国际经济学_理论与政策_课件_第12章V3.0

- 格式:ppt

- 大小:601.00 KB

- 文档页数:44

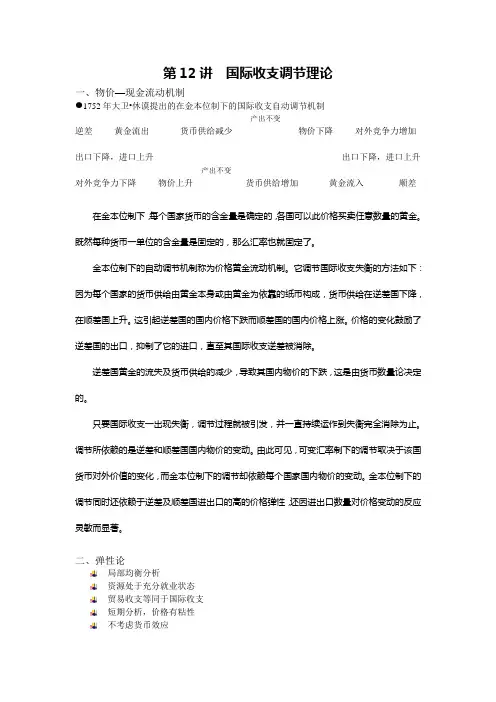

第12讲国际收支调节理论一、物价—现金流动机制1752年大卫•休谟提出的在金本位制下的国际收支自动调节机制产出不变逆差黄金流出货币供给减少物价下降对外竞争力增加出口下降,进口上升出口下降,进口上升产出不变对外竞争力下降物价上升货币供给增加黄金流入顺差在金本位制下,每个国家货币的含金量是确定的,各国可以此价格买卖任意数量的黄金。

既然每种货币一单位的含金量是固定的,那么汇率也就固定了。

金本位制下的自动调节机制称为价格黄金流动机制。

它调节国际收支失衡的方法如下:因为每个国家的货币供给由黄金本身或由黄金为依靠的纸币构成,货币供给在逆差国下降,在顺差国上升。

这引起逆差国的国内价格下跌而顺差国的国内价格上涨。

价格的变化鼓励了逆差国的出口,抑制了它的进口,直至其国际收支逆差被消除。

逆差国黄金的流失及货币供给的减少,导致其国内物价的下跌,这是由货币数量论决定的。

只要国际收支一出现失衡,调节过程就被引发,并一直持续运作到失衡完全消除为止。

调节所依赖的是逆差和顺差国国内物价的变动。

由此可见,可变汇率制下的调节取决于该国货币对外价值的变化,而金本位制下的调节却依赖每个国家国内物价的变动。

金本位制下的调节同时还依赖于逆差及顺差国进出口的高的价格弹性,还因进出口数量对价格变动的反应灵敏而显著。

二、弹性论局部均衡分析资源处于充分就业状态贸易收支等同于国际收支短期分析,价格有粘性不考虑货币效应不考虑收入效应通过进出口市场进行探讨货币贬值对国际收支的影响进出口市场运行机制外汇市场的需求来自于进口市场外汇市场的供给来自于出口市场小国情况——出口需求弹性和进口供给弹性无穷大出口需求弹性和进口需求弹性无穷大出口需求弹性和进口需求弹性为零出口供给弹性和进口供给弹性无穷大马歇尔—勒纳条件满足弹性论的基本条件进出口供给弹性无穷大最初的贸易是平衡的其他贸易国不进行贸易报复对外贬值的速度快于对内贬值的速度当进出口的供给曲线都是无限弹性,即水平的时候,此公式有效。

Chapter 12 第三题和第五题练习提示3. (a)Credit Debit An American buys a share of German stock(Financial account, U.S. asset import) -The American pays with a check on his Swiss bank account(Financial account, U.S. asset import) +(b) If the German stock seller deposits the U.S. check in its German bank,Credit Debit An American buys a share of German stock(Financial account, U.S. asset import) -The American pays with a check on his American bank account(Financial account, U.S. asset export) +(c)Credit Debit The sale of dollars by the Korean government(Financial account, U.S. asset export) -The Korean citizens who buy the dollars use them to buy American goods(Current account, U.S. goods export) +Credit Debit The sale of dollars by the Korean government(Financial account, U.S. asset export) -The Korean citizens who buy the dollars use them to buy American assets(Financial account, U.S. asset export) +(d) Suppose the company issuing the traveler’s check uses a checking account in France to make payments,Credit Debit The company issuing the traveler’s check pays the French restaurateur for the meal (Current account, U.S. service import) - Sale of claim on the company issuing the traveler’s check(Financial account, U.S. assets export) +(e)Credit Debit The California winemaker contributes a case of cabernet sauvignon abroad(Current account, U.S. unilateral current transfers) - Receivable of the California winemaker(Current account, U.S. goods export) +Credit Debit Receivable of the California winemaker(Current account, U.S. goods export) -The California winemaker contributes a case of cabernet sauvignon abroad(Current account, U.S. unilateral current transfers) +(f)Credit Debit The U.S. owned factory in Britain makes local earning(Current account, U.S. income receipts) +The U.S. owned factory in Britain deposits its local earning in a British bank(Financial account, U.S. asset import) -Credit Debit The U.S. owned factory in Britain uses its local earning to reinvest(Current account, U.S. income receipts) -The U.S. owned factory in Britain makes the payment for reinvestment(Financial account, U.S. asset import) +5.(a) Since Pecunia had a current account deficit of $1b and a nonreserve financial account surplus of $500m in 2002, the balance of Pecunia’s official reserve transaction should be +$500m as follow:Pecunia international transactionCredit Debit Current account -$1b Financial accountThe balance of Pecunia’s official reserve transaction +$500mThe balance of nonreserve assets +$500mThe balance of payment of Pecunia = the negative value of the balance of Pecunia’s official reserve transaction= -$500m.Pecunia had a financial account surplus of $1b in 2002; it implies Pecunia’s net foreign assets decreased by $1b in 2002.(b) Pecunian central bank had to sell $500m, so Pecunian central bank’s foreign reserves decreased by $500m:Pecunia international transactionCredit Debit Current account -$1b Financial accountPecunian official reserve assets +$500mForeign official reserve assets 0 0The balance of nonreserve assets +$500m(c) There was no need for Pecunian central bank to sell dollar, and Pecunian central bank’s foreign reserves increased by $100m as shown below:Pecunia international transactionCredit Debit Current account -$1b Financial accountPecunian official reserve assets -$100m Foreign official reserve assets + $600mThe balance of nonreserve assets +$500m(d)Pecunia international transactionCredit Debit Current account -$1b Financial accountPecunian official reserve assets -$100m Foreign official reserve assets + $600mThe balance of nonreserve assets +$500mThe following is for your reference:3.(a) The purchase of the German stock is a debit in the U.S. financial account. There is acorresponding credit in the U.S. financial account when the American pays witha check on his Swiss bank account because his claims on Switzerland fall by theamount of the check. This is a case in which an American trades one foreign assetfor another.(b) Again, there is a U.S. financial account debit as a result of the purchase of a Germanstock by an American. T he corresponding credit in this case occurs when theGerman seller deposits the U.S. check in its German bank and that bank lends themoney to a German importer (in which case the credit will be in the U.S. currentaccount) o r to an individual or corporation that purchases a U.S. asset (in whichcase the credit will be in the U.S. financial account). Ultimately, there will be someaction taken by the bank which results in a credit in the U.S. balance of payments.(c) The foreign exchange intervention by the French government involves the sale of aU.S. asset, the dollars it holds in the United States, and thus represents a debititem in the U.S. financial account. The French citizens who buy the dollars mayuse them to buy American goods, which would be an American current accountcredit,or an American asset, which would be an American financial accountcredit.(d) Suppose the company issuing the traveler’s check uses a checking account inFrance to make payments. When this company pays the French restaurateur for themeal, its payment represents a debit in the U.S. current account.The company issuing the traveler’s check must sell assets (deplete its checking account in France) to make this payment. This reduction in the French assetsowned by that company represents a credit in the American financial account.(e) There is no credit or debit in either the financial or the current account sincethere has been no market transaction.(f) There is no recording in the U.S. Balance of Payments of this offshore transaction.5.(a) Since non-central bank financial inflows fell short of the current-account deficit by$500 million, the balance of payments of Pecunia (official settlements balance) was–$500 million. The country as a whole somehow had to finance its $1 billioncurrent-account deficit, so Pecunia’s net foreign assets fell by $1 billion.(b) By dipping into its foreign reserves, the central bank of Pecunia financed theportion of the country’s current-account deficit not covered by private financialinflows. Only if foreign central banks had acquired Pecunian assets could thePecunian central bank have avoided using$500 million in reserves to complete the financing of the current account. Thus,Pecunia’s central bank lost $500 million in reserves, which would appear as anofficial financial inflow (of the same magnitude) in the country’s balance ofpayments accounts.(c) If foreign official capital inflows to Pecunia were $600 million, the Central Banknow increased its foreign assets by $100 million. Put another way, the countryneeded only $1 billion to cover its current-account deficit, but $1.1 billion flowed into the country (500 million private and600 million from foreign central banks). The Pecunian central bank must, therefore, have used the extra $100 million in foreign borrowing to increase its reserves. The balance of payments is still –500 million, but this is now comprised of 600 million in foreign Central Banks purchasing Pecunia assets and 100 million of Pecunia’s Central Bank purchasing foreign assets, as opposed to Pecunia selling 500 million in assets. Purchases of Pecunian assets by foreign central banks enter their countries’balance of payments accounts as outflows, which are debit items. The rationale is that the transactions result in foreign payments to the Pecunians who sell the assets.(d) Along with non-central bank transactions, the accounts would show an increase inforeign official reserve assets held in Pecunia of $600 million (a financial account credit, or inflow) and an increase Pecunian official reserve assets held abroad of $100 million (a financial account debit, or outflow). Of course, total net financial inflows of $1 billion just cover the current-account deficit.。