会计信息质量外文文献及翻译解析

- 格式:doc

- 大小:49.00 KB

- 文档页数:10

英文原文Timeliness of Reporting and the Quality of Financial InformationAbstractThis study is designed to investigate the effects of sector, reporting type, and income on firms’ timely annual financial reporting practices listed on Istanbul Stock Exchange (ISE). Regression model is utilized to examine the effects of sector (financial firms),financial statement type (consolidated-non-consolidated firms), and income (positive-negative income) for the years from 2005 to 2008. The results reveal that sector, financial statement type and income have significant impact on timely reporting financial statements of selected firms. The coefficient estimates for sector, financial statement type, and income are statistically significant. Effects of sector and financial statement type on lead time are positive while income’s is negative. Based on the results,non financial firms publish their financial statements later than others. Similarly,consolidated firms report their financial statements later than non-consolidated firms.Finally, firms that report positive income release financial statements earlier than others.Keywords: Timeliness, Reporting Financial Statements, Quality of Financial Information,Lead Time, Timely ReportingJEL Classification Codes:1. IntroductionIn this study, we investigate the effects of sector (financial-non-financial firms), financial statement type (consolidated-non-consolidated financial statements), and income (positive-negative income) on timely reporting practices of companies listed on Istanbul Stock Exchange (ISE –stanbul Menkul Kıymetler Borsası, IMKB). The sector is defined as financial firms andnon-financial firms that are listed on ISE. Financial statement type term is used for firms that report their financial statement as consolidated and non-consolidated. Finally, income is considered as firms that report positive income and negative income. The results of our analysis indicate that those variables have significant impacts on timelines of financial statements.Financial statements and mandatory financial reporting are prominent sources of information for financial statement users in decision making. Financial statements must have certain attributes to be useful: understandable, reliable, relevant, and comparable. Quality of data that financial statements provide is usually checked in accordance with those attributes of statements.High-quality information is essential to the proper functioning of equity markets, financial markets, and financial decisions (Shaw, 2003). In order to be functional, financial information gathered out of financial statements must be useful to its users.The usefulness of accounting information to financial statement users is an important criterion of quality of earnings. Financial data that are not providing useful information to users are not valuable. As a matter of fact, The Financial Accounting Standards Board (FASB) outlines the components of quality information: predictive value, feedback value, timeliness, verifiability,neutrality, and representational faithfulness (Velury and Jenkins, 2006).Timeliness is one of the most important components of relevancy. Both timeliness and relevance are important features of useful information. Therefore, financial statements should be published on time to be useful to its users in their decision making.The concept of timeliness in financial reporting has two dimensions: the frequency of financial reporting and the lag between theend of the reporting period and the date the financial statements are issued (Davies ,1980).Timely corporate financial reporting is an important qualitative attribute and a necessary component of financial accounting. Financial information needs to be available to its users as rapidly as possible to make corporate financial statement information relevant decision making process.Timely reporting on financial statements is necessary for healthy financial markets. Timely financial reporting helps in efficient and timely allocation of resources by reducing dissemination of asymmetric information, by improving pricing of securities, and by mitigating insider trading, leaks and rumors in the market (Kamran, 2003).Many studies have discussed various aspects of corporate governance. In the area of timeliness of financial reporting, for example, the Accounting Principles Board (1970) recognized the general principle several decades ago. The Financial Accounting Standards Board (1980) recognized the importance of timeliness in one of its Concepts Statements (McGee, 2009,).Timeliness is a necessary component of relevant financial information that is receiving increased attention by accounting regulators and listing authorities worldwide. For example, in the United States (U.S.) the Securities and Exchange Commission (SEC), New York Stock Exchange(NYSE), and NASDAQ have issued requirements and recommendations regarding the timely dissemination of financial information (Abdelsalam and Street, 2007,).Timeliness of financial statements is being discussed in the OECD Principles of Corporate Governance1. Discloser and transparency are explained as follows: “The corporate governance framework should ensure that timely and accurate disclosure is made on all material mattersregarding the corporation, including the financial situation, performance, ownership, and governance of the company. Disclosure should include, but not be limited to, material information on:The financial and operating results of the company. Information should be prepared and disclosed in accordance with high quality standards of accounting and financial and non-financial disclosure…” (OECD, 2004,p.22).Timely reporting on financial statements is affected by many factors. The regulations, accounting standards, and sector and firm-specifics are some of those. While there may be many factors, company-specific and audit-related ones have been examined in prior studies as being particularly important. Company-specific factors are those that enable management of a firm either to produce more timely financial statements or to reduce costs of delaying in reporting. Such factors include company size, profitability, gearing, financial condition, industry type and ownership structure(Ansah and Leventis, 2006). In this study, we explore the effects of sector, financial statement type,and income on timely reporting.1.1. The Regulatory Framework for Timely Reporting in TurkeyFor listed companies two legal sources govern timely reporting: Turkish Commercial Code and Law of Capital Market. In addition to those sources, Turkish Accounting Standards Board is publishing accounting standards including timeliness in financial reporting.The Turkish Commercial Code requires annual reports to be prepared at least 15 days before the date of the annual general meeting. In addition, Capital Market Board (CMB) of Turkey published several communiqués related to financial reporting process between 1989 and 2003. In 2003, the Board issued a broad set of financial reporting standards that are translation of International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS). Currently, TurkishAccounting Standards Board (TASB) is the only organization that publishes accounting standards.According to regulations that enacted in 2003, companies that are listed on the stock exchange must publish their audited annual financial statements by the 10th week after their financial year-end.However, consolidated financial statements must be published within 14 weeks of the financial year end(Türel, 2010).2. Review of the LiteratureA number of studies have discussed the aspects and components of timeliness in financial reporting.Actually, most of those studies examine what effects timely reporting of financial statements. The literature contains studies that are discussing international differences on timely reporting of financial statements as well.Many works state mixed conclusions regarding the relationship of timeliness of reporting and the quality of the information being reported. Some studies show that good news is reported before bad news, whereas other studies show that bad news is reported before good news. Some researchers found that many companies are not willing to report bad news and because of that companies take more time to calculate the numbers or apply creative accounting techniques when they need to report bad news.On the other hand, some studies found that bad news are reported before good news because the market would not focus enough on good news (McGee, 2009).Basu (1997) states that reporting bad news sooner could be just because of conservatism and reported earnings respond more completely or quickly to bad news than good news. However,sometimes because of less incentive in tax system, conservatism is not an important variable in reporting bad news or good news sooner (Jindrichovska and Mcleay, 2005).When financial statements are released earlier than expected, they tend to have larger price effects than when they are released on time or later than expected. Further,unexpectedly early reports arecharacterized by good news, whereas unexpectedly late reports tend to bearbad news (Chambers & Penman, 1984). Kross and Schroeder (1984) concludethat abnormal returns of companies that are announced early (late) weresignificantly higher (lower) than the returns of firms that are announcedlate (early). And their results are consistent with previous studies.The relationship between company size and timeliness of financialreports is another aspect being discussed by researchers. Aroly(1989)state that large firms report earnings relatively early, but the associated market reaction tends to be small due to the size effect. Onthe other hand,small size firms release later, but their associated marketreaction tends to be high due to the size effect.Timeliness of financial statements is being discussed from theview of sector characteristics.Türel (2010) indicates that Ahmad andKamarudin (2003) investigate the determinants of audit delay in the KualaLumpur Stock Exchange during the period 1996-2000. The results suggestthat the audit delay is significantly longer for companies classified innon-financial industry.Some researchers examined the timeliness of accounting disclosurefrom the view of stock returns. Alford, and Jones (1994) examine thetimeliness of accounting disclosures and report that firms who file beyondthe filing requirement have poorer performance by both accountingmeasures and stock returns. The late filers have lower returns on equity,smaller growth in earnings per share, higher financial leverage, and lowerinternal liquidity for the fiscal year in which they file late.Marketadjusted stock returns are also lower during the fiscal year in which thefirm files late.Furthermore, the authors find that market adjusted stockreturns for late filers are lower in the post 90-day period, past the timewhen an investor would already be aware that a late filing firm waspotentially facing financial difficulty.Our study is designed to test the effects of sector, financial statement type, and income on timely reporting. Research is designed based on data that are collected from ISE for the selected firms.3. Research Design3.1. SampleData were gathered for the companies listed on ISE for the years 2005, 2006, 2007, and 2008. Number of firms by years indicated in Table 1. We chose our sample on the basis of the following criteria. We eliminated the firms that do not have sufficient data because of bankruptcy or any other reasons.Table 1: Number of firmsNumber of firms by yearsYear Number of firms2005 3102006 3192007 3232008 316In most studies (Ansah and Leventis (2006), McGee (2009), Türel (2010)), timeliness was defined by counting the number of days that elapsed between year-end and the date of the financial reporting deadline. As in Ansah and Leventis (2006), we define “timeliness” as the number of days between a firm’s financial year-end and the day on which the firm publishes its financial statements according to regulatory deadline. Lead-time is used instead of “delay” to denote timeliness because firms released financial statements by legal deadline. Therefore we present lead-time as dependent variable in the model that we developed below.3.2. The ModelIn this study following model is designed to examine the effects ofsector(non-financial- financial firms),firm-specific-types of reporting (consolidated-non-consolidated), and income on timely reporting financial statements. The model designed for the years 2005-2008. We estimated the model by ordinary least squares (OLS) method to evaluate variables below.Table 2: Regression ModelLEAD-TIME = b0 + b1SECTOR + b2 FINSTATYPE + b3INCOME + ELEAD-TIME= Lead-time is the number of days between financial year-end and the date release of firm’s annualSECTOR = Type of firm is represented by a 1 for non-financial firms, a 0 for financialFINSTATYPE = Type of financial statement is represented by a1 for consolidated, a 0 for non-consolidatedINCOME = Firms with positive net income were assigned as 1, otherwise as 0.4 .ConclusionsWe estimated the model by ordinary least squares (OLS) method to evaluate the variables. The coefficient estimates for sector, financial statements type , and income are statistically significant. Effects of sector and financial statements type on lead-time are positive while income is negative.Effects of sector and financial statement type on lead time are positive while income is negative. The presence of sector has positive effects on timely reporting financial statements. That means non-financial companies publish their financial statements about 6 days later than others.Financial statement type has positive effect on lead time. Consolidated firms are reporting their financial statements about 20 dayslater than non-consolidated firms and this is an expected result. Consolidated financial statements’ publishing deadline is set longer by the regulatory institutions for those firms. Companies that report positive income publish their financial statements about 8 days earlier than others. It can be said that firms that are reporting loss release the news late.The statistical test reveals that sector, financial statements type and income have significant impacts on timely reporting financial statements of selected firms for the years of 2005-2008. The coefficient estimates for sector, financial statement type, and income are statistically significant.中文原文报告的及时性和财务信息的质量摘要本研究的目的是调查部门,报告类型和收入的影响,这些是列在伊斯坦布尔证券交易所关于上市企业及时年度的财务报告。

封面目录1 绪论 (3)1 Introduction (4)2 会计信息失真的原因 (5)2.1 会计法律法规体系的局限性 (5)2.2 会计工作人员的疏漏 (5)2.3 职业道德的背离 (5)2.4 政府监管机制不完善 (6)2 The reason of the accounting information distortion (7)2.1 The limitation of accountant laws and regulations system (7)2.2 The accountancy fault (7)2.3 Occupational ethics deviating (8)2.4 The imperfect government mechanism (8)3 会计信息失真的对策 (9)3.1 建立标准化的会计准则,加强会计制度的建设 (9)3.2 建立和完善公司内部监管体系 (9)3.3 完善会计人员监管体系,加大违规的惩处力度 (9)3.4 完善职业资格证制度,加大后续教育的力度,提高会计人员的综合素质 (10)3 The Countermeasure of Accounting Information Distortion (11)3.1 Standard accounting guide line and strengthen the construction of accounting system .. 113.2 Establishing and perfecting enterprise internal control system. (11)3.3 Perfecting accountant supervises system, enhancing punishment. (12)3.4 Consummating employed qualifications system, enhancing following education,improving the accountant quality comprehensively. (12)4 结论 (14)Conclusions (15)摘要这些年,会计信息失真已经影响到了社会经济秩序,本文主要分析了我国会计信息失真产生的原因,及其对策。

文献信息:文献标题:Effect of information quality due accounting regulatory changes: Applied case to Mexican real sector(会计准则的变化对会计信息质量的影响:以墨西哥实体行业为例)国外作者:HHG Sánchez,KAC Alejandro,ABM Sáenz,et al文献出处:《Contaduría Y Administración》,2017,62:761-774字数统计:英文2232单词,12176字符;中文3801汉字外文文献:Effect of information quality due accounting regulatory changes: Applied case to Mexican real sector Abstract The purpose of this paper is to examine whether changes in accounting standards improve value relevance of financial information on listed companies in Mexico. The research was conducted for the period 2000–2013 using a sample of 141 companies that report to the Mexican stock exchange using the methodology of panel data. Our findings show that changes in local regulations (generally accepted accounting principles) to internationally approved standards (Financial Reporting Standards and International Financial Reporting Standards) increase the value relevance and therefore the quality of information. The study shows that the accounting information with international Financial Reporting Standards is more trustworthy for foreign and national investors.Keywords:Quality of accounting information; Financial Reporting Standards; International Financial Reporting Standards; Accounting principlesIntroductionThe research done regarding the quality of the accounting information is of interest to different agents such as the institutions that issue standards, e.g., the FASB(Financial Accounting Standards Board) or the IASB (International Accounting Standards Board), financial intermediaries, regulatory bodies, researchers and academics, and in general, to the users of financial statements for the making of decisions.Our work contributes to the debate on whether the adoption of the accounting standards adapted throughout the period of 2000 to 2013 are associated with the improvement of the quality of accounting information. The objective of this work is to analyze if the changes in the accounting standards improve the evaluative relevance of the financial information in listed companies in Mexico. We intend to show if the variables of accounting profit and book value of the net worth are associated with the market value of the companies listed in the Mexican Stock Exchange.Our discoveries show that the changes from local standards (Generally Accepted Accounting Principles) to internationally homologated standards (International Financial Reporting Standards) increase the evaluative relevance and therefore the quality of the information.Theoretical frameworkQuality of the accounting informationThe accounting information is used to understand the economic reality of the company in order to make adequate decisions, so that it should be defined through the quality of the same (Dumitru, 2011). Said quality of the accounting information has been receiving greater attention due to the recent accounting scandals. However, despite the increasing importance given to this issue, the quality of accounting remains a vague term which is difficult to define (Bartov et al., 2005; Hribar, Kravel, & Wilson, 2014).There are a great number of definitions regarding the concept of the quality of accounting information, from a quantitative approximation the following works stand out: Penamn and Zhang (2002), Dechow and Schrand (2004) and Dechow, Ge, and Schrand (2010), who define high quality through the predictive effect of the accounting income on the future valuation of the company. On the other hand, Barthet al. (2008) state that there is quality in the result when the accounting information is less manipulated, a more opportune acknowledgment of the losses is present, and an increase in the predictive capability is given by the regression between the fundamental and market variables.Dechow et al. (2010) mention that there is no measure of quality for all decision models. Other authors such as Ball, Robin, and Wu (2003), Ball and Shivakumar (2005) and Burgstahler, Hail, and Leuz (2006) state that the quality of the accounting information varies according to increase in the number of users that have access to privileged information, as this is how the asymmetry of the information is resolved in private companies.Despite the lack of a clear definition of the accounting quality, several studies use measures that are considered substitutes of accounting quality, for example, the administration of profits, the opportune acknowledgment of losses and the evaluative relevance (Barth et al., 2008). In our research, we considered the evaluative relevance to measure the quality of the information as in Francis, LaFond, Olsson, and Schipper (2004) and Agostino et al. (2011). The investigation in evaluative relevance has been fundamentally carried out in developed countries. However, there is a lack of evidence in developing countries, like in Latin America and Mexico.International Financial Reporting StandardsThe IFRS are accounting standards issued by the Financial Accounting Standards Board (IASB), an independent organization with headquarters in London, United Kingdom. They pretend to be a set of rules that, ideally, would be applied in the same manner to the financial reports by the public companies of the world. Between 1973 and 2000, the international standards were issued by the organization that preceded the IASB, the International Accounting Standards Committee (IASC). This organization was created in 1973 by professional associations of accountants in Australia, Canada, Germany, Japan, Mexico, the Netherlands, the United Kingdom and Ireland, and the United States. During this period, the rules of the IASC were described as “International Accounting Standards” (IAS).Since April 2001, this task of elaborating the standards has been undertaken by areconstructed IASB. The IASB describes its rules under the ne w label: “International Financial Reporting Standards” (IFRS), even though it continues to acknowledge (accept as rightful) the previous standards (IAS) issued by the former regulatory organization (IASC), the IASB is better financed, has better personnel and is more independent than its predecessor.For Ball (2006) there are three advantages to the adoption of the IFRS, firstly they produce economies of scale, given that they are only invented once, they would be a type of public asset, and the marginal cost of their implementation to a new company is zero. The second advantage is that they protect auditors from the manipulation of information by the administrators; and the third advantage is that they allow comparing information between different countries. This third comparability advantage facilitates the cross-border investment and the integration of the capital market (Aggarwal, Klapper, & Wysocki, 2005).In the last decade there has been an increasing interest on how the corporate reports are able to mitigate agency problems and the lack of information. The literature (Armstrong, Barth, & Riedl, 2010; Ball et al., 2003; Rawashdeh, 2003) has attempted to give an answer to issues such as whether international standards produce relevant or quality information for the investors and interested parties. Regarding this issue, for Barth et al. (2008) the IFRS are higher quality standards than the national ones, which could prove to have a “reputational effect” on the companies that voluntarily adopt them.Although, there could be differences in the implementation of IFRS derived from transparency and enforceability issues. Daske, Hail, Leuz, and Verdi (2007) found that the economic effects of the adoption of the IFRS depend on having a serious commitment to transparency. Similarly, Daske, Hail, Leuz, and Verdi (2008) concluded that the effects of the capital market in thefaceof the changes implemented by the IFRS when they are obligatory only present themselves in countries with strict regimes and where the institutional environment provides strong incentives for the companies to be transparent. It would be expected that the standard changes have a greater positive effect on developed markets.MethodologyThe sample is comprised by 141 issuing companies of the Mexican Stock Exchange (BMV) during the period of 2000–2013, considering only the real sector. For the purpose of this study, we have consulted the Economática database in order to obtain the quarterly series of accounting and market variables.In this research we intend to determine whether the fundamental accounting variables have evaluative relevance and, consequently, financial standing in the stock market in Mexico. First of all, we would like to know if there is financial standing in the Mexican market during the study period (2000–2013). To this end, based on the studies of Mohan and John (2011) and Dorantes (2013) we shall determine the significance in EBIT (Earnings before interest and taxes) and of Equity (Equity of the Company). The hypotheses would be as follows:H1: the fundamental variables (EBIT and Equity) have an impact in the capitalization of the company.In addition, we determined if the IFRS, measured as a dichotomous variable, has an impact on capitalization as determined by Agostino et al. (2011) and Cameran, Campa, and Pettinicchio (2014) in their study. Thus, our second hypothesis would be as follows:H2: the effect of the IFRS is greater than that of the GAAP and the effect of the FRS is greater than that of the GAAP.On the other hand, in order to be more conclusive with our results we divided our sample in preand post-adoption of the IFRS as with Bartov et al. (2005) and Barth et al. (2008). Furthermore, we shall demonstrate if increases in the predictive capability exist, and in order to prove this, our third and fourth hypotheses would be as follows: H3 : The EBIT (Earnings before interest and taxes) and the Equity increase their significance and value by changing the study periods of GAAP to FRS and to IFRS.H4 : The predictive capabilityincreases after moving from a period of local standards (GAAP and FRS) to aperiod of international standards (IFRS).In order to prove the first twohypotheses,weusedthefullstudyperiod,i.e.,from2000 to 2013, and for the third and four hypotheses we identified three periods: (1) GAAP from 2000 to 2005; (2) FRS from 2006 to 2011; and, (3) IFRS from 2012 to the third quarter of 2013. For the latter case the dummy variables were eliminated.ConclusionsThe market carries out its assessments differently depending on the standard implemented in its development. We determined the quality of the accounting standard measured through an increment in the evaluative relevance of the financial information. In this sense, the reliability in the accounting standards has increased since 2006, year in which the Generally Accepted Principles stopped being used and were adapted to the International Financial Reporting Standards creating the Financial Reporting Standards (FRS).This study offers important contributions for the Mexican market. First of all, foreign and national investors have certain skepticism regarding the transparency of the companies when divulging their accounting information and of the institutions responsible of monitoring the adoption of the accounting regulations (Dorantes, 2013). In this sense, our results show that the coefficients of the fundamental and control variables are significant, furthermore, the two dichotomous variables (FRS and IFRS) are also significant and positive, with the coefficient of the IFRS variable being greater than the coefficient of the FRS. This shows that the changes in the accounting standards have an impact on the quality of the information during the study period of 2000–2013, with the period of the IFRS having the greater relevance than that of the FRS. With these results, some tranquility can be provided to the investors with regard to our institutions and the transparency of our companies.Second of all, with the purpose of demonstrating a greater importance in our results and valuing the adaptation of the FRS and IFRS, we opted to cut the period in these two cases with the purpose of finding the effect in the 7 quarters after the adoption of each of these standards. Our results show that the change with greater impact in the evaluative relevance is produced when the IFRS are adapted, having been measured through the increase in the coefficients of the fundamental variablesand the predictive capability of the model , which shows that the work of the CINIF has been effective; our results are similar to those obtained by Bartov et al. (2005) and Barth et al. (2008).Third of all, regarding the advantages of the incorporation of the IFRS based on Ball (2006) and which were able to be transferred to the Mexican market on the basis of our findings, it could be that the investors could enjoy of more precise, complete and timely information that allows them to have less information asymmetry and thus decrease the problems of risk. Furthermore, the incorporation of the IFRS improved the processing of information, which betters the efficiency in the markets and the reflection of the accounting information on the stock prices. It also reduces the international comparability differences, which could eliminate barriers in acquisitions and divestments, compensating investors with an increase in the acquisition premiums.Fourth, the IFRS allow for greater quality accounting information, which improves transparency and the corporative government. Due to the fact that the IFRS are based on regulations (Barth et al., 2007), the administrators are more controlled in the manipulation of information and thus could present less agency problems, all for the benefit of the stockholders. Finally, the recognition of losses in an opportune manner results in the administrators being able to have information faster regarding the investments that are generating losses and thus navigate to investments that generate positive VPNs (Ball & Shivakumar, 2005).Finally, our findings prove the need to dedicate additional efforts to achieve a unique set of accounting standards accepted in the capital markets at an international level in order tomakesustainable the transparency made possible by both the FRS and the IFRS. We can thus conclude two things, on the one hand, investors can reliably consider accounting information as an investment criterion, on the other, company administrators must become aware that the fundamental variables of the companies can benefit or harm the market performance of the same, and thus it is necessary that companies have a sustainable financial performance.中文译文:会计准则的变化对会计信息质量的影响:以墨西哥实体行业为例摘要本文的目的是研究会计准则的变化是否提高了墨西哥上市公司的财务信息的价值相关性。

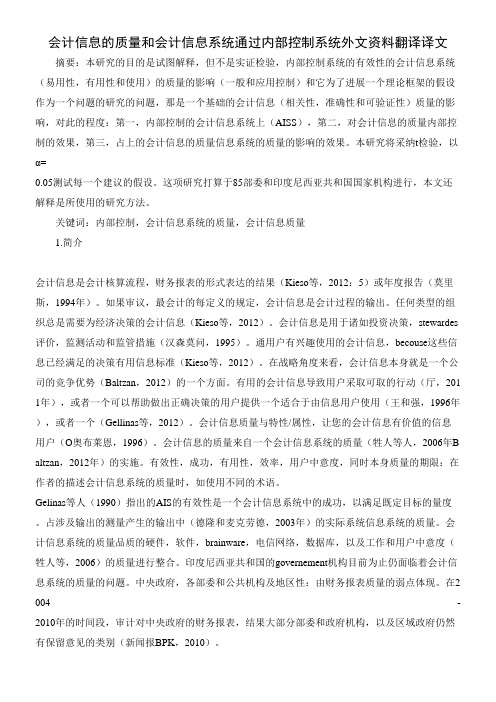

会计信息的质量和会计信息系统通过内部控制系统外文资料翻译译文摘要:本研究的目的是试图解释,但不是实证检验,内部控制系统的有效性的会计信息系统(易用性,有用性和使用)的质量的影响(一般和应用控制)和它为了进展一个理论框架的假设作为一个问题的研究的问题,那是一个基础的会计信息(相关性,准确性和可验证性)质量的影响,对此的程度:第一,内部控制的会计信息系统上(AISS),第二,对会计信息的质量内部控制的效果,第三,占上的会计信息的质量信息系统的质量的影响的效果。

本研究将采纳t检验,以α=0.05测试每一个建议的假设。

这项研究打算于85部委和印度尼西亚共和国国家机构进行,本文还解释是所使用的研究方法。

关键词:内部控制,会计信息系统的质量,会计信息质量1.简介会计信息是会计核算流程,财务报表的形式表达的结果(Kieso等,2012:5)或年度报告(莫里斯,1994年)。

如果审议,最会计的每定义的规定,会计信息是会计过程的输出。

任何类型的组织总是需要为经济决策的会计信息(Kieso等,2012)。

会计信息是用于诸如投资决策,stewardes 评价,监测活动和监管措施(汉森莫问,1995)。

通用户有兴趣使用的会计信息,becouse这些信息已经满足的决策有用信息标准(Kieso等,2012)。

在战略角度来看,会计信息本身就是一个公司的竞争优势(Baltzan,2012)的一个方面。

有用的会计信息导致用户采取可取的行动(厅,201 1年),或者一个可以帮助做出正确决策的用户提供一个适合于由信息用户使用(王和强,1996年),或者一个(Gellinas等,2012)。

会计信息质量与特性/属性,让您的会计信息有价值的信息用户(O奥布莱恩,1996)。

会计信息的质量来自一个会计信息系统的质量(牲人等人,2006年B altzan,2012年)的实施。

有效性,成功,有用性,效率,用户中意度,同时本身质量的期限:在作者的描述会计信息系统的质量时,如使用不同的术语。

The Quality of Accounting Information and The Accounting Information System through The Internal Control Systems: AStudy on Ministry and State Agencies of The Republic ofIndonesiaFardinalAccounting Doctoral Program Faculty of Economic and BusinessPadjadjaran University-IndonesiaE-mail: ferdinal@AbstractThe purpose of this study is an attempt to explain, but not empirically tested, the effect of the effectiveness of internal control system (general and application controls) on the quality of accounting information systems (ease of use, usefulness and usage) and its impact on the quality of accounting information (relevance, accuracy, and verifiability) in order to develop a theoretical framework as a basis of the hypothesis as an answer to the question of the study, that is, to the extent of which: (1) the effect of internal control on accounting information systems (AISs), (2) the effect of internal control on the quality of accounting information, and (3) the effect of the quality of accounting information systems on the quality of accounting information. This study will use a t test by α = 0.05 to test each of the proposed hypothesis. The study is scheduled to be conducted in 85 Ministries and State Agencies of the Republic of Indonesia. Also explained in this paper is the research methodology used. Keywords: Internal Control, Quality of Accounting Information Systems, Quality of Accounting Information 1. IntroductionAccounting information is the results of accounting processes, generally presented in a form of financial statement (Kieso et al, 2012:5) or an annual report (Maurice, 1994). If scrutinized, most of every definitions of accounting states that accounting information is the output of accounting processes.Organization of any kind always needs accounting information for economic decision making (Kieso et al, 2012). Accounting information is used for such things as investment decision, stewardes evaluation, monitoring activities and regulatory measures (Hansen & Mowen, 1995). By using accounting information, decision makers would obtain information on the future of their companies, such as forecasting that involves annual plans, strategic plans, and decision alternatives (Susanto, 2008). The users are interested in using the accounting information, becouse those information has fulfilled a decision-usefulness-information criterion (Kieso et al, 2012). In a strategic perspective, accounting information itself is one of the aspects of a company’s competitive advantage (Baltzan, 2012).Useful accounting information is an one that fits for used by the information user (Wang & Strong, 1996), or one that cause user take to desirable actions (Hall, 2011), or one that may help the users in making proper decisions (Gellinas et al, 2012). Accounting information quality is an information with characteristics/attributes that make the accounting information valuable for the users (O Brien, 1996).The quality of accounting information comes from the implementation of an accounting information systems quality (Sacer et al, 2006. Baltzan, 2012). Among of author use different terminologies when describing the quality of Accounting information system, such as: effectiveness, success, usefulness, efficiency, user satisfaction, and also the term of quality itself. Gelinas et al (1990) suggests that the effectiveness of AIS is a measure of an accounting information system success to meet the established goals. A quality of accounting information system concerned with the measurement of output the actual system that produces the ouput (Delon & McLeod, 2003). An accounting information system quality is an integration of quality hardware, software, brainware, telecommunication network, data base, and quality of work and user satisfaction (Sacer et al, 2006). The governement institutions of the Republic of Indonesia are until currently still faced with a problem of the quality of accounting information system. That is reflected by the weakness of quality of the financial statements of: central governments, the ministries and public institutions and the regionals. In the time period of 2004-2010, results of audit on the financial statements of central government’s, most of ministries and state agencies, and regional government still have a qualified opinion categories (Warta BPK, 2010). Gamawan Fauzi (2012) said, a target of 50% of the regional governments to attain the unqualified opinion categories in 2014 is hard to realize. The problem of low quality of the government financial statements, as a reflection of the poor quality of the accounting information system, is due to among others the weakness of internal controlling system (Warta BPK, 2011).The objective of accounting information systems is to provide the reliable accounting information on a timely basis (Guan, 2006). An internal control system is a series of procedures designed such that provide management with reasonable assurance that the accounting information that provide by an accounting information system presents is reliable and made available timely (Guan, 2006). An accounting information system and record keeping will not success in completely and accurately processing all transaction unless controls, known as internal control, are built into the system (Millchamp & Taylor, 2008).The purpose of this study is to develop a model to find out evidences or answers of the following problems: (1) how extent of which the effect of an internal control system on the quality of AIS, (2) how extent of which the effect of an internal control system on the quality of accounting information, and (3) how extent of which the effect of the quality of accounting information systems quality on the Accounting Information quality .2. Review of Literature2.1. Accounting Information QualityThe value of information is directly linked to how it helps decision makers achieve their organization’s goals. Valuable information can help people and their organizations perform their tasks more efficiently and effectively (Stair and Reynolds, 2012). Furthermore, information of high quality, that is, information product whose characteristics, attributes, or qualities help makes it valuable to them (O Briens, 2004).The quality of accounting information can be explained by several dimensions. Hall (2011) suggests that the dimensions of information quality consist of: relevance, timeliness, accuracy, completeness, and summarizing. Moreover, Gelinas et al (2012) and McLeod (2007) put forward that dimensions of the quality of information are: accurate, timely, relevance, and completeness. Far earlier, Hicks (1993) states relevance, timeliness, accuracy and verifiability as the criteria of information quality. Whereas Maurice (1994) and O’ Briens & Marakas (2010) summarizes the important of information and groups them into three dimensions, namely: time (consist of: timeliness, currency, frequency, time period); content (accuracy, relevance, completeness, conciseness, scope, performance); and form (clarity, detail, order, presentation, media) In this study, the dimensions of accounting information quality are: (1) Relevancy. The Extent to which data is applicable and helpul for the task at hand (Wang & Strong, 1996), the contents of a report or document must serve a purpose (Hall, 2011). (2) Accuracy. The Information must be free from material errors (Hall, 2011). (3) Verifiability, the ability of confirm the accuracy of information by tracing information to its original source (Hicks, 1993)2.2. Accounting Information System QualityAccounting information system is a collection of data and processing procedures that creates needed information for its users (Bagranof et al, 2011). Accounting information systems (AISs) is a collection of resources, such as people and equipment, designed to transform financial and other data into information. This information is communicated to a wide variety of decision makers. AISs perform this transformation whether they are essentially manual systems or thoroughly computerized (Bodnar & Hopwood, 2010).According to Stair & Reynolds (2010), an accounting information systems quality is usually flexible, efficient, accessible, and timely. Seddon (1997) state that an information system success thus conceptualized as a value judgment made by an one from stakeholders’ viewpoints. Moreover, Gelinas & Wriggins (1990) suggest that the effectiveness of an accounting information systems is a measures of accounting information system success to meet the established goals. Meanwhile, Delon & McLean (1992) state that the quality of system is concerned with the measurement of the actual system in producing output.D&M IS Success Model developed by Delon & McLean (1992) and The Technical Acceptance Model (TAM) developed by Fred Davis (1989) are widely used as references by many authors in measuring the dimensions of accounting information system success. In D&M IS Success Model, the quality of AIS is accounted for by using six dimensions, namely: (1) system quality, (2) information quality, (3) use, (4) user satisfaction, (5) individual impact and (6) organizational impact. In Technical Acceptance Model (TAM) (1989) the factors that can lead the best attitudes to a system and then receive and apply the system are used as the measure of accounting information system success, namely: (1) perceived usefulness, (2) perceived ease of use, and (3) actual use (usage). Then, a related model is also proposed by Seddon (1997) which includes: system quality, information quality, perceived usefulness, user satisfaction, and information systems (IS) use. Within the context of the current study, perceived usefulness, perceived ease of use and Information system (IS) use (usage) will be considered as a well-respected dimensions of Accounting Information Systems Quality.Perceived usefulness, refers to the degree to which a person believes that using a particular system would enhance his or her job performance (Davis, 1989). Whereas perceived ease of use refers to the degree to which a person believes that using a particular system would be free effort (Davis, 1989). As for an Information system(IS) use (usage) refers to and manner in which a person utilizes the capabilities of an information systems (Petter et al, 2008),2.3. Internal ControlAn internal control consists of policies and procedures designed to provide a reasonable assurance to management that the company has accomplished its goals and objectives (Elder et al, 2010). The reason for management to design an effective internal control system is so as to achieve three main goals, namely: (1) reliability of financial statements, (2) effectiveness and efficiency of company’s operations, and (3) compliance to laws and regulations (Messier et al, 2006).An internal control system consists of some components, namely: a) the control environment, (b) the entity’s risk assessment process, (c) the information systems and communications, (d) the control activities, and (e) the monitoring and controls (Bodnar & Hoopwod, 2010). The components of internal control are designed and implemented by management to assure reasonably that the goals of internal control will be achieved (Arens, 2008). Then, so as to assure that each component of an internal control system is implemented in a spesific application system contained in an organization’s every transaction cycle, the company designs a transaction processing internal control (Bodnar & Hoopwod, 2010). A transaction processing control consists of a general control and an application control.A general controls are designed to assure that information processing is undertaken in a reasonably control and consistent environment. These control have an impacts on the effectiveness of the application controls and processing functions that involves the use of the accounting information`system (Nash & Heagy, 1993). A general control consists of (Bodnar & Hoopwod, 2010:149)•The plan of data processing organization: Segretation of duties; responsibility for authorization, custody, and record keeping for handling and processing of transaction.•General operating procedures: definition of personel, reliability of personnel, training of personnel, competence of personnel, rotaion of duities, form design, prenumbered forms.•Equipment control features: Backup and recovery, transaction trail, error-sources statistics.Equipment and data-access controls: Secure custody, dual access/dual controlOn the other side, an application control is designed to control accounting applications so as to secure the completeness and accuracy, appropriate authorization, and transaction processing validation (Nash & Heagy, 1993). An application control consists of (Bodnar & Hoopwod, 2010):•Input controls, are designed to prevent or detect errors in the input stage of data processing. Typical input control include: Authorization, exception input, passwords, bacth serial number, control registers, amount control total, document control total, line control total, hash total, sequence cheking, completeness cheking, check digit, expiration etc.•Process controls, are designed to provide assurances that processing has occurred according to intended specifications and that no transactions have been lost or incorrectly inserted into the processing stream.Typical processing control include: Mechanization, default option, run-to-run totals, celaring account, summary processoing, automated error correction.•Output controls, are designed to check that input and processing resulted in valid output and that outputs are distributed properly. Typical ouput control include: Reconciliation, aging, suspense file, suspense account, periodic audit, discrepancy reports, upstream resubmission3. Theoretical Framework3.1. Internal Control and Accounting Information Systems SuccessAccounting information system success is influenced by the effectiveness of internal controlling system. An effective internal control can assure the appropriateness of data entry works, processing techniques, storage methods, and the accuracy of information produced (O Brien & Marakas, 2010). Internal controlling system is designed to monitor and keep the quality and security of information system activities in implementing input, process, and output activities (O Brien & Marakas, 2010). The development of an internal control in a computer-based accounting information system will help management protects corporate assets from suffering losses and embezzlement and keeps company financial data accuracy (Jones & Rama, 2003). Neither accounting information nor record keeping system will not success processing all transactions without an internal control system (Millchamp & Taylor, 2008).The results of prior study showed that an internal control has significant influence on the effectiveness of an accounting information system. A study by Iceman & Hilson (2012) concluded that, on average, accounting errors in weak internal control systems were reported more than in strong internal control systems. Guan (2006) offered an essential concept on the implementation of an internal control in an accounting information system toprotect integrally or to minimize the probability of occurrence of errors or frauds originated in accounting information systems.3.2. Internal Control and Quality of Accounting InformationThe goal of an internal control in an organization is to assure that all transactions are recorded in accurate numbers, in appropriate accounts, and in proper accounting periods so as to enable the presentation of financial statements in accordance with relevant accounting and legal standards (Millchamp & Taylor 2008). Companies are required to develop an internal control intended to provide a reasonable assurance that their financial statements have been presented fairly (Arens et al, 2008). A financial statement will probably not comply accounting standards (GAAP) if internal control over financial statements were inadequate (Arens, 2008).The effects of an internal control on the quality of accounting information are also substantiated by the results of some prior study. The result of Ronald & Houmes (2012) studied indicated that the students of two universities involved in their study increasingly understood that internal control has a significant effect on the reliability of a financial statement. A weak internal control results in weak revenue recognition, segretation of duties, and period end reports and inappropriate accounts reconciliation (Ge & McVay, 2005). The results of study by Doyle, Ge W & Mc Vay (2007) showed that the weakness of internal control has an effect on the low quality of accruals add more the evidences of the existence of an effect internal control on the quality of an accounting information.3.3. Accounting Information System Success and Quality of Accounting InformationAn accounting information system may help managers by providing information needed for them o implement managerial functions (O Brien, 1996). The purpose of an accounting information system is to produce financial statements designated for both external and internal users (Scot, 1986). Meanwhile, Hall (2010) suggested that, fundamentally, the purposes of an accounting information system are to: (a) present information on the organizational resources used, (b) present information related to management decision making, and (c) present information in order to help operational personnel successfully implement their duties in efficient and effective ways. Then, the main purpose of companies in building an accounting information system is to process accounting data so as to transform it into accounting information that is needed by many user to reduce risks in decision making (Azhar Susanto, 2008).The effectiveness of an accounting information system is related to the activities of data collection, inputing, p rocessing, and storage as well as to accounting information reporting management and control for organizations to obtain accounting information of high quality (Pairat, 2012). Accounting information system success may enhance the accuracy of financial statements (Salehi et al, 2000). Moreover, the effectiveness of an accounting information system may affect the increase of financial statement quality and accelerate corporate transaction processes (Sajadi et al, 2008).4. Study Models and HypothesisBased on the prior literature discussion, the conceptual model is shown in figure below:Figure: Theoretical Framework ModelTo test this model, the following hypothesis were proposed as follows:H.1: Internal control system affects the quality of an accounting information systemH.2: Internal control system affects the quality of accounting informationH.3: The quality of accounting information system affects the quality of accounting information5. MethodologyThe research objects are the internal control system, the quality of accounting information system, and thequality of accounting information. The population in this study is consists of 85 ministries and public institutions of Republic of Indonesia. The observation unit consists of those personnel that are involved in implementing accounting activities, namely: input data processing personnel, financial statement providers, and the heads of accounting departments. The sample is picked up randomly by a random sample technique. This study uses primary data collected by spreading questionnaire by mail (mail survey) to each of the respondents. The data collected is then tested for its validity and reliability so that the data is valid to be processed. Then, the data is analyzed descriptively in order to describe the characteristics of each research variable. The data will be analyzed is by using path analysis with consideration of the pattern of relationships between variables that are correlative, causality and recursive. Each hypothesis to be tested by a statistical t test: Ho is rejected if tcount> tcritical, α = 0.05 level.6. ConclusionsThe model developed in this study may explain the influence of the internal control system on the quality of accounting information systems and the quality of accounting information. The model will enable we examine and predict whether the components of internal control systems have been adequately applied in accounting information systems. The results of this study later, is specifically will show the components or dimensions of any system of internal control which is the main cause of weak internal control systems of ministries and state agencies of the Republic of Indonesia. Thus, based on the findings of this study, the author will propose some suggestions for improving the effectiveness of internal control system so that the quality of accounting information systems for the better. Accordingly, the financial statements of the ministries and state agencies of the Republic Indonesia can be provided in accordance with high quality standards.ReferencesAllan Millchamp & John Taylor, (2008). Auditing, 9th ed., South Western, P. 85, 86Alvin A. Arens, Randal J. Elder, & Mark S. Beasly, (2008). Auditing dan Jasa Assurance, Pendekatan Terintegrasi, Edisi ke-12, Jilid 1, Bahasa Indonesia language edition published by Penerbit Erlangga. Jakarta. P. 371, 373, 375Azhar Susanto, (2008). Sistem Informasi Akuntansi: Struktur Pengendalian Risiko Pengembangan. Edisi Perdana, Lingga Jaya, Bandung, P.8Azhar Susanto, (2009). Sistem Informasi Manajemen: Pendekatan Terstruktur Resiko Pengembangan. Edisi Perdana, Lingga Jaya, Bandung.Baltzan, Paige, (2012). Business Driven Information System. 3rd Edition NY: McGraw-Hill, P. 14)Delon, W.H. & Mclean, E.R., (1992). Information Success The Quest For Dependent Variable, Information System Research, Vol. 3. No. 1, Pp. 60-95Dellon, W.H. Delon & Ephraim R. Mclean, 2003. The Delon and McLean Model of Information Systems Succes: A Ten Years Update, Journal Of Management Information Systems/ Spring 2003. Vol. 19, No. 4. Pp. 9-30. F. Davis, (1989). Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Quartely, 13, September, Pp. 319-340Donald E. Kieso, Jerry Weygandt, & Terry D. Warfield, (2012). Intermediate Accounting. 14th Edition. UK: John Willey and Sons, Inc. Pp.5-6Don R. Hansen, & Maryanne M. Mowen, (1995). Cost Management Accounting And Control. South Western College Publishing. P.35Doyle, J., Ge W, and McVay, S., (2007). Accrual Quality and Internal Control Over Financial Reporting. Accounting Review, Vol 82. No. 5. Pp. 1141-1170.Frederich L. Jones and Dasaratha V. Rama., (2003). Accounting Information Systems,A Business Process Approach. :South Western, P. 7Gamawan Fauzi, (2012). Target 50% Daerah WTP Pada Tahun 2014 Sulit Dicapai. Harian Kompas, Rabu, 25 Juli, P. 4.George Scot, (1996Ge W and McVay, S., (2005). The Disclosure of Material Weakness in Internal Control After The Sarbanes-Oxley Act. Accounting Horizons, Vol. 19. No. 3. Pp. 137-158.Gelinas, Ulrich, A. Oram & W. Wriggins, (1990). Accounting Information Systems. Boston: Pwskent Publishing Company.Gelinas, Ulrich & Dull , B. Richard, (2012). Accounting Information Systems, 9th ed. South Western Cengage Learning. 5191 Natorp Boulevard Mason, USA. P. 19George H. Bodnar , William S. Hoopwood, (2010). Accounting Information Systems, 10th ed. NJ: Prentice Hall. P.1, 49, 133 &151.George M. Scott, (1986). Principles Of Management Information Systems. NY: Mc-Graw-Hill. P.Glover Messier & Prawitt, (2006). Auditing and Assurance Services: A Systematic Approach. 4th ed. NY: McGraw-Hill. P.220-----------------------, (2011). LKPP (2010 Wajar Dengan Pengecualian. Warta BPK, edisi 05-Vol Mei, pp. 12-13. Halim Alamsyah, (2011). Bank Indonesia Akui Banyak Bank Dibobol Karena Pengawasan Internal Memble. /2011/07/07/bi-akui-banyak-bank-dibobol- karena- pengawasan-internal- memble/ Jakarta,Rabu (22/06).Iceman & Hillson, (1990). Distribution of Audited Detected Errors Parttioned by Internal Control. Journal of Accounting, Auditing & Finance. Vol. 5. No. 4. Pp. 527-548.James A. Hall, (2011). Accounting Information System. 7th ed, South-Western Publishing Co. p. 11-14James A. O’Brien & George M. Marakas, (2010). Management Information Systems: Managing Information Technology In The Bussiness Enterprise.15th ed. NY: McGraw-Hill. P.353, 495James A. O’Brien & George M. Marakas, (2004). Management Information Systems: Managing Information Technology In The Bussiness Enterprise. 10th ed. NY: McGraw-Hill.James A. O’Brien & George M. Marakas, 1996. Management Information Systems: Managing Information Technology In The Bussiness Enterprise. 13rd Ed. NY: McGraw-Hill. P. 365James O. Hickss Jr., (1993). Management Information Systems: A User Perspective. 3rd ed: West Publishing Co. P. 67-68John F. Nash & Cynthia D. Heagy, (1993). Accounting Information Systems, 3rd ed, South-Western Publisihing Co. P. 484 & 497Mahdi Salehi, Vahab Rostami, & Abdolkarim Mogadam, (2000). Usefulness of Accounting Information in Emerging Economy: Emperical Evidence of Iran, Journal Revista De Contabilidad-Spanish Accounting Review (pp.Maurice L. Hirsch, Jr., (1994). Advanced Management Accounting, 2nd: South Western Publishing. P. 17 McLeod Raymond, (2007). Sistem Informasi Manajemen. Edisi Ke-7, Versi Bahasa Indonesia, Jakarta: PT. PrenhallindoNancy A. Bagranof, Mark G. Simkin, & Carolyn S. Norman, (2010). Accounting Information Systems. Seventh Edition: South-Western. P. 5Pornpandejwittaya & Pairat, (2012). Effectiveness of AIS: Effect on Performance of Thai-Listed Firms In Thailand, International Journal Of Business Research, July, 2012. Vol 12 Issue 3.Randal J. Elder, Mark S. Beasley, & Alvin A. Arens, (2010). Auditind and Assurance Sevices An Integrated Approach. NJ: Prentice-Hall. P . 290Romuald A. Stone, (1994). Leadership and information System Management: A Literatur review, Computers In Human Behavior. Vol. 10, Issue 4, Winter. pp. 559-568.Ronald F. Premuroso, Robert Houmes, (2012). Financial Statement Risk Assessment Following the COSO Framework: An Instructional Case Study. International Journal of Accounting and Information Management, Vol. 20. No. 1. Pp. 26-48.Sacer, Ivana M., Zager K., and Tusek B. (2006). Accounting Information System’s Quality as The Ground For Quality Business Reporting, IAIDS International Conference e-commerce, ISBN: 972-8924-23-2. P. 6, 62 Sajadi, H. M. Dastgir, & H. Hashem Nejad, (2008). Evaluation of The Effectiveness of Accounting Information Systems, International Journal Of Information & Technology Science, Vol. 6, No. 2, July & Dec.Seddon P, (1997). Respecification and Extension of The delone and McLean Model of IS Success”, Information Systems Research, Vol. 8 Issue 3, pp. 240-253.Soesilo Bambang Yudhoyono, (2013). Masih Ada Kebocoran Pajak, Berat Capai Target Pajak 2013.Harian Kompas. Jum’at, 22 Maret, Hal. 17Stacie Petter, William DeLone, & Ephraim McLean, (2008). Measuring information systems success: models, dimensions, measures, and interrelationships. European Journal of Information Systems, pp. 236-263Stair, Ralph M. & George W. Reynolds, (2010). Principles Of Information Systems, Course Technology. 9th Editions. NY: Mc-Graw-Hill. P. 7, 57Wang, R. Y. and Strong, D.M., (1996). Beyond accuracy: What data quality means to data consumers. Journal of Management Information Systems, Vol. 12, No. 4, pp. 5-33.Yuhong Guan, Yuhong Guan, (2006). A Study on The Internal Control of Accounting Information Systems. International Confrence on Computer and Communication Technologies in Argiculture Engineering, Januari, 12.。

The our country accounting firm trustworthiness studies currentlyAbstract: Trustworthiness is the soul of CPA ethics and the reputation of an honest-based Accountants Affairs Office is more important than the outstanding achievement. And the honesty of an Accountants Affairs is also an important part of social credit system. If some certified public accountants pay out the trustworthiness in breach of faith principle, not only risk and failure but also they will lose the limit trustworthiness wealth which is existent-relied, and the value of the existence of Accountants Affairs Office is nothing left. Therefore, to solve the problem of trustworthiness loss and strengthen the construction of trustworthiness is urgent affair. This thesis mainly illustrates the concrete meaning and requirement of honesty among certified public accountants, sums up the status quo that our country’s CPA impress the trustworthiness construction of entire trade due to the deficiency of professional ability and independence, analyzes the reasons of honesty loss are not only the internal reason that driving by benefit to lose independence but also the exterior reason such as information asymmetry, assigning mechanism is not so nice, organizing structure is defective and some others, and the thesis also provide some advice and strategy to strengthen the trustworthinessconstruction of CPA trade.目前我国会计师事务所诚信研究摘要:诚信是注册会计师职业道德的精髓,以诚信为核心的会计师事务所声誉比业绩更重要,会计师事务所诚信是社会信用制度的重要组成部分。

本科毕业论文(设计)外文翻译外文出处Journal of Accountancy;Aug80, V ol.150 Issue 2,P105-120,16p外文作者Miller, Paul B. W.原文:Statement of Financial Accounting Concepts No.2—Qualitative Characteristics of Accounting InformationPrimary Decision-Specific QualitiesRelevance and reliability are the two primary qualities that make accounting information useful for decision making. Subject to constraints imposed by cost and materiality, increased relevance and increased reliability are the characteristics that make information a more desirable commodity-that is, one useful in making decisions. If either of those qualities is completely missing, the information will not be useful. Though, ideally, the choice of an accounting alternative should produce information that is both more reliable and more relevant it may be necessary to sacrifice some of one quality for a gain in another.To be relevant, information must be timely and it must have predictive value or feedback value or both. To be reliable, information must have representational faithfulness and it must be verifiable and neutral. Comparability, which includes consistency, is a secondary quality that interacts with relevance and reliability to contribute to the usefulness of information. Two constraints are include in the hierarchy, both primarily quantitative in character. Information can be useful and yet be too costly to justify providing it. To be useful and worth providing, the benefits of information should exceed its cost. All of the qualities of information shown are subject to a materiality threshold, and that is also shown as a constraint.RelevanceRelevant accounting information is capable of making a difference in a decision by helping users to form predictions about the outcomes of past, present and future events or to confirm or correct prior expectations. Information can make a difference to decisions by improving decision makers’ capacities to predict or by providing feedback on earlier expectations. Usually, information does both at once, because knowledge about the outcomes of actions already taken will generally improve decision makers’ abilities to predict the results of similar future actions. Wit hout a knowledge of the past, the basis for a prediction will usually be lacking. Without an interest in the future, knowledge of the past is sterile.Timeliness, that is, having information available to decision makers before it loses its capacity to influence decisions, is an ancillary aspect of relevance. If information is not available when it is needed or becomes available so long after the reported events that it has no value for future action, it lacks relevance and is of little or no use. Timeliness alone cannot make information relevant, but a lack of timeliness can rob information of relevance it might otherwise have had.ReliabilityThe reliability of a measure rests on the faithfulness with which it represents what it purports to represent, coupled with an assurance for the user that it has that representational quality. To be useful, information must be reliable as well as relevant. Degrees of reliability must be recognized. It is hardly ever a question of black or white, but rather of more reliability or less. Reliability rests upon the extent to which the accounting description or measurement is verifiable and representational faithful. Neutrality of information also interacts with those two components of reliability to affect the usefulness of the information.Verifiability is a quality that may be demonstrated by securing a high degree of consensus among independent measures using the same measurement methods. Representational faithfulness, on the other hand, refers to the correspondence or events those numbers purport to represent. A high degree of correspondence, however, does not guarantee that an accounting measurement will be relevant to the user’s needs if the resources or events represented by the measurement are inappropriate tothe purpose at hand.Neutrality means that, in formulating or implementing standards, the primary concern should be the relevance and reliability of the information that results, not the effect that the new rule may have on a particular interest. A neutral choice between accounting alternatives is free from bias towards a predetermined result. The objectives of financial reporting serve many different information users who have diverse interests, and no one predetermined result is likely to suit all interests.Comparability and ConsistencyInformation about a particular enterprise gains greatly in usefulness, if it can be com pared with similar information about other enterprises and with similar information about the same enterprise for some other period or some other point in time. Comparability between enterprises and consistency in the application of methods over time increases the informational value of comparisons of relative economic opportunities or performance. The significance of information, especially qua ntitative information, depends to a great extent on the user’s ability to relate it to some benchmark.MaterialityMateriality is a pervasive concept that relates to the qualitative characteristics, especially relevance and reliability. Materiality and relevance are both defined in terms of what influences or makes a difference to a decision maker, but the two terms can be distinguished. A decision not to disclose certain information may be made, say, because investors have no need for that kind of information (it is nit relevant) or because the amounts involved are too small to make a difference (they are not material). Magnitude by itself, without regard to the nature of the item and the circumstances in which the judgment has to be made, will not generally be a sufficient basis for a materiality judgment. The Board’s present position is that no general standards of materiality ban be formulated to take into account all the considerations that enter into an experienced human judgment. Quantitative materiality criteria may be given by the Board in specific standards in the future, as in the past, as appropriate.Source: Journal of Accountancy;Aug80, V ol.150 Issue 2, P105-120,16p译文:财务会计概念的声明——会计信息质量特征制定具体决策的主要特征相关性和可靠性是使会计信息对于制定决策有用的最主要的两个特征。

The Optimization Method of Financial Statements Based on Accounting Management TheoryABSTRACTThis paper develops an approach to enhance the reliability and usefulness of financial statements. International Financial Reporting Standards (IFRS) was fundamentally flawed by fair value accounting and asset-impairment accounting. According to legal theory and accounting theory, accounting data must have legal evidence as its source document. The conventional “mixed attribute” accounting system should be re placed by a “segregated” system with historical cost and fair value being kept strictly apart in financial statements. The proposed optimizing method will significantly enhance the reliability and usefulness of financial statements.I.. INTRODUCTIONBased on international-accounting-convergence approach, the Ministry of Finance issued the Enterprise Accounting Standards in 2006 taking the International Financial Reporting Standards (hereinafter referred to as “the International Standards”) for reference. The Enterprise Accounting Standards carries out fair value accounting successfully, and spreads the sense that accounting should reflect market value objectively. The objective of accounting reformation following-up is to establish the accounting theory and methodology which not only use international advanced theory for reference, but also accord with the needs of China's socialist market economy construction. On the basis of a thorough evaluation of the achievements and limitations of International Standards, this paper puts forward a stand that to deepen accounting reformation and enhance the stability of accounting regulations.II. OPTIMIZA TION OF FINANCIAL STATEMENTS SYSTEM: PARALLELING LISTING OF LEGAL FACTS AND FINANCIAL EXPECTA TIONAs an important management activity, accounting should make use of information systems based on classified statistics, and serve for both micro-economic management and macro-economic regulation at the same time. Optimization of financial statements system should try to take all aspects of the demands of the financial statements in both macro and micro level into account.Why do companies need to prepare financial statements? Whose demands should be considered while preparing financial statements? Those questions are basic issues we should consider on the optimization of financial statements. From the perspective of "public interests", reliability and legal evidence are required as qualitative characters, which is the origin of the traditional "historical cost accounting". From the perspective of "private interest", security investors and financial regulatory authoritieshope that financial statements reflect changes of market prices timely recording "objective" market conditions. This is the origin of "fair value accounting". Whether one set of financial statements can be compatible with these two different views and balance the public interest and private interest? To solve this problem, we design a new balance sheet and an income statement.From 1992 to 2006, a lot of new ideas and new perspectives are introduced into China's accounting practices from international accounting standards in a gradual manner during the accounting reform in China. These ideas and perspectives enriched the understanding of the financial statements in China. These achievements deserve our full assessment and should be fully affirmed. However, academia and standard-setters are also aware that International Standards are still in the process of developing .The purpose of proposing new formats of financial statements in this paper is to push forward the accounting reform into a deeper level on the basis of international convergence.III. THE PRACTICABILITY OF IMPROVING THE FINANCIAL STATEMENTS SYSTEMWhether the financial statements are able to maintain their stability? It is necessary to mobilize the initiatives of both supply-side and demand-side at the same time. We should consider whether financial statements could meet the demands of the macro-economic regulation and business administration, and whether they are popular with millions of accountants.Accountants are responsible for preparing financial statements and auditors are responsible for auditing. They will benefit from the implementation of the new financial statements.Firstly, for the accountants, under the isolated design of historical cost accounting and fair value accounting, their daily accounting practice is greatly simplified. Accounting process will not need assets impairment and fair value any longer. Accounting books will not record impairment and appreciation of assets any longer, for the historical cost accounting is comprehensively implemented. Fair value information will be recorded in accordance with assessment only at the balance sheet date and only in the annual financial statements. Historical cost accounting is more likely to be recognized by the tax authorities, which saves heavy workload of the tax adjustment. Accountants will not need to calculate the deferred income tax expense any longer, and the profit-after-tax in the solid line table is acknowledged by the Company Law, which solves the problem of determining the profit available for distribution.Accountants do not need to record the fair value information needed by security investors in the accounting books; instead, they only need to list the fair value information at the balance sheet date. In addition, because the data in the solid line table has legal credibility, so the legal risks of accountants can be well controlled. Secondly, the arbitrariness of the accounting process will be reduced, and the auditors’ review process will be greatly simplified. The independent auditors will not have to bear the considerable legal risk for the dotted-line table they audit, because the risk of fair value information has been prompted as "not supported by legalevidences". Accountants and auditors can quickly adapt to this financial statements system, without the need of training. In this way, they can save a lot of time to help companies to improve management efficiency. Surveys show that the above design of financial statements is popular with accountants and auditors. Since the workloads of accounting and auditing have been substantially reduced, therefore, the total expenses for auditing and evaluation will not exceed current level as well.In short, from the perspectives of both supply-side and demand-side, the improved financial statements are expected to enhance the usefulness of financial statements, without increase the burden of the supply-side.IV. CONCLUSIONS AND POLICY RECOMMENDATIONSThe current rule of mixed presentation of fair value data and historical cost data could be improved. The core concept of fair value is to make financial statements reflect the fair value of assets and liabilities, so that we can subtract the fair value of liabilities from assets to obtain the net fair value.However, the current International Standards do not implement this concept, but try to partly transform the historical cost accounting, which leads to mixed using of impairment accounting and fair value accounting. China's accounting academic research has followed up step by step since 1980s, and now has already introduced a mixed-attributes model into corporate financial statements.By distinguishing legal facts from financial expectations, we can balance public interests and private interests and can redesign the financial statements system with enhancing management efficiency and implementing higher-level laws as main objective. By presenting fair value and historical cost in one set of financial statements at the same time, the statements will not only meet the needs of keeping books according to domestic laws, but also meet the demand from financial regulatory authorities and security investorsWe hope that practitioners and theorists offer advices and suggestions on the problem of improving the financial statements to build a financial statements system which not only meets the domestic needs, but also converges with the International Standards.基于会计管理理论的财务报表的优化方法摘要本文提供了一个方法,以提高财务报表的可靠性和实用性。

有关会计信息质量的参考文献会计信息质量参考文献1. Beneish, M. D. (1999). Detecting earning manipulation. Financial Analysts Journal, 55(2), 24-36.2. Ballas, V., & Galanis, G. (2003). Investigating audit quality in the audit market: An empirical analysis. Managerial Auditing Journal, 18(8), 544-555.3. Ferguson, R., Gordon, S.B. and Feroz, E. (2004). The Effects of SFAS No. 133 on Financial Reporting Quality. Financial Analysts Journal, 60(4), 35-48.4. Cohen, J. R., & Zarowin, P. (1999). Accruals manipulation and external fraud: Evidence from a focus study. The Accounting Review, 74(3), 423-437.5. Kumar, A., and Subramanyam, K. R. (2001). Quality of accruals and Earnings Management. Accounting Review, 76(3), 459-473.6. Ahmed, A.S., and Duellman, S.C. (2005). Effects of Earnings Management on the Quality of Financial Reporting: A Review and Research Opportunities. Journal of Accounting and Public Policy, 24(5), 361-386.7. Dechow, P. M., Hull, R. and Sloan, R. G. (2005). Enforcement of Accounting Rules When Incentives and Opportunities Differ: Evidence from the Toxic Releases Inventory. Journal of Accounting and Economics, 39(3), 307-337.8. Robison, S., and Johnson, S (2006). An Examination of Auditor Quality, Audit Committees, and Financial Reporting Quality. TheAccounting Review, 81(1), 139-161.9. Gonedes, N.J. (2007). Reducing Earnings Management Opportunities: Fair Value Accounting and Other Strategies. Managerial Auditing Journal, 22(2), 139-152.10. Brown, L., Lo, K., and Lys, T. Z. (2008). Earnings Management and Corporate Governance: The Role of the Board and the Audit Committee. Journal of Corporate Finance, 14(3), 257-274.。

中英文对照外文翻译文献(文档含英文原文和中文翻译)译文:译文(一)世界贸易的飞速发展和国际资本的快速流动将世界经济带入了全球化时代。

在这个时代, 任何一个国家要脱离世界贸易市场和资本市场谋求自身发展是非常困难的。

会计作为国际通用的商业语言, 在经济全球化过程中扮演着越来越重要的角色, 市场参与者也对其提出越来越高的要求。

随着市场经济体制的逐步建立和完善,有些国家加入世贸组织后国际化进程的加快,市场开放程度的进一步增强,市场经济发育过程中不可避免的各种财务问题的出现,迫切需要完善的会计准则加以规范。

然而,在会计准则制定过程中,有必要认真思考理清会计准则的概念,使制定的会计准则规范准确、方便操作、经济实用。

由于各国家的历史、环境、经济发展等方面的不同,导致目前世界所使用的会计准则在很多方面都存在着差异,这使得各国家之间的会计信息缺乏可比性,本国信息为外国家信息使用者所理解的成本较高,在很大程度上阻碍了世界国家间资本的自由流动。

近年来,许多国家的会计管理部门和国家性的会计、经济组织都致力于会计准则的思考和研究,力求制定出一套适于各个不同国家和经济环境下的规范一致的会计准则,以增强会计信息的可比性,减少国家各之间经济交往中信息转换的成本。

译文(二)会计准则就是会计管理活动所依据的原则, 会计准则总是以一定的社会经济背景为其存在基础, 也总是反映不同社会经济制度、法律制度以及人们习惯的某些特征, 因而不同国家的会计准则各有不同特点。

但是会计准则毕竟是经济发展对会计规范提出的客观要求。

它与社会经济发展水平和会计管理的基本要求是相适应的,因而,每个国家的会计准则必然具有某些共性:1. 规范性每个企业有着变化多端的经济业务,而不同行业的企业又有各自的特殊性。

而有了会计准则,会计人员在进行会计核算时就有了一个共同遵循的标准,各行各业的会计工作可在同一标准的基础上进行,从而使会计行为达到规范化,使得会计人员提供的会计信息具有广泛的一致性和可比性,大大提高了会计信息的质量。

会计信息质量在投资中的决策作用对私人信息和监测的影响安妮比蒂,美国俄亥俄州立大学瓦特史考特廖,多伦多大学约瑟夫韦伯,美国麻省理工学院1简介管理者与外部资本的供应商信息是不对称的在这种情况下企业是如何影响金融资本的投资的呢?越来越多的证据表明,会计质量越好,越可以减少信息的不对称和对融资成本的约束。

与此相一致的可能性是,减少了具有更高敏感性的会计质量的公司的投资对内部产生的现金流量。

威尔第和希拉里发现,对企业投资和与投资相关的会计质量容易不足,是容易引发过度投资的原因。

当投资效率低下时,会计的质量重要性可以减轻外部资本的影响,供应商有可能获得私人信息或可直接监测管理人员。

通过访问个人信息与控制管理行为,外部资本的供应商可以直接影响企业的投资,降低了会计质量的重要性。

符合这个想法的还有比德尔和希拉里的比较会计对不同国家的投资质量效益的影响。

他们发现,会计品质的影响在于美国投资效益,而不是在日本。

他们认为,一个可能的解释是不同的是债务和股权的美国版本的资本结构混合了SUS的日本企业。

我们研究如何通过会计质量灵敏度的重要性来延长不同资金来源对企业的投资现金流量的不同影响。

直接测试如何影响不同的融资来源会计,通过最近获得了债务融资的公司来投资敏感性现金流的质量的效果,债务融资的比较说明了对那些不能够通过他们的能力获得融资的没有影响。

为了缓解这一问题,我们限制我们的样本公司有所有最近获得的债务融资和利用访问的差异信息和监测通过公共私人债务获得连续贷款的建议。

我们承认,投资内部现金流敏感性可能较低获得债务融资的可能性。

然而,这种可能性偏见拒绝了我们的假设。

具体来说,我们确定的数据样本证券公司有1163个采样公司(议会),通过发行资本公共债务或银团债务。

我们限制我们的样本公司最近获得的债务融资持有该公司不断融资与借款。

然而,在样本最近获得的债务融资的公司,也有可能是信号,在资本提供进入私人信息差异和约束他们放在管理中的行为。

相关理论意味着减少公共债务持有人获取私人信息,因而减少借款有效的监测。

在这些参数的基础上,我们预测,会计质量应该有一个对企业的投资现金流比与银行债务的公共债务公司影响较大,。

第二,我们预计,对公司的会计质量的投资波利效果,资本投资者入境计划,将取决于是否贷款合同限制投资。

我们预测,当企业面临投资合同限制,过度投资问题是部分需要解决的,会计质量变得不那么值钱了,不太可能影响到投资现金流灵敏度。

提供关于这些假设的证据,我们估计的投资模型内部现金流分别进行公司抽样调查,只有公共债务问题,有问题的公司,银团贷款的样本。

在这些回归中,我们与我们的互动措施的现金流量变量会计质量调查是否影响会计质量的投资现金流敏感性。

对于银行的样本,我们进一步互动的现金流和会计质量变量的乘积投资限制的变量,以研究是否资本开支公约影响投资现金流敏感性。

我们同时采用了普通最小二乘法(OLS)和内源性转换模型的估计,以解决潜在的样本选择偏差与银行的债务从公众产生融资选择。

我们第一阶段的决定因素模型,融资与私人债务市场遵循Bharath。

我们估计第二阶段的投资模型回归政权分开对企业具有公共与私人债务。

这些制度的回归也在资本开支内生性控制公约的选择使用从决定因素第一阶段回归模型拟合值包括在债务合同的投资限制。

与以前的研究结果一致,我们发现,投资是敏感的内部现金流量和投资现金流敏感性都会较高地降低公司会计质量。

这些结果说明了双方的举行与内生转换模型回归。

我们还发现,两个估计技术,减少投资限制,投资现金流敏感性,降低了会计质量的重要性。

在这总体样本的分析使用中,我们没有发现二者之间的关系类型的贷款人提供资金和会计质量影响投资现金流的敏感性。

在一系列的敏感性分析中,我们也考虑了可能性,投资现金流敏感性获取信息不仅仅是financ-荷兰国际集团的制约,但关于公司的投资机会也是为了解决这个问题的关注,我们研究的资金来源与投资现金的影响流敏感性的财政约束与无约束的企业公司不同。

要确定企业财务约束,我们使用的事前定义金融约束的基础上,吴怀特德2004指数。

我们预期该公司的财务约束投资,谁拥有更大的信息不对称问题,谁将更加依赖于内部产生的资金。

同样,投资现金流敏感性为财政浓度,紧张的企业将取决于会计信息的品质,私人信息的存在,以及合同投入使用限制。

根据这些推测,我们发现,对于经济约束事务所、会计师质量是同样重要的投资在减少,在私人信息存在现金流敏感性。

这些结果支持这一假说,即私人信息和会计质量作为替代品。

在第二个敏感性分析,我们采用资产负债表的流动性方法,去解决发展中捕获的我们关注的机会现金流措施影响现金流和协会之间的投资目的。

阿尔梅达Campello和魏兹巴赫(2004)认为更换与现金持有量的变化会减少投资的进而影响投资机会集合,如现金余额变动应与融资约束的情况下的投资机会相一致。

与以往的结果是相同的,我们发现,会计质量降低现金流量的敏感性,但贷款人获得私人信息减少了这种影响。

我们的研究结果证实了在麻省理工学院会计质量的重要性,信息不对称对投资的负面影响,现金流的敏感度。

我们的研究结果也与比德尔和希拉里的一贯2006年会计质量参数一致,应发挥其作用时,以较低的CAPI-塔尔供应商的选择信息解决问题的缓解机制。

然而,他们没有通过与会计质量发挥的作用不一致来改善投资在债券市场的效率。

我们的论文也拓展了我们对帐户重要性的认识,其手段是识别环境信息,其中该公司的质量会计信息是可能重要的。

当信息-尝试问题可能是最大时,会计信息质量更显得尤为重要。

然而,在这些设置中,如果供应商施加外部资本合同投资限制,或有机会获得私人信息,那么会计质量并不那么重要。