会计学企业决策的基础

- 格式:ppt

- 大小:254.50 KB

- 文档页数:10

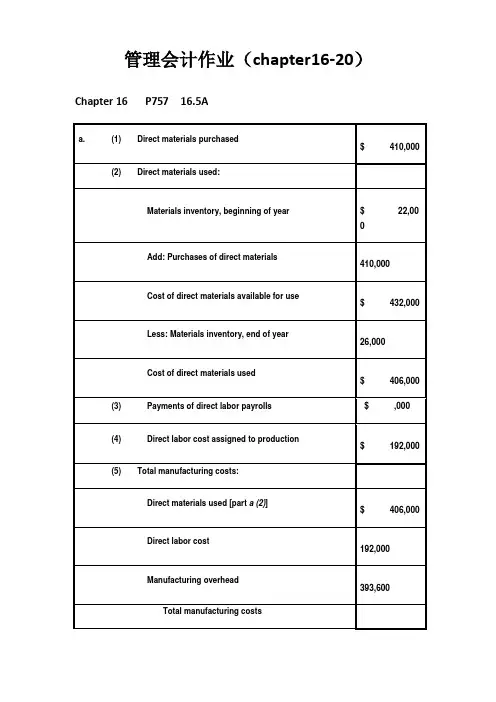

管理会计作业(chapter16-20)

Chapter 16 P757 16.5A

a. (1) Direct materials purchased

$ 410,000

(2) Direct materials used:

Materials inventory, beginning of year

$ 22,000

Add: Purchases of direct materials

410,000

Cost of direct materials available for use

$ 432,000

Less: Materials inventory, end of year

26,000

Cost of direct materials used

$ 406,000

(3) Payments of direct labor payrolls $ ,000

(4) Direct labor cost assigned to production

$ 192,000

(5) Total manufacturing costs:

Direct materials used [part a (2)]

$ 406,000

Direct labor cost

192,000

Manufacturing overhead

393,600

Total manufacturing costs

$ 991,600

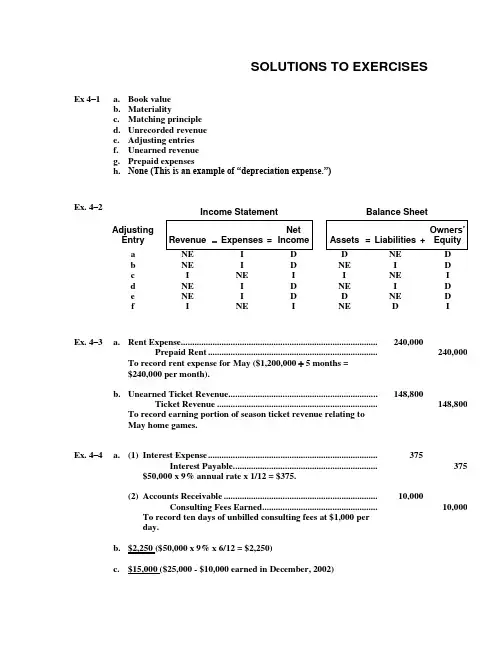

SOLUTIONS TO EXERCISES

Ex 4–1 a. Book value

b. Materiality

c. Matching principle

d. Unrecorded revenue

e. Adjusting entries

f. Unearned revenue

g. Prepaid expenses

h. None (This is an example of ―depreciation expense.‖)

Ex. 4–2 Income Statement Balance Sheet

Adjusting

Entry

Revenue

Expenses

= Net

Income

Assets

=

Liabilities

+ Owners’

Equity

a NE I D D NE D

b NE I D NE I D

c I NE I I NE I

d NE I D NE I D

e NE I D D NE D

f I NE I NE D I

Ex. 4–3 a. Rent Expense....................................................................................... 240,000

Prepaid Rent ........................................................................... 240,000

To record rent expense for May ($1,200,000 5 months =

$240,000 per month).

b. Unearned Ticket Revenue .................................................................. 148,800

会计学的基本原理与方法

会计学作为一门重要的管理学科,研究的是财务信息的收集、记录、分析和报告。它的基本原理和方法为企业和组织提供了财务决策和管理的基础。本文将介绍会计学的基本原理和方法,以及其在实际应用中的重要性和影响。

一、会计学的基本原理

会计学的基本原理是指在进行财务信息处理和报告时,所遵循的核心原则。以下是几个重要的会计学基本原理:

1. 记账原则:会计学要求按照事实发生和经济实质来进行财务信息的记录。即记录应该基于实际交易和实际发生的事实,而不仅仅是根据法律形式。

2. 成本原则:会计学要求以成本为基础,对企业的资产和负债进行计量。成本原则强调资产和负债应该按照其购买或获取成本进行记录,而不是按照市场价值或未来可能的价值。

3. 核算周期原则:会计学要求进行会计核算时,将财务信息按一定的时间间隔进行分期,形成财务报表。常见的核算周期有日报、月报、年报等。

4. 一贯性原则:会计学要求在进行财务信息记录和报告时,保持一贯性和连续性。这意味着在变更会计政策或会计估计时,需要进行适当的说明和调整,确保财务信息的可比性和连贯性。 二、会计学的基本方法

会计学的基本方法是指在实践中用于收集、记录、分析和报告财务信息的步骤和程序。以下是几种常用的会计学基本方法:

1. 会计核算:会计核算是会计学的核心方法,它包括了对企业的各种经济业务进行记录和分类,形成财务账簿和财务报表。会计核算主要包括日常记账、总账、明细账、科目汇总等过程。

2. 财务分析:财务分析是会计学的重要环节,通过对财务报表的分析,了解企业的财务状况、经营绩效和发展潜力。常用的财务分析方法包括比率分析、趋势分析、垂直分析等。

3. 预算编制:预算编制是会计学应用的重要方法之一,它通过对企业未来一段时间的收入和支出进行合理预测和安排,帮助企业制定经济目标、支出计划和经营策略。

4. 决策支持:会计学提供了财务信息的基础,可以用于各种经营决策的支持。企业可以利用会计学方法,对不同的经营方案进行财务分析和评估,为决策者提供依据和参考。

Ending Inventory=130,000-38,500=91,500(inventory at the time of thb.Periodic inventory system.Because he doesn't know the loss of thefprofit method to estimate the cost of inventory that have been stolen.But in a perpetual iof merchandise are recorded immediately as they occur.So he doesn't record the inventory usystem,but using the periodic inventory system.

E.8.10a.Cost Ratio=Goods available for sale at cost/ Goods available for s COGS=Net sales*Cost rate=600,000*58%=348,000 ●Inventory valued at old cost(usually the higher cost) ●Most conservative method during period of rising prices;often result in lower inco

E.8.9a.Cost of goods available for sale=50.000+80,000=130,000 Cost Ratio=1-GPM=1-45%=55% COGS=70,000*55%=38,500 InventoryTo transfer the cost of 90 products from inventory to cost of goods e.FIFO:●Cost of goods sold is based on older costs(usually the lower costs) ●Inventory valued at most recent cost(usually the higher cost) ●May overstate income during period of rising prices; may increase income taxes due LIFO:●Cost of goods sold is based on recent costs(usually the higher costs) Total cost of goods for sale InventoryTo transfer the cost of 90 products from inventory to cost of goods d.May.10 60 generators from April.9 @ 1,500 30 generators from May.1 @ 1,600 Total cost of goods for saleTo transfer the cost of 90 products from inventory to cost of goods identification methodb.May.10 Cost of goods for sale InventoryTo transfer the cost of 90 products from inventory to cost of goods c.May.10 70 generators from April.9 @ 1,500 20 generators from May.1 @ 1,600chap