Retained Mode Parallel Rendering for Scalable Tiled Displays

- 格式:pdf

- 大小:546.78 KB

- 文档页数:5

Chap 11.Mostly the objective of a business is not to make a profit.错2. A corporation is a business that is legally separate and distinct from its owners.对3. Accounting is a service that provides many different users with financial information to make economic decisions.对4. Primary users of accounting information are accountants.错5. "Managerial accounting is primarily concerned with the recording and reporting of economic data and activities of an entity for use by owners, creditors, governmental agencies, and the public." 错6. The financial statements of a proprietorship should include the owner's personal assets and liabilities.错7. The unit of measurement concept requires that economic data be recorded in a common unit of measurement 对8. "If a building is appraised for $90,000, offered for sale at $95,000, and the buyer pays $85,000 cash for it, the buyer would record the building at $90,000." 错9.An entity that is organized according to state or federal statutes and in which ownership is divided into shares of stock is a答案BA. proprietorshipB. corporationC. partnershipD. governmental unit10.Which of the following best describes accounting? BA. records economic data but does not communicate the data to users according to any specific rulesB. is an information system that provides reports to stakeholdersC. is of no use by individuals outside of the businessD. is used only for filling out tax returns and for financial statements for various type of governmental reporting requirements11. The two most common specialized fields of accounting in practice are BA. forensic accounting and financial accountingB. managerial accounting and financial accountingC. managerial accounting and environmental accountingD. financial accounting and tax accounting systems12.Which of the following is not a characteristic of financial accounting ______ CA. external reportingB. general-purpose informationC. future orientationD. standard and uniform reporting13.The business entity concept means that DA. the owner is part of the business entityB. an entity is organized according to state or federal statutesC. an entity is organized according to the rules set by the FASBD. "the entity is an individual economic unit for which data are recorded, analyzed, and reported"14."For accounting purposes, the business entity should be considered separate from its owners if the entity is" DA. a corporationB. a proprietorshipC. a partnershipD. all of the above15."Tom Smith is the owner of a small bookstore. He mainly does business through the internet so that the store has no physical office room and the ordersare dealt with at home. As a result, such bills as electricity, heating, telephone, and housecleaning are all recorded as expenses of the bookstore. This is not correct from the viewpoint of _______" AA. the separate entity conceptB. the going concern assumptionC. the accounting period conceptD. the monetary measurement assumption16.Which of the followings assures the accounting information users of timely decision___________ CA. the separate entity conceptB. the going concern assumptionC. the accounting period conceptD. the monetary measurement assumption17."Smith Company purchased $105,000 of computer equipment from Brown Company. Smith Company paid for the equipment using cash that had been obtained from the initial investment by Connie Smith. The transaction involving the computer equipment should be recorded on the accounting records of which of the following entities?" DA. Smith Company and Connie Smith's personal recordsB. Brown Company and Connie Smith's personal recordsC. Brown CompanyD. Smith Company and Brown Company18."The Reynolds Company estimated that the value of its land had increased from $10,000 to $16,000 and therefore wrote up the land account to $16,000. Which accounting concept(s) was (were) violated?" CA. separate entity conceptB. money measurement conceptC. historical cost conceptD. accounting period concept19.“Equipment with an estimated m arket value of $45,000 is offered for sale at $65,000. The equipment is acquired for $10,000 in cash and a note payable of $40,000 due in 30 days. The amount used in the buyer's accounting records to record this acquisition is" AA.50000B.65000C.10000D.4500020."(mark out all correct answers) Which of the followings should not be included in the financial records of Delicious Sam, a bakery at the corner of the street ____________" A C DA. "Sweetie Alice, another bakery located opposite to Delicious Sam, lowered its price for brown bread from 50 cents to 30 cents "B. Delicious Sam purchased 100kg of flour for $50C. "Sweetie Alice sold cookie of $10 to Sam, the owner of Delicious Sam."D. Delicious Sam promised free delivery to bulk buying customers in order to compete with Sweetie Alice.E. Sam withdrew $200 from his personal bank account to pay the bill from the miller who supplied flour to Delicious SamChap 2 –a3.An asset must have a physical substance and can be touched. 错9. Match each of the following items to: a. assets; b. liabilities; c. owners' equity;d. none of above items. 1.ending inventory ; 2.accounts payable to the suppliers;3.salaries due but unpaid;4.accounts receivable;5.retained earnings;6.capital stock;7.prepaid insurance答案:a b b a c c a13.How does the collection of cash from a customer who was previously put on account affect the accounting equation?答案CA.assets decrease; owner's equity decreases B.assets increase; owner's equity increasesC. assets increase; assets decreaseD. assets increase; liabilities increase25.(mark out all correct answers) The owner’s equity accounts of a partnership might be答案 B D EA. capital stockB. "Tom Smith, capital"C. retained earningsD. "Alice Butler, capital"E. "Pauline Jones, capital"Chap 2 –b3.Indicate for each of following transactions should related accounts be debited or credited. 1.Purchased inventory on account. The inventory account should be____; 2.Borrowed money from a bank. The notes payable account should be___; 3.Issued stock for cash. The capital stock should be____ 答案D C C6.Owner's equity is increased by 答案BA. cashB. revenueC. accounts receivableD. all of the above8."For a corporation, temporary proprietorship accounts are supposed to replace the ____________________ account temporarily."答案 retained earnings12.Consuming goods and services in the process of generating revenues results in expenses. 对17. Net profit reported in the Income statement will not be reduced when the corporation declares and pays cash dividends to the stockholders 对21. A credit signifies a decrease in 答案AA. drawingsB. liabilitiesC. capitalD. revenue27."Land, originally purchased for $20,000, is sold for $75,000 in cash. What is the effect of the sale on the accounting equation?" 答案BA. "assets increase $75,000; owner's equity increases $75,000"B. "assets increase $55,000; owner's equity increases $55,000"C. "assets increase $75,000; liabilities decrease $20,000; owner's equity increases $55,000"D. "assets increase $20,000; no change for liabilities; owner's equity increases $75,000"29.Which of the following entries records the payment of an account payable? 答案 DA. debit Cash; credit Accounts PayableB. debit Accounts Receivable; credit CashC. debit Cash; credit Supplies ExpenseD. debit Accounts Payable; credit CashChap 3 –a2.Which one of the following is a purpose of the ledger rather than a purpose of the journal?答案 AA. to show increases and decreases in accountsB. to show a chronological order for transactionsC. to show a complete transaction in one placeD. to help locate errors10.The accounting entry to record the purchase of office supplies for cash will not involve an expense account. 对14.The process of transferring the data from the journal to the ledger accounts is posting. 对20.Posting a transaction twice will not cause the trial balance totals to be unequal.对21.Journalizing a transaction with both the debit and the credit for $69 instead of $96 will cause the trial balance to be out of balance. 错23."The total number at the bottom of the trial balance should equal to the total number at the bottom of the balance sheet, because they both show the equality of the accounting equation." 错24.(mark out all correct answers) The credit column of a T/B might include _______ accounts。

财务英语资产负债表Balance Sheet一、资产ASSETS流动资产: CURRENT ASSETS货币资金Cash and cash equivalents交易性金融资产Financial assets held for trading应收票据Notes receivable应收账款Accounts receivable减:坏帐准备Less:Provision for bad debts预付款项Advances to suppliers应收利息Interests receivable应收股利Dividends receivable其他应收款Other receivables存货Inventories其中:原材料Including:Raw materials库存成品及商品Inventory of finished goods低值易耗品Consumbles一年内到期的非流动资产Non-current assets maturing/due within one year 其他流动资产Other current assets流动资产合计TOTAL CURRENT ASSETS非流动资产:NON-CURRENT ASSETS可供出售金融资产Available-for-sale financial assets持有至到期投资Held-to-maturity investments长期应收款Long-term receivables长期股权投资long-term equity investments投资性房地产Investment real estate固定资产(固定资产原价)Fixed assets(Original value of fixed assets)减:累计折旧Less:Accumulated depreciation固定资产净值Fixed assets-net value减:固定资产减值准备Reserve for fixed assets impairment固定资产净额Net fixed assets在建工程Construction in progress工程物资Project materials固定资产清理Disposal of fixed assets生产性生物资产Productive biological assets油气资产Oil and natural gas assets无形资产Intangible assets开发支出Development costs商誉Goodwill长期待摊费用Long-term deferred expenses递延所得税资产Deferred income tax assets其他非流动资产Other non-current assets非流动资产合计TOTAL NON-CURRENT ASSETS资产总计TOTAL ASSETS二、负债LIABILITIES流动负债:CURRENT LIABILITIES短期借款Short-term borrowings交易性金融负债Financial assets held for liabilities应付票据Notes payable应付账款Accounts payable预收款项Payments received in advance应付职工薪酬Employee benefits payable/Staff remuneration payables应交税费Taxes and surcharges payable应付利息Interests payable应付股利Dividends payable其他应付款Other payables一年内到期的非流动负债Non-current liabilities maturing within one year其他流动负债Other current liabilities流动负债合计TOTAL CURRENT LIABILITIES非流动负债:NON-CURRENT LIABILITIES长期借款Long-term borrowings应付债券Debt securities issued长期应付款Long-term payables专项应付款Specific item payable预计负债Provisions for liabilities递延所得税负债Deferred income tax liabilities其他非流动负债Other non-current liabilities非流动负债合计TOTAL NON-CURRENT LIABILITIES负债合计TOTAL LIABILITIES三、所有者权益(或股东权益):OWNERS' EQUITY (or shareholders' equity)实收资本(或股本)Paid-up capital (or share capital)其中:国家资本National capital 集体资本Collateral capital 法人资本Legal person's capital个人资本Personal capital外商资本Foreign capital资本公积Capital reserves减:库存股Treasury stock盈余公积Surplus reserves未分配利润Retained earnings/Undistributed profit所有者权益(或股东权益)合计TOTAL OWNERS' EQUITY (OR SHAREHOLDERS' EQUITY)负债和所有者权益(或股东权益)总计TOTAL LIABILITIES AND OWNERS' EQUITY 利润表Income Statement一、营业总收入Overall sales/Overall income营业收入Including: Sales/Income from operations/Income from operations其中:主营业务收入Sales/Income from main business/Income from main business 其他业务收入Sales/Income from other business/Income from other business利息收入Interests income已赚保费Insurance premiums earned手续费及佣金收入Handling charges and commissions income二、营业总成本Overall costs营业成本Including: Costs of operations其中:主营业务成本Costs of main business其他业务成本Costs of other business利息支出Interests expenses手续费及佣金支出Handling charges and commissions expenses退保金Refund of insurance premiums赔付支出净额Net payments for insurance claims提取保险合同准备金净额Net provision for insurance contracts保单红利支出Commissions on insurance policies分保费用Cession charges营业税金及附加Taxes and surcharges on operations销售费用Selling and distribution expenses管理费用General and administrative expenses其中:业务招待费Entertainment expenses/Business entertainment研究与开发费Research and development costs财务费用Financial expenses其中:利息支出Interests expenses利息收入Interests income汇兑净损失Foreign exchange net loss资产减值损失Impairment loss on assets加:公允价值变动收益(损失以“-”号填列)Plus: Gain or loss from changes in fair values 投资收益(损失以“-”号填列)Investment income其中:对联营企业和合营企业的投资收益Including: Investment income from joint ventures and affiliates汇兑收益(损失以“-”号填列)Gain or loss on foreign exchange transactions三、营业利润(亏损以“-”号填列)Profit from operations加:营业外收入Plus: Non-operating profit其中:非流动资产处置利得Gain from disposal of non-current assets非货币性资产交换利得Gain from exchange of non-monetary assets 政府补助Governmental subsidy债务重组利得Gain of debt restructuring减:营业外支出Less: Non-operating expenses其中:非流动资产处置损失Loss from disposal of non-current assets非货币性资产交换损失Loss from exchange of non-monetary assets债务重组损失Loss of debt restructuring四、利润总额(亏损总额以“-”号填列)Profit before tax加:应弥补亏损Loss to cover减:所得税费用Less: Income tax expenses五、净利润(净亏损以“-”号填列)Net profit其中:被合并方在合并前实现的净利润Among which: Net profit recognized before the merger归属于母公司所有者的净利润Net profit attributable to shareholders of parent company 少数股东损益Minority interest income六、每股收益:Earnings per share (EPS)基本每股收益Basic EPS稀释每股收益Diluted EPS七、其他综合收益Other comprehensive income八、综合收益总额Total comprehensive income归属于母公司所有者的综合收益总额Total comprehensive income attributable to shareholders of parent company归属于少数股东的综合收益总额Total comprehensive income attributable to minority shareholders现金流量表Statement of cash flows一、经营活动产生的现金流量Cash flows from operating activities销售商品、提供劳务收到的现金Cash received from the sales of goods and the rendering of services客户存款和同业存放款项净增加额Net increase in deposits from customers and placements from corporations in the same industry向中央银行借款净增加额Net increase in loan from central bank向其他金融机构拆入资金净增加额Net increase in funds borrowed from other financial institutions收到原保险合同保费取得的现金Cash premiums received on original insurance contracts 收到再保险业务现金净额Cash received from re-insurance business保户储金及投资款净增加额Net increase in deposits and investments from insurers处置交易性金融资产净增加额Net increase in disposal of trading financial assets收取利息、手续费及佣金的现金Interest, handling charges and commissions received 拆入资金净增加额Net increase in funds deposit回购业务资金净增加额Net increase in repurchasement business funds收到的税费返还Receipts of tax refunds收到其他与经营活动有关的现金Other cash received relating to operating activities其中:企业内部银行收到的现金Including: Cash received by in-house bank经营活动现金流入小计Sub-total of cash inflows from operating activities购买商品、接受劳务支付的现金Cash payments for goods purchased and services received客户贷款及垫款净增加额Net increase in loans and payments on behalf存放中央银行和同业款项净增加额Net increase in deposits with centre bank and interbank支付原保险合同赔付款项的现金Payments of claims for original insurance contracts支付利息、手续费及佣金的现金Interests, handling charges and commissions paid支付保单红利的现金Commissions on insurance policies paid支付给职工以及为职工支付的现金Cash payments to and on behalf of employees支付的各项税费Payments of all types of taxes支付其他与经营活动有关的现金Other cash payments relating to operating activities经营活动现金流出小计Sub-total of cash outflows from operating activities经营活动产生的现金流量净额Net cash flows from operating activities二、投资活动产生的现金流量:Cash flows from investing activities收回投资收到的现金Cash received from disposals and withdraw on investment取得投资收益收到的现金Cash received from returns on investments处置固定资产、无形资产和其他长期资产收回的现金净额Net cash received from disposals of fixed assets, intangible assets and other long-term assets处置子公司及其他营业单位收到的现金净额Net cash received from disposals of subsidiaries and other business units收到其他与投资活动有关的现金Other cash received relating to investing activities投资活动现金流入小计Sub-total of cash inflows from investing activities购建固定资产、无形资产和其他长期资产支付的现金Cash payments to acquire and construct fixed assets, intangible assets and other long-term assets投资支付的现金Cash payments to acquire investments质押贷款净增加额Net increase in secured loans取得子公司及其他营业单位支付的现金净额Net cash payments for acquisitions of subsidiaries and other business units支付的其他与投资活动有关的现金Other cash payments relating to investing activities 投资活动现金流出小计Sub-total of cash outflows from investing activities投资活动产生的现金流量净额Net cash flows from investing activities三、筹资活动产生的现金流量Cash flows from financing activities吸收投资所收到的现金Cash received from investors in making investment in the enterprise其中:子公司吸收少数股东投资收到的现金Including:Cash received from issuing shares of minority shareholders取得借款所收到的现金Cash received from borrowings发行债券收到的现金Proceeds from issuance of bonds收到的其他与筹资活动有关的现金Other cash received relating to financing activities 筹资活动现金流入小计Sub-total of cash outflows from financing activities偿还债务所支付的现金Cash repayments of amounts borrowed分配股利、利润或偿付利息所支付的现金Cash payments for distribution of dividends or profits, or cash payments for interest expenses其中:子公司支付给少数股东的股利、利润Including: Subsidiary companies pay cash to minority shareholders for interest expenses and distribution of dividends or profit 支付的其他与筹资活动有关的现金Other cash payments relating to financing activities 筹资活动现金流出小计Sub-total of cash outflows from financing activities筹资活动产生的现金流量净额Net cash flows from financing activities四、汇率变动对现金及现金等价物的影响Effect of foreign exchange rate changes on cash and cash equivalents五、现金及现金等价物净增加额Net increase in cash and cash equivalents加:期初现金及现金等价物余额Plus:Cash and cash equivalents at beginning of period 六、期末现金及现金等价物余额Cash and cash equivalents at end of period本月实际Actual for this month去年同期The corresponding period of last year本年累计Accumulative total for this year行次Line金额Amount项目Item。

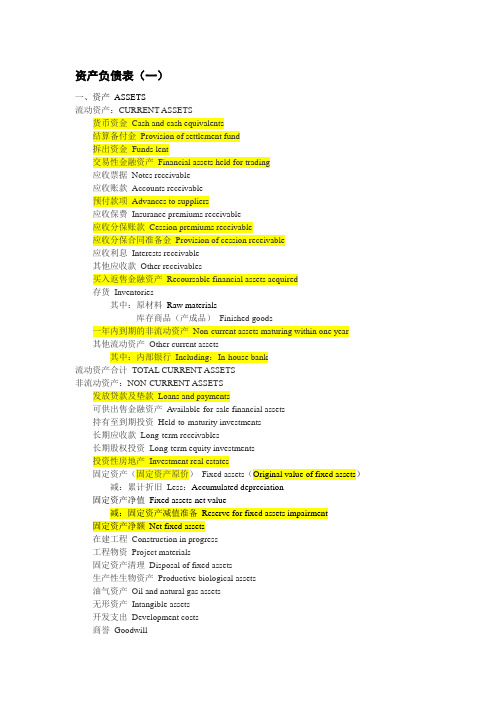

资产负债表(一)一、资产ASSETS流动资产:CURRENT ASSETS货币资金Cash and cash equivalents结算备付金Provision of settlement fund拆出资金Funds lent交易性金融资产Financial assets held for trading应收票据Notes receivable应收账款Accounts receivable预付款项Advances to suppliers应收保费Insurance premiums receivable应收分保账款Cession premiums receivable应收分保合同准备金Provision of cession receivable应收利息Interests receivable其他应收款Other receivables买入返售金融资产Recoursable financial assets acquired存货Inventories其中:原材料Raw materials库存商品(产成品)Finished goods一年内到期的非流动资产Non-current assets maturing within one year其他流动资产Other current assets其中:内部银行Including:In-house bank流动资产合计TOTAL CURRENT ASSETS非流动资产:NON-CURRENT ASSETS发放贷款及垫款Loans and payments可供出售金融资产Available-for-sale financial assets持有至到期投资Held-to-maturity investments长期应收款Long-term receivables长期股权投资Long-term equity investments投资性房地产Investment real estates固定资产(固定资产原价)Fixed assets(Original value of fixed assets)减:累计折旧Less:Accumulated depreciation固定资产净值Fixed assets-net value减:固定资产减值准备Reserve for fixed assets impairment 固定资产净额Net fixed assets在建工程Construction in progress工程物资Project materials固定资产清理Disposal of fixed assets生产性生物资产Productive biological assets油气资产Oil and natural gas assets无形资产Intangible assets开发支出Development costs商誉Goodwill长期待摊费用Long-term deferred expenses递延所得税资产Deferred income tax assets其他非流动资产Other non-current assets其中:特准储备物资Including:Physical assets reserve specifically authorized非流动资产合计TOTAL NON-CURRENT ASSETS资产总计TOTAL ASSETS二、负债LIABILITIES流动负债:CURRENT LIABILITIES短期借款Short-term borrowings向中央银行借款Borrowings from central bank吸收存款及同业存放Deposits from customers and interbank拆入资金Deposit funds交易性金融负债Financial assets held for liabilities应付票据Notes payable应付账款Accounts payable预收款项Payments received in advance卖出回购金融资产款Funds from sales of financial assets with repurchasement agreement 应付手续费及佣金Handling charges and commissions payable应付职工薪酬Employee benefits payable其中:应付工资Including:Wages payable应付福利费Welfare payable其中:职工奖励及福利基Including:Bonus and welfare fund for staff and workers应交税费Taxes and surcharges payable其中:应交税金Including:Taxes payable应付利息Interests payable应付股利Dividends payable其他应付款Other payables应付分保账款Cession insurance premiums payable保险合同准备金Provision for insurance contracts代理买卖证券款Funds received as agent of stock exchange代理承销证券款Funds received as stock underwrite一年内到期的非流动负债Non-current liabilities maturing within one year其他流动负债Other current liabilities其中:内部银行Including:In-house bank流动负债合计TOTAL CURRENT LIABILITIES非流动负债:NON-CURRENT LIABILITIES长期借款Long-term borrowings应付债券Debt securities issued长期应付款Long-term payables专项应付款Specific item payable预计负债Estimated Liabilities递延所得税负债Deferred tax liabilities其他非流动负债Other non-current liabilities其中:特准储备基金Including:Authorized reserve fund非流动负债合计TOTAL NON-CURRENT LIABILITIES负债合计TOTAL LIABILITIES三、所有者权益(或股东权益):OWNERS' EQUITY(or shareholders' equity)实收资本(或股本)Paid-up capital(or share capital)国家资本National capital集体资本Collective capital法人资本Legal person’s capital其中:国有法人资本State-owned legal person's capital集体法人资本Collective legal person's capital个人资本Personal capital外商资本Foreign capital减:已归还投资Less:Investment returned实收资本净额Net paid-up capital资本公积Capital reserves减:库存股Treasury stock专项储备Special reserves盈余公积Surplus reserves其中:法定公积金Statutory surplus reserve任意公积金Other surplus reserve储备基金Reserve fund企业发展基金Enterprise expansion fund利润归还投资Profits capitalized on return of investment一般风险准备Provision for normal risks未分配利润Retained earnings/Undistributed profits外币报表折算差额Exchange differences on translating foreign operations归属于母公司所有者权益合计Total equity attributable to the shareholders of parent companyTotal equity attributable to the shareholders of parent company少数股东权益Minority shareholders' equity (B/S)所有者权益合计TOTAL OWNERS' EQUITY负债和所有者权益总计TOTAL LIABILITIES AND OWNERS' EQUITY资产负债表(二)一、资产ASSETS流动资产: CURRENT ASSETS货币资金Cash and cash equivalents交易性金融资产Financial assets held for trading应收票据Notes receivable应收账款Accounts receivable减:坏帐准备Less:Provision for bad debts预付款项Advances to suppliers应收股利Dividends receivable其他应收款Other receivables存货Inventories其中:原材料Including:Raw materials库存成品及商品Inventory of finished goods低值易耗品Consumbles一年内到期的非流动资产Non-current assets maturing/due within one year 其他流动资产Other current assets流动资产合计TOTAL CURRENT ASSETS非流动资产:NON-CURRENT ASSETS可供出售金融资产Available-for-sale financial assets持有至到期投资Held-to-maturity investments长期应收款Long-term receivables长期股权投资long-term equity investments投资性房地产Investment real estate固定资产(固定资产原价)Fixed assets(Original value of fixed assets)减:累计折旧Less:Accumulated depreciation固定资产净值Fixed assets-net value减:固定资产减值准备Reserve for fixed assets impairment 固定资产净额Net fixed assets在建工程Construction in progress工程物资Project materials固定资产清理Disposal of fixed assets生产性生物资产Productive biological assets油气资产Oil and natural gas assets无形资产Intangible assets开发支出Development costs商誉Goodwill长期待摊费用Long-term deferred expenses递延所得税资产Deferred income tax assets其他非流动资产Other non-current assets非流动资产合计TOTAL NON-CURRENT ASSETS资产总计TOTAL ASSETS二、负债LIABILITIES流动负债:CURRENT LIABILITIES短期借款Short-term borrowings交易性金融负债Financial assets held for liabilities应付票据Notes payable应付账款Accounts payable预收款项Payments received in advance应付职工薪酬Employee benefits payable/Staff remuneration payables应交税费Taxes and surcharges payable应付股利Dividends payable其他应付款Other payables一年内到期的非流动负债Non-current liabilities maturing within one year其他流动负债Other current liabilities流动负债合计TOTAL CURRENT LIABILITIES非流动负债:NON-CURRENT LIABILITIES长期借款Long-term borrowings应付债券Debt securities issued长期应付款Long-term payables专项应付款Specific item payable预计负债Provisions for liabilities递延所得税负债Deferred income tax liabilities其他非流动负债Other non-current liabilities非流动负债合计TOTAL NON-CURRENT LIABILITIES负债合计TOTAL LIABILITIES三、所有者权益(或股东权益):OWNERS' EQUITY (or shareholders' equity)实收资本(或股本)Paid-up capital (or share capital)其中:国家资本National capital集体资本Collateral capital法人资本Legal person's capital个人资本Personal capital外商资本Foreign capital资本公积Capital reserves减:库存股Treasury stock盈余公积Surplus reserves未分配利润Retained earnings/Undistributed profit所有者权益(或股东权益)合计TOTAL OWNERS' EQUITY (OR SHAREHOLDERS' EQUITY)负债和所有者权益(或股东权益)总计TOTAL LIABILITIES AND OWNERS' EQUITY利润表一、营业总收入Overall sales/Overall income其中:营业收入Including: Sales/Income from operations/Income from operations 其中:主营业务收入Sales/Income from main business/Income from main business 其他业务收入Sales/Income from other business/Income from other business 利息收入Interests income已赚保费Insurance premiums earned手续费及佣金收入Handling charges and commissions income二、营业总成本Overall costs其中:营业成本Including: Costs of operations其中:主营业务成本Costs of main business其他业务成本Costs of other business利息支出Interests expenses手续费及佣金支出Handling charges and commissions expenses退保金Refund of insurance premiums赔付支出净额Net payments for insurance claims提取保险合同准备金净额Net provision for insurance contracts保单红利支出Commissions on insurance policies分保费用Cession charges营业税金及附加Taxes and surcharges on operations销售费用Selling and distribution expenses管理费用General and administrative expenses其中:业务招待费Entertainment expenses/Business entertainment研究与开发费Research and development costs财务费用Financial expenses其中:利息支出Interests expenses利息收入Interests income汇兑净损失Foreign exchange net loss资产减值损失Impairment loss on assets加:公允价值变动收益(损失以“-”号填列)Plus: Gain or loss from changes in fair values 投资收益(损失以“-”号填列)Investment income其中:对联营企业和合营企业的投资收益Including: Investment income from joint ventures and affiliates汇兑收益(损失以“-”号填列)Gain or loss on foreign exchange transactions三、营业利润(亏损以“-”号填列)Profit from operations加:营业外收入Plus: Non-operating profit其中:非流动资产处置利得Gain from disposal of non-current assets非货币性资产交换利得Gain from exchange of non-monetary assets政府补助Governmental subsidy债务重组利得Gain of debt restructuring减:营业外支出Less: Non-operating expenses其中:非流动资产处置损失Loss from disposal of non-current assets非货币性资产交换损失Loss from exchange of non-monetary assets债务重组损失Loss of debt restructuring四、利润总额(亏损总额以“-”号填列)Profit before tax加:应弥补亏损Loss to cover减:所得税费用Less: Income tax expenses五、净利润(净亏损以“-”号填列)Net profit其中:被合并方在合并前实现的净利润Among which: Net profit recognized before the merger归属于母公司所有者的净利润Net profit attributable to shareholders of parent company 少数股东损益Minority interest income六、每股收益:Earnings per share (EPS)基本每股收益Basic EPS稀释每股收益Diluted EPS七、其他综合收益Other comprehensive income八、综合收益总额Total comprehensive income归属于母公司所有者的综合收益总额Total comprehensive income attributable to shareholders of parent company归属于少数股东的综合收益总额Total comprehensive income attributable to minority shareholders现金流量表(都要校对一下)一、经营活动产生的现金流量Cash flows from operating activities销售商品、提供劳务收到的现金Cash received from the sales of goods and the rendering of services客户存款和同业存放款项净增加额Net increase in deposits from customers and placements from corporations in the same industry向中央银行借款净增加额Net increase in loan from central bank向其他金融机构拆入资金净增加额Net increase in funds borrowed from other financial institutions收到原保险合同保费取得的现金Cash premiums received on original insurance contracts收到再保险业务现金净额Cash received from re-insurance business保户储金及投资款净增加额Net increase in deposits and investments from insurers处置交易性金融资产净增加额Net increase in disposal of trading financial assets收取利息、手续费及佣金的现金Interest, handling charges and commissions received拆入资金净增加额Net increase in funds deposit回购业务资金净增加额Net increase in repurchasement business funds收到的税费返还Receipts of tax refunds收到其他与经营活动有关的现金Other cash received relating to operating activities 其中:企业内部银行收到的现金Including: Cash received by in-house bank经营活动现金流入小计Sub-total of cash inflows from operating activities购买商品、接受劳务支付的现金Cash payments for goods purchased and services received客户贷款及垫款净增加额Net increase in loans and payments on behalf存放中央银行和同业款项净增加额Net increase in deposits with centre bank and interbank支付原保险合同赔付款项的现金Payments of claims for original insurance contracts支付利息、手续费及佣金的现金Interests, handling charges and commissions paid支付保单红利的现金Commissions on insurance policies paid支付给职工以及为职工支付的现金Cash payments to and on behalf of employees支付的各项税费Payments of all types of taxes支付其他与经营活动有关的现金Other cash payments relating to operating activities经营活动现金流出小计Sub-total of cash outflows from operating activities经营活动产生的现金流量净额Net cash flows from operating activities二、投资活动产生的现金流量:Cash flows from investing activities收回投资收到的现金Cash received from disposals and withdraw on investment取得投资收益收到的现金Cash received from returns on investments处置固定资产、无形资产和其他长期资产收回的现金净额Net cash received from disposals of fixed assets, intangible assets and other long-term assets处置子公司及其他营业单位收到的现金净额Net cash received from disposals of subsidiariesand other business units收到其他与投资活动有关的现金Other cash received relating to investing activities投资活动现金流入小计Sub-total of cash inflows from investing activities购建固定资产、无形资产和其他长期资产支付的现金Cash payments to acquire and construct fixed assets, intangible assets and other long-term assets投资支付的现金Cash payments to acquire investments质押贷款净增加额Net increase in secured loans取得子公司及其他营业单位支付的现金净额Net cash payments for acquisitions of subsidiaries and other business units支付的其他与投资活动有关的现金Other cash payments relating to investing activities投资活动现金流出小计Sub-total of cash outflows from investing activities投资活动产生的现金流量净额Net cash flows from investing activities三、筹资活动产生的现金流量Cash flows from financing activities吸收投资所收到的现金Cash received from investors in making investment in the enterprise其中:子公司吸收少数股东投资收到的现金Including:Cash received from issuing shares of minority shareholders取得借款所收到的现金Cash received from borrowings发行债券收到的现金Proceeds from issuance of bonds收到的其他与筹资活动有关的现金Other cash received relating to financing activities筹资活动现金流入小计Sub-total of cash outflows from financing activities偿还债务所支付的现金Cash repayments of amounts borrowed分配股利、利润或偿付利息所支付的现金Cash payments for distribution of dividends or profits, or cash payments for interest expenses其中:子公司支付给少数股东的股利、利润Including: Subsidiary companies pay cash to minority shareholders for interest expenses and distribution of dividends or profit支付的其他与筹资活动有关的现金Other cash payments relating to financing activities筹资活动现金流出小计Sub-total of cash outflows from financing activities筹资活动产生的现金流量净额Net cash flows from financing activities四、汇率变动对现金及现金等价物的影响Effect of foreign exchange rate changes on cash and cash equivalents五、现金及现金等价物净增加额Net increase in cash and cash equivalents加:期初现金及现金等价物余额Plus:Cash and cash equivalents at beginning of period六、期末现金及现金等价物余额Cash and cash equivalents at end of period本月实际Actual for this month去年同期The corresponding period of last year本年累计Accumulative total for this year行次Line金额Amount项目Item。

Debugging and Profiling in Microsoft VisualStudio with Parallel NsightNVIDIA Parallel Nsight™Visual Studio integrated development for GPU and CPUProfileDebugNVIDIA Parallel Nsight for Graphics & Compute Graphics Inspector ✓Real-time inspection of Direct3D API calls Investigate GPU pipeline state ✓See contributing fragments with PixelHistory ✓Profile frames to find GPU bottlenecks System Analysis ✓View CPU & GPU events on a single timeline Examine workload dependencies ✓CUDA, Direct3D, and OpenGL API Trace ✓Profile CUDA kernels using performance counters Free License!CUDA/Graphics Debugger ✓GPU Accelerated CUDA and HLSLdebugging✓Examine shaders executing in parallel ✓Identify issues with conditionalbreakpointsParallel Nsight for Compute Developers“With the advent of Parallel Nsight and CUDA support for debugging, the [CUDA] development process now more closely resembles that of traditional parallel CPU code”Jacques du T oit – Scientific ComputingCUDA Build System▪Visual Studio 2008 SP1 and 2010 SP1▪CUDA project wizard▪Project setting extensions▪Visual C++ and .NET project integrationParallel Nsight CUDA Debugging▪Native GPU debugging with mixed CUDA-C/PTX/SASS assembly ▪Debugger attach to running process▪Conditional breakpoint with program variables▪GPU memory views and data breakpoints▪CUDA expression engine and stack frame support▪Massively-threaded GPU kernels navigation▪CUDA memory checker▪CUDA system informationParallel Nsight CUDA Profiling▪CUDA profiler with live counter reconfiguration▪Unlimited experiments on live kernels▪Advanced profiling experiments•Achieved occupancy•Instruction throughput▪Kernel profiling filteringFully Featured Configurations… Remote PC 2 GPUs Tesla + GPU ✓ Application and system trace ✓ CUDA profiling ✓ CUDA debugger✓ CUDA memory checker✓ WDDM driver✓ Tesla Compute Cluster driver Multi-OSPartially Featured Configuration…Single GPU ✓ Application and system trace ✓ CUDA profiling✓ WDDM driverNew in Parallel Nsight 2.1CUDA Toolkit 4.1 supportSupport for CUDA C/C++ debugging on OptimusNew CUDA and system information pageCUDA parallel warp watch viewGPU break on assertDebugging asynchronous kernel launchesNew CUDA profiling experimentsFlow control efficiency and branch divergenceMemory coalescing and cache efficiencyStatistics on issue dependencies and stall reasons OpenCL 1.1 API trace supportAvailable Q4 2011 RC2 available now!CUDA info page CUDA warp watch viewDemo – CUDA▪Similar experience as CPU debugging ▪Debug the ‘parallel’▪PTX/SASS▪Memory - PTX/SASSDemo – CUDA TraceDemo – CUDA ProfilingHow can I learn more about Parallel Nsight?▪Download—/▪Parallel Nsight documentation—Start → All Programs → NVIDIA Parallel Nsight 2.1 → User Guide▪Parallel Nsight instruction videos—/object/gtc-express-webinar.html▪CUDA books and references—Programming Massively Parallel Processors—CUDA by Example。

The Evolution and Impact of the Tram inUrban TransportationThe tram, a symbol of urban progress and modernization, has undergone significant changes throughout its history. Originating in the 19th century, the tram revolutionized urban transportation by providing an efficient and cost-effective mode of transport for commuters. Fast-forward to the 21st century, and the tram has not only retained its relevance but has also evolved to embrace modern technology, becoming a crucial component of sustainable urban transport systems.The earliest trams were steam-powered and operated on rails laid specifically for their use. These trams wereslow and noisy, but they were a vast improvement over the horse-drawn carriages that preceded them. As technology progressed, electric trams became the norm, offering a cleaner and quieter mode of transportation. Electric trams were powered by overhead wires, eliminating the need for noisy and polluting steam engines.Today, the tram has further evolved to incorporate modern technology. Many cities have invested in light railsystems, which offer a blend of tram and subway-style transportation. These systems often feature air-conditioned cars, GPS tracking, and real-time passenger information displays. In addition, some cities have even experimented with tram systems that run on batteries, further reducing their environmental impact.The impact of the tram on urban transportation cannot be overstated. Trams provide a reliable and efficient mode of transport for thousands of commuters daily. They offer a cost-effective alternative to private vehicles, reducing congestion and air pollution. Furthermore, trams encourage community development by connecting different parts of the city, fostering economic growth and cultural exchange.However, the success of the tram depends on several factors, including the quality of the infrastructure, the efficiency of the service, and the willingness of thepublic to use it. Poorly maintained tracks or infrequent services can lead to a decline in ridership, rendering the tram system ineffective. Therefore, it is crucial forcities to invest in their tram systems, ensuring they are well-maintained and offer a reliable service.In conclusion, the tram has played a pivotal role in urban transportation for over a century. Its evolution from steam-powered carriages to modern light rail systems has seen it adapt to the changing needs of cities, becoming a crucial component of sustainable urban transport systems.As technology continues to advance, the tram is poised to play an even more significant role in shaping the future of urban transportation.**电车在城市交通中的演变与影响**电车,作为城市进步与现代化的象征,在其历史长河中经历了显著的变化。

英文会计报表编辑锁定FINANCIAL REPORT COVER报表所属期间之期末时间点 Period Ended所属月份 Reporting Period报出日期 Submit Date记账本位币币种 Local Reporting Currency审核人 Verifier填表人 Preparer中文名英文会计报表外文名FINANCIAL REPORT COVER所属月份Reporting Period报出日期Submit Date审核人Verifier目录1. 1 资产负债表2. 2 损益表3. 3 流量表英文会计报表资产负债表编辑Balance Sheet资产 Assets流动资产 Current Assets货币资金 Bank and Cash短期投资 Current Investment一年内到期委托贷款 Entrusted loan receivable due within one year减:一年内到期委托贷款减值准备 Less: Impairment for Entrusted loan receivable due within one 减:短期投资跌价准备 Less: Impairment for current investment短期投资净额 Net bal of current investment应收票据 Notes receivable应收股利 Dividend receivable应收利息 Interest receivable应收账款 Account receivable减:应收账款坏账准备 Less: Bad debt provision for Account receivable应收账款净额 Net bal of Account receivable其他应收款 Other receivable减:其他应收款坏账准备 Less: Bad debt provision for Other receivable其他应收款净额 Net bal of Other receivable预付账款 Prepayment应收补贴款 Subsidy receivable存货 Inventory减:存货跌价准备 Less: Provision for Inventory存货净额 Net bal of Inventory已完工尚未结算款 Amount due from customer for contract work待摊费用 Deferred Expense一年内到期的长期债权投资 Long-term debt investment due within one year一年内到期的应收融资租赁款 Finance lease receivables due within one year 其他流动资产 Other current assets流动资产合计 Total current assets长期投资 Long-term investment长期股权投资 Long-term equity investment委托贷款 Entrusted loan receivable长期债权投资 Long-term debt investment长期投资合计 Total for long-term investment减:长期股权投资减值准备 Less: Impairment for long-term equity investment 减:长期债权投资减值准备 Less: Impairment for long-term debt investment 减:委托贷款减值准备 Less: Provision for entrusted loan receivable长期投资净额 Net bal of long-term investment其中:合并价差 Include: Goodwill (Negative goodwill)固定资产 Fixed assets固定资产原值 Cost减:累计折旧 Less: Accumulated Depreciation固定资产净值 Net bal减:固定资产减值准备 Less: Impairment for fixed assets固定资产净额 NBV of fixed assets工程物资 Material holds for construction of fixed assets在建工程 Construction in progress减:在建工程减值准备 Less: Impairment for construction in progress在建工程净额 Net bal of construction in progress固定资产清理 Fixed assets to be disposed of固定资产合计 Total fixed assets无形资产及其他资产 Other assets & Intangible assets无形资产 Intangible assets减:无形资产减值准备 Less: Impairment for intangible assets无形资产净额 Net bal of intangible assets长期待摊费用 Long-term deferred expense融资租赁——未担保余值 Finance lease – Unguaranteed residual values融资租赁——应收融资租赁款 Finance lease – Receivables其他长期资产 Other non-current assets无形及其他长期资产合计 Total other assets & intangible assets递延税项 Deferred Tax递延税款借项 Deferred Tax assets资产总计 Total assets负债及所有者(或股东)权益 Liability & Equity流动负债 Current liability短期借款 Short-term loans应付票据 Notes payable应付账款 Accounts payable已结算尚未完工款预收账款 Advance from customers应付工资 Payroll payable应付福利费 Welfare payable应付股利 Dividend payable应交税金 Taxes payable其他应交款 Other fees payable其他应付款 Other payable预提费用 Accrued Expense预计负债 Provision递延收益 Deferred Revenue一年内到期的长期负债 Long-term liability due within one year其他流动负债 Other current liability流动负债合计 Total current liability长期负债 Long-term liability长期借款 Long-term loans应付债券 Bonds payable长期应付款 Long-term payable专项应付款 Grants & Subsidies received其他长期负债 Other long-term liability长期负债合计 Total long-term liability递延税项 Deferred Tax递延税款贷项 Deferred Tax liabilities负债合计 Total liability少数股东权益 Minority interests所有者权益(或股东权益) Owners’ Equity实收资本(或股本) Paid in capital减;已归还投资 Less: Capital redemption实收资本(或股本)净额 Net bal of Paid in capital资本公积 Capital Reserves盈余公积 Surplus Reserves其中:法定公益金 Include: Statutory reserves未确认投资损失 Unrealised investment losses未分配利润 Retained profits after appropriation其中:本年利润 Include: Profits for the year外币报表折算差额 Translation reserve所有者(或股东)权益合计 Total Equity负债及所有者(或股东)权益合计 Total Liability & Equity英文会计报表损益表编辑Income statement and profit appropriation一、主营业务收入 Revenue减:主营业务成本 Less: Cost of Sales主营业务税金及附加 Sales Tax二、主营业务利润(亏损以“—”填列) Gross Profit ( - means loss)加:其他业务收入 Add: Other operating income减:其他业务支出 Less: Other operating expense减:营业费用 Selling & Distribution expense管理费用 G&A expense财务费用 Finance expense三、营业利润(亏损以“—”填列) Profit from operation ( - means loss)加:投资收益(亏损以―—‖填列) Add: Investment income补贴收入 Subsidy Income营业外收入 Non-operating income减:营业外支出 Less: Non-operating expense四、利润总额(亏损总额以“—”填列) Profit before Tax减:所得税 Less: Income tax少数股东损益 Minority interest加:未确认投资损失 Add: Unrealised investment losses五、净利润(净亏损以―—‖填列) Net profit ( - means loss)加:年初未分配利润 Add: Retained profits其他转入 Other transfer-in六、可供分配的利润 Profit available for distribution( - means loss)减:提取法定盈余公积 Less: Appropriation of statutory surplus reserves提取法定公益金 Appropriation of statutory welfare fund提取职工奖励及福利基金 Appropriation of staff incentive and welfare fund提取储备基金 Appropriation of reserve fund提取企业发展基金 Appropriation of enterprise expansion fund利润归还投资 Capital redemption七、可供投资者分配的利润 Profit available for owners' distribution减:应付优先股股利 Less: Appropriation of preference share's dividend提取任意盈余公积 Appropriation of discretionary surplus reserve应付普通股股利 Appropriation of ordinary share's dividend转作资本(或股本)的普通股股利 Transfer from ordinary share's dividend to paid in capital八、未分配利润 Retained profit after appropriation补充资料: Supplementary Information:1.出售、处置部门或被投资单位收益 Gains on disposal of operating divisions or investments2.自然灾害发生损失 Losses from natural disaster3.会计政策变更增加(或减少)利润总额 Increase (decrease) in profit due to changes in accounting 4. 会计估计变更增加(或减少)利润总额 Increase (decrease) in profit due to changes in accou5. 债务重组损失 Losses from debt restructuring英文会计报表流量表编辑Cash Flow Statement一、经营活动产生的现金流量: Cash Flow from Operating Activities:销售商品、提供劳务收到的现金 Cash received from sales of goods or rendering services收到的税费返还 Refunds of taxes收到的其他与经营活动有关的现金 Cash received relating to other operating activities现金流入小计 Sub-total of cash inflows购买商品、接受劳务支付的现金 Cash paid for goods or receiving services支付给职工以及为职工支付的现金 Cash paid to and on behalf of employees支付的各项税费 Tax payments支付的其他与经营活动有关的现金 Cash paid relating to other operating activities现金流出小计 Sub-total of cash outflows经营活动产生的现金流量净额 Net Cash Flow from Operating Activities二、投资活动产生的现金流量: Cash Flow from Investing Activities:收回投资所收到的现金 Cash received from disposal of investments处置子公司和其他经营单位收到的现金 Cash received from disposal of subsidiary or other operating bu 取得投资收益所收到的现金 Cash received from investments income处置固定资产、无形资产和其他长期资产而收到的现金净额 Net cash received from disposal of fixed as 购买子公司所收到的现金 Cash received by acquisition of subsidiary收到的其他与投资活动有关的现金 Cash received relating to other investing activities现金流入小计 Sub-total of cash inflows购建固定资产、无形资产和其他长期资产所支付的现金 Cash paid to acquire fixed assets, intangible as 投资所支付的现金 Cash paid to acquire investments支付的其他与投资活动有关的现金 Cash payments relating to other investing activities现金流出小计 Sub-total of cash outflows投资活动产生的现金流量净额 Net Cash Flow from Investing Activities三、筹资活动产生的现金流量: Cash Flow from Financing Activities:吸收投资所收到的现金 Cash received by investors借款所收到的现金 Cash received from borrowings其中:从金融机构借款所收到的现金 Include: Cash received from financial institution borrowings收到的其他与筹资活动有关的现金 Cash received relating to other financing activities现金流入小计 Sub-total of cash inflows偿还债务所支付的现金 Repayments of borrowings其中:偿还金融机构债务所支付的现金 Include: Repayments of financial institution borrowings分配股利、利润和偿付利息所支付的现金 Dividends paid, profit distributed or interest paid支付的其他与筹资活动有关的现金 Cash payments relating to other financing activities现金流出小计 Sub-total of cash outflows筹资活动产生的现金流量净额 Net Cash Flow from Financing Activities四、汇率变动对现金的影响额 Effect of Foreign Currency Translation五、现金及现金等价物净增加额 Net Increase (Decrease) in Cash and Cash Equivalents现金流量附表: Supplementary Information:1.将净利润调节为经营活动的现金流量: Reconciliation of Net Profit to Cash Flow from Operatin净利润 Net Profit加:少数股东损益 Add: Minority interest加:计提的资产减值准备 Impairment losses on assets固定资产折旧 Depreciation of fixed assets无形资产摊销 Amortisation of intangible assets长期待摊费用摊销 Amortisation of long-term deferred expenses待摊费用减少(减:增加) Decrease (increase) in deferred expenses预提费用增加(减:减少) Increase (decrease) in accrued expenses处置固定资产、无形资产和其他长期资产的损失(减、收益) Losses (gains) on disposal of fixed a固定资产报废损失 Losses on write-off of fixed assets财务费用 Finance expense (income)投资损失(减、收益) Losses (gains) arising from investments递延税款贷款(减、借项) Deferred tax credit (debit)存货的减少(减、增加) Decrease (increase) in inventories经营性应收项目的减少(减、增加) Decrease (increase) in receivables under operating activities经营性应付项目的增加(减、减少) Increase (decrease) in payables under operating activities其他 Others经营活动产生的现金流量净额 Net cash flow from operating activities2.不涉及现金收支的投资和筹资活动: Investing and Financing Activities that do not Involve Cash Rece 债务转为资本 Conversion of debt into capital一年内到期的可转换公司债券 Reclassification of convertible bonds expiring within one year as融资租入固定资产 Fixed assets acquired under finance leases3.现金及现金等价物净增加情况: Net Increase in Cash and Cash Equivalents:现金的期末余额 Cash at the end of the period减:现金的期初余额 Less: cash at the beginning of the year加:现金等价物的期末余额 Add: cash equivalents at the end of the period减:现金等价物的期初余额 Less: cash equivalents at the beginning of the period现金及现金等价物净增加额 Net increase in cash and cash equivalentsn one yearnvestmentsnges in accounting policiesaccounting estimatesr other operating business unitsdisposal of fixed assets, intangible assets and other long-term assets ssets, intangible assets and other long-term assetsn borrowingsborrowingsrating Activities:xed assets, intangible assets and other long-term assetsivitiesng activitiest Involve Cash Receipts and Payments:ar as current liability。

完整英文版资产负债表、利润表及现金流量表Balance Sheet 资产负债表ITEM项目Cash 货币资金Short term investments短期投资Notes receivable 应收票据Dividend receivable应收股利Interest receivable应收利息Accounts receivable 应收帐款Other receivables 其他应收款Accounts prepaid预付帐款Future guarantee 期货保证金Allowance receivable 应收补贴款Export drawback receivable应收出口退税Inventories存货Including: Raw materials其中:原材料Finished goods 产成品(库存商品)Prepaid and deferred expenses 待摊费用Unsettled G/L on current assets 待处理流动资产净损失Long-term debenture investment falling due in a year 一年内到期的长期债权投资Other current assets其他流动资产Total current assets 流动资产合计Long-term investment:长期投资:Including long term equity investment 其中:长期股权投资Long term securities investment 长期债权投资Incorporating price difference*合并价差Total long-term investment 长期投资合计Fixed assets-cost 固定资产原价Less: Accumulated Depreciation减:累计折旧Fixed assets-net value 固定资产净值Less: Impairment of fixed assets 减:固定资产减值准备Net value of fixed assets固定资产净额Disposal of fixed assets 固定资产清理Project material 工程物资Construction in Progress在建工程Unsettled G/L on fixed assets 待处理固定资产净损失Total tangible assets 固定资产合计Intangible assets 无形资产Including and use rights 其中:土地使用权Deferred assets 递延资产(长期待摊费用)Including: Fixed assets repair其中:固定资产修理Improvement expenditure of fixed assets固定资产改良支出Other long term assets 其他长期资产Among it: Specially approved reserving materials 其中:特准储备物资Total intangible assets and other assets 无形及其他资产合计Deferred assets debits递延税款借项Total Assets 资产总计Balance Sheet 资产负债表(续表)ITEM 项目Short-term loans短期借款Notes payable 应付票款Accounts payab1e 应付帐款Advances from customers预收帐款Accrued wages 应付工资Welfare payable 应付福利费Profits payable应付利润(股利)Taxes payable应交税金Other payable to government其他应交款Other creditors 其他应付款Provision for expenses预提费用Accrued liabilities 预计负债Long term liabilities due within one year 一年内到期的长期负债Other current liabilities 其他流动负债Total current liabilities 流动负债合计Long-term loans payable长期借款Bonds payable 应付债券long-term accounts payable 长期应付款Special accounts payable专项应付款Other long-term liabilities 其他长期负债Including: Special reserve fund 其中:特准储备资金Total long term liabilities 长期负债合计Deferred taxation credit 递延税款贷项Total liabilities 负债合计Minority interests * 少数股东权益Subscribed Capital 实收资本(股本)National capital 国家资本Collective capital 集体资本/ entity capital法人资本Legal person’sIncluding: State-owned legal person’s capital 其中:国有法人资本Collective legal person’s capital集体法人资本Personal capital 个人资本Foreign businessmen’s capital 外商资本Capital surplus 资本公积surplus reserve 盈余公积Including: statutory surplus reserve 其中:法定盈余公积public welfare fund 公益金Supplermentary current capital 补充流动资本Unaffirmed investment loss* 未确认的投资损失(以“-”号填列)Retained earnings 未分配利润Converted difference in Foreign Currency Statements 外币报表折算差额Total shareholder’s equity 所有者权益合计Total Liabilities & Equity 负债及所有者权益总计INCOME STATEMENT 利润表ITEMS 项目Sales of products 产品销售收入Including:Export sales 其中:出口产品销售收入Less:Sales discount and allowances 减:销售折扣与折让Net sales of products 产品销售净额Less:Sales tax 减:产品销售税金Cost of sales产品销售成本Including:Cost of export sales其中:出口产品销售成本Gross profit on sales产品销售毛利Less:Selling expenses 减:销售费用General and administrative expenses管理费用Financial expenses 财务费用Including:Interest expenses (minus interest income) 其中:利息支出(减利息收入)Exchange losses(minus exchange gains) 汇兑损失(减汇兑收益)Profit on sales 产品销售利润Add:profit from other operations加:其他业务利润Operating profit营业利润Add:Income on investment 加:投资收益Add:Non-operating income 加:营业外收入Less:Non-operating expenses 减:营业外支出Add:adjustment of loss and gain for previous years加:以前年度损益调整Total profit利润总额Less:Income tax 减:所得税Net profit 净利润Cash Flows Statement 现金流量表Prepared by:Period: Unit: 拟制人:时间:单位:Items 项目1.Cash Flows from Operating Activities: cash流量从经营活动:01)Cash received from sales of goods or rendering of services 所收到的现金从销售货物或提供劳务02)Rental received收到的租金Value added tax on sales received and refunds of value增值税销售额收到退款的价值03)added tax paid 增值税缴纳04)Refund of other taxes and levy other than value added tax退回的其他税收和征费以外的增值税07)Other cash received relating to operating activities其他现金收到有关经营活动08)Sub-total of cash inflows 分,总现金流入量09)Cash paid for goods and services 用现金支付的商品和服务10)Cash paid for operating leases 用现金支付经营租赁11)Cash paid to and on behalf of employees 用现金支付,并代表员工12)Value added tax on purchases paid 增值税购货支付13)Income tax paid 所得税的缴纳14)Taxes paid other than value added tax and income tax 支付的税款以外的增值税和所得税17)Other cash paid relating to operating activities其他现金支付有关的经营活动18)Sub-total of cash outflows 分,总的现金流出19)Net cash flows from operating activities净经营活动的现金流量2.Cash Flows from Investing Activities: 所收到的现金收回投资20)Cash received from return of investments 所收到的现金从分配股利,利润21)Cash received from distribution of dividends or profits所收到的现金从国债利息收入22)Cash received from bond interest income 现金净额收到的处置固定资产,无形资产流向与投资活Net cash received from disposal of fixed assets, intangible cash动23)assets and other long-term assets 资产和其他长期资产26)Other cash received relating to investing activities其他收到的现金与投资活动27)Sub-total of cash inflows小计的现金流入量Cash paid to acquire fixed assets, i ntangible assets 用现金支付购建固定资产,无形资产28)and other long-term assets 和其他长期资产29)Cash paid to acquire equity investments用现金支付,以获取股权投资30)Cash paid to acquire debt investments 用现金支付收购债权投资33)Other cash paid relating to investing activities 其他现金支付的有关投资活动34)Sub-total of cash outflows 分,总的现金流出35)Net cash flows from investing activities投资活动产生的净现金流量,3.Cash Flows from Financing Activities:cash流量筹资活动:36)Proceeds from issuing shares从发行股票的收益,37)Proceeds from issuing bonds 由发行债券的收益,38)Proceeds from borrowings 由借款的收益,41)Other proceeds relating to financing activities 其他收益有关的融资活动42)Sub-total of cash inflows 小计的现金流入量43)Cash repayments of amounts borrowed的现金偿还债务所支付的44)Cash payments of expenses on any financing activities 对任何融资活动现金支付的费用,45)Cash payments for distribution of dividends or profits分配股利或利润支付现金,46)Cash payments of interest expenses 以现金支付的利息费用47)Cash payments for finance leases融资租赁以现金支付,48)Cash payments for reduction of registered capital减少注册资本以现金支付,51)Other cash payments relating to financing activities其他现金收支有关的融资活动52)Sub-total of cash outflows 分,总的现金流出53)Net cash flows from financing activities 从融资活动的净现金流量4.Effect of Foreign Exchange Rate Changes on Cash effect的外汇汇率变动对现金 Increase in Cash and Cash Equivalents net增加现金和现金等价物Supplemental Information补充资料1.Investing and Financing Activities that do not Involve inCash Receipts and Payments 不参与现金收款和付款的投资活动和筹资活动56)Repayment of debts by the transfer of fixed assets偿还债务的转让固定资产57)Repayment of debts by the transfer of investments偿还债务的转移投资58)Investments in the form of fixed assets投资在形成固定资产59)Repayments of debts by the transfer of inventories偿还债务的转移库存量2.Reconciliation of Net Profit to Cash Flows from Operating Activities 调整的净利润现金流量从经营活动62)Net profit 净利润63)Add provision for bad debt or bad debt written off补充规定的坏帐或不良债务注销64)Depreciation of fixed assets固定资产折旧65)Amortization of intangible assets 无形资产摊销损失处置固定资产,无形Losses on disposal of fixed assets, intangible assets资产66)and other long-term assets (or deduct: gains) 和其他长期资产(或减:收益)67)Losses on scrapping of fixed assets 损失固定资产报废68)Financial expenses 财务费用69)Losses arising from investments (or deduct: gains) 引起的损失由投资管理(或减:收益)70)Defered tax credit (or deduct: debit) defered税收抵免(或减:借记卡)71)Decrease in inventories (or deduct:increase) 减少存货(或减:增加)72)Decrease in operating receivables (or deduct: increase) 减少经营性应收(或减:增加)73)Increase in operating payables (or deduct: decrease)增加的经营应付账款(或减:减少)74)Net payment on value added tax (or deduct: net receipts净支付的增值税(或减:收益净额75)Net cash flows from operating activities净经营活动的现金流量 Increase in Cash and Cash Equivalents net增加现金和现金等价物76)cash at the end of the period 在此期限结束的现金,77)Less: cash at the beginning of the period 减:现金期开始78)Plus: cash equivalents at the end of the period加:现金等价物在此期限结束79)Less: cash equivalents at the beginning of the period 减:现金等价物期开始80)Net increase in cash and cash equivalents 净增加现金和现金等价物一、资产类Assets流动资产Current assets货币资金Cash and cash equivalents现金Cash银行存款Cash in bank其他货币资金Other cash and cash equivalents外埠存款Other city Cash in bank银行本票Cashier's cheque银行汇票Bank draft信用卡Credit card信用证保证金L/C Guarantee deposits存出投资款Refundable deposits短期投资Short-term investments股票Short-term investments - stock债券Short-term investments - corporate bonds基金Short-term investments - corporate funds其他Short-term investments - other短期投资跌价准备Short-term investments falling price reserves应收款Account receivable应收票据Note receivable银行承兑汇票Bank acceptance商业承兑汇票Trade acceptance应收股利Dividend receivable应收利息Interest receivable应收账款Account receivable其他应收款Other notes receivable坏账准备Bad debt reserves预付账款Advance money应收补贴款Cover deficit by state subsidies of receivable库存资产Inventories物资采购Supplies purchasing原材料Raw materials包装物Wrappage低值易耗品Low-value consumption goods材料成本差异Materials cost variance自制半成品Semi-Finished goods库存商品Finished goods商品进销差价Differences between purchasing and selling price委托加工物资Work in process - outsourced委托代销商品Trust to and sell the goods on a commission basis受托代销商品Commissioned and sell the goods on a commission basis 存货跌价准备Inventory falling price reserves分期收款发出商品Collect money and send out the goods by stages待摊费用Deferred and prepaid expenses长期投资Long-term investment长期股权投资Long-term investment on stocks股票投资Investment on stocks其他股权投资Other investment on stocks长期债权投资Long-term investment on bonds债券投资Investment on bonds其他债权投资Other investment on bonds长期投资减值准备Long-term investments depreciation reserves股权投资减值准备Stock rights investment depreciation reserves债权投资减值准备Bcreditor's rights investment depreciation reserves委托贷款Entrust loans本金Principal利息Interest减值准备Depreciation reserves固定资产Fixed assets房屋Building建筑物Structure机器设备Machinery equipment运输设备Transportation facilities工具器具Instruments and implement累计折旧Accumulated depreciation固定资产减值准备Fixed assets depreciation reserves房屋、建筑物减值准备Building/structure depreciation reserves机器设备减值准备Machinery equipment depreciation reserves工程物资Project goods and material专用材料Special-purpose material专用设备Special-purpose equipment预付大型设备款Prepayments for equipment为生产准备的工具及器具Preparative instruments and implement for fabricate 在建工程Construction-in-process安装工程Erection works在安装设备Erecting equipment-in-process技术改造工程Technical innovation project大修理工程General overhaul project在建工程减值准备Construction-in-process depreciation reserves固定资产清理Liquidation of fixed assets无形资产Intangible assets专利权Patents非专利技术Non-Patents商标权Trademarks, Trade names著作权Copyrights土地使用权Tenure商誉Goodwill无形资产减值准备Intangible Assets depreciation reserves专利权减值准备Patent rights depreciation reserves商标权减值准备trademark rights depreciation reserves未确认融资费用Unacknowledged financial charges待处理财产损溢Wait deal assets loss or income长期待摊费用Long-term deferred and prepaid expenses待处理财产损溢Wait deal assets loss or income待处理流动资产损溢Wait deal intangible assets loss or income待处理固定资产损溢Wait deal fixed assets loss or income二、负债类Liability短期负债Current liability短期借款Short-term borrowing应付票据Notes payable银行承兑汇票Bank acceptance商业承兑汇票Trade acceptance应付账款Account payable预收账款Deposit received代销商品款Proxy sale goods revenue应付工资Accrued wages应付福利费Accrued welfarism应付股利Dividends payable应交税金Tax payable应交增值税value added tax payable进项税额Withholdings on VAT已交税金Paying tax转出未交增值税Unpaid VAT changeover减免税款Tax deduction销项税额Substituted money on V AT出口退税Tax reimbursement for export进项税额转出Changeover withnoldings on V AT出口抵减内销产品应纳税额Export deduct domestic sales goods tax转出多交增值税Overpaid V AT changeover未交增值税Unpaid V AT应交营业税Business tax payable应交消费税Consumption tax payable应交资源税Resources tax payable应交所得税Income tax payable应交土地增值税Increment tax on land value payable应交城市维护建设税Tax for maintaining and building cities payable应交房产税Housing property tax payable应交土地使用税Tenure tax payable应交车船使用税Vehicle and vessel usage license plate tax(VVULPT) payable应交个人所得税Personal income tax payable其他应交款Other fund in conformity with paying其他应付款Other payables预提费用Drawing expense in advance其他负债Other liabilities待转资产价值Pending changerover assets value预计负债Anticipation liabilities长期负债Long-term Liabilities长期借款Long-term loans一年内到期的长期借款Long-term loans due within one year一年后到期的长期借款Long-term loans due over one year应付债券Bonds payable债券面值Face value, Par value债券溢价Premium on bonds债券折价Discount on bonds应计利息Accrued interest长期应付款Long-term account payable应付融资租赁款Accrued financial lease outlay一年内到期的长期应付Long-term account payable due within one year 一年后到期的长期应付Long-term account payable over one year专项应付款Special payable一年内到期的专项应付Long-term special payable due within one year 一年后到期的专项应付Long-term special payable over one year递延税款Deferral taxes三、所有者权益类OWNERS' EQUITY资本Capita实收资本(或股本) Paid-up capital(or stock)实收资本Paicl-up capital实收股本Paid-up stock已归还投资Investment Returned公积资本公积Capital reserve资本(或股本)溢价Capital(or Stock) premium接受捐赠非现金资产准备Receive non-cash donate reserve股权投资准备Stock right investment reserves拨款转入Allocate sums changeover in外币资本折算差额Foreign currency capital其他资本公积Other capital reserve盈余公积Surplus reserves法定盈余公积Legal surplus任意盈余公积Free surplus reserves法定公益金Legal public welfare fund储备基金Reserve fund企业发展基金Enterprise expension fund利润归还投资Profits capitalizad on return of investment利润Profits本年利润Current year profits利润分配Profit distribution其他转入Other chengeover in提取法定盈余公积Withdrawal legal surplus提取法定公益金Withdrawal legal public welfare funds提取储备基金Withdrawal reserve fund提取企业发展基金Withdrawal reserve for business expansion提取职工奖励及福利基金Withdrawal staff and workers' bonus and welfare fund利润归还投资Profits capitalizad on return of investment应付优先股股利Preferred Stock dividends payable提取任意盈余公积Withdrawal other common accumulation fund应付普通股股利Common Stock dividends payable转作资本(或股本)的普通股股利Common Stock dividends change to assets(or stock)未分配利润Undistributed profit四、成本类Cost生产成本Cost of manufacture基本生产成本Base cost of manufacture辅助生产成本Auxiliary cost of manufacture制造费用Manufacturing overhead材料费Materials管理人员工资Executive Salaries奖金Wages退职金Retirement allowance补贴Bonus外保劳务费Outsourcing fee福利费Employee benefits/welfare会议费Coferemce加班餐费Special duties市内交通费Business traveling通讯费Correspondence电话费Correspondence水电取暖费Water and Steam税费Taxes and dues租赁费Rent管理费Maintenance车辆维护费Vehicles maintenance油料费Vehicles maintenance培训费Education and training接待费Entertainment图书、印刷费Books and printing运费Transpotation保险费Insurance premium支付手续费Commission杂费Sundry charges折旧费Depreciation expense机物料消耗Article of consumption劳动保护费Labor protection fees季节性停工损失Loss on seasonality cessation劳务成本Service costs五、损益类Profit and loss收入Income业务收入OPERATING INCOME主营业务收入Prime operating revenue产品销售收入Sales revenue服务收入Service revenue其他业务收入Other operating revenue材料销售Sales materials代购代售包装物出租Wrappage lease出让资产使用权收入Remise right of assets revenue返还所得税Reimbursement of income tax其他收入Other revenue投资收益Investment income短期投资收益Current investment income长期投资收益Long-term investment income计提的委托贷款减值准备Withdrawal of entrust loans reserves 补贴收入Subsidize revenue国家扶持补贴收入Subsidize revenue from country其他补贴收入Other subsidize revenue营业外收入NON-OPERATING INCOME非货币性交易收益Non-cash deal income现金溢余Cash overage处置固定资产净收益Net income on disposal of fixed assets 出售无形资产收益Income on sales of intangible assets固定资产盘盈Fixed assets inventory profit罚款净收入Net amercement income支出Outlay业务支出Revenue charges主营业务成本Operating costs产品销售成本Cost of goods sold服务成本Cost of service主营业务税金及附加Tax and associate charge营业税Sales tax消费税Consumption tax城市维护建设税Tax for maintaining and building cities资源税Resources tax土地增值税Increment tax on land value其他业务支出Other business expense销售其他材料成本Other cost of material sale其他劳务成本Other cost of service其他业务税金及附加费Other tax and associate charge费用Expenses营业费用Operating expenses代销手续费Consignment commission charge运杂费Transpotation保险费Insurance premium展览费Exhibition fees广告费Advertising fees管理费用Adminisstrative expenses职工工资Staff Salaries修理费Repair charge低值易耗摊销Article of consumption办公费Office allowance差旅费Travelling expense工会经费Labour union expenditure研究与开发费Research and development expense福利费Employee benefits/welfare职工教育经费Personnel education待业保险费Unemployment insurance劳动保险费Labour insurance医疗保险费Medical insurance会议费Coferemce聘请中介机构费Intermediary organs咨询费Consult fees诉讼费Legal cost业务招待费Business entertainment技术转让费Technology transfer fees矿产资源补偿费Mineral resources compensation fees排污费Pollution discharge fees房产税Housing property tax车船使用税Vehicle and vessel usage license plate tax(VVULPT) 土地使用税Tenure tax印花税Stamp tax财务费用Finance charge利息支出Interest exchange汇兑损失Foreign exchange loss各项手续费Charge for trouble各项专门借款费用Special-borrowing cost营业外支出Nonbusiness expenditure捐赠支出Donation outlay减值准备金Depreciation reserves非常损失Extraordinary loss处理固定资产净损失Net loss on disposal of fixed assets 出售无形资产损失Loss on sales of intangible assets固定资产盘亏Fixed assets inventory loss债务重组损失Loss on arrangement罚款支出Amercement outlay所得税Income tax以前年度损益调整Prior year income adjustment。

Retained Mode Parallel Rendering forScalable Tiled DisplaysTom van der Schaaf – Luc Renambot – Desmond Germans – Hans Spoelder – Henri Bal {tvdscha | renambot | bal}@cs.vu.nl{desmond | hs}@nat.vu.nlFaculty of Sciences - Vrije UniversiteitDe Boelelaan 1081, 1081 HV Amsterdam, The NetherlandsI IntroductionThe current trend in hardware for parallel graphics is to use clusters of off-the-shelf PCs instead of high-end super computers. This trend has emerged since the dramatic change in the price/performance ratio of today’s PCs. Using large, high-resolution displays is another trend that is currently emerging. High resolution allows for detailed scientific visualization, and overcomes the limited screen resolution of standard monitors. Large displays also have applications in teaching environments, where multiple people (small groups or full classroom) are looking at a single large screen.The goal of this project is to investigate the field of parallel rendering in the context of scalable tiled displays. A renderer calculates a 2D picture from a 3D model specified by the programmer. A parallel renderer uses multiple processors to calculate a single image. The target system for this parallel renderer is a so-called tiled display, a high-resolution screen. It consists of several projectors that compose a single, seamless image onto the screen. For this project, a cluster of off-the-shelf PCs with off-the-shelf video hardware does the rendering. These PCs control the projectors, and calculate the image in parallel. This work is based on the Aura API developed by the vrije Universiteit, Amsterdam. Aura is designed as a portable 3D graphics retained-mode layer for scientific visualization in virtual reality [8].The contributions of this paper are:• It presents a retained-mode API for 3D graphics, with a portable implementation across a variety of VR platforms (several operating systems and hardware environments),• Two different implementations of the API are presented, with different tradeoffs in scalability and performance,• It presents a preliminary performance study, with a focus on the network requirements of different benchmark applications.The rest of the paper is organized as follow. Section II discusses briefly the work that has been done already in the field of rendering and parallel rendering. Next, Section III describes the important issues in parallel rendering for tiled displays. Section IV introduces WireGL, as a possible choice of parallel rendering for tiled displays. Measurements on WireGL exposed a scalability problem, caused by the fact that WireGL is an immediate mode renderer. Therefore, two different renderers, called Aura ‘Broadcast’ and Aura ‘Multiple Copies’, have been designed using a different paradigm, called retained mode. Both are described in Section V. Using several benchmarks, we compare our implementations to WireGL in Section VI, showing that retained mode indeed allows for better scalability.WorkII RelatedParallel rendering adds processors to the calculation to achieve higher performances. In 1994, Molnar et al described a sorting classification for parallel rendering [3]. Three different types of sorting are proposed, based on where in the rendering pipeline sorting takes place. The three modes are sort-first, sort-middle and sort-last. However, adding computing power and graphic resources is generally used in two ways. The first option is to distribute all 3D objects over all processors, and then each object is rendered by one processor. The alternative is to split the screen into a number of tiles and to let each processor render all objects that have to be displayed onto that tile. This approach usually causes some objects to be rendered by multiple processors, because those objects intersect multiple tiles.Much work has been devoted to the field of parallel rendering. The full version of this paper discuss the advantages and drawbacks of several parallel rendering systems, among them: GLX [14], WireGL [2, 4, 5]from Stanford University, PGL (Parallel Graphics Library) [25] from NASA Institute for Computer Applications in Science and Engineering (ICASE), Parallel Mesa Library [26] from the University of New-York, the Power Wall [21] and the Infinity Wall [22], the Distributed Graphics Database (DGD) system by Ben Schaeffer of the University of Illinois [10], and finally the different systems proposed by Princeton University [20].III Parallel RenderingThis section discusses the general issues in parallel rendering. First the hardware is described to form the background of all that follows. Then three important design issues in parallel rendering are discussed.1 OverviewThe application (i.e. the program that uses the parallel renderer) runs on a single computer: the client. A fast network (e.g. Myrinet) connects the client to a cluster of computers: the servers or renderers. The servers are connected to a set of projectors; each server controls one projector. Every projector is responsible for ‘drawing’ a rectangular region of the screen (a projector-tile). Each server is responsible for assembling the final image of its projector and correcting the image for a seamless integration with its neighbors, and finally sending the image to the projector, as described Figure 1. The rendering of the image is done in parallel on all servers. The software layer correcting the images for a seamless projection is beyond the scope of this paper and consequently not addressed here.AURA ProgramHigh-speed network Image correction : color, geometry, seam ProjectorProjector ProjectorTile 1Tile 2Tile N Renderer Renderer RendererFigure 1, Parallel Rendering for Tiled DisplayThe following subsections contain the main implementation issues that have to be considered when building a parallel renderer.2 The Application Programming Interface (API)The interface of the graphics library is a critical issue. Ideally the interface is easy to use and flexible, allowing the programmer to use every feature of the underlying hardware efficiently. When making a choice for an interface, two options are possible: a new interface, designed specifically for the purpose of a tiled display, or an existing interface. The latter has the advantage that existing applications, for that API, can run on the tiled display without any changes to the source code. In fact, when using dynamic link libraries, no access to source code is necessary. The first option requires rewriting of all applications, to be used for the new API. Writing a new interface is, of course, much work, but allows the interface to be optimized for the target environment.3 CommunicationThere are two main ways of communication for a parallel renderer [10]. The first approach (let us call it ‘multiple copies’) replicates the application to all servers, with some frustum adjustments during rendering (see Figure 2, left). These adjustments are necessary to let every server draw only a sub-frustum to form a correct viewing volume. In order to be able to do interaction (keyboard, mouse, tracker, etc…) with the user and I/O, theclient must broadcast a message that informs the other applications of the event. This way assures that every server performs exactly the same actions. In addition, to prevent temporally misaligned images, the frames must be synchronized.Figure 2, The ‘Multiple Copies’ approach versus the ‘Broadcast’ ApproachThe other approach (‘broadcast’) has the application running only on the client. In this case, all graphics commands from the API are broadcast to all servers, instead of executed (see figure 2, right). Again, each server manages a sub-frustum. Synchronization between frames is needed. Although this approach is called broadcast here, it is not mandatory to use broadcast. Some objects could be sent only to those servers, which eventually draws it onto the screen. By clever use of bounding boxes, multicast, and normal point-to-point communication, it is possible to reduce the required bandwidth.The main advantage of the ‘multiple copies’ approach lies in the area of performance. Since there is hardly any communication necessary (only synchronization) it runs very fast. However, there is much redundancy; all servers perform the same actions. Also the scene graph (or all scene data if there is no graph) is replicated on all servers. Multiple copies approach might be the ideal solution, but it has two main drawbacks. The first is the fact that I/O can be a big problem. If the application requires data from a file or database, all servers require that information and all must read the file or database. It is clear that multiple accesses to the same database cause a scalability problem. A second problem is that this approach is not transparent. The application must use functions provided by the API for handling user interactions (mouse, keyboard, trackers) so that these can be transferred to the servers. Also, for other functions that require synchronization, like generating random numbers, the programmer must use functions provided by the API instead of his own. Lack of transparency, albeit very little, makes this approach unsuitable for existing APIs. ‘Broadcast’ has the advantage that all cluster-related issues can be hidden in the implementation of the interface. This complete transparency enables the implementation of an existing API. Furthermore, I/O is straightforward for the ‘Broadcast’ approach. Only one application is running; only one application reads files or databases. To the outside world, the application now behaves like an ordinary application on a single node. The disadvantage is performance. Because this approach requires graphics commands to be sent over the network, it potentially eats up much bandwidth. If the application is complex enough, available bandwidth becomes the limiting factor.Besides these two general approaches, there is also a lot to be developed on a lower level. Especially the broadcast approach requires a carefully designed communication protocol that minimizes communication overhead. Several strategies can be used for this, such as:− Fast compression and decompression of packets to send them in a smaller size.− Collapsing multiple packets into one, to prevent latency problems.− Preventing the sending of data to servers that do not need that data for displaying their part of the scene.− Choosing between function shipping and data shipping.4 ImplementationImplementation issues are described in the full paper.IV ExperimentsThis section compares the parallel renderers described Aura ‘multiple copies’ and Aura ‘broadcast’ to WireGL. First, it describes the programs used for testing. Then it discusses the results for some communication benchmark tests and the results for test with rendering.1 The Benchmark ProgramsThe comparisons between Aura and WireGL in this section are based on tests with three different demo programs. All three programs are original (optimized) OpenGL programs. For usage with WireGL, these programs remained unmodified. For Aura, the test programs were all almost completely rewritten. The output of the Aura programs is, however, identical to the output of their respective OpenGL/WireGL versions. The three demos are:• Fire: The fire program is a Glut demo. It displays a grass plain with a number of textured trees. In the center of this field, a ‘fire’ burns. The fire consists of a large number of triangles that fly through the air according to a complex formula.• Atlantis: It displays two whales and a dolphin swimming in circles in front of the camera. In the center of the screen, a number of sharks are swimming. Like the fire demo, Atlantis is an immediate-mode program. The objects (fire or sharks) are updated every frame.• Cube: It displays a large (≥ 1000) number of cubes that rotate as a whole in front of the camera. The Aura version of this program is completely retained mode. Because every cube has a different color and material it uses just as many different states as there are cubes. This proved to be a great performance hazard for the sequential Aura program.Each benchmark can be scaled to increase scene complexity. We tested each one in two configurations: light and heavy. Fire and Atlantis have been chosen for their immediate mode nature. They should prove that both Aura versions can handle immediate mode programs and that they do not perform much worse than WireGL. In addition, Fire serves as an example of a worst-case program for WireGL. Due to the unfortunate implementation of Fire, WireGL consumes high amounts of bandwidth. Cube serves as an example retained mode program. It is used to show that both Aura implementations perform much better than WireGL on this type of program. The results of the testing are in the next two subsections.Analysis2 CommunicationThe full paper presents a communication analysis for the described benchmarks, focusing on bandwidth requirements and scalability issues. This study is performed on a large-scale Myrinet PC cluster, without rendering.Analysis3 RenderingThe final paper will contain full results with rendering on a small-scale cluster of PCs, cluster designed dedicated for parallel rendering: high-performance dual-cpu nodes with NVIDIA GeForce3 graphics card.4 DiscussionThe full paper presents a detailed discussion on the presented rendered (‘multiple copies’ and ‘broadcast’) versus the well-known WireGL system. The analysis focuses on issues such as performance, scalability, required latency and bandwidth, and finally ease of programming.V ConclusionThis paper focuses on rendering for large tiled displays using an off-the-shelf cluster of PCs. The Stanford University parallel renderer WireGL is the leading renderer in the field. It has the advantage of compatibility with all existing OpenGL programs. However, its scalability is poor. The two Aura renderers presented in this paper try to solve this scalability problem, by using retained mode graphics instead of immediate mode graphics. Aura ‘Multiple Copies’ uses simple replication of the application and synchronization to achieve the best performance. Aura ‘Broadcast’ broadcasts scene data to co-operating PCs to achieve complete transparency. Tests regarding the communication requirements of WireGL and both Aura versions show that Aura ‘Multiple Copies’ has by far the fastest communication and the best scalability. Aura ‘Broadcast’, a more flexible and transparent renderer than Aura ‘Multiple Copies’, performs almost as good on real retained mode benchmarktests. On the more immediate mode oriented tests, it performs slightly worse than WireGL. Some optimizations to Aura ‘Broadcast’ can improve its performance.It has never been the purpose of this paper to show that Aura is ‘better’ than WireGL. It tries to show that there are alternatives. For OpenGL programs, WireGL is the way to go. However, if a new 3D-visualization program is designed to run on a parallel renderer, WireGL might not be the obvious choice. If performance is an issue, Aura (or any other immediate mode renderer) might be a better choice. Aura also has a simpler, more natural interface. The choice between Aura ‘Broadcast’ and Aura ‘Multiple Copies’ also requires some thought. If the program is to run on a cluster only and does not read large files or databases from a remote location, Aura ‘Multiple Copies’ is the best option. Otherwise, Aura ‘Broadcast’ performs better.References[1] Rudrajit Samanta, Jiannan Zheng, Thomas Funkhouser, Kai Li, and Jaswinder Pal Singh. Loadbalancing for multi-projector rendering systems. Proceedings of SIGGRAPH/Eurographics Workshop on Graphics Hardware, pages 107-116, August 1999.[2] Ian Buck, Greg Humphreys, and Pat Hanrahan. Tracking graphics state for networked rendering.Proceedings of SIGGRAPH/Eurographics Workshop on Graphics Hardware, August 2000.[3] Michael Cox, Steven Molnar, David Ellsworth, and Henry Fuchs. A sorting classification of parallelrendering. IEEE Computer Graphics and Algorithms, pages 23-32, July 1994.[4] Greg Humphreys and Pat Hanrahan. A distributed graphics system for large tiled displays. IEEEVisualization ’99, pages 215-224, October 1999.[5] Ian Buck, Greg Humphreys, Matthew Elldridge, and Pat Hanrahan. Distributed Rendering for scalableDisplays. SC2000: High Performance Networking and Computing, November 2000.[6] Rudrajit Samanta, Thomas Funkhouser, Kai Li, and Jaswinder Pal Singh. Hybrid Sort-First and Sort-Last Parallel Rendering with a Cluster of PCs. SIGGRAPH 2000.[7] Thomas W. Crockett. Parallel Rendering. NASA/ICASE Report, April 1995.[8] Desmond Germans, Hans J.W. Spoelder, Luc Renambot and Henri E. Bal. VIRPI: A High-LevelToolkit for Interactive Scientific Visualization in Virtual Reality. IPT/EGVE 2001, May 2001.[9] Rudrajit Samanta, Thomas Funkhouser and Kai Li. Parallel rendering with K-Way replication. IEEE2001 Symposium on Parallel Graphics, October 2001.[10] Ben Schaeffer. A Software System for inexpensive VR via Graphics Clusters. 2000./ClusteredVR/paper/DGDoverview.htm.[11] Mason Woo, OpenGL ARB, Jackie Neider, Tom Davis, Dave Shreiner. The OpenGL ProgrammingGuide, Third Edition. Addison-Wesley, 1999.Interactive Computer Graphics with OpenGL, Second Edition. Addison-Wesley, 2000.Angel.[12] E.[13] Mark Segal and Kurt Akeley. The OpenGL Graphics Interface: A Specification. 1993.[14] Phil Karlton. OpenGL Graphics with the X Window System (Version 1.2). Silicon Graphics. 1997./mjk_asd/glxspec/glxspec.html.Notes for a Computer Graphics Programming Course. In development for future Cunningham.[15] Stevepublication. California State University Stanislaus. 2001./~rsc/CS3600F00/FrontStuff.pdf.Computer Networks, Third Edition. Prentice-Hall, 1996.Tanenbaum.S.[16] AndrewParallel Computing - Theory and Practice, second edition. McGraw-Hill, 1994.[17] M.J.Quinn.[18] Foley, van Dam, Feiner and Hughes. Computer Graphics – Principles and Practice, Second Edition.Addison-Wesley, 1990.[19] Homan Igehy, Gordon Stoll and Pat Hanrahan. The design of a Parallel Graphics Interface. Proceedingsof SIGGRAPH ’98, pages 141-150, July 1998.[20] Yuqun Chen, Han Chen, Douglas W. Clark, Zhiyan Liu, Grant Wallace and Kai Li. SoftwareEnvironments for Cluster-based Display Systems. In FirstIEEE/ACM International Symposium on Cluster Computing and the Grid, May2001.[21] University of Minnesota. Power Wall. /research/powerwall/powerwall.html.[22] M. Czernuszenko, D. Pape, D. Sandin, T. DeFanti, G. Dawe and M. Brown. The ImmersaDesk andInfinity Wall projection-based virtual reality displays. In Computer Graphics, May 1997.[23] Carl Mueller. The sort-first rendering architecture for high-performance graphics. 1995 Symposium onInteractive 3D Graphics, pages 75-84, 1995.[24] Thomas W. Crockett. An introduction to parallel rendering. Parallel Computing, 23:819-843, 1997.[25] Thomas W. Crockett. PGM: A Parallel Graphics Library for Distributed Memory Applications./reports/interim/29/Abstract.html.[26] Tulika Mitra and Tzi-cker Chiueh. Implementation and Evaluation of the Parallel Mesa Library.Technical Report, State University of New York at Stony Brook, 1998.。