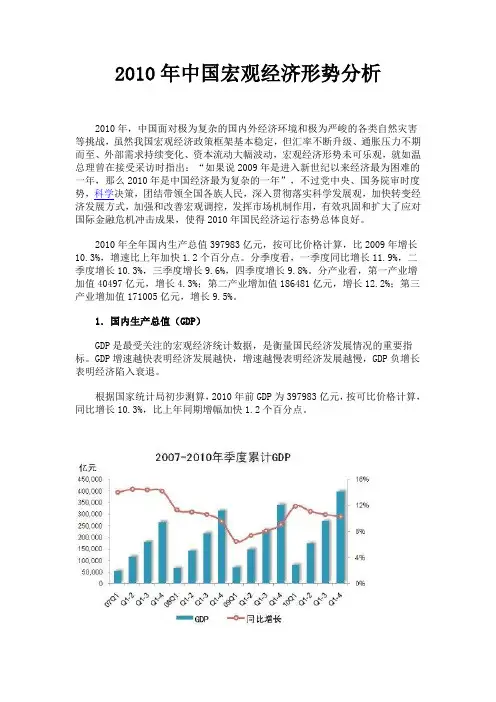

2010年10月国际金融市场运行综述

- 格式:pdf

- 大小:219.95 KB

- 文档页数:4

F|NANelAL 0EV∈LoPMENTs

2010年10月国际金融市场运行综述

Overview of lnternationaI financiaI markets ln October 201 0

中国人民银行上海总部调查统计研究部 Statistics and Research Department,People’S Bank of China Shanghai Head Office

摘要 2010年10月,受市场对美联储重启量化宽松政策的预期影响,美元对主要货币继续走弱。美元、日元短期利率微降, 欧元、英镑短期利率开始回升。美国、英国、德国中长期国债收益率从低位有所回升,日本中长期国债收益率维持低位。 除日本股市下跌外,其他主要股指振荡上涨。 Abstract In October 201 0,impacted by the market expectation of Federal Reserve’S second quantitative easing policy,the US dollar continued to decline against major currencies.Short—term interest rates of USD and JPY dropped slightly,while the rates of EUR and GBP started to rise.Mid—and long—term T-bond yields of the US,UK and Germany increased from a low level,while the yields of Japan remained at a low leve1.Apart from Japan’S stock market,other major stock markets rose with fluctuations.

The US dollar continued to decline against major _currencies

I n 0ctober.the US dollar lndex had a V-shaped trend with fluctuations.1n the first half of this month,

impacted by the market expectation of Federal

Reserve’S second quantitative easing policy and

some negative US econom。ic data,the US dollar

index continued to falI and closed at the year—low of 76.65 on October 1 4.However.in the second

half of October,the market expected that Federal

Reserve’S quantitative easing volume would be smaller than expected,and some strong economic

data were released,SO the US dollar index went up

with fluctuations.Of this,owing to the unexpected

interest rate rises by Chinese central bank,the index

increased by 1.6%on October 1 9.It closed this

month at 77l27.down 1.8%month—on—month. 一 美元对主要货币继续走弱

1 O

国公布的多数经济数据表现不佳(如9月非农就业人

1:3、8月工厂订单)等因素影响,美元指数延续上月 跌势继续走低,14日收于年内低点76 65。下半月,

因市场认为美联储量化宽松规模或不如之前预期,公

布的一些经济数据(如9月零售销售、新屋开工、新 屋和成屋销售、10月美国经济咨商会消费者信心指数、

9月耐用品订单等)强于预期.美元指数在振荡中有

所回升。其问.受中国央行意 ̄,I,/JD息影响 美元指数 1 9日单日上涨1.6%。月末.美元指数收于77.27,

较上月末下跌1.8%。 欧元兑美元汇率前期上升.后期盘整。月初以

来,欧元区公布了一些表现良好的经济数据(如10

月Sentix投资者信心指数好于预期、二季度GDP季率 增速创4年最高等).而美国欲重启量化宽松货币政策,

84.0O 83.O0 82.OO 81 0O 8&O0 79.00 78.0O 77.0O 76.0O 09.O1 O9-15 09-29 10-13 1 0_27

受此影响.欧元兑美元汇率振荡上升,14日收于8个

月来高点1.4078。其后.由于欧元区公布的经济数据 好坏不一(如10月综合采购经理人指数不及预期、8 月工业订单和10月经济景气指数好于预期等).欧元

兑美元汇率呈盘整走势。月末,欧元兑美元汇率收于

1 3947 较上月末上升2.3%。 英镑兑美元汇率呈 型走势。上半月,市场

对美联储将重启量化宽松的预期升温,英国9月服务

业采购经理人指数和9月D Pl数据强于预期.因此, 英镑汇率总体上升.14日收于8个月来高点1.6007。

其后,因英国公布的经济数据表现疲弱(如10月工

业订单降至4个月来低点、9月零售销售不及预期等),

市场预期英格兰银行可能将重启量化宽松政策,英镑 汇率振荡下行至22日。此后.在英国三季度GDP增

速超预期、标准普尔将英国经济前景评级由”负面”

上调为“稳定”等因素影响下,英镑兑美元汇率上涨。

月末 英镑兑美元汇率收于1 6038.较上月末上升 2 1%。

美元兑日元汇率下降。本月,由于市场预期美联

储将进一步实施量化宽松措施,美元兑日元汇率延续 上月末走势振荡下行。尽管日本银行月初宣布降息并

扩大购买证券规模,日本财务大臣也多次重申政府将

在必要时采取包括干预汇市在内的 果断”行动以抑 EUR/USD exchange rate went up with fluctuations

at first,and reached the highest point of 1.4078 in

8 months on October 1 4.1t then cOnsOlidated and

closed this month at 1.3947,up 2.3%compared with the month—ago figure.GBP/USD rate had a N—shaped

trend and reached the highest point of 1.6007 in

8 months on OCtobe r 14.and closed this month

at 1.6038,up 2.1%compared with the month—ago figure.USD/JPY rate kept dropping with fluctuations

in October.and closed this month near a record low

Of 80.39.down 3_7%compared with the month—ago

figure. Short-lerm i眦ere吼rates of USD and JPY dropped slightly,

while the rates Of EUR and GBP started to rise

ln October,European Central Bank and Bank of

England announced to maintain their interest rates, while Bank of Japan announced to cut its benchmark

interest rate frOm 0.1%tO 0.0.1%.1n view of the

attitudes of diferent central banks.FederaI Reserve

would implement second quantitative easing policy, while European Central Bank would maintain its

monetary policy and optimism ove r economic

recovery.Because of the unexpected strong GDP data in Q3,the market expectation of new quantitative

easing policy by Bank of England weakened. Impacted by the above factors.short—term interest

rates of USD and JPYfell_and the USD and JPY 3M

Libor rates closed this month at 0.286%and 0.1 97%

respectively。down 0.4 bp and 1.9 bps month-on-

month respectively.Short—term interest rates of EUR and GBP rose.and the EUR and GBP 3M Libor rates closed this month at 0.987%and 0.741%respectively.

uD 1 3.9 bps and 0.9 bp month-on-month respectively. Mid-and Iong・lerm T_bond yields of the US.UK and

Germany increased from a Iow leve1.while tile yields of

惹0 镰 黯黧鬻 镶

53 国…一…

%

——

一tYr.Li ̄一敲元L 葵镑LIbor… …墨元L淑”

Japan remained at a low level All US T—bond yields went down at the beginning

of October.Of this,the 2Y and 5Y T—bond yields

even hit thei r reco rd low points.and the 1 0Y

T-bond yield also hit the lowest point since Janua ̄

2009.However,these T—bond yields went up with fIuctuations in the middle of October.At end—October.