罗斯公司理财Chap004全英文题库及答案

- 格式:doc

- 大小:1.04 MB

- 文档页数:86

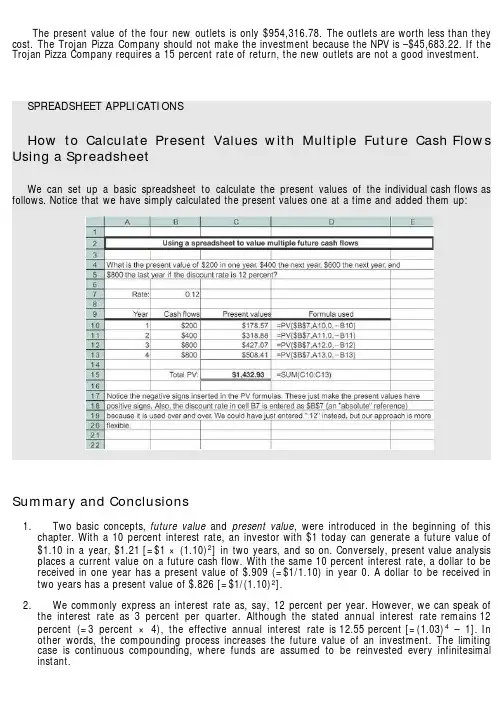

The present value of the four new outlets is only $954,316.78. The outlets are worth less than they cost. The Trojan Pizza Company should not make the investment because the NPV is –$45,683.22. If the Trojan Pizza Company requires a 15 percent rate of return, the new outlets are not a good investment.SPREADSHEET APPLICATIONSHow to Calculate Present Values with Multiple Future Cash Flows Using a SpreadsheetWe can set up a basic spreadsheet to calculate the present values of the individual cash flows as follows. Notice that we have simply calculated the present values one at a time and added them up:Summary and Conclusions1. Two basic concepts, future value and present value, were introduced in the beginning of thischapter. With a 10 percent interest rate, an investor with $1 today can generate a future value of $1.10 in a year, $1.21 [=$1 × (1.10)2] in two years, and so on. Conversely, present value analysis places a current value on a future cash flow. With the same 10 percent interest rate, a dollar to be received in one year has a present value of $.909 (=$1/1.10) in year 0. A dollar to be received in two years has a present value of $.826 [=$1/(1.10)2].2. We commonly express an interest rate as, say, 12 percent per year. However, we can speak ofthe interest rate as 3 percent per quarter. Although the stated annual interest rate remains 12 percent (=3 percent × 4), the effective annual interest rate is 12.55 percent [=(1.03)4 – 1]. In other words, the compounding process increases the future value of an investment. The limiting case is continuous compounding, where funds are assumed to be reinvested every infinitesimal instant.3. A basic quantitative technique for financial decision making is net present value analysis. Thenet present value formula for an investment that generates cash flows (C i) in future periods is:The formula assumes that the cash flow at date 0 is the initial investment (a cash outflow).4. Frequently, the actual calculation of present value is long and tedious. The computation of thepresent value of a long-term mortgage with monthly payments is a good example of this. We presented four simplifying formulas:5. We stressed a few practical considerations in the application of these formulas:1. The numerator in each of the formulas, C, is the cash flow to be received one full periodhence.2. Cash flows are generally irregular in practice. To avoid unwieldy problems, assumptions tocreate more regular cash flows are made both in this textbook and in the real world.3. A number of present value problems involve annuities (or perpetuities) beginning a fewperiods hence. Students should practice combining the annuity (or perpetuity) formula withthe discounting formula to solve these problems.4. Annuities and perpetuities may have periods of every two or every n years, rather thanonce a year. The annuity and perpetuity formulas can easily handle such circumstances.5. We frequently encounter problems where the present value of one annuity must beequated with the present value of another annuity.Concept Questions1. Compounding and Period As you increase the length of time involved, what happens tofuture values? What happens to present values?2. Interest Rates What happens to the future value of an annuity if you increase the rate r?What happens to the present value?3. Present Value Suppose two athletes sign 10-year contracts for $80 million. In one case, we’retold that the $80 million will be paid in 10 equal installments. In the other case, we’re told that the $80 million will be paid in 10 installments, but the installments will increase by 5 percent per year.Who got the better deal?4. APR and EAR Should lending laws be changed to require lenders to report EARs instead ofAPRs? Why or why not?5. Time Value On subsidized Stafford loans, a common source of financial aid for collegestudents, interest does not begin to accrue until repayment begins. Who receives a bigger subsidy,a freshman or a senior? Explain.Use the following information to answer the next five questions:Toyota Motor Credit Corporation (TMCC), a subsidiary of Toyota Motor Corporation, offered some securities for sale to the public on March 28, 2008. Under the terms of the deal, TMCC promised to repay the owner of one of these securities $100,000 on March 28, 2038, but investors would receive nothing until then. Investors paid TMCC $24,099 for each of these securities; so they gave up $24,099 on March 28, 2008, for the promise of a $100,000 payment 30 years later.6. Time Value of Money Why would TMCC be willing to accept such a small amount today($24,099) in exchange for a promise to repay about four times that amount ($100,000) in the future?7. Call Provisions TMCC has the right to buy back the securities on the anniversary date at aprice established when the securities were issued (this feature is a term of this particular deal).What impact does this feature have on the desirability of this security as an investment?8. Time Value of Money Would you be willing to pay $24,099 today in exchange for $100,000 in30 years? What would be the key considerations in answering yes or no? Would your answerdepend on who is making the promise to repay?9. Investment Comparison Suppose that when TMCC offered the security for $24,099 the U.S.Treasury had offered an essentially identical security. Do you think it would have had a higher or lower price? Why?10. Length of Investment The TMCC security is bought and sold on the New York StockExchange. If you looked at the price today, do you think the price would exceed the $24,099 original price? Why? If you looked in the year 2019, do you think the price would be higher or lower than today’s price? Why?Questions and Problems: connect™BASIC (Questions 1–20)1. Simple Interest versus Compound Interest First City Bank pays 9 percent simple intereston its savings account balances, whereas Second City Bank pays 9 percent interest compounded annually. If you made a $5,000 deposit in each bank, how much more money would you earn from your Second City Bank account at the end of 10 years?2. Calculating Future Values Compute the future value of $1,000 compounded annually for1. 10 years at 6 percent.2. 10 years at 9 percent.3. 20 years at 6 percent.4. Why is the interest earned in part (c) not twice the amount earned in part (a)?3. Calculating Present Values For each of the following, compute the present value:4. Calculating Interest Rates Solve for the unknown interest rate in each of the following:5. Calculating the Number of Periods Solve for the unknown number of years in each of thefollowing:6. Calculating the Number of Periods At 9 percent interest, how long does it take to doubleyour money? To quadruple it?7. Calculating Present Values Imprudential, Inc., has an unfunded pension liability of $750million that must be paid in 20 years. To assess the value of the firm’s stock, financial analysts want to discount this liability back to the present. If the relevant discount rate is 8.2 percent, what is the present value of this liability?8. Calculating Rates of Return Although appealing to more refined tastes, art as a collectiblehas not always performed so profitably. During 2003, Sotheby’s sold the Edgar Degas bronze sculpture Petite Danseuse de Quartorze Ans at auction for a price of $10,311,500. Unfortunately for the previous owner, he had purchased it in 1999 at a price of $12,377,500. What was his annual rate of return on this sculpture?9. Perpetuities An investor purchasing a British consol is entitled to receive annual paymentsfrom the British government forever. What is the price of a consol that pays $120 annually if the next payment occurs one year from today? The market interest rate is 5.7 percent.10. Continuous Compounding Compute the future value of $1,900 continuously compounded for1. 5 years at a stated annual interest rate of 12 percent.2. 3 years at a stated annual interest rate of 10 percent.3. 10 years at a stated annual interest rate of 5 percent.4. 8 years at a stated annual interest rate of 7 percent.11. Present Value and Multiple Cash Flows Conoly Co. has identified an investment projectwith the following cash flows. If the discount rate is 10 percent, what is the present value of these cash flows? What is the present value at 18 percent? At 24 percent?12. Present Value and Multiple Cash Flows Investment X offers to pay you $5,500 per year fornine years, whereas Investment Y offers to pay you $8,000 per year for five years. Which of these cash flow streams has the higher present value if the discount rate is 5 percent? If the discount rate is 22 percent?13. Calculating Annuity Present Value An investment offers $4,300 per year for 15 years, withthe first payment occurring one year from now. If the required return is 9 percent, what is the value of the investment? What would the value be if the payments occurred for 40 years? For 75 years? Forever?14. Calculating Perpetuity Values The Perpetual Life Insurance Co. is trying to sell you aninvestment policy that will pay you and your heirs $20,000 per year forever. If the required return on this investment is 6.5 percent, how much will you pay for the policy? Suppose the Perpetual Life Insurance Co. told you the policy costs $340,000. At what interest rate would this be a fair deal? 15. Calculating EAR Find the EAR in each of the following cases:16. Calculating APR Find the APR, or stated rate, in each of the following cases:17. Calculating EAR First National Bank charges 10.1 percent compounded monthly on itsbusiness loans. First United Bank charges 10.4 percent compounded semiannually. As a potential borrower, to which bank would you go for a new loan?18. Interest Rates Well-known financial writer Andrew Tobias argues that he can earn 177percent per year buying wine by the case. Specifically, he assumes that he will consume one $10 bottle of fine Bordeaux per week for the next 12 weeks. He can either pay $10 per week or buy a case of 12 bottles today. If he buys the case, he receives a 10 percent discount and, by doing so, earns the 177 percent. Assume he buys the wine and consumes the first bottle today. Do you agree with his analysis? Do you see a problem with his numbers?19. Calculating Number of Periods One of your customers is delinquent on his accounts payablebalance. You’ve mutually agreed to a repayment schedule of $600 per month. You will charge .9 percent per month interest on the overdue balance. If the current balance is $18,400, how long will it take for the account to be paid off?20. Calculating EAR Friendly’s Quick Loans, Inc., offers you “three for four or I knock on yourdoor.” This means you get $3 today and repay $4 when you get your paycheck in one week (orelse). What’s the effective annual return Friendly’s earns on this lending business? If you were brave enough to ask, what APR would Friendly’s say you were paying?INTERMEDIATE (Questions 21–50)21. Future Value What is the future value in seven years of $1,000 invested in an account with astated annual interest rate of 8 percent,1. Compounded annually?2. Compounded semiannually?3. Compounded monthly?4. Compounded continuously?5. Why does the future value increase as the compounding period shortens?22. Simple Interest versus Compound Interest First Simple Bank pays 6 percent simpleinterest on its investment accounts. If First Complex Bank pays interest on its accounts compounded annually, what rate should the bank set if it wants to match First Simple Bank over an investment horizon of 10 years?23. Calculating Annuities You are planning to save for retirement over the next 30 years. To dothis, you will invest $700 a month in a stock account and $300 a month in a bond account. The return of the stock account is expected to be 10 percent, and the bond account will pay 6 percent.When you retire, you will combine your money into an account with an 8 percent return. How much can you withdraw each month from your account assuming a 25-year withdrawal period?24. Calculating Rates of Return Suppose an investment offers to quadruple your money in 12months (don’t believe it). What rate of return per quarter are you being offered?25. Calculating Rates of Return You’re trying to choose between two different investments, bothof which have up-front costs of $75,000. Investment G returns $135,000 in six years. Investment H returns $195,000 in 10 years. Which of these investments has the higher return?26. Growing Perpetuities Mark Weinstein has been working on an advanced technology in lasereye surgery. His technology will be available in the near term. He anticipates his first annual cash flow from the technology to be $215,000, received two years from today. Subsequent annual cash flows will grow at 4 percent in perpetuity. What is the present value of the technology if the discount rate is 10 percent?27. Perpetuities A prestigious investment bank designed a new security that pays a quarterlydividend of $5 in perpetuity. The first dividend occurs one quarter from today. What is the price of the security if the stated annual interest rate is 7 percent, compounded quarterly?28. Annuity Present Values What is the present value of an annuity of $5,000 per year, with thefirst cash flow received three years from today and the last one received 25 years from today? Usea discount rate of 8 percent.29. Annuity Present Values What is the value today of a 15-year annuity that pays $750 a year?The annuity’s first payment occurs six years from today. The annual interest rate is 12 percent for years 1 through 5, and 15 percent thereafter.30. Balloon Payments Audrey Sanborn has just arranged to purchase a $450,000 vacation homein the Bahamas with a 20 percent down payment. The mortgage has a 7.5 percent stated annualinterest rate, compounded monthly, and calls for equal monthly payments over the next 30 years.Her first payment will be due one month from now. However, the mortgage has an eight-year balloon payment, meaning that the balance of the loan must be paid off at the end of year 8. There were no other transaction costs or finance charges. How much will Audrey’s balloon payment be in eight years?31. Calculating Interest Expense You receive a credit card application from Shady BanksSavings and Loan offering an introductory rate of 2.40 percent per year, compounded monthly for the first six months, increasing thereafter to 18 percent compounded monthly. Assuming you transfer the $6,000 balance from your existing credit card and make no subsequent payments, how much interest will you owe at the end of the first year?32. Perpetuities Barrett Pharmaceuticals is considering a drug project that costs $150,000 todayand is expected to generate end-of-year annual cash flows of $13,000, forever. At what discount rate would Barrett be indifferent between accepting or rejecting the project?33. Growing Annuity Southern California Publishing Company is trying to decide whether to reviseits popular textbook, Financial Psychoanalysis Made Simple. The company has estimated that the revision will cost $65,000. Cash flows from increased sales will be $18,000 the first year. These cash flows will increase by 4 percent per year. The book will go out of print five years from now.Assume that the initial cost is paid now and revenues are received at the end of each year. If the company requires an 11 percent return for such an investment, should it undertake the revision? 34. Growing Annuity Your job pays you only once a year for all the work you did over theprevious 12 months. Today, December 31, you just received your salary of $60,000, and you plan to spend all of it. However, you want to start saving for retirement beginning next year. You have decided that one year from today you will begin depositing 5 percent of your annual salary in an account that will earn 9 percent per year. Your salary will increase at 4 percent per year throughout your career. How much money will you have on the date of your retirement 40 years from today?35. Present Value and Interest Rates What is the relationship between the value of an annuityand the level of interest rates? Suppose you just bought a 12-year annuity of $7,500 per year at the current interest rate of 10 percent per year. What happens to the value of your investment if interest rates suddenly drop to 5 percent? What if interest rates suddenly rise to 15 percent?36. Calculating the Number of Payments You’re prepared to make monthly payments of $250,beginning at the end of this month, into an account that pays 10 percent interest compounded monthly. How many payments will you have made when your account balance reaches $30,000? 37. Calculating Annuity Present Values You want to borrow $80,000 from your local bank tobuy a new sailboat. You can afford to make monthly payments of $1,650, but no more. Assuming monthly compounding, what is the highest APR you can afford on a 60-month loan?38. Calculating Loan Payments You need a 30-year, fixed-rate mortgage to buy a new home for$250,000. Your mortgage bank will lend you the money at a 6.8 percent APR for this 360-month loan. However, you can only afford monthly payments of $1,200, so you offer to pay off any remaining loan balance at the end of the loan in the form of a single balloon payment. How large will this balloon payment have to be for you to keep your monthly payments at $1,200?39. Present and Future Values The present value of the following cash flow stream is $6,453when discounted at 10 percent annually. What is the value of the missing cash flow?40. Calculating Present Values You just won the TVM Lottery. You will receive $1 million todayplus another 10 annual payments that increase by $350,000 per year. Thus, in one year you receive $1.35 million. In two years, you get $1.7 million, and so on. If the appropriate interest rate is 9 percent, what is the present value of your winnings?41. EAR versus APR You have just purchased a new warehouse. To finance the purchase, you’vearranged for a 30-year mortgage for 80 percent of the $2,600,000 purchase price. The monthly payment on this loan will be $14,000. What is the APR on this loan? The EAR?42. Present Value and Break-Even Interest Consider a firm with a contract to sell an asset for$135,000 three years from now. The asset costs $96,000 to produce today. Given a relevant discount rate on this asset of 13 percent per year, will the firm make a profit on this asset? At what rate does the firm just break even?43. Present Value and Multiple Cash Flows What is the present value of $4,000 per year, at adiscount rate of 7 percent, if the first payment is received 9 years from now and the last payment is received 25 years from now?44. Variable Interest Rates A 15-year annuity pays $1,500 per month, and payments are madeat the end of each month. If the interest rate is 13 percent compounded monthly for the first seven years, and 9 percent compounded monthly thereafter, what is the present value of the annuity? 45. Comparing Cash Flow Streams You have your choice of two investment accounts.Investment A is a 15-year annuity that features end-of-month $1,200 payments and has an interest rate of 9.8 percent compounded monthly. Investment B is a 9 percent continuously compounded lump-sum investment, also good for 15 years. How much money would you need to invest in B today for it to be worth as much as Investment A 15 years from now?46. Calculating Present Value of a Perpetuity Given an interest rate of 7.3 percent per year,what is the value at date t = 7 of a perpetual stream of $2,100 annual payments that begins at date t = 15?47. Calculating EAR A local finance company quotes a 15 percent interest rate on one-year loans.So, if you borrow $26,000, the interest for the year will be $3,900. Because you must repay a total of $29,900 in one year, the finance company requires you to pay $29,900/12, or $2,491.67, per month over the next 12 months. Is this a 15 percent loan? What rate would legally have to be quoted? What is the effective annual rate?48. Calculating Present Values A 5-year annuity of ten $4,500 semiannual payments will begin 9years from now, with the first payment coming 9.5 years from now. If the discount rate is 12 percent compounded monthly, what is the value of this annuity five years from now? What is the value three years from now? What is the current value of the annuity?49. Calculating Annuities Due Suppose you are going to receive $10,000 per year for five years.The appropriate interest rate is 11 percent.1. What is the present value of the payments if they are in the form of an ordinary annuity?What is the present value if the payments are an annuity due?2. Suppose you plan to invest the payments for five years. What is the future value if thepayments are an ordinary annuity? What if the payments are an annuity due?3. Which has the highest present value, the ordinary annuity or annuity due? Which has thehighest future value? Will this always be true?50. Calculating Annuities Due You want to buy a new sports car from Muscle Motors for$65,000. The contract is in the form of a 48-month annuity due at a 6.45 percent APR. What will your monthly payment be?CHALLENGE (Questions 51–76)51. Calculating Annuities Due You want to lease a set of golf clubs from Pings Ltd. The leasecontract is in the form of 24 equal monthly payments at a 10.4 percent stated annual interest rate, compounded monthly. Because the clubs cost $3,500 retail, Pings wants the PV of the lease payments to equal $3,500. Suppose that your first payment is due immediately. What will your monthly lease payments be?52. Annuities You are saving for the college education of your two children. They are two yearsapart in age; one will begin college 15 years from today and the other will begin 17 years from today. You estimate your children’s college expenses to be $35,000 per year per child, payable at the beginning of each school year. The annual interest rate is 8.5 percent. How much money must you deposit in an account each year to fund your children’s education? Your deposits begin one year from today. You will make your last deposit when your oldest child enters college. Assume four years of college.53. Growing Annuities Tom Adams has received a job offer from a large investment bank as aclerk to an associate banker. His base salary will be $45,000. He will receive his first annual salary payment one year from the day he begins to work. In addition, he will get an immediate $10,000 bonus for joining the company. His salary will grow at 3.5 percent each year. Each year he will receive a bonus equal to 10 percent of his salary. Mr. Adams is expected to work for 25 years.What is the present value of the offer if the discount rate is 12 percent?54. Calculating Annuities You have recently won the super jackpot in the Washington StateLottery. On reading the fine print, you discover that you have the following two options:1. You will receive 31 annual payments of $175,000, with the first payment being deliveredtoday. The income will be taxed at a rate of 28 percent. Taxes will be withheld when the checks are issued.2. You will receive $530,000 now, and you will not have to pay taxes on this amount. Inaddition, beginning one year from today, you will receive $125,000 each year for 30 years.The cash flows from this annuity will be taxed at 28 percent.Using a discount rate of 10 percent, which option should you select?55. Calculating Growing Annuities You have 30 years left until retirement and want to retirewith $1.5 million. Your salary is paid annually, and you will receive $70,000 at the end of the current year. Your salary will increase at 3 percent per year, and you can earn a 10 percent return on the money you invest. If you save a constant percentage of your salary, what percentage of your salary must you save each year?56. Balloon Payments On September 1, 2007, Susan Chao bought a motorcycle for $25,000. Shepaid $1,000 down and financed the balance with a five-year loan at a stated annual interest rate of8.4 percent, compounded monthly. She started the monthly payments exactly one month after thepurchase (i.e., October 1, 2007). Two years later, at the end of October 2009, Susan got a new job and decided to pay off the loan. If the bank charges her a 1 percent prepayment penalty based on the loan balance, how much must she pay the bank on November 1, 2009?57. Calculating Annuity Values Bilbo Baggins wants to save money to meet three objectives.First, he would like to be able to retire 30 years from now with a retirement income of $20,000 per month for 20 years, with the first payment received 30 years and 1 month from now. Second, he would like to purchase a cabin in Rivendell in 10 years at an estimated cost of $320,000. Third, after he passes on at the end of the 20 years of withdrawals, he would like to leave an inheritance of $1,000,000 to his nephew Frodo. He can afford to save $1,900 per month for the next 10 years.If he can earn an 11 percent EAR before he retires and an 8 percent EAR after he retires, how much will he have to save each month in years 11 through 30?58. Calculating Annuity Values After deciding to buy a new car, you can either lease the car orpurchase it with a three-year loan. The car you wish to buy costs $38,000. The dealer has a special leasing arrangement where you pay $1 today and $520 per month for the next three years. If you purchase the car, you will pay it off in monthly payments over the next three years at an 8 percent APR. You believe that you will be able to sell the car for $26,000 in three years. Should you buy or lease the car? What break-even resale price in three years would make you indifferent between buying and leasing?59. Calculating Annuity Values An All-Pro defensive lineman is in contract negotiations. Theteam has offered the following salary structure:All salaries are to be paid in a lump sum. The player has asked you as his agent to renegotiate the terms. He wants a $9 million signing bonus payable today and a contract value increase of $750,000. He also wants an equal salary paid every three months, with the first paycheck three months from now. If the interest rate is 5 percent compounded daily, what is the amount of his quarterly check? Assume 365 days in a year.60. Discount Interest Loans This question illustrates what is known as discount interest. Imagineyou are discussing a loan with a somewhat unscrupulous lender. You want to borrow $20,000 for one year. The interest rate is 14 percent. You and the lender agree that the interest on the loan will be .14 × $20,000 = $2,800. So, the lender deducts this interest amount from the loan up front and gives you $17,200. In this case, we say that the discount is $2,800. What’s wrong here?61. Calculating Annuity Values You are serving on a jury. A plaintiff is suing the city for injuriessustained after a freak street sweeper accident. In the trial, doctors testified that it will be five years before the plaintiff is able to return to work. The jury has already decided in favor of the plaintiff. You are the foreperson of the jury and propose that the jury give the plaintiff an award to cover the following: (1) The present value of two years’ back pay. The plaintiff’s annual salary for the last two years would have been $42,000 and $45,000, respectively. (2) The present value of five years’ future salary. You assume the salary will be $49,000 per year. (3) $150,000 for pain and suffering. (4) $25,000 for court costs. Assume that the salary payments are equal amounts paid at the end of each month. If the interest rate you choose is a 9 percent EAR, what is the size of the settlement? If you were the plaintiff, would you like to see a higher or lower interest rate?62. Calculating EAR with Points You are looking at a one-year loan of $10,000. The interest rateis quoted as 9 percent plus three points. A point on a loan is simply 1 percent (one percentage point) of the loan amount. Quotes similar to this one are very common with home mortgages. The interest rate quotation in this example requires the borrower to pay three points to the lender up front and repay the loan later with 9 percent interest. What rate would you actually be paying here? What is the EAR for a one-year loan with a quoted interest rate of 12 percent plus two points? Is your answer affected by the loan amount?63. EAR versus APR Two banks in the area offer 30-year, $200,000 mortgages at 6.8 percent andcharge a $2,100 loan application fee. However, the application fee charged by Insecurity Bank and Trust is refundable if the loan application is denied, whereas that charged by I. M. Greedy and Sons Mortgage Bank is not. The current disclosure law requires that any fees that will be refunded if the applicant is rejected be included in calculating the APR, but this is not required with nonrefundable。

罗斯公司理财第四章全英文题库及答案Chapter 04 - Discounted Cash Flow ValuationChapter 04 Discounted Cash Flow Valuation Answer KeyMultiple Choice Questions1. An annuity stream of cash flow payments is a set of:A. level cash flows occurring each time period for a fixed length of time.B. level cash flows occurring each time period forever.C. increasing cash flows occurring each time period for a fixed length of time.D. increasing cash flows occurring each time period forever.E. arbitrary cash flows occurring each time period for no more than10 years.Difficulty level: Easy Topic: ANNUITY Type: DEFINITIONS2. Annuities where the payments occur at the end of each time period are called _____, whereas_____ refer to annuity streams with payments occurring at the beginning of each time period.A. ordinary annuities; early annuitiesB. late annuities; straight annuitiesC. straight annuities; late annuitiesD. annuities due; ordinary annuitiesE. ordinary annuities; annuities dueDifficulty level: Easy Topic: ANNUITIES DUE Type: DEFINITIONS4-1Chapter 04 - Discounted Cash Flow Valuation 3. An annuity stream where the payments occur forever is called a(n):A. annuity due.B. indemnity.C. perpetuity.D. amortized cash flow stream.E. amortization table.Difficulty level: Easy Topic: PERPETUITY Type: DEFINITIONS4. The interest rate expressed in terms of the interest payment made each period is called the_____ rate.A. stated annual interestB. compound annual interestC. effective annual interestD. periodic interestE. daily interestDifficulty level: Easy Topic: STATED INTEREST RATES Type: DEFINITIONS5. The interest rate expressed as if it were compounded once per year is called the _____ rate.A. stated interestB. compound interestC. effective annualD. periodic interestE. daily interestDifficulty level: Easy Topic: EFFECTIVE ANNUAL RATE Type: DEFINITIONS4-2Chapter 04 - Discounted Cash Flow Valuation6. The interest rate charged per period multiplied by the number of periods per year is called the_____ rate.A. effective annualB. annual percentageC. periodic interestD. compound interestE. daily interestDifficulty level: Easy Topic: ANNUAL PERCENTAGE RATE Type: DEFINITIONS7. Paying off long-term debt by making installment payments is called: A. foreclosing on the debt.B. amortizing the debt.C. funding the debt.D. calling the debt.E. None of the above.Difficulty level: Easy Topic: AMORTIZATION Type: DEFINITIONS8. You are comparing two annuities which offer monthly payments for ten years. Both annuitiesare identical with the exception of the payment dates. Annuity A pays on the first of each monthwhile annuity B pays on the last day of each month. Which one of the following statements iscorrect concerning these two annuities?A. Both annuities are of equal value today.B. Annuity B is an annuity due.C. Annuity A has a higher future value than annuity B.D. Annuity B has a higher present value than annuity A.E. Both annuities have the same future value as of ten years from today.Difficulty level: Medium Topic: ORDINARY ANNUITY VERSUS ANNUITY DUE Type: CONCEPTS4-3Chapter 04 - Discounted Cash Flow Valuation9. You are comparing two investment options. The cost to invest in either option is the same today. Both options will provide you with $20,000 of income. Option A pays five annual payments starting with $8,000 the first year followed by four annual payments of $3,000 each. Option B pays five annual payments of $4,000 each. Which one of the following statements is correct given these two investment options?A. Both options are of equal value given that they both provide $20,000 of income.B. Option A is the better choice of the two given any positive rate of return.C. Option B has a higher present value thanoption A given a positive rate of return. D. Option B has a lower future value at year 5 than option A given a zero rate of return. E. Option A is preferable because it is an annuity due.Difficulty level: Medium Topic: UNEVEN CASH FLOWS AND PRESENT VALUE Type: CONCEPTS10. You are considering two projects with the following cash flows:Which of the following statements are true concerning these two projects?I. Both projects have the same future value at the end of year 4, given a positive rate of return. II. Both projects have the same future value given a zero rate of return. III. Both projects have the same future value at any point in time, given a positive rate of return. IV. Project A has a higher future value than project B, given a positive rate of return. A. II onlyB. IV onlyC. I and III onlyD. II and IV onlyE. I, II, and III onlyDifficulty level: Medium Topic: UNEVEN CASH FLOWS AND FUTURE VALUE Type: CONCEPTS4-4Chapter 04 - Discounted Cash Flow Valuation11. A perpetuity differs from an annuity because:A. perpetuity payments vary with the rate of inflation.B. perpetuity payments vary with the market rate of interest.C. perpetuity payments are variable while annuity payments are constant.D. perpetuity payments never cease.E. annuity payments never cease.Difficulty level: Easy Topic: PERPETUITY VERSUS ANNUITY Type: CONCEPTS12. Which one of the following statements concerning the annual percentage rate is correct? A. The annual percentage rate considers interest on interest.B. The rate of interest you actually pay on a loan is called the annual percentage rate.C. The effective annual rate is lower than the annual percentage rate when an interest rate is compounded quarterly.D. When firms advertise the annual percentage rate they areviolating U.S. truth-in-lending laws.E. The annual percentage rate equals the effective annual rate when the rate on an account is designated as simple interest.Difficulty level: Medium Topic: ANNUAL PERCENTAGE RATE Type: CONCEPTS13. Which one of the following statements concerning interest ratesis correct? A. The stated rate is the same as the effective annual rate.B. An effective annual rate is the rate that applies if interest were charged annually.C. The annual percentage rate increases as the number of compounding periods per year increases.D. Banks prefer more frequent compounding on their savings accounts.E. For any positive rate of interest, the effective annual rate will always exceed the annual percentage rate.Difficulty level: Medium Topic: INTEREST RATES Type: CONCEPTS4-5Chapter 04 - Discounted Cash Flow Valuation14. Which of the following statements concerning the effectiveannual rate are correct? I. When making financial decisions, you should compare effective annual rates rather than annual percentage rates.II. The more frequently interest is compounded, the higher the effective annual rate. III. A quoted rate of 6% compounded continuously has a higher effective annual rate than if the rate were compounded daily.IV. When borrowing and choosing which loan to accept, you should select the offer with the highest effective annual rate.A. I and II onlyB. I and IV onlyC. I, II, and III onlyD. II, III, and IV onlyE. I, II, III, and IVDifficulty level: Medium Topic: EFFECTIVE ANNUAL RATE Type: CONCEPTS15. The highest effective annual rate that can be derived from an annual percentage rate of 9% is computed as:A. .09e - 1.B. e.09 , q.C. e , (1 + .09).D. e.09 - 1.E. (1 + .09)q.Difficulty level: Medium Topic: CONTINUOUS COMPOUNDING Type: CONCEPTS16. The time value of money concept can be defined as:A. the relationship between the supply and demand of money.B. the relationship between money spent versus money received.C. the relationship between a dollar to be received in the future and a dollar today.D. the relationship between interest rate stated and amount paid.E. None of the above.Difficulty level: Easy Topic: TIME VALUE Type: CONCEPTS4-6Chapter 04 - Discounted Cash Flow Valuation17. Discounting cash flows involves:A. discounting only those cash flows that occur at least 10 years in the future.B. estimating only the cash flows that occur in the first 4 years of a project.C. multiplying expected future cash flows by the cost of capital.D. discounting all expected future cash flows toreflect the time value of money. E. taking the cash discount offered on trade merchandise.Difficulty level: Easy Topic: CASH FLOWS Type: CONCEPTS18. Compound interest:A. allows for the reinvestment of interest payments.B. does not allow for the reinvestment of interest payments.C. is the same as simple interest.D. provides a value that is less than simple interest.E. Both A and D.Difficulty level: Easy Topic: INTEREST Type: CONCEPTS19. An annuity:A. is a debt instrument that pays no interest.B. is a stream of payments that varies with current market interest rates.C. is a level stream of equal payments through time.D. has no value.E. None of the above.Difficulty level: Easy Topic: ANNUITY Type: CONCEPTS4-7Chapter 04 - Discounted Cash Flow Valuation20. The stated rate of interest is 10%. Which form of compounding will give the highesteffective rate of interest?A. annual compoundingB. monthly compoundingC. daily compoundingD. continuous compoundingE. It is impossible to tell without knowing the term of the loan.Difficulty level: Easy Topic: COMPOUNDING Type: CONCEPTS21. The present value of future cash flows minus initial cost is called:A. the future value of the project.B. the net present value of the project.C. the equivalent sum of the investment.D. the initial investment risk equivalent value.E. None of the above.Difficulty level: Easy Topic: PRESENT VALUE Type: CONCEPTS22. Find the present value of $5,325 to be received in one period if the rate is 6.5%.A. $5,000.00B. $5,023.58C. $5,644.50D. $5,671.13E. None of the above.Difficulty level: Easy Topic: PRESENT VALUE - SINGLE SUM Type: PROBLEMS4-8Chapter 04 - Discounted Cash Flow Valuation23. If you have a choice to earn simple interest on $10,000 forthree years at 8% or annually compounded interest at 7.5% for threeyears which one will pay more and by how much? A. Simple interest by $50.00B. Compound interest by $22.97C. Compound interest by $150.75D. Compound interest by $150.00E. None of the above.Simple Interest = $10,000 (.08)(3) = $2,400; 3Compound Interest = $10,000((1.075) - 1) = $2,422.97;Difference = $2,422.97 - $2,400 = $22.97Difficulty level: Easy Topic: SIMPLE & COMPOUND INTEREST Type: PROBLEMS24. Bradley Snapp has deposited $7,000 in a guaranteed investment account with a promised rate of 6% compounded annually. He plans toleave it there for 4 full years when he will make a down payment on acar after graduation. How much of a down payment will he be able to make?A. $1,960.00B. $2,175.57C. $8,960.00D. $8,837.34E. $9,175.574$7,000 (1.06) = $8,837.34Difficulty level: Easy Topic: FUTURE VALUE - SINGLE SUM Type: PROBLEMS4-9Chapter 04 - Discounted Cash Flow Valuation25. Your parents are giving you $100 a month for four years whileyou are in college. At a 6% discount rate, what are these payments worth to you when you first start college? A. $3,797.40B. $4,167.09C. $4,198.79D. $4,258.03E. $4,279.32Difficulty level: Easy Topic: ORDINARY ANNUITY AND PRESENT VALUE Type: PROBLEMS4-10Chapter 04 - Discounted Cash Flow Valuation26. You just won the lottery! As your prize you will receive $1,200a month for 100 months. Ifyou can earn 8% on your money, what is this prize worth to you today?A. $87,003.69B. $87,380.23C. $87,962.77D. $88,104.26E. $90,723.76Difficulty level: Easy Topic: ORDINARY ANNUITY AND PRESENT VALUE Type: PROBLEMS4-11Chapter 04 - Discounted Cash Flow Valuation27. Todd is able to pay $160 a month for five years for a car. If the interest rate is 4.9%, howmuch can Todd afford to borrow to buy a car? A. $6,961.36B. $8,499.13C. $8,533.84D. $8,686.82E. $9,588.05Difficulty level: Easy Topic: ORDINARY ANNUITY AND PRESENT VALUE Type: PROBLEMS4-12Chapter 04 - Discounted Cash Flow Valuation28. You are the beneficiary of a life insurance policy. Theinsurance company informs you that you have two options for receiving the insurance proceeds. You can receive a lump sum of $50,000 today or receive payments of $641 a month for ten years. You can earn 6.5% on your money. Which option should you take and why?A. You should accept the payments because they are worth $56,451.91 today.B. You should accept the payments because they are worth$56,523.74 today. C. You should accept the payments because they are worth $56,737.08 today. D. You should accept the $50,000 because the payments are only worth $47,757.69 today. E. You should accept the $50,000 because the payments are only worth $47,808.17 today.Difficulty level: Medium Topic: ORDINARY ANNUITY AND PRESENT VALUE Type: PROBLEMS4-13Chapter 04 - Discounted Cash Flow Valuation29. Your employer contributes $25 a week to your retirement plan. Assume that you work for your employer for another twenty years and that the applicable discount rate is 5%. Given theseassumptions, what is this employee benefit worth to you today? A. $13,144.43B. $15,920.55C. $16,430.54D. $16,446.34E. $16,519.02Difficulty level: Medium Topic: ORDINARY ANNUITY AND PRESENT VALUE Type: PROBLEMS4-14Chapter 04 - Discounted Cash Flow Valuation30. You have a sub-contracting job with a local manufacturing firm. Your agreement calls forannual payments of $50,000 for the next five years. At a discount rate of 12%, what is this jobworth to you today?A. $180,238.81B. $201,867.47C. $210,618.19D. $223,162.58E. $224,267.10Difficulty level: Medium Topic: ORDINARY ANNUITY AND PRESENT VALUE Type: PROBLEMS4-15Chapter 04 - Discounted Cash Flow Valuation31. The Ajax Co. just decided to save $1,500 a month for the next five years as a safety net for recessionary periods. The money will be set aside in a separate savings account which pays 3.25% interest compounded monthly. It deposits the first $1,500 today. If the company had wanted to deposit an equivalent lump sum today, how much would it have had to deposit? A. $82,964.59B. $83,189.29C. $83,428.87D. $83,687.23E. $84,998.01Difficulty level: Medium Topic: ANNUITY DUE AND PRESENT VALUE Type: PROBLEMS4-16Chapter 04 - Discounted Cash Flow Valuation32. You need some money today and the only friend you have that has any is your ‘miserly' friend. He agrees to loan you the money you need, if you make payments of $20 a month for the next six months. In keeping with his reputation, he requires that the first payment be paid today. He also charges you 1.5% interest per month. How much money are you borrowing? A. $113.94B. $115.65C. $119.34D. $119.63E. $119.96Difficulty level: Medium Topic: ANNUITY DUE AND PRESENT VALUE Type: PROBLEMS4-17Chapter 04 - Discounted Cash Flow Valuation33. You buy an annuity which will pay you $12,000 a year for ten years. The payments are paid on the first day of each year. What is the value of this annuity today at a 7% discount rate? A. $84,282.98B. $87,138.04C. $90,182.79D. $96,191.91E. $116,916.21Difficulty level: Medium Topic: ANNUITY DUE AND PRESENT VALUE Type: PROBLEMS4-18Chapter 04 - Discounted Cash Flow Valuation34. You are scheduled to receive annual payments of $10,000 for each of the next 25 years. Your discount rate is 8.5%. What is the difference in the present value if you receive these payments at the beginning of each year rather than at the end of each year? A. $8,699B. $9,217C. $9,706D. $10,000E. $10,850Difference = $111,040.97 - $102,341.91 = $8,699.06 = $8,699 (rounded) Note: The difference = .085 , $102,341.91 = $8,699.06Difficulty level: Medium Topic: ORDINARY ANNUITY VERSUS ANNUITY DUE Type: PROBLEMS4-19Chapter 04 - Discounted Cash Flow Valuation35. You are comparing two annuities with equal present values. The applicable discount rate is 7.5%. One annuity pays $5,000 on the first day of each year for twenty years. How much does the second annuity pay each year for twenty years if it pays at the end of each year? A. $4,651B. $5,075C. $5,000D. $5,375E. $5,405Because each payment is received one year later, then the cash flow has to equal: $5,000 , (1+ .075) = $5,375Difficulty level: Medium Topic: ORDINARY ANNUITY VERSUS ANNUITY DUE Type: PROBLEMS4-20Chapter 04 - Discounted Cash Flow Valuation36. Martha receives $100 on the first of each month. Stewartreceives $100 on the last day of each month. Both Martha and Stewartwill receive payments for five years. At an 8% discount rate, what is the difference in the present value of these two sets of payments? A. $32.88B. $40.00C. $99.01D. $108.00E. $112.50Difference = $4,964.72 - $4,931.84 = $32.88Difficulty level: Medium Topic: ORDINARY ANNUITY VERSUS ANNUITY DUE Type: PROBLEMS4-21Chapter 04 - Discounted Cash Flow Valuation 37. What is the future value of $1,000 a year for five years at a 6% rate of interest?A. $4,212.36B. $5,075.69C. $5,637.09D. $6,001.38E. $6,801.91Difficulty level: Easy Topic: ORDINARY ANNUITY AND FUTURE VALUE Type: PROBLEMS38. What is the future value of $2,400 a year for three years at an 8% rate of interest?A. $6,185.03B. $6,847.26C. $7,134.16D. $7,791.36E. $8,414.67Difficulty level: Easy Topic: ORDINARY ANNUITY AND FUTURE VALUE Type: PROBLEMS4-22Chapter 04 - Discounted Cash Flow Valuation39. Janet plans on saving $3,000 a year and expects to earn 8.5%.How much will Janet have atthe end of twenty-five years if she earns what she expects? A. $219,317.82B. $230,702.57C. $236,003.38D. $244,868.92E. $256,063.66Difficulty level: Easy Topic: ORDINARY ANNUITY AND FUTURE VALUE Type: PROBLEMS4-23Chapter 04 - Discounted Cash Flow Valuation40. Toni adds $3,000 to her savings on the first day of each year. Tim adds $3,000 to his savingson the last day of each year. They both earn a 9% rate of return. What is the difference in theirsavings account balances at the end of thirty years?A. $35,822.73B. $36,803.03C. $38,911.21D. $39,803.04E. $40,115.31Difference = $445,725.65 - $408,922.62 = $36,803.03Note: Difference = $408,922.62 , .09 = $36,803.03Difficulty level: Medium Topic: ANNUITY DUE VERSUS ORDINARY ANNUITY Type: PROBLEMS4-24Chapter 04 - Discounted Cash Flow Valuation41. You borrow $5,600 to buy a car. The terms of the loan call for monthly payments for fouryears at a 5.9% rate of interest. What is the amount of each payment?A. $103.22B. $103.73C. $130.62D. $131.26E. $133.04Difficulty level: Easy Topic: ORDINARY ANNUITY PAYMENTS Type: PROBLEMS4-25Chapter 04 - Discounted Cash Flow Valuation42. You borrow $149,000 to buy a house. The mortgage rate is 7.5% and the loan period is 30 years. Payments are made monthly. If you pay for the house according to the loan agreement, how much total interest will you pay?A. $138,086B. $218,161C. $226,059D. $287,086E. $375,059Total interest = ($1,041.83 , 30 , 12) - $149,000 = $226,058.80 = $226,059 (rounded)Difficulty level: Medium Topic: ORDINARY ANNUITY PAYMENTS AND COST OF INTEREST Type: PROBLEMS4-26Chapter 04 - Discounted Cash Flow Valuation43. The Great Giant Corp. has a management contract with its newly hired president. The contract requires a lump sum payment of $25 millionbe paid to the president upon the completion of her first ten years of service. The company wants to set aside an equal amount of funds each year to cover this anticipated cash outflow. The company can earn 6.5% on these funds. How much must the company set aside each year for this purpose? A. $1,775,042.93B. $1,798,346.17C. $1,801,033.67D. $1,852,617.25E. $1,938,018.22Difficulty level: Easy Topic: ORDINARY ANNUITY PAYMENTS AND FUTURE VALUE Type: PROBLEMS4-27Chapter 04 - Discounted Cash Flow Valuation44. You retire at age 60 and expect to live another 27 years. On the day you retire, you have $464,900 in your retirement savings account. You are conservative and expect to earn 4.5% on your money during your retirement. How much can you withdraw from your retirement savings each month if you plan to die on the day you spend your last penny?A. $2,001.96B. $2,092.05C. $2,398.17D. $2,472.00E. $2,481.27Difficulty level: Medium Topic: ORDINARY ANNUITY PAYMENTS AND PRESENT VALUE Type: PROBLEMS4-28Chapter 04 - Discounted Cash Flow Valuation45. The McDonald Group purchased a piece of property for $1.2 million. It paid a down payment of 20% in cash and financed the balance. The loan terms require monthly payments for 15 years at an annual percentage rate of 7.75% compounded monthly. What is the amount of each mortgage payment?A. $7,440.01B. $8,978.26C. $9,036.25D. $9,399.18E. $9,413.67Amount financed = $1,200,000 , (1 - .2) = $960,000Difficulty level: Medium Topic: ORDINARY ANNUITY PAYMENTS AND PRESENT VALUE Type: PROBLEMS4-29Chapter 04 - Discounted Cash Flow Valuation46. You estimate that you will have $24,500 in student loans by the time you graduate. Theinterest rate is 6.5%. If you want to have this debt paid in full within five years, how much mustyou pay each month?A. $471.30B. $473.65C. $476.79D. $479.37E. $480.40Difficulty level: Medium Topic: ORDINARY ANNUITY PAYMENTS AND PRESENT VALUE Type: PROBLEMS4-30Chapter 04 - Discounted Cash Flow Valuation47. You are buying a previously owned car today at a price of $6,890. You are paying $500down in cash and financing the balance for 36 months at 7.9%. What is the amount of each loanpayment?A. $198.64B. $199.94C. $202.02D. $214.78E. $215.09Amount financed = $6,890 - $500 = $6,390Difficulty level: Medium Topic: ORDINARY ANNUITY PAYMENTS AND PRESENT VALUE Type: PROBLEMS4-31Chapter 04 - Discounted Cash Flow Valuation48. The Good Life Insurance Co. wants to sell you an annuity which will pay you $500 per quarter for 25 years. You want to earn a minimum rate of return of 5.5%. What is the most youare willing to pay as a lump sum today to buy this annuity? A. $26,988.16B. $27,082.94C. $27,455.33D. $28,450.67E. $28,806.30Difficulty level: Medium Topic: ORDINARY ANNUITY PAYMENTS AND PRESENT VALUE Type: PROBLEMS4-32Chapter 04 - Discounted Cash Flow Valuation49. Your car dealer is willing to lease you a new car for $299 a month for 60 months. Payments are due on the first day of each month starting with the day you sign the lease contract. If your cost of money is 4.9%, what is the current value of the lease? A. $15,882.75B. $15,906.14C. $15,947.61D. $16,235.42E. $16,289.54Difficulty level: Medium Topic: ANNUITY DUE PAYMENTS AND PRESENT VALUE Type: PROBLEMS4-33Chapter 04 - Discounted Cash Flow Valuation50. Your great-aunt left you an inheritance in the form of a trust. The trust agreement states that you are to receive $2,500 on the firstday of each year, starting immediately and continuing for fifty years. What is the value of this inheritance today if the applicable discount rate is 6.35%? A. $36,811.30B. $37,557.52C. $39,204.04D. $39,942.42E. $40,006.09Difficulty level: Medium Topic: ANNUITY DUE PAYMENTS AND PRESENT VALUE Type: PROBLEMS51. Beatrice invests $1,000 in an account that pays 4% simple interest. How much more could she have earned over a five-year period if the interest had compounded annually? A. $15.45B. $15.97C. $16.65D. $17.09E. $21.67Ending value at 4% simple interest = $1,000 + ($1,000 , .04 , 5) = $1,200.00; Ending value at 54% compounded annually = $1,000 , (1 +.04) = $1,216.65;Difference = $1,216.65 - $1,200.00 = $16.65Difficulty level: Easy Topic: SIMPLE VERSUS COMPOUND INTEREST Type: PROBLEMS4-34Chapter 04 - Discounted Cash Flow Valuation52. Your firm wants to save $250,000 to buy some new equipment three years from now. The plan is to set aside an equal amount of money on the first day of each year starting today. The firm can earn a 4.7% rate of return. How much does the firm have to save each year to achieve its goal?A. $75,966.14B. $76,896.16C. $78,004.67D. $81.414.14E. $83,333.33Difficulty level: Medium Topic: ANNUITY DUE PAYMENTS AND FUTURE VALUE Type: PROBLEMS4-35Chapter 04 - Discounted Cash Flow Valuation53. Today is January 1. Starting today, Sam is going to contribute $140 on the first of each month to his retirement account. His employer contributes an additional 50% of the amount contributed by Sam. If both Sam and his employer continue to do this and Sam can earn a monthly rateof ? of 1 percent, how much will he have in his retirement account 35 years from now?A. $199,45.944B. $200,456.74C. $249,981.21D. $299,189.16E. $300,685.11Difficulty level: Medium Topic: ANNUITY DUE PAYMENTS AND FUTURE VALUE Type: PROBLEMS54. You are considering an annuity which costs $100,000 today. The annuity pays $6,000 a year. The rate of return is 4.5%. What is the length of the annuity time period? A. 24.96 yearsB. 29.48 yearsC. 31.49 yearsD. 33.08 yearsE. 38.00 yearsDifficulty level: Medium Topic: ORDINARY ANNUITY TIME PERIODS AND PRESENT VALUE Type: PROBLEMS4-36Chapter 04 - Discounted Cash Flow Valuation55. Today, you signed loan papers agreeing to borrow $4,954.85 at 9% compounded monthly.The loan payment is $143.84 a month. How many loan payments must you make before theloan is paid in full?A. 29.89B. 36.00C. 38.88D. 40.00E. 41.03Difficulty level: Medium Topic: ORDINARY ANNUITY TIME PERIODS AND PRESENT VALUE Type: PROBLEMS4-37Chapter 04 - Discounted Cash Flow Valuation56. Winston Enterprises would like to buy some additional land and build a new factory. The anticipated total cost is $136 million. The owner of the firm is quite conservative and will only do this when the company has sufficient funds to pay cash for the entire expansion project. Management has decided to save $450,000 a month for thispurpose. The firm earns 6% compounded monthly on the funds it saves. How long does the company have to wait before expanding its operations?A. 184.61 monthsB. 199.97 monthsC. 234.34 monthsD. 284.61 monthsE. 299.97 monthsDifficulty level: Medium Topic: ORDINARY ANNUITY TIME PERIODS AND FUTURE VALUE Type: PROBLEMS4-38Chapter 04 - Discounted Cash Flow Valuation57. Today, you are retiring. You have a total of $413,926 in your retirement savings and have the funds invested such that you expect to earn an average of 3%, compounded monthly, on this money throughout your retirement years. You want to withdraw $2,500 at the beginning of every month, starting today. How long will it be until you run out of money? A. 185.00 monthsB. 213.29 monthsC. 227.08 monthsD. 236.84 months。

Chapter 01 - Introduction to Corporate FinanceChapter 01 Introduction to Corporate Finance Answer KeyMultiple Choice Questions1. The person generally directly responsible for overseeing the tax management, cost accounting, financial accounting, and information system functions is the:A. treasurer.B. director.C. controller.D. chairman of the board.E. chief executive officer.Difficulty level: EasyTopic: CONTROLLERType: DEFINITIONS2. The person generally directly responsible for overseeing the cash and credit functions,financial planning, and capital expenditures is the:A. treasurer.B. director.C. controller.D. chairman of the board.E. chief operations officer.1-1Chapter 01 - Introduction to Corporate Finance3. The process of planning and managing a firm's long-term investments is called:A. working capital management.B. financial depreciation.C. agency cost analysis.D. capital budgeting.E. capital structure.Difficulty level: EasyTopic: CAPITAL BUDGETINGType: DEFINITIONS4. The mixture of debt and equity used by a firm to finance its operations is called:A. working capital management.B. financial depreciation.C. cost analysis.D. capital budgeting.E. capital structure.5. The management of a firm's short-term assets and liabilities is called:A. working capital management.B. debt management.C. equity management.D. capital budgeting.E. capital structure.1-2Chapter 01 - Introduction to Corporate Finance6. A business owned by a single individual is called a:A. corporation.B. sole proprietorship.C. general partnership.D. limited partnership.E. limited liability company.7. A business formed by two or more individuals who each have unlimited liability for businessdebts is called a:A. corporation.B. sole proprietorship.C. general partnership.D. limited partnership.E. limited liability company.8. The division of profits and losses among the members of a partnership is formalized in the:A. indemnity clause.B. indenture contract.C. statement of purpose.D. partnership agreement.E. group charter.9. A business created as a distinct legal entity composed of one or more individuals or entities iscalled a:A. corporation.B. sole proprietorship.C. general partnership.D. limited partnership.E. unlimited liability company.Difficulty level: EasyTopic: CORPORATIONType: DEFINITIONS1-3Chapter 01 - Introduction to Corporate Finance10. The corporate document that sets forth the business purpose of a firm is the:A. indenture contract.B. state tax agreement.C. corporate bylaws.D. debt charter.E. articles of incorporation.11. The rules by which corporations govern themselves are called:A. indenture provisions.B. indemnity provisions.C. charter agreements.D. bylaws.E. articles of incorporation.12. A business entity operated and taxed like a partnership, but with limited liability for theowners, is called a:A. limited liability company.B. general partnership.C. limited proprietorship.D. sole proprietorship.E. corporation.13. The primary goal of financial management is to:A. maximize current dividends per share of the existing stock.B. maximize the current value per share of the existing stock.C. avoid financial distress.D. minimize operational costs and maximize firm efficiency.E. maintain steady growth in both sales and net earnings.14. A conflict of interest between the stockholders and management of a firm is called:A. stockholders' liability.B. corporate breakdown.C. the agency problem.D. corporate activism.E. legal liability.1-4Chapter 01 - Introduction to Corporate Finance15. Agency costs refer to:A. the total dividends paid to stockholders over the lifetime of a firm.B. the costs that result from default and bankruptcy of a firm.C. corporate income subject to double taxation.D. the costs of any conflicts of interest between stockholders and management.E. the total interest paid to creditors over the lifetime of the firm.16. A stakeholder is:A. any person or entity that owns shares of stock of a corporation.B. any person or entity that has voting rights based on stock ownership of a corporation.C. a person who initially started a firm and currently has management control over the cashflows of the firm due to his/her current ownership of company stock.D. a creditor to whom the firm currently owes money and who consequently has a claim on thecash flows of the firm.E. any person or entity other than a stockholder or creditor who potentially has a claim on thecash flows of the firm.17. The Sarbanes Oxley Act of 2002 is intended to:A. protect financial managers from investors.B. not have any effect on foreign companies.C. reduce corporate revenues.D. protect investors from corporate abuses.E. decrease audit costs for U.S. firms.18. The treasurer and the controller of a corporation generally report to the:A. board of directors.B. chairman of the board.C. chief executive officer.D. president.E. chief financial officer.19. Which one of the following statements is correct concerning the organizational structure ofa corporation?A. The vice president of finance reports to the chairman of the board.B. The chief executive officer reports to the board of directors.C. The controller reports to the president.D. The treasurer reports to the chief executive officer.E. The chief operations officer reports to the vice president of production.Difficulty level: MediumTopic: ORGANIZATIONAL STRUCTUREType: CONCEPTS1-5Chapter 01 - Introduction to Corporate Finance20. Which one of the following is a capital budgeting decision?A. determining how much debt should be borrowed from a particular lenderB. deciding whether or not to open a new storeC. deciding when to repay a long-term debtD. determining how much inventory to keep on handE. determining how much money should be kept in the checking account21. The Sarbanes Oxley Act was enacted in:A. 1952.B. 1967.C. 1998.D. 2002.E. 2006.22. Since the implementation of Sarbanes-Oxley, the cost of going public in the United Stateshas:A. increased.B. decreased.C. remained about the same.D. been erratic, but over time has decreased.E. It is impossible to tell since Sarbanes-Oxley compliance does not involve direct cost to thefirm.23. Working capital management includes decisions concerning which of the following?I. accounts payableII. long-term debtIII. accounts receivableIV. inventoryA. I and II onlyB. I and III onlyC. II and IV onlyD. I, II, and III onlyE. I, III, and IV onlyDifficulty level: MediumTopic: WORKING CAPITAL MANAGEMENTType: CONCEPTS1-6Chapter 01 - Introduction to Corporate Finance24. Working capital management:A. ensures that sufficient equipment is available to produce the amount of product desired on adaily basis.B. ensures that long-term debt is acquired at the lowest possible cost.C. ensures that dividends are paid to all stockholders on an annual basis.D. balances the amount of company debt to the amount of available equity.E. is concerned with the upper portion of the balance sheet.Difficulty level: EasyTopic: WORKING CAPITAL MANAGEMENTType: CONCEPTS25. Which one of the following statements concerning a sole proprietorship is correct?A. A sole proprietorship is the least common form of business ownership.B. The profits of a sole proprietorship are taxed twice.C. The owners of a sole proprietorship share profits as established by the partnership agreement.D. The owner of a sole proprietorship may be forced to sell his/her personal assets to paycompany debts.E. A sole proprietorship is often structured as a limited liability company.Difficulty level: EasyTopic: SOLE PROPRIETORSHIPType: CONCEPTS26. Which one of the following statements concerning a sole proprietorship is correct?A. The life of the firm is limited to the life span of the owner.B. The owner can generally raise large sums of capital quite easily.C. The ownership of the firm is easy to transfer to another individual.D. The company must pay separate taxes from those paid by the owner.E. The legal costs to form a sole proprietorship are quite substantial.Difficulty level: EasyTopic: SOLE PROPRIETORSHIPType: CONCEPTS1-7Chapter 01 - Introduction to Corporate Finance27. Which one of the following best describes the primary advantage of being a limited partnerrather than a general partner?A. entitlement to a larger portion of the partnership's incomeB. ability to manage the day-to-day affairs of the businessC. no potential financial lossD. greater management responsibilityE. liability for firm debts limited to the capital investedDifficulty level: EasyTopic: PARTNERSHIPType: CONCEPTS28. A general partner:A. has less legal liability than a limited partner.B. has more management responsibility than a limited partner.C. faces double taxation whereas a limited partner does not.D. cannot lose more than the amount of his/her equity investment.E. is the term applied only to corporations which invest in partnerships.Difficulty level: EasyTopic: PARTNERSHIPType: CONCEPTS29. A partnership:A. is taxed the same as a corporation.B. agreement defines whether the business income will be taxed like a partnership or acorporation.C. terminates at the death of any general partner.D. has less of an ability to raise capital than a proprietorship.E. allows for easy transfer of interest from one general partner to another.Difficulty level: EasyTopic: PARTNERSHIPType: CONCEPTS1-8Chapter 01 - Introduction to Corporate Finance30. Which of the following are disadvantages of a partnership?I. limited life of the firmII. personal liability for firm debtIII. greater ability to raise capital than a sole proprietorshipIV. lack of ability to transfer partnership interestA. I and II onlyB. III and IV onlyC. II and III onlyD. I, II, and IV onlyE. I, III, and IV onlyDifficulty level: MediumTopic: PARTNERSHIPType: CONCEPTS31. Which of the following are advantages of the corporate form of business ownership?I. limited liability for firm debtII. double taxationIII. ability to raise capitalIV. unlimited firm lifeA. I and II onlyB. III and IV onlyC. I, II, and III onlyD. II, III, and IV onlyE. I, III, and IV onlyDifficulty level: MediumTopic: CORPORATIONType: CONCEPTS32. Which one of the following statements is correct concerning corporations?A. The largest firms are usually corporations.B. The majority of firms are corporations.C. The stockholders are usually the managers of a corporation.D. The ability of a corporation to raise capital is quite limited.E. The income of a corporation is taxed as personal income of the stockholders.Difficulty level: EasyTopic: CORPORATIONType: CONCEPTS1-9Chapter 01 - Introduction to Corporate Finance33. Which one of the following statements is correct?A. Both partnerships and corporations incur double taxation.B. Both sole proprietorships and partnerships are taxed in a similar fashion.C. Partnerships are the most complicated type of business to form.D. Both partnerships and corporations have limited liability for general partners and shareholders.E. All types of business formations have limited lives.Difficulty level: MediumTopic: BUSINESS TYPESType: CONCEPTS34. The articles of incorporation:A. can be used to remove company management.B. are amended annually by the company stockholders.C. set forth the number of shares of stock that can be issued.D. set forth the rules by which the corporation regulates its existence.E. can set forth the conditions under which the firm can avoid double taxation.35. The bylaws:A. establish the name of the corporation.B. are rules which apply only to limited liability companies.C. set forth the purpose of the firm.D. mandate the procedure for electing corporate directors.E. set forth the procedure by which the stockholders elect the senior managers of the firm.36. The owners of a limited liability company prefer:A. being taxed like a corporation.B. having liability exposure similar to that of a sole proprietor.C. being taxed personally on all business income.D. having liability exposure similar to that of a general partner.E. being taxed like a corporation with liability like a partnership.Difficulty level: MediumTopic: LIMITED LIABILITY COMPANYType: CONCEPTS1-10Chapter 01 - Introduction to Corporate Finance37. Which one of the following business types is best suited to raising large amounts ofcapital?A. sole proprietorshipB. limited liability companyC. corporationD. general partnershipE. limited partnershipDifficulty level: EasyTopic: CORPORATIONType: CONCEPTS38. Which type of business organization has all the respective rights and privileges ofa legalperson?A. sole proprietorshipB. general partnershipC. limited partnershipD. corporationE. limited liability companyDifficulty level: EasyTopic: CORPORATIONType: CONCEPTS39. Financial managers should strive to maximize the current value per share of the existingstock because:A. doing so guarantees the company will grow in size at the maximum possible rate.B. doing so increases the salaries of all the employees.C. the current stockholders are the owners of the corporation.D. doing so means the firm is growing in size faster than its competitors.E. the managers often receive shares of stock as part of their compensation.Difficulty level: EasyTopic: GOAL OF FINANC IAL MANAGEMENTType: CONCEPTS1-11Chapter 01 - Introduction to Corporate Finance40. The decisions made by financial managers should all be ones which increase the:A. size of the firm.B. growth rate of the firm.C. marketability of the managers.D. market value of the existing owners' equity.E. financial distress of the firm.Difficulty level: EasyTopic: GOAL OF FINANCIAL MANAGEMENTType: CONCEPTS41. Which one of the following actions by a financial manager creates an agency problem?A. refusing to borrow money when doing so will create losses for the firmB. refusing to lower selling prices if doing so will reduce the net profitsC. agreeing to expand the company at the expense of stockholders' valueD. agreeing to pay bonuses based on the book value of the company stockE. increasing current costs in order to increase the market value of the stockholders' equity42. Which of the following help convince managers to work in the best interest of the stockholders?I. compensation based on the value of the stockII. stock option plansIII. threat of a proxy fightIV. threat of conversion to a partnershipA. I and II onlyB. II and III onlyC. I, II and III onlyD. I and III onlyE. I, II, III, and IVDifficulty level: MediumTopic: AGENCY PROBLEMType: CONCEPTS1-12Chapter 01 - Introduction to Corporate Finance43. Which form of business structure faces the greatest agency problems?A. sole proprietorshipB. general partnershipC. limited partnershipD. corporationE. limited liability company44. A proxy fight occurs when:A. the board solicits renewal of current members.B. a group solicits proxies to replace the board of directors.C. a competitor offers to sell their ownership in the firm.D. the firm files for bankruptcy.E. the firm is declared insolvent.45. Which one of the following parties is considered a stakeholder of a firm?A. employeeB. short-term creditorC. long-term creditorD. preferred stockholderE. common stockholderDifficulty level: EasyTopic: STAKEHOLDERSType: CONCEPTS46. Which of the following are key requirements of the Sarbanes-Oxley Act?I. Officers of the corporation must review and sign annual reports.II. Officers of the corporation must now own more than 5% of the firm's stock. III. Annual reports must list deficiencies in internal controlsIV. Annual reports must be filed with the SEC within 30 days of year end.A. I onlyB. II onlyC. I and III onlyD. II and III onlyE. II and IV onlyDifficulty level: MediumTopic: SARBANES-OXLEYType: CONCEPTS1-13Chapter 01 - Introduction to Corporate Finance47. Insider trading is:A. legal.B. illegal.C. impossible to have in our efficient market.D. discouraged, but legal.E. list only the securities of the largest firms.48. Sole proprietorships are predominantly started because:A. they are easily and cheaply setup.B. the proprietorship life is limited to the business owner's life.C. all business taxes are paid as individual tax.D. All of the above.E. None of the above.Difficulty level: EasyTopic: SOLE PROPRIETORSHIPSType: CONCEPTS49. Managers are encouraged to act in shareholders' interests by:A. shareholder election of a board of directors who select management.B. the threat of a takeover by another firm.C. compensation contracts that tie compensation to corporate success.D. Both A and B.E. All of the above.Difficulty level: MediumTopic: GOVERNANCEType: CONCEPTS50. The Securities Exchange Act of 1934 focuses on:A. all stock transactions.B. sales of existing securities.C. issuance of new securities.D. insider trading.E. Federal Deposit Insurance Corporation (FDIC) insurance.Difficulty level: MediumTopic: REGULATIONType: CONCEPTS1-14Chapter 01 - Introduction to Corporate Finance51. The basic regulatory framework in the United States was provided by:A. the Securities Act of 1933.B. the Securities Exchange Act of 1934.C. the monetary system.D. A and B.E. All of the above.Difficulty level: MediumTopic: REGULATIONType: CONCEPTS52. The Securities Act of 1933 focuses on:A. all stock transactions.B. sales of existing securities.C. issuance of new securities.D. insider trading.E. Federal Deposit Insurance Corporation (FDIC) insurance.Difficulty level: EasyTopic: REGULATIONType: CONCEPTS53. In a limited partnership:A. each limited partner's liability is limited to his net worth.B. each limited partner's liability is limited to the amount he put into the partnership.C. each limited partner's liability is limited to his annual salary.D. there is no limitation on liability; only a limitation on what the partner can earn.E. None of the above.Difficulty level: EasyTopic: LIMITED PARTNERSHIPType: CONCEPTS1-15Chapter 01 - Introduction to Corporate Finance54. Accounting profits and cash flows are:A. generally the same since they reflect current laws and accounting standards.B. generally the same since accounting profits reflect when the cash flows are received.C. generally not the same since GAAP allows for revenue recognition separate from the receiptof cash flows.D. generally not the same because cash inflows occur before revenue recognition.E. Both c and d.1-16。