intermediate-accounting课后习题(8)

- 格式:pdf

- 大小:20.02 MB

- 文档页数:79

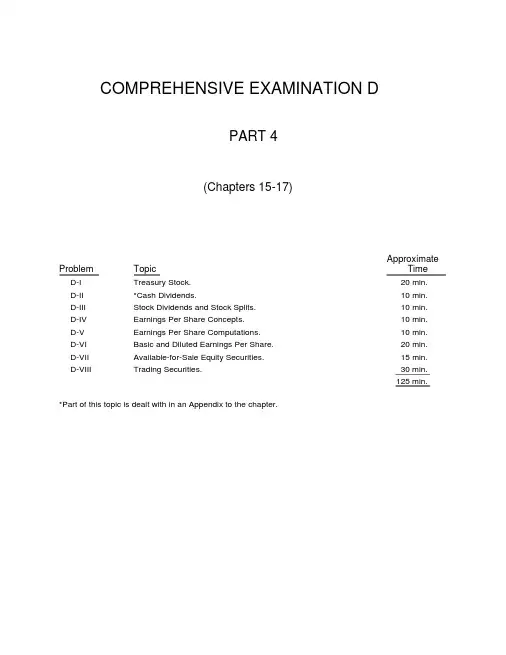

COMPREHENSIVE EXAMINATION DPART 4(Chapters 15-17)Approximate Problem Topic Time D-I Treasury Stock. 20 min.D-II *Cash Dividends. 10 min.D-III Stock Dividends and Stock Splits. 10 min.D-IV Earnings Per Share Concepts. 10 min.D-V Earnings Per Share Computations. 10 min.D-VI Basic and Diluted Earnings Per Share. 20 min.D-VII Available-for-Sale Equity Securities. 15 min.D-VIII Trading Securities. 30 min.125 min.*Part of this topic is dealt with in an Appendix to the chapter.D - 2Test Bank for Intermediate Accounting, Fifteenth EditionProblem D-I— Treasury StockThe stockholders' equity section of Carey Co.'s balance sheet at December 31, 2014, was as follows:Common stock--$10 par (authorized 1,000,000 shares,issued and outstanding 600,000 shares) $ 6,000,000 Paid-in capital in excess of par 1,500,000Retained earnings 3,250,000$10,750,000InstructionsPrepare journal entries (1, 2, and 4) and show proper disclosure (3) to reflect the following treasury stock transactions showing how each is accounted for under the cost method. (Show computations.)1. On January 4, 2015, having idle cash, Carey Co. repurchased 25,000 shares of its out-standing stock for $500,000.2. On March 4, Carey sold 5,000 of these reacquired shares at $24 per share.3. Show the proper disclosures in the stockholders' equity section of the balance sheet issued atthe end of the first quarter, March 31, 2015. Assume net income of $100,000 during the firstquarter.4. On June 30, 2015 the firm sold 10,000 of the reacquired shares for $17 per share.*Problem D-II— Cash DividendsBell Company has stock outstanding as follows: Common, $10 par value per share, 140,000 shares; Preferred, 4%; $100 par value per share, 8,000 shares. The Preferred is cumulative and participating up to an additional 3% of par; two years are in arrears (not including the current year); and the total amount of cash dividends declared for both classes of stock is $192,000.InstructionsPrepare the entry for the dividend declaration, separating the dividend into the common and preferred portions.Comprehensive Examination D D - 3 Problem D-III— Stock Dividends and Stock SplitsStock dividends and stock splits are common forms of corporate stock distribution to stockholders. Consider each of the numbered statements. You are to decide whether it:A. Applies to both stock dividends and stock splits.B. Applies to neither.C. Applies to stock splits only.D. Applies to stock dividends only.E. Applies to stock splits effected in the form of a dividend only.F. Applies to both stock splits effected in the form of a dividend and a stock dividend.(In each instance, the issuing company has only one class of stock.)InstructionsPrint next to the number of each statement below, the single capital letter of the description whichapplies to the statement.Statements____ 1. The distribution is a multiple as contrasted to a fraction of the number of shares previously outstanding.____ 2. The total number of shares outstanding is increased.____ 3. The individual stockholder's share of net assets is increased.____ 4. There is no transfer between retained earnings and capital stock accounts, other than to the extent occasioned by legal requirements.____ 5. There is no change in the total stockholders' equity of the issuing corporation.____ 6. The retained earnings available for dividends are increased.____ 7. Retained earnings in the amount of the distribution are transferred to capital stock, in some instances in an amount in excess of that required by the laws of the state ofincorporation.____ 8. Subsequent per-share earnings, if any, are decreased.____ 9. The par (or stated value) of the stock is unchanged.D - 4Test Bank for Intermediate Accounting, Fifteenth EditionProblem D-IV— Earnings Per Share ConceptsIndicate which of the following securities would be included in the computation of "basic earningsper share," and which would be included in the computation of "diluted earnings per share." Placea "B" before those which affect only basic EPS, a "D" before those which affect only diluted EPS,a "BD" before those which affect both basic and diluted EPS, and an "N" before those securitieswhich do not affect EPS computations. Assume that, where applicable, the appropriate securitiesare dilutive.____ 1. Warrants to purchase additional common shares.____ 2. Common stock.____ 3. Nonconvertible debenture bonds.____ 4. Convertible, noncumulative preferred stock.____ 5. Cumulative, nonconvertible preferred stock.____ 6. Convertible bonds.____ 7. Executive stock options.____ 8. Notes payable.Problem D-V— Earnings Per Share ComputationsJones, Inc. has net income (30% tax rate) of $1,400,000 for 2015, and an average number of shares outstanding during the year of 500,000 shares. The corporation issued $2,000,000 par value of 10-year, 9% convertible bonds on January 1, 2013 at a $180,000 discount. The convertible bonds are convertible into 70,000 shares of common stock. Assume the company uses the straight-line method for amortizing bond discount.InstructionsCompute the earnings per share data, excluding any notes if required.Comprehensive Examination D D - 5 Problem D-VI— Basic and Diluted Earnings Per ShareAssume that the following data relate to Rosen, Inc. for the year 2015:Net income (30% tax rate) $3,500,000Average common shares outstanding 2015 1,000,000 shares10% cumulative convertible preferred stock:Convertible into 80,000 shares of common $1,600,0008% convertible bonds; convertible into 75,000shares of common $2,500,000Stock options:Exercisable at the option price of $25 per share;average market price in 2015, $30 84,000 shares InstructionsCompute (a) basic earnings per share, and (b) diluted earnings per share.Problem D-VII—Available-for-Sale Equity InvestmentsOn January 2, 2014, Norwin Company purchased 2,000 shares of Oslo Company common stockfor $60,000. The stock has a par value of $10 and is part of the total stock outstanding of 20,000shares of Oslo Company. Norwin Company intends the stock to be available for sale. Total stockholders' equity of Oslo Company on January 2, 2014 was $600,000.InstructionsPrepare necessary journal entries on the books of Norwin Company for the following transactions.If no entry is required, write "none" in the space provided. (Round all calculations to the nearestcent.)(a) January 2, 2014: Norwin purchases the shares described above.(b) December 31, 2014: Norwin receives a $.75 per share dividend from Oslo, and Osloannounces a net income for 2014 of $250,000.(c) December 31, 2014: According to The Wall Street Journal, Oslo common is selling for $27per share. Norwin's management views this decline as being only temporary in nature.Oslo's common is Norwin's only available-for-sale security.(d) February 15, 2015: Norwin sells 1,000 of the shares purchased on January 2, 2014 at $32per share.D - 6Test Bank for Intermediate Accounting, Fifteenth EditionProblem D-VIII— Trading SecuritiesThe information below relates to Milton Company's trading securities in 2014 and 2015.(a) Prepare the journal entries for the following transactions.January 1, 2014 Purchased $400,000 par value of GLF Company bonds at 97 plus accruedinterest. The bonds pay interest annually at 9% each December 31.Broker's commission was $4,000.September 1, 2014 Sold $200,000 par value of GLF Company bonds at 94 plus accrued interest. Broker's commission, taxes, and fees were $2,000.September 5, 2014 Purchased 5,000 shares of Hayes, Inc. common stock for $30 per share.The broker's commission on the purchase amounted to $2,000.December 31, 2014 Make the appropriate entry for the GLF Company bonds.December 31, 2014 The market prices of the trading securities at December 31 were: Hayes,Inc. common stock, $31 per share; and GLF Company bonds, 99. Makethe appropriate entry.July 1, 2015 Milton sold 1/2 of the Hayes, Inc. common stock at $33 per share. Broker'scommissions, taxes, and fees were $1,000.December 1, 2015 Milton purchased 600 shares of Ramirez, Inc. common stock at $45 per share. Broker's commission was $500.December 31, 2015 Make the appropriate entry for the GLF Company bonds.December 31, 2015 The market prices of the trading securities at December 31 were: Hayes,Inc. common stock, $34 per share; GLF Company bonds, 98; and Ramirez,Inc. common stock, $47 per share. Make the appropriate entry.(b) Present the financial statement disclosure (balance sheet and income statement) of MiltonCompany's transactions in trading securities for each of the years 2014 and 2015.Appropriate financial statement subheadings must be disclosed.Comprehensive Examination D D - 7 Solutions — Comprehensive Examination DProblem D-I— Solution.1. Treasury Stock .............................................................................. 500,000Cash .................................................................................. 500,000 2. Cash ............................................................................................. 120,000Treasury Stock .................................................................. 100,000Paid-in Capital from Treasury Stock ................................... 20,000 3. Stockholders' equity:Common stock, $10 par, 1,000,000 shares authorized,600,000 shares issued, 580,000 shares outstanding $ 6,000,000 Paid-in capital in excess of par value 1,500,000Paid-in capital from treasury stock 20,000Retained earnings 3,350,00010,870,000 Less: Cost of 20,000 shares held in treasury (400,000)Total stockholders' equity $10,470,0004. Cash ............................................................................................. 170,000Paid-in Capital from Treasury Stock .............................................. 20,000Retained Earnings ......................................................................... 10,000Treasury Stock .................................................................. 200,000*Problem D-II— Solution.Retained Earnings .............................................................................. 192,000 Dividends Payable, Preferred .................................................. 112,000Dividends Payable, Common .................................................. 80,000 Computations:Preferred Common Total Arrears—$800,000 × 4% × 2 $64,000 $ 64,000Preference—$800,000 × 4% 32,000 32,000Common—$1,400,000 × 4% $ 56,000 56,000Participating 2%* 16,000 24,000 40,000$112,000 $ 80,000 $192,000 * [($192,000 – $152,000) ÷($600,000 + $1,400,000)]Test Bank for Intermediate Accounting, Fifteenth EditionD - 8Problem D-III— Solution.1. C 4. E 7. F2. A 5. A 8. A3. B 6. B 9. FProblem D-IV— Solution.1. D 5. BD2. BD 6. D3. N 7. D4. D 8. NProblem D-V — Solution.Basic earnings per share($1,400,000 ÷500,000 shares) $2.80 Diluted earnings per share$1,400,000 + .7($180,000 + $18,000)—————————————————$2.70 500,000 + 70,000Problem D-VI — Solution.$3,500,000 – $160,000(a) Basic EPS = ——————————— = $2.231,500,000(b) Shares EarningsStart 1,500,000 $3,340,000Convertible preferred 80,000 160,000Convertible bonds 75,000 140,000*Options 14,000** 01,669,000 $3,640,000*($2,500,000 ×.08) ×(1 – .30)**[($30 – $25) ÷$30] ×84,000$3,640,000 ÷ 1,669,000 = $2.18 DEPSComprehensive Examination D D - 9Problem D-VII— Solution.(a) Equity Investments ..................................................................... 60,000Cash ............................................................................... 60,000(b) Cash .......................................................................................... 1,500Dividend Revenue .......................................................... 1,500 No entry to accrue investee profits because fair value, not equity, method is being used.(c) Unrealized Holding Gain or Loss—Equity ................................... 6,000Fair Value Adjustment (Available-for-Sale) ..................... 6,000(d) Cash (1,000 × $32) ..................................................................... 32,000Gain on Sale of Securities ............................................... 2,000$30) .................................... 30,000 Equity Investments (1,000 ×Problem D-VIII— Solution.January 1, 2014*.97) + $4,000 ....................................... 392,000Debt Investments ($400,000 ×Cash ........................................................................................ 392,000September 1, 2014Cash ($188,000 + $12,000 – $2,000) .................................................. 198,000Loss on Sale of Investments ............................................................... 10,000 Debt Investments .................................................................... 196,000Interest Revenue ..................................................................... 12,000September 5, 2014Equity Investments .............................................................................. 152,000 Cash ........................................................................................ 152,000December 31, 2014*Cash ($150,000 × .09) ......................................................................... 13,500 Interest Revenue ..................................................................... 13,500December 31, 2014Fair Value Adjustment (Trading) .......................................................... 5,000 Unrealized Holding Gain or Loss—Income ($348,000 – $353,000) 5,000D - 10Test Bank for Intermediate Accounting, Fifteenth EditionJuly 1, 2015Cash ($82,500 – $1,000) ..................................................................... 81,500 Gain on Sale of Investments .................................................... 5,500 Equity Investments .................................................................. 76,000December 1, 2015Equity Investments .............................................................................. 27,500 Cash ........................................................................................ 27,500December 31, 2015Cash .................................................................................................... 13,500 Interest Revenue ..................................................................... 13,500December 31, 2015Fair Value Adjustment (Trading) ........................................................... 14,200 Unrealized Holding Gain or Loss—Income ............................. 14,200 ($375,500 – $394,200) - $5,000December 31,Balance Sheet 2014 2015 Current assets:Equity Investments, at fair value $353,000 $394,200Income StatementOther revenue and gains:Interest Revenue $13,500 $13,500 Unrealized holding gain on trading securities 5,000 14,200 Gain on sale of securities 5,500 Other expenses and losses:Loss on sale of securities 10,000。

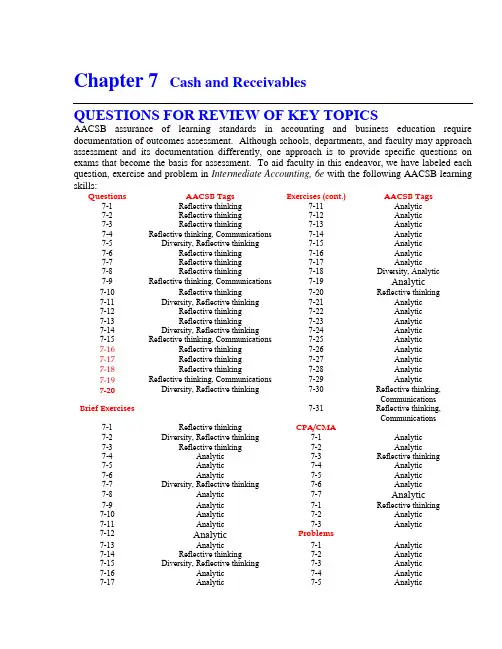

Chapter 7 Cash and ReceivablesQUESTIONS FOR REVIEW OF KEY TOPICSAACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach assessment and its documentation differently, one approach is to provide specific questions on exams that become the basis for assessment. To aid faculty in this endeavor, we have labeled each question, exercise and problem in Intermediate Accounting, 6e with the following AACSB learning skills:Questions AACSB Tags Exercises (cont.)AACSB Tags 7-1Reflective thinking 7-11Analytic7-2 Reflective thinking 7-12Analytic7-3Reflective thinking 7-13Analytic7-4Reflective thinking, Communications 7-14Analytic7-5Diversity, Reflective thinking 7-15Analytic7-6Reflective thinking 7-16Analytic7-7Reflective thinking 7-17Analytic7-8Reflective thinking 7-18Diversity, Analytic7-9Reflective thinking, Communications 7-19Analytic7-10Reflective thinking 7-20 Reflective thinking7-11Diversity, Reflective thinking 7-21Analytic7-12Reflective thinking 7-22Analytic7-13Reflective thinking 7-23Analytic7-14Diversity, Reflective thinking 7-24 Analytic7-15Reflective thinking, Communications 7-25Analytic7-16 Reflective thinking7-26Analytic7-17 Reflective thinking7-27 Analytic7-18 Reflective thinking7-28 Analytic7-19 Reflective thinking, Communications7-29 Analytic7-20 Diversity, Reflective thinking7-30 Reflective thinking,CommunicationsBrief Exercises 7-31 Reflective thinking,Communications 7-1Reflective thinking CPA/CMA7-2Diversity, Reflective thinking 7-1Analytic7-3Reflective thinking 7-2Analytic7-4 Analytic 7-3Reflective thinking7-5Analytic 7-4 Analytic7-6Analytic 7-5Analytic7-7Diversity, Reflective thinking 7-6Analytic7-8Analytic 7-7Analytic7-9Analytic 7-1Reflective thinking7-10Analytic 7-2Analytic7-11Analytic 7-3Analytic7-12Analytic Problems7-13 Analytic 7-1Analytic7-14Reflective thinking 7-2Analytic7-15 Diversity, Reflective thinking 7-3Analytic7-16 Analytic 7-4 Analytic7-17 Analytic 7-5 AnalyticExercises7-6 Analytic 7-1Analytic7-7Analytic 7-2Analytic 7-8Analytic 7-3 Diversity, Analytic 7-9 Diversity, Analytic 7-4Analytic 7-10Analytic 7-5Analytic 7-11Analytic 7-6 Analytic 7-12Analytic 7-7 Analytic 7-13Analytic 7-8Analytic 7-14Analytic 7-9Analytic 7-15 Analytic 7-10AnalyticQUESTIONS FOR REVIEW OF KEY TOPICSQuestion 7-1Cash equivalents usually include negotiable instruments as well as highly liquid investments that have a maturity date no longer than three months from date of purchase.Question 7-2Internal control procedures involving accounting functions are intended to improve the accuracy and reliability of accounting information and to safeguard the company’s assets. The separation of duties means that employees involved in recordkeeping should not also have physical responsibility for assets.Question 7-3Management must document the company’s internal controls and assess their adequacy. The auditors must provide an opinion on management’s assessment. The Public Company Accounting Oversight Board’s Auditing Standard No. 5, which supersedes Auditing Standard No. 2, further requires the auditor to express its own opinion on whether the company has maintained effective internal control over financial reporting.Question 7-4A compensating balance is an amount of cash a depositor (debtor) must leave on deposit in an account at a bank (creditor) as security for a loan or a commitment to lend. The classification and disclosure of a compensating balance depends on the nature of the restriction and the classification of the related debt. If the restriction is legally binding, then the cash will be classified as either current or noncurrent (investments and funds or other assets) depending on the classification of the related debt. In either case, note disclosure is appropriate. If the compensating balance arrangement is informal and no contractual agreement restricts the use of cash, note disclosure of the arrangement including amounts involved is appropriate. The compensating balance can be included in the cash and cash equivalents category of current assets.Question 7-5Yes, IFRS and U.S. GAAP differ in how bank overdrafts are treated. Under IFRS, overdrafts can be offset against other cash accounts. Under U.S. GAAP overdrafts must be treated as liabilities.Answers to Questions (continued)Question 7-6Trade discounts are reductions below a list price and are used to establish a final price for a transaction. The reduced price is the starting point for initial valuation of the transaction. A cash discount is a reduction, not in the selling price of a good or service, but in the amount to be paid by a credit customer if the receivable is paid within a specified period of time.Question 7-7The gross method of accounting for cash discounts considers discounts not taken as part of sales revenue. The net method considers discounts not taken as interest revenue, because they are viewed as compensation to the seller for allowing the buyer to defer payment.Question 7-8When returns are material and a company can make reasonable estimates of future returns, an allowance for sales returns is established. At a financial reporting date, this provides an estimate of the amount of future returns for prior sales, and involves a debit to sales returns and a credit to allowance for sales returns for the estimated amount. Allowance for sales returns is a contra account to accounts receivable. When returns actually occur in the future reporting period, the allowance for sales returns is debited.Question 7-9Even when specific customer accounts haven’t been proven uncollectible by the end of the reporting period, bad debt expense properly should be matched with sales revenue on the income statement for that period. Likewise, since it’s not expected that all accounts receivable will be collected, the balance sheet should report only the expected net realizable value of that asset. So, to record the bad debt expense and the related reduction of accounts receivable when the amount hasn’t been determined, an estimate is needed. In an adjusting entry, we record bad debt expense and reduce accounts receivable for an estimate of the amount that eventually will prove uncollectible.If uncollectible accounts are immaterial or not anticipated, or it’s not possible to reliably estimate uncollectible accounts, an allowance for uncollectible accounts is not appropriate. In these few cases, any bad debts that do arise simply are written off as bad debt expense at the time they prove uncollectible.Answers to Questions (continued)Question 7-10The income statement approach to estimating bad debts determines bad debt expense directly by relating uncollectible amounts to credit sales. The balance sheet approach to estimating future bad debts indirectly determines bad debt expense by estimating the net realizable value for accounts receivable that exist at the end of the period. In other words, the allowance for uncollectible accounts at the end of the period is estimated and then bad debt expense is determined by adjusting the allowance account to reflect net realizable value.Question 7-11A company has to separately disclose trade receivables and receivables from related parties under U.S. GAAP, but not under IFRS.Question 7-12The assignment of all accounts receivable in general as collateral for debt requires no special accounting treatment other than note disclosure of the agreement. Question 7-13The accounting treatment of receivables factored with recourse depends on whether certain criteria are met. If the criteria are met, the factoring is accounted for as a sale. If they are not met, the factoring is accounted for as a loan. In addition, note disclosure may be required. Accounts receivable factored without recourse are accounted for as the sale of an asset. The difference between the book value and the fair value of proceeds received is recognized as a gain or a loss.Question 7-14U.S. GAAP focuses on whether control of assets has shifted from the transferor to the transferee. In contrast, IFRS focuses on whether the company has transferred “substantially all of the risks and rewards of ownership,” as well as whether the company has transferred control. Under IFRS:If the company transfers substantially all of the risks and rewards of ownership, the transfer is treated as a sale.If the company retains substantially all of the risks and rewards of ownership, the transfer is treated as a secured borrowing.If neither conditions 1 or 2 hold, the company accounts for the transaction as a sale if it has transferred control, and as a secured borrowing if it has retained control.Answers to Questions (continued)Question 7-15When a note is discounted, a financial institution, usually a bank, accepts the note and gives the seller cash equal to the maturity value of the note reduced by a discount. The discount is computed by applying a discount rate to the maturity value and represents the financing fee the bank charges for the transaction.The four-step process used to account for a discounted note receivable is as follows:1. Accrue any interest revenue earned since the last payment date (or date of thenote).2. Compute the maturity value.3. Subtract the discount the bank requires (discount rate times maturity valuetimes the remaining length of time from date of discounting to maturity date) from the maturity value to compute the proceeds to be received from the bank (maturity value less discount).pute the difference between the proceeds and the book value of the noteand related interest receivable. The treatment of the difference will depend on whether the discounting is accounted for as a sale or as a loan. If it’s a sale the difference is recorded as a loss or gain on the sale; if it’s a loan the difference is viewed as interest expense or interest revenue.Question 7-16A company’s investment in receivables is influenced by several related variables, to include the level of sales, the nature of the product or service, and credit and collection policies. The receivables turnover and average collection period ratios are designed to monitor receivables.Question 7-17The items necessary to adjust the bank balance might include deposits outstanding (including undeposited cash), outstanding checks, and any bank errors discovered during the reconciliation process. The items necessary to adjust the book balance mi ght include collections made by the bank on the company’s behalf, service and other charges made by the bank, NSF (nonsufficient funds) check charges, and any company errors discovered during the reconciliation process.Answers to Questions (concluded)Question 7-18A petty cash fund is established by transferring a specified amount of cash from the company’s general checking account to an employee designated as the petty cash custodian. The fund is replenished by writing a check to the petty cash custodian for the sum of the bills paid with petty cash. The appropriate expense accounts are recorded from petty cash vouchers at the time the fund is replenished.Question 7-19When a creditor’s investment in a receivable becomes impaired, due to a troubled debt restructuring or for any other reason, the receivable is re-measured based on the discounted present value of currently expected cash flows at the loan’s original effective rate (regardless of the extent to which expected cash receipts have been reduced). The extent of the impairment is the difference between the carrying amount of the receivable (the present value of the receivable’s cash flows prior to the restructuring) and the present value of the revised cash flows discounted at the loan’s original effective rate. This difference is recorded as a loss at the time the receivable is reduced.Question 7-20No. Under both U.S. GAAP and IFRS, a company can recognize in net income the recovery of impairment losses of accounts and notes receivable.BRIEF EXERCISESBrief Exercise 7-1The company could improve its internal control procedure for cash receipts by segregating the duties of recordkeeping and the handling of cash. Jim Seymour, responsible for recordkeeping, should not also be responsible for depositing customer checks.Brief Exercise 7-2Under IFRS the cash balance would be $245,000, because they could offset the two accounts. Under U.S. GAAP the balance would be $250,000, because they could not offset the two accounts.Brief Exercise 7-3All of these items would be included as cash and cash equivalents except the U.S. Treasury bills, which would be included in the current asset section of the balance sheet as short-term investments.Brief Exercise 7-4Income before tax in 2012 will be reduced by $2,500, the amount of the cash discounts.$25,000 x 10 = $250,000 x 1% = $2,500Brief Exercise 7-5Income before tax in 2011 will be reduced by $2,500, the anticipated amount of cash discounts.$25,000 x 10 = $250,000 x 1% = $2,500Brief Exercise 7-6Estimated returns = $10,600,000 x 8% = $848,000Less: Actual returns (720,000)Remaining estimated returns $128,000Brief Exercise 7-7Singletary cannot combine the two types of receivables under U.S. GAAP, as the director is a related party. Under IFRS a combined presentation would be allowed. Brief Exercise 7-8(1) Bad debt expense = $1,500,000 x 2% = $30,000(2) Allowance for uncollectible accounts:Beginning balance $25,000Add: Bad debt expense 30,000Deduct: Write-offs (16,000)Ending balance $39,000Brief Exercise 7-9(1) A llowance for uncollectible accounts:Beginning balance $ 25,000Deduct: Write-offs (16,000)Required allowance (33,400)*Bad debt expense $24,400(2) Required allowance = $334,000** x 10% = $33,400*Accounts receivable:Beginning balance $ 300,000Add: Credit sales 1,500,000Deduct: Cash collections (1,450,000)Write-offs (16,000)Ending balance $ 334,000** Brief Exercise 7-10Allowance for uncollectible accounts:Beginning balance $30,000Add: Bad debt expense 40,000Deduct: Required allowance (38,000)Write-offs $32,000Brief Exercise 7-11Credit sales $8,200,000Deduct: Cash collections (7,950,000)Write-offs (32,000)* Year-end balance in A/R (2,000,000)Beginning balance in A/R $1,782,000*Allowance for uncollectible accounts:Beginning balance $30,000Add: Bad debt expense 40,000Deduct: Required allowance (38,000)Write-offs $32,000 Brief Exercise 7-122011 interest revenue:$20,000 x 6% x 1/12 =$1002012 interest revenue:$20,000 x 6% x 2/12 =$200Brief Exercise 7-13Assets decrease by $7,000:Cash increases by $100,000 x 85% = $ 85,000Receivable from factor increases by($11,000 – $3,000 fee) 8,000Accounts receivable decrease (100,000)Net decrease in assets $ (7,000)Liabilities would not change as a result of this transaction.Income before income taxes decreases by $7,000(the loss on sales of receivables)The journal entry to record the transaction is as follows:Brief Exercise 7-14Logitech would account for the transfer as a secured borrowing. The receivables remain on the company’s books and a liability is recorded for the amount borrowed plus the bank’s fee.Brief Exercise 7-15Under IFRS, Huling would treat this transaction as a secured borrowing, because they retain substantially all of the risks and rewards of ownership. Under U.S. GAAP, Huling would treat this transaction as a sale, because they have transferred control. Note, however, that in practice we would typically expect for the entity that has the risks and rewards of ownership to also have control over the assets, so we would expect these criteria to usually lead to the same accounting.Brief Exercise 7-16Brief Exercise 7-17Receivables turnover = $320,000 = 5.33$60,000*($50,000 + 70,000) 2 = $60,000*Average collection = 365 = 68 daysperiod 5.33EXERCISESExercise 7-1Requirement 1Cash and cash equivalents includes:a. Balance in checking account $13,500Balance in savings account 22,100b. Undeposited customer checks 5,200c. Currency and coins on hand 580f. U.S. treasury bills with 2-month maturity 15,000Total $56,380Requirement 2d. The $400,000 savings account will be used for future plant expansion andtherefore should be classified as a noncurrent asset, either in other assets orinvestments.e. The $20,000 in the checking account is a compensating balance for a long-term loan and should be classified as a noncurrent asset, either in otherassets or investments.f. The $20,000 in 7-month treasury bills should be classified as a current assetalong with other temporary investments.Exercise 7-2Requirement 1Cash and cash equivalents includes:Cash in bank – checking account $22,500U.S. treasury bills 5,000Cash on hand 1,350Undeposited customer checks 1,840Total $30,690Requirement 2The $10,000 in 6-month treasury bills should be classified as a current asset along with other temporary investments.Exercise 7-3Requirement 1: U.S. GAAPCurrent Assets:Cash $175,000Current Liabilities:Bank Overdrafts $ 15,000 Requirement 2: IFRSCurrent Assets:Cash $160,000(No current liabilities with respect to overdrafts.)Exercise 7-4Requirement 1Sales price = 100 units x $600 = $60,000 x 70% = $42,000Requirement 2Exercise 7-4 (concluded)Requirement 3Requirement 1, using the net method:Requirement 2, using the net method:Exercise 7-5Requirement 1Sales price = 1,000 units x $50 = $50,000Requirement 2Exercise 7-6 Requirement 1Requirement 2Exercise 7-7Requirement 1Estimated returns = 4% x $11,500,000 = $460,000Less: Actual returns (450,000)Remaining estimated returns $10,000Note: another series of journal entries that produce the same end result would be:Exercise 7-7 (continued)Requirement 2Beginning balance in allowance account $300,000 Add: Year-end estimate 460,000 Less: Actual returns (450,000) Ending balance in allowance account $310,000Exercise 7-8Requirement 1Bad debt expense = $67,500 (1.5% x $4,500,000)Requirement 2Allowance for uncollectible accountsBalance, beginning of year $42,000 Add: Bad debt expense for 2011 (1.5% x $4,500,000) 67,500 Less: End-of-year balance (40,000) Accounts receivable written off $69,500 Requirement 3$69,500 — the amount of accounts receivable written off.Exercise 7-9Requirement 1To record the write-off of receivables.To reinstate an account previously written off and to record the collection.Allowance for uncollectible accounts:Balance, beginning of year $32,000Deduct: Receivables written off (21,000) Add: Collection of receivable previously written off 1,200Balance, before adjusting entry for 2011 bad debts 12,200Required allowance: 10% x $625,000 (62,500) Bad debt expense $50,300 To record bad debt expense for the year.Requirement 2Current assets:Accounts receivable, net of $62,500 allowancefor uncollectible accounts $562,500Exercise 7-10Using the direct write-off method, bad debt expense is equal to actual write-offs. Collections of previously written-off receivables are recorded as revenue.Allowance for uncollectible accounts:Balance, beginning of year $17,280Deduct: Receivables written off (17,100)Add: Collection of receivables previously written off 2,200Less: End of year balance (22,410)Bad debt expense for the year 2011 $20,030 Exercise 7-11($ in millions)Allowance for uncollectible accounts:Balance, beginning of year $16Add: Bad debt expense 14Less: End of year balance (18)Write-offs during the year $ 12*Accounts receivable analysis:Balance, beginning of year ($1,084 + 16)$ 1,100Add: Credit sales 4,271Less: Write-offs* (12)Less: Balance end of year ($953 + 18) (971)Cash collections $4,388Exercise 7-12Requirement 1Requirement 22011 income before income taxes would be understated by $900 2012 income before income taxes would be overstated by $900.Exercise 7-13Requirement 1Requirement 2$ 1,800 interest for 9 months÷ $28,200 sales price= 6.383% rate for 9 monthsx 12/9to annualize the rate_______= 8.511% effective interest rateExercise 7-14Requirement 1Book value of stock $16,000Plus gain on sale of stock 6,000= Note receivable $22,000Interest reported for the year $ 2,200= 10% rate Divided by value of note $ 22,000 Requirement 2To record sale of stock in exchange for note receivable.To accrue interest on note receivable for twelve months.Exercise 7-15Exercise 7-16Exercise 7-17Exercise 7-18Mountain High retains significant risks and rewards and therefore must treat the transfer as a secured borrowing. The accounts receivable stay on the balance sheet of Mountain High, and they must record a liability.Exercise 7-19Step 1: Accrue interest earned.Step 2: Add interest to maturity to calculate maturity value.Step 3: Deduct discount to calculate cash proceeds.Step 4: To record a loss for the difference between the cash proceeds and the note’s book value.Exercise 7-20List A List Bc 1. Internal control a. Restriction on cash.j 2. Trade discount b. Cash discount not taken is sales revenue.g 3. Cash equivalents c. Includes separation of duties.h 4. Allowance for uncollectibles d. Bad debt expense a % of credit sales.i 5. Cash discount e. Recognizes bad debts as they occur.l 6. Balance sheet approach f. Sale of receivables to a financial institution.d 7. Income statement approach g. Include highly liquid investments.k 8. Net method h. Estimate of bad debts.a 9. Compensating balance i. Reduction in amount paid by credit customer.m 10. Discounting j. Reduction below list price.b 11. Gross method k. Cash discount not taken is interest revenue.e 12. Direct write-off method l. Bad debt expense determined by estimating realizablevalue.f 13. Factoring m. Sale of note receivable to a financial institution.Exercise 7-21Requirement 1Step 1: To accrue interest earned for two months on note receivableStep 2: Add interest to maturity to calculate maturity value.Step 3: Deduct discount to calculate cash proceeds.Exercise 7-21 (continued)Step 4: To record a loss for the difference between the cash proceeds and the note’s book value.Exercise 7-21 (concluded)Requirement 2To accrue interest earned on note receivable.Exercise 7-22Second quarter:Receivables turnover = $16,629 = 1.62$10,244Average collection = 91 = 56 daysperiod 1.62Third quarter:Receivables turnover = $13,648 =1.36$10,068Average collection = 91 = 67 daysperiod 1.36Exercise 7-23Average collection period = 365 ÷ Accounts receivable turnover = 50 days Accounts receivable turnover = 365 ÷ 50 = 7.3Average accounts receivable = ($400,000 + 300,000) ÷ 2 = $350,000 Accounts receivable turnover = Net sales ÷ Average accounts receivable7.3 = Net sales ÷ $350,000Net sales = 7.3 x $350,000 =$2,555,000Exercise 7-24To establish the petty cash fund.To replenish the petty cash fund.Exercise 7-25Exercise 7-26Compute balance per bank statement:Balance per books $23,820 Deduct: Deposits outstanding (2,340) Add: Checks outstanding 1,890 Deduct: Bank service charges (38) Balance per bank $23,332Exercise 7-27Requirement 1Requirement 2To correct error in recording cash receipt from credit customer.To record credits to cash revealed by the bank reconciliation.Note: Each of the adjustments to the book balance required journal entries.None of the adjustments to the bank balance require entries.Exercise 7-28A NALYSISPrevious Value:Accrued 2010 interest (10% x $12,000,000)$ 1,200,000Principal 12,000,000Carrying amount of the receivable$13,200,000 New Value:Interest $1 million x 1.73554 * = $1,735,540Principal $11 million x 0.82645 ** = 9,090,950Present value of the receivable (10,826,490) Loss:$ 2,373,510* present value of an ordinary annuity of $1: n=2, i=10% (from Table 4)** present value of $1: n=2, i=10% (from Table 2)J OURNAL E NTRIESJanuary 1, 2011Loss on troubled debt restructuring (to balance) ......... 2,373,510Accrued interest receivable (account balance) ........ 1,200,000 Note receivable ($12,000,000 - 10,826,490) ........... 1,173,510 December 31, 2011Cash (required by new agreement) ................. ............ 1,000,000Note receivable (to balance) ....................... ….. ........ 82,649Interest revenue (10% x $10,826,490) ........ ............ 1,082,649December 31, 2012Cash (required by new agreement) ................. ............ 1,000,000Note receivable (to balance) ........................... ............ 90,861Interest revenue (10% x [$10,826,490 + 82,649]) ... 1,090,861*Cash (required by new agreement) ................. ............ 11,000,000Note receivable (balance) ........................... ............ 11,000,000 * rounded to amortize the note to $11,000,000 (per schedule below)Exercise 12-28 (concluded)Amortization Schedule – Not requiredCash Effective Increase in Outstanding Interest Interest Balance Balance by agreement 10% x Outstanding Balance Discount Reduction10,826,4901 1,000,000 .10 (10,826,490) = 1,082,649 82,649 10,909,1392 1,000,000 .10 (10,909,139) = 1,090,861* 90,861 11,000,0002,000,000 2,173,510 173,510* roundedExercise 7-29A NALYSISPrevious Value:Accrued 2010 interest (10% x $240,000)$ 24,000Principal 240,000Carrying amount of the receivable$264,000New Value:$11,555 + 11,555 + 11,555 + 240,000=$274,665$274,665 x 0.82645 * = (226,997) Loss:$37,003* present value of $1: n=2, i=10% (from Table 2)J OURNAL E NTRIESJanuary 1, 2011Loss on troubled debt restructuring (to balance) ......... 37,003Accrued interest receivable (10% x $240,000) ........ 24,000 Note receivable ($240,000 - 226,997) ........ ............ 13,003 December 31, 2011Note receivable (to balance) ........................... ............ 22,700Interest revenue (10% x $226,997) ............. ............ 22,700 December 31, 2012Note receivable (to balance) ........................... ............ 24,968Interest revenue (10% x [$226,997 + 22,700]) ........ 24,968* Cash (required by new agreement) ................. ............ 274,665Note receivable (balance) ........................... ............ 274,665 * rounded to amortize the note to $274,665 (per schedule below)Exercise 7-29 (concluded)Amortization Schedule – Not requiredCash Effective Increase in Outstanding Interest Interest Balance Balance by agreement 10% x Outstanding Balance Discount Reduction226,9971 0 .10 (226,997) = 22,700 22,700 249,6972 0 .10 (249,697) = 24,968* 24,968 274,66547,668 47,668* roundedExercise 7-30Requirement 1The specific citation that specifies these disclosure policies is FASB ACS 310–10–50–9: “Receivables—Overall—Disclosure—Accounting Policies for Credit Losses and Doubtful Accounts.”Requirement 2FASB ACS 310–10–50–9 reads as follows:“In addition to disclosures required by this Subsection and Subtopic 450-20, an entity shall disclose a description of the accounting policies and methodology the entity used to estimate its allowance for loan losses, allowance for doubtful accounts, and any liability for off-balance-sheet credit losses and related charges for loan, trade receivable or other credit losses in the notes to the financial statements. Such a description shall identify the factors that influenced management's judgment (for example, historical losses and existing economic conditions) and may also include discussion of risk elements relevant to particular categories of financial instruments.”。

Appendix A Derivatives QuestionsA-1Reflective thinkingA-2Reflective thinkingA-3AnalyticA-4Reflective thinkingA-5Reflective thinkingA-6Reflective thinkingA-7Reflective thinkingExercisesA-1Reflective thinkingA-2AnalyticA-3AnalyticA-4AnalyticA-5AnalyticA-6AnalyticProblemsA-1 AnalyticA-2 Analytic, CommunicationsA-3 AnalyticCasesA-1A-2A-3A-4QUESTIONS FOR REVIEW OF KEY TOPICSQuestion A-1These instruments “derive” their values or contract ually required cash flows from some other security or index.Question A-2The FASB has taken the position that the income effects of the hedge instrument and the income effects of the item being hedged should be recognized at the same time.Question A-3I f interest rates change, the change in the debt’s fair value will be less than the change in the swap’s fair value. The gain or loss on the $500,000 notional difference will not be offset by a corresponding loss or gain on debt. Any increase or decrease in income resulting from a hedging arrangement would be a result of hedge ineffectiveness such as this.Question A-4A futures contract is an agreement between a seller and a buyer that calls for the seller to deliver a certain commodity (such as wheat, silver, or Treasury bond) at a specific future date, at a predetermined price. Such contracts are actively traded on regulated futures exchanges. If the “commodity” is a financial instrument, such as a Treasury bill, commercial paper, or a CD, the contract is called a financial futures agreement.Question A-5An interest rate swap exchanges fixed interest payments for floating rate payments, or vice versa, without exchanging the underlying notional amount.Question A-6All derivatives, without exception, are reported on the balance sheet as either assets or liabilities at fair (or market) value. The rationale is that (a) derivatives create either rights or obligations that meet the FASB’s definition of assets or liabilities and (b) fair value is the most meaningful measurement.Question A-7A gain or loss from a cash flow hedge is deferred as other comprehensive income until it can be recognized in earnings along with the earnings effect of the item being hedged.EXERCISESExercise A-1Indicate (by abbreviation) the type of hedge each activity described below would represent.Hedge TypeFV Fair value hedgeCF Cash flow hedgeFC Foreign currency hedgeN Would not qualify as a hedgeActivityFV 1.An options contract to hedge possible future price changes of inventory.CF 2.A futures contract to hedge exposure to interest rate changes prior to replacing bank notes when they mature.CF 3.An interest rate swap to synthetically convert floating rate debt into fixed rate debt.FV 4.An interest rate swap to synthetically convert fixed rate debt into floating rate debt.FV 5.A futures contract to hedge possible future price changes of timber covered by a firm commitment to sell.CF 6.A futures contract to hedge possible future price changes of a forecasted sale of tin.FC 7.ExxonMobil’s net investment in a Kuwait oil field.CF 8.An interest rate swap to synthetically convert floating rate interest on a stock investment into fixed rate interest.N 9.An interest rate swap to synthetically convert fixed rate interest on a held-to-maturity debt investment into floating rate interest.CF 10.An interest rate swap to synthetically convert floating rate interest on a held-to-maturity debt investment into fixed rate interest.FV 11.An interest rate swap to synthetically convert fixed rate interest on a stock investment into floating rate interest.Exercise A-2Requirement 1January 1 March 31 June 30 Fair value of interest rate swap0 $6,472 $11,394 Fair value of note payable$200,000 $206,472 $211,394 Fixed rate 10% 10% 10% Floating rate 10% 8% 6% Fixed interest receipts $5,000 $5,000 Floating payments 4,000 3,000 Net interest receipts (payments) $1,000 $2,000Exercise A-2 (concluded)Requirement 2January 1Cash 200,000Notes payable 200,000 To record the issuance of the noteMarch 31Interest expense ([10% x ¼] x $200,000) 5,000Cash 5,000 To record interestCash ($5,000 – ([8% x ¼] x $200,000)) 1,000Interest expense 1,000 To record the net cash settlementInterest rate swap [asset] ($6,472 – 0) 6,472Holding gain – interest rate swap 6,472 To record change in fair value of the derivativeHolding loss - hedged note 6,472Note payable ($206,472 – 200,000)6,472 To record change in fair value of the noteJune 30Interest expense ([10% x ¼] x $200,000) 5,000Cash 5,000 To record interestCash ($5,000 – ([6% x ¼] x $200,000)) 2,000Interest expense 2,000 To record the net cash settlementInterest rate swap [asset] ($11,394 – 6,472) 4,922Holding gain – interest rate swap 4,922 To record change in fair value of the derivativeHolding loss - hedged note 4,922Note payable ($211,394 – 206,472)4,922 To record change in fair value of the noteExercise A-3Requirement 1January 1 March 31 June 30Fair value of interest rate swap0 $6,472 $11,394 Fair value of investment$200,000 $206,472 $211,394 Fixed rate 10% 10% 10% Floating rate 10% 8% 6% Fixed interest payments $5,000 $5,000 Floating interest receipts (4,000) (3,000) Net interest payments $1,000 $2,000Exercise A-3 (concluded)Requirement 2January 1Investment in notes 200,000Cash 200,000 To record the investment of the noteMarch 31Cash 5,000Interest revenue ([10% x ¼] x 200,000)5,000 To record interestInterest revenue 1,000Cash ($5,000 – ([8% x ¼] x $200,000))1,000 To record the net cash settlementHolding loss – interest rate swap 6,472Interest rate swap [liability] ($6,472 – 0)6,472 To record change in fair value of the derivativeInvestment in notes ($206,472 – 200,000) 6,472Holding gain - hedged investment 6,472 To record change in fair value of the investmentJune 30Cash 5,000Interest revenue ([10% x ¼] x $200,000)5,000 To record interestInterest revenue 2,000Cash ($5,000 – ([6% x ¼] x $200,000))2,000 To record the net cash settlementHolding loss – interest rate swap 4,922Interest rate swap [liability] ($11,394 – $6,472)4,922 To record change in fair value of the derivativeInvestment in notes ($211,394 – 206,472) 4,922Holding gain - hedged investment 4,922 To record change in fair value of the investmentExercise A-4Requirement 1June 30Fair value of interest rate swap$11,394Fair value of note payable$220,000Fixed rate 10%Floating rate 6%Fixed receipts $5,000 ([10% x ¼] x $200,000) Floating payments (3,000) ([6% x ¼] x $200,000) Net interest receipts (payments) $2,000Exercise A-4 (concluded)Requirement 2Your entries would be the same whether there was or was not an additional rise in the fair value of the note (higher than that of the swap) on June 30 due to investors’ perceptions that the creditworth iness of LLB was improving. When a note’s fair value changes by an amount different from that of a designated hedge instrument for reasons unrelated to interest rates, we ignore those changes. We recognize only the fair value changes in the hedged item that we can attribute to the risk being hedged (interest rate risk in this case). The entries would be:June 30Interest expense ([10% x ¼] x $200,000) 5,000Cash 5,000To record interestCash ($5,000 – ([6% x ¼] x $200,000)) 2,000Interest expense 2,000To record the net cash settlementInterest rate swap [asset] ($11,394 – 6,472) 4,922Holding gain – interest rate swap 4,922To record change in fair value of the derivativeHolding loss - hedged note 4,922Note payable ($211,394 – 206,472)4,922To record change in fair value of the note due to interestExercise A-5January 1Cash 200,000Notes payable 200,000 To record the issuance of the noteMarch 31Interest expense ([10% x ¼] x $200,000)5,000Cash 5,000 To record interestCash ($5,000 – ([8% x ¼] x $200,000))1,000Interest rate swap ($6,472 - 0)6,472Interest revenue ([10% x ¼] x $0)0 Holding gain - interest rate swap (to balance)7,472 To record the net cash settlement, accrued interest on theswap, and change in fair value of the derivativeHolding loss - hedged note 6,472Notes payable ($206,472 – 200,000)6,472 To record change in fair value of the note due to interestJune 30Interest expense ([8% x ¼] x $206,472)4,129Notes payable (difference)871 Cash ([10% x ¼] x $200,000)5,000 To record interestCash ($5,000 – ([6% x ¼] x $200,000))2,000Interest rate swap ($11,394 – 6,472)4,922Interest revenue ([8% x ¼] x $6,472)129 Holding gain - interest rate swap (to balance)6,793 To record the net cash settlement, accrued interest on theswap, and change in fair value of the derivativeHolding loss - hedged note 5,793Notes payable ($211,394 – 206,472 + 871)5,793 To record change in fair value of the note due to interestExercise A-6Requirement 1June 30Fair value of interest rate swap$11,394Fair value of note payable$220,000Fixed rate 10%Floating rate 6%Fixed receipts $5,000 ([10% x ¼] x 200,000) Floating payments (3,000) ([6% x ¼] x 200,000) Net interest receipts (payments) $2,000Exercise A-6 (concluded)Requirement 2Your entries would be the same whether there was or was not an additional rise in the fair value of the note (higher than that of the swap) on June 30 due to investors’ perce ptions that the creditworthiness of LLB was improving. When a note’s fair value changes by an amount different from that of a designated hedge instrument for reasons unrelated to interest rates, we ignore those changes. We recognize only the fair value changes in the hedged item that we can attribute to the risk being hedged (interest rate risk in this case). The entries would be:June 30Interest expense ([8% x ¼] x $206,472)4,129Notes payable (difference)871Cash ([10% x ¼] x $200,000)5,000To record interestCash ($5,000 – ([6% x ¼] x $200,000))2,000Interest rate swap ($11,394 – 6,472)4,922Interest revenue ([8% x ¼] x $6,472)129Holding gain - interest rate swap (to balance)6,793To record the net cash settlement, accrued interest on theswap, and change in fair value of the derivativeHolding loss - hedged note 5,793Notes payable ($211,394 – 206,472 + 871)5,793To record change in fair value of the note due to interestPROBLEMSProblem A-1Requirement 1January 1 December 312011 2011 2012 2013 Fixed rate 8% 8% 8% 8% Floating rate 8% 9% 7% 7% Fixed receipts $ 8,000 $8,000 $8,000 Floating payments 9,000 7,000 7,000 Net interest receipts (payments) $(1,000) $1,000 $ 1,000Requirement 2January 1, 2011Cash 100,000Notes payable 100,000To record the issuance of the noteDecember 31, 2011Interest expense (8% x $100,000)8,000Cash 8,000To record interestInterest expense 1,000Cash ($8,000 – [9% x $100,000])1,000To record the net cash settlementHolding loss–interest rate swap (to balance)1,759Interest rate swap (0 – $1,759)1,759To record the change in fair value of the derivativeNotes payable ($98,241 – 100,000)1,759Holding gain–hedged note 1,759To record change in fair value of the noteProblem A-1 (continued)Requirement 3December 31, 2012Interest expense (8% x $100,000)8,000Cash 8,000 To record interestCash ($8,000 – [7% x $100,000])1,000Interest expense 1,000 To record the net cash settlementInterest rate swap ($935 – [–1,759])2,694Holding gain–interest rate swap (to balance)2,694 To record the change in fair value of the derivativeHolding loss–hedged note ($100,935 – 98,241)2,694Notes payable (to balance)2,694 To record change in fair value of the note due to interestProblem A-1 (continued)Requirement 4December 31, 2013Interest expense (8% x $100,000)8,000Cash 8,000 To record interestCash ($8,000 – [7% x $100,000])1,000Interest expense1,000 To record the net cash settlementHolding loss - interest rate swap (to balance)935Interest rate swap (0 – $935)935 To record the change in fair value of the derivativeNotes payable ($100,000 – 100,935)935Holding gain - hedged note 935 To record change in fair value of the note due to interestNote payable 100,000Cash 100,000 To repay the loanProblem A-1 (continued) Requirement 5Jan. 1, 2011Dec. 31, 2011BalanceDec. 31, 2012BalanceDec. 31, 2013BalanceProblem A-1 (continued)Requirement 6Income Statement + (-)2011(8,000) Interest expense(1,000) Interest expense(1,759) Holding loss – interest rate swap1,759 Holding gain – hedged note(9,000) Net effect – same as floating interest payment on swap 2012(8,000) Interest expense1,000 Interest expense2,694 Holding gain – interest rate swap(2,694) Holding loss – hedged note(7,000) Net effect – same as floating interest payment on swap 2013(8,000) Interest expense1,000 Interest expense(935) Holding loss – interest rate swap935 Holding gain – hedged note(7,000) Net effect – same as floating interest payment on swapProblem A-1 (concluded)Requirement 7Your entries would not be affected. When a note’s fair value changes by an amount different from that of a designated hedge instrument for reasons unrelated to interest rates, we ignore those changes. We recognize only the fair value changes in the hedged item that we can attribute to the risk being hedged (interest rate risk in this case). The entries still would be:Interest expense (8% x $100,000)8,000Cash 8,000To record interestInterest expense 1,000Cash ($8,000 – [9% x $100,000])1,000To record the net cash settlementHolding loss–interest rate swap (to balance)1,759Interest rate swap (0 – $1,759)1,759To record the change in fair value of the derivativeNotes payable ($98,241 – 100,000)1,759Holding gain–hedged note 1,759To record change in fair value of the noteProblem A-2Requirement 1CMOS has an unrealized gain due to the increase in the value of the derivative (not necessarily the same amount). Because interest rates declined, the swap will enable CMOS to pay the lower floating rate (receive cash on the net settlement of interest). The value of the swap (an asset) represents the present value of expected future net cash receipts. That amount has increased, as has the swap’s fair value, creating the unrealized gain. There is an offsetting loss on the bonds(a liability) because the fair value of the company’s debt has increased. Becausethe loss on the bonds exactly offsets the gain on the swap, earnings will neither increase nor decrease due to the hedging arrangement.Requirement 2CMOS would have an unrealized loss due to the decrease in the value of the derivative. Because interest rates increased, the swap will cause CMOS to pay the higher floating rate (pay cash on the net settlement of interest). The value of the swap (an asset) represents the present value of expected future net cash receipts. That amount has decreased, as has the swap’s fair value, creating the unrealized loss. There is an offsetting gain on the bonds (a liability) because the fair value of the company’s debt has decreased. Because the gain on the bonds exactly offsets the loss on the swap, earnings will neither increase nor decrease due to the hedging arrangement.Problem A-2 (continued)Requirement 3The unrealized gain on the swap and loss on the bonds would not be affected.When a hedged debt’s fair value changes by an amount different from that of a designated hedge instrument for reasons unrelated to interest rates, we ignore those changes. We recognize only the fair value changes in the hedged item that we can attribute to the risk being hedged (due to interest rate risk in this case).Because the loss on the bonds exactly offsets the gain on the swap, earnings will neither increase nor decrease due to the hedging arrangement.Requirement 4There would be an unrealized gain due to the increase in the value of the derivative. There is an unrealized loss on the bonds (a liability). However, the gain on the derivative would be $20,000 more than the loss on the bonds. Because the loss on the bonds is less than the gain on the swap, earnings will increase by $20,000 (ignoring taxes) due to the hedging arrangement, an effect resulting from hedge ineffectiveness. This is an intended effect of hedge accounting. To the extent that a hedge is effective, the earnings effect of a derivative cancels out the earnings effect of the item being hedged. All ineffectiveness of a hedge is recognized currently in earnings.Problem A-2 (concluded)Requirement 5There would be an unrealized loss due to a decrease in the value of the derivative,a liability to BIOS. Because interest rates declined, the swap would cause BIOSto receive the lower floating rate (pay cash on the net settlement of interest). The value of the swap represents the present value of expected future net cash payments. That amount has increased, as has the swap’s fair value, creating the unrealized loss. There would be an offsetting gain, though, on the bond investment because the fair value of the company’s investment has increased.Because the gain on the bonds exactly offsets the loss on the swap (a liability), earnings will neither increase nor decrease due to the hedging arrangement.Problem A-3Requirement 1January 1 December 312011 2011 2012 2013 Fixed rate 8% 8% 8% 8% Floating rate 8% 9% 7% 7% Fixed payments $ 8,000 $8,000 $8,000 Floating payments 9,000 7,000 7,000 Net interest receipts (payments) $(1,000) $1,000 $ 1,000Requirement 2January 1, 2011Cash 100,000Notes payable 100,000To record the issuance of the noteDecember 31, 2011Interest expense (8% x $100,000)8,000Cash 8,000To record interestInterest expense (8% x $0)0Holding loss–interest rate swap (to balance)2,759Interest rate swap (0 – $1,759)1,759Cash ($8,000 – [9% x $100,000])1,000To record the net cash settlement, accrued interest on theswap, and change in fair value of the derivativeNotes payable ($98,241 – 100,000)1,759Holding gain–hedged note 1,759To record change in fair value of the note due to interestProblem A-3 (continued)Requirement 3December 31, 2012Interest expense (9% x $98,241)8,842Notes payable (difference)842 Cash (8% x $100,000)8,000 To record interestCash ($8,000 – [7% x $100,000])1,000Interest rate swap ($935 – [– 1,759])2,694Interest expense (9% x $1,759)158Holding gain–interest rate swap (to balance)3,852 To record the net cash settlement, accrued interest on theswap, and change in fair value of the derivativeHolding loss–hedged note ($100,935 – 98,241 – 842)1,852Notes payable (to balance)1,852 To record change in fair value of the note due to interestProblem A-3 (continued)Requirement 4December 31, 2013Interest expense (7% x $100,935)7,065Notes payable (difference)935 Cash (8% x $100,000)8,000 To record interestCash ($8,000 – [7% x $100,000])1,000Holding loss–interest rate swap (to balance)0Interest rate swap (0 – $935)935 Interest revenue (7% x $935)65 To record the net cash settlement, accrued interest on the swap,and change in fair value of the derivativeNotes payable ($100,000 – 100,935 + 935)0Holding gain–hedged note 0 To record change in fair value of the note due to interestNote payable 100,000Cash 100,000 To repay the loanProblem A-3 (continued) Requirement 5Jan. 1, 2011Dec. 31, 2011BalanceDec. 31, 2012BalanceDec. 31, 2013BalanceProblem A-3 (continued)Requirement 6Income Statement + (-)2011(8,000) Interest expense(2,759) Holding loss – interest rate swap1,759 Holding gain – hedged note(9,000) Net effect – same as floating interest payment on swap 2012(8,842) Interest expense(158) Interest expense3,852 Holding gain – interest rate swap(1,852) Holding loss – hedged note(7,000) Net effect – same as floating interest payment on swap 2013(7,065) Interest expense65 Interest revenue(0) Holding loss – interest rate swap0 Holding gain – hedged note(7,000) Net effect – same as floating interest payment on swapProblem A-3 (concluded)Requirement 7Your entries would not be affected. When a note’s fair value changes by an amount different from that of a designated hedge instrument for reasons unrelated to interest rates, we ignore those changes. We recognize only the fair value changes in the hedged item that we can attribute to the risk being hedged (interest rate risk in this case). The entries still would be:Interest expense (8% x $100,000)8,000Cash 8,000To record interestInterest expense (8% x $0)0Holding loss–interest rate swap (to balance)2,759Interest rate swap (0 – $1,759)1,759Cash ($8,000 – [9% x $100,000])1,000To record the net cash settlement, accrued interest on theswap, and change in fair value of the derivativeNotes payable ($98,241 – 100,000)1,759Holding gain–hedged note 1,759CASESReal World Case A-1Requirement 1When Johnson & Johnson indicates that it expects that substantially all of the balance of deferred net gains on derivatives will be reclassified into earnings over the next 12 months as a result of transactions that are expected to occur over that period, it is saying that these as-yet-unrecognized net gains will be included in net income.A gain or loss from certain hedges is deferred as other comprehensive income until it can be recognized in earnings along with the earnings effect of the item being hedged. Requirement 2A gain or loss from a “fair value”hedge is recognized immediately in earnings along with the loss or gain from the item being hedged. On the other hand, a gain or loss from a “cash flow”hedge is deferred in the manner described by Johnson & Johnson until it can be recognized in earnings along with the earnings effect of the item being hedged. The hedging transactions referred to by Johnson & Johnson might also include foreign currency hedges used to hedge foreign currency exposure to a forecasted transaction because they are treated as a cash flow hedge.Communication Case A-2Depending on the assumptions made, different views can be convincingly defended. The process of developing and synthesizing the arguments will likely be more beneficial than any single solution. Each student should benefit from participating in the process, interacting first with his or her partner, then with the class as a whole. It is important that each student actively participate in the process. Domination by one or two individuals should be discouraged.Hedging means taking an action that is expected to produce exposure to a particula r type of risk that’s precisely the opposite of an actual risk to which the company already is exposed. Under existing hedge accounting, if the contract meets specified hedging criteria, the income effects of the hedge instrument and the income effects of the item being hedged should be recognized at the same time.Arguments raised may focus on a variety of issues including:•Which hedges should qualify for special accounting? Hedges of risk of loss? Hedges that reduce the variability of outcomes?•Should treatment be different for fair value hedges and cash flow hedges?•Should only risk exposures arising from existing assets or liabilities qualify for special accounting? Should anticipated transactions be included also?•To what extent if any must there be correlation between the gains and losses on the hedge instrument and the item being hedged?•How should any deferred gain or loss be classified prior to recognition?Real World Case A-3The following is a copy of the 13-Week U.S. Treasury Bill Futures: Settlement Prices as of September 21, 2009:Daily Settlements for 13-Week U.S.Treasury Bill Futures (PRELIMINARY)Trade Date:OCT 09 - - - - UNCH 99.51 - -NOV 09 - - - - UNCH 99.47 - -DEC 09 - - - - UNCH 99.47 - -MAR 10 - - - - UNCH 99.37 - -JUN 10 - - - - UNCH 99.27 - -SEP 10 - - - - UNCH 99.27 - -TotalResearch Case A-4[Note: This case requires the student to reference a journal article.]Requirement 1According to the authors, the primary problems or issues the FASB was attempting to address with the standard are the following:∙Previous accounting guidance for derivatives and hedging was incomplete.Only a few types of derivatives used today were specifically addressed inaccounting standards. SFAS No. 52, Foreign Currency Translation, addresses forward foreign exchange contracts, and SFAS No. 80, Accounting for Futures Contracts, addresses exchange-traded futures contracts. Similarly, those twostandards were the only ones that specifically provided for hedge accounting.The Emerging Issues Task Force (EITF) addressed the accounting for somederivatives and for some hedging activities not covered in Statements 52 or 80;however, that effort was on an ad hoc basis. Large gaps remained in theauthoritative accounting guidance. Accounting practice had filled some ofthose gaps on issues such as "synthetic instrument accounting" without anycommonly understood limitations on their appropriate use. The result of thisaccounting hodgepodge was that a) many derivative instruments were carried "off balance sheet" regardless of whether they are part of a hedging strategy, b) practices were inconsistent among entities and for similar instruments held by the same entity, and c) users of financial reports were confused or even misled.∙Previous accounting guidance for derivatives and hedging was inconsistent.Under the previous accounting guidance (FASB standards and EITFconsensuses), the required accounting treatment may have differed depending on the type of instrument used in hedging and the type of risk being hedged.For example, an anticipated transaction could qualify as a hedged item only if the hedging instrument was a nonforeign currency futures contract or anonforeign currency purchased option. Additionally, derivatives weremeasured differently under the previous accounting standards--futurescontracts were reported at fair value, foreign currency forward contracts atamounts that reflect changes in foreign exchange rates but not other valuechanges, and other derivatives unrecognized or reported at nominal amounts that were a small fraction of the value of their potential cash flows. Otherhedge accounting inconsistencies related to level of risk assessment(transaction-based versus entity-wide) and measurement of hedgeeffectiveness.Case A-4 (concluded)∙Previous accounting guidance for derivatives and hedging was complex. The lack of a single, comprehensive approach to accounting for derivatives andhedging made the accounting guidance very complex. The incompleteness ofthe FASB statements on derivatives and hedging forced entities to look to avariety of different sources, including the numerous EITF issues andnonauthoritative literature, to determine how to account for specificinstruments or transactions. Because there was often nothing directly on point, entities were forced to analogize to existing guidance. Because differentsources of analogy often conflict, a wide range of answers could often besupported, and no answer was safe from later challenge.∙Effects of derivatives were not apparent. Under the previous varied practices, derivatives may or may not have been recognized in the financial statements. If recognized in the financial statements, realized and unrealized gains and losses on derivatives may have been deferred from earnings recognition and reported as part of the carrying amount (or basis) of a related item or as if they arefreestanding assets or liabilities. As a result, users of financial statements found it difficult to determine what an entity has or has not done with derivatives and what the related effects were. It was difficult to understand how financialstatements could purport to present financial position without reporting thematerial benefits and obligations associated with derivative instruments. Requirement 2In considering the issues, the FASB made four fundamental decisions that became the cornerstones of the proposed statement. According to the article, those fundamental decisions were:∙Derivatives are assets or liabilities and should be reported in the financial statements.∙Fair value is the most relevant measure for financial instruments and the only relevant measure for derivatives.∙Only items that are assets or liabilities should be reported as such in the financial statements. A derivative loss should not be reported as an assetbecause it has no future economic benefit associated with it.∙Hedge accounting should be provided for only qualifying transactions, and one aspect of qualification should be an assessment of offsetting changes in fairvalues or cash flows.。