Chapter 28 - Investment Policy and the Framework of the CFA Institute

- 格式:doc

- 大小:124.50 KB

- 文档页数:65

CFA考试一级章节练习题精选0331-41附详解)1、Bruce Smith, CFA, covers East European equities for Marlborough Investments,an investment management firm with a strong presence in emerging markets.Forthe purpose of compliance with the Global Investments Performance Standards(GAPS?) , Marlborough Investments' total assets include:【单选题】A.only fee-paying discretionary assets.B.both fee-paying discretionary assets and non-fee-paying discretionary assets.C.all fee-paying and non-fee-paying, discretionary and nondiscretionary assets.正确答案:C答案解析:GAPS?规定公布的公司总资产里面既包含了支付费用的和不支付费用的资产,也包括了自由决断的和非自由决断的资产的市场价值。

2、Which of the following statements about the Global Investment PerformanceStandards ( GAPS?) is NOT accurate? The GAPS? standards require that acomposite:【单选题】A.is selected according to pre-established criteria.B.is an aggregation of one or more portfolios managed according to a similarinvestment mandate, objective or strategy.C.include a statement referring to the performance of a single, existing clientportfolio as being "calculated in accordance with the Global InvestmentPerformance Standards".正确答案:C答案解析:因为遵守GAPS?已经遵守其所规定的计算方法,所以无须说明“是根据GAPS?来计算的”。

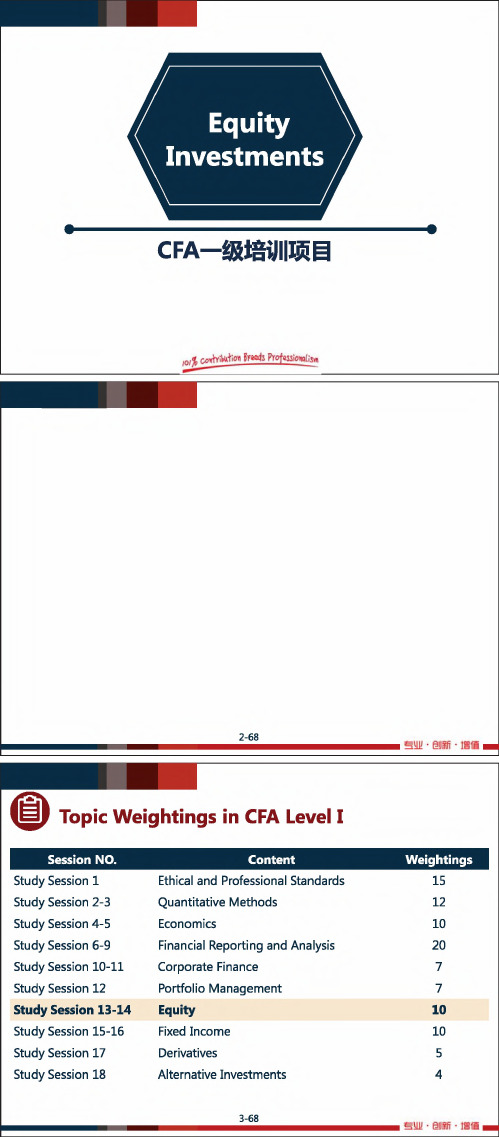

CFAlevelI、II、III级教材科目与章节一览高顿金融分析师汇聚全球金融圈成员,发现每一个优秀的你。

关注CFA协会将其官方教材电子版绑定在CFA报名费用之中,因此每一位CFA考生都会获得一份当期的电子版官方教材curriculum,当然大多数考生也需要纸质版,所以费用会增加170美元到考试报名里面,由于许多考生习惯使用Study Notes进行备考复习,因此对于CFA协会的官方教材了解不多,CFA协会教材curriculum各级别书名列出,以便考生备考使用。

CFA Level I 教材名称:Volume 1: Ethical and professional Standards, Quantitative MethodsVolume 2: EconomicsVolume 3: Financial StatementVolume 4: Corporate Finance and Portfolio ManagementVolume 5: Equity and Fixed IncomeVolume 6: Derivatives and Alternative InvestmentCFA一级教材名称译:第1卷:道德和专业标准,定量分析方法第2卷:经济学第3卷:财务报表第4卷:公司财务和投资组合管理第5卷:股票和固定收益第6卷:衍生工具和另类投资CFA Level II 教材名称:Volume 1: Ethical and professional Standards, Quantitative Methods, and EconomicsVolume 2: Financial Statement AnalysisVolume 3: Corporate FinanceVolume 4: Asset Valuation and EquityVolume 5: Fixed lncomeVolume 6: Derivatives and portfolio ManagementCFA二级教材名称译:第1卷:道德和专业标准,定量方法和经济学第2卷:财务报表分析第3卷:企业融资第4卷:资产评估和股权第5卷:固定lncome第6卷:衍生工具和投资组合管理CFA Level III 教材名称:Volume 1: Ethical and professional StandardsVolume 2:Behavioral Finance, individual investors, and institutional investorsVolume 3: Capital Market expectations, market valuation, and asset allocationVolume 4: Fixed income and equity portfolio managementVolume 5: Alternative investments, risk management, andthe application of derivativesVolume 6: Portfolio: Execution, evaluation and attribultion, and global investment performance standardsCFA三级教材名称译:第1卷:道德和专业标准第2卷:行为金融,个人投资者和机构投资者第3卷:资本市场的预期,市场估值和资产配置第4卷:固定收益和股票投资组合管理第5卷:另类投资,风险管理,衍生品的应用第6卷:组合:执行,评估和attribultion,以及全球投资表现标准▎本文由高顿金融分析师微信进行整理。

COOPERATION AND FACILITATION INVESTMENT AGREEMENT BETWEEN THE FEDERATIVE REPUBLIC OF BRAZIL ANDThe Federative Republic of Braziland(hereinafter designated as the “Parties”or individually as “Party”),PREAMBLEWishing to strengthen and to enhance the bonds of friendship and the spirit of continuous cooperation between the Parties;Seeking to create and maintain favourable conditions for the investments of investors of a Party in the territory of the other Party;Seeking to stimulate, streamline and support bilateral investments, thus opening new integration opportunities between the Parties;Recognizing the essential role of investment in promoting sustainable development;Considering that the establishment of a strategic partnership between the Parties in the area of investment will bring wide-ranging and mutual benefits;Recognizing the importance of fostering a transparent and friendly environment for investments by investors of the Parties;Reassuring their regulatory autonomy and policy space;Wishing to encourage and strengthen contacts between the private sectors and the Governments of the two countries; andSeeking to create a mechanism for technical dialogue and foster government initiatives that may contribute to a significant increase in mutual investment;Agree, in good faith, to the following Cooperation and Facilitation Investment Agreement, hereinafter referred to as “Agreement”, as follows:PART I – Scope of the Agreement and DefinitionsArticle 1Objective1.The objective of this Agreement is to promote cooperation between the Parties in order to facilitate and encourage mutual investment, through the establishment of a an institutional framework for the management of an agenda for further investment cooperation and facilitation, as well as through mechanisms for risk mitigation and prevention of disputes, among other instruments mutually agreed on by the Parties.Article 2Scope and Coverage1. This Agreement shall apply to all investments made before or after its entry into force.2. This Agreement shall not limit the rights and benefits which an investor of a Party enjoys under national or international law in the territory of the other Party.3. For greater certainty, the Parties reaffirm that this Agreement shall apply without prejudice to the rights and obligations derived from the Agreements of the World Trade Organization.4. This agreement shall not prevent the adoption and implementation of new legal requirements or restrictions to investors and their investments, as long as they are consistent with this Agreement.Article 3Definitions1. For the purpose of this Agreement:1.1 Enterprise means: any entity constituted or organized under applicable law, whether or not for profit, whether privately owned or State--owned, including any corporation, trust, partnership, sole proprietorship, joint venture and entities without legal personality;1.2 Host State means the Party where the investment is made.1.3 Investment means a direct investment of an investor of one Party, established or acquired in accordance with the laws and regulations of the other Party, that s, directly or indirectly, allows the investor to exert control or significant degree of influence over the management of the production of goods or provision of services in the territory of the other Party, including but not limited to:a)an enterprise;b)shares, stocks, participations and other equity types in an enterprise;c) movable or immovable property and other property rights such as mortgages,liens, pledges, encumbrances or similar rights and obligations;d) concession, license or authorization granted by the Host State to the investor ofthe other Party;e) loans and debt instruments to a company:f) intellectual property rights as defined or referenced to in the Trade-RelatedAspects of Intellectual Property Rights of the World Trade Organization(TRIPS)For the purposes of this Agreement and for greater certainty, "Investment" does not include:i) an order or judgment issued as a result of a lawsuit or an administrative process;ii) debt securities issued by a Party or loans granted from a Party to the other Party,bonds, debentures, loans or other debt instruments of a State-owned enterprise of aParty that is considered to be public debt under the legislation of that Party;ii) portfolio investments, i.e., those that do not allow the investor to exert asignificant degree of influence in the management of the company; andiii) claims to money that arise solely from commercial contracts for the sale ofgoods or services by an investor in the territory of a Party to a national or anenterprise in the territory of another Party, or the extension of credit in connectionwith a commercial transaction, or any other claims to money that do not involve thekind of interests set out in sub-paragraphs (a)-(e) above.1.4 Investor means a national, permanent resident or enterprise of a Party that has made an investment in the territory of the other Party;1.5 Income means the values obtained by an investment, including profits, interests, capital gains, dividends or "royalties".1.6 Measure means any measure adopted by a Party, whether in the form of law, regulation, rule, procedure, decision, administrative ruling, or any other form.1.7 National means a natural person that has the nationality of a Party, according to its laws and regulations.1.8 Territory means the territory, including its land and aerial spaces, the exclusive economic zone, territorial sea, seabed and subsoil within which the Party exercises its sovereign rights or jurisdiction, in accordance with international law and its internal legislation.PART II – Regulatory Measures and Risk MitigationArticle 4Admission and treatment1. Each Party shall admit and encourage investments of investors of the other Party, according to their respective laws and regulations.2. Each Party shall grant to investments and investors of the other Party treatment according to the due process of law.3. In line with the principles of this Agreement, each Party shall ensure that all measures that affect investment are administered in a reasonable, objective and impartial manner, in accordance with their respective laws and regulations.Article 5National Treatment1. Without prejudice to the exceptions in force under its legislation on the date of entry into force of this Agreement, each Party shall accord to investors of another Party treatment no less favourable than that it accords, in like circumstances, to its own investors with respect to the expansion, management, conduct, operation, and sale or other disposition of investments in its territory.2. Without prejudice to the exceptions in force under its legislation on the date of entry into force of this Agreement, each Party shall accord to investments of investors of the other Party treatment no less favourable than that it accords, in like circumstances, to investments in its territory of its own investors with respect to the expansion, management, conduct, operation, and sale or other disposition of investments.3. For greater certainty, whether treatment is accorded in ‘like circumstances’ depends on the totality of the circumstances, including whether the relevant treatment distinguishes between investors or investments on the basis of legitimate public interest objectives.4. For greater certainty, this Article shall not be construed to require any Party to compensate for any inherent competitive disadvantages which result from the foreign character of the investor or investments.Article 6Most-Favoured-Nation Treatment1. Each Party shall accord to investors of another Party treatment no less favourable than that it accords, in like circumstances, to investors of any non-Party with respect to the expansion, management, conduct, operation, and sale or other disposition of investments in its territory.2. Each Party shall accord to investments of investors of the other Party treatment no less favourable than that it accords, in like circumstances, to investments in its territory of investors of any non-Party with respect to the expansion, management, conduct, operation, and sale or other disposition of investments.3. This Article shall not be construed to require a Party to grant to an investor of another Party or their investments the benefit of any treatment, preference or privilege arising from:(i) provisions relating to investment dispute settlement contained in an investmentagreement or an investment chapter of a commercial agreement; or(ii) any agreement for regional economic integration, free trade area, customs unionor common market, of which a Party is a member .4. For greater certainty, whether treatment is accorded in ‘like circumstances’ depends on the totality of the circumstances, including whether the relevant treatment distinguishes between investors or investments on the basis of legitimate public welfare objectives.Article 7Expropriation1. Each Party shall not directly nationalize or expropriate investments of investors of the other Party, except:a) for a public purpose or necessity or when justified as social interest;b) in a non-discriminatory manner;c) on payment of effective compensation, according to paragraphs 2 to 4; andd) in accordance with due process of law.2. The compensation shall:a) Be paid without undue delay;b) Be equivalent to the fair market value of the expropriated investment,immediately before the expropriating measure has taken place (“expropriationdate”);c) Not reflect any change in the market value due to the knowledge of theintention to expropriate, before the expropriation date; andd) Be completely payable and transferable, according to Article 9.3. The compensation to be paid shall not be inferior to the fair market value on the expropriation date, plus interests at a rate determined according to market criteria accrued since the expropriation date until the date of payment, according to the legislation of the Host State.4. The Parties shall cooperate to improve the mutual knowledge of their respective national legislations regarding investment expropriation.5. For greater certainty, this article only provides for direct expropriation, where an investment is nationalized or otherwise directly expropriated through formal transfer of title or ownership rights.Article 8Compensation for Losses1. The investors of a Party whose investments in the territory of the other Party suffer losses due to war or other armed conflict, revolution, state of emergency, insurrection, riot or any other similar events, shall enjoy, with regard to restitution, indemnity or other form of, compensation, the same treatment as the latter Party accords to its own investors or the treatment accorded to investors of a third party, whichever is more favourable to the affected investor.2. Each Party shall provide the investor restitution, compensation, or both, as appropriate, in accordance with Article 6 of this Agreement, in the event that investments suffer losses in its territory in any situation referred to in paragraph 1 resulting from:(a) requisitioning of its investment or part thereof by the forces or authorities of thelatter Party; or(b) destruction of its investment or any part thereof by the forces or authorities ofthe latter Party.Article 9Transparency1. Each Party shall ensure that its laws, regulations, procedures and general administrative resolutions related to any matter covered by this Agreement, in particular regarding qualification, licensing and certification, are published without delay and, when possible, in electronic format, as to allow interested persons of the other Party to be aware of such information.2. Each Party shall endeavour to allow reasonable opportunity to those stakeholders interested in expressing their opinions on the proposed measures.3. Whenever possible, each Party shall publicize this Agreement to their respective public and private financial agents, responsible for the technical evaluation of risks and the approval of loans, credits, guarantees and related insurances for investment in the territory of the other Party.Article 10Transfers1. Each Party shall allow that the transfer of funds related to an investment be made freely and without undue delay, to and from their territory. Such transfers include:(a) the initial capital contribution or any addition thereof in relation to themaintenance or expansion of such investment;(b) income directly related to the investment;(c) the proceeds of sale or total or partial liquidation of the investment;(d) the repayments of any loan, including interests thereon, relating directly to theinvestment;(e) the amount of a compensation.2. Without prejudice to paragraph 1, a Party may, in an equitable and non-discriminatory manner and in good faith, prevent a transfer if such transfer is prevented under its laws relating to:(a)bankruptcy, insolvency or the protection of the rights of creditors;(b)criminal infractions;(c)financial reports or maintenance of transfers' registers when necessary tocooperate with law enforcement or with financial regulators; or(d) the guarantee for the enforcement of decisions in judicial or administrativeproceedings.3.. Nothing in this Agreement shall be construed as to prevent a Party from adopting or maintaining temporary restrictive measures in respect of payments or transfers for current account transactions in the event of serious difficulties in the balance of payments and external financial difficulties or threat thereof.4. Nothing in this Agreement shall be construed as to prevent a Party from adopting or maintaining temporary restrictive measures in respect of payments or transfers related to capital movements:(a) in the case of serious difficulties in the balance of payments or externalfinancial difficulties or threat thereof; or(b) where, in exceptional circumstances, payments or transfers from capitalmovements generate or threaten to generate serious difficulties for macroeconomicmanagement.5. The adoption of temporary restrictive measures to transfers if there are serious difficulties in the balance of payments in the cases described in paragraphs 1 and 2, must be non-discriminatory and in accordance with the Articles of the Agreement of the International Monetary Fund.Article 11Tax Measures1. No provision of this Agreement shall be interpreted as an obligation of one Party to give to an investor from the other Party, concerning his or her investments, the benefit of any treatment, preference or privilege arising out of any agreement to avoid double taxation, current or future, of which a Party to this Agreement is a party or becomes a party.2. No provision of this Agreement shall be interpreted in a manner that prevents the adoption or implementation of any measure aimed at ensuring the equitable or effective imposition or collection of taxes, according to the Parties´ respective laws and regulations, so long as such a measure is not applied as to constitute a means of arbitrary or unjustifiable discrimination or a disguised restriction.Article 12Prudential Measures1. Nothing in this Agreement shall be construed to prevent a Party from adopting or maintaining prudential measures, such as:(a)the protection of investors, depositors, financial market participants, policy-holders,policy-claimants, or persons to whom a fiduciary duty is owed by a financial institution;(b)the maintenance of the safety, soundness, integrity or financial responsibility of financialinstitutions; and(c)ensuring the integrity and stability of a Party's financial system.2. Where such measures do not conform with the provisions of this Agreement, they shall not be used as a means of circumventing the commitments or obligations of the Party under this Agreement.Article 13Security Exceptions1. Nothing in this Agreement shall be construed to prevent a Party from adopting or maintaining measures aimed at preserving its national security or public order, or to apply the provisions of their criminal laws or comply with its obligations regarding the maintenance of international peace and security in accordance with the provisions of the United Nations Charter.2. Measures adopted by a Party under paragraph 1 of this Article or the decision based on national security laws or public order that at any time prohibit or restrict the realization of an investment in its territory by an investor of another Party shall not be subject to the dispute settlement mechanism under this Agreement.Article 14Corporate Social Responsibility1. Investors and their investment shall strive to achieve the highest possible level of contribution to the sustainable development of the Host State and the local community, through the adoption of a high degree of socially responsible practices, based on the voluntary principles and standards set out in this Article.2. The investors and their investment shall endeavour to comply with the following voluntary principles and standards for a responsible business conduct and consistent with the laws adopted by the Host State receiving the investment:a) Contribute to the economic, social and environmental progress, aiming atachieving sustainable development;b) Respect the internationally recognized human rights of those involved in thecompanies’ activitie s;c) Encourage local capacity building through close cooperation with the localcommunity;d) Encourage the creation of human capital, especially by creating employmentopportunities and offering professional training to workers to;e) Refrain from seeking or accepting exemptions that are not established in thelegal or regulatory framework relating to human rights, environment, health,security, work, tax system, financial incentives, or other issues;f) Support and advocate for good corporate governance principles, and developand apply good practices of corporate governance;g) Develop and implement effective self-regulatory practices and managementsystems that foster a relationship of mutual trust between the companies and thesocieties in which its operations are conducted;h) Promote the knowledge of and the adherence to, by workers, the corporatepolicy, through appropriate dissemination of this policy, including programs forprofessional training;i) Refrain from discriminatory or disciplinary action against employees whosubmit grave reports to the board or, whenever appropriate, to the competentpublic authorities, about practices that violate the law or corporate policy;j) Encourage, whenever possible, business associates, including service providers and outsources, to apply the principles of business conduct consistent with theprinciples provided for in this Article; andk) Refrain from any undue interference in local political activities.Article 15Investment Measures and Combating Corruption and Illegality1. Each Party shall adopt measures and make efforts to prevent and fight corruption, money laundering and terrorism financing with regard to matters covered by this Agreement, in accordance with its laws and regulations.2. Nothing in this Agreement shall require any Party to protect investments made with capital or assets of illicit origin or investments in the establishment or operation of which illegal acts have been demonstrated to occur and for which national legislation provides asset forfeiture.Article 16Provisions on Investment and Environment, Labor Affairs and Health1. Nothing in this Agreement shall be construed to prevent a Party from adopting, maintaining or enforcing any measure it deems appropriate to ensure that investment activity in its territory is undertaken in a manner according to labor, environmental and health legislations of that Party, provided that this measure is not applied in a manner which would constitute a means of arbitrary or unjustifiable discrimination or a disguised restriction.2. The Parties recognize that it is inappropriate to encourage investment by lowering the standards of their labor and environmental legislation or measures of health. Therefore, each Party guarantees it shall not amend or repeal, nor offer the amendment or repeal of such legislation to encourage the establishment, maintenance or expansion of an investment in itsterritory, to the extent that such amendment or repeal involves decreasing their labor, environmental or health standards. If a Party considers that another Party has offered such an encouragement, the Parties will address the issue through consultations.PART III- Institutional Governance and Dispute PreventionArticle 17Joint Committee for the Administration of the Agreement1. For the purpose of this Agreement, the Parties hereby establish a Joint Committee for the administration of this Agreement (hereinafter referred as “Joint Committee”).2. This Joint Committee shall be composed of government representatives of both Parties designated by their respective Governments.3. The Joint Committee shall meet at such times, in such places and through such means as the Parties may agree. Meetings shall be held at least once a year, with alternating chairmanships between the Parties.4. The Joint Committee shall have the following functions and responsibilities:a) Supervise the implementation and execution of this Agreement;b) Discuss and divulge opportunities for the expansion of mutual investment;c) Coordinate the implementation of the mutually agreed cooperation andfacilitation agendas;d) Consult with the private sector and civil society, when applicable, on theirviews on specific issues related to the work of the Joint Committee;e) Seek to resolve any issues or disputes concerning investments of investors of aParty in an amicable manner; andf) Supplement the rules for arbitral dispute settlement between the Parties.5. The Parties may establish ad hoc working groups, which shall meet jointly or separately from the Joint Committee.6. The private sector may be invited to participate in the ad hoc working groups, whenever authorized by the Joint Committee.7. The Joint Committee shall establish its own rules of procedure.Article 18Focal Points or “Ombudsmen”1. Each Party shall designate a National Focal Point, or “Ombudsm a n”, which shall have as its main responsibility the support for investor from the other Party in its territory.2. In Brazil, the “Ombudsman”/National Focal Point shall be within the Chamber of Foreign Trade – CAMEX1.3. In, the “Ombudsman”/National Focal Point shall be .4. The National Focal Point, among other responsibilities, shall:a) Endeavour to follow the recommendations of the Joint Committee and interactwith the National Focal Point of the other Party, in accordance with thisAgreement;b) Follow up on requests and enquiries of the other Party or of investors of theother Party with the competent authorities and inform the stakeholders on theresults of its actions;c) to assess, in consultation with relevant government authorities, suggestions andcomplaints received from the other Party or investors of the other Party andrecommend, as appropriate, actions to improve the investment environment;d) seek to prevent differences in investment matters, in collaboration withgovernment authorities and relevant private entities;e) Provide timely and useful information on regulatory issues on generalinvestment or on specific projects; andf) Report its activities and actions to the Joint Committee, when appropriate.5. Each Party shall determine time limits for the implementation of each of its functions and responsibilities, which will be communicated to the other Party.6. Each Party shall designate a single agency or authority as its National Focal Point, which shall give prompt replies to notifications and requests by the Government and investors from the other Party.Article 19Exchange of Information between Parties1.The Parties shall exchange information, whenever possible and relevant to reciprocal investments, concerning business opportunities, procedures, and requirements for investment, particularly through the Joint Committee and its National Focal Points.2. For this purpose, the Party shall provide, when requested, in a timely fashion and with respect for the level of protection granted, information related, in particular, to the following items:a) Regulatory conditions for investment;b) Governmental programs and possible related incentives;1 The Chamber of Foreign Trade (CAMEX) is part of the Government Council of the Presidency of the Federative Republic of Brazil. Its main body is the Council of Ministers, which is an interministerial body.c) Public policies and legal frameworks that may affect investment;d) Legal framework for investment, including legislation on the establishment ofcompanies and joint ventures;e) Related international treaties;f) Customs procedures and tax regimes;g) Statistical information on the market for goods and services;h) Available infrastructure and public services;i) Governmental procurement and public concessions;j) Social and labour requirements;k) Immigration legislation;l) Currency exchange legislation;m) Information on legislation of specific economic sectors or segments previously identified by the Parties; andn) Regional projects and agreements related to on investment.3. The Parties shall also exchange information on Public-Private Partnerships (PPPs), especially through greater transparency and quick access to the information on the legislation.Article 20Treatment of Protected Information1. The Parties shall respect the level of protection of information provided by the submitting Party, according to the respective national legislation on the matter.2. None of the provisions of the Agreement shall be construed to require any Party to disclose protected information, the disclosure of which would jeopardize law enforcement or otherwise be contrary to the public interest or would violate the privacy or harm legitimate business interests. For the purposes of this paragraph, protected information includes confidential business information or information considered privileged or protected from disclosure under the applicable laws of a Party.Article 21Interaction with the Private SectorRecognizing the key role played by the private sector, the Parties shall publicize, among the relevant business sectors, general information on investment, regulatory frameworks and business opportunities in the territory of the other Party.Article 22Cooperation between Agencies Responsible for Investment PromotionThe Parties shall promote cooperation between their investment promotion agencies in order to facilitate investment in the territory of the other Party.Article 23Disputes Prevention1. The National Focal Points, or “Ombudsmen”, shall act in coordination with each other and with the Joint Committee in order to prevent, manage and resolve any disputes between the Parties.2. Before initiating an arbitration procedure, in accordance with Article 24 of this Agreement, any dispute between the Parties shall be the object of consultations and negotiations between the Parties and be previously examined by the Joint Committee.3. A Party may submit a specific question and call a meeting of the Joint Committee according to the following rules:a) to initiate the procedure, the interested Party must submit a written request tothe other Party, specifying the name of the affected investors, the specificmeasure in question, and the findings of fact and law underlying the request.The Joint Committee shall meet within sixty (60) days from the date of therequest;b) The Joint Committee shall have 60 days, extendable by mutual agreement by 60additional days, upon justification, to evaluate the relevant information aboutthe presented case and to submit a report. The report shall include:i) Identification of the Party;ii) Identification of the affected investors, as presented by the Parties;iii) Description of the measure under consultation; andiv) Conclusions of the consultations between the Parties;.c) In order to facilitate the search for a solution between the Parties, wheneverpossible, the following persons shall participate in the bilateral meeting:i) Representatives of the affected investors;ii) Representatives of the governmental or non-governmental entities involved in the measure or situation under consultation.d) The procedure for dialogue and bilateral consultations may be concluded byany Party, after the sixty (60) days referred to in subparagraph b). The JointCommittee shall present its report in the subsequent meeting of the JointCommittee, which shall be held no later than fifteen (15) days after the date of。

Portfolio ManagementPortfolio Management: An OverviewDescribe the portfolio approach to investing1.The portfolio perspective refers to evaluating individual investments by theircontribution on the risk and return of an investor’s portfolio.投资组合视角指的是通过投资组合对风险和回报的贡献来评估个人投资。

2.把所有钱用于买一只股票并不是一种portfolio perspective,把钱分散在多只证券中才能降低风险,增加收益。

3.One measure of the benefits of diversification is the diversification ratio. It iscalculated as the ratio of the risk of an equally weighted portfolio of n securities to the risk of a single security selected at random from the n securities.衡量多样化的好处之一是多样化比率。

它计算的是n证券等加权组合的风险与随机从n证券中选择的单一证券的风险之比。

4.If the average standard deviation of returns for the n stocks is 25%, and thestandard deviation of returns for an equally weighted portfolio of the n stocks is 18%, the diversification ratio is 18/25=0.72.Describe types of investors and distinctive characteristics and needs of each1.Individual investor个人投资者就是个人为了满足生活目标而进行理财的投资者,是牺牲当前消费以期获得未来更高水平消费的个人。

CFA一、二级练习题精选及答案0516-10CFA Level I1.Alan Quanta, CFA, provides credit rating analysis of high-yield bonds using external credit ratings as a foundation. At the end of the last quarter, Quanta's firm, North Investment Bank, held a large position in the bonds of Veyron Corporation, a real estate company with all of its land holdings in a country recently downgraded by several credit rating agencies. The downgrades made Veyron bonds extremely difficult to sell because the bond price has dropped every day since the downgrades. Quanta has been asked by his supervisor to contact institutional clients of the firm to convince them that Veyron bonds are still an attractive purchase, especially at these lower prices. Quanta does not consider the Veyron bonds a buy at this price level. According to the CFA Institute Code of Ethics and Standards of Professional Conduct, the most appropriate action for Quanta is toA. obey his supervisor's request.B. ignore his supervisor's request.C. promote the bonds with appropriate disclosures.Correct answer: B"Guidance for Standards I–VII," CFA Institute2013 Modular Level I, Vol. 1, Reading 2, Standard I (B) Independence and Objectivity, GuidanceStudy Session 1-2-bDistinguish between conduct that conforms to the CFA Institute Code of Ethics and Standards of Professional Conduct and conduct that violates the Code and Standards.B is correct. Quanta should refuse to promote the bonds, which he does not rate as a buy, because his opinion of the Veyron bonds must not be affected by internal pressure or compensation. If Quanta followed the request from his supervisor, he would be in violation of Standard I (B) Independence and Objectivity. Quanta must refuse to promote Veyron bonds until they are an attractive purchase based on fundamental analysis and market pricingCFA Level II1-6:The government of a developing countrypublished a Request for Proposal (RFP) for the development of policies toimprove the business conduct of its capital markets licensees with the hope ofimproving confidence levels among investors.Kingfisher Financial Development Partnersresponded with a detailed proposal including the following justifications forwhy the firm should win the tender.Justification1:With a team of three CFAcharterholders, Kingfisher is more qualified than our competitors to designpolicies to uphold and enhance capital market integrity. Justification2:Each team member must annually renewhis or her commitment to abide by the CFA Institute Code of Ethics and Standardsof Professional Conduct.Justification 3:In addition, every team member passed the CFAexams on the first try.Later, Kingfisher was notified that it wonthe tender. Kingfisher's team consists of team leader Khalid Juma, CFA, and histwo associates, Vimal Bachu, CFA, and Anila Patel, CFA. Kingfisher and thegovernment agree the first step to improve market integrity is to create anindustrywide Code of Conduct based on the CFA Institute Code of Ethics andStandards of Professional Conduct. Although the Code and Standards are notadopted in full, the decision is made to concentrate on four main areas:Professionalism, Capital Market Integrity, Duties to Clients, and InvestmentRecommendations.The Kingfisher team subsequently drafts thefollowing policy statements:Levelsof ProfessionalismFinancial services professionals must actin a professional manner at all times to help protect the integrity of thecountry's capital markets. As such, financial services professionals mustensure they meet, at a minimum, three major requirements. Professionals must:(1) disclose all conflicts of interest; (2) selectively differentiate servicesto clients; and (3) outline all manager compensationarrangements for clients.CapitolMarket IntegrityFinancial services professionals mustprotect the integrity of the capital markets by ensuring that any insiderinformation obtained is managed in such a way as to prevent the generalinvesting public from being disadvantaged. In addition, no financial servicesprofessional can knowingly participate in any activity devised to misleadinvestors or distort any price-setting mechanism.Dutiesto ClientsClients' interests must come before thoseof the financial services firm and/or its staff. To ensure clients' interestsare protected,all portfolios must be invested according to each client'sinvestment plan and must be well diversified across all asset classesavailable. Furthermore, fund managers must annually review client needs andobjectives and rebalance portfolios if required.InvestmentRecommendationsAll investment recommendations should bemade after extensive research undertaken by or on behalf of the firm. Inaddition, each research report must:Requirement 1:be reviewed by peers as soon as practical to ensure that adequate basisand due diligence policies,were followed;Requirement 2:be assessed to determine the quality of the recommendation over time;andRequirement 3:name only those team members who took part in the research and agreedwith the recommendation.The Kingfisher team and the governmentcommittee meet to agree on the draft Code. Members of the government committeesuggest an additional policy "Each financial services firm must have acompliance supervisor to ensure that:Task 1:systemsare in place to detect violations of laws, rules, regulations, firm policies,and the industrywide Code ofConduct and to enforce investment-relatedcompliance policies;Task 2:the firm has adequate documented compliancepolicies and procedures; it trains all personnel on the same and makes sure thepolicies and procedures are followed; andTask 3: inadequateprocedures are identified and recommendations to correct inadequate proceduresare submitted to senior management forapproval and implementation."Question1Which of Kingfisher's statements in the RFPregarding its qualifications most likely violates the CFA Institute Code ofEthics and Standards of Professional Conduct?A.Justification 1B.Justification 2C.Justification 3Question2Regarding the proposed policy statementrelating to Levels of Professionalism, which requirement least Likely reflectsany of the CFA Institute Code of Ethics and Standards of Professional Conduct?A.Conflicts of interestB.Differentiation of servicespensation arrangementsQuestion3Do any of Kingfisher's proposed policystatements related to Capital Market Integrity most likely violate any CFAInstitute Code of Ethics and Standards of Professional Conduct?A.No.B.Yes, regarding marketmanipulation.C.Yes, regarding materialnonpublic information.Question4Which of Kingfisher's proposed requirementsto ensure Duties to Clients is least appropriate to prevent violations of CFAInstitute Code of Ethics and Standards of Professional Conduct? The requirementcalling for a(n):A.periodic review.B.investment plan.C.well-diversified portfolio.Question5Which of Kingfisher's proposed requirementsregarding investment recommendations is most appropriate to prevent violationsof CFA Institute Standard V (A) Diligence and Reasonable Basis?A.Requirement 1B.Requirement 2C.Requirement 3Question6Which of the following governmentcommittee-suggested tasks would least likely conform to CFA Institute StandardIV (C) Responsibilities of Supervisors?A.Task 1B.Task 2C.Task 31. Correct answer:ACFA Institute Guidance for Standards I-VII2013 Modular Level IL Vol. 1, Reading 2,Section Standard VII (B) Reference to CFA Institute, the CFA Designation, andthe CFA Program, GuidanceStudy Session 1-2-aDemonstrate a thorough knowledge of the CFAInstitute Code of Ethics and Standards of Professional Conduct by interpretingthe Code and Standards to specific situations.A is correct because it is a violation ofStandard VII (B) Reference to the CFA Institute, the CFA Designation, and theCFA Program to imply that the competencies of a CFA charterholder are superiorto those of others not holding the designation. R is not a violation, however,to factually state that charterholders must annually renew their commitment toabide by the CFA Institute Code of Ethics and Standards of ProfessionalConduct or that each of the team memberspassed all three CFA exams in their first try.2. Correct answer:BCFA Institute Guidance for Standards I-VII2013 Modular Level II, Vol. 1, Reading 2,Sections Standard III(B) Fair Dealing, Guidance; Standard IV (B) AdditionalCompensation Arrangements, Guidance; StandardVI (A) Disclosure of Conflicts,Guidance Study Session 1-2-a Demonstrate a thorough knowledge of the CFAInstitute Code of Ethics and Standards of Professional Conduct by interpretingthe Code and Standards to specific situations.B is correct because Standard III(B) FairDealing accommodates the differentiation of services to clients as long as suchservices are not offered selectively. The different service levels should bedisclosed to clients and prospective clients and should be available toeveryone. A requirement to disclose all conflicts of interest would not violateStandard VI (A) Disclosure of Conflicts, nor would the outline of all compensationarrangements violate Standard IV (B) Additional Compensation Arrangements.3. Correct answer:ACFA Institute Guidance for Standards I-VII2013 Modular Level II Vol. 1. Reading 2,Sections Standard II (A) Material Nonpublic Information. Guidance; Standard II(B) Market Manipulation, GuidanceStudy Session 1-2-aDemonstrate a thorough knowledge of the CFAInstitute Code of Ethics and Standards of Professional Conduct by interpretingthe Code and Standards to specific situations.A is correct because Kingfisher's proposedgeneral principles related to Capital Market Integrity properly address in principleStandard II (A) Material Nonpublic Information and Standard II(8) MarketManipulation.Standard II (A) does not disallow thepossession of insider information but does disallow using the information totake unfair advantage of the general investing public. Standard II (B) requiresthe prohibition of: (1)market manipulation, that is, dissemination of false ormisleading information: and (2) transactions that deceive or would be likely tomislead market participants by distorting the price-setting mechanism offinancial instruments.4. Correct answer:C"Guidance for Standards I-VII".CFA Institute2013 Modular Level II Vol. 1, Reading 2,Section Standard III (A) Developing the Client's PortfolioStudy Session 1-2-bRecommend practices and procedures designedto prevent violations of the Code of Ethics and Standards of ProfessionalConduct.C is correct because Standard III (A)Loyalty, Prudence and Care requires a client's portfolio to be managed byinvestment guidelines agreed with the client. Some clients' investmentobjectives may not allow for a diversified portfolio across all asset classesavailable. "Therefore, to do so may violate this Standard."5. Correct answer:BCFA Institute Guidance for Standards I-VII2013 Modular Level II Vol. 1, Reading 2,Section Standard V (A) Diligence and Reasonable Basis, GuidanceStudy Session 1-2-bviolations of the CFA Institute Code of Ethics and Standards ofProfessional Conduct.B is correct because it is recommended todevelop and use measurable criteria for assessing the quality of research tohelp comply with Standard V (A) Diligence and Reasonable Basis. Therefore, the researchrecommendations need to be assessed to determine their validity over time. Didthe process and the analyst's view lead to the right recommendation? That is,did clients have the potential to benefit from the recommendation? Ifrecommendations consistently over time prove to be wrong. perhaps the researchprocesses need to be changed-or the analysts themselves!6.Correct answer:ACFA Institute Guidance for Standards 1-VII2013 Modular level II, Vol. 1, Reading 2,Section Standard IV (C) Responsibilities of Supervisors, GuidanceStudy Session 1-2-bviolations of the CFA Institute Code of Ethics and Standards ofProfessional ConductA is correct because Task 1 is insufficientin that Standard IV(C) Responsibilities of Supervisors requires supervisors toenforce non-investment-related policies as well as investment-related policies.。

IFRS12 International Financial Reporting Standard12Disclosure of Interests in Other EntitiesIn May2011the International Accounting Standards Board(IASB)issued IFRS12Disclosure of Interests in Other Entities.IFRS12replaced the disclosure requirements in IAS27Consolidated and Separate Financial Statements,IAS28Investments in Associates and IAS31Interests in Joint Ventures.In June2012,IFRS12was amended by Consolidated Financial Statements,Joint Arrangements and Disclosure of Interests in Other Entities:Transition Guidance(Amendments to IFRS10,IFRS11and IFRS12).These amendments provided additional transition relief in IFRS12,limiting the requirement to present adjusted comparative information to only the annual period immediately preceding the first annual period for which IFRS12is applied.Furthermore, for disclosures related to unconsolidated structured entities,the amendments removed the requirement to present comparative information for periods before IFRS12is first applied.Other IFRSs have made minor consequential amendments to IFRS12,including Investment Entities(Amendments to IFRS10,IFRS12and IAS27)(issued October2012).IFRS Foundation A505IFRS12C ONTENTSfrom paragraph INTRODUCTION IN1 INTERNATIONAL FINANCIAL REPORTING STANDARD12 DISCLOSURE OF INTERESTS IN OTHER ENTITIESOBJECTIVE1 Meeting the objective2 SCOPE5 SIGNIFICANT JUDGEMENTS AND ASSUMPTIONS7 Investment entity status9A INTERESTS IN SUBSIDIARIES10 The interest that non-controlling interests have in the group’s activities andcash flows12 The nature and extent of significant restrictions13 Nature of the risks associated with an entity’s interests in consolidatedstructured entities14 Consequences of changes in a parent’s ownership interest in a subsidiarythat do not result in a loss of control18 Consequences of losing control of a subsidiary during the reporting period19 INTERESTS IN UNCONSOLIDATED SUBSIDIARIES(INVESTMENT ENTITIES)19A INTERESTS IN JOINT ARRANGEMENTS AND ASSOCIATES20 Nature,extent and financial effects of an entity’s interests in jointarrangements and associates21 Risks associated with an entity’s interests in joint ventures and associates23 INTERESTS IN UNCONSOLIDATED STRUCTURED ENTITIES24 Nature of interests26 Nature of risks29 APPENDICESA Defined termsB Application guidanceC Effective date and transitionD Amendments to other IFRSsFOR THE ACCOMPANYING DOCUMENTS LISTED BELOW,SEE PART B OF THIS EDITIONAPPROVAL BY THE BOARD OF IFRS12ISSUED IN MAY2011APPROVAL BY THE BOARD OF CONSOLIDATED FINANCIAL STATEMENTS,JOINT ARRANGEMENTS AND DISCLOSURE OF INTERESTS IN OTHERENTITIES:TRANSITION GUIDANCE(AMENDMENTS TO IFRS10,IFRS11ANDIFRS12)ISSUED IN JUNE2012APPROVAL BY THE BOARD OF INVESTMENT ENTITIES(AMENDMENTS TOIFRS10,IFRS12AND IAS27)ISSUED IN OCTOBER2012A506IFRS FoundationIFRS12 BASIS FOR CONCLUSIONSIFRS Foundation A507IFRS12International Financial Reporting Standard12Disclosure of Interests in Other Entities (IFRS12)is set out in paragraphs1–31and Appendices A–D.All the paragraphs have equal authority.Paragraphs in bold type state the main principles.Terms defined in Appendix A are in italics the first time they appear in the IFRS.Definitions of other terms are given in the Glossary for International Financial Reporting Standards.IFRS12 should be read in the context of its objective and the Basis for Conclusions,the Preface to International Financial Reporting Standards and the Conceptual Framework for Financial Reporting.IAS8Accounting Policies,Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies in the absence of explicit guidance.A508IFRS FoundationIFRS12 IntroductionIN1IFRS12Disclosure of Interests in Other Entities applies to entities that have an interest in a subsidiary,a joint arrangement,an associate or an unconsolidatedstructured entity.IN2The IFRS is effective for annual periods beginning on or after1January2013.Earlier application is permitted.Reasons for issuing the IFRSIN3Users of financial statements have consistently requested improvements to the disclosure of a reporting entity’s interests in other entities to help identify theprofit or loss and cash flows available to the reporting entity and determine thevalue of a current or future investment in the reporting entity.IN4They highlighted the need for better information about the subsidiaries that are consolidated,as well as an entity’s interests in joint arrangements and associatesthat are not consolidated but with which the entity has a special relationship.IN5The global financial crisis that started in2007also highlighted a lack of transparency about the risks to which a reporting entity was exposed from itsinvolvement with structured entities,including those that it had sponsored.IN6In response to input received from users and others,including the G20leaders and the Financial Stability Board,the Board decided to address in IFRS12theneed for improved disclosure of a reporting entity’s interests in other entitieswhen the reporting entity has a special relationship with those other entities.IN7The Board identified an opportunity to integrate and make consistent the disclosure requirements for subsidiaries,joint arrangements,associates andunconsolidated structured entities and present those requirements in a singleIFRS.The Board observed that the disclosure requirements of IAS27Consolidatedand Separate Financial Statements,IAS28Investments in Associates and IAS31Interestsin Joint Ventures overlapped in many areas.In addition,many commented thatthe disclosure requirements for interests in unconsolidated structured entitiesshould not be located in a consolidation standard.Therefore,the Boardconcluded that a combined disclosure standard for interests in other entitieswould make it easier to understand and apply the disclosure requirements forsubsidiaries,joint ventures,associates and unconsolidated structured entities. Main features of the IFRSIN8The IFRS requires an entity to disclose information that enables users of financial statements to evaluate:(a)the nature of,and risks associated with,its interests in other entities;and(b)the effects of those interests on its financial position,financialperformance and cash flows.IFRS Foundation A509IFRS12General requirementsIN9The IFRS establishes disclosure objectives according to which an entity discloses information that enables users of its financial statements(a)to understand:(i)the significant judgements and assumptions(and changes tothose judgements and assumptions)made in determining thenature of its interest in another entity or arrangement(iecontrol,joint control or significant influence),and indetermining the type of joint arrangement in which it has aninterest;and(ii)the interest that non-controlling interests have in the group’sactivities and cash flows;and(b)to evaluate:(i)the nature and extent of significant restrictions on its ability toaccess or use assets,and settle liabilities,of the group;(ii)the nature of,and changes in,the risks associated with itsinterests in consolidated structured entities;(iii)the nature and extent of its interests in unconsolidatedstructured entities,and the nature of,and changes in,the risksassociated with those interests;(iv)the nature,extent and financial effects of its interests in jointarrangements and associates,and the nature of the risksassociated with those interests;(v)the consequences of changes in a parent’s ownership interest in asubsidiary that do not result in a loss of control;and(vi)the consequences of losing control of a subsidiary during thereporting period.IN10The IFRS specifies minimum disclosures that an entity must provide.If the minimum disclosures required by the IFRS are not sufficient to meet thedisclosure objective,an entity discloses whatever additional information isnecessary to meet that objective.IN11The IFRS requires an entity to consider the level of detail necessary to satisfy the disclosure objective and how much emphasis to place on each of therequirements in the IFRS.An entity shall aggregate or disaggregate disclosuresso that useful information is not obscured by either the inclusion of a largeamount of insignificant detail or the aggregation of items that have differentcharacteristics.IN12Investment Entities(Amendments to IFRS10,IFRS12and IAS27),issued in October 2012,introduced an exception to the principle in IFRS10Consolidated FinancialStatements that all subsidiaries shall be consolidated.The amendments define aninvestment entity and require a parent that is an investment entity to measureits investment in particular subsidiaries at fair value through profit or loss inaccordance with IFRS9Financial Instruments(or IAS39Financial Instruments: A510IFRS FoundationIFRS12Recognition and Measurement,if IFRS9has not yet been adopted)instead of consolidating those subsidiaries in its consolidated and separate financial statements.Consequently,the amendments also introduced new disclosure requirements for investment entities in this IFRS and IAS27Separate Financial Statements.IFRS Foundation A511IFRS12International Financial Reporting Standard12Disclosure of Interests in Other EntitiesObjective1The objective of this IFRS is to require an entity to disclose information that enables users of its financial statements to evaluate:(a)the nature of,and risks associated with,its interests in otherentities;and(b)the effects of those interests on its financial position,financialperformance and cash flows.Meeting the objective2To meet the objective in paragraph1,an entity shall disclose:(a)the significant judgements and assumptions it has made in determining:(i)the nature of its interest in another entity or arrangement;(ii)the type of joint arrangement in which it has an interest(paragraphs7–9);(iii)that it meets the definition of an investment entity,if applicable(paragraph9A);and(b)information about its interests in:(i)subsidiaries(paragraphs10–19);(ii)joint arrangements and associates(paragraphs20–23);and(iii)structured entities that are not controlled by the entity(unconsolidated structured entities)(paragraphs24–31).3If the disclosures required by this IFRS,together with disclosures required by other IFRSs,do not meet the objective in paragraph1,an entity shall disclosewhatever additional information is necessary to meet that objective.4An entity shall consider the level of detail necessary to satisfy the disclosure objective and how much emphasis to place on each of the requirements in thisIFRS.It shall aggregate or disaggregate disclosures so that useful information isnot obscured by either the inclusion of a large amount of insignificant detail orthe aggregation of items that have different characteristics(see paragraphsB2–B6).Scope5This IFRS shall be applied by an entity that has an interest in any of the following:(a)subsidiaries(b)joint arrangements(ie joint operations or joint ventures)A512IFRS FoundationIFRS12(c)associates(d)unconsolidated structured entities.6This IFRS does not apply to:(a)post-employment benefit plans or other long-term employee benefitplans to which IAS19Employee Benefits applies.(b)an entity’s separate financial statements to which IAS27SeparateFinancial Statements applies.However,if an entity has interests inunconsolidated structured entities and prepares separate financialstatements as its only financial statements,it shall apply therequirements in paragraphs24–31when preparing those separatefinancial statements.(c)an interest held by an entity that participates in,but does not have jointcontrol of,a joint arrangement unless that interest results in significantinfluence over the arrangement or is an interest in a structured entity.(d)an interest in another entity that is accounted for in accordance withIFRS9Financial Instruments.However,an entity shall apply this IFRS:(i)when that interest is an interest in an associate or a joint venturethat,in accordance with IAS28Investments in Associates and JointVentures,is measured at fair value through profit or loss;or(ii)when that interest is an interest in an unconsolidated structuredentity.Significant judgements and assumptions7An entity shall disclose information about significant judgements and assumptions it has made(and changes to those judgements andassumptions)in determining:(a)that it has control of another entity,ie an investee as described inparagraphs5and6of IFRS10Consolidated Financial Statements;(b)that it has joint control of an arrangement or significant influenceover another entity;and(c)the type of joint arrangement(ie joint operation or joint venture)when the arrangement has been structured through a separate vehicle.8The significant judgements and assumptions disclosed in accordance with paragraph7include those made by the entity when changes in facts andcircumstances are such that the conclusion about whether it has control,jointcontrol or significant influence changes during the reporting period.9To comply with paragraph7,an entity shall disclose,for example,significant judgements and assumptions made in determining that:(a)it does not control another entity even though it holds more than half ofthe voting rights of the other entity.(b)it controls another entity even though it holds less than half of thevoting rights of the other entity.IFRS Foundation A513IFRS12(c)it is an agent or a principal(see paragraphs B58–B72of IFRS10).(d)it does not have significant influence even though it holds20per cent ormore of the voting rights of another entity.(e)it has significant influence even though it holds less than20per cent ofthe voting rights of another entity.Investment entity status9A When a parent determines that it is an investment entity in accordance with paragraph27of IFRS10,the investment entity shall discloseinformation about significant judgements and assumptions it has made indetermining that it is an investment entity.If the investment entity does nothave one or more of the typical characteristics of an investment entity(seeparagraph28of IFRS10),it shall disclose its reasons for concluding that it isnevertheless an investment entity.9B When an entity becomes,or ceases to be,an investment entity,it shall disclose the change of investment entity status and the reasons for the change.Inaddition,an entity that becomes an investment entity shall disclose the effect ofthe change of status on the financial statements for the period presented,including:(a)the total fair value,as of the date of change of status,of the subsidiariesthat cease to be consolidated;(b)the total gain or loss,if any,calculated in accordance withparagraph B101of IFRS10;and(c)the line item(s)in profit or loss in which the gain or loss is recognised(ifnot presented separately).Interests in subsidiaries10An entity shall disclose information that enables users of its consolidated financial statements(a)to understand:(i)the composition of the group;and(ii)the interest that non-controlling interests have in thegroup’s activities and cash flows(paragraph12);and(b)to evaluate:(i)the nature and extent of significant restrictions on itsability to access or use assets,and settle liabilities,of thegroup(paragraph13);(ii)the nature of,and changes in,the risks associated with itsinterests in consolidated structured entities(paragraphs14–17);(iii)the consequences of changes in its ownership interest in asubsidiary that do not result in a loss of control(paragraph18);andA514IFRS FoundationIFRS12(iv)the consequences of losing control of a subsidiary duringthe reporting period(paragraph19).11When the financial statements of a subsidiary used in the preparation of consolidated financial statements are as of a date or for a period that is differentfrom that of the consolidated financial statements(see paragraphs B92and B93of IFRS10),an entity shall disclose:(a)the date of the end of the reporting period of the financial statements ofthat subsidiary;and(b)the reason for using a different date or period.The interest that non-controlling interests have in thegroup’s activities and cash flows12An entity shall disclose for each of its subsidiaries that have non-controlling interests that are material to the reporting entity:(a)the name of the subsidiary.(b)the principal place of business(and country of incorporation if differentfrom the principal place of business)of the subsidiary.(c)the proportion of ownership interests held by non-controlling interests.(d)the proportion of voting rights held by non-controlling interests,ifdifferent from the proportion of ownership interests held.(e)the profit or loss allocated to non-controlling interests of the subsidiaryduring the reporting period.(f)accumulated non-controlling interests of the subsidiary at the end of thereporting period.(g)summarised financial information about the subsidiary(seeparagraph B10).The nature and extent of significant restrictions13An entity shall disclose:(a)significant restrictions(eg statutory,contractual and regulatoryrestrictions)on its ability to access or use the assets and settle theliabilities of the group,such as:(i)those that restrict the ability of a parent or its subsidiaries totransfer cash or other assets to(or from)other entities within thegroup.(ii)guarantees or other requirements that may restrict dividendsand other capital distributions being paid,or loans and advancesbeing made or repaid,to(or from)other entities within thegroup.(b)the nature and extent to which protective rights of non-controllinginterests can significantly restrict the entity’s ability to access or use theassets and settle the liabilities of the group(such as when a parent isobliged to settle liabilities of a subsidiary before settling its ownIFRS Foundation A515IFRS12liabilities,or approval of non-controlling interests is required either toaccess the assets or to settle the liabilities of a subsidiary).(c)the carrying amounts in the consolidated financial statements of theassets and liabilities to which those restrictions apply.Nature of the risks associated with an entity’s interestsin consolidated structured entities14An entity shall disclose the terms of any contractual arrangements that could require the parent or its subsidiaries to provide financial support to aconsolidated structured entity,including events or circumstances that couldexpose the reporting entity to a loss(eg liquidity arrangements or credit ratingtriggers associated with obligations to purchase assets of the structured entity orprovide financial support).15If during the reporting period a parent or any of its subsidiaries has,without having a contractual obligation to do so,provided financial or other support to aconsolidated structured entity(eg purchasing assets of or instruments issued bythe structured entity),the entity shall disclose:(a)the type and amount of support provided,including situations in whichthe parent or its subsidiaries assisted the structured entity in obtainingfinancial support;and(b)the reasons for providing the support.16If during the reporting period a parent or any of its subsidiaries has,without having a contractual obligation to do so,provided financial or other support to apreviously unconsolidated structured entity and that provision of supportresulted in the entity controlling the structured entity,the entity shall disclosean explanation of the relevant factors in reaching that decision.17An entity shall disclose any current intentions to provide financial or other support to a consolidated structured entity,including intentions to assist thestructured entity in obtaining financial support.Consequences of changes in a parent’s ownershipinterest in a subsidiary that do not result in a loss ofcontrol18An entity shall present a schedule that shows the effects on the equity attributable to owners of the parent of any changes in its ownership interest in asubsidiary that do not result in a loss of control.Consequences of losing control of a subsidiary duringthe reporting period19An entity shall disclose the gain or loss,if any,calculated in accordance with paragraph25of IFRS10,and:(a)the portion of that gain or loss attributable to measuring any investmentretained in the former subsidiary at its fair value at the date whencontrol is lost;andA516IFRS FoundationIFRS12(b)the line item(s)in profit or loss in which the gain or loss is recognised(ifnot presented separately).Interests in unconsolidated subsidiaries(investment entities)19A An investment entity that,in accordance with IFRS10,is required to apply the exception to consolidation and instead account for its investment in a subsidiaryat fair value through profit or loss shall disclose that fact.19B For each unconsolidated subsidiary,an investment entity shall disclose:(a)the subsidiary’s name;(b)the principal place of business(and country of incorporation if differentfrom the principal place of business)of the subsidiary;and(c)the proportion of ownership interest held by the investment entity and,if different,the proportion of voting rights held.19C If an investment entity is the parent of another investment entity,the parent shall also provide the disclosures in19B(a)–(c)for investments that arecontrolled by its investment entity subsidiary.The disclosure may be providedby including,in the financial statements of the parent,the financial statementsof the subsidiary(or subsidiaries)that contain the above information.19D An investment entity shall disclose:(a)the nature and extent of any significant restrictions(eg resulting fromborrowing arrangements,regulatory requirements or contractualarrangements)on the ability of an unconsolidated subsidiary to transferfunds to the investment entity in the form of cash dividends or to repayloans or advances made to the unconsolidated subsidiary by theinvestment entity;and(b)any current commitments or intentions to provide financial or othersupport to an unconsolidated subsidiary,including commitments orintentions to assist the subsidiary in obtaining financial support.19E If,during the reporting period,an investment entity or any of its subsidiaries has,without having a contractual obligation to do so,provided financial orother support to an unconsolidated subsidiary(eg purchasing assets of,orinstruments issued by,the subsidiary or assisting the subsidiary in obtainingfinancial support),the entity shall disclose:(a)the type and amount of support provided to each unconsolidatedsubsidiary;and(b)the reasons for providing the support.19F An investment entity shall disclose the terms of any contractual arrangements that could require the entity or its unconsolidated subsidiaries to providefinancial support to an unconsolidated,controlled,structured entity,includingevents or circumstances that could expose the reporting entity to a loss(egliquidity arrangements or credit rating triggers associated with obligations topurchase assets of the structured entity or to provide financial support).IFRS Foundation A517IFRS1219G If during the reporting period an investment entity or any of its unconsolidated subsidiaries has,without having a contractual obligation to do so,providedfinancial or other support to an unconsolidated,structured entity that theinvestment entity did not control,and if that provision of support resulted inthe investment entity controlling the structured entity,the investment entityshall disclose an explanation of the relevant factors in reaching the decision toprovide that support.Interests in joint arrangements and associates20An entity shall disclose information that enables users of its financial statements to evaluate:(a)the nature,extent and financial effects of its interests in jointarrangements and associates,including the nature and effects of itscontractual relationship with the other investors with joint control of,or significant influence over,joint arrangements and associates(paragraphs21and22);and(b)the nature of,and changes in,the risks associated with its interestsin joint ventures and associates(paragraph23).Nature,extent and financial effects of an entity’sinterests in joint arrangements and associates21An entity shall disclose:(a)for each joint arrangement and associate that is material to thereporting entity:(i)the name of the joint arrangement or associate.(ii)the nature of the entity’s relationship with the joint arrangementor associate(by,for example,describing the nature of theactivities of the joint arrangement or associate and whether theyare strategic to the entity’s activities).(iii)the principal place of business(and country of incorporation,ifapplicable and different from the principal place of business)ofthe joint arrangement or associate.(iv)the proportion of ownership interest or participating share heldby the entity and,if different,the proportion of voting rightsheld(if applicable).(b)for each joint venture and associate that is material to the reportingentity:(i)whether the investment in the joint venture or associate ismeasured using the equity method or at fair value.(ii)summarised financial information about the joint venture orassociate as specified in paragraphs B12and B13.A518IFRS FoundationIFRS12(iii)if the joint venture or associate is accounted for using the equitymethod,the fair value of its investment in the joint venture orassociate,if there is a quoted market price for the investment.(c)financial information as specified in paragraph B16about the entity’sinvestments in joint ventures and associates that are not individuallymaterial:(i)in aggregate for all individually immaterial joint ventures and,separately,(ii)in aggregate for all individually immaterial associates.21A An investment entity need not provide the disclosures required by paragraphs21(b)–21(c).22An entity shall also disclose:(a)the nature and extent of any significant restrictions(eg resulting fromborrowing arrangements,regulatory requirements or contractualarrangements between investors with joint control of or significantinfluence over a joint venture or an associate)on the ability of jointventures or associates to transfer funds to the entity in the form of cashdividends,or to repay loans or advances made by the entity.(b)when the financial statements of a joint venture or associate used inapplying the equity method are as of a date or for a period that isdifferent from that of the entity:(i)the date of the end of the reporting period of the financialstatements of that joint venture or associate;and(ii)the reason for using a different date or period.(c)the unrecognised share of losses of a joint venture or associate,both forthe reporting period and cumulatively,if the entity has stoppedrecognising its share of losses of the joint venture or associate whenapplying the equity method.Risks associated with an entity’s interests in jointventures and associates23An entity shall disclose:(a)commitments that it has relating to its joint ventures separately fromthe amount of other commitments as specified in paragraphs B18–B20.(b)in accordance with IAS37Provisions,Contingent Liabilities and ContingentAssets,unless the probability of loss is remote,contingent liabilitiesincurred relating to its interests in joint ventures or associates(includingits share of contingent liabilities incurred jointly with other investorswith joint control of,or significant influence over,the joint ventures orassociates),separately from the amount of other contingent liabilities.IFRS Foundation A519。