hkas20 government grant

- 格式:pdf

- 大小:204.49 KB

- 文档页数:8

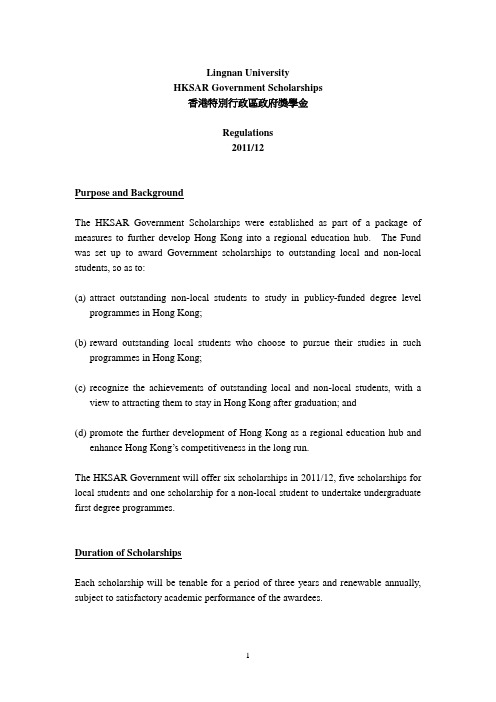

Lingnan UniversityHKSAR Government Scholarships香港特別行政區政府獎學金Regulations2011/12Purpose and BackgroundThe HKSAR Government Scholarships were established as part of a package of measures to further develop Hong Kong into a regional education hub. The Fund was set up to award Government scholarships to outstanding local and non-local students, so as to:(a)attract outstanding non-local students to study in publicy-funded degree levelprogrammes in Hong Kong;(b)reward outstanding local students who choose to pursue their studies in suchprogrammes in Hong Kong;(c)recognize the achievements of outstanding local and non-local students, with aview to attracting them to stay in Hong Kong after graduation; and(d)promote the further development of Hong Kong as a regional education hub andenhance Hong Kong’s competitiveness in the long run.The HKSAR Government will offer six scholarships in 2011/12, five scholarships for local students and one scholarship for a non-local student to undertake undergraduate first degree programmes.Duration of ScholarshipsEach scholarship will be tenable for a period of three years and renewable annually, subject to satisfactory academic performance of the awardees.Value of ScholarshipsThe scholarships shall be HK$40,000 each per year for local students and HK$80,000 per year for a Mainland fee-paying student.Eligibility and CriteriaScholarships are awarded to first-year local students under a three-year programme and second-year Mainland fee-paying students under a four-year programme, having regard to following considerations:(a)excellent performance in academic studies;(b)recognized contribution to the institution/society;(c) demonstrated leadership and good communication skills; and(d) strong commitment to the Hong Kong community.Selection Procedures(a)In September, the Registry of Lingnan University shall generate a list of first-yearlocal admitttees from Faculty of Arts, Faculty of Business and Faculty of Social Sciences on the strength of their HKALE results.(b)The University will shortlist second-year Mainland fee-paying students admittedto Lingnan University under a four-year degree programme based on their academic results of the last academic year.(c)The scholarships shall be open for application by first-year local students andsecond-year Mainland fee-paying students as well.(d)In early November, Student Services Centre will invite shortlisted local andMainland fee-paying students to attend an internal interview conducted by the Standing Panel of Scholarships of the University. The Panel comprises Dean of Students as convenor; one academic staff respectively from each of Faculty of Arts, Faculty of Business and Faculty of Social Sciences and Director of Student Services as members; as well as one representative form the Students’ Union as observer.(e)The decision of the scholarship selection panel shall be final, and shall not besubject to appeal from students.(f)The nominations will be sent to the Government Secretariat, HKSAR.(g)In end November, the University shall then make a firm offer of scholarships, andwill inform successful candidates to sign an undertaking.Conditions for RenewalRenewal of each scholarship is on an annual basis, subject to continued outstanding academic performance in the preceding academic year (i.e. a cumulative GPA of 3.0 or above). The University scholarship selection panel will assess the performance of candidates eligible for scholarship renewal and confirms that they meet the requirement.Payment of ScholarshipsThe scholarship grants will be disbursed to the awardees in two equal instalments, in October and January respectively.Revision and AmendmentsAll conditions stated above may be revised, amended and updated from time to time upon agreement between the HKSAR Government and the University.。

icontents (6/12)MEMBERS' HANDBOOK CONTENTS OF VOLUME II(Updated to June 2012)Issue/(Reviewdate)PREFACE AND FRAMEWORKPREFACE Preface to Hong Kong Financial Reporting Standards ....................................10/06(9/10) CONCEPTUAL FRAMEWORKConceptual Framework for Financial Reporting ..............................................10/10HONG KONG ACCOUNTING STANDARDS (HKAS)HKAS 1 Revised Presentation of Financial Statements .............................................................12/07 (6/12) HKAS 2 Inventories .....................................................................................................3/04(1/10) HKAS 7 Statement of Cash Flows ...............................................................................12/04(1/10)HKAS 8 Accounting Policies, Changes in Accounting Estimates and Errors .................9/04(1/10) HKAS 10 Events after the Reporting Period ...................................................................3/04(1/10)HKAS 11 Construction Contracts ...................................................................................12/04(3/10) HKAS 12 Income Taxes ................................................................................................11/04(4/12) HKAS 16 Property, Plant and Equipment .......................................................................11/05(6/12) HKAS 17 Leases ...........................................................................................................12/04(6/10) HKAS 18 Revenue ........................................................................................................11/04(3/10) HKAS 19 Employee Benefits .........................................................................................12/04(7/11) HKAS 19 (2011) Employee Benefits .........................................................................................7/11HKAS 20 Accounting for Government Grants and Disclosure of Government Assistance ............................................................................................... 12/04(3/10) HKAS 21 The Effects of Changes in Foreign Exchange Rates .......................................3/04(6/10) HKAS 23 Revised Borrowing Costs .............................................................................................6/07(3/10)HKAS 24 Related Party Disclosures ..............................................................................12/04(11/09) HKAS 24 Revised Related Party Disclosures ..............................................................................11/09 HKAS 26 Accounting and Reporting by Retirement Benefit Plans ..................................8/04 HKAS 27 Revised Consolidated and Separate Financial Statements ...........................................3/08(6/11)HKAS 27 (2011) Separate Financial Statements .......................................................................6/11 HKAS 28 Investments in Associates ..............................................................................3/04(6/11)HKAS 28 (2011)Investments in Associates and Joint Ventures ................................................6/11Issue/(Reviewdate) HKAS 29 Financial Reporting in Hyperinflationary Economies ....................................3/04(4/10) HKAS 31 Interests in Joint Ventures ...........................................................................12/04(6/11) HKAS 32 Financial Instruments: Presentation .............................................................11/04(6/12) HKAS 33 Earnings per Share .....................................................................................3/04(3/10) HKAS 34 Interim Financial Reporting..........................................................................10/04(6/12) HKAS 36 Impairment of Assets ..................................................................................8/04(3/10) HKAS 37 Provisions, Contingent Liabilities and Contingent Assets .............................11/04(3/10) HKAS 38 Intangible Assets .........................................................................................8/04(3/10) HKAS 39 Financial Instruments: Recognition and Measurement .................................1/06(5/10) HKAS 40 Investment Property ....................................................................................11/05(6/10) HKAS 41 Agriculture ..................................................................................................12/04(6/10)HONG KONG FINANCIAL REPORTING STANDARDS (HKFRS)First-time Adoption of Hong Kong Financial Reporting Standards ...............12/08(6/12) HKFRS 1RevisedHKFRS 2 Share-based Payment ................................................................................4/04(2/10) HKFRS 3Business Combinations ...............................................................................3/08(2/12) RevisedHKFRS 4 Insurance Contracts ....................................................................................3/06(2/10) HKFRS 5 Non-current Assets Held for Sale and Discontinued Operations...................8/04(2/10) HKFRS 6 Exploration for and Evaluation of Mineral Resources ...................................2/05(2/10) HKFRS 7 Financial Instruments: Disclosures ..............................................................9/05(2/12) HKFRS 8 Operating Segments ..................................................................................3/07(11/09) HKFRS 9 Financial Instruments ..................................................................................11/09 (12/11) HKFRS 10 Consolidated Financial Statements .............................................................6/11 HKFRS 11 Joint Arrangements .....................................................................................6/11 HKFRS 12 Disclosure of Interests in Other Entities .......................................................6/11 HKFRS 13 Fair Value Measurement .............................................................................6/11Improvements to HKFRSs 2010 ................................................................... 5/10 IMPROVEMENTSTO HKFRSs 2010contents (6/12)iiIssue/(Reviewdate)HONG KONG (IFRIC) INTERPRETATIONS (HK(IFRIC)-Int)HK(IFRIC)-Int 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities ......8/04(7/10) HK(IFRIC)-Int 2 Members’ Shares in Co-operative Entities and Similar Instruments .................2/05(6/12) HK(IFRIC)-Int 4 Determining whether an Arrangement contains a Lease .................................2/05(7/10) HK(IFRIC)-Int 5 Rights to Interests arising from Decommissioning, Restoration andEnvironmental Rehabilitation Funds ..........................................................2/05(7/10) HK(IFRIC)-Int 6 Liabilities arising from Participating in a Specific Market – WasteElectrical and Electronic Equipment...........................................................9/05 HK(IFRIC)-Int 7 Applying the Restatement Approach under HKAS 29 Financial Reportingin Hyperinflationary Economies ................................................................1/06(7/10) HK(IFRIC)-Int 8 Scope of HKFRS 2 .........................................................................................5/06(7/10) HK(IFRIC)-Int 9 Reassessment of Embedded Derivatives .......................................................5/06(7/10) HK(IFRIC)-Int 10 Interim Financial Reporting and Impairment ...................................................9/06(7/10) HK(IFRIC)-Int 11 HKFRS 2–Group and Treasury Share Transactions ......................................1/07(7/10) HK(IFRIC)-Int 12 Service Concession Arrangements .................................................................3/07(8/10) HK(IFRIC)-Int 13 Customer Loyalty Programmes ......................................................................9/07(4/12) HK(IFRIC)-Int 14 HKAS 19 —The Limit on a Defined Benefit Asset, Minimum Funding9/07(4/12) Requirements and their Interaction ............................................................HK(IFRIC)-Int 15 Agreements for the Construction of Real Estate .............................................8/08(8/10) HK(IFRIC)-Int 16 Hedges of a Net Investment in a Foreign Operation........................................8/08(8/10) HK(IFRIC)-Int 17 Distributions of Non-cash Assets to Owners ...................................................12/08(8/10) HK(IFRIC)-Int 18 Transfers of Assets from Customers...............................................................2/09(8/10) HK(IFRIC)-Int 19 Extinguishing Financial Liabilities with Equity Instruments...............................12/09 HK(IFRIC)-Int 20 Stripping Costs in the Production Phase of a Surface Mine 11/11 HONG KONG INTERPRETATIONS (HK-Int)*HK-Int 4 Leases – Determination of the Length of Lease Term in respect of HongKong Land Leases ....................................................................................6/06 (12/09) HK-Int 5 Presentation of Financial Statements – Classification by the Borrower ofa Term Loan that Contains a Repayment on Demand Clause ....................11/10Note: * With effect from 24 May 2005, all Interpretations that are developed locally by the Institute are named Hong Kong Interpretations.HONG KONG (SIC) INTERPRETATIONS (HK(SIC)-Int)HK(SIC)-Int 10 Government Assistance – No Specific Relation to Operating Activities ..........12/04(8/10) HK(SIC)-Int 12 Consolidation – Special Purpose Entities ........................................................2/05(6/11) HK(SIC)-Int 13 Jointly Controlled Entities – Non-Monetary Contributions by Venturers ...........12/04(6/11) HK(SIC)-Int 15 Operating Leases – Incentives ......................................................................12/04(9/10) HK(SIC)-Int 25 Income Taxes – Changes in the Tax Status of an Enterprise or itsShareholders ............................................................................................12/04(8/10) HK(SIC)-Int 27 Evaluating the Substance of Transactions Involving the Legal Form of aLease ........................................................................................................12/04(9/10)contents (6/12)iiiivIssue/(Reviewdate)HK(SIC)-Int 29 Service Concession Arrangements: Disclosures .............................................12/04(8/10) HK(SIC)-Int 31 Revenue – Barter Transactions Involving Advertising Services .......................12/04(9/10) HK(SIC)-Int 32 Intangible Assets – Web Site Costs ................................................................12/04(9/10)GLOSSARY Glossary of Terms Relating to Hong Kong Financial Reporting Standards ........ 3/08(9/10) HKFRS-PE HONG KONG FINANCIAL REPORTING STANDARD FORPRIVATE ENTITIES ............................................................................ 4/10 (2/11)SME-FRF & SME-FRS SMALL AND MEDIUM-SIZED ENTITY FINANCIAL REPORTING FRAMEWORK AND FINANCIAL REPORTING STANDARD .......................................... 8/05 (2/11) ACCOUNTING GUIDELINES (AG)AG 1 Preparation and Presentation of Accounts from Incomplete Records ..............3/84 AG 5 Merger Accounting for Common Control Combinations ..................................11/05 AG 7 Preparation of Pro Forma Financial Information for Inclusion inInvestment Circulars..................................................................................3/06ACCOUNTING BULLETINS (AB)AB 1 Disclosure of Loans to Officers .......................................................................8/85 AB 3 Guidance on Disclosure of Directors’ Remuneration.......................................1/00 AB 4 Guidance on the Determination of Realised Profits and Losses in theContext of Distributions under the Hong Kong Companies Ordinance........5/10。

二十国集团领导人布里斯班峰会公报(双语)当地时间11月16日,二十国集团领导人第九次峰会15日至16日在澳大利亚布里斯班举行。

峰会发表公报,全文如下:二十国集团领导人布里斯班峰会公报(2014年11月15日-16日)G20 Leaders’ CommuniquéBrisbane Summit, 15-16 November 20141、促进全球增长以提高各国人民生活水平、创造高质量就业,是我们最重要的任务。

我们对一些主要经济体的更强劲增长势头表示欢迎。

但全球经济复苏依然缓慢和不均衡,未能带来我们需要的就业。

解决供给限制是释放经济增长潜力的关键,但世界经济也面临需求不足的制约。

包括金融市场和地缘政治紧张等风险依然存在。

因此,我们承诺本着伙伴关系开展工作,以促进增长、提高经济抗风险能力、加强全球机构。

1. Raising global growth to deliver better living standards and quality jobs for people across the world is our highest priority. We welcome stronger growth in some key economies. But the global recovery is slow, uneven and not delivering the jobs needed. The global economy is being held back by a shortfall in demand, while addressing supply constraints is key to lifting potential growth. Risks persist, including in financial markets and from geopolitical tensions. We commit to work in partnership to lift growth, boost economic resilience and strengthen global institutions.2、我们决心应对这些挑战,加快努力实现强劲、可持续、平衡增长并创造就业。

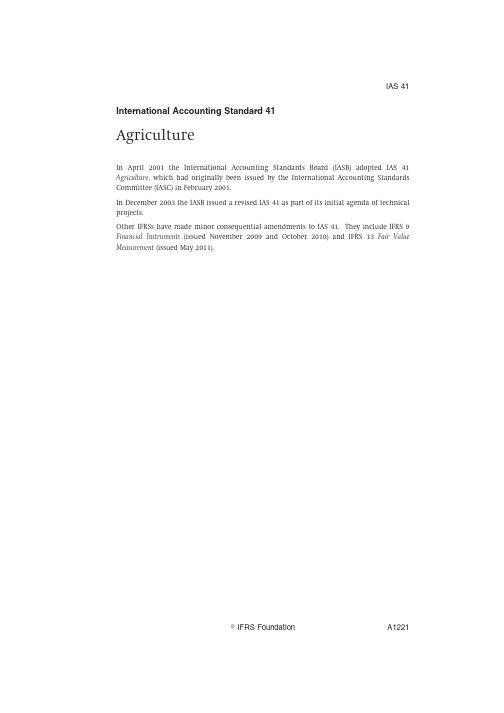

IAS41 International Accounting Standard41AgricultureIn April2001the International Accounting Standards Board(IASB)adopted IAS41 Agriculture,which had originally been issued by the International Accounting Standards Committee(IASC)in February2001.In December2003the IASB issued a revised IAS41as part of its initial agenda of technical projects.Other IFRSs have made minor consequential amendments to IAS41.They include IFRS9 Financial Instruments(issued November2009and October2010)and IFRS13Fair Value Measurement(issued May2011).IFRS Foundation A1221IAS41C ONTENTSfrom paragraph INTRODUCTION IN1 INTERNATIONAL ACCOUNTING STANDARD41AGRICULTUREOBJECTIVESCOPE1 DEFINITIONS5 Agriculture-related definitions5 General definitions8 RECOGNITION AND MEASUREMENT10 Gains and losses26 Inability to measure fair value reliably30 GOVERNMENT GRANTS34 DISCLOSURE40 General40 Additional disclosures for biological assets where fair value cannot bemeasured reliably54 Government grants57 EFFECTIVE DATE AND TRANSITION58FOR THE ACCOMPANYING DOCUMENTS LISTED BELOW,SEE PART B OF THIS EDITIONBASIS FOR CONCLUSIONSBASIS FOR IASC’S CONCLUSIONSILLUSTRATIVE EXAMPLESA1222IFRS FoundationIAS41 International Accounting Standard41Agriculture(IAS41)is set out in paragraphs1–61.All the paragraphs have equal authority but retain the IASC format of the Standard when it was adopted by the IASB.IAS41should be read in the context of its objective and the Basis for Conclusions,the Preface to International Financial Reporting Standards and the Conceptual Framework for Financial Reporting.IAS8Accounting Policies,Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies in the absence of explicit guidance.IFRS Foundation A1223IAS41IntroductionIN1IAS41prescribes the accounting treatment,financial statement presentation, and disclosures related to agricultural activity,a matter not covered in otherStandards.Agricultural activity is the management by an entity of the biologicaltransformation of living animals or plants(biological assets)for sale,intoagricultural produce,or into additional biological assets.IN2IAS41prescribes,among other things,the accounting treatment for biological assets during the period of growth,degeneration,production,and procreation,and for the initial measurement of agricultural produce at the point of harvest.It requires measurement at fair value less costs to sell from initial recognition ofbiological assets up to the point of harvest,other than when fair value cannot bemeasured reliably on initial recognition.However,IAS41does not deal withprocessing of agricultural produce after harvest;for example,processing grapesinto wine and wool into yarn.IN3There is a presumption that fair value can be measured reliably for a biological asset.However,that presumption can be rebutted only on initial recognition fora biological asset for which quoted market prices are not available and for whichalternative fair value measurements are determined to be clearly unreliable.Insuch a case,IAS41requires an entity to measure that biological asset at its costless any accumulated depreciation and any accumulated impairment losses.Once the fair value of such a biological asset becomes reliably measurable,anentity should measure it at its fair value less costs to sell.In all cases,an entityshould measure agricultural produce at the point of harvest at its fair value lesscosts to sell.IN4IAS41requires that a change in fair value less costs to sell of a biological asset be included in profit or loss for the period in which it arises.In agriculturalactivity,a change in physical attributes of a living animal or plant directlyenhances or diminishes economic benefits to the entity.Under atransaction-based,historical cost accounting model,a plantation forestry entitymight report no income until first harvest and sale,perhaps30years afterplanting.On the other hand,an accounting model that recognises andmeasures biological growth using current fair values reports changes in fairvalue throughout the period between planting and harvest.IN5IAS41does not establish any new principles for land related to agricultural activity.Instead,an entity follows IAS16Property,Plant and Equipment or IAS40Investment Property,depending on which standard is appropriate in thecircumstances.IAS16requires land to be measured either at its cost less anyaccumulated impairment losses,or at a revalued amount.IAS40requires landthat is investment property to be measured at its fair value,or cost less anyaccumulated impairment losses.Biological assets that are physically attached toland(for example,trees in a plantation forest)are measured at their fair valueless costs to sell separately from the land.IN6IAS41requires an unconditional government grant related to a biological asset measured at its fair value less costs to sell to be recognised in profit or loss when,and only when,the government grant becomes receivable.If a government A1224IFRS FoundationIAS41grant is conditional,including when a government grant requires an entity notto engage in specified agricultural activity,an entity should recognise thegovernment grant in profit or loss when,and only when,the conditionsattaching to the government grant are met.If a government grant relates to abiological asset measured at its cost less any accumulated depreciation and anyaccumulated impairment losses,the entity applies IAS20Accounting forGovernment Grants and Disclosure of Government Assistance.IN7IAS41is effective for annual financial statements covering periods beginning on or after1January2003.Earlier application is encouraged.IN8IAS41does not establish any specific transitional provisions.The adoption of IAS41is accounted for in accordance with IAS8Accounting Policies,Changes inAccounting Estimates and Errors.IN9The illustrative examples accompanying IAS41provide examples of the application of the Standard.The Basis for Conclusions summarises the Board’sreasons for adopting the requirements set out in IAS41.IFRS Foundation A1225IAS41International Accounting Standard41AgricultureObjectiveThe objective of this Standard is to prescribe the accounting treatment anddisclosures related to agricultural activity.Scope1This Standard shall be applied to account for the following when they relate to agricultural activity:(a)biological assets;(b)agricultural produce at the point of harvest;and(c)government grants covered by paragraphs34and35.2This Standard does not apply to:(a)land related to agricultural activity(see IAS16Property,Plant andEquipment and IAS40Investment Property);and(b)intangible assets related to agricultural activity(see IAS38IntangibleAssets).3This Standard is applied to agricultural produce,which is the harvested product of the entity’s biological assets,only at the point of harvest.Thereafter,IAS2Inventories or another applicable Standard is applied.Accordingly,this Standarddoes not deal with the processing of agricultural produce after harvest;forexample,the processing of grapes into wine by a vintner who has grown thegrapes.While such processing may be a logical and natural extension ofagricultural activity,and the events taking place may bear some similarity tobiological transformation,such processing is not included within the definitionof agricultural activity in this Standard.4The table below provides examples of biological assets,agricultural produce,and products that are the result of processing after harvest:Biological assets Agricultural produce Products that are theresult of processingafter harvestSheep Wool Y arn,carpetFelled trees Logs,lumberTrees in a plantationforestPlants Cotton Thread,clothingHarvested cane SugarDairy cattle Milk Cheesecontinued... A1226IFRS FoundationIAS41 ...continuedBiological assets Agricultural produce Products that are theresult of processingafter harvestPigs Carcass Sausages,cured hamsBushes Leaf Tea,cured tobaccoVines Grapes WineFruit trees Picked fruit Processed fruit DefinitionsAgriculture-related definitions5The following terms are used in this Standard with the meanings specified:Agricultural activity is the management by an entity of the biologicaltransformation and harvest of biological assets for sale or for conversioninto agricultural produce or into additional biological assets.Agricultural produce is the harvested product of the entity’s biologicalassets.A biological asset is a living animal or plant.Biological transformation comprises the processes of growth,degeneration,production,and procreation that cause qualitative orquantitative changes in a biological asset.Costs to sell are the incremental costs directly attributable to the disposalof an asset,excluding finance costs and income taxes.A group of biological assets is an aggregation of similar living animals orplants.Harvest is the detachment of produce from a biological asset or thecessation of a biological asset’s life processes.6Agricultural activity covers a diverse range of activities;for example,raising livestock,forestry,annual or perennial cropping,cultivating orchards andplantations,floriculture and aquaculture(including fish farming).Certaincommon features exist within this diversity:(a)Capability to change.Living animals and plants are capable of biologicaltransformation;(b)Management of change.Management facilitates biological transformationby enhancing,or at least stabilising,conditions necessary for the processto take place(for example,nutrient levels,moisture,temperature,fertility,and light).Such management distinguishes agricultural activityfrom other activities.For example,harvesting from unmanaged sources(such as ocean fishing and deforestation)is not agricultural activity;andIFRS Foundation A1227IAS41(c)Measurement of change.The change in quality(for example,genetic merit,density,ripeness,fat cover,protein content,and fibre strength)orquantity(for example,progeny,weight,cubic metres,fibre length ordiameter,and number of buds)brought about by biologicaltransformation or harvest is measured and monitored as a routinemanagement function.7Biological transformation results in the following types of outcomes:(a)asset changes through(i)growth(an increase in quantity orimprovement in quality of an animal or plant),(ii)degeneration(adecrease in the quantity or deterioration in quality of an animal orplant),or(iii)procreation(creation of additional living animals orplants);or(b)production of agricultural produce such as latex,tea leaf,wool,andmilk.General definitions8The following terms are used in this Standard with the meanings specified:Carrying amount is the amount at which an asset is recognised in thestatement of financial position.Fair value is the price that would be received to sell an asset or paid totransfer a liability in an orderly transaction between market participantsat the measurement date.(See IFRS13Fair Value Measurement.)Government grants are as defined in IAS20Accounting for GovernmentGrants and Disclosure of Government Assistance.9[Deleted]Recognition and measurement10An entity shall recognise a biological asset or agricultural produce when, and only when:(a)the entity controls the asset as a result of past events;(b)it is probable that future economic benefits associated with theasset will flow to the entity;and(c)the fair value or cost of the asset can be measured reliably.11In agricultural activity,control may be evidenced by,for example,legal ownership of cattle and the branding or otherwise marking of the cattle onacquisition,birth,or weaning.The future benefits are normally assessed bymeasuring the significant physical attributes.12A biological asset shall be measured on initial recognition and at the end of each reporting period at its fair value less costs to sell,except for thecase described in paragraph30where the fair value cannot be measuredreliably.A1228IFRS FoundationIAS4113Agricultural produce harvested from an entity’s biological assets shall be measured at its fair value less costs to sell at the point of harvest.Suchmeasurement is the cost at that date when applying IAS2Inventories oranother applicable Standard.14[Deleted]15The fair value measurement of a biological asset or agricultural produce may be facilitated by grouping biological assets or agricultural produce according tosignificant attributes;for example,by age or quality.An entity selects theattributes corresponding to the attributes used in the market as a basis forpricing.16Entities often enter into contracts to sell their biological assets or agricultural produce at a future date.Contract prices are not necessarily relevant inmeasuring fair value,because fair value reflects the current market conditionsin which market participant buyers and sellers would enter into a transaction.As a result,the fair value of a biological asset or agricultural produce is notadjusted because of the existence of a contract.In some cases,a contract for thesale of a biological asset or agricultural produce may be an onerous contract,asdefined in IAS37Provisions,Contingent Liabilities and Contingent Assets.IAS37applies to onerous contracts.[Deleted]17–2122An entity does not include any cash flows for financing the assets,taxation,or re-establishing biological assets after harvest(for example,the cost of replantingtrees in a plantation forest after harvest).23[Deleted]24Cost may sometimes approximate fair value,particularly when:(a)little biological transformation has taken place since initial costincurrence(for example,for fruit tree seedlings planted immediatelyprior to the end of a reporting period);or(b)the impact of the biological transformation on price is not expected to bematerial(for example,for the initial growth in a30-year pine plantationproduction cycle).25Biological assets are often physically attached to land(for example,trees in a plantation forest).There may be no separate market for biological assets that areattached to the land but an active market may exist for the combined assets,thatis,the biological assets,raw land,and land improvements,as a package.An entity may use information regarding the combined assets to measure thefair value of the biological assets.For example,the fair value of raw land andland improvements may be deducted from the fair value of the combined assetsto arrive at the fair value of biological assets.IFRS Foundation A1229IAS41Gains and losses26A gain or loss arising on initial recognition of a biological asset at fair value less costs to sell and from a change in fair value less costs to sell ofa biological asset shall be included in profit or loss for the period inwhich it arises.27A loss may arise on initial recognition of a biological asset,because costs to sell are deducted in determining fair value less costs to sell of a biological asset.Again may arise on initial recognition of a biological asset,such as when a calf isborn.28A gain or loss arising on initial recognition of agricultural produce at fair value less costs to sell shall be included in profit or loss for the period inwhich it arises.29A gain or loss may arise on initial recognition of agricultural produce as a result of harvesting.Inability to measure fair value reliably30There is a presumption that fair value can be measured reliably for a biological asset.However,that presumption can be rebutted only oninitial recognition for a biological asset for which quoted market pricesare not available and for which alternative fair value measurements aredetermined to be clearly unreliable.In such a case,that biological assetshall be measured at its cost less any accumulated depreciation and anyaccumulated impairment losses.Once the fair value of such a biologicalasset becomes reliably measurable,an entity shall measure it at its fairvalue less costs to sell.Once a non-current biological asset meets thecriteria to be classified as held for sale(or is included in a disposal groupthat is classified as held for sale)in accordance with IFRS5Non-currentAssets Held for Sale and Discontinued Operations,it is presumed that fairvalue can be measured reliably.31The presumption in paragraph30can be rebutted only on initial recognition.An entity that has previously measured a biological asset at its fair value lesscosts to sell continues to measure the biological asset at its fair value less costs tosell until disposal.32In all cases,an entity measures agricultural produce at the point of harvest at its fair value less costs to sell.This Standard reflects the view that the fair value ofagricultural produce at the point of harvest can always be measured reliably.33In determining cost,accumulated depreciation and accumulated impairment losses,an entity considers IAS2,IAS16and IAS36Impairment of Assets.Government grants34An unconditional government grant related to a biological asset measured at its fair value less costs to sell shall be recognised in profit orloss when,and only when,the government grant becomes receivable.A1230IFRS FoundationIAS4135If a government grant related to a biological asset measured at its fair value less costs to sell is conditional,including when a government grantrequires an entity not to engage in specified agricultural activity,anentity shall recognise the government grant in profit or loss when,andonly when,the conditions attaching to the government grant are met.36Terms and conditions of government grants vary.For example,a grant may require an entity to farm in a particular location for five years and require theentity to return all of the grant if it farms for a period shorter than five years.Inthis case,the grant is not recognised in profit or loss until the five years havepassed.However,if the terms of the grant allow part of it to be retainedaccording to the time that has elapsed,the entity recognises that part in profitor loss as time passes.37If a government grant relates to a biological asset measured at its cost less any accumulated depreciation and any accumulated impairment losses(see paragraph30),IAS20is applied.38This Standard requires a different treatment from IAS20,if a government grant relates to a biological asset measured at its fair value less costs to sell or agovernment grant requires an entity not to engage in specified agriculturalactivity.IAS20is applied only to a government grant related to a biologicalasset measured at its cost less any accumulated depreciation and anyaccumulated impairment losses.Disclosure39[Deleted]General40An entity shall disclose the aggregate gain or loss arising during the current period on initial recognition of biological assets and agriculturalproduce and from the change in fair value less costs to sell of biologicalassets.41An entity shall provide a description of each group of biological assets.42The disclosure required by paragraph41may take the form of a narrative or quantified description.43An entity is encouraged to provide a quantified description of each group of biological assets,distinguishing between consumable and bearer biologicalassets or between mature and immature biological assets,as appropriate.Forexample,an entity may disclose the carrying amounts of consumable biologicalassets and bearer biological assets by group.An entity may further divide thosecarrying amounts between mature and immature assets.These distinctionsprovide information that may be helpful in assessing the timing of future cashflows.An entity discloses the basis for making any such distinctions.44Consumable biological assets are those that are to be harvested as agricultural produce or sold as biological assets.Examples of consumable biological assetsare livestock intended for the production of meat,livestock held for sale,fish infarms,crops such as maize and wheat,and trees being grown for lumber.BearerIFRS Foundation A1231IAS41biological assets are those other than consumable biological assets;for example,livestock from which milk is produced,grape vines,fruit trees,and trees fromwhich firewood is harvested while the tree remains.Bearer biological assets arenot agricultural produce but,rather,are self-regenerating.45Biological assets may be classified either as mature biological assets or immature biological assets.Mature biological assets are those that have attainedharvestable specifications(for consumable biological assets)or are able tosustain regular harvests(for bearer biological assets).46If not disclosed elsewhere in information published with the financial statements,an entity shall describe:(a)the nature of its activities involving each group of biologicalassets;and(b)non-financial measures or estimates of the physical quantities of:(i)each group of the entity’s biological assets at the end of theperiod;and(ii)output of agricultural produce during the period.47–48[Deleted]49An entity shall disclose:(a)the existence and carrying amounts of biological assets whose title isrestricted,and the carrying amounts of biological assets pledged assecurity for liabilities;(b)the amount of commitments for the development or acquisition ofbiological assets;and(c)financial risk management strategies related to agriculturalactivity.50An entity shall present a reconciliation of changes in the carrying amount of biological assets between the beginning and the end of thecurrent period.The reconciliation shall include:(a)the gain or loss arising from changes in fair value less costs to sell;(b)increases due to purchases;(c)decreases attributable to sales and biological assets classified asheld for sale(or included in a disposal group that is classified as heldfor sale)in accordance with IFRS5;(d)decreases due to harvest;(e)increases resulting from business combinations;(f)net exchange differences arising on the translation of financialstatements into a different presentation currency,and on thetranslation of a foreign operation into the presentation currencyof the reporting entity;and(g)other changes.A1232IFRS FoundationIAS4151The fair value less costs to sell of a biological asset can change due to both physical changes and price changes in the market.Separate disclosure ofphysical and price changes is useful in appraising current period performanceand future prospects,particularly when there is a production cycle of more thanone year.In such cases,an entity is encouraged to disclose,by group orotherwise,the amount of change in fair value less costs to sell included in profitor loss due to physical changes and due to price changes.This information isgenerally less useful when the production cycle is less than one year(forexample,when raising chickens or growing cereal crops).52Biological transformation results in a number of types of physical change—growth,degeneration,production,and procreation,each of which isobservable and measurable.Each of those physical changes has a directrelationship to future economic benefits.A change in fair value of a biologicalasset due to harvesting is also a physical change.53Agricultural activity is often exposed to climatic,disease and other natural risks.If an event occurs that gives rise to a material item of income or expense,thenature and amount of that item are disclosed in accordance with IAS1Presentation of Financial Statements.Examples of such an event include an outbreakof a virulent disease,a flood,a severe drought or frost,and a plague of insects.Additional disclosures for biological assets where fairvalue cannot be measured reliably54If an entity measures biological assets at their cost less any accumulated depreciation and any accumulated impairment losses(see paragraph30)at the end of the period,the entity shall disclose for such biologicalassets:(a)a description of the biological assets;(b)an explanation of why fair value cannot be measured reliably;(c)if possible,the range of estimates within which fair value is highlylikely to lie;(d)the depreciation method used;(e)the useful lives or the depreciation rates used;and(f)the gross carrying amount and the accumulated depreciation(aggregated with accumulated impairment losses)at thebeginning and end of the period.55If,during the current period,an entity measures biological assets at their cost less any accumulated depreciation and any accumulated impairmentlosses(see paragraph30),an entity shall disclose any gain or lossrecognised on disposal of such biological assets and the reconciliationrequired by paragraph50shall disclose amounts related to suchbiological assets separately.In addition,the reconciliation shall includethe following amounts included in profit or loss related to thosebiological assets:(a)impairment losses;IFRS Foundation A1233IAS41(b)reversals of impairment losses;and(c)depreciation.56If the fair value of biological assets previously measured at their cost less any accumulated depreciation and any accumulated impairment lossesbecomes reliably measurable during the current period,an entity shalldisclose for those biological assets:(a)a description of the biological assets;(b)an explanation of why fair value has become reliably measurable;and(c)the effect of the change.Government grants57An entity shall disclose the following related to agricultural activity covered by this Standard:(a)the nature and extent of government grants recognised in thefinancial statements;(b)unfulfilled conditions and other contingencies attaching togovernment grants;and(c)significant decreases expected in the level of government grants. Effective date and transition58This Standard becomes operative for annual financial statements covering periods beginning on or after1January2003.Earlier application is encouraged.If an entity applies this Standard for periods beginning before1January2003,itshall disclose that fact.59This Standard does not establish any specific transitional provisions.The adoption of this Standard is accounted for in accordance with IAS8Accounting Policies,Changes in Accounting Estimates and Errors.60Paragraphs5,6,17,20and21were amended and paragraph14deleted by Improvements to IFRSs issued in May2008.An entity shall apply thoseamendments prospectively for annual periods beginning on or after1January2009.Earlier application is permitted.If an entity applies the amendments foran earlier period it shall disclose that fact.61IFRS13,issued in May2011,amended paragraphs8,15,16,25and30and deleted paragraphs9,17–21,23,47and48.An entity shall apply thoseamendments when it applies IFRS13.A1234IFRS Foundation。

Comparison of Hong Kong Accounting Standards with International Accounting Standards (IASs)/ International Financial Reporting Standards (IFRSs)for the June 2006 examinationsHKG document TitleINTdocumentTitleExaminablePaper(s)Preface to Hong Kong Financial Reporting Standards 1.1, 2.5, 2.6, 3.13.6Framework for the Preparation and Presentation of Financial Statements Framework for the Preparation and Presentation of Financial Statements 1.1 (Note 5), 2.5,2.6,3.1, 3.6HKAS 1 Presentation of Financial Statements IAS 1Presentation of Financial Statements 1.1, 2.5, 2.6, 3.1, 3.6HKAS 1 Amendment Capital Disclosures 1.1, 2.5, 2.6, 3.1,3.6HKAS 2 Inventories IAS 2 Inventories 1.1, 2.5, 2.6, 3.1,3.6HKAS 7 Cash Flow Statements IAS 7 Cash Flow Statements 1.1 (Note 1), 2.5(Note 1), 2.6, 3.1,3.6HKAS 8 Accounting Policies, Changes in Accounting Estimates and Errors IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors 1.1, 2.5, 2.6, 3.1,3.6HKAS 10 Events After the Balance Sheet Date IAS 10Events After the Balance Sheet Date 1.1, 2.5, 2.6, 3.1, 3.6HKAS 11 Construction Contracts IAS 11 Construction Contracts 2.5, 2.6, 3.1, 3.6 HKAS 12 Income Taxes IAS 12 Income Taxes 2.5, 2.6, 3.1, 3.6 HKAS 14 Segment Reporting IAS 14 Segment Reporting 2.5, 2.6, 3.1, 3.6HKAS 16 Property, Plant and EquipmentIAS 16 Property, Plant and Equipment 1.1, 2.5, 2.6, 3.1, 3.6HKAS 17 Leases IAS 17 Leases 2.5, 2.6, 3.1, 3.6HKAS 18 RevenueIAS 18 Revenue 1.1, 2.5, 2.6, 3.1,3.6HKAS 19 Employee Benefits IAS 19 Employee Benefits 3.6HKAS19 Amendment Employee Benefits – Actuarial Gains and Losses, Group Plans andDisclosures3.6HKAS 20 Accounting for Government Grants and Disclosure of Government Assistance IAS 20Accounting for Government Grants and Disclosure of GovernmentAssistance2.5, 2.6,3.1, 3.6HKAS 21 The Effects of Changes in Foreign Exchange Rates IAS 21 The Effects of Changes in Foreign Exchange Rates 3.6HKAS 23 Borrowing Costs IAS 23 Borrowing Costs 2.5, 2.6, 3.1, 3.6 HKAS 24 Related Party Disclosures IAS 24 Related Party Disclosures 2.5, 2.6, 3.1, 3.6 HKAS 27 Consolidated and Separate Financial Statements IAS 27 Consolidated and Separate Financial Statements 2.5, 2.6, 3.1, 3.6HKAS 28 Investments in AssociatesIAS 28 Investments in Associates2.5, 2.6,3.1, 3.6HKAS 29 Financial Reporting in Hyperinflationary Economies IAS 29 Financial Reporting in Hyperinflationary Economies 3.6HKAS 31 Investments in Joint Ventures IAS 31 Interests in Joint Ventures 2.5, 2.6, 3.1, 3.6 HKAS 32 Financial Instruments: Disclosure and Presentation IAS 32 Financial Instruments: Disclosure and Presentation 2.5, 2.6, 3.1, 3.6 HKAS 33 Earnings per Share IAS 33 Earnings per Share 2.5, 2.6, 3.1, 3.6HKAS 34 Interim Financial Reporting IAS 34 Interim Financial Reporting 3.6HKAS 36 Impairment of Assets IAS 36 Impairment of Assets 2.5, 2.6, 3.1, 3.6HKAS 37 Provisions, Contingent Liabilities and Contingent Assets IAS 37 Provisions, Contingent Liabilities and Contingent Assets 1.1 (Note 2), 2.5,2.6,3.1, 3.6HKAS 38 Intangible Assets IAS 38 Intangible Assets 1.1 (Note 3), 2.5,2.6,3.1, 3.6HKAS 39 Financial Instruments: Recognition and Measurement IAS 39 Financial Instruments: Recognition and Measurement 2.5, 2.6, 3.1, 3.6HKAS 39 Amendment Transition and Initial Recognition of Financial Assets and FinancialLiabilities2.5, 2.6,3.1 ,3.6HKAS 39AmendmentCash Flow Hedge Accounting of Forecast Intragroup Transactions 2.5, 2.6, 3.1 ,3.6 HKAS 39AmendmentThe Fair Value Option 2.5, 2.6, 3.1 ,3.6HKAS 39 & HKFRS 4 Amendment Financial Instruments: Recognition and Measurement and InsuranceContracts – Financial Guarantee Contracts2.5, 2.6,3.1 ,3.6(HKFRS 4 Amend3.6 only)HKAS 40 Investment Property IAS 40 Investment Property 2.5, 2.6, 3.1, 3.6HKAS 41 Agriculture IAS 41 Agriculture 3.6 HKFRS 1 First-time adoption of Hong Kong Financial Reporting Standards IFRS 1 First –time adoption of International Financial Reporting Standards 2.5, 2.6, 3.1, 3.6HKFRS 1 & 6 Amendment First-time Adoption of Hong Kong Financial Reporting Standards andExploration for and Evaluation of Mineral Resources2.5, 2.6,3.1, 3.6(HKFRS 6 Amend3.6 only)HKFRS 2 Share-based Payment IFRS 2 Share-based Payment 3.6HKFRS 3 Business Combinations IFRS 3 Business Combinations 1.1 (Note 6), 2.5,2.6,3.1, 3.6 HKFRS 4 Insurance Contracts IFRS 4 Insurance Contracts 3.6HKFRS 5 Non-current Assets Held for Sale and Discontinued Operations IFRS 5 Non-current Assets Held for Sale and Discontinued Operations 1.1 (Note 4), 2.5,2.6,3.1, 3.6 HKFRS 7 Financial Instruments: Disclosures IFRS 7 Financial Instruments: Disclosures 2.5, 2.6, 3.1, 3.6 HKFRS 6 Exploration for and Evaluation of Mineral Resources IFRS 6 Exploration for and Evaluation of Mineral Resources 3.6HK-INT 3 Revenue – Pre Completion Contracts for the Sale of DevelopmentProperties2.5, 2.6,3.1, 3.6 HK-INT 4 Leases – Determination of The Length of Lease Term in respect of HongKong Land Leases2.5, 2.6,3.1, 3.6 HKAS-INT 10 Government Assistance – No Specific Relation to Operating Activites SIC 10 Government assistance – No specific relation to operating activities 2.5, 2.6, 3.1, 3.6 HKAS-Int 12 Consolidation – Special Purpose Entities SIC 12 Consolidation – Special Purpose Entities 3.6HKAS-Int 12 Amendment Scope of HKAS-Int 12 Consolidation – Special Purpose Entities3.6HKAS-Int 13 Jointly Controlled Entities – Non-Monetary Contributions by Venturers SIC 13 Jointly Controlled Entities – Non-Monetary Contributions by Venturers 3.6 HKAS-Int 15 Operating Leases – Incentives SIC 15 Operating Leases – Incentives 3.6 HKAS-Int 21 Income Taxes – Recovery of Revalued Non-Depreciable Assets SIC 21 Income Taxes – Recovery of Revalued Non-Depreciable Assets 3.6HKAS-Int 25 Income Taxes – Changes in the Tax Status of an Enterprise or Its Shareholders SIC 25 Income Taxes – Changes in the Tax Status of an Enterprise or ItsShareholders3.6HKAS-Int 27 Evaluating the Substance of Transactions Involving the Legal Form of a Lease SIC 27 Evaluating the Substance of Transactions In the Legal Form of a Lease3.6HKAS-Int 29 Disclosure – Service Concession Arrangements SIC 29 Disclosure – Service Concession Arrangements 3.6HKAS-Int 31 Revenue – Barter Transactions Involving Advertising Services SIC 31 Revenue – Barter Transactions Involving Advertising Services 3.6HKAS-Int 32 Intangible Assets – Web Site Costs SIC 32 Intangible Assets – Web Site Costs 3.6HKFRS-Int 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities IFRIC 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities 3.6HKFRS-Int 4 Determining Whether an Arrangement contains a Lease IFRIC 4 Determining Whether an Arrangement contains a Lease 2.5, 2.6, 3.1, 3.6HKFRS-Int 5 Rights to Interests arising from Decommissioning, Restoration and Environmental Rehabilitation Funds IFRIC 5 Rights to Interests arising from Decommissioning, Restoration andEnvironmental Funds3.6 IFRIC 7 Applying the Restatement Approach under IAS 29, Financial Reporting in Hyperinflationary Economies3.6 DP Preliminary Views on Accounting Standards for Small and Medium-sized Entities3.6 ED Proposed Amendment to IFRS 3, Business Combinations 3.6 ED Proposed Amendment to IAS 27, Consolidated and Separate FinancialStatements3.6 ED Proposed Amendment to IAS 37, Provisions, Contingent Liabilities andContingent Assets3.6 DP Measurement Bases for Financial Reporting – Measurement on InitialRecognition3.6 DP Management Commentary 3.6Notes1. Cash flow statements are examinable for 1.1 and2.5 but excluding group cash flow statements and cash flow statements including foreign currency.2. Examinable for 1.1 only to the extent of candidates providing definitions and simple calculations.3. Examinable for 1.1 only to cover basic knowledge of Research and Development and Goodwill.4. Examinable for 1.1 only to cover disclosures in relation to Discontinuing Operations.5. The Framework for the preparation of financial statements is examinable for 1.1 at an introductory level only.6. Examinable for 1.1 only to cover basic consolidation.。

国外行政决策体制的特点及借鉴

王春香

【期刊名称】《大连干部学刊》

【年(卷),期】2007(023)002

【摘要】欧美发达国家对行政决策体制非常重视,不仅在理论方面成果丰硕,而且在实践方面也成绩斐然,值得我们借鉴.

【总页数】3页(P33-35)

【作者】王春香

【作者单位】中共盐城市委党校,江苏,盐城,224001

【正文语种】中文

【中图分类】D6

【相关文献】

1.当代西方公共行政决策体制及其借鉴价值 [J], 宋世明;王思武

2.行政审查制度:行政纠纷非诉解决的新方式——以国外实践经验为借鉴 [J], 冯勇

3.浅析高校"行政化"问题的解决——国外高校管理改革和发展趋势与解决行政权力和学术权力冲突的借鉴 [J], 张慧

4.借鉴国外依法行政经验完善我国依法行政体系 [J], 安增娟

5.试论我国行政信访权利救济功能的完善——对国外议会行政监察专员制度的考察与借鉴 [J], 杨建锋

因版权原因,仅展示原文概要,查看原文内容请购买。

/中华会计网校会计人的网上家园IAS 20政府补助ACCA P2 考试:IAS 20 Government GrantsIAS 20 Accounting for Government Grants and Disclosure of Government Assistance considers the accounting treatment for government grants that are income-based grants and asset based. This section only considers the issues relating to asset-based grants.Accounting TreatmentThe standard allows two possible methods of accounting for asset-based grants.Present as Deferred IncomeThe grant will be presented as deferred income in the statement of finan cia l position. Deferred income is included in the liability section of the statement of financial position, split between non-current and current elements.The deferred income will be credited to profits over the life of the related asset, in the same manner in which that asset is depreciated.Deduct From Cost of AssetThe other option is to deduct the grant from the cost of the asset.The effect on profits will be the same as the previous method due to the fact that the charge for depreciation will now be based on the net cost of the asset.Granted AssetSome intangible assets may be acquired free of charge, or for nominal consideration, by way of a government grant (e.g. airport landing rights, licences to operate radio or television stations, import quotas, rights to emit pollution).Under IAS 20, both the intangible asset (debit entry) and the grant (credit entry) may be recorded initially at either fair value or cost (which may be zero).。

MEMBERS' HANDBOOKCONTENTS OF VOLUME II(Updated to May 2017)Issue/(Reviewdate) PREFACE AND FRAMEWORKPREFACE Preface to Hong Kong Financial Reporting Standards .....................................10/06(4/15)CONCEPTUALFRAMEWORKConceptual Framework for Financial Reporting ................................................10/10HONG KONG ACCOUNTING STANDARDS (HKAS)HKAS 1RevisedPresentation of Financial Statements................................................................12/07(1/17) HKAS 2 Inventories .........................................................................................................3/04(2/14) HKAS 7 Statement of Cash Flows ..................................................................................12/04(6/16) HKAS 8 Accounting Policies, Changes in Accounting Estimates and Errors .................9/04(2/14) HKAS 10 Events after the Reporting Period .....................................................................3/04(2/14) HKAS 11 Construction Contracts ......................................................................................12/04(3/10) HKAS 12 Income Taxes ....................................................................................................11/04(6/16) HKAS 16 Property, Plant and Equipment .........................................................................11/05(1/17) HKAS 17 Leases ...............................................................................................................12/04(1/17) HKAS 18 Revenue ............................................................................................................11/04(5/14) HKAS 19(2011)Employee Benefits.............................................................................................7/11(12/16)HKAS 20 Accounting for Government Grants and Disclosure of GovernmentAssistance ...................................................................................................12/04(2/14) HKAS 21 The Effects of Changes in Foreign Exchange Rates ........................................3/04(5/14) HKAS 23RevisedBorrowing Cost……………………………….......................................................6/07(1/17)HKAS 24RevisedRelated Party Disclosures .................................................................................11/09 (11/16) HKAS 26 Accounting and Reporting by Retirement Benefit Plans ...................................8/04HKAS 27(2011)Separate Financial Statements .........................................................................6/11(1/17)HKAS 28 (2011) Investments in Associates and Joint Ventures ..................................................6/11(1/17)HKAS 29 Financial Reporting in Hyperinflationary Economies .....................................3/04(4/10) HKAS 32 Financial Instruments: Presentation ...............................................................11/04(11/14) HKAS 33 Earnings per Share ........................................................................................3/04(5/14) HKAS 34 Interim Financial Reporting ............................................................................10/04(12/16) HKAS 36 Impairment of Assets .....................................................................................8/04(1/17) HKAS 37 Provisions, Contingent Liabilities and Contingent Assets ..............................11/04(11/16) HKAS 38 Intangible Assets ............................................................................................8/04(1/17) HKAS 39 Financial Instruments: Recognition and Measurement ..................................1/06(11/16) HKAS 40 Investment Property .......................................................................................11/05(4/17) HKAS 41 Agriculture ......................................................................................................12/04(1/17)HONG KONG FINANCIAL REPORTING STANDARDS (HKFRS)First-time Adoption of Hong Kong Financial Reporting Standards ...............12/08(1/17) HKFRS 1RevisedHKFRS 2 Share-based Payment ...................................................................................4/04(11/16) HKFRS 3Business Combinations ..................................................................................3/08(11/16) RevisedHKFRS 4 Insurance Contracts .......................................................................................3/06(01/17) HKFRS 5 Non-current Assets Held for Sale and Discontinued Operations ...................8/04(12/16) HKFRS 6 Exploration for and Evaluation of Mineral Resources ....................................2/05(2/10) HKFRS 7 Financial Instruments: Disclosures ................................................................9/05(12/16) HKFRS 8 Operating Segments .....................................................................................3/07(12/16) HKFRS 9 Financial Instruments .....................................................................................11/09 (09/14) HKFRS 9 Financial Instruments (Hedge Accounting) ...................................................12/13 Financial Instruments .....................................................................................09/14 HKFRS 9(2014)HKFRS 10 Consolidated Financial Statements ...............................................................6/11(1/17) HKFRS 11 Joint Arrangements ........................................................................................6/11(12/16) HKFRS 12 Disclosure of Interests in Other Entities .........................................................6/11(1/17) HKFRS 13 Fair Value Measurement ................................................................................6/11(11/16) HKFRS 14 Regulatory Deferral Accounts ........................................................................2/14(1/17) HKFRS 15 Revenue from Contracts with Customers ......................................................7/14(6/16) HKFRS 16 Leases ............................................................................................................5/16 Annual Improvements to HKFRSs 2014-2016 Cycle.....................................3/17 ANNUALIMPROVEMENTSHONG KONG (IFRIC) INTERPRETATIONS (HK(IFRIC)-Int)HK(IFRIC)-Int 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities ......8/04(7/10) HK(IFRIC)-Int 2 Members’ Shares in Co-operative Entities and Similar Instruments .................2/05(2/14) HK(IFRIC)-Int 4 Determining whether an Arrangement contains a Lease ..................................2/05(2/14) HK(IFRIC)-Int 5 Rights to Interests arising from Decommissioning, Restoration andEnvironmental Rehabilitation Funds ............................................................2/05(2/14) HK(IFRIC)-Int 6 Liabilities arising from Participating in a Specific Market – WasteElectrical and Electronic Equipment .............................................................9/05 HK(IFRIC)-Int 7 Applying the Restatement Approach under HKAS 29 Financial Reportingin Hyperinflationary Economies...................................................................1/06(7/10) HK(IFRIC)-Int 9 Reassessment of Embedded Derivatives .........................................................5/06(2/14) HK(IFRIC)-Int 10 Interim Financial Reporting and Impairment ....................................................9/06(7/12) HK(IFRIC)-Int 12 Service Concession Arrangements ...................................................................3/07(1/17) HK(IFRIC)-Int 13 Customer Loyalty Programmes .........................................................................9/07(2/14) HK(IFRIC)-Int 14 HKAS 19 —The Limit on a Defined Benefit Asset, Minimum Funding9/07(11/16) Requirements and their Interaction ..............................................................HK(IFRIC)-Int 15 Agreements for the Construction of Real Estate ...............................................8/08(8/10) HK(IFRIC)-Int 16 Hedges of a Net Investment in a Foreign Operation .........................................8/08(5/14) HK(IFRIC)-Int 17 Distributions of Non-cash Assets to Owners .....................................................12/08(5/14) HK(IFRIC)-Int 18 Transfers of Assets from Customers .................................................................2/09(8/10) HK(IFRIC)-Int 19 Extinguishing Financial Liabilities with Equity Instruments ...............................12/09(5/14) HK(IFRIC)-Int 20 Stripping Costs in the Production Phase of a Surface Mine 11/11 HK(IFRIC)-Int 21 Levies 6/13 HONG KONG INTERPRETATIONS (HK-Int)*HK-Int 4 Leases – Determination of the Length of Lease Term in respect of HongKong Land Leases .......................................................................................6/06 (12/09) HK-Int 5 Presentation of Financial Statements – Classification by the Borrower ofa Term Loan that Contains a Repayment on Demand Clause ....................11/10Note: * With effect from 24 May 2005, all Interpretations that are developed locally by the Institute are named Hong Kong Interpretations.HONG KONG (SIC) INTERPRETATIONS (HK(SIC)-Int)HK(SIC)-Int 10 Government Assistance – No Specific Relation to Operating Activities ..........12/04(8/10) HK(SIC)-Int 15 Operating Leases – Incentives .........................................................................12/04(9/10) HK(SIC)-Int 25 Income Taxes – Changes in the Tax Status of an Enterprise or itsShareholders ................................................................................................12/04(8/10) HK(SIC)-Int 27 Evaluating the Substance of Transactions Involving the Legal Form of aLease ............................................................................................................12/04(9/10)HK(SIC)-Int 29 Service Concession Arrangements: Disclosures ..............................................12/04(8/10) HK(SIC)-Int 31 Revenue – Barter Transactions Involving Advertising Services .......................12/04(5/14) HK(SIC)-Int 32 Intangible Assets – Web Site Costs ..................................................................12/04(5/14)GLOSSARY Glossary of Terms Relating to Hong Kong Financial Reporting Standards ......... 3/08(11/14) HONG KONG FINANCIAL REPORTING STANDARD FOR PRIVATEENTITIES (HKFRS-PE)HKFRS-PE HONG KONG FINANCIAL REPORTING STANDARD FORPRIVATE ENTITIES ................................................................................. 4/10 (9/15)HKFRS-PE (Revised) HONG KONG FINANCIAL REPORTING STANDARD FORPRIVATE ENTITIES (REVISED) ........................................................... 5/17 SMALL AND MEDIUM-SIZED ENTITY FINANCIAL REPORTING FRAMEWORKAND FINANCIAL REPORTING STANDARD (SME-FRF & SME-FRS)SME-FRF &SME-FRSSME-FRF & SME-FRF .................................................................................... 8/05 (2/11)SME-FRF &SME-FRS(Revised)SME-FRF & SME-FRF (Revised)..................................................................... 3/14(12/15)ACCOUNTING GUIDELINES (AG)AG 1 Preparation and Presentation of Accounts from Incomplete Records ..............3/84AG 5 Merger Accounting for Common Control Combinations ...................................05/11 (11/13) AG 7 Preparation of Pro Forma Financial Information for Inclusion inInvestment Circulars.....................................................................................3/06ACCOUNTING BULLETINS (AB)AB 3 Guidance on Disclosure of Directors’ Remuneration ........................................1/00AB 4 Guidance on the Determination of Realised Profits and Losses in theContext of Distributions under the Hong Kong Companies Ordinance........5/10AB 5 Guidance for the Preparation of a Business Review under the Hong KongCompanies Ordinance Cap. 622..................................................................7/14AB 6 Guidance on the Requirements of Section 436 of the Hong KongCompanies Ordinance Cap. 622..................................................................6/15。