管理会计英文版

- 格式:pptx

- 大小:636.92 KB

- 文档页数:55

会计英语科目介绍1. Introduction在学习会计的过程中,学习和掌握会计英语是非常重要的。

会计英语科目是会计领域的专业术语,有助于我们理解和运用相关会计概念。

本文将介绍一些常见的会计英语科目及其英文表达,帮助读者更好地理解和掌握会计英语。

2. Financial Accounting(财务会计)财务会计是指对一个组织的财务状况和经营成果进行记录、分析和报告的过程。

以下是一些与财务会计相关的会计英语科目:2.1 Assets(资产)•Cash(现金)•Accounts receivable(应收账款)•Inventory(存货)•Property, Plant, and Equipment(固定资产)2.2 Liabilities(负债)•Accounts payable(应付账款)•Notes payable(应付票据)•Long-term debt(长期负债)2.3 Equity(所有者权益)•Common stock(普通股)•Retned earnings(留存盈余)2.4 Revenue(收入)•Sales revenue(销售收入)•Service revenue(服务收入)2.5 Expenses(费用)•Cost of goods sold(销售成本)•Rent expense(租金支出)3. Managerial Accounting(管理会计)管理会计是指用于内部决策、规划和控制的会计信息。

以下是一些与管理会计相关的会计英语科目:3.1 Cost(成本)•Direct costs(直接成本)•Indirect costs(间接成本)•Fixed costs(固定成本)•Variable costs(变动成本)3.2 Budgeting(预算)•Operating budget(经营预算)•Capital budget(资本预算)3.3 Decision Making(决策)•Cost-volume-profit analysis(成本-销售-利润分析)•Break-even point(盈亏平衡点)3.4 Performance Evaluation(绩效评估)•Return on investment(投资回报率)•Balanced scorecard(平衡记分卡)4. Auditing(审计)审计是指对财务报表的真实性、完整性和准确性进行独立检查和评估的过程。

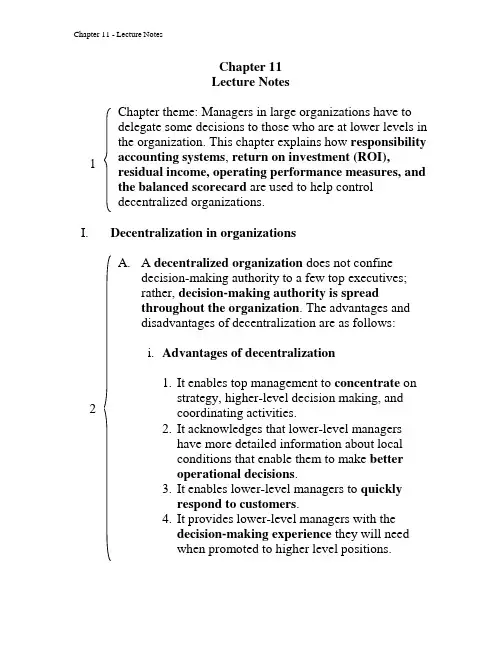

Chapter 11Lecture NotesChapter theme: Managers in large organizations have to Array delegate some decisions to those who are at lower levels inthe organization. This chapter explains how responsibilityaccounting systems, return on investment (ROI),residual income, operating performance measures, andthe balanced scorecard are used to help controldecentralized organizations.I.Decentralization in organizationsA. A decentralized organization does not confinedecision-making authority to a few top executives;rather, decision-making authority is spreadthroughout the organization. The advantages anddisadvantages of decentralization are as follows:i.Advantages of decentralization1.It enables top management to concentrate onstrategy, higher-level decision making, andcoordinating activities.2.It acknowledges that lower-level managershave more detailed information about localconditions that enable them to make betteroperational decisions.3.It enables lower-level managers to quicklyrespond to customers.4.It provides lower-level managers with thedecision-making experience they will needwhen promoted to higher level positions.5. It often increases motivation , resulting in increased job satisfaction and retention, as well as improved performance.ii. Disadvantages of decentralization1. Lower-level managers may make decisionswithout fully understanding the “big picture.”2. There may be a lack of coordination amongautonomous managers.a. The balanced scorecard can help reducethis problem by communicating acompany’s strategy throughout theorganization.3. Lower-level managers may have objectivesthat differ from those of the entireorganization.a. This problem can be reduced by designingperformance evaluation systems thatmotivate managers to make decisions thatare in the best interests of the company.4. It may be difficult to effectively spreadinnovative ideas in a strongly decentralizedorganization.II. Responsibility accountingA. Responsibility accounting systems link lower-levelmanagers’ decision -making authority withaccountability for the outcomes of those decisions.The term responsibility center is used for any part of an organization whose manager has control over, and is accountable for cost, profit, or investments. Thethree primary types of responsibility centers are cost centers, profit centers, and investment centers.i.Cost center1.The manager of a cost center hascontrol overcosts, but not over revenue or investment funds.a.Service departments such as accounting,general administration, legal, and personnelare usually classified as cost centers, as aremanufacturing facilities.b.Standard cost variances and flexiblebudget variances, such as those discussedin Chapters 10 and 11, are often used toevaluate cost center performance.ii.Profit center1.The manager of a profit center has control overboth costs and revenue.a.Profit center managers are often evaluatedby comparing actual profit to targeted orbudgeted profit.iii.I nvestment center1.The manager of an investment center hascontrol over cost, revenue, and investmentsin operating assets.b.Investment center managers are usuallyevaluated using return on investment (ROI)or residual income, as discussed later in thischapter.III. Evaluating investment center performance – return on investmentLearning Objective 1: Compute return on investment Array (ROI) and show how changes in sales, expenses, andassets affect ROI.A. Key concepts/definitionsi. Investment center performance is often evaluatedusing a measure called return on investment(ROI), which is defined as follows:Net operating incomeROIAverage operating assetsii. Net operating income is income before taxes and is sometimes referred to as EBIT (earnings beforeinterest and taxes). Operating assets include cash,accounts receivable, inventory, plant andequipment, and all other assets held for operatingpurposes.1. Net operating income is used in the numeratorbecause the denominator consists only ofoperating assets.2. The operating asset base used in the formula istypically computed as the average of the assetsbetween the beginning and the end of the year.iii. N et book value versus gross cost1. Most companies use thenet book value (i.e.,acquisition cost less accumulated depreciation)of depreciable assets to calculate averageoperating assets.a. With this approach, ROI mechanicallyincreases over time as the accumulateddepreciation increases. Replacing a fully-depreciated asset with a new asset willdecrease ROI.2. An alternative to net book value is the grosscost of the asset, which ignores accumulateddepreciation.a. With this approach, ROI does not growautomatically over time, rather it staysconstant. Replacing a fully-depreciatedasset does not adversely affect ROI.B. Understanding ROIi. Du Pont pioneered the use of ROI and recognizedthe importance of looking at the components ofROI, namely margin and turnover.1. Margin is computed as shown and is improvedby increasing unit sales, increasing sellingprices, or reducing operating expenses. Thelower the operating expenses per dollar of sales,the higher the margin earned.2. Turnover is computed as shown. It incorporates a crucial area of a manager’s responsibility – the investment in operating assets. Excessive funds tied up in operating assets depress turnover and lower ROI.Helpful Hint: Emphasize that both margin and turnover affect profitability. As an example, ask students tocompare the margins and turnovers of grocery stores to jewelry stores. In equilibrium, every industry should have roughly the same ROI. Groceries, because of their short shelf life, have high turnovers relative to fine jewelry. If the ROIs are to be comparable in grocery stores and in jewelry stores, the margins would have to be higher in jewelry stores.ii. To illustrate how to increase ROI, assume that Regal Company reports the results shown:1. Given this information, its current ROI is 15%.2. Suppose that Regal’s manager invests in a $30,000 piece of equipment that increases sales by $35,000 while increasing operating expenses by $15,000. a. In this case, the ROI increases from 15% to 21.8%.C. Criticisms of ROIi. Just telling managers to increase ROI may not beenough. Managers may not know how toincrease ROI in a manner that is consistent with the company’s strategy.1. This is why ROI is best used as part of abalanced scorecard.ii. A manager who takes over a business segment typically inherits many committed costs over which the manager has no control. This may make it difficult to assess this manager relative to other managers.iii. A manager who is evaluated based on ROI may reject investment opportunities that areprofitable for the whole company but that would have a negative impact on the manager’sperformance evaluation.Helpful Hint: When discussing the criticisms of ROI and other measures of profitability, ask students to play the role of a manager who anticipates a short tenure. This manager will want to increase ROI as quickly as possible. Ask students to list the activities that could be undertaken to increase ROI that, in reality, would hurt the company as a whole.IV. Residual incomeLearning Objective 2: Compute residual income and understand its strengths and weaknesses.A. Defining residual incomei. Residual income is the net operating income that an investment center earns above the minimum required return on its assets .B. Calculating residual incomei. The equation for computing residual income is asshown. Notice: 1. This computationdiffers from ROI. ROI measures net operating income earned relativeto the investment in average operating assets. Residual income measures net operating income earned less the minimum required return on average operating assets. ii. Zepher, Inc. - an example1. Assume the information as given for a division of Zepher, Inc.2. The residual income ($10,000) is computed by subtracting the minimum required return ($20,000) from the actual income ($30,000).C.Motivation and residual income i. The residual income approach encourages managers to make investments that are profitable for the entire company but that would be rejected by managers who are evaluated using the ROI formula. More specifically:1. It motivates managers to pursue investmentswhere the ROI associated with thoseinvestments exceeds the company’s minimumrequired return but is less than the ROI beingearned by the managers.Quick Check – ROI versus residual incomeD.Divisional comparison and residual income i.The residual income approach has one majordisadvantage. It cannot be used to compare the performance of divisions of different sizes.ii. Zepher, Inc. – continued1. Recall that the Retail Division of Zepher hadaverage operating assets of $100,000, aminimum required rate of return of 20%, netoperating income of $30,000, and residualincome of $10,000.2. Assume that the Wholesale Division of Zepherhad average operating assets of $1,000,000, aminimum required rate of return of 20%, netoperating income of $220,000, and residualincome of $20,000.3. The residual income numbers suggest that the Wholesale Division outperformed the Retail Division because its residual income is $10,000 higher. However: a. The Retail Division earned an ROI of30% compared to an ROI of 22% forthe Wholesale Division. TheWholesale Division’s residual incomeis larger than the Retail Divisionsimply because it is a bigger division .V.Operating performance measuresLearning Objective 3: Compute throughput time,delivery cycle time, and manufacturing cycle efficiency (MCE).A. Key definitions/conceptsi. Throughput (manufacturing cycle) time is theelapsed time from when production is started until finished goods are shipped to customers.1. This includes process time, inspection time, move time, and queue time . Process time is the only value-added activity of the fourmentioned.ii. Delivery cycle time is the elapsed time from whena customer order is received until the finished goods are shipped.iii. Manufacturing cycle efficiency (MCE) iscomputed by dividing value-added time by throughput time.1. The goal is to increase this measure.2. Any non-value-added time results in an MCE of less than 1.0.Quick Check – internal business process measures VI. Balanced scorecardLearning Objective 4: Understand how to construct and use a balanced scorecard.A. Key conceptsi. A balanced scorecard consists of an integratedset of performance measures that are derived from and support a company’s strategy. Importantly, the measures included in a company’s balanced scorecard are unique to its specific strategy . ii. The balanced scorecard enables top managementto translate its strategy into four groups of performance measures – financial, customer, internal business process, and learning and growth − that employees can understand and influence.1.The premise of these four groups of measuresis that learning is necessary to improveinternal business processes, which in turnimproves the level of customer satisfaction, which in turn improves financial results.a.Note the emphasis on improvement, notjust attaining some specific objective.iii.The balanced scorecard relies onnon-financial measures in addition to financial measures fortwo reasons:1.Financial measures are lag indicators thatsummarize the results of past actions. Non-financial measures are leading indicators offuture financial performance.2.Top managers are ordinarily responsible forfinancial performance measures – not lowerlevel managers. Non-financial measures aremore likely to be understood and controlledby lower level managers.iv.While the entire organization has an overall balanced scorecard, each responsible individualshould have his or her own personal scorecard as well.1.A personal scorecard should contain measuresthat can be influenced by the individual beingevaluated and that support the measures in theoverall balanced scorecard.v. A balanced scorecard, whether for an individualor the company as a whole, should have measures that are linked together on a cause-and-effect basis .1. Each link can be read as a hypothesis in the form “If we improve this performance measure, then this other performance measure shouldalso improve.”2. In essence, the balanced scorecard lays out a theory of how a company can take concrete actions to attain desired outcomes. If the theory proves false or the company alters its strategy, the measures within the scorecard are subject to change .vi. Incentive compensation for employeesprobably should be linked to balanced scorecard performance measures .1. However, this should only be done after the organization has been successfully managed with the scorecard for some time – perhaps a year or more . Managers must be confident that the measures are reliable, not easilymanipulated, and understandable by those being evaluated with them.B. The balanced scorecard – an example i. Assume that Jaguar pursues a strategy as shown on this slide. Examples of measures that Jaguar might select with their corresponding cause-and-effect linkages include:1. If “employee skills in installing options ” increases, then the “number of options available ” should increase and the “time to install an option ” should decrease.2. If the “number of options available ” increases and the “time to install an option” decreases, then “customer surveys: satisfaction with options available” should increase.3. If the “customer surveys: satisfaction with options available ” increases, then the “number of cars sold ” should increase.4. If the “time to install an option ” decreases and the “customer surveys: satisfaction with options available ” increases, then the “contribution margin per car ” should increase.5. If the “number of cars sold ” and the “contribution margin per car ” increase, then the “profit ” should incr ease.。

Chapter 6Lecture NotesChapter theme: Two general approaches are used for valuing inventories and cost of goods sold. One approach, called absorption costing , is generally used for external reporting purposes. The other approach, called variable costing , is preferred by some managers for internal decision making and must be used when an income statement is prepared in the contribution format . This chapter shows how these two methods differ from each other. It also explains how to create segmented contribution format income statements.I. Overview of variable and absorption costingLearning Objective 1: Explain how variable costing differs from absorption costing and compute unit product costsunder each method.Three simplifying assumptions are made in this chapter:i. Normal costing (rather than actual costing) is used (i.e., predetermined overhead rates are used to applyoverhead costs to product.ii. The actual number of units produced is used as theallocation base for assigning actual fixed manufacturingoverhead costs to products.iii. V ariable manufacturing costs per unit and the totalfixed manufacturing overhead cost per period remainconstant.2 3B. Variable costing treats only those costs of production that vary with output as product costs. This approach dovetails with the contribution approach income statement andsupports CVP analysis because of its emphasis onseparating variable and fixed costs.i. The cost of a unit of product consists of directmaterials, direct labor, and variable overhead .Helpful Hint: For simplicity, nearly all examples, exhibits, problems, and exercises in this chapter treat direct labor as a variable cost. However, students should be reminded that labor is essentially a fixed cost in some companies. This is a growing phenomenon as pointed out in earlier chapters.Under variable costing, direct labor would not be included in product costs when it is a fixed cost. This point is reinforced in the discussion on theory of constraints at the end of the chapter.ii. Fixed manufacturing overhead and both variable andfixed selling and administrative expenses are treated asperiod costs and deducted from revenue as incurred.Helpful Hint: Emphasize that the only difference between variable and absorption costing is in how the two methods treat fixed manufacturing overhead costs. Also, emphasize that under both methods, selling and administrative costs are period costs and are not product costs.C. Absorption costing treats all costs of production as product costs, regardless of whether they are variable or fixed. Since no distinction is made between variable and fixed costs,absorption costing is not well suited for CVP computations.i. The cost of a unit of product consists of directmaterials, direct labor, and both variable and fixedoverhead .ii. Variable and fixed selling and administrative expensesare treated as period costs and are deducted fromrevenue as incurred.Quick Check – absorption vs. variable costingII. Harvey Company —an exampleA. Unit cost computationsi. Assume Harvey Company produces a single product with available information as shown.ii. The unit product costs under absorption and variablecosting would be $16 and $10, respectively.1. Under absorption costing, all production costs ,variable and fixed, are included when determiningunit product cost.2. Under variable costing, only the variableproduction costs are included in product costs.Helpful Hint: Before beginning the forthcoming incomecomparisons, remind students of the relationship between ending inventory and net operating income. Higher ending inventory results in higher net operating income since costs of goods available for sale less ending inventory equals cost of goods sold. Therefore, a higher ending inventory results in a lower expense (cost of goods sold) deducted to arrive at net operating income.Learning Objective 2: Prepare income statements using both variable and absorption costing.B. Income comparison of variable and absorption costingi. Harvey Company —additional assumptions.1.20,000 units were sold during the year. 2.The selling price per unit is$30. 3. There isno beginning inventory. ii. Variable costing1. The unit product cost is $10.2. All $150,000 of fixed manufacturing cost is expensed in the current period.3. The net operating income is $90,000. iii. Absorption costing1. The unit product cost is $16.2. The fixed manufacturing overhead cost deferred in inventory is $30,000 (= 5,000 units × $6 per unit).3. The net operating income is $120,000.Helpful Hint: Explain that under absorption costing, therecognition of fixed costs as an expense is really a timing issue. When the items are sold, the fixed costs will bereflected on the income statement as part of cost of goods sold.Learning objective 3: Reconcile variable costing and absorption costing net operating incomes and explain whythe two amounts differ.iv. Comparing the two methods1. Under absorption costing, $120,000 of fixedmanufacturing overhead is included in cost of goodssold and $30,000 is deferred in ending inventory asan asset on the balance sheet.2. Under variable costing, the entire $150,000 of fixedmanufacturing overhead is treated as a periodexpense.a. The variable costing ending inventory is $30,000less than absorption costing , thus explaining thedifference in net operating income between thetwo methods.3. The difference in net operating income between thetwo methods ($30,000) can also be reconciled bymultiplying the number of units in ending inventory(5,000 units ) by the fixed manufacturing overheadper unit ($6) that is deferred in ending inventoryunder absorption costing.C. Extended comparisons of income datai. Harvey Company —additional assumptions/facts1. 30,000 units were sold in year2. 2. The selling price per unit, variable costs per unit,total fixed costs, and number of units producedremain unchanged .3. 5,000 units are in beginning inventory.ii. Unit cost computations1.Since the variable costs per unit, total fixed costs, and the number of units produced remained unchanged, the unit cost computations also remain unchanged. iii. Variable costing 1. The unit product cost is $10. 2. All $150,000 of fixed manufacturing overhead cost is expensed in the current period. 3. The net operating income is $260,000. iv. Absorption costing 1. The unit product cost is $16. 2. The fixed manufacturing overhead cost released from inventory is $30,000 (= 5,000 units × $6 per unit). 3. The net operating income is $230,000.v. Comparing the two methods 1. The difference in net operating income between the two methods ($30,000) can be reconciled by multiplying the number of units in beginning inventory (5,000 units ) by the fixed manufacturing overhead per unit ($6) that is released from beginning inventory under absorption costing.2. Across the two-year time frame, both methods reported the same total net operating income ($350,000). This is because over an extended period of time sales cannot exceed production, nor canproduction much exceed sales. The shorter the timeperiod, the more the net operating income figureswill tend to differ.D. Summary of key insightsi.Whenunits produced equals units sold, the twomethods report the same net operating income .ii. When units produced are greater than units sold , asin year 1 for Harvey, absorption net operating incomeis greater than variable costing net operating income . iii. When units produced are less than units sold , as inyear 2 for Harvey, absorption costing net operatingincome is less than variable costing net operatingincome .III. Advantages of variable costing and the contribution approachA. Enabling CVP analysisi. Variable costing categorizes costs as fixed and variable so it is much easier to use this income statement format for CVP analysis.ii.Absorption costing assigns per unit fixed manufacturing overhead costs to production. This can potentiallyproduce positive net operating income even whenthe number of units sold is less than the breakevenpoint.B. Explaining changes in net operating incomei.Variable costingnet operating income is only affectedby changes in unit sales. It is not affected by thenumber of units produced. As a general rule, when salesgo up net operating income goes up and vice versa.ii.Absorption costing net operating income is influenced by changes in unit sales and units of production. Netoperating income can be increased simply by producingmore units even if those units are not sold.D.Supporting decision makingi.Variable costing correctly identifies the additionalvariable costs incurred to make one more unit. Italso emphasizes the impact of fixed costs on profits.ii.Absorption costing gives the impression that fixed manufacturing overhead is variable with respect tothe number of units produced, but it is not. This canlead to inappropriate pricing decisions and productdiscontinuation decisions.IV. Segmented income statements and the contribution approach Learning Objective 4: Prepare a segmented incomestatement that differentiates traceable fixed costs fromcommon fixed costs and use it to make decisions.A.Key concepts/definitionsi. A segment is a part or activity of an organizationabout which managers would like cost, revenue, orprofit data.ii.Examples of segments include divisions of acompany, sales territories, individual stores, servicecenters, manufacturing plants, marketingdepartments, individual customers, and product lines.iii.There are two keys to building segmented income statements.1.First, a contribution format should be usedbecause it separates fixed from variable costsand it enables the calculation of a contributionmargin.a.The contribution margin is especially useful indecisions involving temporary uses ofcapacity such as special orders.2.Second, traceable fixed costs should be separatedfrom common fixed costs to enable thecalculation of a segment margin. Furtherclarification of these terms is as follows:a. A traceable fixed cost of a segment is a fixed cost that is incurred because of the existence of the segment. If the segment were eliminated, the fixed cost would disappear. Examples of traceable fixed costs include: (1). The salary of the Fritos product manager at PepsiCo is a traceable fixed cost of the Fritos business segment of PepsiCo. (2). The maintenance cost for the building in which Boeing 747s are assembled is a traceable fixed cost of the 747 business segment of Boeing.b. A common fixed cost is a fixed cost that supports the operations of more than one segment, but is not traceable in whole or in part to any one segment . Examples of common fixed costs include: (1). The salary of the CEO of General Motors is a common fixed cost of the various divisions of General Motors. (2). The cost of heating a Safeway or Kroger grocery store is a common fixed cost of the various departments – groceries, produce, bakery, etc. c. It is important to realize that the traceable fixed costs of one segment may be a common fixed cost of another segment . For example: (1). The landing fee paid to land an airplane atan airport is traceable to a particular flight, but it is not traceable to first-class, business-class, and economy-class passengers.Helpful Hint: In practice, a great deal of disagreement exists about what costs are traceable and what costs are common. Some people claim that except for direct materials, virtually all costs are common fixed costs that cannot be traced to products. Others assert that all costs are traceable toproducts; there are no common costs. The truth probably lies somewhere in the middle – many costs can be traced to products but not all costs.d. A segment margin is computed by subtracting the traceable fixed costs of a segment from itscontribution margin.(1). The segment margin is a valuable tool forassessing the long-run profitability of asegment.(2). Allocating common costs to segmentsreduces the value of the segment marginas a guide to long-run segmentprofitability.Helpful Hint: Explain that a segment should notautomatically be eliminated if its segment margin is negative. If a company that produces hair-styling productsdiscontinues its styling gel, sales on its shampoo and conditioner might fall due to the unavailability of the eliminated product.B. Segmented income statements – an examplei.Assume that Webber, Inc. has two divisions –the Computer Division and the Television Division.1. The contribution format income statement for the Television Division is as shown. Notice:a. Cost of goods sold consists of variable manufacturing costs.b. Fixed and variable costs are listed in separate sections .c. Contribution margin is computed by taking sales minus variable costs.d. The divisional segment margin represents the Television Division’s contribution to overall company profits. 2. The Television Division’s results can be rolled into Webber, Inc.’s overall results as shown. Notice: a. The results of the Television and Computer Divisions sum to the results shown for the whole company. b. The common costs for the company as a whole ($25,000) are not allocated to the divisions . 3. The Television Division’s results can also be broken down into smaller segments. This enables us to see how traceable fixed costs of the Television Division can become common costs of smaller segments . a. Assume that the Television Division can be broken down into two major product lines – Regular and Big Screen . b. Assume that the segment margins for these two product lines are as shown. c. Of the $90,000 of fixed costs that were previously traceable to the Television Division, $80,000 (= $45,000 + $35,000) is traceable to the two product lines and $10,000 is a common cost.C. Segmented income statements —decision making and break-even analysisi.To illustrate how the Television Division’s results can be used fordecision making, assume Webber believes that if the Television Division spends $5,000 additionaldollars on advertising it will increase sales of Regular and Big Screen televisions by 5%. Webber can compute the profit impact of this course of action as follows:1. The Regular product line contribution margin would increase by $5,250.2. The Big Screen product line contribution margin would increase by $2,250.3. The Television Division’s segment margin would increase by $2,500. Learning Objective 5: Compute companywide and segment break-even points for a company with traceable fixed costs. ii. To demonstrate how to calculate companywide and segmented break-even points , let’s refer back to the companywide income statement segmented into the Television and Computer Divisions. 1. The companywide break-even point is computed by dividing the sum of the company’s traceable fixed costs and common fixed costs by the company’s overall contribution margin ratio . a. This equation can be used to compute Webber’s companywide break-even point of $361,111.2. A business segment’s break-even point is computedby dividing its traceable fixed costs by itscontribution margin ratio.a. Using this equation, the break-even point for theTelevision Division is $180,000.b. The break-even point for the Computer Divisionis $133,333.3. Notice that the companywide common fixed costsare excluded from the segment break-evencalculations. This occurs because the common fixed costs are not traceable to segments and they are not influenced by segment-level decisions.Segmented income statements—common mistakesA.Omission of costsi.The costs assigned to a segment should include all thecosts attributable to that segment from the company’sentire value chain as discussed in Chapter 12.1.Since only manufacturing costs are included inproduct costs under absorption costing, thosecompanies that choose to use absorption costing forsegment reporting purposes will omit from theirprofitability analysis all “upstream” and“downstream” costs.a.“Upstream” costs include research anddevelopment and product design costs.b.“Downstream” costs include marketing,distribution, and customer service costs.c. Although these “upstream” and “downstream” costs are nonmanufacturing costs, they are just as essential to determining product profitability asare manufacturing costs. Omitting them fromprofitability analysis will result in theundercosting of products.Helpful Hint: An example of a company with a very high amount of upstream and downstream costs is apharmaceutical company such as Merck. A great deal of its costs are comprised of research and development and marketing.B. Inappropriate methods for assigning traceable costs to segmentsi.Failure to trace costs directly1. Costs that can be traced directly to specific segments of a company should not be allocated to othersegments . Rather, such costs should be chargeddirectly to the responsible segment. For example: a. The rent for a branch office of an insurancecompany should be charged directly against thebranch office rather than included in acompanywide overhead pool and then spreadthroughout the company.ii. Inappropriate allocation base1. Some companies allocate costs to segments using arbitrary bases . Costs should be allocated tosegments for internal decision making purposes only when the allocation base actually drives the cost being allocated. For example:a. Sales are frequently used to allocate selling and administrative expenses to segments. This should only be done if sales drive these expenses.C. Arbitrarily dividing common costs among segments i. Common costs should not be arbitrarily allocated to segments based on the rational e that “someone has to cover the common costs” for two reasons:1. First, this practice may make a profitable business segment appear to be unprofitable. If the segment is eliminated the revenue lost may exceed the real traceable costs that are avoided.2. Second, allocating common fixed costs forcesmanagers to be held accountable for costs that they cannot control.Quick Check – common costsV. Income statements—an external reporting perspectiveA. Companywide income statementsi.Practically speaking,absorption costing is requiredfor external reports in the United States. IFRS alsorequire absorption costing for external reports.ii.Probably because of the cost of maintaining twoseparate costing systems, most companies useabsorption costing for their external and internal reports.iii.W ith all of the advantages of the contribution approach, one may wonder why the absorption approach is used atall. Perhaps the biggest reason is because:1.Advocates of absorption costing argue that it bettermatches costs with revenues. They contend thatfixed manufacturing costs are just as essential tomanufacturing products as are the variable costs.2.Advocates of variable costing view fixedmanufacturing costs as capacity costs. They arguethat fixed manufacturing costs would be incurredeven if no units were produced.B. Segmented financial informationi. U.S. GAAP and IFRS require publicly-tradedcompanies to include segmented financial data intheir annual reports. These rulings have implications forinternal segment reporting because:.1. They mandate that companies must prepare external Array segmented reports using the same methods that theyuse for internal segmented reports. This requirement motivates managers to avoid using the contribution approach for internal reporting purposes because if they did they would be required to:a. Share this sensitive data with the public.b. Reconcile these reports with applicable rules forconsolidated reporting purposes.。