Introduction Financial__ Accounting

- 格式:ppt

- 大小:610.00 KB

- 文档页数:7

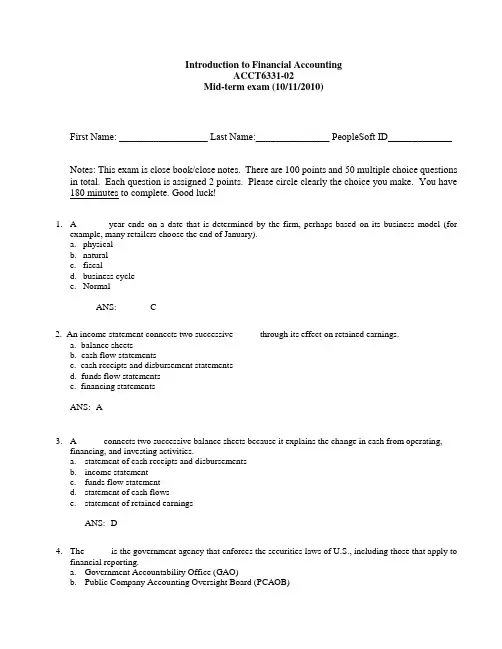

Introduction to Financial AccountingACCT6331-02Mid-term exam (10/11/2010)First Name: __________________ Last Name:_______________ PeopleSoft ID_____________ Notes: This exam is close book/close notes. There are 100 points and 50 multiple choice questions in total. Each question is assigned 2 points. Please circle clearly the choice you make. You have 180 minutes to complete. Good luck!1. A _____ year ends on a date that is determined by the firm, perhaps based on its business model (forexample, many retailers choose the end of January). a. physical natural fiscalbusiness cycle Normal b. c. d. e.ANS: C2. An income statement connects two successive _____ through its effect on retained earnings. a. balance sheetsb. cash flow statementsc. cash receipts and disbursement statementsd. funds flow statementse. financing statementsA ANS: A3. A _____ connects two successive balance sheets because it explains the change in cash from operating,financing, and investing activities.a. statement of cash receipts and disbursementsb. income statementc. funds flow statementd. statement of cash flowse. statement of retained earningsD ANS: D4. The _____ is the government agency that enforces the securities laws of U.S., including those that apply to financial reporting.a. Government Accountability Office (GAO)b. Public Company Accounting Oversight Board (PCAOB)c. International Accounting Standards Board (IASB)d. Financial Accounting Standards Board (FASB)e. U.S. Securities and Exchange Commission (SEC)E ANS: E5. The balance sheet of Allhear, a communications firm, for the year ended December 31, 2009, showedcurrent assets of $20 million, current liabilities of $16 million, shareholders’ equity of $17 million, and noncurrent assets of $29 million.Compute the amount of noncurrent liabilities on Allhear’s balance sheet at the end of 2009.a. $5 millionb. $10 millionc. $12 milliond. $13 millione. $16 millionE ANS: Ecurrent assets of $20 million + noncurrent assets of $29 million = total assets of $49 million=current liabilities of $16 million + noncurrent liabilities + shareholders’ equity of $17million = $49 million, therefore noncurrent liabilities = $16 million6. The income statement of Peoples Motors Corporation, a U.S. automotive manufacturer, for the year endedDecember 31, 2009, reported revenues of $207,000, cost of sales of $165,000, other operating expenses, including income taxes of $50,000, and net financing income, after taxes, of $6,000. Compute the amount of net income or loss that Peoples Motors reported for 2009.a. net income of $0b. net income of $2,000c. net loss of $2,000d. net income of $8,000e. net loss of $8,000C ANS: CNet inocme=207,000-165,000-50,000+6,000=-2,0007. To carry out their plans, firms require financing, that is, funds from owners and creditors. Owners providefunds to a firm and in return receive ownership interests. For a corporation, the ownership interests are:a. Common Stock Sharesb. Corporate Bondsc. Notes Receivabled. Notes Payablee. Certificates of DepositA ANS: A8. To maintain the balance sheet equality, it is necessary to report every event and transaction in a dual manner.If a transaction results in an increase in the left hand side of the balance sheet equation, dual transactions recording requires that which of the following must occur, to maintain the balance sheet equation:a. decrease another assetb. increase a liabilityc. increase shareholders equityd. all of the above will maintain the balance sheet equatione. none of the aboveANS: D9. Temporary accounts are for recordinga. revenues and expensesb. assetsc. liabilitiesd. shareholders’ equitye. assets, liabilities, and shareholders’ equityA ANS: A10. Current assets are expected to be converted to cash withina. a weekb. a monthc. a quarterd. a yeare. two yearsD ANS: D11. The _____ are linked (that is, they articulate) through the shareholders’ equity account, Retained Earnings.a. balance sheet and the income statementb. balance sheet and the statement of cash flowsc. statement of cash flows and the income statementd. all of the abovee. none of the aboveA ANS: A12. Magestic Foods Group, a European food retailer that operates supermarkets in seven countries, engaged inthe following transaction during 2009: purchased and received inventory costing €500 million on account from various suppliers. Indicate the effects of the transaction on the balance sheet equation. Magestic Foods Group reports its results in millions of euros.a. Assets + €500 million; Liabilities + €500 millionb. Assets + €500 million; Shareholders’ Equity + €500 millionc. Liabilities + €500 million; Shareholders’ Equity + €500 milliond. Liabilities + €500 million; Shareholders’ Equity - €500 millione. Assets + €500 million; Shareholders’ Equity - €500 millionA ANS: A13. Benezra S.A., a large Brazilian petrochemical company, reported a balance of R$1,600 million in AccountsReceivable at the beginning of 2009 and R$1,500 million at the end of 2009. Its income statement reported total Sales Revenue of R$12,000 million for 2009. Assuming that Benezra makes all sales on account, compute the amount of cash collected from customers during 2009.a. 12,000b. 11,900c. 12,100d. 13,600e. 13,500ANS: CAR at beginning of year+sales-cash receipts=AR at end of year1,600+12,000-cash receipts=1,500, therefore cash receipt=12,10014. In 2008, Southwest Airlines had net working capital of $87 million and current assets of $2,893 million. Thefirm’s current liabilities are:a. $2,980 millionb. $2,806 millionc. $87 milliond. $2,893 millione. There is not enough information to calculate the amount.Answer: bNet working capital = current assets – current liabilities.Current liabilities = Current assets – Net working capital = $2,893 - $87 = $2,80615. The closing process involves:a. reducing to zero the balance in each income statement accountb. debiting the revenue accountsc. crediting the expense accountsd. transferring to Retained Earnings the differences between total revenues and total expensese. all of the aboveE ANS: E16. The criteria for asset recognition includea. The firm owns or controls the right to use the item.b. The right to use the item arises as a result of a past transaction or exchange.c. The future benefit can be quantified with a reasonable degree of precision.d. all of the abovee. none of the aboveD ANS: D17. During fiscal 2007, Kohl’s had sales of $16,473,734, Cost of merchandise sold of $10,459,549 and grossprofit of $6,014,185. What was net income for 2007? ($ in thousands)a. $6,014,185 thousandb. $7,682,249 thousandc. $13,696,434 thousandd. $22,487,919 thousande. There is not enough information to calculate the amount.Answer: eRationale: Sales – Total expenses = Net income. There is no information about total expenses, so we cannot compute Net income.18. During 2007, Skechers U.S.A., Inc. had Sales of $1,394.2 million, Gross profit of $600 million and Selling,general, and administrative expenses of $491.2 million. What was Skechers’ Cost of sales for 2007?a. $794.2 millionb. $303 millionc. $903 milliond. $411.8 millione. There is not enough information to calculate the amount.Answer: aRationale: Sales – Cost of sales = Gross profit$1,394.2 – Cost of sales = $600. Cost of sales = $794.219. In 2007, Nordstrom, Inc. reported the following (in millions):What amount did Nordstrom report as total assets?a. $2,239 millionb. $4,485 millionc. $3,365 milliond. $8,961 millione. None of the aboveAnswer: eRationale: Total assets = Total liabilities + EquityTotal assets = $1,635 + $2,850 + $1,115 = $5,600. This amount is not given in the problem.20. The _____ account accumulates the amounts of the undistributed earnings over time.a. Treasury Stockb. Cashc. Additional Paid-in-Capitald. Retained Earningse. Common StockD ANS: D21. During fiscal 2007, E. I. DuPont de Nemours and Company recorded cash of $28,893 million from customersfor accounts receivable collections. Which of the following financial statement effects template entries captures this transaction?Rev-enuesa. +28,893 -28,893(AR)=+28,893(Retainedearnings)+28,893 –= +28,893b. +28,893 -28,893(AR)= –=c. +28,893(AR)=+28,893(Retainedearnings)+28,893 –= +28,893d. -28,893 +28,893(AR)=Answer: bRationale: Collecting cash from customers increases cash and decreases accounts receivable. There is no income statement effect.22. During fiscal 2008, Black & Decker Corporation reported Net income of $293.6 million and paid dividends of$101.8 million. Which of the following describes how these transactions would affect Black and Decker’s equity accounts? (in millions)a. Increase contributed capital by $293.6 and decrease earned capital by $101.8b. Decrease contributed capital by $101.8 and increase earned capital by $293.6c. Increase contributed capital by $191.8d. Increase earned capital by $191.8e. None of the aboveAnswer: dRationale: Net income increases earned capital and dividends decrease earned capital. The net effect is an increase to earned capital.23. During its first three months of operations, Kay’s Bakery, Inc. purchased supplies such as plates, napkins,bags, and cutlery for $1,500 and recorded the entire $1,500 as an expense. Supplies on hand at the end of the first quarter, amount to $400. To prepare financial statement for the first quarter, the company must record which of the following accounting adjustments?a. Increase Supplies expense by $400 and decrease Supplies inventory by $400b. Increase Supplies expense by $1,100 and decrease Supplies inventory by $1,100c. Increase Supplies inventory by $400 and decrease Supplies expense by $400d. Increase Supplies inventory by $1,100 and decrease Supplies expense by $1,100e. None of the aboveAnswer: cRationale: Supplies on hand are $400, these must be recorded with an increase to supplies inventory of $400.24. Separately disclosing assets and income from operations that a firm has decided to discontinue (and disposeof or abandon) allows users to form better predictions ofa. past earnings.b. current earnings.c. future earnings.d. all of the abovee. none of the aboveC ANS: C25. Which of the following is/are false?a. Firms do not necessarily recognize revenues when they receive cashb. Firms do not necessarily recognize expenses when they disburse cash.c. Net income will not necessarily equal cash flow from operations each period.d. A profitable firm will likely borrow funds in order to remain in business.e. None of the above are falseE ANS: E26. As a general principle, under the accrual basis of accounting, the firm recognizes revenue when thetransaction meets which of the following conditions?a. completion of the earnings process, onlyb. receipt of assets from the customer, onlyc. completion of the earnings process and receipt of assets from the customerd. expiration of the warranty period, onlye. receipt of the final payment, onlyC ANS: C27. During the month of March 2010, Weaver World, a tax-preparation service, had the following transactions.Billed $74,000 in revenues on creditReceived $41,000 from customers’ accounts receivableIncurred expenses of $33,500 but only paid $19,425 cash for these expensesPrepaid $5,555 for computer services to be used next monthWhat was the company’s accrual basis net income for the month?a. $16,020b. $10,465c. $40,500d. none of the aboveAnswer: c.Rationale:Revenues (earned) $74,000Expenses (incurred) $33,500Net income $40,50028. Ames Corp. purchased new equipment during the year but neglected to record depreciation. What is theeffect of this omission on each of the named accounts?Accumulated Retained DepreciationDepreciation Earnings Expensea. Understated Overstated Understatedb. Understated No effect Overstatedc. Overstated Understated Understatedd. Overstated No effect Overstatede. Overstated Understated OverstatedA ANS: A29. Julia Corporation purchased an insurance policy for three years beginning January 1, Year 2, and recordedthe $6,000 premium in the Prepaid Insurance account. Assuming the company made the appropriate journal entries to record the payment of premium on January 1, Year 2, what adjusting entry is required to reflect the proper balances, in the insurance-related accounts at year-end, on December 31, Year 2?a. Insurance Expense 2,000Prepaid Insurance 2,000b. Prepaid Insurance 2,000Insurance Expense 2,000c. Insurance Expense 4,000Prepaid Insurance 4,000d. Insurance Expense 6,000Prepaid Insurance 6,000e. Prepaid Insurance 4,000Insurance Expense 4,000ANS: A30. When a firm’s average total assets equals average shareholders’ equity.a. ROA is greater than ROEb. ROA is less than ROEc. ROA equals ROEd. Cannot determineAnswer: c31. If Company A has a higher net operating profit margin (NOPM) than Company B, then Company A’sRNOA will definitely be higher. Please indicate if the above statement is true or false.a. Trueb. FalseAnswer: FalseRationale: RNOA depends on NOPM but also depends on operating asset productivity (NOAT). If Com-pany B had a much higher operating asset productivity, its RNOA could be higher despite the lower prof-itability.32. The 2008 financial statements of The Washington Post Company reveal average shareholders’ equity of$3,171,176 thousand, net operating profit after tax (NOPAT) of $79,895 thousand, net income of $65,722 thousand, and average net operating assets (NOA) of $ 3,279,742 thousand. The company’s r eturn on equity (ROE) for the year is:a. 2.00%b. 2.07%c. 2.44%d. 2.52%e. There is not enough information to calculate the ratio.Answer: bRationale: ROE = Net income/Average shareho lders’ equity = $65,722 / $3,171,176 ≈ 2.07%33.Based on the information provided in question #32, the return on net operating assets (RNOA) for TheWashington Post Company for 2008 is:b. 2.07%c. 2.44%d. 2.52%e. There is not enough information to calculate the ratio.Answer: cRationale: RNOA = net operating profit after tax/Average net operating assets = $79,895 /$3,279,742=2.44%34.Based on the information provided in question #32, the nonoperating return for The Washington PostCompany for 2008 is:a. -0.37%b. 0.37%c. 2.44%d. 2.52%e. There is not enough information to calculate the ratio.Answer: aRationale: nonoperating return = ROE-operating return = 2.07%-2.44%=-0.37%35. The 2008 balance sheet of Whole Foods Market reports operating assets of $3,380,736 thousand, operatingliabilities of $945,542 thousand, and nonoperating liabilities of $929,170 thousand. Whole Food’s average net operating assets for the year are:a. $2,451,566 thousandb. $2,435,194 thousandc. $2,443,380 thousandd. $3,380,736 thousande.There is not enough information to calculate the amount.Answer: eRationale: Average net operating assets requires two years of balance sheet data. The question only pro-vided one year’s data, thus, there is not enough information to calculate the amount.36. Net operating profit after tax (NOPAT) includes operating revenues less operating expenses such as:a. Cost of goods sold (COGS)b. Selling, general and administrative expenses (SG&A)c. After-tax earnings from investments and interest expensesd. all of the abovee. a and b onlyAnswer: eRationale: NOPAT is net operating profit after tax. After-tax earnings from investments and interest ex-penses are not included because they are nonoperating items.37. The fiscal 2008 financial statements of BJ Services shows net operating profit margin (NOPM) of 11.69%,net operating asset turnover (NOAT) of 1.46, return on equity of 19.37%, and adjusted return on assets of8.17%. What is the company’s nonoperating return?a. 2.30%b. 7.68%d. 27.54%e. There is not enough information to calculate the ratio.Answer: aRationale: Nonoperating return = ROE ─ operating return = 19.37% - (11.69% × 1.46) = 2.3026% = 2.30% 38. Sam’s Club (part of the WalMart consolidated operations) collects annual non-refundable membership feesfrom customers. When should Sam’s Club recognize revenue for these membership fees?a. immediately when cash is received because the fees are nonrefundableb. evenly over the membership yearc. evenly over the current fiscal yeard. at the end of the membership year when Sam’s has discharged its obligation to the customere. pro rata over the customer’s actual purchasing patt ernAnswer: bRationale: Sam’s should record membership fees evenly over the year even if the fee is nonrefundable b e-cause Sam’s has an obligation to stay open for business for a year to honor the customer’s membership. 39. Life Technologies Corporation and Affymetrix Inc. are competitors in the life sciences and clinicalhealthcare industry. Following is a table of Total revenue and R&D expenses for both companies.Life Technologies Corporation Affymetrix Inc2008 2007 2006 2008 2007 2006 Total revenue $1,620,323 $1,281,747 $1,151,175 $410,249 $371,320 $355,317R&D expenses $142,505 $115,833 $104,343 $84,482 $72,740 $86,296Which of the following is true?a. Life Technologies Corporation is the more R&D intensive company of the two.b. Life Technologies Corporation has become more R&D intensive over the three years.c. Affymetrix grew its R&D by more in 2008 as compared to Life Technologies.d. Affymetrix is less R&D intensive in 2008 than in 2006.e. None of the abovehint: R&D intensity is measured by R&D expense as a percentage of total revenue. Growth of R&D in 2008 is measured by (R&D in 2008)/ (R&D in 2007)-1Answer: dRationale: To make comparisons, we need to common size the R&D expenditures of both firms by scaling by total revenues and calculate growth rates.Life Technologies Corporation Affymetrix Inc2008 2007 2006 2008 2007 2006Commonsized R&D 8.8% 9.0% 9.1% 20.6% 19.6% 24.3%R&D growth 23.03% 11.01% 16.14% -15.71%Affymetrix spends proportionately more on R&D than Life Technologies, thus a is not true. Life Technol-ogies has spent less on R&D over the three year period, thus b is not true. Affymetrix grew R&D by 16% in 2008 compared to Life Technologies’ growth of 23%, thus c is not true. Af fymetrix decreased R&D from24.3% in 2006 to 20.6% in 2008, thus d is true.40. For fiscal year 2009, Ice Cream Inc. reports return on total assets (ROA) of 12%. The total average assets for2009 is $120,000 and average shareholders’ equity is $80,000. What is the company’s ROE for 2009?a. 8%b. 18%c. 12%d. There is not enough information to determine ROE.Answer: bRationale: ROE=ROA*(average assets/average equity)=0.12*(120,000/80,000)=0.1841. Compared to historical cost accounting, fair market value accounting is:a. less reliable but more relevant;b. less reliable and less relevant;c. more reliable and more relevant;d. more reliable and less relevant;Answer: aRationale: Fair market value is more subject to manipulation, although it is more relevant to investment decision.42. Boatman Company has account payable balance of $50,000 at the beginning of 2009 and $20,000 at end of2009. During 2009, the total purchase on credit made by the company is $85,000. Assuming all purchases from suppliers are made in credit, how much cash payment is made to the suppliers during 2009?a.$30,000b.$65,000c.$115,000d.Not enough information to determineAnswer: cRationale: cash payment = beginning A/P + purchase on credit – ending A/P =50,000+85,000-20,000=115,00043. Smart Planning Accounting and Tax Service has account receivable balance of $20,000 at the end of 2008.During 2008, the company made $17,000 sales on credit and collected $22,000 cash payments from cus-tomers. Assuming all cash collections from customers are applied toward account receivable, what is the beginning balance of account receivable for 2008?a.$39,000b.$25,000c.$37,000d.Not enough information to determineAnswer: bRationale: A/R beginning balance = ending A/R – sales on credit + cash collection =20,000-17,000+22,000=25,00044. On January 1, 2009, Bright and Shiny Cleaning Service received $3,000 from a customer for prepayment ofcleaning services to be performed evenly for the next three months. The accountant at Bright and Shinyrecords the transaction by debiting cash and crediting revenue for $3,000. What impact does this mistake have on assets, liabilities and equity?Assets Liabilities Equitya. Understated Overstated Understatedb. No effect Understated Overstatedc. Overstated Understated Overstatedd. Overstated No effect OverstatedAnswer: bRationale: The accountant should debt cash and credit unearned revenue for $3,000.Unearned revenue is a liability account. Therefore, the liability is understated and revenue,and thus, retained earnings is overstated by the same amount.45. During fiscal year 2008, Hanlon Company’s purchased merchandise inventory at a cost of $38,960. Thebeginning and ending balance of inventory account for 2008 is $7,065 and $8,906 respectively. What is the cost of goods sold during the year?a.$38,960b.$1,841c.$46,025d.$37,119e.Cannot determine using the information providedAnswer: dRationale: COGS=beginning inventory + purchase - ending inventory = 7,065+38,960 – 8,906 =37,119 46. Penno Corporation has net income of $50,000 during 2009. The following table summarizes the changes inaccount receivable, inventory and account payable during the year. Assume there is no depreciation expense.There is no other change in assets or liabilities. What is the cash flow from operating activities for 2009?a.$17,000b.$27,000c.$83,000d.$50,000Answer: cRationale: cash flows from operating activities = net income + depreciation expense + (-) any decrease (increase) in current assets + (-) any increase (decrease) in current liabilities = 50,000 – 15,000 + 20,000 + 28,000 = 83,00047. To convert net income to cash flows from operating activities, depreciation expensea. should be added back on net income to arrive at cash flows from operating activities;b. should be subtracted from net income to arrive at cash flows from operating activities;c. has no impact on the conversion from net income to cash flows from operating activities;Answer: a48. Liquidity refers toa. The life cycle of the companyb. The amount of receivables the company has in the balance sheetc. The amount of financial leveraged. None of the aboveAnswer: dRationale: Liquidity refers to cash, the amount on hand, the amount generated from operating activities, and the amount that can be raised on relatively short notice.49. The current ratio is a measure of:a. Solvencyb. Bankruptcy positionc. Short-term debt paying abilityd. LeverageAnswer: cRationale: The current ratio is a measure of short-term debt paying ability50. The fiscal 2008 balance sheet for Whole Foods Market reports the following data. What is the company’squick ratio?a. 0.05b. 0.22c. 0.71d. 0.93e. None of the aboveAnswer: bRationale: Quick ratio = (Cash + Accounts receivable) / Current liabilities = ($30,534 + $115,424)/ $666,177 =0.22。

会计的基本英语知识点汇总1. Introduction to Accounting会计简介Accounting is the systematic process of identifying, recording, measuring, classifying, summarizing, interpreting, and communicating financial information. It plays a crucial role in the management and decision-making processes of businesses and organizations.会计是一种系统性的流程,用于识别、记录、度量、分类、总结、解释和传达财务信息。

它在企业和组织的管理和决策过程中发挥着至关重要的作用。

2. Basic Accounting Principles基本会计原则There are several fundamental principles that underpin the field of accounting:有几个基本原则支撑着会计领域:a) Accrual Principle: This principle states that financial transactions should be recorded when they occur and not when the cash is received or paid out.应计原则:该原则规定财务交易应在其发生时记录,而不是在现金收到或支付时记录。

b) Matching Principle: This principle states that expenses should be recognized in the same accounting period as the revenues they help generate.配比原则:该原则规定支出应在与其相关的收入产生的同一会计期间内确认。

大学各专业名称英文翻译——文科方面ARTS澳门历史研究Study of the History of Macao办公管理Office Management办公设备运用Using Desktop Publishing in Business比较管理学Comparative Management比较诗学Comparative Poetics比较文化学Comparative Cult urology比较文学研究Study of Comparative Literature必修课4-10学分Restricted (4-10 Credits needed)病理生理学Pathological Physiology财务报告介绍An Introduction to Financial Accounting Statements 财务报告运用Using Financial Accounting Statements财务管理学Financial Management财务会计学Financial Accounting财务理论与方法Finance Theory & Methods财政与金融Finance财政与金融学研究Study of Finance财政预算Preparing Financial Forecasts产业经济学Industrial Economics传统文化与现代化Tradition Culture and Modernization当代国际关系研究Contemporary International Relations Studies当代世界发展研究Contemporary World Development Studies当代中国外交与侨务专题研究Monographic Studies of Diplomacy and Overseas C hinese Affairs of Contemporary China德语(第二外语) German (2nd foreign language)第一外语(英语) English (1st foreign language)电力系统Power Electronic Systems电子数据Digital Electronics电子通信Electronic Communications电子原理Electrical Principles断代文化史研究Study of Dynastic History of Culture多媒体:多媒体应用开发Multimedia: Developing Multimedia Application多用户操作系统Multi-User Operating Systems耳鼻喉科学Otolaryngology发展经济学Economics of Development放射生态学Radioecology分布式应用程序的设计与开发:概况Distributed application Design and Developme nt: An Introduction分子细胞与组织生物学Molecular, Cellular and Tissue Biology分子遗传学Molecular Genetics妇产科学Gynecology & Obstetrics高级生物化学Advanced Biochemistry高级水生生物学Advanced Hydrobiology工程实践与应用沟通(提升行业沟通技能)Communication (Developing a Communication Strategy for Vocational Purposes)沟通:实用技能Communication: Practical Skills管理经济学Management Economics管理决策Management Decision-Making管理理论研究|| Management Theory Studies管理理论与实践|| Management Theory & Practice管理学研究|| Management Research光化学|| Photochemistry国际关系案例分析|| Case Studies of International Affairs国际关系学导论|| Introduction of International Relations国际金融市场研究|| International Financial Market Study国际金融研究|| Study of International Finance国际经济关系研究|| International Economic Relations国际经济环境|| The International Economic Environment国际经济政治制度比较研究|| Comparative Researches on International Economic & Political Structure国际音标的应用|| Application of International Phonetic Alphabet国际战略与大国关系|| International Strategy国际政治经济学|| International Political Economy国际组织与国际制度|| International organization and International System海外汉学|| Sinology Abroad海外华侨华人概论|| Researches on Overseas Chinese海外华人文学研究|| Study of Overseas Chinese Literature汉语词汇学|| Chinese Lexicology汉语方言调查|| Survey of Chinese Dialects汉语方言概要|| Outline of Chinese Dialects汉语方言学专书选读|| Selected Reading of Chinese Dialectology汉语方言研究|| Studies of Chinese Dialects汉语史名著选读|| Selected Reading of Chinese History汉语音韵学|| Chinese Phonology汉语语法史|| History of Chinese Grammar汉语语法学名著选读|| Selected Reading of Chinese Grammar宏观经济环境|| The Macro Economic Environment宏观经济学|| Macro-economics互联网:WEB服务器的管理|| Internet: Web Server Management互联网:电子商务入门|| Internet : Introducing E Commerce互联网:网络客户服务|| Internet : Internet Client Service互联网:网络配制与管理|| Internet: Configuration and Administration of Internet Services华侨华人史|| History of Overseas Chinese华侨华人与国际关系|| Ethnic Chinese and International Relations环境生物学|| Environmental Biology回族史|| History of Chinese Muslims会计基本理论与方法|| Basic Theories & Approaches of计算数学1 || Mathematics of Computing 1计算数学2 || Mathematics of Computing 2解剖生理学|| Anatomical Physiology金融工程学|| Financial Engineering金融机构风险管理|| Risk Management by Financial Institution金融热点及前沿问题专题研究|| Research on Financial l Central & Up-to-date Issues经济数量分析方法|| Methods of Economic & Mathematic Analysis经济数量分析方法|| Methods of Economic Quantitative Analysis跨文化管理学|| Cross-Cultural Management临床血液病学|| Clinical Hematology马克思主义与当代科技革命|| Marxism & Contemporary Science & Technology R evolution马克思主义与当代社会思潮|| Marxism & Contemporary Social Trends o f Thoug ht美术理论|| Theory of Fine Art美术史|| History of Fine Art蒙古史|| History of the Mongols免疫生物学|| Immunobiology免疫学|| Immunology免疫学|| Immunology民族政策与民族理论研究|| Study of Policies and Theories on Nation laities明清档案|| Archives in Ming and Qing Dynasties模拟电路|| Analogue Electronics南海诸岛史研究|| Study of the History of Islands in the South Chi na Sea企业财务与资本营运|| Company Finance & Capital Operation企业管理理论与实务|| Theory & Practice of Business Management企业应用软件的开发:概况|| Enterprise Application Development: An Introduction 全球化研究|| Globalization Studies人工器官|| Artificial organs人力资源管理研究方法|| Study Methods of Human Resource Management人体解剖学|| Human Anatomy人文地理文化学|| Cult urology of Humane Geography日常交流(法语/德语/意大利语/西班牙语1、2、3级)|| Basic communication in Fr ench/German/Italian/Spanish(Levels 1,2&3)日语(第二外语) || Japanese (2nd foreign language)软件开发:抽象数据结构|| Software Development: Abstract Data Structure软件开发:第四代开发环境|| Software Development: Fourth Generation Environm ent软件开发:高级编程|| Software Development: Advanced Programming软件开发:过程式程序设计|| Software Development: Procedural Programming软件开发:汇编语言和编程|| Software Development: Assembly Language and Int erface Programming软件开发:结构设计方法|| Software Development: Structure Design Methods软件开发:开发计划|| Software Development: Program Planning软件开发:快速应用开发和原型技术|| Software Development: Rapid Applications Development and Prototyping软件开发:面向对象编程|| Software Development: Object oriented Programming 软件开发:面象对象设计|| Software Development: Object oriented Design软件开发:事件驱动程序设计|| Software Development:: Event Driven Programmin g 软件开发:网站开发|| Software Development: Developing the WWW软件开发:应用软件开发|| Software商业法规|| Law for Business商业模式|| Structure of Business商业情报管理|| Business Information Management商业统计1 || Business Statistics 1商业统计2 || Business Statistics 2商业信息技术运用(电子数据表和Word处理应用软件)|| Using Information Technol ogy in Business(Spreadsheets &Word Processing Applications)商业信息技术运用(数据库和Word处理应用软件)|| Using Information Technology in Business (Database & Word Processing Applications)社会语言学|| Sociolinguistics审计学|| Auditing生物材料|| Biomaterials生物材料测试技术|| Modern Testing Methods of Biomaterials生物分子的探测和操纵|| Signals Bimolecular Detection and Manipulation生物力学|| Biomechanics生物流变学|| Biorheology生物信息学|| Bioinformatics物医学工程前沿|| Advances in Biomedical Engineering生物医学信号处理与建模|| Biomedical Signal Processing and Modeling生物制片及电镜技术|| Biological Section and Electronic Microscope Technique 生物制片及电镜技术|| Biological Section and Electronic Microscope Technique生殖工程|| Reproductive Engineering世界经济与政治研究|| World Economy & Politics Studies水生动物生理生态学|| Physiological Ecology of Aquatic Animal水生生物学研究进展|| Study Progress on Aquatic Biology水域生态学|| Aquatic Ecology思想道德修养|| Understand of Ideology and Morality宋代政治制度研究|| Study of the Political System of Song Dynasty宋明理学史研究|| Study of the History of Neo-Confucianism in Son g and Ming Dynasties提高个人成效|| Developing Personal Effectiveness通信工程|| Communication and Industry网络会计研究|| Network Accounting Studies微观经济环境|| The Micro Economic Environment微观经济学与宏观经济学|| Micro-economics & Macro-economics微型计算机系统|| Microcomputer Systems文化语言学|| Cultural Linguistics文献学|| Bibliography文学与文化|| Literature and Culture文艺美学|| Aesthetics of Literature and Art文艺学专题研究|| Special Study of Literature Theory西方史学理论|| Historical Theories in the West西方文论|| Western Literary Theories系统开发:关系数据库|| Systems Development: Rational Database Systems系统开发概论|| Systems Development Introduction系统生态学|| System Ecology细胞超微结构|| Cell Ultra structure细胞超微生物学|| Cell Ultra microbiology细胞生长因子|| Cell Growth Factor现代公司会计研究|| Study of Modern Company Accounting现代汉语诗学|| Modern Chinese Poetics现代汉语语法研究|| Studies of Modern Chinese Grammar现代经济与金融理论研究|| Study of Modern Economy & Finance Theory现代商业复合信息|| Presenting complex Business Information现代商业信息|| Presenting Business Information现代审计理论与方法研究|| Study of Modern Audit Theories & Approaches香港历史研究|| Study of the History of Hong Kong项目管理|| Project Management项目设计|| Project Studies新制度经济学|| New Institutional Economics新制度经济学|| New Institutional Economics信息工程:应用软件|| Information Technology: Applications Software 1信息技术和信息系统|| Information Technology Information Systems and Service s信息技术应用软件|| Information Technology Applications Software选修课总学分|| Total optional credits required血液分子细胞生物学|| Hematological Cell and Molecular Biology训诂学史|| History of Chinese Traditional Semantics亚太经济政治与国际关系|| Economy, Politics and International Relations in Asia n-Pacific Region眼科学|| Ophthalmology医学分子生物学|| Medical Molecular Biology医学基因工程|| Gene Engineering in Medicine医学统计学|| Medical Statistics医学图像处理|| Image Processing医学物理学|| Medical Physics医学信息学|| Medi-formatics医学遗传学|| Medical Genetics医学影像技术|| Medical Imaging Technique医学影像诊疗与介入放射学|| Medical Imaging Diagnosis & Treatment and Interve ning Radiology译介学|| Medio-Translatology音韵学史|| History of Chinese Phonology应用统计|| Applied Statistics应用统计|| Applied Statistics用户支持|| Providing Support to Users语义学|| Semantics藻类生理生态学|| Ecological Physiology in Algae增强团队合作意识|| Developing the Individual Within a Team政治学研究|| Politics Studies中国古代历史文献的考释与利用之一:宋史史料学之二:元史史料学之三:港澳史料学之四:边疆民族史料学|| Utilization and Interpretation of Ancient Chinese Hist orical Literature 中国古代史的断代研究之一:宋史研究之二:元史研究之三:明清史研究|| Dynastic History of China中国古代史的专题研究之一:宋元明清经济史之二:二十世纪宋史研究评价之三:中国文化史之四:中西文化交流史之五:港澳史研究之六:中国边疆民族史之七:西域史研究|| Studies of History of China中国古代文化史|| History of Chinese Ancient Culture中国古代文论|| Ancient Chinese Literary Theories中国古典美学研究|| Study of Chinese Classical Aesthetics中国教育史|| History of Education in China中国经济问题研究|| Economic Problems Research in China中国区域文化研究之一:岭南文化史之二:潮汕文化史|| Re search on Chinese Re gional Culture中国少数民族文化专题研究|| Study of Special Subjects on Cultures of Chinese Minority Nationality中国思想史|| History of Chinese Ideologies中国与大国关系史之一:中美关系史之二:中俄关系史之三:中英关系史之四:中日关系史|| History of Relations Between China and Major Powers中国与世界地区关系史之一:与中亚地区关系史之二:与东南亚地区关系史之三:与东北亚地区关系史之四:与南亚地区关系史|| History of Relations Between China an d Other Regions o f the World中国语言文学与文化|| Chinese Languages, Literatures and Cultures中外关系史名著导读|| Reading Guide of Famous Works on the History of Sino-Foreign Relations中外关系史史料学|| Science of Historical Data on the History of S info-Foreign Relations中外关系史研究|| Researches on the History of Sino-Foreign Relations中外史学理论与方法研究|| Researches on Theory and Method About Si no-Forei gn History Science中外文化交流史|| History of Sino-Foreign Cultural Exchanges中外文论|| Chinese and Western Literature Theories中西交通史|| History of Communication Between China and the West资本市场研究|| Study of Capital Market资本营运、财务与管理会计理论和方法研究|| Study of Theories & Appr oaches of Capital Operation, Financial Management Accounting资本运营与财务管理研究|| Capital Operation and Financial Management Researc h组织工程进展|| Advances in Tissue Engineering组织行为理论|| organizational Behavior Theory《中华人民共和国学位条例》“Regulations Concerning Academic Degrees in the People's Republic of Chin a”结业证书Certificate of Completion毕业证书Certificate of Graduation肄业证书Certificate of Completion/Incompletion/Attendance/Study教育学院College/Institute of Education中学Middle[Secondary] School师范学校Normal School[upper secondary level]师范专科学校Normal Specialized Postsecondary College师范大学Normal[Teachers] University公正书Notaries Certificate专科学校Postsecondary Specialized College广播电视大学Radio and Television University中等专科学校Secondary Specialized School自学考试Self-Study Examination技工学校Skilled Workers[Training] School 业余大学Spare-Time University职工大学Staff and Workers University大学University(regular, degree-granting) 职业大学Vocational University。

INT0006: INTRODUCTION TO ACCOUNTING & FINANCERevision1: ROLE OF ACCOUNTING IN BUSINESSUSERS OF ACCOUNTING INFORMATION (STAKEHOLDERS)MANAGERSAs those responsible for planning the activities of thebusiness, managers are major users of accounting information.Types of management decisions requiring accountinginformation include: ∙ the pricing of goods [& services] ∙ the quantity of goods to produce∙ investment in new equipment ∙ raising of finance to maintain/expand the business∙ production capacity ∙ purchase of stock These are many of the stakeholders in any business, butthere will be others. Many of these groups are external to the business itself; however they have an interest in the success or failure of the business.Business organisationnCompetitors Lenders Managers OwnersCustomers Suppliers Investment analystsCommunity representative s Government Employees and theirrepresentativesRULES, REGULATIONS AND STANDARDSETHICAL RULESThere are four main ethical rules which accountants should follow. These are NOT legal requirements, but principles of good practice.Prudence –when estimates of the future need to be made –for example over the creditworthiness of a debtor, managers are likely to be optimistic, it is the responsibility of theConsistency –in a company’s accounts. Accountants must keep to the same methods in subsequent accounting periods, to ensure that one year’s figures can be compared to previous periods.Objectivity– Accounts should be prepared with the minimum of bias. This is often not easy, as owners may want to adopt policies which would result in higher profit figures, or in disguising poor results. Often it is wise to resort to the prudence rule, but each case must be considered individually.Relevance– The amount of information which could be disclosed to any stakeholder is virtually limitless. It is important to limit what is provided to that which is relevant to the user’s needs. MEASUREMENT RULESThere are six main measurement rules which govern how data is recorded in accounting in an accounting system.Money measurement– All information should be presented in monetary terms. For example in the accounting records for a farm, we would not wish to know how many cattle the farm had bought and sold, it would be more useful to know the monetary value of the stock transactions.Historic cost–Transactions should be recorded at their original cost. Changes in value are ignored until an asset is disposed of.Realisation– Transactions should be accounted for in the accounting period in which legal title for them has been transferred fro the seller to the buyer.Matching– Can be referred to as the accruals convention. Expenses should be matched to the revenue that they helped generate. Difficulties occur when a business pays in advance or in arrears for an expense. A business will usually be required to pay rent in advance. An adjustment is made to the amount actually paid, so that in the final accounts the figure shown for rent is only that portion of what has been paid which actually relates to the accounting period being reported.Dual Aspect– Every time a transaction takes place there is a twofold effect. For example if a business receives money from a debtor, the amount of cash in the bank will go up and the amount of debtors will go down. This is the basis of double-entry bookkeeping.Materiality – This rule allows us to apply common sense to what is reported in accounts. If an item is insignificant then it can be ignored. It should be remembered that what may be an insignificant amount for a large business, may well be significant to a small business. Large companies usually report figures in £000, whereas a small business will report in whole pounds.Inventories(stock)BOUNDARY RULESBusiness Entity – For accounting purposes a business and its owner(s) are treated as being quite separate and distinct. This means that the owner cannot charge personal expenditure to the business, and any money invested in the business by the owner(s)is treated as a claim against the business.Going concern – financial statements should be produced on the assumption that the business will continue into the foreseeable future. If the accountant thinks that the business is not a going concern then the accounts would be prepared as if the business were to be closed.2: Statement of Financial Position (The Balance Sheet)THE MAJOR FINANCIAL STATEMENTSThe three main financial statements produced by a business are:The Cash Flow statement – showing cash movements over the accounting periodThe Income Statement (also known as the profit and loss account) which shows how much wealth was generated over the accounting period The Balance Sheet – showing the accumulated wealth at the end of the accounting periodTHE BALANCE SHEETThe balance sheet shows the financial position of a business at a particular moment of time. It shows the assets of a business and the claims against the business (liabilities and owners capital ).Assets – An asset must arise from a past transaction or event, they must be capable of measurement in monetary terms, they must be under the exclusive control of the business and be held for a probable future benefit.Claims – A claim must arise from a past transaction or event, it must be capable of measurement in monetary terms and will result in an obligation to the business to provide cash or benefit at a future time. Capital – this is the claim that the owners have against the business. Liabilities – The claims of all other parties against the businessTYPES OF ASSETAssets are listed on a balance sheet in a logical order depending on what type of asset they are.Non-current assets are held for the long term benefit of the business. They are the tools of the business.Current assets are held for the short term. The most common current assets are: Inventories (stock), trade receivables (debtors) and cash . They are listed in order of liquidity , with the least liquid being shown first. Most sales are made on credit so current assets can be shown as acycle.TYPES OF CLAIMClaims are normally classified into capital (owner’s claim) and liabilities.Liabilities can be further divided into:Current liabilities – amounts due for settlement in the short term – usually within 12 monthsNon-current liabilities – amounts due to outside parties which are not current liabilities. VALUATION OF ASSETSTangible non-current assets – Normally valued at historic cost – less depreciation. It is possible to decide to re-value these assets to a current fair value or market value. The main consequence of this is that the business must revalue all similar assets at the same time, and then regularly throughout the lives of the assets.Impairment of non-current assets – if an asset is impaired it is worth less than the balance sheet value. This could be caused by changes in market values, obsolescence or factors such as fire.The business must show the impaired value on the balance sheet.Inventories – stock must be valued at the lower of cost and net realisable value. DEPRECIATION AND VALUE OF ASSETS.VALUATION OF ASSETS ON THE BALANCE SHEETNon-current assetsThe historic cost convention means that assets are normally valued at the price paid for them. Most assets lose value over their lifetime. In accountancy this reduction in value is referred to as depreciation. The total depreciation to date of an asset is recorded on the balance sheet. The accumulated depreciation is deducted from the historic cost (or fair value) to show the written down value.To calculate depreciation four factors need to be considered:∙the cost (or fair value) of the asset;∙the useful life of the asset;∙the residual value of the asset (what it will be worth when the business has finished with it);∙the depreciation methodThe cost (fair value) of the assetThe cost figure will include al of the expenses necessary to bring the asset to the business and make it ready for use. This will include delivery costs, legal costs, installation costs and the cost of improvements or alterations.The useful life of the assetA business should estimate the useful life of each asset this will probably be shorter tan the assets actual life. Advances in technology will make computer equipment obsolete long before the equipmentactually stops working.The residual value of the asset Example 3.7Cost of machine £40,000 Estimated residual value at the end of its useful lifeWhen a business disposes of an asset, at the end of its useful life, it may be that the asset will still be of use to someone else and can be sold.Depreciation methodThere are two main methods of depreciation:∙straight line method∙reducing balance methodStraight line methodThis is the most straightforward method.Deduct residual value from the cost of the asset anddivide by the useful life of the assetCost £40,000Residual value £ 1,024£38,97638,976 / 4 = £9,744Depreciation would be charged at £9,744 each yearfor four yearsReducing balance methodThis method is more complicated to calculate,but results in a more accurate depreciationfigure each year. Assets use most of their valuein the early years of their useful life. Thereducing balance method takes account of this.It applies a fixed percentage to the writtendown value of the asset each year to calculateannual depreciation.Current assetsInventories (stock)Changing prices of stock make it more difficult to decide what the value of a business’s inventories should be reported as. Both accounting standards and the prudence convention tell us to value inventory at the lower of cost and net realisable value. However, if the business buys stock regularly throughout the year then the cost will be different for each batch purchased.There are three common methods used to value inventories, all of which make an assumption about the order in which inventories are used:∙FIFO (First in first out) – assumes that the business uses the oldest stock first∙LIFO (Last in first out) – assumes that the business uses the newest stock first∙AVCO (weighted average cost) – assumes that all stock is treated as equal, and recalculates cost based on the quantity purchased at each price.LIFO method is NOT acceptable to use in final accounts.Normally net realisable value will be higher than cost. If for any reason the realisable value is lower than cost, for example inventories have suffered damage, then the balance sheet valuation should be the net realisable value.Trade receivables (debtors)When a business sells goods or services on credit, the amounts owed to the business are shown on the balance sheet as trade receivables or debtors.There is always the risk that some of these debtors may not pay. When it becomes certain that a debt is not going to be paid, the business must reduce the debtors and write off the bad debt as an expense in the financial period.Some businesses assume that a percentage of their debtors will not pay each year, and make a provision for bad debts every year.3: INCOME STATEMENTSTHE INCOME STATEMENT (PROFIT AND LOSS ACCOUNT)The income statement measures how much wealth has been generated by a business over a specified period.It deducts expenses from revenues to arrive at a profit figure.RECOGNITION OF REVENUERevenue should only be recognised when it has been realised. In practice this means that the business should only show revenue:–When it can be measured;–When it is probable that it will be received; and–The associated costs can be measured.ACCRUALS AND PREPAYMENTSThe expenses shown on the income statement are those incurred in the accounting period. In the normal course of business some expenses are paid in advance and some are paid in arrears.EXPENSES PAID IN ADVANCEWhen a business pays in advance, it will usually have paid for some of next years expenses. For example, rent is often paid in advance. The amount paid which relates to next year’s rent is NOT shown as an expense this year. Instead it appears on the balance sheet as a prepayment.EXPENSES PAID IN ARREARSIf an expense has not yet been paid for, the total amount incurred in the accounting period is shown as an expense on the income statement, with the amount not yet paid appearing on the balance sheet as an accrual4: SHARE CAPITALSHARE CAPITALAll Companies issue ordinary shares. The people who hold these shares own the business, they are known as shareholders or members. Ordinary shares are also known as equities.A company is formed by at least one person –the subscriber– that person agrees to buy a number of shares in the company. The money paid for those shares is the company’s share capital. The share capital will be made up of a number of shares of a certain denomination, such as 10p, 50p and £1 this is known as the nominal value.Limited Liability CompaniesA limited liability company is an artificial person in law. It has many of the same rights and responsibilities as a real person. A limited company is incorporated.It is a straightforward task to create a company. The subscriber, or promoter, fills in some simple forms and pays a small fee to the Registrar of Companies, who then issues a Certificate of Incorporation which evidences that the company exists.The company is quite separate from its owners. If the company is sued, the most that any owner (shareholder) can lose is limited to the amount they have paid, or agreed to pay, for their shareholding. In order to show stakeholders that a company has the right to limited liability the company must include in its name the word limited if it is a private limited company or plc if it is a public limited company.The main difference between private andpublic limited companies is that publiccompanies can offer their shares for saleto the general public.Types of sharesWhen a company is formed theincorporation documents state themaximum value of shares which thecompany will issue. This is called theauthorised share capital. Normally thecompany will not issue all of its authorisedshare capital at incorporation, it will onlyissue as much as it needs for immediate requirements. The amount of shares actually issued to shareholders is called the issued share capital. This allows the company to raise more capital in the future by issuing more shares.Sometimes shareholders have the right to pay for their shares by instalments. Until the whole amount has been paid, these shares will be known as partly paid. When the final instalment has been paid, the shares are known as fully paid.There are two main types of shares: ordinary shares and preference shares. Ordinary shareholders are not entitled to any dividend. The board of directors will decide each year if a dividend is to be paid, and how much that dividend will be. Preference shareholders are normally entitled to a specified amount of dividend. The preference shareholders dividend is paid before any ordinary shareholders dividend. Sometimes preference shares are cumulative, meaning that if a company cannot pay a dividend one year, the dividend unpaid will be added to the following year’s divid end.Raising capitalAs a company grows it may wish to raise more capital. It can then issue some more of its authorised share capital to new or existing shareholders.A private company can only issue shares to people it knows. Public companies can advertise a share issue, and often will take out a large advert in the main newspapers.Issues of new shares will normally be at a price higher than the nominal value of the shares. This is because its existing shares will be valued at a higher price. The extra that is paid for these new shares is called share premium.Methods of issuing new shares:∙Rights issues, made to existing shareholders, in proportion to their existing shareholdings∙Public issues, made to the general public∙Private placings, made to selected individuals, who are approached and asked if they would be interested in investing.A company may, under specific circumstances, buy back its own shares. This is rare, and the procedure laid out in the Companies Acts must be followed.Bonus issuesA company may issue shares to its existing shareholders, without raising capital. Companies frequently issue bonus shares as a method of reorganising its capital. The shareholders will each gain extra shares, but their ownership of the business will remain unchanged. Since there are more shares in issue, the value of each individual share will go down, making the shares more attractive to potential new investors.SOURCES OF FINANCEINTERNAL SOURCES OF FINANCEThese are sources which do not require the agreement of anyone outside the business. They are quick and easy to access, cheaper than external sources and flexible.Short term finance can be obtained by:∙ Reducing the levels of stock.∙ Arranging longer credit periods with suppliers ∙ Ensuring debtors pay more quickly Long term finance can be provided by retained profits. All of the profits of the business which have not been distributed to shareholders by dividend can be made available to invest in the business. It would also be possible to raise funds internally by selling un-used assets.EXTERNAL SOURCES OF FINANCEExternal sources of finance are more expensive to raise, and more time consuming. In the short term the most common form of externalfinance in the bank overdraft . Most businesses will have an overdraft agreement in place with their bankers.Debt factoring – a factoring company will take over the debts of a business, for a cash advance, usually less than 80% of the total debts. The factor will then collect the debts of the business, and repay the remaining 20% (less charges and interest) to the business.Invoice discounting is where a financial institution loans a percentage of the total debtors of a business, but without agreeing to collect the debts for thebusiness. In the longer term a business may raise finance byissuing new shares, either ordinary shares orpreference shares.Most businesses will also rely on long term loans .The details of the loan will be set out at the beginning, whether the loan is from a bank obtained through the issue of loan stock.Long term bank loans will normally be secured against the property of the business. If the business fails to repay the loan, the bank has the right to take the property of the business and sell it to repay the loan.5: WORKING CAPITAL CONTROLDEFINITIONTotal internal financeTighter credit controlDelayed payment to trade payablesReduced inventories levels Long-termShort-term Retained profitsOrdinary sharesBankoverdraft Debt factoringPreference shares Loans Total finance Long- term Short-termLeases Hire purchase agreementsInvoice discountingWorking capital is defined as current assets less current liabilities.The cash cycle shows the circulation of working capital in a business. This show how creditors (suppliers) provide stock, which is sold to debtors, who will eventually pay cash and so on.MANAGING WORKING CAPITALA business’s financial health depends on effective management of working capital.Managing inventories (stock) ∙ know stock levels, and perform physical checks (stocktakes) to make sure the information is correct.∙ re-order stock at appropriate times to make sure that the business does not run out, or hold too much. If prices are expected to rise then it may be wise to stockpile to save money in the future ∙ Monitor actual stock against budgeted stock as part of the budgetary control systemJust in time inventories managementJust in time (JIT) inventories management can help avoid the need to hold stock. Businesses must develop excellent relationships with their suppliers and their customers, so that customers give them notice of when they intend to order goods, and suppliers guarantee to fulfil orders in the minimum possible time.Managing receivables (debtors)Selling goods on credit will result in costs for a business. These include the administrative costs, bad debts and opportunity costs . However selling on credit is widespread, and so most businesses will offer credit terms to some of their customers.A business must have clear policies about who to give credit to, the amount and term of credit it will offer, how it will collect debts and how to reduce the risk of non-payment. Managing CashA cash flow forecast allows managers to monitor cash balances, so that surplus funds can be invested and borrowing facilities can be arranged if necessary.Managing payables (creditors)A business should negotiate suitable credit terms with its suppliers, and make prompt payment according to those terms. Businesses which obtain a reputation for slow payment will often impair their credit rating, and find further credit difficult to obtain.6: RATIO ANALYSISFINANCIAL RATIOSFinancial ratios are a quick and simple way of assessing the financial health of a business.STOCKCASHTYPES OF FINANCIAL RATIOSProfitabilityProfitability ratios relate profit to other key figures in the financial statements. Profit measures are the central measures of operating achievement.Activity (Efficiency)Activity ratios measure the efficiency with which the business utilises its assets, providing insights into management policy and operational efficiency.LiquidityLiquidity ratios examine the ability of the business to meet its short-term commitments. It is vital that a firm has the capacity to pay debts when they fall due. Poor liquidity can undermine the confidence of creditors/lendersGearing (Leverage)Gearing is important in the assessment of financial risk. Gearing ratios examine the relative contributions of investors and lenders, and the capacity of the business to service and repay loans.InvestmentSome ratios are calculated for the benefit of investors. They measure the performance of the business as it applies to the owners of the business. These investor ratios are often quoted in the financial press. Profitability ratiosActivity/Efficiency ratiosLiquidity ratiosGearing ratiosInvestor ratiosOverheads budgetTrade receivablesbudgetTrade payablesbudgetCapital expenditure budget Raw materials purchases budgetSales budget Direct labour budgetCash budgetLIMITATIONS OF FINANCIAL RATIOSAlthough ratios are a quick and easy to understand method of analysing the financial state of abusiness, there are some important limitations.∙ Quality of financial statements – if the prudence concept has been applied to reduce the stated value of an asset, then the ratios using that value will be lower. If the financial statements have been produced with the intention to mislead, then the ratios will be incorrect. ∙ Limited focus – it is important not to rely only on ratio analysis. Looking at the actual data can help to show a better picture of the business ∙ Comparison – ratios mean nothing on their own. They must be compared with something. It is important to compare ‘like with like’. Ideally we can compare across several years in the same business. Alternatively comparisons can be made with ‘industry standard’ figures. ∙ Balance sheet ratios – remember that the balance sheet represents one moment in the life of the business. The figures on the balance sheet may not reflect the true financial position of the business. ∙ Qualitative information – there is a lot that can be found out about a business by examining information which is NOT involved with numbers. How happy are the staff? Can the directors be trusted?7: BUDGETING AND BUDGETARY CONTROL AND PREPARATIONBUDGETINGEvery successful business plans for the future. Typically a business will produce a long-term plan aimed at achieving its business objectives. In order to achieve this plan, shorter term plans, for 12 months at a time will be produced. An important part of the short term plan will be a financial budget.TYPES OF BUDGETThere are many parts to a budget, all of which involve predicting future business conditions.Normally the process will begin with the sales budget . The business will forecast how many sales it will make, and at what selling price.Having decided on the level of sales, a production budget can be prepared, which will take into account the opening and closing inventories which the business wishes to maintain. The production budget then leads to materials purchases budget , direct labour budget and overheads budget.During this process the business can calculate the expected costs of all items in the budgets, and decide whether there is a need to purchase non-current assets.All of the information in these individual budgets will be put together into a budgeted income statement, balance sheet and cash flow statement.Limiting factors.It is possible that some of the items necessary to achieve budget are not available in the required quantities. Often a supplier of raw materials will be unable to meet increased orders, or there will be insufficient skilled labour available. These limiting factors may mean that the budget must be amended.BUDGETARY CONTROLBudgets allow managers to control the business. It allows them to check, on a regular basis, that the business is performing according to the budget. If things are not going according to plan, something can be done to put things right.Often managers will only receive information about items which are not going according to budget This is a form of exception reporting.When actual figures do not equal budgeted figures the difference is known as a variance. Variances can be favourable or adverse. Both adverse and favourable variance must be investigated so that they can be explained.FLEXING THE BUDGETThe budgets discussed so far have been fixed budget. They are based on a best estimate of the future. Usually as the business carries on, things will change. If, for example, production was budgeted at 10,000 units, but an unexpected order arrived which meant that production increased to 12,000 units, it would be necessary to change the budget figures to show this increased activity. This process is known as flexing the budget.QUALITY OF BUDGETSIn order to make sure that the budget is a useful tool it should be prepared carefully. The figures used to estimate costs should be achievable. Some businesses use an ideal budget which in practice is not achievable. If a business is trying to work with a budget which is not achievable staff will be demotivated.Budget holders should be involved in the production of the budget, as they will be able to estimate figures for their particular areas of the business.8: BREAKEVEN ANALYSISTHE BEHAVIOUR OF COSTSCosts in a business behave in different ways as the volume of activity changes. There are three ways that the costs could behave within a range of activity levels:Variable costs – These are costs where the cost varies in proportion to the activity level. For example if a carpentry workshop makes two tables, it will use twice as much wood.Fixed costs – These are costs which do not normally change when levels of activity change. The cost of rental for the carpentry workshop will normally remain the same whether they produce 1 or 100tables.Eventually, if business expanded a lot, the carpentry business may need to expand its operation, and rent another workshop. In this event this fixed cost would become a stepped cost.Semi variable costs – Some costs are a mixture of the two, they have a part of the cost which is fixed and the remainder which is variable. Some mobile phone bills will charge a set amount per month, but will charge more depending on how many calls are made.MARGINAL COSTINGMarginal costing requires us to classify all costs as variable, fixed or semi-variable. As we have seen all businesses must meet their fixed costs, whether or not they produce and sell goods. The selling price of a unit, less its variable costs will contribute towards the fixed costs. His gives us the marginal costing equation:contribution = selling price per unit BREAK-EVEN ANALYSISThe break-even point of a business is when it makes neither a profit nor a loss . This can be calculated by dividing the total fixedcosts of the business, by the contribution per unit, giving the number of unit sales needed to break-even.Multiply the number of units by the selling price to give the break-even point (BEP) in monetary terms.If a target profit is required, then this can be added to fixed costs, and the total divided by the contribution per units to show total sales required in order to achieve the target profit.USES OF BREAK-EVEN ANALYSISBusinesses use break-even analysis when forecasting future levels of activity. This is a useful tool to show the effects of changes in costs, and also changes in selling price. Managers can clearly identify sales levels to achieve predicted profit figuresRent cost (£)R。