英文版罗斯公司理财习题答案Chap020

- 格式:docx

- 大小:22.28 KB

- 文档页数:10

CHAPTER 8MAKING CAPITAL INVESTMENT DECISIONSAnswers to Concepts Review and Critical Thinking Questions1.In this context, an opportunity cost refers to the value of an asset or other input that will be used in aproject. The relevant cost is what the asset or input is actually worth today, not, for example, what it cost to acquire.2. a.Yes, the reduction in the sales of the company’s other products, referred to as erosion, andshould be treated as an incremental cash flow. These lost sales are included because they are a cost (a revenue reduction) that the firm must bear if it chooses to produce the new product.b. Yes, expenditures on plant and equipment should be treated as incremental cash flows. Theseare costs of the new product line. However, if these expenditures have already occurred, they are sunk costs and are not included as incremental cash flows.c. No, the research and development costs should not be treated as incremental cash flows. Thecosts of research and development undertaken on the product during the past 3 years are sunk costs and should not be included in the evaluation of the project. Decisions made and costs incurred in the past cannot be changed. They should not affect the decision to accept or reject the project.d. Yes, the annual depreciation expense should be treated as an incremental cash flow.Depreciation expense must be taken into account when calculating the cash flows related to a given project. While depreciation is not a cash expense that directly affects cash flow, it decreases a firm’s net income and hence, lowers its tax bill for the year. Because of this depreciation tax shield, the firm has more cash on hand at the end of the year than it would have had without expensing depreciation.e.No, dividend payments should not be treated as incremental cash flows. A firm’s decision topay or not pay dividends is independent of the decision to accept or reject any given investment project. For this reason, it is not an incremental cash flow to a given project. Dividend policy is discussed in more detail in later chapters.f.Yes, the resale value of plant and equipment at the end of a project’s life should be treated as anincremental cash flow. The price at which the firm sells the equipment is a cash inflow, and any difference between the book value of the equipment and its sale price will create gains or lossesthat result in either a tax credit or liability.g.Yes, salary and medical costs for production employees hired for a project should be treated asincremental cash flows. The salaries of all personnel connected to the project must be included as costs of that project.3.Item I is a relevant cost because the opportunity to sell the land is lost if the new golf club is produced. Item II is also relevant because the firm must take into account the erosion of sales of existing products when a new product is introduced. If the firm produces the new club, the earnings from the existing clubs will decrease, effectively creating a cost that must be included in the decision.Item III is not relevant because the costs of Research and Development are sunk costs. Decisions made in the past cannot be changed. They are not relevant to the production of the new clubs.4.For tax purposes, a firm would choose MACRS because it provides for larger depreciationdeductions earlier. These larger deductions reduce taxes, but have no other cash consequences.Notice that the choice between MACRS and straight-line is purely a time value issue; the total depreciation is the same; only the timing differs.5.It’s probably only a mild over-simplification. Current liabilities will all be paid, presumably. Thecash portion of current assets will be retrieved. Some receivables won’t be collected, and some inventory will not be sold, of course. Counterbalancing these losses is the fact that inventory sold above cost (and not replaced at the end of the project’s life) acts to increase working capital. These effects tend to offset one another.6.Management’s discretion to set the firm’s capital structure is applicable at the firm level. Since anyone particular project could be financed entirely with equity, another project could be financed with debt, and the firm’s overall capital structure remains unchanged, financing cost s are not relevant in the analysis of a project’s incremental cash flows according to the stand-alone principle.7.The EAC approach is appropriate when comparing mutually exclusive projects with different livesthat will be replaced when they wear out. This type of analysis is necessary so that the projects havea common life span over which they can be compared; in effect, each project is assumed to existover an infinite horizon of N-year repeating projects. Assuming that this type of analysis is valid implies that the project cash flows remain the same forever, thus ignoring the possible effects of, among other things: (1) inflation, (2) changing economic conditions, (3) the increasing unreliability of cash flow estimates that occur far into the future, and (4) the possible effects of future technology improvement that could alter the project cash flows.8.Depreciation is a non-cash expense, but it is tax-deductible on the income statement. Thusdepreciation causes taxes paid, an actual cash outflow, to be reduced by an amount equal to the depreciation tax shield, t c D. A reduction in taxes that would otherwise be paid is the same thing as a cash inflow, so the effects of the depreciation tax shield must be added in to get the total incremental aftertax cash flows.9.There are two particularly important considerations. The first is erosion. Will the “essentialized”book simply displace copies of the existing book that would have otherwise been sold? This is of special concern given the lower price. The second consideration is competition. Will other publishers step in and produce such a product? If so, then any erosion is much less relevant. A particular concern to book publishers (and producers of a variety of other product types) is that the publisher only makes money from the sale of new books. Thus, it is important to examine whether the new book would displace sales of used books (good from the publisher’s perspective) or new books (not good). The concern arises any time there is an active market for used product.10.Definitely. The damage to Porsche’s reputation is definitely a factor the company needed to consider.If the reputation was damaged, the company would have lost sales of its existing car lines.11.One company may be able to produce at lower incremental cost or market better. Also, of course,one of the two may have made a mistake!12.Porsche would recognize that the outsized profits would dwindle as more products come to marketand competition becomes more intense.Solutions to Questions and ProblemsNOTE: All end-of-chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability constraints, when these intermediate steps are included in this solutions manual, rounding may appear to have occurred. However, the final answer for each problem is found without rounding during any step in the problem.Basicing the tax shield approach to calculating OCF, we get:OCF = (Sales – Costs)(1 – t C) + t C DepreciationOCF = [($5 × 2,000 – ($2 × 2,000)](1 – 0.35) + 0.35($10,000/5)OCF = $4,600So, the NPV of the project is:NPV = –$10,000 + $4,600(PVIFA17%,5)NPV = $4,7172.We will use the bottom-up approach to calculate the operating cash flow for each year. We also mustbe sure to include the net working capital cash flows each year. So, the total cash flow each year will be:Year 1 Year 2 Year 3 Year 4 Sales Rs.7,000 Rs.7,000 Rs.7,000 Rs.7,000Costs 2,000 2,000 2,000 2,000Depreciation 2,500 2,500 2,500 2,500EBT Rs.2,500 Rs.2,500 Rs.2,500 Rs.2,500Tax 850 850 850 850Net income Rs.1,650 Rs.1,650 Rs.1,650 Rs.1,650OCF 0 Rs.4,150 Rs.4,150 Rs.4,150 Rs.4,150Capital spending –Rs.10,000 0 0 0 0NWC –200 –250 –300 –200 950Incremental cashflow –Rs.10,200 Rs.3,900 Rs.3,850 Rs.3,950 Rs.5,100The NPV for the project is:NPV = –Rs.10,200 + Rs.3,900 / 1.10 + Rs.3,850 / 1.102 + Rs.3,950 / 1.103 + Rs.5,100 / 1.104NPV = Rs.2,978.333. Using the tax shield approach to calculating OCF, we get:OCF = (Sales – Costs)(1 – t C) + t C DepreciationOCF = (R2,400,000 – 960,000)(1 – 0.30) + 0.30(R2,700,000/3)OCF = R1,278,000So, the NPV of the project is:NPV = –R2,700,000 + R1,278,000(PVIFA15%,3)NPV = R217,961.704.The cash outflow at the beginning of the project will increase because of the spending on NWC. Atthe end of the project, the company will recover the NWC, so it will be a cash inflow. The sale of the equipment will result in a cash inflow, but we also must account for the taxes which will be paid on this sale. So, the cash flows for each year of the project will be:Year Cash Flow0 – R3,000,000 = –R2.7M – 300K1 1,278,0002 1,278,0003 1,725,000 = R1,278,000 + 300,000 + 210,000 + (0 – 210,000)(.30)And the NPV of the project is:NPV = –R3,000,000 + R1,278,000(PVIFA15%,2) + (R1,725,000 / 1.153)NPV = R211,871.465. First we will calculate the annual depreciation for the equipment necessary for the project. Thedepreciation amount each year will be:Year 1 depreciation = R2.7M(0.3330) = R899,100Year 2 depreciation = R2.7M(0.4440) = R1,198,800Year 3 depreciation = R2.7M(0.1480) = R399,600So, the book value of the equipment at the end of three years, which will be the initial investment minus the accumulated depreciation, is:Book value in 3 years = R2.7M – (R899,100 + 1,198,800 + 399,600)Book value in 3 years = R202,500The asset is sold at a gain to book value, so this gain is taxable.Aftertax salvage value = R202,500 + (R202,500 – 210,000)(0.30)Aftertax salvage value = R207,750To calculate the OCF, we will use the tax shield approach, so the cash flow each year is:OCF = (Sales – Costs)(1 – t C) + t C DepreciationYear Cash Flow0 – R3,000,000 = –R2.7M – 300K1 1,277,730.00 = (R1,440,000)(.70) + 0.30(R899,100)2 1,367,640.00 = (R1,440,000)(.70) + 0.30(R1,198,800)3 1,635,630.00 = (R1,440,000)(.70) + 0.30(R399,600) + R207,750 + 300,000Remember to include the NWC cost in Year 0, and the recovery of the NWC at the end of the project.The NPV of the project with these assumptions is:NPV = – R3.0M + (R1,277,730/1.15) + (R1,367,640/1.152) + (R1,635,630/1.153)NPV = R220,655.206. First, we will calculate the annual depreciation of the new equipment. It will be:Annual depreciation charge = €925,000/5Annual depreciation charge = €185,000The aftertax salvage value of the equipment is:Aftertax salvage value = €90,000(1 – 0.35)Aftertax salvage value = €58,500Using the tax shield approach, the OCF is:OCF = €360,000(1 – 0.35) + 0.35(€185,000)OCF = €298,750Now we can find the project IRR. There is an unusual feature that is a part of this project. Accepting this project means that we will reduce NWC. This reduction in NWC is a cash inflow at Year 0. This reduction in NWC implies that when the project ends, we will have to increase NWC. So, at the end of the project, we will have a cash outflow to restore the NWC to its level before the project. We also must include the aftertax salvage value at the end of the project. The IRR of the project is:NPV = 0 = –€925,000 + 125,000 + €298,750(PVIFA IRR%,5) + [(€58,500 – 125,000) / (1+IRR)5]IRR = 23.85%7.First, we will calculate the annual depreciation of the new equipment. It will be:Annual depreciation = £390,000/5Annual depreciation = £78,000Now, we calculate the aftertax salvage value. The aftertax salvage value is the market price minus (or plus) the taxes on the sale of the equipment, so:Aftertax salvage value = MV + (BV – MV)t cVery often, the book value of the equipment is zero as it is in this case. If the book value is zero, the equation for the aftertax salvage value becomes:Aftertax salvage value = MV + (0 – MV)t cAftertax salvage value = MV(1 – t c)We will use this equation to find the aftertax salvage value since we know the book value is zero. So, the aftertax salvage value is:Aftertax salvage value = £60,000(1 – 0.34)Aftertax salvage value = £39,600Using the tax shield approach, we find the OCF for the project is:OCF = £120,000(1 – 0.34) + 0.34(£78,000)OCF = £105,720Now we can find the project NPV. Notice that we include the NWC in the initial cash outlay. The recovery of the NWC occurs in Year 5, along with the aftertax salvage value.NPV = –£390,000 – 28,000 + £105,720(PVIFA10%,5) + [(£39,600 + 28,000) / 1.15]NPV = £24,736.268.To find the BV at the end of four years, we need to find the accumulated depreciation for the firstfour years. We could calculate a table with the depreciation each year, but an easier way is to add the MACRS depreciation amounts for each of the first four years and multiply this percentage times the cost of the asset. We can then subtract this from the asset cost. Doing so, we get:BV4 = $9,300,000 – 9,300,000(0.2000 + 0.3200 + 0.1920 + 0.1150)BV4 = $1,608,900The asset is sold at a gain to book value, so this gain is taxable.Aftertax salvage value = $2,100,000 + ($1,608,900 – 2,100,000)(.40)Aftertax salvage value = $1,903,5609. We will begin by calculating the initial cash outlay, that is, the cash flow at Time 0. To undertake theproject, we will have to purchase the equipment and increase net working capital. So, the cash outlay today for the project will be:Equipment –€2,000,000NWC –100,000Total –€2,100,000Using the bottom-up approach to calculating the operating cash flow, we find the operating cash flow each year will be:Sales €1,200,000Costs 300,000Depreciation 500,000EBT €400,000Tax 140,000Net income €260,000The operating cash flow is:OCF = Net income + DepreciationOCF = €260,000 + 500,000OCF = €760,000To find the NPV of the project, we add the present value of the project cash flows. We must be sure to add back the net working capital at the end of the project life, since we are assuming the net working capital will be recovered. So, the project NPV is:NPV = –€2,100,000 + €760,000(PVIFA14%,4) + €100,000 / 1.144NPV = €173,629.3810.We will need the aftertax salvage value of the equipment to compute the EAC. Even though theequipment for each product has a different initial cost, both have the same salvage value. The aftertax salvage value for both is:Both cases: aftertax salvage value = $20,000(1 – 0.35) = $13,000To calculate the EAC, we first need the OCF and NPV of each option. The OCF and NPV for Techron I is:OCF = – $34,000(1 – 0.35) + 0.35($210,000/3) = $2,400NPV = –$210,000 + $2,400(PVIFA14%,3) + ($13,000/1.143) = –$195,653.45EAC = –$195,653.45 / (PVIFA14%,3) = –$84,274.10And the OCF and NPV for Techron II is:OCF = – $23,000(1 – 0.35) + 0.35($320,000/5) = $7,450NPV = –$320,000 + $7,450(PVIFA14%,5) + ($13,000/1.145) = –$287,671.75EAC = –$287,671.75 / (PVIFA14%,5) = –$83,794.05The two milling machines have unequal lives, so they can only be compared by expressing both on an equivalent annual basis, which is what the EAC method does. Thus, you prefer the Techron II because it has the lower (less negative) annual cost.。

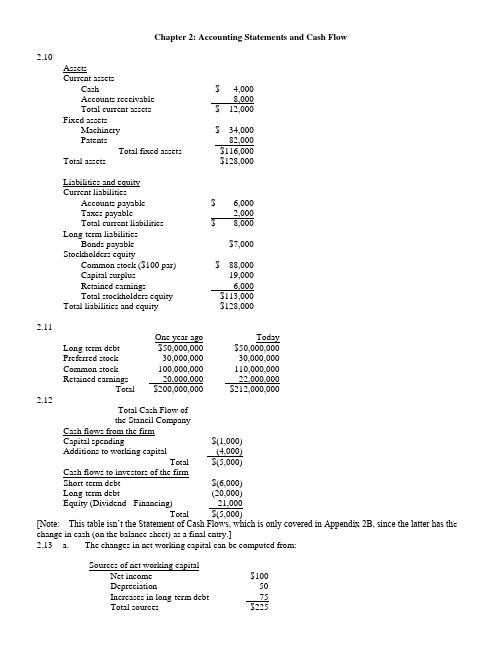

Chapter 2: Accounting Statements and Cash Flow2.10AssetsCurrent assetsCash $ 4,000Accounts receivable 8,000Total current assets $ 12,000Fixed assetsMachinery $ 34,000Patents 82,000Total fixed assets $116,000Total assets $128,000Liabilities and equityCurrent liabilitiesAccounts payable $ 6,000Taxes payable 2,000Total current liabilities $ 8,000Long-term liabilitiesBonds payable $7,000Stockholders equityCommon stock ($100 par) $ 88,000Capital surplus 19,000Retained earnings 6,000Total stockholders equity $113,000Total liabilities and equity $128,0002.11One year ago TodayLong-term debt $50,000,000 $50,000,000Preferred stock 30,000,000 30,000,000Common stock 100,000,000 110,000,000Retained earnings 20,000,000 22,000,000Total $200,000,000 $212,000,0002.12Total Cash Flow ofthe Stancil CompanyCash flows from the firmCapital spending $(1,000)Additions to working capital (4,000)Total $(5,000)Cash flows to investors of the firmShort-term debt $(6,000)Long-term debt (20,000)Equity (Dividend - Financing) 21,000Total $(5,000)[Note: This table isn’t the Statement of Cash Flows, which is only covered in Appendix 2B, since the latter has th e change in cash (on the balance sheet) as a final entry.]2.13 a. The changes in net working capital can be computed from:Sources of net working capitalNet income $100Depreciation 50Increases in long-term debt 75Total sources $225Uses of net working capitalDividends $50Increases in fixed assets* 150Total uses $200Additions to net working capital $25*Includes $50 of depreciation.b.Cash flow from the firmOperating cash flow $150Capital spending (150)Additions to net working capital (25)Total $(25)Cash flow to the investorsDebt $(75)Equity 50Total $(25)Chapter 3: Financial Markets and Net Present Value: First Principles of Finance (Advanced)3.14 $120,000 - ($150,000 - $100,000) (1.1) = $65,0003.15 $40,000 + ($50,000 - $20,000) (1.12) = $73,6003.16 a. ($7 million + $3 million) (1.10) = $11.0 millionb.i. They could spend $10 million by borrowing $5 million today.ii. They will have to spend $5.5 million [= $11 million - ($5 million x 1.1)] at t=1.Chapter 4: Net Present Valuea. $1,000 ⨯ 1.0510 = $1,628.89b. $1,000 ⨯ 1.0710 = $1,967.15c. $1,000 ⨯ 1.0520 = $2,653.30d. Interest compounds on the interest already earned. Therefore, the interest earned inSince this bond has no interim coupon payments, its present value is simply the present value of the $1,000 that will be received in 25 years. Note: As will be discussed in the next chapter, the present value of the payments associated with a bond is the price of that bond.PV = $1,000 /1.125 = $92.30PV = $1,500,000 / 1.0827 = $187,780.23a. At a discount rate of zero, the future value and present value are always the same. Remember, FV =PV (1 + r) t. If r = 0, then the formula reduces to FV = PV. Therefore, the values of the options are $10,000 and $20,000, respectively. You should choose the second option.b. Option one: $10,000 / 1.1 = $9,090.91Option two: $20,000 / 1.15 = $12,418.43Choose the second option.c. Option one: $10,000 / 1.2 = $8,333.33Option two: $20,000 / 1.25 = $8,037.55Choose the first option.d. You are indifferent at the rate that equates the PVs of the two alternatives. You know that rate mustfall between 10% and 20% because the option you would choose differs at these rates. Let r be thediscount rate that makes you indifferent between the options.$10,000 / (1 + r) = $20,000 / (1 + r)5(1 + r)4 = $20,000 / $10,000 = 21 + r = 1.18921r = 0.18921 = 18.921%The $1,000 that you place in the account at the end of the first year will earn interest for six years. The $1,000 that you place in the account at the end of the second year will earn interest for five years, etc. Thus, the account will have a balance of$1,000 (1.12)6 + $1,000 (1.12)5 + $1,000 (1.12)4 + $1,000 (1.12)3= $6,714.61PV = $5,000,000 / 1.1210 = $1,609,866.18a. $1.000 (1.08)3 = $1,259.71b. $1,000 [1 + (0.08 / 2)]2 ⨯ 3 = $1,000 (1.04)6 = $1,265.32c. $1,000 [1 + (0.08 / 12)]12 ⨯ 3 = $1,000 (1.00667)36 = $1,270.24d. $1,000 e0.08 ⨯ 3 = $1,271.25e. The future value increases because of the compounding. The account is earning interest on interest. Essentially, the interest is added to the account balance at the e nd of every compounding period. During the next period, the account earns interest on the new balance. When the compounding period shortens, the balance that earns interest is rising faster.The price of the consol bond is the present value of the coupon payments. Apply the perpetuity formula to find the present value. PV = $120 / 0.15 = $800a. $1,000 / 0.1 = $10,000b. $500 / 0.1 = $5,000 is the value one year from now of the perpetual stream. Thus, the value of theperpetuity is $5,000 / 1.1 = $4,545.45.c. $2,420 / 0.1 = $24,200 is the value two years from now of the perpetual stream. Thus, the value of the perpetuity is $24,200 / 1.12 = $20,000.pply the NPV technique. Since the inflows are an annuity you can use the present value of an annuity factor.ANPV = -$6,200 + $1,200 81.0= -$6,200 + $1,200 (5.3349)= $201.88Yes, you should buy the asset.Use an annuity factor to compute the value two years from today of the twenty payments. Remember, the annuity formula gives you the value of the stream one year before the first payment. Hence, the annuity factor will give you the value at the end of year two of the stream of payments.A= $2,000 (9.8181)Value at the end of year two = $2,000 20.008= $19,636.20The present value is simply that amount discounted back two years.PV = $19,636.20 / 1.082 = $16,834.88The easiest way to do this problem is to use the annuity factor. The annuity factor must be equal to $12,800 / $2,000 = 6.4; remember PV =C A T r. The annuity factors are in the appendix to the text. To use the factor table to solve this problem, scan across the row labeled 10 years until you find 6.4. It is close to the factor for 9%, 6.4177. Thus, the rate you will receive on this note is slightly more than 9%.You can find a more precise answer by interpolating between nine and ten percent.[ 10% ⎤[6.1446 ⎤a ⎡r ⎥bc ⎡6.4 ⎪ d⎣9%⎦⎣6.4177 ⎦By interpolating, you are presuming that the ratio of a to b is equal to the ratio of c to d.(9 - r ) / (9 - 10) = (6.4177 - 6.4 ) / (6.4177 - 6.1446)r = 9.0648%The exact value could be obtained by solving the annuity formula for the interest rate. Sophisticated calculators can compute the rate directly as 9.0626%.[Note: A standard financial calculator’s TVM keys can solve for this rate. With annuity flows, the IRR key on “advanced” financial c alculators is unnecessary.]a. The annuity amount can be computed by first calculating the PV of the $25,000 which youThat amount is $17,824.65 [= $25,000 / 1.075]. Next compute the annuity which has the same present value.A$17,824.65 = C 507.0$17,824.65 = C (4.1002)C = $4,347.26Thus, putting $4,347.26 into the 7% account each year will provide $25,000 five years from today.b. The lump sum payment must be the present value of the $25,000, i.e., $25,000 / 1.075 =$17,824.65The formula for future value of any annuity can be used to solve the problem (see footnote 11 of the text).Option one: This cash flow is an annuity due. To value it, you must use the after-tax amounts. Theafter-tax payment is $160,000 (1 - 0.28) = $115,200. Value all except the first payment using the standard annuity formula, then add back the first payment of $115,200 to obtain the value of this option.AValue = $115,200 + $115,200 30.010= $115,200 + $115,200 (9.4269)= $1,201,178.88Option two: This option is valued similarly. You are able to have $446,000 now; this is already on an after-tax basis. You will receive an annuity of $101,055 for each of the next thirty years. Those payments are taxable when you receive them, so your after-tax payment is $72,759.60 [= $101,055 (1 - 0.28)].AValue = $446,000 + $72,759.60 30.010= $446,000 + $72,759.60 (9.4269)= $1,131,897.47Since option one has a higher PV, you should choose it.et r be the rate of interest you must earn.$10,000(1 + r)12 = $80,000(1 + r)12= 8r = 0.18921 = 18.921%First compute the present value of all the payments you must make for your children’s educati on. The value as of one year before matriculation of one child’s education isA= $21,000 (2.8550) = $59,955.$21,000 415.0This is the value of the elder child’s education fourteen years from now. It is the value of the younger child’s education sixteen years from today. The present value of these isPV = $59,955 / 1.1514 + $59,955 / 1.1516= $14,880.44You want to make fifteen equal payments into an account that yields 15% so that the present value of the equal payments is $14,880.44.A= $14,880.44 / 5.8474 = $2,544.80Payment = $14,880.44 / 15.015This problem applies the growing annuity formula. The first payment is$50,000(1.04)2(0.02) = $1,081.60.PV = $1,081.60 [1 / (0.08 - 0.04) - {1 / (0.08 - 0.04)}{1.04 / 1.08}40]= $21,064.28This is the present value of the payments, so the value forty years from today is$21,064.28 (1.0840) = $457,611.46se the discount factors to discount the individual cash flows. Then compute the NPV of the project. NoticeYou can still use the factor tables to compute their PV. Essentially, they form cash flows that are a six year annuity less a two year annuity. Thus, the appropriate annuity factor to use with them is 2.6198 (= 4.3553 - 1.7355).Year Cash Flow Factor PV0.9091 $636.371$70020.8264 743.769003 1,000 ⎤4 1,000 ⎥ 2.6198 2,619.805 1,000 ⎥6 1,000 ⎦7 1,250 0.5132 641.508 1,375 0.4665 641.44Total $5,282.87NPV = -$5,000 + $5,282.87= $282.87Purchase the machine.Chapter 5: How to Value Bonds and StocksThe amount of the semi-annual interest payment is $40 (=$1,000 ⨯ 0.08 / 2). There are a total of 40 periods;i.e., two half years in each of the twenty years in the term to maturity. The annuity factor tables can be usedto price these bonds. The appropriate discount rate to use is the semi-annual rate. That rate is simply the annual rate divided by two. Thus, for part b the rate to be used is 5% and for part c is it 3%.A+F/(1+r)40PV=C Tra. $40 (19.7928) + $1,000 / 1.0440 = $1,000Notice that whenever the coupon rate and the market rate are the same, the bond is priced at par.b. $40 (17.1591) + $1,000 / 1.0540 = $828.41Notice that whenever the coupon rate is below the market rate, the bond is priced below par.c. $40 (23.1148) + $1,000 / 1.0340 = $1,231.15Notice that whenever the coupon rate is above the market rate, the bond is priced above par.a. The semi-annual interest rate is $60 / $1,000 = 0.06. Thus, the effective annual rate is 1.062 - 1 =0.1236 = 12.36%.A+ $1,000 / 1.0612b. Price = $30 12.006= $748.48A+ $1,000 / 1.0412c. Price = $30 1204.0= $906.15Note: In parts b and c we are implicitly assuming that the yield curve is flat. That is, the yield in year 5applies for year 6 as well.rice = $2 (0.72) / 1.15 + $4 (0.72) / 1.152 + $50 / 1.153= $36.31The number of shares you own = $100,000 / $36.31 = 2,754 sharesPrice = $1.15 (1.18) / 1.12 + $1.15 (1.182) / 1.122 + $1.152 (1.182) / 1.123+ {$1.152 (1.182)(1.06) / (0.12 - 0.06)} / 1.123= $26.95[Insert before last sentence of question: Assume that dividends are a fixed proportion of earnings.] Dividend one year from now = $5 (1 - 0.10) = $4.50Price = $5 + $4.50 / {0.14 - (-0.10)}= $23.75Since the current $5 dividend has not yet been paid, it is still included in the stock price.Chapter 6: Some Alternative Investment Rulesa. Payback period of Project A = 1 + ($7,500 - $4,000) / $3,500 = 2 yearsPayback period of Project B = 2 + ($5,000 - $2,500 -$1,200) / $3,000 = 2.43 yearsProject A should be chosen.b. NPV A = -$7,500 + $4,000 / 1.15 + $3,500 / 1.152 + $1,500 / 1.153 = -$388.96NPV B = -$5,000 + $2,500 / 1.15 + $1,200 / 1.152 + $3,000 / 1.153 = $53.83Project B should be chosen.a. Average Investment:($16,000 + $12,000 + $8,000 + $4,000 + 0) / 5 = $8,000Average accounting return:$4,500 / $8,000 = 0.5625 = 56.25%b. 1. AAR does not consider the timing of the cash flows, hence it does not consider the timevalue of money.2. AAR uses an arbitrary firm standard as the decision rule.3. AAR uses accounting data rather than net cash flows.aAverage Investment = (8000 + 4000 + 1500 + 0)/4 = 3375.00Average Net Income = 2000(1-0.75) = 1500=> AAR = 1500/3375=44.44%a. Solve x by trial and error:-$8,000 + $4,000 / (1 + x) + $3000 / (1 + x)2 + $2,000 / (1 + x)3 = 0x = 6.93%b. No, since the IRR (6.93%) is less than the discount rate of 8%.Alternatively, the NPV @ a discount rate of 0.08 = -$136.62.a. Solve r in the equation:$5,000 - $2,500 / (1 + r) - $2,000 / (1 + r)2 - $1,000 / (1 + r)3- $1,000 / (1 + r)4 = 0By trial and error,IRR = r = 13.99%b. Since this problem is the case of financing, accept the project if the IRR is less than the required rate of return.IRR = 13.99% > 10%Reject the offer.c. IRR = 13.99% < 20%Accept the offer.d. When r = 10%:NPV = $5,000 - $2,500 / 1.1 - $2,000 / 1.12 - $1,000 / 1.13 - $1,000 / 1.14When r = 20%:NPV = $5,000 - $2,500 / 1.2 - $2,000 / 1.22 - $1,000 / 1.23 - $1,000 / 1.24= $466.82Yes, they are consistent with the choices of the IRR rule since the signs of the cash flows change only once.A/ $160,000 = 1.04PI = $40,000 715.0Since the PI exceeds one accept the project.Chapter 7: Net Present Value and Capital BudgetingSince there is uncertainty surrounding the bonus payments, which McRae might receive, you must use the expected value of McRae’s bonuses in the computation of the PV of his contract. McRae’s salary plus the expected value of his bonuses in years one through three is$250,000 + 0.6 ⨯ $75,000 + 0.4 ⨯ $0 = $295,000.Thus the total PV of his three-year contract isPV = $400,000 + $295,000 [(1 - 1 / 1.12363) / 0.1236]+ {$125,000 / 1.12363} [(1 - 1 / 1.123610 / 0.1236]= $1,594,825.68EPS = $800,000 / 200,000 = $4NPVGO = (-$400,000 + $1,000,000) / 200,000 = $3Price = EPS / r + NPVGO= $4 / 0.12 + $3=$36.33Year 0 Year 1 Year 2 Year 3 Year 4 Year 51. Annual Salary$120,000 $120,000 $120,000 $120,000 $120,000 Savings2. Depreciation 100,000 160,000 96,000 57,600 57,6003. Taxable Income 20,000 -40,000 24,000 62,400 62,4004. Taxes 6,800 -13,600 8,160 21,216 21,2165. Operating Cash Flow113,200 133,600 111,840 98,784 98,784 (line 1-4)$100,000 -100,0006. ∆ Net workingcapital7. Investment $500,000 75,792*8. Total Cash Flow -$400,000 $113,200 $133,600 $111,840 $98,784 $74,576*75,792 = $100,000 - 0.34 ($100,000 - $28,800)NPV = -$400,000+ $113,200 / 1.12 + $133,600 / 1.122 + $111,840 / 1.123+ $98,784 / 1.124 + $74,576 / 1.125= -$7,722.52Real interest rate = (1.15 / 1.04) - 1 = 10.58%NPV A = -$40,000+ $20,000 / 1.1058 + $15,000 / 1.10582 + $15,000 / 1.10583= $1,446.76NPV B = -$50,000+ $10,000 / 1.15 + $20,000 / 1.152 + $40,000 / 1.153= $119.17Choose project A.PV = $120,000 / {0.11 - (-0.06)}t = 0 t = 1 t = 2 t = 3 t = 4 t = 5 t = 6 ...$12,000 $6,000 $6,000 $6,000$4,000$12,000 $6,000 $6,000 ...The present value of one cycle is:A+ $4,000 / 1.064PV = $12,000 + $6,000 306.0= $12,000 + $6,000 (2.6730) + $4,000 / 1.064= $31,206.37The cycle is four years long, so use a four year annuity factor to compute the equivalent annual cost (EAC).AEAC = $31,206.37 / 406.0= $31,206.37 / 3.4651= $9,006The present value of such a stream in perpetuity is$9,006 / 0.06 = $150,100o evaluate the word processors, compute their equivalent annual costs (EAC).BangAPV(costs) = (10 ⨯ $8,000) + (10 ⨯ $2,000) 414.0= $80,000 + $20,000 (2.9137)= $138,274EAC = $138,274 / 2.9137= $47,456IOUAPV(costs) = (11 ⨯ $5,000) + (11 ⨯ $2,500) 3.014- (11 ⨯ $500) / 1.143= $55,000 + $27,500 (2.3216) - $5,500 / 1.143= $115,132EAC = $115,132 / 2.3216= $49,592BYO should purchase the Bang word processors.Chapter 8: Strategy and Analysis in Using Net Present ValueThe accounting break-even= (120,000 + 20,000) / (1,500 - 1,100)= 350 units. The accounting break-even= 340,000 / (2.00 - 0.72)= 265,625 abalonesb. [($2.00 ⨯ 300,000) - (340,000 + 0.72 ⨯ 300,000)] (0.65)= $28,600This is the after tax profit.Chapter 9: Capital Market Theory: An Overviewa. Capital gains = $38 - $37 = $1 per shareb. Total dollar returns = Dividends + Capital Gains = $1,000 + ($1*500) = $1,500 On a per share basis, this calculation is $2 + $1 = $3 per sharec. On a per share basis, $3/$37 = 0.0811 = 8.11% On a total dollar basis, $1,500/(500*$37) = 0.0811 = 8.11%d. No, you do not need to sell the shares to include the capital gains in the computation of the returns. The capital gain is included whether or not you realize the gain. Since you could realize the gain if you choose, you should include it.The expected holding period return is:()[]%865.1515865.052$/52$75.54$50.5$==-+There appears to be a lack of clarity about the meaning of holding period returns. The method used in the answer to this question is the one used in Section 9.1. However, the correspondence is not exact, because in this question, unlike Section 9.1, there are cash flows within the holding period. The answer above ignores the dividend paid in the first year. Although the answer above technically conforms to the eqn at the bottom of Fig. 9.2, the presence of intermediate cash flows that aren’t accounted for renders th is measure questionable, at best. There is no similar example in the body of the text, and I have never seen holding period returns calculated in this way before.Although not discussed in this book, there are two generally accepted methods of computing holding period returns in the presence of intermediate cash flows. First, the time weighted return calculates averages (geometric or arithmetic) of returns between cash flows. Unfortunately, that method can’t be used here, because we are not given the va lue of the stock at the end of year one. Second, the dollar weighted measure calculates the internal rate of return over the entire holding period. Theoretically, that method can be applied here, as follows: 0 = -52 + 5.50/(1+r) + 60.25/(1+r)2 => r = 0.1306.This produces a two year holding period return of (1.1306)2 – 1 = 0.2782. Unfortunately, this book does not teach the dollar weighted method.In order to salvage this question in a financially meaningful way, you would need the value of the stock at the end of one year. Then an illustration of the correct use of the time-weighted return would be appropriate. A complicating factor is that, while Section 9.2 illustrates the holding period return using the geometric return for historical data, the arithmetic return is more appropriate for expected future returns.E(R) = T-Bill rate + Average Excess Return = 6.2% + (13.0% -3.8%) = 15.4%. Common Treasury Realized Stocks Bills Risk Premium -7 32.4% 11.2% 21.2%-6 -4.9 14.7 -19.6-5 21.4 10.5 10.9 -4 22.5 8.8 13.7 -3 6.3 9.9 -3.6 -2 32.2 7.7 24.5 Last 18.5 6.2 12.3 b. The average risk premium is 8.49%.49.873.125.246.37.139.106.192.21=++-++- c. Yes, it is possible for the observed risk premium to be negative. This can happen in any single year. The.b.Standard deviation = 03311.0001096.0=.b.Standard deviation = = 0.03137 = 3.137%.b.Chapter 10: Return and Risk: The Capital-Asset-Pricing Model (CAPM)a. = 0.1 (– 4.5%) + 0.2 (4.4%) + 0.5 (12.0%) + 0.2 (20.7%) = 10.57%b.σ2 = 0.1 (–0.045 – 0.1057)2 + 0.2 (0.044 – 0.1057)2 + 0.5 (0.12 – 0.1057)2+ 0.2 (0.207 – 0.1057)2 = 0.0052σ = (0.0052)1/2 = 0.072 = 7.20%Holdings of Atlas stock = 120 ⨯ $50 = $6,000 ⨯ $20 = $3,000Weight of Atlas stock = $6,000 / $9,000 = 2 / 3Weight of Babcock stock = $3,000 / $9,000 = 1 / 3a. = 0.3 (0.12) + 0.7 (0.18) = 0.162 = 16.2%σP 2= 0.32 (0.09)2 + 0.72 (0.25)2 + 2 (0.3) (0.7) (0.09) (0.25) (0.2)= 0.033244σP= (0.033244)1/2 = 0.1823 = 18.23%a.State Return on A Return on B Probability1 15% 35% 0.4 ⨯ 0.5 = 0.22 15% -5% 0.4 ⨯ 0.5 = 0.23 10% 35% 0.6 ⨯ 0.5 = 0.34 10% -5% 0.6 ⨯ 0.5 = 0.3b. = 0.2 [0.5 (0.15) + 0.5 (0.35)] + 0.2[0.5 (0.15) + 0.5 (-0.05)]+ 0.3 [0.5 (0.10) + 0.5 (0.35)] + 0.3 [0.5 (0.10) + 0.5 (-0.05)]= 0.135= 13.5%Note: The solution to this problem requires calculus.Specifically, the solution is found by minimizing a function subject to a constraint. Calculus ability is not necessary to understand the principles behind a minimum variance portfolio.Min { X A2 σA2 + X B2σB2+ 2 X A X B Cov(R A , R B)}subject to X A + X B = 1Let X A = 1 - X B. Then,Min {(1 - X B)2σA2 + X B2σB2+ 2(1 - X B) X B Cov (R A, R B)}Take a derivative with respect to X B.d{∙} / dX B = (2 X B - 2) σA2+ 2 X B σB2 + 2 Cov(R A, R B) - 4 X B Cov(R A, R B)Set the derivative equal to zero, cancel the common 2 and solve for X B.X BσA2- σA2+ X B σB2 + Cov(R A, R B) - 2 X B Cov(R A, R B) = 0X B = {σA2 - Cov(R A, R B)} / {σA2+ σB2 - 2 Cov(R A, R B)}andX A = {σB2 - Cov(R A, R B)} / {σA2+ σB2 - 2 Cov(R A, R B)}Using the data from the problem yields,X A = 0.8125 andX B = 0.1875.a. Using the weights calculated above, the expected return on the minimum variance portfolio isE(R P) = 0.8125 E(R A) + 0.1875 E(R B)= 0.8125 (5%) + 0.1875 (10%)= 5.9375%b. Using the formula derived above, the weights areX A = 2 / 3 andX B = 1 / 3c. The variance of this portfolio is zero.σP 2= X A2 σA2 + X B2σB2+ 2 X A X B Cov(R A , R B)= (4 / 9) (0.01) + (1 / 9) (0.04) + 2 (2 / 3) (1 / 3) (-0.02)= 0This demonstrates that assets can be combined to form a risk-free portfolio.14.2%= 3.7%+β(7.5%) ⇒β = 1.40.25 = R f + 1.4 [R M– R f] (I)0.14 = R f + 0.7 [R M– R f] (II)(I) – (II)=0.11 = 0.7 [R M– R f] (III)[R M– R f ]= 0.1571Put (III) into (I) 0.25 = R f + 1.4[0.1571]R f = 3%[R M– R f ]= 0.1571R M = 0.1571 + 0.03= 18.71%a. = 4.9% + βi (9.4%)βD= Cov(R D, R M) / σM 2 = 0.0635 / 0.04326 = 1.468= 4.9 + 1.468 (9.4) = 18.70%Weights:X A = 5 / 30 = 0.1667X B = 10 / 30 = 0.3333X C = 8 / 30 = 0.2667X D = 1 - X A - X B - X C = 0.2333Beta of portfolio= 0.1667 (0.75) + 0.3333 (1.10) + 0.2667 (1.36) + 0.2333 (1.88)= 1.293= 4 + 1.293 (15 - 4) = 18.22%a. (i) βA= ρA,MσA / σMρA,M= βA σM / σA= (0.9) (0.10) / 0.12= 0.75(ii) σB= βB σM / ρB,M= (1.10) (0.10) / 0.40= 0.275(iii) βC= ρC,MσC / σM= (0.75) (0.24) / 0.10= 1.80(iv) ρM,M= 1(v) βM= 1(vi) σf= 0(vii) ρf,M= 0(viii) βf= 0b. SML:E(R i) = R f + βi {E(R M) - R f}= 0.05 + (0.10) βiSecurity βi E(R i)A 0.13 0.90 0.14B 0.16 1.10 0.16C 0.25 1.80 0.23Security A performed worse than the market, while security C performed better than the market.Security B is fairly priced.c. According to the SML, security A is overpriced while security C is under-priced. Thus, you could invest in security C while sell security A (if you currently hold it).a. The typical risk-averse investor seeks high returns and low risks. To assess thetwo stocks, find theReturns:State of economy ProbabilityReturn on A*Recession 0.1 -0.20 Normal 0.8 0.10 Expansion0.10.20* Since security A pays no dividend, the return on A is simply (P 1 / P 0) - 1. = 0.1 (-0.20) + 0.8 (0.10) + 0.1 (0.20) = 0.08 = 0.09 This was given in the problem.Risk:R A - (R A -)2 P ⨯ (R A -)2 -0.28 0.0784 0.00784 0.02 0.0004 0.00032 0.12 0.0144 0.00144 Variance 0.00960Standard deviation (R A ) = 0.0980βA = {Corr(R A , R M ) σ(R A )} / σ(R M ) = 0.8 (0.0980) / 0.10= 0.784βB = {Corr(R B , R M ) σ(R B )} / σ(R M ) = 0.2 (0.12) / 0.10= 0.24The return on stock B is higher than the return on stock A. The risk of stock B, as measured by itsbeta, is lower than the risk of A. Thus, a typical risk-averse investor will prefer stock B.b. = (0.7) + (0.3) = (0.7) (0.8) + (0.3) (0.09) = 0.083σP 2= 0.72 σA 2 + 0.32 σB 2 + 2 (0.7) (0.3) Corr (R A , R B ) σA σB = (0.49) (0.0096) + (0.09) (0.0144) + (0.42) (0.6) (0.0980) (0.12) = 0.0089635 σP = = 0.0947 c. The beta of a portfolio is the weighted average of the betas of the components of the portfolio. βP = (0.7) βA + (0.3) βB = (0.7) (0.784) + (0.3) (0.240) = 0.621Chapter 11:An Alternative View of Risk and Return: The Arbitrage Pricing Theorya. Stock A:()()R R R R R A A A m m Am A=+-+=+-+βεε105%12142%...Stock B:()()R R R R R B B m m Bm B=+-+=+-+βεε130%098142%...Stock C:()R R R R R C C C m m Cm C=+-+=+-+βεε157%137142%)..(.b.()[]()[]()[]()()()()()()[]()()CB A m cB A m c m B m A m CB A P 25.045.030.0%2.14R 1435.1%925.1225.045.030.0%2.14R 37.125.098.045.02.130.0%7.1525.0%1345.0%5.1030.0%2.14R 37.1%7.1525.0%2.14R 98.0%0.1345.0%2.14R 2.1%5.1030.0R 25.0R 45.0R 30.0R ε+ε+ε+-+=ε+ε+ε+-+++++=ε+-++ε+-++ε+-+=++= c.i.()R R R A B C =+-==+-==+-=105%1215%142%)1113%09815%142%)137%157%13715%142%168%..(..46%.(......ii.R P =+-=12925%1143515%142%)138398%..(..To determine which investment investor would prefer, you must compute the variance of portfolios created bymany stocks from either market. Note, because you know that diversification is good, it is reasonable to assume that once an investor chose the market in which he or she will invest, he or she will buy many stocks in that market.Known:E EF ====001002 and and for all i.i σσεε..Assume: The weight of each stock is 1/N; that is, X N i =1/for all i.If a portfolio is composed of N stocks each forming 1/N proportion of the portfolio, the return on the portfolio is 1/N times the sum of the returns on the N stocks. Recall that the return on each stock is 0.1+βF+ε.()()()()()()[]()()()()()()()[]()[]()[]()()[]()()()()()j i 2j i 22j i i 2222222222P P P P iP ,0.04Corr 0.01,Cov s =isvariance the ,N as limit In the ,Cov 1/N 1s 1/N s )(1/N 1/N F 2F E 1/N F E 0.10.1/N F 0.1E R E R E R Var 0.101/N 00.1E 1/N F E 0.11/N F 0.1E R E 1/N F 0.1F 0.1(1/N)R 1/N R εε+β=εε+β∞⇒εε-+ε+β=ε∑+εβ+β=ε+β=-ε+β+=-==+β+=ε+β+=ε∑+β+=ε+β+=ε+β+==∑∑∑∑∑∑∑∑()()()()()()Thus,F R f E R E R Var R Corr Var R Corr ii ip P p i j PijR 1i =++=++===+=+010*********002250040002500412212111222.........,,εεεεεεa.()()()()Corr Corr Var R Var R i j i j p pεεεε112212000225000225,,..====Since Var ()()R p 1 Var R 2p 〉, a risk averse investor will prefer to invest in the second market.b. Corr ()()εεεε112090i j j ,.,== and Corr 2i()()Var R Var R pp120058500025==..。

Chapter 20Issuing Securities to the Public Multiple Choice Questions1. An equity issue sold directly to the public is called:A. a rights offer.B. a general cash offer.C. a restricted placement.D. a fully funded sales.E. a standard call issue.2. An equity issue sold to the firm's existing stockholders is called:A. a rights offer.B. a general cash offer.C. a private placement.D. an underpriced issue.E. an investment banker's issue.3. Management's first step in any issue of securities to the public is:A. to file a registration form with the SEC.B. to distribute copies of the preliminary prospectus.C. to distribute copies of the final prospectus.D. to obtain approval from the board of directors.E. to prepare the tombstone advertisement.4. A rights offering is:A. the issuing of options on shares to the general public to acquire stock.B. the issuing of an option directly to the existing shareholders to acquire stock.C. the issuing of proxies which are used by shareholders to exercise their voting rights.D. strictly a public market claim on the company which can be traded on an exchange.E. the awarding of special perquisites to management.5. Companies use tombstone advertisements in the financial press to:A. announce the death of the company.B. announce the failure of a financial strategy.C. announce the availability of a new issue of a corporate security.D. notify the public of foreclosure.E. None of the above.6. The first public equity issue made by a company is a(n):A. initial private offering.B. initial public offering.C. secondary offering.D. seasoned new issue.E. None of the above.7. The first public equity issue that is made by a company is referred to as:A. a rights issue.B. a general cash offer.C. an initial public offering.D. an unseasoned issue.E. Both C and D.8. A new public equity issue from a company with equity previously outstanding is called a(n):A. initial public offering.B. seasoned equity issue.C. unseasoned equity issue.D. private placement.E. syndicate.9. The green shoe option is used to:A. cover oversubscription.B. cover excess demand.C. provide additional reward to the investment bankers for a risky issue.D. provide additional reward to the issuing firm for a risky issue.E. Both A and B.10. Dilution refers to:A. the increase in stock value due to wider ownership of stock.B. the loss in existing shareholder's equity.C. the loss in new shareholder's equity.D. the loss in all shareholder's equity, both existing shareholders and new shareholders.E. None of the above.11. During the SEC waiting period the potential issuing company can issue a preliminary prospectus which contains:A. exactly the same information as the final prospectus except an indication of SEC approval.B. all the information as the final prospectus including red writing stating it is a red herring.C. very limited financial information and red writing stating it is preliminary.D. only a description of what the funds are to be used for.E. information very similar to the final prospectus without a price nor with SEC approval.12. A company must file a registration statement with the SEC providing various financial and company history information. The registration statement does not need to be filed if:A. the issue is less than $50 million.B. the loan matures within 9 months.C. the issue is less than $5.0 million.D. Both A and B.E. Both B and C.13. Regulation A security issues are exempt from full SEC registration filing and use only a brief offering statement if:A. the issue is for less than $5,000,000.B. insiders sell no more than $1,500,000 of stock.C. insiders sell no more than 100,000,000 shares.D. Both A and C.E. Both A and B.14. Potential investors learn of the information concerning the firm and its new issue from the:A. pre-underwriting negotiating meeting.B. red herring.C. letter of commitment.D. emails from their former finance professor.E. rights offering.15. A registration statement is effective on the 20th day after filing unless:A. the SEC is backlogged with statements.B. a tombstone ad is issued indicating its demise.C. a letter of comment suggesting changes is issued by the SEC.D. a syndicate can be formed sooner.E. None of the above.16. Investment banks perform which of the following services for corporate issuers:A. formulating the method used to issue the securities.B. pricing the new securities.C. selling the new securities.D. All of the above.E. None of the above.17. A group of investment bankers who pool their efforts to underwrite a security are known as a(n):A. amalgamate.B. conglomerate.C. green shoe group.D. klatch.E. syndicate.18. A firm commitment arrangement with an investment banker occurs when:A. the syndicate is in place to handle the issue.B. the spread between the buying and selling price is less than one percent.C. the issue is solidly accepted in the market evidenced by a large price increase.D. when the investment banker buys the securities for less than the offering price and accepts the risk of not being able to sell them.E. when the investment banker sells as much of the security as the market can bear without a price decrease.19. Which of the following is not normally an example of the services offered by investment bankers?A. Aiding in the sale of securitiesB. Facilitating mergersC. Acting as brokers to both individuals and institutional clientsD. Offering checking accounts to corporationsE. Both C and D20. In a best efforts offering the investment banker makes their money primarily by:A. earning the spread between the buying and offering price.B. earning a commission on each share sold.C. earning the discount between the buying and offering price.D. charging a flat fee for all services.E. None of the above.21. Under the _____ method, the underwriter buys the securities for less than the offering price and accepts the risk of not selling the issue, while under the _____ method, the underwriter does not purchase the shares but merely acts as an agent.A. best efforts; firm commitmentB. firm commitment; best effortsC. general cash offer; best effortsD. competitive offer; negotiated offerE. seasoned; unseasoned22. Professor Jay Ritter found best-efforts offerings are:A. reserved for the premier customers because they deserve 'best-efforts'.B. used most often with seasoned equity issues.C. used with small IPO issues.D. attractive because of price stability.E. None of the above.23. Empirical evidence suggests that new equity issues are generally:A. priced efficiently by the market.B. overpriced by investor excitement concerning a new issue.C. overpriced resulting from SEC regulation.D. underpriced, in part, to counteract the winner's curse.E. underpriced resulting from SEC regulation.24. The diagonal listing of investment bankers on tombstone advertisements reflects their ____ relative to the other investment bankers listed below.A. prestigeB. ability to manage selling syndicatesC. role as a firm commitment buyerD. role as a best efforts sellerE. None of the above25. The reputational capital of investment bankers is based on their roles as intermediaries with more in-depth knowledge of the issuer. Investment bankers maintain their reputation by:A. certifying the issue.B. monitoring the issuing firm's management and performance.C. pricing issues fairly.D. All of the above.E. None of the above.26. The key difference between a negotiated offer and a competitive offer is that:A. the underwriters can not set the spread in a negotiated bid but can in a competitive offer.B. the issuing firm can offer its securities to the highest bidder in a competitive bid but in a negotiated bid only one investment banker is used.C. the issuing firm works the underwriter for the best spread in a negotiated bid which will be less than that available in a competitive offer.D. the underwriter will not do a full investigation in a negotiated bid because the company is at their mercy, while in a competitive bid the underwriter must be extra diligent.E. None of the above.27. The offering price is set to make an issue attractive to the market and provide a good price to the issuer. Which of the following is/are true?A. Empirical studies by Ritter have shown that the average firm commitments have had a17.8% underpricing on the first day of trading.B. Empirical studies have shown that best efforts sales have underpricing on the first day of trading.C. Some issues which rose dramatically on the first day of trading were viewed as successfully priced by the underwriter because it helped build a long-term investment base.D. All of the above.E. None of the above.28. Empirical evidence suggests that upon announcement of a new equity issue, current stock prices generally:A. drop, perhaps because the new issue reflects management's view that common stock is currently overvalued.B. remain about the same since an efficient market anticipates a new equity issue.C. increase, perhaps because the issues are associated with positive NPV projects.D. increase, because the market supply is always less than demand.E. increase, because underwriters exercise their green shoe option.29. Underpricing can possibly be explained by:A. oversubscription of an issue.B. strong demand by investors.C. undersubscription of an issue.D. Both B and C.E. Both A and B.30. Debt capacity is often given as a reason for the value of the stock falling when equity is issued. The reason for this is:A. the high issue costs of a debt offering must be paid by the shareholders.B. the priority position of the equity is lowered.C. management has information that the probability of default has risen, limiting the debt capacity and causing the firm to raise equity capital.D. All of the above.E. None of the above31. A study by Lee, Lockhead, Ritter, and Zhao that examined the underwriting discount and other direct costs of going public with a debt or equity offering, found:A. the direct expenses are higher for equity than debt offerings.B. substantial economies of scale are prevalent.C. underpricing, on average, is similar in magnitude to total direct expenses.D. All of the above.E. None of the above.32. The six components that make up the total costs of new issues are:A. the spread; other direct expenses such as filing fees; indirect expenses such as management time; economies of scale; abnormal returns and the Green Shoe option.B. the discount; other direct expenses such as filing fees; indirect expenses such as management time; due diligence costs; abnormal returns and the Green Shoe option.C. the spread; other direct expenses such as filing fees; indirect expenses such as management time; abnormal returns; underpricing and the Green Shoe option.D. the spread; other direct expenses such as filing fees; economies of scale; due diligence costs; abnormal returns and underpricing.E. None of the above.33. In comparison to debt issuance expenses, the total direct costs of equity issues are:A. considerably less.B. about the same.C. meaningless.D. considerably greater.E. None of the above.34. To determine the value of a rights offering, the stockholder needs to know the following two pieces of information in addition to the current stock price:A. the subscription price and the number of rights needed to acquire a new share.B. the amount of new equity to be raised and the number of rights needed to acquire a new share.C. the amount of new equity to be raised and standby fee.D. the detachment date and the subscription price.E. None of the above.35. Assuming everything else is constant, when a stock goes ex-rights its price should:A. decrease since the stockholder is losing an option.B. increase since the corporation no longer has the right to force the stockholder to convert.C. remain the same since an efficient market would anticipate this change.D. move up or down depending on whether a small investor wanted to exercise his/his rights.E. None of the above.36. If a shareholder or investor wants to acquire new stock under a rights plant they must:A. acquire new stock in the market to get a controlling fraction of shares to be eligible for rights.B. simply pay a registration fee and turn in the subscription price.C. acquire the correct rights per share desired, then turn the rights and the total subscription price into the subscription agent.D. acquire the correct rights and wait for the company to send you the stock.E. call their broker and sell some CBOE options to make any money.37. Which of the following statements is true?A. The subscription price is generally above the old stock price.B. The subscription price is generally above the ex-rights price.C. The subscription price is generally below the old stock price.D. Both A and B.E. Both B and C.38. A shareholder who has rights is:A. always better off to exercise the rights.B. always better off to sell the rights into the market.C. able to exercise their rights or sell them.D. never in the same ownership position again with rights.E. None of the above.39. A standby underwriting arrangement provides the:A. company with methods to cancel the offering.B. company with an alternate investment banker if there is conflict between the issuer and the agent.C. investment banker with an oversubscription privilege to ensure profits are earned.D. company with an alternative avenue of sale to ensure success of the rights offering.E. investment bankers with an added syndication for the rights offering.40. Professor Clifford W. Smith, in evaluating issuance costs from underwritten issues, rights issues with standby underwriting, and a pure rights issues, found that 90% of the issues are underwritten, which was the most expensive method. This is done because:A. investment bankers know more than CFOs and they may buy the issue at an agreed upon price and disburse the funds sooner.B. investment bankers can increase the price received by increasing confidence in the issue, and they will buy the issue at an agreed upon price and disburse the cash sooner.C. investment bankers provide other services including price counseling, increasing public confidence, and providing funds to the issuer sooner.D. investment bankers know how to price the issue, and would not need to set as low as a price as the subscription price and provide price counseling.E. None of the above.41. Corporations use the shelf registration method of security sales because:A. preregistered securities can be quickly brought to market.B. the main registration process is eliminated for up to two years.C. their stock is below investment grade.D. Both A and B.E. Both B and C.42. In terms of costs of issuing equity, Professor Clifford W. Smith finds that the ranking of methods, from cheapest to most expensive, is:A. rights issue with standby underwriting, equity issue with underwriting, pure rights issue.B. pure rights issue, rights issue with standby underwriting, equity issue with underwriting.C. pure rights issue, preferred stock and debt issue with underwriting for an IPO, rights issue with standby underwriting.D. equity issue with underwriting, rights issue with standby underwriting, pure rights issue.E. equity issue with underwriting, pure rights issue, rights issue with standby underwriting.43. Arguments to explain why most equity issues are underwritten versus sold through a rights offering are:A. underwriters buy at an agreed upon price and bear some risk of selling the issue.B. cash proceeds are available sooner in underwriting and the issue is available to a wider market.C. investment bankers can provide market advice and certify the issue for potential investors.D. All of the above.E. None of the above.44. Corporations are allowed to use the shelf registration method if they:A. are rated investment grade and have aggregate market stock value of more than $150 million.B. have not violated the 1934 Securities Act in the past 12 months.C. have not defaulted on its debt in the past 3 years.D. All of the above.E. None of the above.45. Arguments against the use of the shelf-registration are:A. only technology and manufacturing-based firms can use it.B. less current information available to investors might raise the cost of debt.C. possible market overhang from future issues depressing price.D. Both A and C.E. Both B and C.46. The market for venture capital refers to the:A. private financial marketplace for servicing small, young firms.B. bond markets.C. market for selling rights to individuals who already own shares.D. market for selling equity securities for firms with equity already outstanding.E. None of the above.47. Rule 144A provides the framework for the issuance of private securities to qualified institutional investors. To buy private securities, institutional investors:A. must be willing to hold a less liquid security and manage a fund.B. must be willing to make a market in the security and be a primary market dealer.C. must be a limited partner in the issue and willing to reduce the illiquidity of the security.D. must be willing to hold a less liquid security and have $100 million under management.E. None of the above.48. Venture capitalists provide financing for new firms from the seed and start-up stage all the way to mezzanine and bridge financing. In exchange for financing, entrepreneurs give:A. a high interest rate debt instrument and control.B. an equity position and usually board of director positions.C. up the right to have an initial public offering.D. control to a court appointed trustee.E. the venture capitalists jobs as CEOs and CFOs.49. An IPO of a firm formerly financed by venture capital is carried out for what primary purposes?A. Insiders can sell their shares or cash outB. Generate cash to pay down bank indebtednessC. To establish a market value for the equity and provide funds for operationsD. All of the above.E. None of the above.50. Which of the following is not one of the four main functions that underwriters provide?A. Risk bearingB. MarketingC. Auditing the financial statementsD. CertificationE. Monitoring51. Types of dilution include:A. dilution of percentage ownershipB. dilution of market shareC. dilution of book value and earnings per shareD. A and CE. All of the above52. The Wordsmith Corporation has 10,000 shares outstanding at $30 each. They expect to raise $150,000 by a rights offering with a subscription price of $25. How many rights must you turn in to get a new share?A. 0.60B. 1.20C. 1.67D. 2.00E. Insufficient data to determine53. Assuming everything else is constant, if a stock's old price is $25 and the ex-rights or new stock price is $19, then the value of the right is:A. $-6.B. $6.C. impossible to determine without the subscription price.D. impossible to determine without the number of rights needed to buy one share.54. The LaPorte Corporation has a new rights offering that allows you to buy one share of stock with 3 rights and $20 per share. The stock is now selling ex-rights for $26. The price rights-on is:A. $22.00B. $24.00C. $26.00D. $28.00E. impossible to determine without the cum-rights price.55. Regional Power wants to raise $10 million in new equity. The subscription price is $20. There are currently 3 million shares outstanding, each with 1 right. How many rights are needed to purchase 1 share?A. 1B. 3C. 5D. 6E. 856. The Overland Corporation intends to issue 50,000 new shares to raise funds for expansion of current plant facilities. The current share price is $40 and there are 500,000 shares outstanding. The number of rights needed to buy a share of stock should be:A. 1B. 10C. 40D. 400E. indeterminate without the subscription price.57. The Schroeder Corporation has 20,000 shares outstanding at $20 each. They expect to raise $200,000 by a rights offering with a subscription price of $25. How many rights must you turn in to get a new share?A. 1.25B. 1.50C. 2.00D. 2.50E. Insufficient data to determine58. Assuming everything else is constant, if a stock's old price is $40 and the ex-rights or new stock price is $32, then the value of the right is:A. $-8.B. $8.C. impossible to determine without the subscription price.D. impossible to determine without the number of rights needed to buy one share.59. The Holly Corporation has a new rights offering that allows you to buy one share of stock with 4 rights and $25 per share. The stock is now selling ex-rights for $30. The price rights-on is:A. $21.00B. $25.00C. $30.00D. $31.25E. impossible to determine without the cum-rights price.60. Bradley Power wants to raise $40 million in new equity. The subscription price is $25. There are currently 5 million shares outstanding, each with 1 right. How many rights are needed to purchase 1 share?A. 1.000B. 3.000C. 3.125D. 4.525E. 6.52561. The Shields Corporation intends to issue 100,000 new shares to raise funds for expansion of current plant facilities. The current share price is $20 and there are 500,000 shares outstanding. The number of rights needed to buy a share of stock should be:A. 1B. 5C. 20D. 50E. indeterminate without the subscription price.62. For a particular stock the old stock price is $20, the ex-rights price is $15, and the number of rights needed to buy a new share is 2. Assuming everything else constant, the subscription price is ______ .A. $5B. $13C. $17D. $18E. $20Essay QuestionsThe Holyoke Corporation has 120,000 shares outstanding with a current market price of $8.10 per share. The company needs to raise an additional $36,000 to finance new expenditures, and has decided on a rights issue. The issue will allow current stockholders to purchase one additional share for 20 rights at a subscription price of $6 per share.63. Calculate the ex-rights price that would make a new stockholder indifferent between buying shares at the old stock price and exercising the rights or buying the shares ex-rights.64. If the ex-rights price were set at $7.90, would you as a potential new stockholder choose to buy shares ex-rights or buy shares at the old price and exercise your rights?65. Suppose that the company was also considering structuring the rights issue to allow for an additional share to be purchased for 10 rights at a subscription price of $3. Prove that a stockholder with 100 shares would be indifferent between purchasing a new share for 10 rights at $3 or purchasing a new share for 20 rights at $6.66. Explain the advantages of a shelf-registration to an issuer. How can timeliness of disclosure and a potential market overhang work against a shelf-registration?67. The evidence on IPO sales is varied from issue to issue, but there are three common themes; underpricing, underperformance, and the reasons for going public. Explain these three themes.68. The Direct Interactive Publishing Company is planning to raise $200 million dollars in new capital. There are currently 50 million shares outstanding with an estimated market price of $60 each. The corporate officers are debating whether to use a rights offering (with or without a standby underwriting) or have the issue fully underwritten. The company is currently listed on a regional exchange and plans to list on a national exchange after the security issue. List and explain three advantages/disadvantages of each method.69. Discuss what a Dutch auction is and how it works.70. Lamar Inc. is attempting to raise $5,000,000 in new equity with a rights offering. The subscription price will be $40 per share. The stock currently sells for $50 per share and there are 250,000 shares outstanding. How many rights are needed to buy a new share?71. Lamar Inc. is attempting to raise $5,000,000 in new equity with a rights offering. The subscription price for the 125,000 new shares will be $40 per share. The stock currently sells for $50 per share and there are 250,000 shares outstanding. What will the price per share be if all rights are exercised?Chapter 20 Issuing Securities to the Public Answer KeyMultiple Choice Questions1. An equity issue sold directly to the public is called:A. a rights offer.B. a general cash offer.C. a restricted placement.D. a fully funded sales.E. a standard call issue.Difficulty level: EasyTopic: EQUITY ISSUEType: DEFINITIONS2. An equity issue sold to the firm's existing stockholders is called:A. a rights offer.B. a general cash offer.C. a private placement.D. an underpriced issue.E. an investment banker's issue.Difficulty level: EasyTopic: RIGHTS OFFERType: DEFINITIONS3. Management's first step in any issue of securities to the public is:A. to file a registration form with the SEC.B. to distribute copies of the preliminary prospectus.C. to distribute copies of the final prospectus.D. to obtain approval from the board of directors.E. to prepare the tombstone advertisement.Difficulty level: EasyTopic: SECURITY ISSUANCEType: DEFINITIONS4. A rights offering is:A. the issuing of options on shares to the general public to acquire stock.B. the issuing of an option directly to the existing shareholders to acquire stock.C. the issuing of proxies which are used by shareholders to exercise their voting rights.D. strictly a public market claim on the company which can be traded on an exchange.E. the awarding of special perquisites to management.Difficulty level: MediumTopic: RIGHTS OFFERINGType: DEFINITIONS5. Companies use tombstone advertisements in the financial press to:A. announce the death of the company.B. announce the failure of a financial strategy.C. announce the availability of a new issue of a corporate security.D. notify the public of foreclosure.E. None of the above.Difficulty level: EasyTopic: NEW ISSUANCEType: DEFINITIONS6. The first public equity issue made by a company is a(n):A. initial private offering.B. initial public offering.C. secondary offering.D. seasoned new issue.E. None of the above.Difficulty level: EasyTopic: INITIAL PUBLIC OFFERINGType: DEFINITIONS7. The first public equity issue that is made by a company is referred to as:A. a rights issue.B. a general cash offer.C. an initial public offering.D. an unseasoned issue.E. Both C and D.Difficulty level: MediumTopic: INITIAL PUBLIC OFFERINGType: DEFINITIONS8. A new public equity issue from a company with equity previously outstanding is called a(n):A. initial public offering.B. seasoned equity issue.C. unseasoned equity issue.D. private placement.E. syndicate.Difficulty level: EasyTopic: SEASONED EQUITY OFFERINGType: DEFINITIONS9. The green shoe option is used to:A. cover oversubscription.B. cover excess demand.C. provide additional reward to the investment bankers for a risky issue.D. provide additional reward to the issuing firm for a risky issue.E. Both A and B.Difficulty level: MediumTopic: GREEN SHOE PROVISIONType: DEFINITIONS。