corp taxChapter 4

- 格式:ppt

- 大小:431.50 KB

- 文档页数:34

CHAPTER 2: ASSET CLASSES AND FINANCIALINSTRUMENTSPROBLEM SETS1. Preferred stock is like long-term debt in that it typically promises a fixed paymenteach year. In this way, it is a perpetuity. Preferred stock is also like long-term debt in that it does not give the holder voting rights in the firm.Preferred stock is like equity in that the firm is under no contractual obligation tomake the preferred stock dividend payments. Failure to make payments does not set off corporate bankruptcy. With respect to the priority of claims to the assets of thefirm in the event of corporate bankruptcy, preferred stock has a higher priority than common equity but a lower priority than bonds.2. Money market securities are called cash equivalents because of their high levelof liquidity. The prices of money market securities are very stable, and they canbe converted to cash (i.e., sold) on very short notice and with very lowtransaction costs. Examples of money market securities include Treasury bills,commercial paper, and banker's acceptances, each of which is highly marketableand traded in the secondary market.3. (a) A repurchase agreement is an agreement whereby the seller of a securityagrees to “repurchase” it from the buyer on an agreed upon date at an agreedupon price. Repos are typically used by securities dealers as a means forobtaining funds to purchase securities.4. Spreads between risky commercial paper and risk-free government securitieswill widen. Deterioration of the economy increases the likelihood of default oncommercial paper, making them more risky. Investors will demand a greaterpremium on all risky debt securities, not just commercial paper.5.6. Municipal bond interest is tax-exempt at the federal level and possibly at thestate level as well. When facing higher marginal tax rates, a high-incomeinvestor would be more inclined to invest in tax-exempt securities.7. a. You would have to pay the ask price of:161.1875% of par value of $1,000 = $1611.875b. The coupon rate is 6.25% implying coupon payments of $62.50annually or, more precisely, $31.25 semiannually.c. The yield to maturity on a fixed income security is also known as its requiredreturn and is reported by The Wall Street Journal and others in the financialpress as the ask yield. In this case, the yield to maturity is 2.113%. An investorbuying this security today and holding it until it matures will earn an annualreturn of 2.113%. Students will learn in a later chapter how to compute boththe price and the yield to maturity with a financial calculator.8. Treasury bills are discount securities that mature for $10,000. Therefore, a specific T-bill price is simply the maturity value divided by one plus the semi-annual return:P = $10,000/1.02 = $9,803.929. The total before-tax income is $4. After the 70% exclusion for preferred stockdividends, the taxable income is: 0.30 ⨯ $4 = $1.20Therefore, taxes are: 0.30 ⨯ $1.20 = $0.36After-tax income is: $4.00 – $0.36 = $3.64Rate of return is: $3.64/$40.00 = 9.10%10. a. You could buy: $5,000/$64.69 = 77.29 shares. Since it is not possible to tradein fractions of shares, you could buy 77 shares of GD.b. Your annual dividend income would be: 77 ⨯ $2.04 = $157.08c. The price-to-earnings ratio is 9.31 and the price is $64.69. Therefore:$64.69/Earnings per share = 9.3 ⇒ Earnings per share = $6.96d. General Dynamics closed today at $64.69, which was $0.65 higher thanyesterday’s price of $64.0411. a. At t = 0, the value of the index is: (90 + 50 + 100)/3 = 80At t = 1, the value of the index is: (95 + 45 + 110)/3 = 83.333The rate of return is: (83.333/80) - 1 = 4.17%b. In the absence of a split, Stock C would sell for 110, so the value of theindex would be: 250/3 = 83.333 with a divisor of 3.After the split, stock C sells for 55. Therefore, we need to find the divisor(d) such that: 83.333 = (95 + 45 + 55)/d ⇒ d = 2.340. The divisor fell,which is always the case after one of the firms in an index splits its shares.c. The return is zero. The index remains unchanged because the return foreach stock separately equals zero.12. a. Total market value at t = 0 is: ($9,000 + $10,000 + $20,000) = $39,000Total market value at t = 1 is: ($9,500 + $9,000 + $22,000) = $40,500Rate of return = ($40,500/$39,000) – 1 = 3.85%b.The return on each stock is as follows:r A = (95/90) – 1 = 0.0556r B = (45/50) – 1 = –0.10r C = (110/100) – 1 = 0.10The equally weighted average is:[0.0556 + (-0.10) + 0.10]/3 = 0.0185 = 1.85%13. The after-tax yield on the corporate bonds is: 0.09 ⨯ (1 – 0.30) = 0.063 = 6.30%Therefore, municipals must offer a yield to maturity of at least 6.30%.14. Equation (2.2) shows that the equivalent taxable yield is: r = r m/(1 –t), so simplysubstitute each tax rate in the denominator to obtain the following:a. 4.00%b. 4.44%c. 5.00%d. 5.71%15. In an equally weighted index fund, each stock is given equal weight regardless of itsmarket capitalization. Smaller cap stocks will have the same weight as larger cap stocks.The challenges are as follows:•Given equal weights placed to smaller cap and larger cap, equal-weighted indices (EWI) will tend to be more volatile than their market-capitalization counterparts;•It follows that EWIs are not good reflectors of the broad market that they represent; EWIs underplay the economic importance of larger companies.•Turnover rates will tend to be higher, as an EWI must be rebalancedback to its original target. By design, many of the transactions would beamong the smaller, less-liquid stocks.16. a. The ten-year Treasury bond with the higher coupon rate will sell for a higherprice because its bondholder receives higher interest payments.b. The call option with the lower exercise price has more value than one with ahigher exercise price.c. The put option written on the lower priced stock has more value than onewritten on a higher priced stock.17. a. You bought the contract when the futures price was $7.8325 (see Figure2.11 and remember that the number to the right of the apostrophe represents aneighth of a cent). The contract closes at a price of $7.8725, which is $0.04 morethan the original futures price. The contract multiplier is 5000. Therefore, thegain will be: $0.04 ⨯ 5000 = $200.00b. Open interest is 135,778 contracts.18. a. Owning the call option gives you the right, but not the obligation, to buy at$180, while the stock is trading in the secondary market at $193. Since thestock price exceeds the exercise price, you exercise the call.The payoff on the option will be: $193 - $180 = $13The cost was originally $12.58, so the profit is: $13 - $12.58 = $0.42b. Since the stock price is greater than the exercise price, you will exercise the call.The payoff on the option will be: $193 - $185 = $8The option originally cost $9.75, so the profit is $8 - $9.75 = -$1.75c. Owning the put option gives you the right, but not the obligation, to sell at $185,but you could sell in the secondary market for $193, so there is no value inexercising the option. Since the stock price is greater than the exercise price,you will not exercise the put. The loss on the put will be the initial cost of$12.01.19. There is always a possibility that the option will be in-the-money at some time prior toexpiration. Investors will pay something for this possibility of a positive payoff.20.Value of Call at Expiration Initial Cost Profita. 0 4 -4b. 0 4 -4c. 0 4 -4d. 5 4 1e. 10 4 6Value of Put at Expiration Initial Cost Profita. 10 6 4b. 5 6 -1c. 0 6 -6d. 0 6 -6e. 0 6 -621. A put option conveys the right to sell the underlying asset at the exercise price. Ashort position in a futures contract carries an obligation to sell the underlying assetat the futures price. Both positions, however, benefit if the price of the underlyingasset falls.22. A call option conveys the right to buy the underlying asset at the exercise price. Along position in a futures contract carries an obligation to buy the underlying assetat the futures price. Both positions, however, benefit if the price of the underlyingasset rises.CFA PROBLEMS1.(d) There are tax advantages for corporations that own preferred shares.2. The equivalent taxable yield is: 6.75%/(1 0.34) = 10.23%3. (a) Writing a call entails unlimited potential losses as the stock price rises.4. a. The taxable bond. With a zero tax bracket, the after-tax yield for thetaxable bond is the same as the before-tax yield (5%), which is greater thanthe yield on the municipal bond.b. The taxable bond. The after-tax yield for the taxable bond is:0.05⨯ (1 – 0.10) = 4.5%c. You are indifferent. The after-tax yield for the taxable bond is:0.05 ⨯ (1 – 0.20) = 4.0%The after-tax yield is the same as that of the municipal bond.d. The municipal bond offers the higher after-tax yield for investors in taxbrackets above 20%.5.If the after-tax yields are equal, then: 0.056 = 0.08 × (1 –t)This implies that t = 0.30 =30%.。

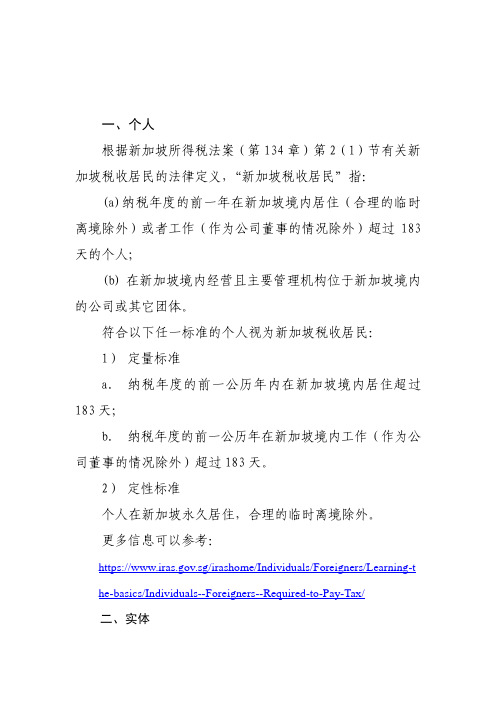

新加坡税收居民身份认定规则 一、个人根据新加坡所得税法案(第134章)第2(1)节有关新加坡税收居民的法律定义,“新加坡税收居民”指:(a)纳税年度的前一年在新加坡境内居住(合理的临时离境除外)或者工作(作为公司董事的情况除外)超过183天的个人;(b)在新加坡境内经营且主要管理机构位于新加坡境内的公司或其它团体。

符合以下任一标准的个人视为新加坡税收居民:1) 定量标准a. 纳税年度的前一公历年内在新加坡境内居住超过183天;b. 纳税年度的前一公历年在新加坡境内工作(作为公司董事的情况除外)超过183天。

2) 定性标准个人在新加坡永久居住,合理的临时离境除外。

更多信息可以参考:https://.sg/irashome/Individuals/Foreigners/Learning-t he-basics/Individuals--Foreigners--Required-to-Pay-Tax/二、实体根据所得税法案第2(1)节有关新加坡税收居民的法律定义,“新加坡税收居民”指:(a)纳税年度的前一年在新加坡境内居住(合理的临时离境除外),或者工作(作为公司董事的情况除外)超过183天的个人;(b)在新加坡境内经营且主要管理机构位于新加坡境内的公司或社会团体。

“其它团体”指:政治团体、高校、个人独资企业、互助会、联谊会等,不包括公司和合伙企业。

总的来说,其它团体包括俱乐部、社团、管理公司、贸易协会、市镇理事会和其它非法人组织。

根据上述定义,公司和其它团体的税收居民身份根据其主要管理机构所在地确定。

“主要管理机构”指作出经营战略决策(如公司政策或发展战略等)的机构。

主要管理机构所在地主要基于客观事实进行认定。

通常来说,制定战略决策的董事会召开地点是关键的考虑因素。

更多信息可以参考以下网站:https://.sg/irashome/Businesses/Companies/Learning-t he-basics-of-Corporate-Income-Tax/Tax-Residence-Status-of-a-Com pany/三、不视为税收居民的实体以下实体视为税收上的透明体:1) 个人独资企业:个人独资企业的收入归属于独资企业经营者个人,因此由其就个人独资企业的收入承担个人所得税纳税义务;2) 合伙企业:合伙企业的收入由每个合伙人就其分得的收入份额承担个人所得税纳税义务。

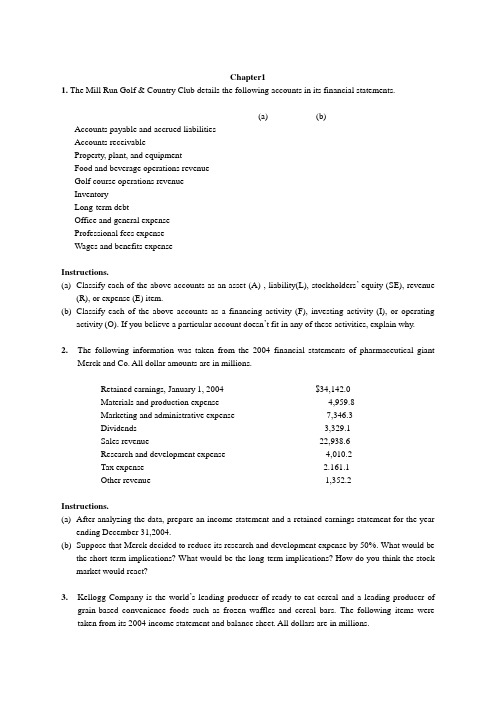

Chapter11. The Mill Run Golf & Country Club details the following accounts in its financial statements.(a) (b)Accounts payable and accrued liabilities ____ ____Accounts receivable ____ ____Property, plant, and equipment ____ ____Food and beverage operations revenue ____ ____Golf course operations revenue ____ ____Inventory ____ ____Long-term debt ____ ____Office and general expense ____ ____Professional fees expense ____ ____Wages and benefits expense ____ ____Instructions.(a)Classify each of the above accounts as an asset (A) , liability(L), stockholders’ equity (SE), revenue(R), or expense (E) item.(b)Classify each of the above accounts as a financing activity (F), investing activity (I), or operatingactivity (O). If you believe a particular account doesn’t fit in any of these activities, explain why.2.The following information was taken from the 2004 financial statements of pharmaceutical giantMerck and Co. All dollar amounts are in millions.Retained earnings, January 1, 2004 $34,142.0Materials and production expense 4,959.8Marketing and administrative expense 7,346.3Dividends 3,329.1Sales revenue 22,938.6Research and development expense 4,010.2Tax expense 2.161.1Other revenue 1,352.2Instructions.(a)After analyzing the data, prepare an income statement and a retained earnings statement for the yearending December 31,2004.(b)Suppose that Merck decided to reduce its research and development expense by 50%. What would bethe short-term implications? What would be the long-term implications? How do you think the stock market would react?3.Kellogg Company is the world’s leading producer of ready-to-eat cereal and a leading producer ofgrain-based convenience foods such as frozen waffles and cereal bars. The following items were taken from its 2004 income statement and balance sheet. All dollars are in millions._____Retained earnings $2,701.3 _____ Long-term debt $3,892.6 _____Cost of goods sold 5,298.7 _____ Inventories 681.0 _____Selling and administrative expense 2,634.1 _____ Net sales 9,613.9 _____Cash 417.4 _____ Accounts payable 767.2 _____Notes payable 709.7 _____Common stock 103.8 _____Interest expense 308.6 _____ Income tax expense 475.3_____ Other expense 6.6Instructions.Perform each of the following.(a)In each case identify whether the item is an asset (A), liability (L), stockholders’ equity (SE),revenue (R), or expense (E).(b)Prepare an income statement for Kellogg Company for the year ended December 31, 2004.4.The following items were taken from the balance sheet of Nike, Inc.(1)Cash $828.0 (7) Inventories $1,633.6(2)Accounts receivable 2,120.2 (8) Income taxes payable 118.2(3)Common stock 890.6 (9) Property, plant, and equipment 1,586.9(4)Notes payable 146.0 (10)Retained earnings 3,891.1(5)Other assets 1,722.9 (11)Accounts payable 763.8(6)Other liabilities 2,081.9Instructions.Perform each of the following.(a)Classify each of these items as an asset, liability, or stockholders’ equity. (All dollars are inmillions.)(b)Determine Nike’s accounting equation by calculating the value of total assets, total liabilities,and total stockholders’ equity.(c)To what extent dose Nike rely on debt versus equity financing?Chapter 2.1.These items are taken from the financial statements of Donovan Co. at December 31.2007Building $105,800Accounts receivable 12,600Prepaid insurance 4,680Cash 16,840Equipment 82,400Land 61,200Insurance expense 780Depreciation expense 5,300Common stock 62,000Retained earnings (January 1, 2007) 40,000Accumulated depreciation-building 45,600Accounts payable 9,500Mortgage payable 93,600Accumulated depreciation-equipment 18,720Interest payable 3,600Bowling revenues 19,180Instructions.Prepare a classified balance sheet. Assume that $13,600 of the mortgage payable will be paid in 2008.2. The following items were taken from the 2004 financial statements of Texas Instruments, Inc.(All dollars are in millions.)Long-term debt $ 368 Cash $ 2,668 Common stock 2,488 Accumulated depreciation 5,655 Prepaid expense 326 Accounts payable 1,444 Property, plant, and equipment 9,573 Other noncurrent assets 1,927Other current assets 554 Other noncurrent liabilities 943Other current liabilities 470 Retained earnings 10,575Long-term investments 264 Accounts receivable 1,696Short-term investments 3,690 Inventories 1,256Loans payable in 2005 11Instructions.Prepare a classified balance sheet in good form as of December 31, 2004.3. These financial statement items are for Snyder Corporation at year-end, July 31, 2007.Salaries payable $ 2,080Salaries expense 51,700Utilities expense 22,600Equipment 18,500Accounts payable 4,100Commission revenue 61,100Rent revenue 8,500Long-term note payable 1,800Common stock 16,000Cash 24,200Accounts receivable 9,780Accumulated depreciation 6,000Dividends 4,000Retained earnings (beginning of the year) 35,200Instructions.(a)Prepare an income statement and a retained earnings statement for the year. Snyder Corporation didnot issue any new stock during the year.(b)Prepare a classified balance sheet at July 31.(c)Compute the current ratio and debt to total assets ratio.(d)Suppose that you are the president of Allied Equipment. Your sales manager has approached you witha proposal to sell $20,000 of equipment to Snyder. He would like to provide a loan to Snyder in theform of a 10%, 5-year note payable. Evaluate how this loan would change Snyder’s current ratio and debt to total assets ratio, and discuss whether you would make the sale.4. The chief financial officer (CFO) of SuperClean Corporation requested that the accounting department prepare a preliminary balance sheet on December 30, 007, so that the CFO could get an idea of how the company stood. He knows that certain debt agreements with its creditors require the company to maintain a current ratio of at least 2:1. The preliminary balance sheet is as follows.SUPERCLEAN CORP.Balance SheetDecember 30, 2007Current assets Current liabilitiesCash $30,000 Accounts payable $25,000Accounts receivable 20,000 Salaries payable 15,000 $40,000 Prepaid insurance 10,000 $60,000 Long-term liabilitiesNotes payable 80,000Total liabilities 120,000 Property, plant, and equipment (net) 200,000 Stockholders’ equityTotal assets $260,000 Common stock 100,000Retained earnings 40,000 140,000Total liabilities and stockholders equity$260,000Instructions.(a)Calculate the current ratio and working capital based on the preliminary balance sheet.(b)Based on the results in (a), the CFO requested that $25,000 of cash be used to pay off the balance ofthe accounts payable account on December 31, 2007. Calculate the new current ratio and working capital after the company takes these actions.(c)Discuss the pros and cons of the current ratio and working capital as measures of liquidity.(d)Was it unethical for the CFO to take these steps?5. The following data were taken from the 2004 and 2003 financial statements of American Eagle Outfitters. (All dollars are in thousands.)20042003 Current assets $525,623 $427,878Total assets 865,071 741,339Current liabilities 189,035 141,586Total liabilities 221,401 163,857Total stockholders’ equity 643,670 577,482Cash provided by operating activities 189,469 104,548Capital expenditures 64,173 61,407Dividends paid -0- -0-Instructions.Perform each of the following.(a)Calculate the debt to total assets ratio for each year.(b)Calculate the free cash flow for each year.(c)Discuss American Eagle’s solvency in 2004 versus 2003.(d)Discuss American Eagle’s ability to finance its investment activities with cash provided by operatingactivities, and how any deficiency would be met.Chapter 3.1.During 2007, its first year of operations as a delivery service, Cheng Corp. entered into the following transactions.(1)Issued shares of common stock to investors in exchange for $110,000 in cash.(2)Borrowed $45,000 by issuing bonds.(3)Purchased delivery trucks for $60,000 cash.(4)Received $16,000 from customers for services provided.(5)Purchased supplies for $4,200 on account.(6)Paid rent of $5,600.(7)Performed services on account for $8,000.(8)Paid salaries of $28,000.(9)Paid a dividend of $11,000 to shareholders.InstructionsUsing the following tabular analysis, show the effect of each transaction on the accounting equation. Put explanations for changes to Stockholders’ Equity in the right-hand margin.Assets = Liabilities + Stockholders’EquityCash+Accounts+Supplies+Property,Plant, =Accounts +Bonds + Common + Retained Receivable and Equipment Payable Payable Stock Earningsmonth of business, are as follows.(1)Issued stock to investors for $12,000 in cash.(2)Purchased used car for $8,000 cash for use in business.(3)Purchased supplies on account for $300.(4)Billed customers $2,600 for services performed.(5)Paid $200 cash for advertising start of the business.(6)Received $1,100 cash from customers billed in transaction(4).(7)Paid creditor $300 cash on account.(8)Paid dividends of $400 cash to stockholders.Instructions(a)For each transaction indicate (a) the basic type of account debited and credited (asset,liability, stockholders’ equity); (b) the specific account debited and credited (Cash, Rent Expense, Service Revenue, etc.); (c) whether the specific account is increased or decreased; and (d) the normal balance of the specific account. Use the following format, in which transaction 1 is given as an example.Account Debited Account Credited(a) (b) (c) (d) (a) (b) (c) (d)Trans- Basic Specific Normal Basic Specific Normalaction Type Account Effect Balance Type Account Effect Balance1 Asset Cash Increase Debit Stock- Common Increase Creditholders’stockequity(b)Journalize the transaction. Do not provide explanations.3.This information relates to Matthews Real Estate Agency Corporation.Oct. (1) Stockholders invested $25,000 in exchange for common stock of the corporation.(2)Hires an administrative assistant at an annual salary of $42,000.(3)Buys office furniture for $3,600, on assount.(6)Sells a house and lot for M.E. Mills; commissions due from Mills, $10,800 (notpaid by Mills at this time).(10) Receives cash of $140 as commission for acting as rental agent renting anapartment.(27) Pays $700 on account for the office furniture purchased on October 3.(30) Pays the administrative assistant $3,500 in salary for October.InstructionsPrepare the debit-credit analysis for each transaction as illustrated on pages 119-124.4.Transaction data for Matthews Real Estate Agency are presented in 3 .Journalize the transaction. Do not provide explanations.5.Selected transactions for P.F. Quick Corporation during its first month in business arepresented below.Sept. (1) Issued common stock in exchange for $15,000 cash received from investors.(5) Purchased equipment for $12,000, paying $2,000 in cash and the balance on account.(25) Paid $5,000 cash on balance owed for equipment.(30) Paid $500 cash dividend.P.F. Quick’s chart of accounts shows: Cash, Equipment, Accounts Payable, Common Stock, and Dividends.Instructions(a)Prepare a tabular analysis of the September transaction. The column headings should be:Cash + Equipment = Accounts Payable + Stockholders’ Equity. For transactions affecting stockholders’ equity, provide explanations in the right margin, as shown on page107.(b)Journalize the transaction. Do not provide explanations.(c)Post the transactions to T accounts.Chapter 41.The following independent situations require professional judgement for determining when to recognize revenue from the transaction.(a)Southwest Airlines sells you an advance-purchase airline ticket in September foryour flight home at Christmas.(b)Ultimate Electronics sell you a home theatre on a “no monkey down, no interest, andno payments for one year” promotional deal.(c)The Toronto Blue Jays sells season tickets online to games in the Skydome. Fans canpurchase the tickets at any time, although the season doesn’t officially begin until April. The major league baseball season runs from April through October.(d)In August, you order a sweater from Sears using its online catalog. The sweaterarrives in September in full in November.(e)In August, you order a sweater from Sears using its online catalog. The sweaterarrives in September, and you charge it to your Sears credit card. You receive and pay the Sears bill in October.InstructionIdentify when revenue should be recognized in each of the above situations.2.Your examination of the records of a company that follows the cash basis ofaccounting tells you that the company’s reported cash basis earnings in 2007 are $33,640. If this firm had followed accrual basis accounting practices, it would have reported the following year-end balances.2007 2006 Accounts receivable $3,400 $2,300Unpaid wages owed 1,500 2,400Other unpaid amounts 1,400 1,600 InstructionDetermine the company’s net earning on an accrual basis for 2007. Show all your calculations in an orderly fashion.3.In its first year of operations Bere Company earned $28,000 in service revenue,$6,000 of which was on account and still outstanding at year-end. The remaining $22,000 was received in cash from customers.The company incurred operating expenses of $14,500. Of these expenses $13,000 were paid in cash; $1,500 was still owed on account at year-end. In addition, Bere prepaid $3,600 for insurance coverage that would not be used until the second year of operations.Instructions(a)Calculate the first year’s net earnings under the cash basis of accounting, and calculatethe first year’s net earning under the accrual basis of accounting.(b)Which basis of accounting (cash or accrual) provides more useful information fordecision makers?4.The Radical Edge, a ski tuning and repair shop, opened in November 2006. The company carefully kept track of all its cash receipts and cash payments. The following information is available at the end of the ski season, April 30, 2007.Cash Receipts Cash PaymentsIssue of common shares $20,000Payment for repair equipment $9,200 Rent payments 1,225 Newspaper advertising payment 375 Utility bills payments 970 Part-time helper’s wages payments 2,600 Income tax payment 10,000 Cash receipts from ski and snowboardrepair services 32,150Subtotals 52,150 24,370 Cash balance 27,780 Totals $52,150 $52,150 You learn that repair equipment has an estimated useful life of 5 years. The company rents space at a cost of $175 per month on a one-year lease. The lease contract requires payment of the first and last month s’ rent in advance, which was done. The part-timer helper is owed $220 at April 30, 2007, for unpaid wages. At April 30, 2007, customers owe The Radical Edge $650 for services they have received but have not yet paid for.Instructions(b)Prepare the April 30, 2007, classified balance sheet.5. MaxPlay, a maker of electronic games for kids, has just completed its first year of operations. The company’s sales growth was explosive. To encourage large national stores to carry its products MaxPlay offered 180-day financing-meaning its largest customers do not pay for nearly 6 months. Because MaxPlay is a new company, its components suppliers insist on being paid cash on delivery. Also, it had to pay up front for 2 years of insurance. At the end of the year MaxPlay owed employees for one full month of salaries, but due to a cash shortfall, it promised to pay them the first week of next year.Instructions(a)Explain how cash and accrual accounting would differ for each of the events listed aboveand describe the proper accrual accounting.(b)Assume that at the end of the year MaxPlay reported a favorable net income, yet thecompany’s management is concerned because the company is very short of cash. Explain how MaxPlay could have positive net income and yet run out of cash.6.The ledger of Reliable Rental Agency on March 31 of the current year includes theseselected accounts before adjusting entries have been prepared.Debits Credits Prepaid Insurance $3,600Supplies 3,000Equipment 25,000Accumulated Depreciation-Equipment $8,400Notes Payable 20,000Unearned Rent Revenue 10,200Rent Revenue 60,000Interest Expense 0Wage Expense 14,000An analysis of the accounts shows the following.(1)The equipment depreciates $250 per month.(2)Half of the unearned rent revenue was earned during the quarter.(3)Interest of $440 is accrued on the notes payable.(4)Supplies on band total $850.(5)Insurance expires at the rate of $300 per month.InstructionsPrepare the adjusting entries at March 31, assuming that adjusting entries are made quarterly. Additional accounts are: Depreciation Expense, Insurance Expense, Interest Payable, and supplied Expense.7.Gene Hoffman, D.D.S., opened an incorporated dental practice on January 1, 2007.During the first month of operations the following transactions occurred:such services was earned but not yet billed to the insurance companies.(2)Utility expenses incurrent but not paid prior to January 31 totaled $520.(3)Purchased dental equipment on January 1 for $80,000, paying $20,000 in cash andsigning a $60,000, 3-year note payable (Interest is paid each December 31). The equipment depreciates $400 per month. Interest is $500 per month.(4)Purchased a 1-year malpractice insurance policy on January 1 for $18,000.(5)Purchased $1,750 of dental supplies. On January 31 determined that $350 of supplieswere on hand.InstructionsPrepare the adjusting entries on January 31. Account titles are: Accumulated Depreciation-Dental Equipment, Depreciation Expense, Service Revenue, Accounts Receivable, Insurance Expense, Interest Expense, Interest Payable, Prepaid Insurance, Supplies, Supplies Expense, Utilities Expense, and Utilities Payable.Chapter 5ExercisesE5-1 The following transactions are for Kale Company.1.On December 3 Kale Company sold $480000 of merchandise to Thomson Co., terms1/10,n/30 .The cost of the merchandise sold was 320000.2.On December 8 Thomson Co. was granted an allowance of $28000 for merchandisepurchased on December 3.3.on December 13 Kale company received the balance due from Thomson Co. instructions(a)Prepare the journal entries to record these transactions on the books of Kale Company .Kale uses a perpetual inventory system.(b)Assume that Kale Company received the balance due from Thomson Co. on January 2 ofthe following year instead of December 13. Prepare the journal entry to record the receipt of payment on January 2.E5-2 Assume that on September 1 office depot had an inventory that included a variety of calculators. The company uses a perpetual inventory system. During September these transactions occurred.Sept.6 purchased calculators from black box co. at a total cost of $620,term n/30.Sept .9 Paid freight of $50 on calculators purchased from Black Box Co.Sept 10 Returned calculators to black box co. for $38 credit because they did not meet specifications .Sept 12 Sold calculators costing $520 for $780to University Book Store, terms n/30.Sept14 Granted credit of $45 to University Book Store for the return of one calculator that was not ordered .The calculator cost $28.Sept 20 Sold calculators costing $570 for $900 to Campus Card Shop. InstructionsJournalize the September transactions .E5-3 This information relates to Sherper Co.$220000,terms2/10,n/30.2.On April 6 paid freight costs of $900 on merchandise purchased from Newport.3.On April 7 purchased equipment on account for $26000.4.On April 8 returned some of April 5 merchandise of Newport Company which cost$3600.5.On April 15 paid the amount due to Newport Company in full.Instructions(a) Prepare the journal entries to record the transactions listed above on the books of SherperCo. uses a perpetual inventory system.(b) Assume that Sherper Co. paid the balance due to Newport Company on May 4 instead of April 15.Prepare the journal entry to record this payment.E5-8 In its income statement for the year ended December 31,2007,Knitz Company reported the following condensed data.Administrative expenses $435000 selling expenses $ 690000Cost of goods sold 987000 Loss on sale of equipment 83500Interest expense 68000 Net sales 2350000Interest revenue 45000Instructions(a)Prepare a multiple-step income statement.(b)Calculate the profit margin ratio and gross profit rate.(c)In 2006 Knitz had a profit margin ratio of 9%. Is the decline in 2007 a cause forconcern?E5-9 In its income statement for the year ended June 30,2004, The Clorox Company report the following condensed data (dollars in millions ).Selling and Research andAdministrative expenses $ 552 development expense $ 84Net sales 4324 Income tax expense 294Interest expense 30 Other income 1Advertising expense 429 Cost of goods sold 2387 Instructions(a)Prepare a multiple step income statement.(b)Calculate the gross profit rate and the profit margin ratio and explain what each means.(c)Assume by marketing department has presented a plan to increase advertising expensesby $300 million . It expects thos plan to result in an increase in both net sales and cost of goods sold of 25%. Redo parts (a) and (b) and discuss whether this plan has merit.(Assume a tax rate of 35%,and round all amounts to whole dollars .)E5-10 The trial balance of Rachel Company at the end of its fisical year , August 31 , 2007, includes these accounts :Merchandise Inventory $19200; Purchases $144000; Sales $190000; Freight-in $8000; Sales Returns and Allowances $3000;Freight-out $1000;and Purchase Returns and Allowances $5000. The ending merchandise inventory is $25000.InstructionsPrepare a cost of goods sold section for the year ending August 31.Chapter 6ExercisesE6-2Dennis Lee ,an auditor with Knapp CPAs, is performing a review of Nathan Company’s inentory account. Nathan did not have a good year, and top management is under pressure to boost reported income. According to its records, the inventory balance at year-end was $740000.However, the following information was not considered when determining that amount.1.Included in the company’s count were goods with a cost of $250000 that the company isholding on consignment.The goods belong to Anya Corporation.2.The physical count did not include goods purchased by Nathan with a cost of $40000that were shipped FOB shipping point on December 28 and did not arrive at Nathan’s warehouse until January 33.Included in the inventory account was $17000 of office supplies that were stored in thewarehouse and were to be used by the company’s supervisors and managers during the coming year4.The company received an order on December 29 that was boxed and was sitting on theloading dock awaiting pick-up on Decemeber 31.The shipper picked up the goods on January 1 and deliverde them on January 6.The shipping tems were FOB shipping point.The goods had a selling price of $40000 and a cost of $30000.The goods were not included in the count because they were sitting on the dock.5.On December 29 Nathan shipped goods with a selling price of $80000 and a cost of$60000 to Central Sales Corporation FOB shipping point.The goods arrived on January3.Central Sales had only ordered goods with a selling price of $10000 and a cost of $8000.However, a sales manager at Nathan had authorized the shipment and said that if Central wanted to ship the goods back next week, it could.6.Included in the count was $50000 of goods that were parts for a machine that thecompany on longer made. Given the higi-tech nature of Nathan’s products,it was unlikely that these obsolete parts had any other use .However, management would prefer to keep them on the books at cost, “since that is what we paid for them ,after all.”InstructionsPrepare a schedule to determine the correct inventory amount. Provide explanations for each item above, saying why you did or did not make an adjustment for each item.E6-3 Shippers Inc. had the following inventory situations to consider at January 31.its year end.(a)Goods held on consignment for MailBoxes Corp. since December 12.(b)Goods shipped on consignment to Rinehart Holdings Inc. on January 5(c)Goods shipped to a customer, FOB destination ,on January 29 that are still in transit.(d)Goods shipped to a customer, FOB shipping point, on January 29 that are still in transit.(e)Goods purchased FOB destination from a supplier on January 25,that are still in transit.(f)Goods purchased FOB shipping point from a supplier on January 25,that are still intransit.(g)Office supplies on hand at January 31.InstructionsIdentify which of the preceding items should be included in inventory. If the item should not be included in inventory, state where it should be recorded.E6-4Boarders sells a snowboard, Xpert, that is popular with snowboard enthusiasts. Below if information relating to Boarders’s purchases of Xpert snowboards during September. During the same month, 118 Xpert snowboards were sold. Boarders uses a periodic inventory system.Instructions(a)Compute the ending inventory at September 30 using the FIFO and LIFO methods.Prove the amount allocated to cost of goods sold under each method.(b)For both FIFO and LIFO ,calculate the sum of ending inventory and cost of goods sold.What do you notice about the answers you found for each method?E6-7 Plato Company reports the following for the month of June.(1)FIFO,(2)LIFO,and (3) average cost.(b)Which costing method gives the highest ending inventory? The highest cost of goodssold ?Why?(c)How do the average-cost values for ending inventory and cost of goods sold relate toending inventory and cost of goods sold for FIFO and LIFO?(d)Explain why the average cost is not $6InstructionsCalculate the inventory turnover ratio,days in inventory,and gross profit rate for PepsiCo.,Inc. for 2002,2003, and 2004. Comment on any trends.E6-9 Cody Camera Shop es the lower of cost or market basis for its inventory. The following data are available at December 31.InstructionsWhat amount should be reported on Cody Camera Shop’s financial statements, assuming the lower of cost or market rule is applied?E6-10Deere&Company is a global manufacturer and distributor of agricultural, construction, and forestry equipment. It reportde the following information in its 2004 annual report.Instructions(a)Compute Deere’s inventory turnover ratio and days in inventory for 2004(b)Compute Deere’s current ratio using the 2004 data as presented, and then again afteradjusting for the LIFO reserve(c)Comment on how ignoring the LIFO reserve might affect your evaluation of Deere’sliquidity.chapter 8exercisese-8-3 At the beginning of the current period,Huang Crop. had balances in Accounts Receivable of 200000 and in Allowance for Doubtful Accounts of 9000(credit). During the period,it had net credit sales of 800000 and collections of 743000. It wrote off as uncollectible accounts receivable of 7000.However,a 4000 account previously written off as uncollectible was recovered before the end before the end of the current period . Uncollectible accounts are estimated to total 25000 at the end of period.Instructions(a)Prepare the entries to record sales and collections during the period.(b)Prepare the entry to record the write-off of uncollectible accounts during the period.(c)Prepare the entries to record the recovery of the uncollectible account during the period.(d)Prepare the entry to record bad debts expense for the period.(e)Determine the ending balances in Accounts Receivable and Allowance for Doubtful accounts. (f)What is the net realizable value of the receivables at the end of period?E8-4 The ledger of Garcia Company at the end of the current year shows Accounts Receivable 96000;Credit Sales 780000 ;and Sales Returns and Allowances 40000.Instructions(a)If Garcia uses the direct write-off method to account for uncollectible accounts ,journalize the adjusting entry at December 31,assuming Garcia determines that Allied’s 900 balance is un collectible.(b)IF Allowance for Doubtful Accounts has a credit balance of $1100 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be 10% of accounts receivable.(c)If Allowance for Doubtful Accounts has a debit balance of 500 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be 8% of accounts receivable.E8-5 Hachey Company has accounts receivable of 95100 at March 31,2007.An analysis of the accounts shows these amounts.Credit terms are 2/10,n/30.At March 31,2007,there is a $2200 credit balance in Allowance for Doubtful Accounts prior to adjustment. The company uses the percentage of receivable basis for estimating uncollectible accounts. The company’s estimates of bad debts as shown on next page.。

Revit Structure4 User's Guide25504-050000-5020AAugust 2006Copyright© 2006 Autodesk, Inc.All Rights ReservedThis publication, or parts thereof, may not be reproduced in any form, by any method, for any purpose.AUTODESK, INC., MAKES NO W ARRANTY, EITHER EXPRESS OR IMPLIED, INCLUDING BUT NOT LIMITED TO ANY IMPLIED WARRANTIES OF MERCH ANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE REGARDING TH ESE MATERIALS, AND MAKES SUCH MATERIALS A V AILABLE SOLELY ON AN "AS-IS" BASIS.IN NO EVENT SHALL AUTODESK, INC., BE LIABLE TO ANYONE FOR SPECIAL, COLLATERAL, INCIDENTAL, OR CONSEQUENTIAL DAMAGES IN CONNECTION WITH OR ARISING OUT OF PURCHASE OR USE OF THESE MATERIALS. THE SOLE AND EXCLUSIVE LIABILITY TO AUTODESK, INC., REGARDLESS OF THE FORM OF ACTION, SHALL NOT EXCEED THE PURCHASE PRICE OF THE MATERIALS DESCRIBED HEREIN. Autodesk, Inc., reserves the right to revise and improve its products as it sees fit. This publication describes the state of the product at the time of publication, and may not reflect the product at all times in the future.Autodesk TrademarksThe following are registered trademarks of Autodesk, Inc., in the USA and/or other countries: 3D Props, 3D Studio, 3D Studio MAX, 3D Studio VIZ, 3DSurfer, 3ds max, ActiveShapes, ActiveShapes (logo), Actrix, ADI, AEC Authority (logo), AEC-X, Animator Pro, Animator Studio, ATC, AUGI, AutoCAD, AutoCAD LT, AutoCAD Map, Autodesk, Autodesk Envision, Autodesk Inventor, Autodesk (logo), Autodesk Map, Autodesk MapGuide, Autodesk Streamline, Autodesk University (logo), Autodesk View, Autodesk WalkThrough, Autodesk World, AutoLISP, AutoSketch, backdraft, Biped, bringing information down to earth, Buzzsaw, CAD Overlay, Character Studio, Cinepak, Cinepak (logo), cleaner, Codec Central, combustion, Design Your World, Design Your World (logo), EditDV, Education by Design, gmax, Heidi, HOOPS, Hyperwire, i-drop, Inside Track, IntroDV, Kinetix, lustre, MaterialSpec, Mechanical Desktop, NAAUG, ObjectARX, Physique, Planix, Powered with Autodesk Technology (logo), ProjectPoint, RadioRay, Reactor, Revit, Softdesk, Texture Universe, The AEC Authority, The Auto Architect, VISION*, Visual, Visual Construction, Visual Drainage, Visual Hydro, Visual Landscape, Visual Roads, Visual Survey, Visual Toolbox, Visual Tugboat, Visual LISP, Volo, WHIP!, and WHIP! (logo).The following are trademarks of Autodesk, Inc., in the USA and/or other countries: AutoCAD Learning Assistance, AutoCAD LT Learning Assistance, AutoCAD Simulator, AutoCAD SQL Extension, AutoCAD SQL Interface, AutoSnap, AutoTrack, Built with ObjectARX (logo), burn, , CAiCE, Cinestream, Civil 3D, cleaner central, ClearScale, Colour Warper, Content Explorer, Dancing Baby (image), DesignC enter, Design Doctor, Designer's Toolkit, DesignKids, DesignProf, DesignServer, Design Web Format, DWF, DWFit, DWG Linking, DXF, Extending the Design Team, GDX Driver, gmax (logo), gmax ready (logo),Heads-up Design, jobnet, ObjectDBX, onscreen onair online, Plans & Specs, Plasma, PolarSnap, Productstream, Real-time Roto, Render Queue, Visual Bridge, Visual Syllabus, and Where Design Connects.Autodesk Canada Co. TrademarksThe following are registered trademarks of Autodesk Canada Inc. in the USA and/or Canada, and/or other countries: discreet, fire, flame, flint, flint RT, frost, glass, inferno, MountStone, riot, river, smoke, sparks, stone, stream, vapour, wire.The following are trademarks of Autodesk Canada Inc., in the USA, Canada, and/or other countries: backburner, Multi-Master Editing.Third Party TrademarksAll other brand names, product names or trademarks belong to their respective holders.Third Party Software Program CreditsACIS Copyright© 1989-2001 Spatial Corp. Portions Copyright© 2002 Autodesk, Inc.Copyright© 1997 Microsoft Corporation. All rights reserved.Flash ® is a registered trademark of Macromedia, Inc. in the United States and/or other countries.International CorrectSpell™ Spelling Correction System© 1995 by Lernout & Hauspie Speech Products, N.V. All rights reserved. InstallShield™ 3.0. Copyright© 1997 InstallShield Software Corporation. All rights reserved.PANTONE® Colors displayed in the software application or in the user documentation may not match PANTONE-identified standards. Consult current PANTONE Color Publications for accurate color.PANTONE® and other Pantone, Inc. trademarks are the property of Pantone, Inc.© Pantone, Inc., 2002Pantone, Inc. is the copyright owner of color data and/or software which are licensed to Autodesk, Inc., to distribute for use only in combination with certain Autodesk software products. PANTONE Color Data and/or Software shall not be copied onto another disk or into memory unless as part of the execution of this Autodesk software product.Portions Copyright© 1991-1996 Arthur D. Applegate. All rights reserved.Portions of this software are based on the work of the Independent JPEG Group.RAL DESIGN© RAL, Sankt Augustin, 2002RAL CLASSIC© RAL, Sankt Augustin, 2002Representation of the RAL Colors is done with the approval of RAL Deutsches Institut für Gütesicherung und Kennzeichnung e.V. (RAL German Institute for Quality Assurance and Certification, re. Assoc.), D-53757 Sankt Augustin.Typefaces from the Bitstream® typeface library copyright 1992.Typefaces from Payne Loving Trust© 1996. All rights reserved.AutoCAD 2006 is produced under a license of data derived from DIC Color Guide® from Dainippon Ink and Chemicals, Inc. Copyright © Dainippon Ink and Chemicals, Inc. All rights reserved. DIC Color Guide computer color simulations used in this product may not exactly match DIC Color Guide, DIC color Guide Part 2 identified solid color standards. Use current DIC Color Guide Manuals for exact color reference. DIC and DIC Color Guide are registered trademarks of Dainippon Ink and Chemicals, Inc.Printed manual and help produced with Idiom WorldServer™.WindowBlinds: DirectSkin™ OCX © Stardock®AnswerWorks 4.0 ©; 1997-2003 WexTech Systems, Inc. Portions of this software © Vantage-Knexys. All rights reserved.The Director General of the Geographic Survey Institute has issued the approval for the coordinates exchange numbered TKY2JGD for Japan Geodetic Datum 2000, also known as technical information No H1-N0.2 of the Geographic Survey Institute, to be installed and used within this software product (Approval No.: 646 issued by GSI, April 8, 2002).Portions of this computer program are copyright © 1995-1999 LizardTech, Inc. All rights reserved. MrSID is protected by U.S. Patent No. 5,710,835. Foreign Patents Pending.Portions of this computer program are Copyright ©; 2000 Earth Resource Mapping, Inc.OSTN97 © Crown Copyright 1997. All rights reserved.OSTN02 © Crown copyright 2002. All rights reserved.OSGM02 © Crown copyright 2002, © Ordnance Survey Ireland, 2002.FME Objects Engine © 2005 SAFE Software. All rights reserved.GOVERNMENT USEUse, duplication, or disclosure by the U.S. Government is subject to restrictions as set forth in FAR 12.212 (C ommercial Computer Software-Restricted Rights) and DFAR 227.7202 (Rights in Technical Data and Computer Software), as applicable.1 2 3 4 5 6 7 8 9 10ContentsChapter 1Welcome to Revit Structure 4 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 Copyright Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 Network Deployment Installation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 Licensing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 Standalone Licensing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3Network License Server Setup . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 Install the Network License Manager Tools . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4Obtain Host Name ID Using LMTools . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4Obtain a Network License File . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4Set Up the Network License File . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Configure the Network License Server . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7Combining Network License Files . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7Distributed License Server Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Redundant License Server Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9Network License Client Setup . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10Licensing from Previous Versions of Revit Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 Network License Cascading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10License Server Reporting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10Licensing Extension . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10License Transferring . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11License Borrowing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Subscription Center . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11 Using Help . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12 The Interface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12 Chapter 2Getting Started . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13 What is a Project? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 Creating a Project . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 Beginning a Project . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 Element Classifications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15 Adding Levels and Grids . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15 Massing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17 Massing and Building Maker . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17Massing Terminology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Typical Uses of Massing Studies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Using Imported Geometry in Mass Versus Generic Model Families . . . . . . . . . . . . . . . . . . . . . 18Controlling Visibility of Mass Instances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Using the Mass Editor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Working with Loaded Mass Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Working with In-Place Mass Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20 Multiple Mass Instances in a Project . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21 Common Mass Instance Parameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22Creating Building Elements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22 Building Elements from Massing or Generic Models . . . . . . . . . . . . . . . . . . . . . . . . . . 22 Structural Templates and Structural Analytical Templates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32 Starting a Project with the Structural Template . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32Contents | vCreating Custom Project Templates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32 Creating and Saving the Template . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33 Chapter 3Sketching . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35 Sketching Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36 Creating Sketched Lines . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36Sketching Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36 Sketching Tips . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37 Sketching Design Bar Commands . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38Snap Points . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39Jump Snaps . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40Snapping Tips . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40Valid/Invalid Sketches . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41Modifying Sketches . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42 Creating Ellipses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42 Sketching a Full Ellipse . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42Sketching a Partial Ellipse . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43Resizing an Ellipse . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43 Resizing with Drag Controls . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43 Rotating an Ellipse . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44 Setting the Work Plane . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44 Making the Work Plane Visible . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45Tips for Work Plane Visibility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45Elements Associated with Work Planes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45 Chapter 4Constraint Elements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47 Constraint Elements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48 Creating Constraints . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48Constraints with Dimensions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48Equality Constraints . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48 EQ Label . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49 Constraints and Worksets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49Removing Constraints . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49Constraint Elements Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49 Chapter 5Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51 Family Editor Basics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52 Family Templates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52 Basic Family Templates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52 Design Environment for Creating Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53 Design Considerations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53 General Rules for Geometry Creation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53 Procedure to Define a Family Origin . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54Is Reference Values . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54Reference Lines . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55 Creating Family Types . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57 Within the Family Editor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57Within a Project . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58 Setting Subcategories . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58 Subcategory Procedure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58 Families Tips . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58 Families Included In The Library . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58 Editing Loaded Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59 Edit a Family within a Project or Nested Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59 Reloading Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59 Reload a Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60 Copying Family Types Between Projects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60 Copying a Family Type from the Project Browser . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60Copying a Family Type from the Document Window . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60 Strong and Weak References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60 vi | ContentsSetting Strong and Weak References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61 Dimensions with Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61 Automatic Sketch Dimensions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61 Visibility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61 Effects on Your Geometry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62 Dimensioning with Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62 Labeling Dimensions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62 Dimensioning with Families Tips . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63 Visibility and Detail Levels . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63 Setting Family Geometry Visibility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63 Visibility of Imported Geometry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64 Visibility During Sketching . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64 Setting Detail Level . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64 Instance Parameters and Shape Handles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64 Creating Instance Parameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64 Adding Shape Handles to a Component Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65 Family Types . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68 Creating Family Types . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68 Adding a Type to a Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68 Using Formulas for Numerical Parameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69 Adding a Formula to a Parameter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69 Valid Formula Syntax . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69 Valid Formula Abbreviations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70 Conditional Statements in Formulas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70 Adding a Website Link to Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71 Creating New Family Parameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71 Creating New Parameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71 Modifying Family Parameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72 Profile Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72 Family Templates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73 Creating a Profile Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73 Loading the Family into a Project . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74 Family Editor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74 Family Editor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74 Family Editor Commands . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74 Duplicating Parameterized Elements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76 Solid Geometry Tools . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77 Creating Solid Revolves . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77 Revolved Geometry Tips . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78 Creating Solid Sweeps . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78 Sweep Tips . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79 Creating Solid Blends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79 Blend Tips . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81 Creating a Solid Extrusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81 Extrusion Tips . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82 Void Geometry Tools . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82 Void Extrusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82 Void Blends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83 Void Revolves . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84 Void Sweeps . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85 Cut Geometry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86 Creating a Subcategory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87 Creating Subcategories for the Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87 Assigning the Subcategory to the Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87 Subcategory Tip . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87 Family Geometry Properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87 Extrusion Properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87 Blend Properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88 Revolved Geometry Properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88Contents | viiSweep Properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88Line Properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89 Family Category and Parameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89 Assigning Family Categories . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89Specifying the Always Vertical Parameter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90Specifying the Always Export as Geometry Parameter . . . . . . . . . . . . . . . . . . . . . . . . . . 90Using the Shared Parameter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90Specifying the Work Plane-Based Parameter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91 Loading a Family into Projects or Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91 Load into Projects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91 Creating Vertical Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92 Setting the Always Vertical Parameter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92 Creating Work Plane-based and Face-based Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92 Creating a Work Plane-based Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93 Nested Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93 Family Loading Restrictions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93Creating a Nested Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94Visibility of Nested Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94Creating a Nested Family with Interchangeable Subcomponents . . . . . . . . . . . . . . . . . . . . . . 94 Creating and Applying a Family Type Parameter . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94 Shared Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95 Creating Shared Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95 Creating a Nested Family of Shared Components . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95 Loading Shared Families into a Project . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96Working with Shared Families in a Project . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96Scheduling Shared Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97 In-Place Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97 Creating an In-Place Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98Create Command . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98Editing the In-Place Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98In-Place Families Tip . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98 Changing the Appearance of the Detail Component . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98 Linking Family Parameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98 Creating Family Parameter Links . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99Linking Family Parameters Tip . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99 Loading Generic Annotations into Model Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99 Example Procedure for Adding a Generic Annotation . . . . . . . . . . . . . . . . . . . . . . . . . . . 100 Creating a Column Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101 Starting a Column Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102Specifying How a Column Displays in Project Plan Views . . . . . . . . . . . . . . . . . . . . . . . . . 102 Creating a Truss Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103 Creating a New Family Type . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103 Creating a Label . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 105 Formatting Parameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106Applying the Label to a Tag in the Project . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106Applying the Label to a Titleblock in the Project . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107 Creating a Section Head Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107 Starting the Section Head Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107Setting Parameters for the Section Head . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107Tip for Creating a Section Head Family . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 108 Creating Additional Families . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 108 Automatic Cutouts in Floors and Ceilings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 108 Titleblocks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 108 Creating Titleblocks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 108Titleblock Tips . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 109 viii | Contents。

SAP FI 4.6 Exercises Chipsun, Inc. accumulates sales withholding tax (at time of invoice) on all purchases from a Flagship Corp., a foreign vendor. The rate of withholding tax varies depending on the amount on the invoice. The rates are as follows:•For the first $1,000 of an invoice, 10% is to be withheld•For the next $10,000 of the invoice, 5% is to be withheld•For the next $100,000 of the invoice 1% is to be withheldThe formula sheet is as follows:Scenario 1Assumptions:•The tax code rate is based on 100% of the base amount•No vendor exemption rate on this tax type-tax code combination•The maximum rate including withholding tax amount is well beyond the invoice amount.Example 1. If an invoiced amount is $500 then the withholding tax will be $50Calculation → $500 * 10% = $50Example 2. If the invoiced amount is $10 000 then the withholding tax will be $550Calculation → $1,000 * 10% = $100[$10,000 - $1,000]*5% = $450$550Example 3. If the invoiced amount is $50 000 then the withholding tax will be $990Calculation → $1,000 * 10% = $100[$11,000 - $1,000] * 5% = $500[$50,000 - $11,000] * 1% = $390$990SAP FI 4.6 Exercises[$11,000 - 1,000] * 5% = $ 500[$111,000 - 11,000] * 1% = $1,000$1,600Scenario 2Assumptions:•The tax code rate is based on 80% of the base amount•No vendor exemption rate on this tax type-tax code combination•The maximum rate including withholding tax amount is well beyond the invoice amount.Example 1. If an invoiced amount is $500 then the withholding tax will be $40Calculation → [$500 * 80%] * 10% = $40Example 2. If the invoiced amount is $10,000 then the withholding tax will be $450Calculation → $1,000*10% = $100[[$10,000 * 80%] - $1,000]] * 5% = $350$450Example 3. If the invoiced amount is $50,000 then the withholding tax will be $890Calculation → $1,000 * 10% = $100[$11,000 - $1,000] * 5% = $500[[$50,000 * 80%] -$11,000] *1% = $290$890Example 4. If the invoiced amount is $115,000 then the calculation would be $1,410Calculation → $1,000 * 10% = $ 100[$11,000 – 1,000] * 5% = $ 500[[$115 000 * 80%] - 11 000] * 1% = $ 810$1,410Note: Only when the calculated (To base amount) base amount has reached its maximum does the carryover end.SAP FI 4.6 ExercisesScenario 3Assumptions:•The tax code rate is based on 80% of the base amount and a 3% vendor exemption•No vendor exemption rate on this tax type-tax code combination•The maximum rate including withholding tax amount is well beyond the invoice amount.Example 1. If an invoiced amount is $500 then the withholding tax will be $38.8Calculation → [$500 * 80%] * 10% = $40Less $40 * 3% = $ 1.20$38.80Example 2. If the invoiced amount is $10,000 then the withholding tax will be $436.50Calculation → $1,000*10% = $100[[$10,000 * 80%] - $1,000]] * 5% = $350Less $450 * 3% = $ 13.50$436.50Example 3. If the invoiced amount is $50,000 then the withholding tax will be $863.30Calculation → $1,000 * 10% = $100[$11,000 - $1,000] * 5% = $500[[$50,000 * 80%] -$11,000] *1% = $290Less $890 * 3% = $ 26.70$863.30Example 4. If the invoiced amount is $115,000 then the calculation would be $1,367.70 Calculation → $1,000 * 10% = $ 100[$11,000 – 1,000] * 5% = $ 500[[$115 000 * 80%] - 11 000] * 1% = $ 810Less $1,410 * 3% = $ 42.30$1,367,70 Note: Only when the calculated (To base amount) base amount has reached its maximum does the carryover end.。