does not consider the timevalue of money.2. AAR uses an arbitrary firm standard as the decision rule.3. AAR uses accounting data rather than net cash flows.aAverage Investment = (8000 + 4000 + 1500 + 0)/4 = 3375.00Average Net Income = 2000(1-0.75) = 1500=> AAR = 1500/3375=44.44%a. Solve x by trial and error:-$8,000 + $4,000 / (1 + x) + $3000 / (1 + x)2 + $2,000 / (1 + x)3 = 0x = 6.93%b. No, since the IRR (6.93%) is less than the discount rate of 8%.Alternatively, the NPV @ a discount rate of 0.08 = -$136.62.a. Solve r in the equation:$5,000 - $2,500 / (1 + r) - $2,000 / (1 + r)2 - $1,000 / (1 + r)3- $1,000 / (1 + r)4 = 0By trial and error,IRR = r = 13.99%b. Since this problem is the case of financing, accept the project if the IRR is less than the required rate of return.IRR = 13.99% > 10%Reject the offer.c. IRR = 13.99% < 20%Accept the offer.d. When r = 10%:NPV = $5,000 - $2,500 / 1.1 - $2,000 / 1.12 - $1,000 / 1.13 - $1,000 / 1.14When r = 20%:NPV = $5,000 - $2,500 / 1.2 - $2,000 / 1.22 - $1,000 / 1.23 - $1,000 / 1.24= $466.82Yes, they are consistent with the choices of the IRR rule since the signs of the cash flows change only once.A/ $160,000 = 1.04PI = $40,000 715.0Since the PI exceeds one accept the project.Chapter 7: Net Present Value and Capital BudgetingSince there is uncertainty surrounding the bonus payments, which McRae might receive, you must use the expected value of McRae’s bonuses in the computation of the PV of his contract. McRae’s salary plus the expected value of his bonuses in years one through three is$250,000 + 0.6 ⨯ $75,000 + 0.4 ⨯ $0 = $295,000.Thus the total PV of his three-year contract isPV = $400,000 + $295,000 [(1 - 1 / 1.12363) / 0.1236]+ {$125,000 / 1.12363} [(1 - 1 / 1.123610 / 0.1236]= $1,594,825.68EPS = $800,000 / 200,000 = $4NPVGO = (-$400,000 + $1,000,000) / 200,000 = $3Price = EPS / r + NPVGO= $4 / 0.12 + $3=$36.33Year 0 Year 1 Year 2 Year 3 Year 4 Year 51. Annual Salary$120,000 $120,000 $120,000 $120,000 $120,000 Savings2. Depreciation 100,000 160,000 96,000 57,600 57,6003. Taxable Income 20,000 -40,000 24,000 62,400 62,4004. Taxes 6,800 -13,600 8,160 21,216 21,2165. Operating Cash Flow113,200 133,600 111,840 98,784 98,784 (line 1-4)$100,000 -100,0006. ∆ Net workingcapital7. Investment $500,000 75,792*8. Total Cash Flow -$400,000 $113,200 $133,600 $111,840 $98,784 $74,576*75,792 = $100,000 - 0.34 ($100,000 - $28,800)NPV = -$400,000+ $113,200 / 1.12 + $133,600 / 1.122 + $111,840 / 1.123+ $98,784 / 1.124 + $74,576 / 1.125= -$7,722.52Real interest rate = (1.15 / 1.04) - 1 = 10.58%NPV A = -$40,000+ $20,000 / 1.1058 + $15,000 / 1.10582 + $15,000 / 1.10583= $1,446.76NPV B = -$50,000+ $10,000 / 1.15 + $20,000 / 1.152 + $40,000 / 1.153= $119.17Choose project A.PV = $120,000 / {0.11 - (-0.06)}t = 0 t = 1 t = 2 t = 3 t = 4 t = 5 t = 6 ...$12,000 $6,000 $6,000 $6,000$4,000$12,000 $6,000 $6,000 ...The present value of one cycle is:A+ $4,000 / 1.064PV = $12,000 + $6,000 306.0= $12,000 + $6,000 (2.6730) + $4,000 / 1.064= $31,206.37The cycle is four years long, so use a four year annuity factor to compute the equivalent annual cost (EAC).AEAC = $31,206.37 / 406.0= $31,206.37 / 3.4651= $9,006The present value of such a stream in perpetuity is$9,006 / 0.06 = $150,100o evaluate the word processors, compute their equivalent annual costs (EAC).BangAPV(costs) = (10 ⨯ $8,000) + (10 ⨯ $2,000) 414.0= $80,000 + $20,000 (2.9137)= $138,274EAC = $138,274 / 2.9137= $47,456IOUAPV(costs) = (11 ⨯ $5,000) + (11 ⨯ $2,500) 3.014- (11 ⨯ $500) / 1.143= $55,000 + $27,500 (2.3216) - $5,500 / 1.143= $115,132EAC = $115,132 / 2.3216= $49,592BYO should purchase the Bang word processors.Chapter 8: Strategy and Analysis in Using Net Present ValueThe accounting break-even= (120,000 + 20,000) / (1,500 - 1,100)= 350 units. The accounting break-even= 340,000 / (2.00 - 0.72)= 265,625 abalonesb. [($2.00 ⨯ 300,000) - (340,000 + 0.72 ⨯ 300,000)] (0.65)= $28,600This is the after tax profit.Chapter 9: Capital Market Theory: An Overviewa. Capital gains = $38 - $37 = $1 per shareb. Total dollar returns = Dividends + Capital Gains = $1,000 + ($1*500) = $1,500 On a per share basis, this calculation is $2 + $1 = $3 per sharec. On a per share basis, $3/$37 = 0.0811 = 8.11% On a total dollar basis, $1,500/(500*$37) = 0.0811 = 8.11%d. No, you do not need to sell the shares to include the capital gains in the computation of the returns. The capital gain is included whether or not you realize the gain. Since you could realize the gain if you choose, you should include it.The expected holding period return is:()[]%865.1515865.052$/52$75.54$50.5$==-+There appears to be a lack of clarity about the meaning of holding period returns. The method used in the answer to this question is the one used in Section 9.1. However, the correspondence is not exact, because in this question, unlike Section 9.1, there are cash flows within the holding period. The answer above ignores the dividend paid in the first year. Although the answer above technically conforms to the eqn at the bottom of Fig. 9.2, the presence of intermediate cash flows that aren’t accounted for renders th is measure questionable, at best. There is no similar example in the body of the text, and I have never seen holding period returns calculated in this way before.Although not discussed in this book, there are two generally accepted methods of computing holding period returns in the presence of intermediate cash flows. First, the time weighted return calculates averages (geometric or arithmetic) of returns between cash flows. Unfortunately, that method can’t be used here, because we are not given the va lue of the stock at the end of year one. Second, the dollar weighted measure calculates the internal rate of return over the entire holding period. Theoretically, that method can be applied here, as follows: 0 = -52 + 5.50/(1+r) + 60.25/(1+r)2 => r = 0.1306.This produces a two year holding period return of (1.1306)2 – 1 = 0.2782. Unfortunately, this book does not teach the dollar weighted method.In order to salvage this question in a financially meaningful way, you would need the value of the stock at the end of one year. Then an illustration of the correct use of the time-weighted return would be appropriate. A complicating factor is that, while Section 9.2 illustrates the holding period return using the geometric return for historical data, the arithmetic return is more appropriate for expected future returns.E(R) = T-Bill rate + Average Excess Return = 6.2% + (13.0% -3.8%) = 15.4%. Common Treasury Realized Stocks Bills Risk Premium -7 32.4% 11.2% 21.2%-6 -4.9 14.7 -19.6-5 21.4 10.5 10.9 -4 22.5 8.8 13.7 -3 6.3 9.9 -3.6 -2 32.2 7.7 24.5 Last 18.5 6.2 12.3 b. The average risk premium is 8.49%.49.873.125.246.37.139.106.192.21=++-++- c. Yes, it is possible for the observed risk premium to be negative. This can happen in any single year. The.b.Standard deviation = 03311.0001096.0=.b.Standard deviation = = 0.03137 = 3.137%.b.Chapter 10: Return and Risk: The Capital-Asset-Pricing Model (CAPM)a. = 0.1 (– 4.5%) + 0.2 (4.4%) + 0.5 (12.0%) + 0.2 (20.7%) = 10.57%b.σ2 = 0.1 (–0.045 – 0.1057)2 + 0.2 (0.044 – 0.1057)2 + 0.5 (0.12 – 0.1057)2+ 0.2 (0.207 – 0.1057)2 = 0.0052σ = (0.0052)1/2 = 0.072 = 7.20%Holdings of Atlas stock = 120 ⨯ $50 = $6,000 ⨯ $20 = $3,000Weight of Atlas stock = $6,000 / $9,000 = 2 / 3Weight of Babcock stock = $3,000 / $9,000 = 1 / 3a. = 0.3 (0.12) + 0.7 (0.18) = 0.162 = 16.2%σP 2= 0.32 (0.09)2 + 0.72 (0.25)2 + 2 (0.3) (0.7) (0.09) (0.25) (0.2)= 0.033244σP= (0.033244)1/2 = 0.1823 = 18.23%a.State Return on A Return on B Probability1 15% 35% 0.4 ⨯ 0.5 = 0.22 15% -5% 0.4 ⨯ 0.5 = 0.23 10% 35% 0.6 ⨯ 0.5 = 0.34 10% -5% 0.6 ⨯ 0.5 = 0.3b. = 0.2 [0.5 (0.15) + 0.5 (0.35)] + 0.2[0.5 (0.15) + 0.5 (-0.05)]+ 0.3 [0.5 (0.10) + 0.5 (0.35)] + 0.3 [0.5 (0.10) + 0.5 (-0.05)]= 0.135= 13.5%Note: The solution to this problem requires calculus.Specifically, the solution is found by minimizing a function subject to a constraint. Calculus ability is not necessary to understand the principles behind a minimum variance portfolio.Min { X A2 σA2 + X B2σB2+ 2 X A X B Cov(R A , R B)}subject to X A + X B = 1Let X A = 1 - X B. Then,Min {(1 - X B)2σA2 + X B2σB2+ 2(1 - X B) X B Cov (R A, R B)}Take a derivative with respect to X B.d{∙} / dX B = (2 X B - 2) σA2+ 2 X B σB2 + 2 Cov(R A, R B) - 4 X B Cov(R A, R B)Set the derivative equal to zero, cancel the common 2 and solve for X B.X BσA2- σA2+ X B σB2 + Cov(R A, R B) - 2 X B Cov(R A, R B) = 0X B = {σA2 - Cov(R A, R B)} / {σA2+ σB2 - 2 Cov(R A, R B)}andX A = {σB2 - Cov(R A, R B)} / {σA2+ σB2 - 2 Cov(R A, R B)}Using the data from the problem yields,X A = 0.8125 andX B = 0.1875.a. Using the weights calculated above, the expected return on the minimum variance portfolio isE(R P) = 0.8125 E(R A) + 0.1875 E(R B)= 0.8125 (5%) + 0.1875 (10%)= 5.9375%b. Using the formula derived above, the weights areX A = 2 / 3 andX B = 1 / 3c. The variance of this portfolio is zero.σP 2= X A2 σA2 + X B2σB2+ 2 X A X B Cov(R A , R B)= (4 / 9) (0.01) + (1 / 9) (0.04) + 2 (2 / 3) (1 / 3) (-0.02)= 0This demonstrates that assets can be combined to form a risk-free portfolio.14.2%= 3.7%+β(7.5%) ⇒β = 1.40.25 = R f + 1.4 [R M– R f] (I)0.14 = R f + 0.7 [R M– R f] (II)(I) – (II)=0.11 = 0.7 [R M– R f] (III)[R M– R f ]= 0.1571Put (III) into (I) 0.25 = R f + 1.4[0.1571]R f = 3%[R M– R f ]= 0.1571R M = 0.1571 + 0.03= 18.71%a. = 4.9% + βi (9.4%)βD= Cov(R D, R M) / σM 2 = 0.0635 / 0.04326 = 1.468= 4.9 + 1.468 (9.4) = 18.70%Weights:X A = 5 / 30 = 0.1667X B = 10 / 30 = 0.3333X C = 8 / 30 = 0.2667X D = 1 - X A - X B - X C = 0.2333Beta of portfolio= 0.1667 (0.75) + 0.3333 (1.10) + 0.2667 (1.36) + 0.2333 (1.88)= 1.293= 4 + 1.293 (15 - 4) = 18.22%a. (i) βA= ρA,MσA / σMρA,M= βA σM / σA= (0.9) (0.10) / 0.12= 0.75(ii) σB= βB σM / ρB,M= (1.10) (0.10) / 0.40= 0.275(iii) βC= ρC,MσC / σM= (0.75) (0.24) / 0.10= 1.80(iv) ρM,M= 1(v) βM= 1(vi) σf= 0(vii) ρf,M= 0(viii) βf= 0b. SML:E(R i) = R f + βi {E(R M) - R f}= 0.05 + (0.10) βiSecurity βi E(R i)A 0.13 0.90 0.14B 0.16 1.10 0.16C 0.25 1.80 0.23Security A performed worse than the market, while security C performed better than the market.Security B is fairly priced.c. According to the SML, security A is overpriced while security C is under-priced. Thus, you could invest in security C while sell security A (if you currently hold it).a. The typical risk-averse investor seeks high returns and low risks. To assess thetwo stocks, find theReturns:State of economy ProbabilityReturn on A*Recession 0.1 -0.20 Normal 0.8 0.10 Expansion0.10.20* Since security A pays no dividend, the return on A is simply (P 1 / P 0) - 1. = 0.1 (-0.20) + 0.8 (0.10) + 0.1 (0.20) = 0.08 = 0.09 This was given in the problem.Risk:R A - (R A -)2 P ⨯ (R A -)2 -0.28 0.0784 0.00784 0.02 0.0004 0.00032 0.12 0.0144 0.00144 Variance 0.00960Standard deviation (R A ) = 0.0980βA = {Corr(R A , R M ) σ(R A )} / σ(R M ) = 0.8 (0.0980) / 0.10= 0.784βB = {Corr(R B , R M ) σ(R B )} / σ(R M ) = 0.2 (0.12) / 0.10= 0.24The return on stock B is higher than the return on stock A. The risk of stock B, as measured by itsbeta, is lower than the risk of A. Thus, a typical risk-averse investor will prefer stock B.b. = (0.7) + (0.3) = (0.7) (0.8) + (0.3) (0.09) = 0.083σP 2= 0.72 σA 2 + 0.32 σB 2 + 2 (0.7) (0.3) Corr (R A , R B ) σA σB = (0.49) (0.0096) + (0.09) (0.0144) + (0.42) (0.6) (0.0980) (0.12) = 0.0089635 σP = = 0.0947 c. The beta of a portfolio is the weighted average of the betas of the components of the portfolio. βP = (0.7) βA + (0.3) βB = (0.7) (0.784) + (0.3) (0.240) = 0.621Chapter 11:An Alternative View of Risk and Return: The Arbitrage Pricing Theorya. Stock A:()()R R R R R A A A m m Am A=+-+=+-+βεε105%12142%...Stock B:()()R R R R R B B m m Bm B=+-+=+-+βεε130%098142%...Stock C:()R R R R R C C C m m Cm C=+-+=+-+βεε157%137142%)..(.b.()[]()[]()[]()()()()()()[]()()CB A m cB A m c m B m A m CB A P 25.045.030.0%2.14R 1435.1%925.1225.045.030.0%2.14R 37.125.098.045.02.130.0%7.1525.0%1345.0%5.1030.0%2.14R 37.1%7.1525.0%2.14R 98.0%0.1345.0%2.14R 2.1%5.1030.0R 25.0R 45.0R 30.0R ε+ε+ε+-+=ε+ε+ε+-+++++=ε+-++ε+-++ε+-+=++= c.i.()R R R A B C =+-==+-==+-=105%1215%142%)1113%09815%142%)137%157%13715%142%168%..(..46%.(......ii.R P =+-=12925%1143515%142%)138398%..(..To determine which investment investor would prefer, you must compute the variance of portfolios created bymany stocks from either market. Note, because you know that diversification is good, it is reasonable to assume that once an investor chose the market in which he or she will invest, he or she will buy many stocks in that market.Known:E EF ====001002 and and for all i.i σσεε..Assume: The weight of each stock is 1/N; that is, X N i =1/for all i.If a portfolio is composed of N stocks each forming 1/N proportion of the portfolio, the return on the portfolio is 1/N times the sum of the returns on the N stocks. Recall that the return on each stock is 0.1+βF+ε.()()()()()()[]()()()()()()()[]()[]()[]()()[]()()()()()j i 2j i 22j i i 2222222222P P P P iP ,0.04Corr 0.01,Cov s =isvariance the ,N as limit In the ,Cov 1/N 1s 1/N s )(1/N 1/N F 2F E 1/N F E 0.10.1/N F 0.1E R E R E R Var 0.101/N 00.1E 1/N F E 0.11/N F 0.1E R E 1/N F 0.1F 0.1(1/N)R 1/N R εε+β=εε+β∞⇒εε-+ε+β=ε∑+εβ+β=ε+β=-ε+β+=-==+β+=ε+β+=ε∑+β+=ε+β+=ε+β+==∑∑∑∑∑∑∑∑()()()()()()Thus,F R f E R E R Var R Corr Var R Corr ii ip P p i j PijR 1i =++=++===+=+010*********002250040002500412212111222.........,,εεεεεεa.()()()()Corr Corr Var R Var R i j i j p pεεεε112212000225000225,,..====Since Var ()()R p 1 Var R 2p 〉, a risk averse investor will prefer to invest in the second market.b. Corr ()()εεεε112090i j j ,.,== and Corr 2i()()Var R Var R pp120058500025==..。

Chapter 29Mergers and Acquisitions Multiple Choice Questions1. In a merger or acquisition, a firm should be acquired if itA) generates a positive net present value to the shareholders of an acquiring firm.B) is a firm in the same line of business, in which the acquirer has expertise.C) is a firm in a totally different line of business which will diversity the firm.D) pays a large dividend which will provide cash pass through to the acquiror.E) None of the above.Answer: A Difficulty: Easy Page: 7962. A reason for acquisitions is synergy. Synergy includesA) revenue enhancements.B) cost reductions.C) lower taxes.D) All of the above.E) None of the above.Answer: D Difficulty: Medium Page: 7963. One company wishes to acquire another. Which of the following forms of acquisition does notrequire a formal vote by the shareholders of the acquired firm?A) MergerB) Acquisition of stockC) Acquisition of assetsD) ConsolidationE) All of the above require a formal vote.Answer: B Difficulty: Easy Page: 797-7984. Firm A and Firm B merge to create Firm AB. This is an example ofA) a tender offer.B) an acquisition of assets.C) an acquisition of stock.D) a consolidation.E) Both B and C.Answer: D Difficulty: Easy Page: 7975. Dissatisfied shareholders of the acquired firm in a merger canA) decide not to tender their shares.B) exercise their appraisal rights and demand their shares be purchased at fair value by theacquiring firm.C) decide not to vote for the current management by proxy.D) do nothing and are stuck with the outcome.E) Any of the above.Answer: B Difficulty: Medium Page: 7976. Which of the following is not true of mergers?A) Mergers are legally straightforward.B) Mergers must be approved by a vote of the stockholders of each firm.C) In a merger, the acquiring firm retains its name and identity.D) Mergers represent a public offer to buy shares directly from the stockholders of another firm.E) All of the above are true of mergers.Answer: D Difficulty: Medium Page: 7977. The complete absorption of one firm by another is called aA) merger.B) consolidation.C) oligopolistic agreement.D) All of the above.E) None of the above.Answer: A Difficulty: Easy Page: 7978. The acquisition of stock has the advantage ofA) no shareholder meeting to vote is necessary.B) minority shareholders may exist.C) opening the bidding to others.D) All of the above.E) None of the above.Answer: A Difficulty: Hard Page: 7989. Suppose that Verizon and Sprint were to merge. Ignoring potential antitrust problems, this mergerwould be classified as aA) horizontal merger.B) vertical merger.C) conglomerate merger.D) monopolistic merger.E) None of the above.Answer: A Difficulty: Easy Page: 79810. Suppose that General Motors has made an offer to acquire General Mills. Ignoring potentialantitrust problems, this merger would be classified as aA) monopolistic merger.B) horizontal merger.C) vertical merger.D) conglomerate merger.E) None of the above.Answer: D Difficulty: Easy Page: 79811. Suppose that Exxon-Mobil acquired Schlumberger, an exploration/drilling company. Ignoringpotential antitrust problems, this merger would be classified as aA) monopolistic merger.B) vertical merger.C) conglomerate merger.D) horizontal merger.E) None of the above.Answer: B Difficulty: Easy Page: 79812. Which of the following factors influence the choice between merger and an acquisition of stock?A) Shareholders are dealt with directly to bypass target management and board of directors.B) In a tender offer, usually some minority shareholders do not tender stopping complete firmabsorption.C) Target management may be unfriendly and resist an offer which usually moves the stock priceup.D) All of the above.E) None of the above.Answer: D Difficulty: Hard Page: 79813. A dissident group solicits votes in an attempt to replace existing management. This is called aA) tender offer.B) shareholder derivative action.C) proxy fight or proxy contest.D) management freeze-out.E) shareholder's revenge.Answer: C Difficulty: Easy Page: 79914. If the All-Star Fuel Filling Company, a chain of gasoline stations acquire the Mid-States RefiningCompany, a refiner of oil products, this would be an example of aA) conglomerate acquisition.B) white knight.C) vertical acquisition.D) going-private transaction.E) horizontal acquisition.Answer: C Difficulty: Medium Page: 79815. Which of the following is not true of an acquisition of stock or tender offers?A) No stockholder meetings need to be held.B) No vote is required.C) The bidding firm deals directly with the stockholders of the target firm.D) In most cases, 100% of the stock of the target firm is tendered.E) All of the above are true of tender offers.Answer: D Difficulty: Easy Page: 79816. When the management and/or a small group of investors take over a firm and the shares of the firmare delisted and no longer publicly available, this action is known as aA) consolidation.B) vertical acquisition.C) proxy contest.D) going-private transaction.E) None of the above.Answer: D Difficulty: Easy Page: 79917. Following an acquisition, the assets of the acquired firm to be reported at the fair market value onthe books of the acquiring firm. What form of merger accounting is being used?A) consolidationB) aggregationC) purchaseD) poolingE) None of the aboveAnswer: C Difficulty: Easy Page: 80118. Following an acquisition, the acquiring firm's balance sheet shows an asset labeled "goodwill."What form of merger accounting is being used?A) consolidationB) aggregationC) purchaseD) poolingE) None of the aboveAnswer: C Difficulty: Easy Page: 80119. Synergy occurs when theA) added value is positive from the combination.B) sum of the parts is equal to the whole.C) premium paid to the acquired shareholders equals the NPVD) standstill agreement is effected.E) All of the above.Answer: A Difficulty: Easy Page: 80220. Goodwill from the purchase of another firm isA) adjusted annually on the Statement of Retained Earnings.B) adjusted annually on the Balance Sheet.C) adjusted monthly on the Balance Sheet.D) All of the above.E) None of the above.Answer: B Difficulty: Medium Page: 80121. The DAB Corporation with a book value of $20 million and a market value of $30 million hasmerged with the CLC Corporation with a book value of $6 million and a market value of $8 million at a price of $9 million. If the transaction is a purchase then the total assets on the books of the new company will beA) $26 millionB) $29 millionC) $38 millionD) $39 millionE) None of the above.Answer: D Difficulty: Hard Page: 801Rationale:New Purchase Book Value = MV(DAB) + MV(CLC) + Goodwill = $30 million + $8 million + $1 million = $39 million.22. The DAB Corporation with a book value of $20 million and a market value of $30 million hasmerged with the CLC Corporation with a book value of $6 million and a market value of $8 million at a price of $9 million. If the transaction is a purchase will there be any goodwill and if so what is the amount of goodwill?A) No, goodwill is $0B) Yes, goodwill is $3 millionC) Yes, goodwill is $1 millionD) Can not be calculated with the information given.E) None of the above.Answer: C Difficulty: Hard Page: 801Rationale:Goodwill = $9,000,000 - $8,000,000 = $1,000,00023. The synergy of an acquisition between Firm A and Firm B can be determined byA) subtracting the change in cost from the change in revenue.B) subtracting the change in taxes form the change in revenue.C) subtracting the change in capital requirements from the change in revenues.D) discounting the change in the cash flows of the combined firm by the risk adjusted discountrate.E) discounting the change in the revenues of the combined firm by the risk adjusted discount rate.Answer: D Difficulty: Medium Page: 80224. The value of synergy is estimated by the equation:A) V A + V B - ∆RevenueB) V AB– (V A + V B )C) V AB - V B– TaxesD) V A - V B - ∆CostsE) None of the above.Answer: B Difficulty: Medium Page: 80225. An important reason for acquisitions is that the combined firm may generate greater revenue thatthe two separate firms could. An example of revenue enhancement would not include anelimination of aA) previously ineffective media effort.B) previously ineffective advertising effort.C) weak existing distribution effort.D) decrease in cost.E) All of the above would be examples of revenue enhancement.Answer: D Difficulty: Medium Page: 802-80326. An acquisition may take place because of a real or perceived strategic advantage. An example of astrategic advantage would beA) an aircraft manufacturer buying a laser guidance company for possible advanced flight controlwithout pilots.B) a manufacturer integrating their supply by acquiring downline.C) a corporation completing a spin-off.D) a corporation out-sourcing to achieve cost economies.E) None of the above.Answer: A Difficulty: Hard Page: 80327. Which of the following is not true regarding monopoly power as it relates to acquisitions thatreduce competition?A) The U.S. Justice Department may challenge a merger if it is not determined to benefit society.B) The Federal Trade Commission may challenge a merger if it is not determined to benefitsociety.C) If monopoly power is measured through an acquisition, all firms in an industry should benefitas the industry's price is increased.D) Prices and profits will always decrease and can never increase because of the reduction incompetition.E) All of the above are true regarding monopoly power and mergers.Answer: D Difficulty: Medium Page: 80328. A merger that improves the use of one company's design team and the other company's testinggroup is evidence ofA) replacement of inefficient management.B) one company exercising monopoly power.C) complementary resources.D) minimizing the net operating losses.E) None of the above.Answer: C Difficulty: Easy Page: 80429. The market for corporate control is a phrase that would not describeA) a shift in management motivated to increase the value of the firm.B) top management restructuring of the company.C) an elimination of managerial inefficiency.D) the system where corporate insiders trade personal stock holdings.E) alternative management teams competing for the rights to management corporate activities.Answer: D Difficulty: Easy Page: 80530. Tax gains can result from the use of _____ in an acquisition.A) net operating lossesB) unused debt capacityC) surplus fundsD) All of the above.E) None of the above.Answer: D Difficulty: Medium Page: 80531. The Albatross Company has accumulated net operating losses of $70 million and is likely to enterbankruptcy. The Zephyr Company has earnings of $200 million and is in the 36% marginal tax bracket. Zephyr is considering buying Albatross and liquidating the company and retaining a few of the assets. What is the minimum tax shield value of Albatross to Zephyr?A) $25.2 millionB) $70.0 millionC) $72.0 millionD) Not enough information to calculate.E) None of the above.Answer: A Difficulty: Medium Page: 805Rationale:Minimum value from tax shield = $70,000,000 (.36) = $25,200,00032. One of the most basic reasons for a merger isA) revenue enhancing in the hopes that net capital losses may decrease.B) monopoly power.C) strategic benefits.D) cost reductions.E) to keep lawyers and accountants employed.Answer: D Difficulty: Easy Page: 80333. A corporation with surplus cash flows may use the cash flows toA) pay dividends.B) repurchase shares.C) buy shares in another firm.D) All of the above.E) None of the above.Answer: D Difficulty: Easy Page: 80634. Cowboy Curtiss' Cowboy Hat Company recently completed a merger. When valuing the combinedfirm after the merger, which of the following is an example of the type of common mistake that can occur?A) The use of market values in valuing either the new firm.B) The inclusion of cash flows that are incremental to the decision.C) The use of Curtiss' discount rate when valuing the cash flows of the entire company.D) The inclusion of all relevant transactions cost associated with the acquisition.E) None of the above.Answer: C Difficulty: Medium Page: 80835. Firm A is going to acquire Firm B by selling bonds and using the proceeds to purchase (for cash)the stock of Firm B. What is the appropriate discount rate for use in valuing the benefits of the merger?A) Firm A's cost of debt.B) Firm A's weighted average cost of capital.C) Firm A's cost of equity.D) Firm B's weighted average cost of capital.E) None of the above.Answer: E Difficulty: Medium Page: 80836. When two firms merge and there is no synergy gain but the only change is a reduction in riskA) there is no effect on the bondholders or stockholders.B) both the bondholders and stockholders are made better off.C) the bondholders gain in value while the stockholders lose value.D) the stockholders gain in value while the bondholders lose value.E) None of the above.Answer: C Difficulty: Medium Page: 80937. If two leveraged firms merge, the cost of debt for the new firm will generally be lower than it wasfor the two firms as separate entities. One reason for this isA) strategic fits.B) net operating losses.C) surplus funds.D) co-insurance.E) None of the above.Answer: D Difficulty: Easy Page: 81038. Two firms merge and no synergies occur. Which of the following is true?A) The reduction in risk in the combined firm benefits the bondholders at the expense of thestockholders.B) The value of the debt in the combined firm will likely be greater that the value of the debt in thetwo separate firms.C) The size of the gain to the bondholders depends on the specific reductions in bankruptcy statesafter the merger.D) The bondholders' gain can be described as the co insurance effect.E) All of the above are true.Answer: E Difficulty: Medium Page: 808-81039. Two all-equity firms with the same number of shares outstanding and EPS combine in anon-synergistic merger. The acquiring firm has a P/E of 6 while the acquired firm has a P/E of 10.The combined firm has an equal equity proportion from each of the original firms. Which of the following is correct?A) The new P/E will be 8 and the original firm shares will be more valuable.B) The transaction has provided more value to the acquiring firm and has caused it to grow.C) The P/E will be 8 and the relative value of the original shares will be unchanged.D) All of the above.E) None of the above.Answer: C Difficulty: Hard Page: 80940. Firm V was worth $450 and Firm A had a market value of $375. Firm V acquired Firm A for $425because they thought the combination of the new Firm VA was worth $925. What is the synergy from the merger of Firm V and Firm A?A) $ 50B) $100C) $475D) $500E) None of the above.Answer: B Difficulty: Medium Page: 802Rationale:V AB (V A + V B ) = $925 ($450 + $375) = $10041. Firm V was worth $450 and Firm A had a market value of $375. Firm V acquired Firm A for $425because they thought the combination of the new Firm VA was worth $925. What is the NPV from the merger of Firm V and Firm A?A) $ 0B) $ 50C) $425D) $450E) None of the above.Answer: B Difficulty: Medium Page: 813Rationale:V AB (V A + V B ) - Premium = $925 $450 $375 ($425-$375) = $5042. Firm V is worth $450 and has 100 shares outstanding. Firm A has a market value of $375 and has40 shares outstanding. Firm V to acquire Firm A will swap 80 shares of Firm V for the 40 shares ofFirm A. Firm V believes the combination of the new Firm VA was worth $925. What is the cost of acquiring Firm A if the Firm V and Firm A merge?A) $ 0.00B) $ 36.11C) $100.00D) $325.25E) None of the above.Answer: B Difficulty: Hard Page: 814-815Rationale:$925 (80/180) $375 = $411.11 $375 = $36.1143. Firm V is worth $450 and has 100 shares outstanding. Firm A has a market value of $375 and has40 shares outstanding. In order for Firm V to acquire Firm A, Firm A will swap 80 shares of FirmV for the 40 shares of Firm VA. Firm V believes the combination of the new Firm VA was worth $925. What is the market value exchange ratio of Firm V acquiring Firm A in a merger?A) 1:1B) 1.10:1C) 1.20:1D) 1.37:1E) None of the above.Answer: D Difficulty: Medium Page: 814-815Rationale:$925 /180 = 5.14 ; 2(5.14) / 1(7.50) = 10.28/ 7.5 = 1.3744. In a merger with an exchange of stock, when the premerger prices are used to calculate theexchange ratio. The true cost of the mergerA) is less than the number of shares received times the original market price.B) is equal to the number of shares received times the original market price.C) is greater than the number of shares received times the original market price.D) Unchanged from the premerger value.E) None of the above.Answer: C Difficulty: Medium Page: 81545. Which of the following is a factor in determining whether to finance an acquisition by cash or byshares of stock?A) TaxesB) Sharing gainsC) OvervaluationD) All of the above.E) None of the above.Answer: D Difficulty: Easy Page: 81546. A bear hug is an unfriendly takeover thatA) is so attractive that the target firm's management has little choice but to accept it.B) is the rescue of a target firm by a white knight.C) is made so unattractive, the bidder would not want to complete the deal.D) is financed with junk bonds.E) when the target sells their best assets to avoid an unfriendly takeover.Answer: A Difficulty: Medium Page: 81847. Firm A does well in a boom economy. Firm B does well in a bust economy. The probability of aboom is 50%. The end of period values of the two firms depend on the economy as shown below: Economy Probability Value of A Value of BBoom .5 $1,600 $ 800Bust .5 800 2,000Expected Value $1,200 $ 1,400Both firms have debt outstanding with a face value of $1,000. In order to diversify, the two firms have proposed a merger. The NPV of the merger is zero. Which of the following statements is correct?A) The stockholders are indifferent to merger since the NPV is zero.B) The bondholders are indifferent to merger since the NPV is zero.C) The bondholders stand to gain because the risk of the combined firm is less.D) The stockholders stand to gain because the probability of bankruptcy becomes zero after themerger.E) More than one of the above is correct.Answer: C Difficulty: Medium Page: 832Rationale:Boom BustV AB$2,400 $2,800Required Payment 2,000 2,000Residual $ 400 $ 800Original A debtholders would not get paid in a Bust and B debtholders would not get paid in a Boom. Now, both will always get paid.48. Shareholders in the acquiring firm can have the co-insurance effect reduced byA) selling more debt just before the merger to become more risky.B) retire old debt before the merger announcement and raise an equal amount of debt after themerger.C) after the merger raise more new debt to gain from the interest tax shield and increase risk.D) Both A and B.E) Both B and C.Answer: E Difficulty: Hard Page: 81049. A merger should not take place simply for the purpose ofA) diversification if shareholders can accomplish the same result on there own portfolios.B) increasing the debt capacity for the tax shield gain.C) acquiring free cash flow to be put to use by the acquirer.D) reducing the cost of production.E) None of the above.Answer: A Difficulty: Easy Page: 811-812Use the following to answer questions 50-51:Firm A Firm B Firm ABPrice per share $ 100 $ 15Total earnings 500 $300Shares outstanding 100 30Total Value $10,000 $450 $11,000Firm A has proposed to acquire Firm B at a price of $20 per share for Firm B's stock. The NPV of the merger has been estimated at $400.50. What is the synergy of the merger?A) $ 150B) $ 550C) $ 600D) $ 700E) $10,000Answer: B Difficulty: Medium Page: 802Rationale:Synergy: V AB - [V A + V B] = $11,000 + $450) = $55051. What will be the post-merger price per share for Firm A's stock if Firm A pays in cash?A) $104B) $108C) $110D) $114E) None of the above.Answer: A Difficulty: Hard Page: 812-814Rationale:Net V AB = V AB - Cash Paid = $11,000 - [($20)($30)] = $10,400Price/share = $10,400/100 = $104Alternative calculation: Price = $10,000 + $400 = $10,400/100 = $10452. Which of the following is not a defensive tactic in acquisition battles?A) Shark repellantB) White knightC) Poison pillD) Tiger teethE) Bear hugAnswer: D Difficulty: Easy Page: 81853. A modification to the corporate charter that requires 80% shareholder approval for a takeover iscalled a(n)A) repurchase standstill provision.B) exclusionary self-tender.C) super majority amendment.D) tender offer.E) None of the above.Answer: C Difficulty: Easy Page: 81654. Which of the following is the opposite of a targeted repurchase?A) Repurchase standstill provisionB) Exclusionary self-tenderC) Super majority amendmentD) Tender offerE) None of the above.Answer: B Difficulty: Easy Page: 81755. Which of the following defensive tactics completely eliminates the possibility of a takeover viatender offer?A) Leveraged buyout (LBO)B) Exclusionary self-tenderC) Targeted repurchaseD) Super majority amendmentE) None of the above.Answer: A Difficulty: Easy Page: 817-81856. Compensation paid to top management in the event of a takeover is called aA) poison pill.B) golden parachute.C) self-tender.D) buyout.E) None of the above.Answer: B Difficulty: Easy Page: 81857. As a defensive maneuver, a firm sells major assets to ward off an unfriendly takeover. This is anexample ofA) greenmail.B) a "scorched earth" policy.C) a poison pill.D) crown jewels.E) Both B and D.Answer: E Difficulty: Medium Page: 81858. Concerning the evidence on the benefits and costs of mergers, which of the following statements isnot correct?A) Shareholders in target firms that are acquired benefit substantially.B) The shareholders of bidding firms benefit substantially in successful takeovers.C) The shareholders in target firms that are not acquired benefit substantially.D) Two of the above are not correct.E) All of the above are not correct.Answer: A Difficulty: Medium Page: 820-82159. Large business combinations in Japan are normally carried out through reciprocal ownership ofcommon stock. These networks, or keiretsu, involve a large number of diversified companiescentered around a large bank, industrial firm or trading firm. One of the main benefits of thisstructure is argued to be:A) the monopolistic control of economic segments.B) the reduction of financial distress costs due to ease of restructuring an agreement.C) large scale diversification that cannot be done by individual shareholders.D) greater efficiency in management because the management skills are homogeneous even fordiversified industries.E) None of the above.Answer: B Difficulty: Medium Page: 823Essay Questions60. Firm A does well in a boom economy. Firm B does well in a bust economy. The probability of aboom is 50%. The end of period values of the two firms depend on the economy as shown below: Economy Probability Value of A Value of BBoom .5 $1,600 $ 800Bust .5 800 2,000Expected Value $1,200 $1,400Both firms have debt outstanding with a face value of $1,000. In order to diversify, the two firms have proposed a merger. The NPV of the merger is zero. Determine the gain or loss under each state of economy for the stockholders of A and B separately and for the combined firm AB. Should either the stockholders or bondholders be willing to support the merger? Support with numericalDifficulty: Medium Page: 808-810Answer:Payoff to Shareholders: Boom BustA $1,600–$1,000=$600 $800 – $800 =$ 0B $800 – $800 =$ 0 $2,000–$1,000=$1,000AB $2,400–$2,000=$400 $2,800–$2,000=$ 800 Loss to shareholders: Firm A =$200 Firm B = $ 200Neither shareholders will want to support the merger but bondholders would as their risk is lower and potential gain under a bust is $200.61. Chucky Chester Inc. takes over Billy Bob Burgers from Billy himself for $1 million in cold cash.Billy started the company years ago on an investment of $50,000 in plant and equipment which has long been paid off. The machinery has no accounting value today. Consider the takeover price as fair market value for the equipment. Calculate the tax consequences of the merger, assuming that Chucky Chester decides not to write-up the machinery. Both Billy and Chucky are in the 28% tax bracket.Difficulty: Medium Page: 799-801Answer:Billy Bob: Taxable income = $1,000,000 – $50,000 = $950,000Taxes paid = $ 950,000 (.28) = $266,000After-tax cash flow = $1,000,000 – $266,000 = $734,000 Chucky Chester: Does not recognize any additional taxable income and thedepreciation remains at zero.62. Uncle Fester's Umbrella Company expects taxable income of $250 if State 1 occurs (lots of rain,probability of .4), and -$60 if State two occurs (lots of sunshine, probability of .6). Suzy Suntan expects taxable income of -$200 if State 1 occurs, but $90 if State 2 occurs. Both firms are in the 31% tax bracket. Calculate the IRS's expected total tax collections of the two firms both separately and as one merged firm.Difficulty: Medium Page: 801Answer:Fester Suzy Fester and SuzyState 1 State 2 State 1 State 2 State 1 State 2 Tax Income $250.0 $-60 $-200 $ 90.0 $ 50.0 $30.0Tax 77.5 0 0 27.9 15.5 9.3Net Income $172.5 $-60 $-200 $62.1 $34.5 $ 20.7Total Tax Bill of Separates = (.40) ($77.5) + (.60) (27.9) = $47.74Total Taxes Paid by Merged = (.40) ($15.5) + (.60) ($9.3) = $11.78The expected taxes drop dramatically for the merged firm.63. Firms A and B, both of which are 100% equity, are going to merge. Before the merger, Firm A (100shares outstanding) is worth $15,000. Firm B (50 shares outstanding) is worth $10,000. Thecombined firm is worth $30,000. Firm A will pay $11,500 in cash for Firm B. What is the NPV of the merger to Firm A?Difficulty: Medium Page: 802Answer:Synergy = $30,000 – $15,000 – $10,000 = $5,000NPV = Synergy - Premium = $5,000 – $1,500 = $3,500.Value of Firm A after the acquisition: $30,000 – $11,500 = $18,500NPV to Firm A = $18,500 – $15,000 = $3,500Use the following to answer questions 64-65:Turf-Top Lawn Mower CompanyBalance Sheet(in thousands)Current Assets $600 Current Liabilities $400Other Assets & Investments 100 Long Term Debt 150Net Fixed Assets 900 Equity 1,050Total Assets $1,600 Total Liabilities & Equity $1,600Quick Clean Power Snow Shovel CompanyBalance Sheet(in thousands)Current Assets $200 Current Liabilities $120Other Assets & Investments 40 Long Term Debt 120Net Fixed Assets 300 Equity 300Total Assets $540 Total Liabilities & Equity $54064. The Turf-Top Lawn Mower Company has acquired the Quick Clean Power Snow Shovel Company.Turf-Top has agreed to pay $600 in cash, the money was raised through a new debt issue. Allliabilities will be paid off. The balance sheets of both companies are at market values which are also the book values before the combination. Construct the new balance sheet for this purchase.How has the position of Turf-Top Lawn Mower shareholders changed?Difficulty: Medium Page: 801-802Answer:Repay current liabilities & long-term debt = $120 + $120 = $240. This leaves $360 for equitywhich implies $60 in goodwill.。