Management Accounting Chapter17

- 格式:pdf

- 大小:687.19 KB

- 文档页数:55

主讲:李相志⏹本科教育中的《管理会计》课程要求学生掌握如下内容:成本概念及成本计算的基本方法经营预测的基本方法短期和长期决策的基本方法预算编制的基本方法成本差异分析和业绩考核的基本方法学习内容⏹第一章管理会计概论⏹第二章产品成本计算的基本方法⏹第三章成本分配和作业成本计算⏹第四章成本性态和两种类型的损益表⏹第五章本量利分析⏹第六章经营决策分析⏹第七章长期投资决策分析⏹第八章全面预算与预算控制⏹第九章标准成本和差异分析⏹第十章分权管理与责任会计第一章管理会计概论第一节管理会计的形成与发展会计的定义⏹我国:会计是一种经济管理活动,是经济管理的重要组成部分。

它是通过收集、加工和利用以一定的货币单位作为计量标准的经济信息,对经济活动进行组织、控制、协调和指导的一种管理活动。

⏹西方:会计是一个信息系统,是为了使信息使用者能够作出有根据的判断和决策而认定、计量和传递经济信息的程序会计的目的⏹所有会计信息都是为了帮助有关人员作出经济决策⏹会计信息的特征⏹对决策的相关性和有用性会计信息的使用者⏹利用信息作出短期计划和控制日常经营的内部管理人员⏹利用信息作出非日常性决策和制定全面政策与长期计划的内部管理人员⏹利用信息作出有关决策的外部各方,如投资者、债权人、政府当局等。

会计的两大分支⏹财务会计(Financial accounting)是为企业外部使用者提供财务信息的会计。

它主要通过提供定期的财务报表,为企业外部同企业有经济利益关系的各种社会集团服务,发挥会计信息的外部社会职能。

⏹管理会计(Management accounting)是为企业内部使用者提供管理信息的会计。

它通过对信息进行确认、计量、收集、分析、整理、解释和汇报以帮助企业内部管理人员正确进行经营决策和改善经营管理,发挥会计信息的内部管理职能。

管理会计的形成与发展(一)执行性管理会计阶段(20世纪初到50年代)⏹成本计算得到扩充⏹标准成本制度(standard cost system)与预算控制(budget control)的确立,差异分析、业绩报告的使用。

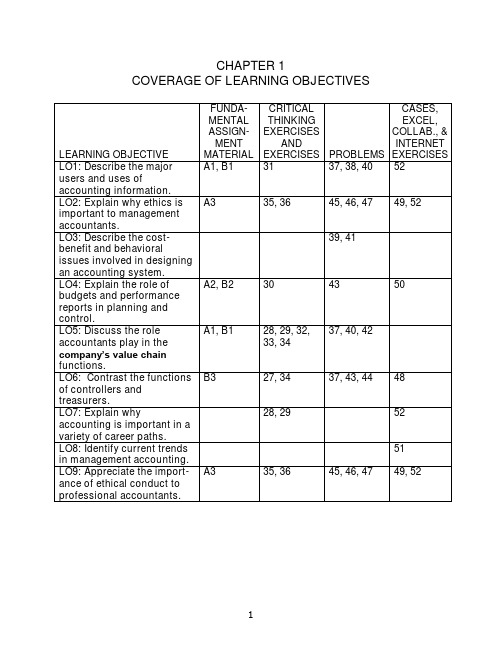

COVERAGE OF LEARNING OBJECTIVESManagerial Accounting and the Business Organization1-A1 (10-15 min.)Because the accountant's duties are often not sharply defined, some of these answers could be challenged:1. Attention directing and problem solving. Budgeting involves makingdecisions about planned activities -- hence, aiding problem solving.Budgets also direct attention to areas of opportunity or concern --hence, directing attention. Reporting against the budget also has ascorekeeping dimension.2. Problem solving. Helps a manager assess the impact of a decision.3. Scorekeeping. Reports on the results of an operation. Could also beattention direction if scrap is an area that might require management decisions.4. Attention directing. Focuses attention on areas that need attention.5. Attention directing. Helps managers learn about the informationcontained in a performance report.6. Scorekeeping. The statement merely reports what has happened.7. Problem solving. The cost comparison is apparently useful becausethe manager wishes to decide between two alternatives. Thus, it aids problem solving.8. Attention directing. Variances point out areas where results differfrom expectations. Interpreting them directs attention to possiblecauses of the differences.9. Problem solving. Aids a decision about where the parts should bemade.10. Scorekeeping. Determining a depreciation schedule is simply anexercise in preparing financial statements to report the results ofactivities.1. Budgeted Actual DeviationsAmounts Amounts or Variances Room rental $ 140 $ 140 $ 0Food 800 1,008 208UEntertainment 600 600 0Decorations 220 190 30FTotal $1,760 $1,938 $178U2. Because of the management by exception rule, room rental andentertainment require no explanation. The actual expenditure forfood exceeded the budget by $208. Of this $208, $150 is explained by attendance of 15 persons more than budgeted (at a budget of $10 per person) and $58 is explained by expenditures above $10 per person.Actual expenditures for decorations were $30 less than the budget. If all desired decorations were purchased, the decorations committee should be commended for their savings.1-A3 (10 min.)All of the situations raise possibilities for violation of the integrity standard. In addition, the manager in each situation must address an additional ethical standard:1. The General Mills manager must respect the confidentiality standard.He or she should not disclose any information about the new cereal.2. Roberto must address his level of competence for the assignment. Ifhis supervisor knows his level of expertise and wants an analysisfrom a “layperson” point of view, he should do it. However, if thesupervisor expects an expert analysis, Roberto must admit his lackof competence.3. The objectivity standard should cause Helen to decline to omit theinformation from her budget. It is relevant information, and itsomission may mislead readers of the budget.Because the accountant’s duties are often not sharply defined, some of these answers could be challenged:1. Scorekeeping. Records events.2. Scorekeeping. Simply recording of what has happened.3. Problem solving. Helps a manager decide between alternatives.4. Attention directing. Directs attention to the use of overtime labor.5. Problem solving. Provides information to managers for decidingbetween alternatives.6. Attention directing. Directs attention to why nursing costs increased.7. Attention directing. Directs attention to areas where actual resultsdiffered from the budget.8. Problem solving. Helps the vice-president to decide which course ofaction is best.9. Scorekeeping. Records costs in the department to which theybelong.10. Scorekeeping. Records actual overtime costs.11. Attention directing. Directs attention to stores with either high or lowratios of advertising expenses to sales.12. Attention directing. Directs attention to causes of returns of the drug.13. Attention directing or problem solving, depending on the use of theschedule. If it is to identify areas of high fuel usage it is attentiondirecting. If it is to plan for purchases of fuel, it is problem solving. 14. Problem solving. Provides information for deciding between twoalternative courses of action.15. Scorekeeping. Records items needed for financial statements.1 & 2. Budget Actual VarianceSales $75,000 $74,860 $ 140UCosts:Fireworks $35,000 $39,500 $4,500ULabor 15,000 13,000 2,000FOther 8,000 8,020 20UProfit $17,000 $14,340 $2,660U3. The cost of fireworks was $4,500 ÷ $35,000 = 13% over budget. Didfireworks suppliers raise their prices? Did competition cause retailprices to be lower than expected? There should be someexplanation for the extra cost of fireworks. Also, the labor cost was$2,000 ÷ $15,000 =13% below budget. It would be useful to discover why this cost was saved. Both sales and other costs were very close to budget.1-B3 (10 - 15 min.)1. Treasurer. Analysts affect the company's ability to raise capital,which is the responsibility of the treasurer.2. Controller. Advising managers aids operating decisions.3. Controller. Advice on cost analysis aids managers' operatingdecisions.4. Controller. Divisional financial statements report on operations.Financial statements are generally produced by the controller'sdepartment.5. Treasurer. Financing the business is the responsibility of thetreasurer.6. Controller. Tax returns are part of the accounting process overseenby the controller.7. Treasurer. Insurance, as with other risk management activities, isusually the responsibility of the treasurer.8. Treasurer. Allowing credit is a financial decision.1-1 Decision makers within and outside an organization use accounting information for three broad purposes:1. Internal reporting to managers for planning and controllingoperations.2. Internal reporting to managers for special decision-making and long-range planning.3. External reporting to stockholders, government, and other interestedparties.1-2 The emphasis of financial accounting has traditionally been on the historical data presented in the external reports. Management accounting emphasizes planning and control purposes.1-3 The branch of accounting described in the quotation is management accounting.1-4 Scorekeeping is the recording of data for a later evaluation of performance. Attention directing is the reporting and interpretation of information for the purpose of focusing on inefficiencies of operation or opportunities for improvement. Problem solving presents a concise analysis of alternative courses of action.1-5 GAAP applies to publicly issued annual financial reports. Internal accounting reports are not restricted by GAAP.1-6 Yes, but it covers more than that. The Foreign Corrupt Practices Act applies to all publicly-held companies and covers the quality of internal accounting control as well as bribes and other matters.1-7 Users cannot easily observe the quality of accounting information. Thus, they rely on the integrity of accountants to be sure the information is accurate. Information that is unreliable is worthless, so if accountants do not have a reputation for integrity, the information they produce will not have value.1-8 Three examples of service organizations are banks, insurance companies, and public accounting firms. Such organizations tend to be labor intensive, have outputs that are difficult to define and measure, and have both inputs and outputs that are difficult or impossible to store.1-9 Two considerations are cost-benefit balance and behavioral effects. Cost-benefit balance refers to how well an accounting system helps achieve management's goals in relation to the cost of the system. The behavioral consideration specifies that an accounting system should be judged by how it will affect the behavior (that is, decisions) of managers.1-10 Yes. The act of recording events has become as much a part of operating activities as the act of selling or buying. For example, cash receipts and disbursements must be traced, and receivables and payables must be recorded, or else gross confusion would ensue.1-11 A budget is a prediction and guide; a performance report is a tabulation of actual results compared with the budget; and a variance reconciles the differences between budget and actual.1-12 No. Management by exception means that management spends more effort on those areas that seem to be out of control and less on areas that are functioning as planned. This method is an efficient way for managers to decide where to put their time and effort.1-13 No. There is no perfect system of automatic control, nor does accounting control anything. Accounting is a tool used by managers in their control of operations.1-14 Information that is relevant for decisions about a product depends on the product's life-cycle stage. Therefore, to prepare and interpret information, accountants should be aware of the current stage of a product's life cycle.1-15 The six functions are: (1) research and development – generation and experimentation with new ideas; (2) product and service process design – detailed design and engineering of products; (3) production – use of resources to produce a product or service; (4) marketing - informing customers of the value and features of products or services; (5) distribution – delivering products or services to customers; and (6) customer service –support provided to customers.1-16 No. Not all of the functions are of equal importance to the success of a company. Measurement and reporting should focus on those functions that enable a company to gain and maintain a competitive edge.1-17 Line managers are directly responsible for the production and sale of goods or services. Staff managers have an advisory function – they support line managers.1-18 Management accountants are the information specialists, even in non-hierarchical companies. However, in such companies they are more directly involved with managers and are often parts of cross-functional teams.1- 19 A treasurer is concerned mainly with the company's financial matters, the controller with operating matters. In large organizations, there are sufficient activities associated with both financial and operating matters to justify two separate positions. In a small organization the same person might be both treasurer and controller.1-20 The four parts of the CMA examination are: (1) economics, finance, and management, (2) financial accounting and reporting, (3) management reporting, analysis, and behavioral issues, and (4) decision analysis and information systems.1-21 This is not true. About one-third of CEOs come from finance or accounting backgrounds. Accounting is excellent preparation for top management positions because accountants are often exposed to many parts of the company early in their careers.1-22 Changes in technology are affecting how accountants operate. They must be able to account for e-commerce transactions efficiently and safely, they often must integrate their accounting systems into ERP systems, and an increasing number are beginning to use XBRL to communicate information electronically.1-23 The essence of the just-in-time philosophy is the elimination of waste, accomplished by reducing the time products spend in the production process and trying to eliminate the time spent in processes that do not add value to the product.1-24 Moving tools and products that are in process from one location to another in a plant is an activity that does not add value to the product. So changing the plant layout to eliminate wasted movement and time improves production efficiency.1-25 The four major responsibilities are: (1) competence - develop knowledge; know and obey laws, regulations, and technical standards; and perform appropriate analyses, (2) confidentiality - refrain from disclosing or using confidential information, (3) integrity - avoid conflicts of interest, refuse gifts that might influence actions, recognize limitations, and avoid activities that might discredit the profession, and (4) objectivity - communicate information fairly, objectively, and completely, within confidentiality constraints.1-26 Standards do not always provide the needed guidance. Sometimes an action borders on being unethical, but it is not clearly an ethical violation. Other times two ethical standards conflict. In situations such as these, accountants must make ethical judgments.1-27 (5-10 min.)Typical activities associated with the treasurer function include:❑Provision of capital❑Investor relations❑Short-term financing❑Banking and custody❑Credits and collections❑Investments❑Risk managementTypical activities associated with the controller function include:❑Planning for control❑Reporting and interpreting❑Evaluating and consulting❑Tax administration❑Government reporting❑Protection of assets❑Economic appraisal1-28 (5-10 min.)Activities 2, 4, 5, and 6 are primarily associated with marketing decisions. The management accountant would assist in these decisions as follows: Boeing Company’s pricing decision requires cost data relevant to the new method of distributing spare parts. will need to know the costs of the advertising program as well as the additional costs of other value chain functions resulting from increased sales. TexMex Foods will need to know the incremental revenues and incremental costs associated with the special order. Target Stores needs to know the impact on both revenues and costs of closing one of its stores.Activities 1, 7, and 8 are primarily associated with production decisions. The management accountant would assist in these decisions as follows. Porsche Motor Company needs an analysis of the costs associated with purchasing the part compared to the costs of making the part. Dell will need to know the costs of the training program and the savings associated with increased efficiencies in the setup and changeover activities. General Motors needs to know the costs and salvage values of the replacement equipment, the proceeds of the sale of the old equipment, and the operating savings associated with the use of the new equipment.1-30 (5 min.)1. Management 4. Management 7. Financial2. Management 5. Management3. Financial 6. Financial1. Performance ReportBudget Actual Variance Explanation Revenues $220,000 $228,000 $8,000 F Additional salesfrom newproducts* Advertising cost 15,000 16,500 (1,500) U New advertisingCampaignNet $6,500 F* From the New Products Report, seven new products were added. This exceeded the plan to add six.2.Factors that may not have been considered include:a.The costs of new products may have exceeded their price.b.Customer satisfaction with new products may not have been partof the new products report.petitors’ reactions to the Starbucks store’s actions may nothave been anticipated.d.External uncontrollable factors such as increases in operatingcosts, adverse weather, changes in the overall economy, newcompetitors entering the market, or key employee turnover mayhave decreased efficiency.1-32 (5 min.)1. Line, support 3. Staff, marketing 5. Staff, support2. Staff, support 4. Line, marketing 6. Line, productionMicrosoft is a company that most students will know and have some understanding of what functions its managers perform. Nevertheless, this may not be an easy exercise for those who have little knowledge of how companies operate.Research & development – Because software companies must continually come out with new products and upgrades to their current products this is a critical function for Microsoft. More than one-fourth of Microsoft’s operating expenses are devoted to R&D.Design of products, services, or processes – For Microsoft the design and R&D process probably overlap considerably. Product design is critical; process design is probably not. One essential part of design is beta testing – that is, field testing of new software. This quality-control step is essential to prevent customer dissatisfaction with new products.Production – Microsoft produces disks and CD-ROMs and the manuals and packaging to go with them. However, they are increasingly delivering software over the Internet, which takes an initial process design and then few resources. It is not likely a major focus for Microsoft.Marketing – Microsoft spends more on sales and marketing than on any other operating expense. Increasing competition in software sales makes marketing essential to the company’s future. This function includes advertising and direct marketing activities, but it also includes activities of the company’s sales force. Distribution – This function is becoming simpler for Microsoft as it delivers more and more software over the Internet. Although the company must stay abreast of competitors in delivery methods, this is not likely to create a major competitive advantage or disadvantage for Microsoft.Customer service – Customer service is important, but Microsoft tries to minimize its costs in this area by product design – making things work right without needing deep computer expertise. Still, poor customer service can severely impact a company, so Microsoft must attend to it.Support functions – Most of the time these are not a major focus. There is one exception recently for Microsoft. Legal support has been front and center. The very future of the company was based on court judgments for which good legal support was essential.The management accountant's major purpose is to provide information that helps line managers in making decisions regarding the planning and controlling of operations. The accountant supplies information for scorekeeping, attention directing, and problem solving. In turn, managers use this and other information for routine and non-routine decisions and for evaluating subordinates and the performance of sub-parts of the organization. Management accountants must walk a delicate line between (1) making sure that managers are properly using the pertinent information and (2) making sure that the managers, not the accountants, are doing the actual managing.1-35(5 min.)Other costs of a poor ethical environment include legal costs and costs due to high employee turnover. Other benefits of a good ethical environment include low employee turnover, low loss from internal theft, and improved customer satisfaction resulting from better quality and service (that result from a more productive work environment).1-36(5 min.)There are numerous examples.“You understand how important it is to record this sale before year end, don’t you?”“Doing it this way is common for all companies in our business, so don’t worry!”“Trust me, the inventory is at the warehouse.”This problem can form the basis of an introductory discussion of the entire field of management accounting.1. The focus of management accounting is on helping internal users tomake better decisions, whereas the focus of financial accounting ison helping external users to make better decisions. Managementaccounting helps in making a host of decisions, including pricing,product choices, investments in equipment, making or buying goods and services, and manager rewards.2. Generally accepted accounting standards or principles affect bothinternal and external accounting. However, change in internalaccounting is not inhibited by generally accepted principles. Forexample, if an organization wants to account for assets on the basisof replacement costs for internal purposes, no outside agency canprohibit such accounting. Of course, this means that organizationsmay have to keep more than one set of records. There is nothingimmoral or unethical about having multiple sets of books, but theyareexpensive. Accounting data are commodities, just like butter or eggs.Innovations in internal accounting systems must meet the samecost-benefit tests that other commodities endure. That is, theirperceived increases in benefits must exceed their perceivedincreases in costs. Ultimately, benefits are measured by whetherbetter decisions are forthcoming in the form of increased net profitsor cost savings.3. Budgets, the formal expressions of management plans, are a majorfeature of management accounting, whereas they are not asprominent in financial accounting. Budgets are major devices forcompelling and disciplining management planning.4. An important use of management accounting information is theevaluation of performance, which often takes the form of comparisonof actual results against budgets, providing incentives and feedback to improve future decisions.5.Accounting systems have an enormous influence on the behavior ofindividuals affected by them. Management accounting is moreconcerned with the likely behavioral effects of various accountingalternatives that may be adopted than is financial accounting.1-38(10 min.)The main point of this question is that cost information is crucial for decisions regarding which products and services should be emphasized or de-emphasized. The incentives to measure costs precisely are far greater when flat fees are being received instead of reimbursements of costs.Note, too, that nonprofit organizations and profit-seeking organizations have similar desires regarding management accounting. Accountability is now in fashion for many purposes, including justification of prices, cost control, and response to criticisms by investors (whether they be donors, taxpayers, or others).When somebody's money is at stake, accounting systems get much love and attention. In a survey of 550 hospitals, hospital financial executives said that improved cost accounting systems "are crucial to responding to changes in hospital payment mechanisms and that better cost information is essential for more profitable and efficient operations." Hospitals will increasingly identify costs by product (type of case), not just by departments.1-39 (10 min.)Paperwork and systems often seem to become ends in themselves. However, the rationale that should underlie systems design is the cost-benefit philosophy or approach that is implied in the quotation. The aim is to get the managers and their subordinates collectively to make better decisions under one system versus another system -- for a given level of costs.Marks & Spencer should look at each of the management accounting reports it produces with an eye toward how it helps managers make better decisions. Does it provide needed scorekeeping? Does it direct attention to aspects of operations that might need altering? Does it provide information for specific management decisions? These types of questions will help identify the benefit of the information in the report.Then the company must consider the cost – not just the cost of collecting the data and preparing the reports, but the cost of educating managers to use the information and the cost of the time to read, digest, and act on the information. Too much information may be costly because it makes it time-consuming (and thus costly) to sift through the reams of information to find the few items that are important. And one cost may be the loss of important information because the total volume of information makes it too difficult to ferret out the important items.1-40(10 min.) Financial information is important in all companies. But how managers get and use financial information can differ depending on the culture and philosophies of the company.Top executives of a company often represent a functional area that is critical to the comparative economic advantage of the company. If technology is crucial, engineers generally hold important executive positions. If marketing differentiates the company from others, marketing executive s usually dominate. But regardless of the source of a company’s competitive advantage, its success will eventually be measured in economic terms. They must attend to financial aspects to thrive and often even to survive.Management accountants must work with the dominant managers in any organization. The modern trend toward use of cross-functional teams places management accountants at the center of the action regardless of what type of managers and executives dominate. Most companies realize that there is a financial dimension to almost every major decision, so they want the financial experts, management accountants, involved in the decisions. But to be accepted as an important part of these teams, the management accountants must know how to help managers in various functional areas. In General Mills, if accountants can’t talk the language of marketing, they will not have great influence. In ArvinMeritor, if they do not understand the information needs of engineers they will not provide value.1-41(10-15 min.)1. Boeing's competitive environment and manufacturing processeschanged greatly during the 1990s. An accounting system that served them well in their old environment would not necessarily be optimal in the 2000s. Boeing's management probably thought that changes in the accounting system were necessary to produce the kind of information necessary to remain competitive.2. A cost-benefit criterion was probably used. Boeing's management maynot have quantified the costs and the benefits, but they certainlyassessed whether the new system would help decisions enough towarrant the cost of the system.Many of the benefits of a better accounting system are hard to measure.They affect many strategic decisions of an organization. Withoutaccurate product costs, management will find it difficult to assess the consequences of their decisions. An accurate accounting system will help to price airplanes and other products competitively.3. More accurate product costs will usually result in better managementdecisions. But if the cost of the accounting system that produces the more accurate costs is too high, it may be best to forego the increased accuracy. The benefit of better decisions must exceed the added cost of the system for a change to be desirable.1-42(10 min.)1. There are many possible activities for each function of Nike's valuechain. Some possibilities are:Research and development -- Determining changes in customers'tastes and preferences for shoes and sportswear to come up withnew products (maybe the next "Air Jordans").Product and service process design -- Design a shoe to meet theincreasing demands of competitive athletes.Production -- Determine where to produce products and negotiatecontracts with the companies producing them.Marketing -- Signing prominent athletes to endorse Nike's products.Distribution -- Select the best locations for warehouses fordistribution to retail outlets.Customer service -- Formulate return policies for products thatcustomers perceive to be defective.2. Accounting information that aids managers' decisions includes:Research and development -- Trends in sales for various products, to determine which are becoming more and less popular.Product and service process design -- Production costs of variousshoe designs.Production -- Measure total costs, including both purchase cost and transportation costs, for production in various parts of the world.Marketing -- The added profits generated by the added sales due toproduct endorsements.Distribution -- Storage and shipping costs for different alternativewarehouse locations.Customer service -- The net cost of returned merchandise, to becompared with the benefits of better customer relations.。

Course Notes 2016 Exams September 15 – June 17 ACCAPaper F2 - 双语讲义Management Accounting管理会计Tutor details2 Intro ductio n ACCA F 2No part of this publication may be reproduced, stored in a retrieval systemor transmitted, in any form or by any means, electronic, mechanical,photocopying, recording or otherwise, without the prior written permissionof First Intuition Publishing Ltd.Any unauthorised reproduction or distribution in any form is strictlyprohibited as breach of copyright and may be punishable by law.© First Intuition Publishing Ltd, 2015ACCA F 2Intro ductio n 3ContentsPageIntroduction 1Contents 31Course structure 52Course materials 53Qualification structure 64The exam 65Question types 76Exam tips 77How to study F2 88Study planner 91: Nature, source and purpose of management information 131Accounting for management 132Sources of data 153Cost classification 174Presenting information 262: Cost accounting techniques 331Accounting for material, labour and overheads 332Absorption and marginal costing 533Cost accounting methods 574Alternative cost accounting 703: Budgeting 751Nature and purpose of budgeting 752Statistical techniques 773Budget preparation 904Flexible budgets 975Capital budgeting and discounted cash flows 986Budgetary control and reporting 1107Behavioural aspects of budgeting 1134: Standard costing 1171Standard costing systems 1172Variance calculations and analysis 1183Reconciliation of budgeted and actual profit 1265: Performance measurement 1291Performance measurement overview 1292Performance measurement – application 1313Cost reductions and value enhancement 1414Monitoring performance and reporting 1424 Intro ductio n ACCA F 2Solutions to lecture examples 145Chapter 1 145 Chapter 2 146 Chapter 3 156 Chapter 4 164 Chapter 5 167Formulae sheets 169ACCA F 2Intro ductio n 5 1Course structureHome Study Introduction – How to Study F2To get off to the best possible start, we recommend you contact your tutor once you have receivedyour study materials. Your tutor will explain how to tackle your studies and get you started on yourfirst Study Session.If you prefer to get started straight away you should read “How to Study F2” below.Study sessionsThis study guide breaks down the syllabus into manageable study sessions, following the syllabus, andnumbered in accordance with the chapters in the Study notes. We tell you which chapters to read, andthen which questions to attempt from the Question Bank.It is not enough just to read the study notes. You must practise questions from the Question Bank asrecommended in each study session. The questions in the Question Bank are the same style as thosein the real exam and will give you exposure to all the possible pitfalls.It is better to attempt them as you go along, when the subject matter is fresh in your mind. You shouldcheck your answers with the answers and make sure you understand the suggested answer for anyquestions you get wrong.Revision sessionsWhen you have completed all the study sessions you should spend some time revising the core topicsWhen you are getting most of these right you are ready to attempt the Mock exam. If at all possibleyou should attempt this under real exam conditions, i.e. to the correct time and with no distractions.You can always come and sit your exam at First Intuition – just call your tutor to arrange a convenienttime.When you have completed the Mock you should check your answers. Make a note of any you getwrong and look at the model solution where given. If you still have any problems call your tutor orcome and see us for some final advice. If you score at least 60% in the Mock then you should be readyto take the real exam.2Course materialsYou will receive the following:First Intuition study notesFirst Intuition Question BankPasscards*Online Study Text (in conjunction with Kaplan EN-Gage)*produced by BPP Learning Media6 Intro ductio n ACCA F 23Qualification structureThe ACCA qualification is structured as follows.Fundamentals Level Knowledge Module F1 AB The Accountant in Business F2 MA Management Accounting F3 FA Financial AccountingFundamentals Level Skills Module F4 CL Corporate LawF5 PM Performance ManagementF6 TX TaxationF7 FR Financial ReportingF8 AA Audit & AssuranceF9 FM Financial Management Professional Level Essentials Module P1 PA Professional AccountantP2 CR Corporate ReportingP3 BA Business AnalysisProfessional Level Options Module (any two of these papers) P4 AFM Advanced Financial ManagementP5 APM Advanced Performance Management P6 ATX Advanced TaxationP7 AAA Advanced Audit & AssuranceAll papers are compulsory unless you gain exemptions from a relevant qualification. The modules must be attempted in the correct order, though you can sit the papers in any order. A maximum of fourpapers can be taken in any one exam sitting. Exams are in June and December each year. TheKnowledge Module subjects are examined by computer-based assessment and can be attempted atany time.4The examF2 is a two-hour computer-based or paper based examination.The paper is in two sectionsSection A contains 35 objective test questions. Each question is worth 2 marks (70 marks intotal)Section B contains 3 multi-task questions. Each question is worth 10 marks (30 marks in t otal).Multi task questions are a new question type which is being introduced in 2014. This newquestion type is explained more fully below.All questions are compulsory.The paper has a pass mark of 50%.ACCA F 2Intro ductio n 75 Question typesThe F2 exam consists of the following types of question: Objective test (OT) –These are single, short, automatically marked questions.Multiple task questions (MTQ) – These questions contain a series of tasks which relate t o one or more scenarios.The types of question that may be included are as follows:OT MTQMultiple Choice You are required to choose one answer from a list of options by clicking on the appropriate radio buttonMultiple Response You are required to select more than one response from the options provided by clicking the appropriate tick boxes Multiple Response Matching You are required to select a response to a number of related statements by clicking on the radio button whichcorresponds to the appropriate response for each statement Number Entry You are required to key in a numerical response to the questionGapfill You are required to enter answers into blank areas Hot SpotYou are required to choose one or more answers by clicking on the appropriate hotspot area/ areas on an imageEach of the above types of question are included in the companion Question Bank. Examples of each of the question types and how they are marked can also be found on the ACCA’s website at Specimen examThe ACCA’s specimen exam reflecting the new exam formats and incorporating all question types, is included in this Question Bank.6 Exam tipsRead the requirement very carefully . With calculation questions there are many opportunities for your examiner to confuse you or try and catch you out. It will be very easy to arrive at a result that is one of the options available.Manage your time . You have an average of 2 minutes and 24 seconds per question. S ome will take longer than others, particularly those that involve calculating a numerical answer. So if you get stuck on a question, make a note of the question number and move on. If you have time at the end of the exam you can go back and tackle the tricky questionsYou may be asked to choose one or more correct statements from a given list. Read each statement carefully. If you are unsure about one or more of them, move on and deal with the statements you do agree with. You may find the correct answer by process of elimination without needing to revisit the statements you are unsure about. In any event you should certainly be able to narrow down your choices.If you think you will run out of time, stop five minutes before the end and guess any remaining answers – remember you have a one in four chance of getting those questions right which could make the difference between a pass and a fail.8 Intro ductio n ACCA F 2 7How to study F2Plan your study timeGet your diary out and decide when, where and how often you want to study. If you followed a FirstIntuition course you would receive a minimum of five full days tuition, and be expected to doadditional work at home. Studying on your own is harder and will take longer. You should expect tospend at least 3 hours studying per week. On this basis it should take approximately two months tolearn the study material, then you should allow additional time for revision and final question practice.Most students should be ready to take the exam 3 months after commencing their studies.Set a target date for the examThis is very important with computer-based exams. If you don’t set a target there is a danger that you will spread your study time over too long a period, will lose momentum or simply not get around totaking the exam. When you set your target bear in mind how you wish to progress through thesyllabus, as from paper F4 onwards you are tied to the paper-based exam sittings in June andDecember. For example, if you wish to progress to the Skills level papers for a December sitting youshould complete your computer-based exams by 31 July.Make the most out of your study sessionsTry and complete each study session in one go so that you learn each topic in turn. Some sessions are longer than others, but make sure you take a break between sessions.Read the ACCA study guide at the start of each session so you know the learning outcomes for thatparticular session. Check the tutor tips for advice on how to tackle questions or which areas focus on.Then read the relevant chapter of the course notes.It is essential that you try the questions from the Question Bank where indicated. You will not passthe exam if you don’t attempt the questions. Check your answers and make sure you understand the workings for any that you get wrong. Often you will find that you got the wrong answer because youdidn’t read the question properly – the examiner does like to try and catch you out! If you get stuckgive your tutor a call and ask for advice.RevisionYou should attempt the additional question banks for each of the revision sessions as well as re-reading the study notes. When you are getting at least half of the questions right you are ready toattempt the Mock Exam. If you achieve at least 60% in the Mocks then you should be ready to attempt the real exam.The real examWhen are ready to attempt the real exam give us a call to arrange your CBE (or contact your nearestCBE centre). We hold weekly exam sessions but will do our best to be flexible so you can sit the examat a time that suits you.ACCA F 2Intro ductio n 9 8Study planner10 Intro ductio n ACCA F 2ACCA F 2Intro ductio n 118.1 Practical Experience Requirements (PER) and Performance ObjectivesACCA requires students to have 36 months’ practical experience in order to become members. Part ofthe practical experience requirements is achieving performance objectives that demonstrate that youcan apply what you’ve learnt when studying to real-life, work activities.ACCA has set out 20 performance objectives in 9 areas. You are required to achieve 13 performanceobjectives – all 9 Essentials performance objectives and any 4 Options performance objectives. ACCAhas provided guidance on which objectives are strongly linked to which exam. The relevant objectivesfor F2, which comprise Essentials and Options objectives, are:Manage self (relevant for all exams)(5)Communicate effectively (relevant for all exams)(6)Use information and communications technology (relevant for all exams)(12)Prepare financial information for management (relevant for F2, F5 and P5)(13)Contribute to budget planning and production (relevant for F2, F5 and P5)(14)Monitor and control budgets (relevant for F2, F5 and P5)No part of this publication may be reproduced, stored in a retrieval system or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of First Intuition Publishing Ltd.Any unauthorised reproduction or distribution in any form is strictly prohibited as breach of copyright and may be punishable by law.© First Intuition Publishing1 Accounting for management(a)Describe the purpose and role of cost and management accounting within an organisation.(b)Compare and contrast financial accounting with cost and management a ccounting.The purpose of cost and management accounting is to assist the management in running theirbusiness to achieve its overall plans, make the correct decisions and to control the business.1 管理会计(a)描述组织内部成本会计和管理会计的目的与作用。

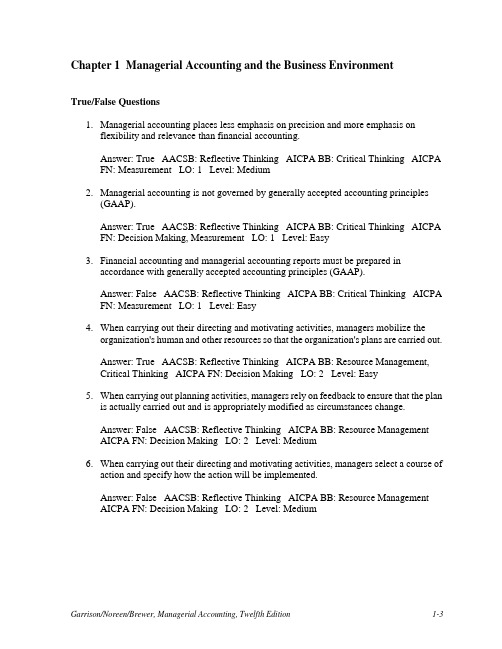

True/False Questions1. Managerial accounting places less emphasis on precision and more emphasis onflexibility and relevance than financial accounting.Answer: True AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Measurement LO: 1 Level: Medium2. Managerial accounting is not governed by generally accepted accounting principles(GAAP).Answer: True AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Decision Making, Measurement LO: 1 Level: Easy3. Financial accounting and managerial accounting reports must be prepared inaccordance with generally accepted accounting principles (GAAP).Answer: False AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Measurement LO: 1 Level: Easy4. When carrying out their directing and motivating activities, managers mobilize theorganization's human and other resources so that the organization's plans are carried out.Answer: True AACSB: Reflective Thinking AICPA BB: Resource Management,Critical Thinking AICPA FN: Decision Making LO: 2 Level: Easy5. When carrying out planning activities, managers rely on feedback to ensure that the planis actually carried out and is appropriately modified as circumstances change.Answer: False AACSB: Reflective Thinking AICPA BB: Resource ManagementAICPA FN: Decision Making LO: 2 Level: Medium6. When carrying out their directing and motivating activities, managers select a course ofaction and specify how the action will be implemented.Answer: False AACSB: Reflective Thinking AICPA BB: Resource ManagementAICPA FN: Decision Making LO: 2 Level: Medium7. Persons occupying staff positions provide support and assistance to other parts of theorganization.Answer: True AACSB: Reflective Thinking AICPA BB: Resource Management AICPA FN: Decision Making LO: 2 Level: Easy8. Staff departments generally have direct authority over line departments in anorganization.Answer: False AACSB: Reflective Thinking AICPA BB: Resource Management AICPA FN: Decision Making LO: 2 Level: Medium9. Informal relationships and channels of communication often develop that do not appearon the organization chart.Answer: True AACSB: Reflective Thinking AICPA BB: Resource Management, Critical Thinking AICPA FN: Decision Making LO: 2 Level: Easy10. The controller's position in a retail company is considered a line position rather than astaff position.Answer: False AACSB: Reflective Thinking AICPA BB: Resource Management AICPA FN: Decision Making LO: 2 Level: Medium11. The Chief Financial Officer of an organization should present facts and refrain fromoffering advice and personal opinion.Answer: False AACSB: Reflective Thinking AICPA BB: Resource Management AICPA FN: Decision Making LO: 2 Level: Medium12. A strategy is a game plan that enables a company to attract customers by distinguishingitself from competitors.Answer: True AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Decision Making LO: 2 Level: Easy13. A strategy requires effective use of Six Sigma improvement techniques.Answer: False AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Decision Making LO: 2 Level: Medium14. A customer value proposition is essentially a reason for customers to choose acompany's products over its competitors' products.Answer: True AACSB: Reflective Thinking AICPA BB: Marketing AICPA FN: Decision Making LO: 2 Level: Easy15. Customer value propositions tend to fall into three broad categories--customer intimacy,operational excellence, and product leadership.Answer: True AACSB: Reflective Thinking AICPA BB: Marketing AICPA FN: Decision Making LO: 2 Level: Easy16. Companies that adopt a customer intimacy strategy are in essence saying to their targetcustomers, “The reason you should choose us is because we understand and respond to your individ ual needs better than our competitors.”Answer: True AACSB: Reflective Thinking AICPA BB: Marketing AICPA FN: Decision Making LO: 2 Level: Easy17. Companies that choose an operational excellence strategy are in essence saying to theircus tomers, “Choose us rather than our competitors because we strive for zero defects.”Answer: False AACSB: Reflective Thinking AICPA BB: Marketing AICPA FN: Decision Making LO: 2 Level: Medium18. A value chain consists of the major business functions that add value to the company'sproducts and services.Answer: True AACSB: Reflective Thinking AICPA BB: Resource Management AICPA FN: Decision Making LO: 2 Level: Easy19. Efforts designed to increase the rate of output should generally be applied to theworkstation that is the constraint.Answer: True AACSB: Reflective Thinking AICPA BB: Resource Management AICPA FN: Decision Making LO: 3 Level: Easy20. The lean thinking model is a five step management approach that organizes resourcessuch as people and machines around the flow of business processes and that pulls units through theses processes in response to customer orders.Answer: True AACSB: Reflective Thinking AICPA BB: Resource Management AICPA FN: Decision Making LO: 3 Level: Easy21. Supply chain management involves acquiring and bringing inside the company all ofthe processes that bring value to customers.Answer: False AACSB: Reflective Thinking AICPA BB: Resource Management AICPA FN: Decision Making LO: 3 Level: Medium22. An enterprise system integrates data across an organization into a single softwaresystem that enables all employees to have simultaneous access to a common set of data.Answer: True AACSB: Reflective Thinking AICPA BB: Leveraging Technology AICPA FN: Leveraging Technology LO: 3 Level: Easy23. Corporate governance is the legal framework that allows managers to control and directlower-level workers on the job.Answer: False AACSB: Reflective Thinking AICPA BB: Resource Management AICPA FN: Decision Making LO: 3 Level: Medium24. The Sarbanes-Oxley Act of 2002 was intended to protect the interests of those whoinvest in publicly traded companies by improving the reliability and accuracy ofcorporate financial reports and disclosures.Answer: True AACSB: Reflective Thinking AICPA BB: Legal AICPA FN:Measurement LO: 3 Level: Easy25. The Standards of Ethical Conduct promulgated by the Institute of ManagementAccountants specifically states, among other things, that management accountants havea responsibility to disclose fully all relevant information that could be reasonably beexpected to influence an intended user's understanding of the reports, comments and recommendations presented.Answer: True AACSB: Ethics AICPA BB: Critical Thinking AICPA FN: Decision Making LO: 4 Level: EasyMultiple Choice Questions26. Managerial accounting places considerable weight on:A) generally accepted accounting principles.B) the financial history of the entity.C) ensuring that all transactions are properly recorded.D) detailed segment reports about departments, products, and customers.Answer: D AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Measurement LO: 1 Level: Easy27. The plans of management are often expressed formally in:A) financial statements.B) performance reports.C) budgets.D) ledgers.Answer: C AACSB: Reflective Thinking AICPA BB: Resource ManagementAICPA FN: Measurement LO: 1 Level: Easy28. The phase of accounting concerned with providing information to managers for use inplanning and controlling operations and in decision making is called:A) throughput time.B) managerial accounting.C) financial accounting.D) controlling.Answer: B AACSB: Reflective Thinking AICPA BB: Resource ManagementAICPA FN: Measurement LO: 1 Level: Easy29. A staff position:A) relates directly to the carrying out of the basic objectives of the organization.B) is supportive in nature, providing service and assistance to other parts of theorganization.C) is superior in authority to a line position.D) none of these.Answer: B AACSB: Reflective Thinking AICPA BB: Resource ManagementAICPA FN: Decision Making LO: 2 Level: Easy30. For a manufacturing company, what type of position (line or staff) is each of thefollowing?Manager of a Data Processing Department Manager of a ProductionDepartmentA) Staff StaffB) Staff LineC) Line StaffD) Line LineAnswer: B AACSB: Reflective Thinking AICPA BB: Resource ManagementAICPA FN: Decision Making LO: 2 Level: Easy31. A _______________ position in an organization is directly related to the achievementof the organization's basic objectives.A) lineB) managementC) staffD) None of the above.Answer: A AACSB: Reflective Thinking AICPA BB: Resource ManagementAICPA FN: Decision Making LO: 2 Level: Easy32. ______________ is an example of a line position.A) Controller for a merchandising companyB) Chief financial officer of a merchandising companyC) Store manager for Best BuyD) Human resources manager for a community collegeAnswer: C AACSB: Reflective Thinking AICPA BB: Resource ManagementAICPA FN: Decision Making LO: 2 Level: Easy33. Which of the following is NOT one of the three major customer value propositionsdiscussed in the text?A) customer intimacyB) discount pricingC) operational excellenceD) product leadershipAnswer: B AACSB: Reflective Thinking AICPA BB: Resource ManagementAICPA FN: Decision Making LO: 2 Level: Easy34. Which of the following is NOT one of the five steps in the lean thinking modeldiscussed in the text?A) Continuously pursue perfection in the business process.B) Identify value in specific products/services.C) Implement an enterprise system.D) Create a pull system that responds to customer orders.Answer: C AACSB: Reflective Thinking AICPA BB: Resource ManagementAICPA FN: Decision Making LO: 2 Level: Easy35. One consequence of a change from a push to a properly implemented pull productionsystem can be:A) an increase in work in process inventories.B) an extremely difficult cultural change due to enforced idleness when demand fallsbelow production capacity.C) an increased mismatch between what is produced and what is demanded bycustomers.D) an increase in raw materials inventories.Answer: B AACSB: Analytic AICPA BB: Industry, Resource Management AICPA FN: Decision Making LO: 3 Level: Hard36. All of the following are characteristics of a pull production system EXCEPT:A) Inventories are reduced to a minimum by purchasing raw materials and producingunits only as needed to meet consumer demand.B) Raw materials are released to production far in advance of being needed to ensureno interruptions in work flows due to shortages of raw materials.C) Products are completed just in time to be shipped to customers.D) Manufactured parts are completed just in time to be assembled into products.Answer: B AACSB: Reflective Thinking AICPA BB: Resource ManagementAICPA FN: Decision Making LO: 3 Level: Medium37. The five step framework used to guide Six Sigma improvement efforts includes all ofthe following EXCEPT:A) Analyze.B) Control.C) Digitize.D) Measure.Answer: C AACSB: Reflective Thinking AICPA BB: Resource ManagementAICPA FN: Decision Making LO: 3 Level: Medium38. The Sarbanes-Oxley Act of 2002 contains all of the following provisions EXCEPT:A) The audit committee of the board of directors of a company must hire, compensate,and terminate the public accounting firm that audits the company's financial reports.B) Financial statements must be audited once every three years by the GovernmentAccounting Office.C) Both the CEO and CFO must certify in writing that their company's financialstatements and accompanying disclosures fairly represent the results of operations.D) A company's annual report must contain an internal control report.Answer: B AACSB: Reflective Thinking AICPA BB: Legal AICPA FN:Measurement LO: 3 Level: Medium39. The Institute of Management Accountants' Standards of Ethical Conduct contains apolicy regarding confidentiality that requires that management accountants:A) refrain from disclosing confidential information acquired in the course of their workexcept when authorized by management.B) refrain from disclosing confidential information acquired in the course of their workin all situations.C) refrain from disclosing confidential information acquired in the course of their workexcept when authorized by management, unless legally obligated to do so.D) refrain from disclosing confidential information acquired in the course of their workin all cases since the law requires them to do so.Answer: C AACSB: Ethics AICPA BB: Critical Thinking AICPA FN: Decision Making LO: 4 Level: Hard40. Which of the following is NOT one of the Institute of Management Accountants' fiveStandards of Ethical Conduct?A) CompetenceB) ConfidentialityC) IndependenceD) IntegrityAnswer: C AACSB: Ethics AICPA BB: Critical Thinking AICPA FN: Decision Making LO: 4 Level: Medium。

F2Management Accounting应知应会单词——By Golden Finance Chapter1Decision-making决策Decline减少Long-term strategic planning长期战略规划Chapter2Attendance record考勤记录Census普查Cluster sampling整群抽样/整群抽样法Continuous data连续性数据Data sources数据源Data types数据类型Discrete data离散性数据Investment centres投资中心Multistage sampling多层抽样法Multistage sampling多步骤抽样Population群体;总体Primary data原始数据;原始资料;一手资料Qualitative定性的Quantitative定量的Quasi-半(用以构成复合词)Quota sampling配额抽样Random numbers随机数Sampling取样;抽样Sampling frame样本框Scatter diagrams散点图;散形图Secondary data二手数据Stratified sampling分层抽样Systematic sampling系统抽样;等距抽样Chapter3Bar chart条形图Component bar chart成分柱状图Compound bar chart复合柱状图Moving averages移动平均Multiple bar chart多重条状图Pie chart饼状图;扇形图Chapter4Administration管理;行政Committed cost承诺成本Committed fixed costs承诺支出的固定费用Composite codes复合编码Composite index numbers复合索引号码Controllable cost可控成本Controllable profit可控利润Cost成本Cost accounting成本会计Cost accounting department成本核算部门Cost accounts成本账户Cost behaviour成本性态Cost behaviour and levels of activity成本性态与活动量Cost behaviour assumptions成本性态前提假设Cost behaviour patterns成本性态模式Cost behaviour principles成本性态原则Cost centre成本中心Cost codes成本代码Cost object成本对象Cost of appraisal成本评估Cost reduction成本减少Cost unit成本单位Curvilinear variable costs曲线变动成本法Direct costs直接成本Direct expenses直接费用Direct labour直接人工Fixed cost固定成本High Low Method高低点法Indirect间接Indirect expenses间接费用Indirect materials间接材料Indirect wages间接工资Memorandum report备忘录Non-controllable cost s不可控成本Price价格(多指单价)Production cost生产成本Responsibility center责任中心Semi-variable cost半变动成本Stepped Fixed costs阶梯成本Trace ability可描性;追溯性Variable cost变量成本Chapter5Bin card库存记录卡Bulk discount大宗购买Continuous stocktaking连续盘存Delivery note送货单Deteriorating inventory质量下降的存货Direct material直接材料Economic batch quantity经济批量Economic order quantity经济订货量FIFO(First in,first out)先入先出Free inventory可用库存GRN;goods received note收货单Idle time闲置时间Incentive schemes激励计划Job cards作业卡Labour turnover劳工周转Maximum level最高存货水平Minimum level最低存货水平oder costs订单成本Periodic stocktaking定期盘存Perpetuity永续性Perpetuity永续盘存Reorder level再订货水平Slow-moving inventories呆滞库存Stock out cost缺货成本Store requisition领料单Transfers and returns of material材料的转移和返回Weighted average pricing加权平均定价法Chapter6Activity ratio生产业务量比率(同production volume ratio)Capacity ratio产能比率Clock card出勤卡Daily time sheets每日工作时间表Day-rate system日付工资系统Direct wages直接人工(蓝领)Group bonus schemes团体奖金计划Individual bonus schemes个人奖金计划Motivation激励overtime premium加班奖金Remuneration methods报酬方法Replacement costs重置成本Chapter7Absorption costing吸收成本法Activity based costing;ABC作业成本法Allocation分配Apportioned costs已分摊成本Cost drivers成本动因Cost pools成本池Departmental absorption rates部门吸收率Distribution overhead运输间接费用Job cost card作业成本卡Job costing作业成本法over-absorption超额分配Overhead经常费用;杂项费用Chapter8Contribution贡献Job costing for internal services内部服务成本计量Chapter9Abnormal gain异常收益Abnormal loss异常损失By-product副产品Equivalent units同等数量Joint product联产品Process costing分布成本法Scrap value废料价值Split off point费用分配点(分离点)weighted average cost method加权平均成本法Chapter10Appraisal costs评估成本Batch costing整批成本法Continuous improvement不断改进Cost of conformance成本Cost of external failure外部失败成本(货物售后)Cost of internal failure内部失败成本(货物出厂前)Cost of non-conformance违规的成本Cost of prevention避免次品成本Cost of quality保证质量成本Cost per service unit每服务单位的成本Cost plus pricing成本+定价法Cumulative weighted average pricing累计加权平均定价法Least squares method最小二乘法Linear equations线性等数Lines of best fit最佳拟合曲线Marginal costing边际成本法Pricing定价法Profit margin利润率Total quality management(TQM)全面质量管理(TQM)Chapter11Additive model加法模型Chain base method链基数方法Coefficient of determination决定系数Consumer Prices Index(CPI)消费价格指数Correlation相关性Correlation and causation相关性和因果关系Correlation coefficient相关系数Correlation in a time series时间序列里的相关性Cyclical variations周期变动Deseasonalisation去季节性影响Index numbers指数Laspeyre indices拉式指数Paasche indices帕氏指数positive correlation正相关Regression lines and time series回归线和时间序列Retail price index零售物价指数Seasonal variations季节差异Weighted aggregate indices加权综合指数Chapter12Aspiration level期望水平Aspirations budget愿望预算Budget committee预算委员会Budget manual预算指南Budget period预算期间Budgetary control预算控制Budgetary slack预算松弛Cell单元格Column列Corporate objectives公司目标Corporate planning公司计划Cost behaviour and budgeting成本性态与预算Departmental budgets部门预算Discretionary fixed costs可自由处置固定成本Dysfunctional decision making破坏性的想法Expectations budget期望预算Goal congruence目标一致Life cycle costing生命周期成本Participative budgeting参与式预算Spreadsheet电子表格Chapter13Cash budget现金Cash budget现金流预算Cost behaviour and decision making成本性态与决策Discounted cash flow现金流贴现Chapter14Avoidable costs可避免的成本Break-even收支平衡Capital expenditure资产性支出Capital income资产性收入Capital transactions资产性收入Cost of capital资金成本Discounted cash flow(DCF)techniques现金贴现方法Discounted payback method贴现还本方法Discounting贴现Net present value净现值Non-relevant costs不相关成本opportunity cost机会成本Rectification Cost改正成本Running cost营运成本Sunk cost沉没成本Chapter15Attainable standard可达到的标准Basic standard基础标准Control控制Control process控制流程Control ratios控制比率Cost behaviour and cost control成本性态与控制Cost control成本控制Cost gap成本差异Differential cost差异成本Direct labour cost variances直接人工成本差异Direct labour efficiency variance直接人工效率差异Direct labour rate variance直接单位人工差异Direct labour total variance直接人工总差异Direct material price variance直接材料定价差异Direct material total variance直接材料费用总差异Direct material usage variance直接材料使用率差异Directly attributable fixed costs直接产生的固定费用Directly attributable overhead直接产生的间接费用Standard cost标准成本Chapter16Accounts payable payment period应付帐款付款期Accounts receivable collection period应收帐款收款期Acid test ratio速动比率(同quick ratio)Asset turnover资产周转率Average age of working capital周转期(同Working capital period)Critical success factor主要成功因素Customer service客户服务Mission使命Working capital period周转期Chapter17Balanced scorecard平衡记分卡Benchmarking标杆管理Cost/sales ratios成本销售比率Current ratio流动比率Current standards现有标准Debt ratios负债比率Interest cover利息覆盖Inventory turnover库存流通率Inventory turnover period库存周转周期Liquidity ratios流动比率Performance measurment业绩测量Profit sharing schemes利润分享计划Quick ratio速动比率Residual income剩余收益Return on capital employed(ROCE)资本回报率Return on investment(ROI)投资回报率Value analysis价值分析Value engineering价值工程。