有关现值汉密尔顿函数的注解

- 格式:doc

- 大小:169.50 KB

- 文档页数:8

罗伯特·卢卡斯论经济增长的机制*1988I.作者简介罗伯特·卢卡斯(Robert E. Lucas, Jr.)1937年,卢卡斯生于华盛顿的雅奇马。

1955年,卢卡斯从西雅图的罗斯福公立学校高中毕业。

1959年,卢卡斯在芝加哥大学本科毕业,获得历史学学士学位。

于1964年获得芝加哥大学的经济学博士学位。

1963年,于卡内基工学院(现卡内基——梅隆大学)任教,在此期间,卢卡斯的经济动力学的全部观点逐渐成形。

卢卡斯于1970年完成、1972年发表代表作《预期和货币中性》,货币中性是他获得诺贝尔奖的演讲主题之一。

1974年卢卡斯回芝加哥教书。

1980年成为芝加哥的约翰·杜威有优异贡献教授。

1995年卢卡斯以其对“理性预期假说的应用和发展”所作的贡献而获得了诺贝尔经济学奖。

卢卡斯首要的理论贡献是开创并领导一个新的宏观经济学派——理性预期学派(又称新古典宏观经济学派),倡导和发展了理性预期与宏观经济学研究的运用理论,深化了人们对经济政策的理解。

此外,他在经济周期理论、宏观经济模型构造、计量方法、动态经济分析以及国际资本流动分析等方面都做出了卓越的贡献。

主要著作有:《理性预期与经济计量实践》(Rational Expectations and Econometric Practice,与T.J.萨金特合著,University Minnesota Press,1981年)《经济周期理论研究》(Studies in Business-Cycle Theory, MIT Press,1981年)《经济周期模型》(Models of Business Cycles, Wiley-Blackwell, 1991年)《经济动态学中的递归法》(Recursive Methods in Economic Dynamics, Harvard University Press, 1989年)II.论著摘要罗伯特·卢卡斯创作了《论经济发展的机制》一文并于1988年发表于《货币经济学杂志》上,这被认为是他的人力资本内生增长理论的经典文章。

罗伯特·卢卡斯论经济增长的机制*1988I.作者简介罗伯特·卢卡斯(Robert E. Lucas, Jr.)1937年,卢卡斯生于华盛顿的雅奇马。

1955年,卢卡斯从西雅图的罗斯福公立学校高中毕业。

1959年,卢卡斯在芝加哥大学本科毕业,获得历史学学士学位。

于1964年获得芝加哥大学的经济学博士学位。

1963年,于卡内基工学院(现卡内基——梅隆大学)任教,在此期间,卢卡斯的经济动力学的全部观点逐渐成形。

卢卡斯于1970年完成、1972年发表代表作《预期和货币中性》,货币中性是他获得诺贝尔奖的演讲主题之一。

1974年卢卡斯回芝加哥教书。

1980年成为芝加哥的约翰·杜威有优异贡献教授。

1995年卢卡斯以其对“理性预期假说的应用和发展”所作的贡献而获得了诺贝尔经济学奖。

卢卡斯首要的理论贡献是开创并领导一个新的宏观经济学派——理性预期学派(又称新古典宏观经济学派),倡导和发展了理性预期与宏观经济学研究的运用理论,深化了人们对经济政策的理解。

此外,他在经济周期理论、宏观经济模型构造、计量方法、动态经济分析以及国际资本流动分析等方面都做出了卓越的贡献。

主要著作有:《理性预期与经济计量实践》(Rational Expectations and Econometric Practice,与T.J.萨金特合著,University Minnesota Press,1981年)《经济周期理论研究》(Studies in Business-Cycle Theory, MIT Press,1981年)《经济周期模型》(Models of Business Cycles, Wiley-Blackwell, 1991年)《经济动态学中的递归法》(Recursive Methods in Economic Dynamics, Harvard University Press, 1989年)II.论著摘要罗伯特·卢卡斯创作了《论经济发展的机制》一文并于1988年发表于《货币经济学杂志》上,这被认为是他的人力资本内生增长理论的经典文章。

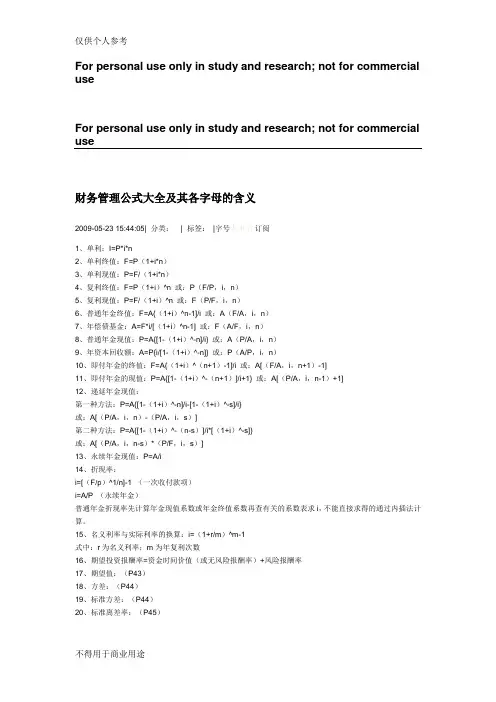

For personal use only in study and research; not for commercial useFor personal use only in study and research; not for commercial use财务管理公式大全及其各字母的含义2009-05-23 15:44:05| 分类:| 标签:|字号大中小订阅1、单利:I=P*i*n2、单利终值:F=P(1+i*n)3、单利现值:P=F/(1+i*n)4、复利终值:F=P(1+i)^n 或:P(F/P,i,n)5、复利现值:P=F/(1+i)^n 或:F(P/F,i,n)6、普通年金终值:F=A{(1+i)^n-1]/i 或:A(F/A,i,n)7、年偿债基金:A=F*i/[(1+i)^n-1] 或:F(A/F,i,n)8、普通年金现值:P=A{[1-(1+i)^-n]/i} 或:A(P/A,i,n)9、年资本回收额:A=P{i/[1-(1+i)^-n]} 或:P(A/P,i,n)10、即付年金的终值:F=A{(1+i)^(n+1)-1]/i 或:A[(F/A,i,n+1)-1]11、即付年金的现值:P=A{[1-(1+i)^-(n+1)]/i+1} 或:A[(P/A,i,n-1)+1]12、递延年金现值:第一种方法:P=A{[1-(1+i)^-n]/i-[1-(1+i)^-s]/i}或:A[(P/A,i,n)-(P/A,i,s)]第二种方法:P=A{[1-(1+i)^-(n-s)]/i*[(1+i)^-s]}或:A[(P/A,i,n-s)*(P/F,i,s)]13、永续年金现值:P=A/i14、折现率:i=[(F/p)^1/n]-1 (一次收付款项)i=A/P (永续年金)普通年金折现率先计算年金现值系数或年金终值系数再查有关的系数表求i,不能直接求得的通过内插法计算。

15、名义利率与实际利率的换算:i=(1+r/m)^m-1式中:r为名义利率;m为年复利次数16、期望投资报酬率=资金时间价值(或无风险报酬率)+风险报酬率17、期望值:(P43)18、方差:(P44)19、标准方差:(P44)20、标准离差率:(P45)21、外界资金的需求量=变动资产占基期销售额百分比x销售的变动额-变动负债占基期销售额百分比x销售的变动额-销售净利率x收益留存比率x预测期销售额22、外界资金的需求量的资金习性分析法:(P55)23、债券发行价格=票面金额x(P/F,i1,n)+票面金额x i2(P/A,i1,n)式中:i1为市场利率;i2为票面利率;n为债券期限如果是不计复利,到期一次还本付息的债券:债券发行价格=票面金额x(1+ i2 x n )x (P/F,i1,n)24、放弃现金折扣的成本=CD/(1-CD)x 360/N x 100%式中:CD为现金折扣的百分比;N为失去现金折扣延期付款天数,等于信用期与折扣期之差25、债券成本:Kb=I(1-T)/B0(1-f)=B*i*(1-T)/B0(1-f)式中:Kb为债券成本;I为债券每年支付的利息;T为所得税税率;B为债券面值;i为债券票面利率;B0为债券筹资额,按发行价格确定;f为债券筹资费率26、银行借款成本:Ki=I(1-T)/L(1-f)=i*L*(1-T)/L(1-f)或:Ki=i(1-T)(当f忽略不计时)式中:Ki为银行借款成本;I为银行借款年利息;L为银行借款筹资总额;T为所得税税率;i为银行借款利息率;f为银行借款筹资费率27、优先股成本:Kp=D/P0(1-T)式中:Kp为优先股成本;D为优先股每年的股利;P0为发行优先股总额28、普通股成本:Ks=[D1/V0(1-f)]+g式中:Ks为普通股成本;D1为第1年股的股利;V0为普通股发行价;g为年增长率29、留存收益成本:Ke=D1/V0+g30、加权平均资金成本:Kw=ΣWj*Kj式中:Kw为加权平均资金成本;Wj为第j种资金占总资金的比重;Kj为第j种资金的成本31、筹资总额分界点:BPi=TFi/Wi式中:BPi为筹资总额分界点;TFi为第i种筹资方式的成本分界点;Wi为目标资金结构中第i种筹资方式所占比例32、边际贡献:M=(p-b)x=m*x式中:M为边际贡献;p为销售单价;b为单位变动成本;m为单位边际贡献;x为产销量33、息税前利润:EBIT=(p-b)x-a=M-a34、经营杠杆:DOL=M/EBIT=M/(M-a)35、财务杠杆:DFL=EBIT/(EBIT-I)36、复合杠杆:DCL=DOL*DFL=M/[EBIT-I-d/(1-T)]37:每股利润无差异点分析公式:[(EBIT-I1)(1-T)-D1]/N1=[(EBIT-I2)(1-T)-D2]/N2当EBIT大于每股利润无差异点时,利用负债集资较为有利;当EBIT小于每股利润无差异点时,利用发行普通股集资较为有利38、经营期现金流量的计算:经营期某年净现金流量=该年利润+该年折旧+该年摊销+该年利息+该年回收额39、非折现评价指标:投资利润率=年平均利润额/投资总额x100%不包括建设期的投资回收期=原始投资额/投产若干年每年相等的现金净流量包括建设期的投资回收期=不包括建设期的投资回收期+建设期40、折现评价指标:净现值(NPV)=-原始投资额+投产后每年相等的净现金流量x年金现值系数净现值率(NPVR)=投资项目净现值/原始投资现值x100%获利指数(PI)=1+净现值率内部收益率=IRR(P/A,IRR,n)=I/NCF 式中:I为原始投资额41、短期证券收益率:K=(S1-S0+P)/S0*100%式中:K为短期证券收益率;S1为证券出售价格;S0为证券购买价格;P为证券投资报酬(股利或利息)42、长期债券收益率:V=I*(P/A,i,n)+F*(P/F,i,n)式中:V为债券的购买价格43、股票投资收益率:V=Σ(j=1~n)Di/(1+i)^j+F/(1+i)^n44、长期持有股票,股利稳定不变的股票估价模型:V=d/K式中:V为股票内在价值;d为每年固定股利;K为投资人要求的收益率45、长期持有股票,股利固定增长的股票估价模型:V=d0(1+g)/(K-g)=d1/(K-g)式中:d0为上年股利;d1为第一年股利46、证券投资组合的风险收益:Rp=βp*(Km - Rf)式中:Rp为证券组合的风险收益率;βp为证券组合的β系数;Km为所有股票的平均收益率,即市场收益率;Rf为无风险收益率47、机会成本=现金持有量x有价证券利率(或报酬率)48、现金管理相关总成本+持有机会成本+固定性转换成本49、最佳现金持有量:Q=(2TF/K)^1/2式中:Q为最佳现金持有量;T为一个周期内现金总需求量;F为每次转换有价证券的固定成本;K为有价证券利息率(固定成本)50、最低现金管理相关总成本:(TC)=(2TFK)^1/251、应收账款机会成本=维持赊销业务所需要的资金x资金成本率52、应收账款平均余额=年赊销额/360x平均收账天数53、维持赊销业务所需要的资金=应收账款平均余额x变动成本/销售收入54、应收账款收现保证率=(当期必要现金支出总额-当期其它稳定可靠的现金流入总额)/当期应收账款总计金额55、存货相关总成本=相关进货费用+相关存储成本=存货全年计划进货总量/每次进货批量x每次进货费用+每次进货批量/2 x 单位存货年存储成本56、经济进货批量:Q=(2AB/C)^1/2式中:Q为经济进货批量;A为某种存货年度计划进货总量;B为平均每次进货费用;C为单位存货年度单位储存成本57、经济进货批量的存货相关总成本:(TC)=(2ABC)^1/258、经济进货批量平均占用资金:W=PQ/2=P(AB/2C)^1/259、年度最佳进货批次:N=A/Q=(AC/2B)^1/260、允许缺货时的经济进货批量:Q=[(2AB/C)(C+R)/R]^1/2式中:S为缺货量;R为单位缺货成本61、缺货量:S=QC/(C+R)62、存货本量利的平衡关系:利润=毛利-固定存储费-销售税金及附加-每日变动存储费x储存天数63、每日变动存储费=购进批量x购进单价x日变动储存费率或:每日变动存储费=购进批量x购进单价x每日利率+每日保管费用64、保本储存天数=(毛利-固定存储费-销售税金及附加)/每日变动存储费65、目标利润=投资额x投资利润率66、保利储存天数=(毛利-固定存储费-销售税金及附加-目标利润)/每日变动存储费67、批进批出该商品实际获利额=每日变动储存费x(保本天数-实际储存天数)68、实际储存天数=保本储存天数-该批存货获利额/每日变动存储费69、批进零售经销某批存货预计可获利或亏损额=该批存货的每日变动存储费x[平均保本储存天数-(实际零售完天数+1)/2]=购进批量x购进单价x变动储存费率x[平均保本储存天数-(购进批量/日均销量+1)/2]=购进批量x单位存货的变动存储费x[平均保本储存天数-(购进批量/日均销量+1)/2]70、利润中心边际贡献总额=该利润中心销售收入总额-该利润中心可控成本总额(或:变动成本总额)71、利润中心负责人可控成本总额=该利润中心边际贡献总额-该利润中心负责人可控固定成本72、利润中心可控利润总额=该利润中心负责人可控利润总额-该利润中心负责人不可控固定成本73、公司利润总额=各利润中心可控利润总额之和-公司不可分摊的各种管理费用、财务费用等74、定基动态比率=分析期数值/固定基期数值75、环比动态比率=分析期数值/前期数值76、流动比率=流动资产/流动负债77、速动比率=速动资产/流动负债78、现金流动负债比率=年经营现金净流量/年末流动负债*100%79、资产负债率=负债总额/资产总额80、产权比率=负债总额/所有者权益81、已获利息倍数=息税前利润/利息支出82、长期资产适合率=(所有者权益+长期负债)/(固定资产+长期投资)83、劳动效率=主营业务收入或净产值/平均职工人数84、周转率(周转次数)=周转额/资产平均余额85、周转期(周转天数)=计算期天数/周转次数=资产平均余额x计算期天数/周转额86、应收账款周转率(次)=主营业务收入净额/平均应收账款余额其中:主营业务收入净额=主营业务收入-销售折扣与折让平均应收账款余额=(应收账款年初数+应收账款年末数)/2应收账款周转天数=(平均应收账款x360)/主营业务收入净额87、存货周转率(次数)=主营业务成本/平均存货其中:平均存货=(存货年初数+存货年末数)/2存货周转天数=(平均存货x360)/主营业务成本88、流动资产周转率(次数)=主营业务收入净额/平均流动资产总额其中:流动资产周转期(天数)=(平均流动资产周转总额x360)/主营业务收入总额89、固定资产周转率=主营业务收入净额/固定资产平均净值90、总资产周转率=主营业务收入净额/平均资产总额91、主营业务利润率=利润/主营业务收入净额92、成本费用利润率=利润/成本费用93、总资产报酬率=(利润总额+利息支出)/平均资产总额94、净资产收益率=净利润/平均净资产x100%95、资本保值增值率=扣除客观因素后的年末所有者权益/年初所有者权益96、社会积累率=上交国家财政总额/企业社会贡献总额上交的财政收入包括企业依法向财政交缴的各项税款。

第32卷第8期财经研究V o l.32N o.8 2006年8月Journal of Finance and Eco no mics A ug.2006 价格歧视下的不可再生资源的开采问题研究于 立,于 左,王建林(东北财经大学产业组织与企业组织研究中心,辽宁大连116025) 摘 要:自Ho te lling开始,不可再生资源开采问题引起了经济学家们的注意,在此过程中,产业组织理论被应用于不可再生资源的研究。

文章分析了价格歧视对不可再生资源开采的影响,结果发现,当资源的垄断开采者面向多个市场时,价格歧视因素可能使资源开采偏离最优路径。

关键词:不可再生资源;垄断;价格歧视;最优开采 中图分类号:F416.2 文献标识码:A文章编号:1001-9952(2006)08-0053-09一、引 言 不可再生资源(non-renewable resources)也称可耗竭资源,包括各种能源如石油、天然气、煤炭,以及非能源矿物质诸如铜、铁矿等,它们是经过数百万年的地质演变而形成的,储量固定不变,在某一时点上的任何使用都会减少后续时点可使用的数量。

对于这些可耗竭资源的一个核心问题是:何种开采方式才是最优的。

H otelling(1931)在其开创性论文中首次研究了这个问题,从而奠定了可耗竭资源经济学的基础。

H otelling认为资源的拥有者会把其资源看成是不断产生回报的资产,当资源价格上升幅度大于银行利率时,拥有者倾向于保留资源;当预计资源价格上升幅度低于银行利率时,拥有者倾向于尽快开采资源,而把卖资源所得的钱存入银行之中,自由竞争条件下的市场调节会使资源的价格以银行利率的速度增长,这就是著名的Hotelling定律。

尽管Hotelling模型看起来十分精美,但由于忽略了太多的因素,其结论与经验事实是不符合的,例如一百多年来能源价格并没有出现持续的增长。

为了更好地解释现实,后来的研究者不断引入各种因素,使用了不同的模型设定继续这个问题的研究。

第30卷 第2期运 筹 与 管 理Vol.30,No.22021年2月OPERATIONSRESEARCHANDMANAGEMENTSCIENCEFeb.2021收稿日期:2019 04 16基金项目:国家自然科学基金资助项目(71974091);湖南省社科成果评审委员会重大项目(XSP20ZDA007);湖南省哲学社会科学基金项目(18YBA368)作者简介:易永锡(1965 ),男,湖南湘潭人,博士,教授,研究方向为环境经济政策;程粟粟(1992 ),男,安徽蚌埠人,硕士研究生,研究方向为环境经济政策;傅春燕(1965 ),女,湖南湘潭人,副教授,研究方向为环境经济政策。

一个关于跨界污染控制的清洁技术创新微分博弈模型易永锡, 程粟粟, 傅春燕(南华大学经济管理与法学学院,湖南衡阳421001)摘 要:把清洁技术水平视为内生变量,构建了一个跨界污染的两国关于清洁技术创新微分博弈模型。

在该模型中,参与国可以通过清洁技术投资或者等待对方创新投资的溢出来提高清洁技术水平,且两国均有两个可以选择的战略,即合作战略和非合作战略。

研究的结果显示,技术外溢强度对参与国的技术投资和技术水平均有负向影响,相比不合作,跨界污染控制合作使各国以更低的代价获得更清洁的技术和更高的社会福利。

关键词:清洁技术;跨界污染;创新;微分博弈中图分类号:F272.3 文章标识码:A 文章编号:1007 3221(2021)02 0025 06 doi:10.12005/orms.2021.0037ADifferentialGameModelonCleanTechnologyInnovationforTransboundaryPollutionControlYIYong xi,CHENGSu su,FUChun yan(SchoolofEconomicManagementandLaw,UniversityofSouthChina,Hengyang421001,China)Abstract:Takingcleantechnologylevelsasanendogenousvariable,thispaperinvestigatesadifferentiagamebetweentwosymmetriccountriesforcleantechnologyinnovationwithtechnologyoverflow.Inthismodel,participatingcountriescanimprovethequalityofcleantechnologyintwoways———investingincleantechnologythem selvesorwaitingforthespilloverofinnovationinvestmentfromeachother.Strategicspacethetwocountriescanchooseincludesnon cooperativeandcooperativestrategies.Theresultsdemonstratethattheintensityoftechnologyspilloverhasanegativeimpactonparticipatingcountries’technologyinvestmentandtechnologylevel.Comparedwithnon cooperation,thecooperationoftransboundarypollutioncontrolenablescountriestoobtaincleanertechnologiesandhighersocialwelfareatalowercost.Keywords:cleantechnology;transboundarypollution;innovation;differentiagame0 引言由于污染物的跨界扩散,使得跨界污染控制成为了一个国际性的难题,引起了各国政府和有关国际机构的高度重视,也引起了学界的广泛关注[1]。

第29卷 第12期运 筹 与 管 理Vol.29,No.122020年12月OPERATIONSRESEARCHANDMANAGEMENTSCIENCEDec.2020收稿日期:2018 03 17基金项目:国家自然科学基金资助项目(71673041);教育部人文社会科学项目(15YJA790093,16YJC790112)作者简介:王磊宁(1987 ),男,陕西咸阳人,东北大学硕士,研究方向:产业政策;通讯作者:郑云虹(1966 ),女,博士,副教授,研究方向:资源与环境政策。

基于EPR政策的耐用品设计寿命的决策研究———从计划报废的视角王磊宁, 郑云虹, 赵瑞(东北大学工商管理学院,辽宁沈阳110167)摘 要:本文探究如何安排延伸生产者责任(EPR)政策从而避免耐用品像快消品一样在短期产生大量废弃物的问题。

文章在已有研究基础上,从计划报废的视角,构建了一个基于连续时间的动态耐用品模型,利用最优控制方法探究了集中式决策的最优结果和分散式决策的市场均衡,并基于二者的比较分析,揭示不同市场结构下EPR政策工具对生产者延长产品设计寿命的激励效果。

最后基于理论模型的分析过程,通过数值模拟和案例分析对研究结论进行验证。

研究表明,在市场完全竞争情形下,实施单一的庇古税或者仅通过押金返还制度既可以将产出调节至最优水平,也能为生产者提供足够的激励延长其产品的设计寿命;在市场不完全竞争情形下,至少需要借助税收和补贴两种EPR政策工具的配合,才能实现产出和设计寿命的最优结果。

关键词:耐用品;EPR政策工具;计划报废;产品设计寿命中图分类号:F205 文章标识码:A 文章编号:1007 3221(2020)12 0051 08 doi:10.12005/orms.2020.0313ResearchonDesignLifeDecisionofDurableGoodsBasedonEPR———FromthePerspectiveofPlannedObsolescenceWANGLei ning,ZHENGYun hong,ZHAORui(SchoolofBusinessandAdministration,NortheasternUniversity,Shenyang110167,China)Abstract:Thispaperdiscusseshowtopreventdurablegoodsfromproducingalargeamountofwasteintheshorttermlikefast movingconsumergoods(FMCG)throughextendedproducerresponsibility(EPR).Onthebasisofexistingresearch,fromtheperspectiveofplannedobsolescence,thisarticlebuildsadynamicmodelofdurablegoods,basedoncontinuoustimeusingtheoptimalcontrolmethodtoexploretheoptimalresultofcentralizeddecisionmakinganddecentralizeddecision makingofmarketequilibrium.Meanwhile,thispaperrevealstheincentiveeffectofEPRconstraintsunderdifferentmarketstructuresforproducerstoextendthelifeoftheproductdesign.Finally,basedontheanalysisprocessofthetheoreticalmodel,theconclusionsoftheresearchareverifiedbynumericalsimulationandcasestudy.Theresultsshowthatundertheperfectcompetitionmarketstructure,theimplementationofasinglePigouviantaxoronlydepositreturnsystemcanrealizetheoptimaloutputandalsoprovideenoughincentiveforproducerstoextendtheservicelifeoftheproductdesign;Inanimperfectcompetitivemarketstructure,atleasttwoEPRconstraints,taxandsubsidy,areneededtoachievetheoptimaloutcomeofoutputanddesignlife.Keywords:durablegoods;EPRpolicytools;plannedobsolescence;productdesignlife0 引言技术创新在给人类带来便利的同时,对生态环境的承载力构成挑战[1],也为固体废弃物的治理带来了诸多不便。

Part 3. The Essentials of Dynamic OptimisationIn macroeconomics the majority of problems involve optimisation over time. Typically a representative agent chooses optimal magnitudes of choice variables from an initial time until infinitely far into the future. There are a number of methods to solve these problems. In discrete time the problem can often be solved using a Lagrangean function. However in other cases it becomes necessary to use the more sophisticated techniques of Optimal Control Theory or Dynamic Programming . This handout provides an introduction to optimal control theory.Special Aspects of Optimisation over Time• Stock - Flow variable relationship.All dynamic problems have a stock-flow structure. Mathematically the flow variables are referred to as control variables and the stock variables as state variables. Not surprisingly the control variables are used to affect (or steer) the state variables. For example in any one period the amount of investment and the amount of money growth are flow variables that affect the stock of output and the level of prices which are state variables.• The objective function is additively seperable. This assumption makes the problem analytically tractable. In essence it allows us to separate the dynamic problem into a sequence of separate (in the objective function) one period optimisation problems. Don't be confused, the optimisation problems are not separate because of the stock-flow relationships, but the elements of the objective function are. To be more precise the objective function is expressed as a sum of functions (i.e. integral or sigma form) each of which depends only on the variables in that period. For example utility in a given period is independent of utility in the previous period.1. Lagrangean TechniqueWe can apply the Lagrangean technique in the usual way.Notationt y = State variable(s) =t μControl variable(s)The control and state variables are related according to some dynamic equation,()t y f y y t t t t ,,1μ=-+ (1)Choosing t μ allows us to alter the change in t y . If the above is a production function we choose =t μ investment to alter t t y y -+1 the change in output over the period. Why does time enter on its own? This would represent the trend growth rate of output.We might also have constraints that apply in each single period such as,()0,,≤t y G t t μ(2)The objective function in discrete time is of the form,()∑=Tt ttt y F 0,,μ(3)The first order conditions with respect to t y are,1. Optimal Control TheorySuppose that our objective is maximise the discounted utility from the use of an exhaustible resource over a given time interval. In order to optimise we would have to choose the optimal rate of extraction. That is we would solve the following problem,()()dt e E S U Max t TEρ-⎰0subject to,()t E dtdS-= )0(S S =()free T S =Where ()t S denotes the stock of a raw material and ()t E the rate of extraction. By choosing the optimal rate of extraction we can choose the optimal stock of oil at each period of time and so maximise utility. The rate of extraction is called the control variable and the stock of the raw material the state variable. By finding the optimal path for the control variable we can find the optimal path for the state variable. This is how optimal control theory works.The relationship between the stock and the extraction rate is defined by a differential equation (otherwise it would not be a dynamic problem). This differential equation is called the equation of motion . The last two are conditions are boundary conditions. The first tells us the current stock, the last tells us we are free to choose the stock at the end of the period. If utility is always increased by using the raw material this must be zero. Notice that the time period is fixed. This is called a fixed terminal time problem.The Maximum PrincipleIn general our prototype problem is to solve,()dt u y t F V Max Tu⎰=0,,()u y t f ty,,=∂∂ ()00y y =To find the first order conditions that define the extreme values we apply a set of condition known as the maximum principle.Step 1. Form the Hamiltonian function defined as,()()()()u y t f t u y t F u y t H ,,,,,,,λλ+=Step 2. Find,),,,(λu y t H Max uOr if as is usual you are looking for an interior solution, apply the weaker condition,0),,,(=∂∂uu y t H λAlong with,()•=∂∂y u y t H λλ,,,()•=∂∂λλy u y t H ,,,()0=T λStep 3. Analyse these conditions.Heuristic Proof of the Maximum PrincipleIn this section we can derive the maximum principle , a set of first order conditions that characterise extreme values of the problem under consideration.The basic problem is defined by,()dt u y t F V Max Tu⎰=0,,()u y t f ty,,=∂∂()00y y =To derive the maximum principle we use attempt to solve the problem using the 'Calculus of Variations'. Essentially the approach is as follows. The dynamic problem is to find the optimal time path for ()t y , although that we can use ()t u to steer ()t y . It ought to be obvious that,()()0=∂∂t u t VWill not do. This simply finds the best choice in any one period without regard to any future periods. Think of the trade off between consumption and saving. We need to choose the paths of the control (state) variable that gives us the highest value of the integral subject to the constraints. So we need to optimise in every time period, given the linkages across periods and the constraints. The Calculus of Variations is a way to transform this into a static optimisation problem.To do this let ()*t u denote the optimal path of the control variable and consider each possible path as variations about the optimal path.()()()t P t u t u ε+=*(3)In this case ε is a small number (the maths sense) and ()t P is a perturbing curve. It simply means all paths can be written as variations about the optimal path. Since we can write the control path this way we can also (must) write the path of the state variable and boundary points in the same way.()()()t q t y t y ε+=*(4)T T T ∆+=*ε (5)T T T y y y ∆+=*ε(6)The trick is that all of the possible choice variables that define the integral path are now functions of .ε As ε varies we can vary the whole path including the endpoints so this trick essentially allows us to solve the dynamic problem as a function of ε as a static problem. That is to find the optimum (extreme value) path we choose the value of ε that satisfies,0=∂∂εV(7) given (3) to (6).Since every variable has been written as a function of ε, (7) is the only necessary condition for an optimum that we need. When this condition is applied it yields the various conditions that are referred to as the maximum principle .In order to show this we first rewrite the problem in a way that allows us to include the Hamiltonian function,()()()dt y u y t f t u y t F V Max T u ⎪⎪⎭⎫ ⎝⎛-+=•⎰,,,, 0λWe can do this because the term inside the brackets is always zero provided the equation of motion is satisfied. Alternatively as,()()dt y t u y t H V Max Tu•-=⎰λ0,,(1)Integrating (by parts)1 the second term in the integral we obtain,()()()()()T T u y T y dt t y t u y t H V Max λλλ-+⎭⎬⎫⎩⎨⎧+=⎰•000,,(2)Now we apply the necessary condition (7) given (3) to (6).Recall that to differentiate an Integral by a Parameter we use Leibniz's rule, (page 9). After simplification this yields,()()()()[]()0,,,0=∆-∆+⎭⎬⎫⎩⎨⎧∂∂+⎥⎦⎤⎢⎣⎡+∂∂=∂∂=•⎰T T t T y T T u y t H dt t p u H t q y H V λλλεε (3)The 3 components of this integral provide the conditions defining the optimum. In particular,()()()⎰=⎭⎬⎫⎩⎨⎧∂∂+⎥⎦⎤⎢⎣⎡+∂∂•ελT dt t p u Ht q y H 00requires that,•-=∂∂λyHand 0=∂∂u HWhich is a key part of the maximum principle.The Transversality Condition1Just letdt y ydt y T TT⎰⎰••-=0λλλTo derive the transversality condition we have to analyse the two terms,()[]()0,,,=∆-∆=T T t y T T u y t H λλFor out prototype problem (fixed terminal time) we must have .0=∆T Therefore the transversality condition is simply that,()0=T λThe first two conditions always apply for 'interior' solutions but the transversality condition has to be defined by the problem at hand. For more on this see Chiang pages 181-184.The Current Value HamiltonianIt is very common in economics to encounter problems in which the objective function includes the following function t e ρ-. It is usually easier to solve these problems using the current value Hamiltonian. For example an optimal consumption problem may have an objective function looking something like,()()dt et C U tρ-∞⎰0Where ρ represents the rate of time discount. In general the Hamiltonian for such problems will be of the form,()()()()u y t f t e u y t F u y t H t ,,,,,,,λλρ+=-The current value Hamiltonian is defined by,()()()u y t f t m u y t F H CV ,,,,+=(1)Where ()()t e t t m ρλ-=. The advantage of the current value Hamiltonian is that the system defined by the first order equations is usually easier to solve. In addition to (1) an alternative is to write,()()()t t CV e u y t f t m e u y t F H ρρ--+=,,,,(2)The Maximum ConditionsWith regard to (2) the first two conditions are unchanged. That is,μμ∂∂=∂∂CV H H and λλ∂∂=∂∂CVH H (3)The third condition is also essentially the same since,•=∂∂=∂∂λyH y H CVHowever it is usual to write this in terms of •m . Since,t t me e m ρρρλ--••-=We can write the third condition as,m yH m CV ρ+∂∂-=•(4)The endpoint can similarly be stated in terms of m since t e m ρλ= the condition ()0=T λmeans that,()()0==T e T T m ρλOr,()0=-T e T m ρ(5)Ramsey model of optimal savingIn the macroeconomics class you have the following problem,Choose consumption to maximise,()()dt t c u e B U t t ⎰∞=-=0βWhere ()g θηρβ---=1 subject to the following constraint,()()()()()()t k g t c t k f t k +--=•ηIn this example ()t c u =, ()t k y =. The Hamiltonian is,()()()()()()()[]g n t c t k f t t C u Be H t +--+=-λβThe basic conditions give us,()()()()0=-'=∂∂-t t c u Be t c Ht λβ (1)()()()()()[]()t g n t k f t t k H λλ&=+-'-=∂∂ (2)Plus,()()()()()()t k g t c t k f t k +--=•η(3)Now we must solve these. Differentiate the right-hand side of (1) with respect to time.This gives you ()t λ& which can then be eliminated from (2). The combined condition can then be rewritten as,()()()()()()[]g t r t c u t c u t cθρ--'''-=&This is the Euler equation. If you assume the instantaneous utility function is CRRA as in class and you calculate the derivatives you should get the same expression.。