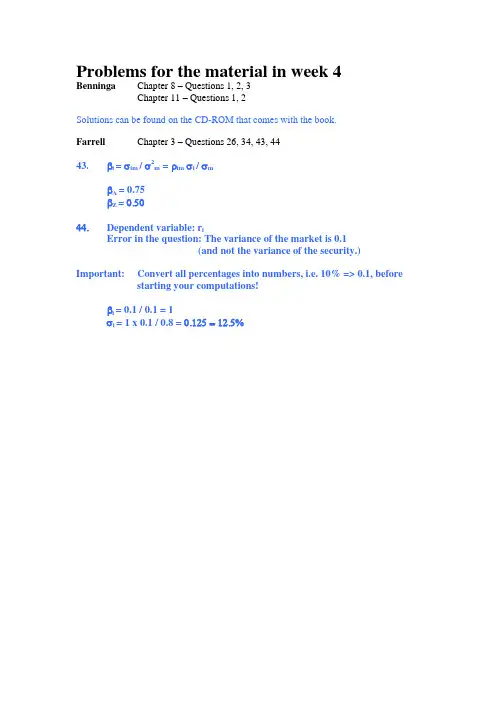

FINS5517_APPLIED PORTFOLIO MANAGEMENT & MODELLING_2005 Semester 2_Week 4solutions

- 格式:pdf

- 大小:24.11 KB

- 文档页数:1

文献信息:文献标题:A Study of Personal Financial Planning Process and Socio-Economic Decision-Making in Households(个人理财规划过程与家庭社会经济决策研究)国外作者:S Shah,AS Bhatt文献出处:《Social Science Electronic Publishing》,2016字数统计:英文2308单词,13376字符;中文4089汉字外文文献:A Study of Personal Financial Planning Process andSocio-Economic Decision-Making in Households Abstract In the current era, planning of finance is assuming extreme importance as myriad financial products are available and individuals’ demands are increasing. Personal financial planning is a process which outlines one’s financial objectives and takes financial decisions in a manner that his goals are achieved. The process of financial planning and decision-making in household has been studied independently by various researchers. However, these are essentially intertwined in nature. In view of this, the researchers have undertaken the task of understanding whether individuals followed the Personal Financial Planning process consciously and whether this was linked to household decision-making, especially in the social and economic areas. This paper also examines gender inequality in household decision-making and how household decision-making evolves with time. The study was conducted in the Ahmedabad district of Gujarat, and a sample size of 196 respondents was selected on judgmental basis to meet the objective of the study. The response rate was 78% (n=150) which is considered to be acceptable for a research study. The sample size was equally split between males and females. The survey was carried out in June- July, 2014.Analysis has been done by using Analysis of Variance(ANOV A), Binary Logistic Regression and Chi-square.It was found that age influences components of Personal financial planning (PFP) like determining one’s financial objectives, knowledge of finance, satisfaction regarding current economic status, and retirement planning. Likewise, gender, income, education, profession and marital status affect various components of PFP. It was also found that household economic and social decisions were related to income and investment of the respondent. Further, it could be inferred that in a household, males held more bargaining power in taking economic decisions, while females exerted more influence in taking social decisions.Key-words: Personal financial planning, financial objective, household economic decisions, household social decisions1.IntroductionHousehold financial management is that activity which is concerned with planning and controlling finances of individuals and households. The concept ‘personal financial management’ is of immense interest to researchers, academicians and policy formulators in the context of global economic crisis and financial inclusion in developing countries. As in the case of a nation or business institution, finance plays a crucial role in the life of an individual, to rich or poor. Mobilisation of finance and its wise and efficient deployment play a strategic role in the well-being of a nation or institution and at the most in the case of a person who is the base or starting point of any economic activity. Personal finance as a branch of economics deals with budgeting, saving, investing, borrowing, lending, insuring, and diversifying.Personal financial planning denotes the process of determining whether and how an individual can meet life goals through the proper management of financial sources.(CFP Board, 2005) Financial literacy and financial well-being are mutually related with each other (UNDP and PFIP, 2010). Financial well-being is the ability to have wealth to serve life - to have the financial means to comfortably attain whatever personal goals one has to enjoy an acceptable lifestyle. Sociological research data indicate that fourfactors strongly predict happiness and overall well-being in most cultures: health, economic status, employment, and family relationships. People are happier when they are healthy, employed, married or in a committed relationship, and financially secure. There is a relationship between an individual’s ability to do something (competence) and well-being (both self-perceived happiness and economic well-being). Well- being is, at least in part, a product of competent behaviour enacted consistently over time. Financial capability and financial competence therefore influence a person’s well-being. The opportunity accorded to people to engage with the formal financial system and how well they manage the money they have will influence their standard of living and the standard of living of those for whom they are responsible.Like never before, researchers, public authorities, community groups, industry associations and international organisations, are initiating financial literacy programmes and want to understand how people can become financially literate, or in other words, have the knowledge, understanding, skills and competence to deal with everyday financial matters and make the right choices for their needs.2.Literature Review2.1.Financial Literacy & PlanningVery few articles and research papers were found those have founded identical theories of personal financial planning. The term personal finance is having its root in micro-economics, finance and behavioral science as this area originated from home economics to various finance theories to behavioral finance. An Individual, as a consumer, is a rational being who tries to use his or her money income to derive the utmost amount of consummation or utility from it. Consumers want to get "the most for their money" or, to exceed their total utility as per ‘Maximisation of utility’ theory. Money is scarce in nature and due to this, consumers tend to be rational in their purchasing decisions. A consumer would spend his money on the best possible purpose or product and only when needed that guarantees optimum utility or a complete sense of satisfaction.Considering the importance of financial literacy, in RBI-OECD Workshop onFinancial Literacy, Bengaluru, in March, 2010 Sri Pranabkumar Mukerjee, Hon’ble Minister for Finance in his speech narrated “Financial literacy and education plays a crucial role in financial inclusion.” He further added that research and existing literature in financial literacy have typically associated an individual’s knowledge of economics and finance with his financial decisions related to savings, spending, borrowing, retirement planning, or portfolio choice. Today, financial competence has become essential due to complex choices and, while the policies need to enable access, the responsibility for saving and investing for the future primarily lies with the individuals. Another study by Miller M., Godfrey N., Levesque B. and Stark E. (2009) discussed the importance of financial literacy for consumers in developing countries, especially in the context of the global financial crisis.The authors stated that financial literacy was an active process, in which communicating information was only the beginning: empowering consumers to take action to improve their financial well-beingwas the ultimate goal. This study presented empirical evidence on thevalue of financial literacy programs and made a case for further research in determining the most effective financial literacy tools, programs and public policies, especially in the context of developing countries. Lusardi A. (2001), a world famous financial literacy scholar and academician, in her article ‘Financial literacy around the world: an overview’ stated that in an increasingly risky and globalised market-place, people must be able to make well-informed financial decisions.2.2.Socio-Economic decisions in householdHousehold decision-making affects many choices with important consequences including the distribution of income, allocation of resources, allocation of time, purchase of goods, and fertility decisions. If there is gender inequality in household decision making then this affects the economic well-being of women and children in the household. Blood and Wolfe (1960) in their study based on households in the Detroit area of the United States, found that comparative resources of the wife and husband were more important determinants in decision-making and power than social norms. The spouse with the greater resource base was more likely to have more decision making power. Similar studies done in lower and middle-income countriesreported different results. Research in Yugoslavia and Greece found that husband’s socio-economic resources were negatively related to his power (Buric and Zecevic 1967, Safilios- Rothschild 1967). A study conducted in India by Rammu (1988) which included urban, dual and single income earning households found that the more resources the partner brought into the marriage, in terms of education, income and occupational status, the more decision-making power he/she possessed. He also found that women who were gainfully employed exercised greater authority in all spheres of decision-making compared to women engaged in domestic housework only. However, even employed women did not succeed in negotiating a noticeable change in the allocation of domestic housework, perhaps a consequence of the timeless social norm of women doing housework. In one more study conducted in Venezuela (Lawrence and Mancini 1998) focused on decision-making concerning four subjects: purchase of household goods, change in residence, household finances and children’s education. The study found that while a majority of households made decisions jointly, more women made decisions concerning the purchase of household goods and children’s education compared to men, while men dominated decisions concerning household finances and change in residence.The process of financial planning and decision-making in household has been studied independently in the previous researches. However, these are essentially intertwined and if one wants to achieve life goals, financial literacy is a necessity. In view of this, the researches undertook the task of understanding whether individuals followed the Personal Financial Planning (PFP) process consciously and whether this was linked to household decision-making, especially in the social and economic areas. Further, there is a dearth of research related to this topic especially in Gujarat state of India. Hence, the researchers carried out the study in Gujarat.3.Research MethodologyOn the basis of review of literature and evidences from psychological studies, the present study has been planned with the following objectives:1)To analyse the effect of demographic variables on household financial planning2)To find out the relationship between financial planning decisions and economic and social decisions3)To find out the gender impact on economic and social decisionsThe study was conducted in the Ahmedabad district of Gujarat, and a sample size of 196 respondents was selected on judgmental basis to meet the objectives of the study. The total number of questionnaires distributed was 196. We received 176 questionnaires, but some of them had one or more missing responses. Such questionnaires were discarded and were not considered for further analysis. The final sample size after discarding the questionnaires with missing responses was 150. Thus the response rate was 78% which is considered to be acceptable for a research study. The respondents carried equal number of males and females. The survey was carried out in June-July, 2014. The profile of the respondents with respect to demographics like age, gender, qualification, income, marital status and household investments has been presented in the data analysis section.The research design for the study is descriptive in nature. The questionnaire constructed for the study included several questions which were continuous and categorical in nature. The survey consisted of questions that covered demographics, financial attitude towards personal financial planning, preferences for investment avenues, and purposes for investment.Definition of ConstructsThe components of personal financial planning were obtained through literature review regarding how individuals consider each component in their household financial planning decisions.•Financial Objective: Financial objectives are life goals converted into monetary terms. They can be categorised based on time period- Short term, Medium term and Long term financial objectives.•Knowledge: Knowledge of financial products, terms, financial services and financial markets required for personal financial management.•Satisfaction: Satisfaction in context to personal financial components viz. obtaining, saving, borrowing, investment planning.•Tax efficiency: Proper management of financial resources to avail various rebates and concessions thereby reducing tax liability.•Insurance Coverage: Adequate insurance coverage of life, health and property against risks associated.•Retirement Income: Availability of sufficient corpus to maintain the same standard of living in non-earning years.Data Analysis ApproachAnalysis is done using SPSS software 19.0 and Microsoft excel.Description of Analytical Tools•To find out the impact of the demographical variables on household financial planning, One-Way Analysis of Variance (ANOV A) has been applied for each component identified through literature review and each demographic variable viz. gender, age, income, education, profession and marital status.•To find out the association between financial and socio-economic decisions, Chi square has been applied.•To further analyse the gender impact on economic and social decisions Bivariate Logistic regression is applied where gender is taken as predictor variable and decision taker as outcome variable.4.Managerial ImplicationsThere is significant association between gender and financial objective, knowledge of finance and retirement planning, wherein males agree more to having knowledge and adequate retirement planning.•The older age group (40 – 60 years) disagree more as compared to other age groups when it comes to satisfaction, financial objective, knowledge and retirement planning processes of financial planning.•The higher income group (above 8 lacs) disagree more when it comes to deriving satisfaction from the current PFP, however, the low income group agreed more to tax efficiency as they fall in the tax exempted category.•The non-employed group had less knowledge of the formal financial planning process as compared to the salaried and business groups, and the business class significantly differed from other two groups for retirement planning component.•The marital status is related to several components of PFP, viz. financial objective, knowledge, tax efficiency, and insurance coverage and the categories differ among themselves marginally for these components. However, the divorced category was found to be lacking on the financial objectives and satisfaction part.Looking at the above findings, it became increasingly clear that the typical target group for conducting financial literacy programs would consist of young and middle-aged, females who are home-makers. But the next question was whether they are influential in household decision- making. If they are not typical decision-makers, the training shall not impact the actual decisions taken in the household. Hence, a few significant economic and social decisions of the household were identified and the role of females was studied. The analysis indicated that males play a dominant role in taking economic decisions while females play a leading role in taking social decisions of the household. Hence, the financial literacy programs while targeting the above-mentioned group should especially capture the process of PFP, with a focus on social decisions taken in the household.中文译文:个人理财规划过程与家庭社会经济决策研究摘要在当前时代,随着金融产品的大量激增,以及个人需求的不断上升,理财规划开始变得非常重要。

Application of the AHP in project managementKamal M.Al-Subhi Al-Harbi *DepartmentofConstructionEngineeringandManagement,KingFahdUniversityofPetroleum&Minerals,KFUPMBox1468,Dhahran31261,SaudiArabiaReceived 12June 1998;received in revised form 2March 1999;accepted 19May 1999AbstractThis paper presents the Analytical Hierarchy Process (AHP)as a potential decision making method for use in project manage-ment.The contractor prequali®cation problem is used as an example.A hierarchical structure is constructed for the prequali®cation criteria and the contractors wishing to prequalify for a project.By applying the AHP,the prequali®cation criteria can be prioritized and a descending-order list of contractors can be made in order to select the best contractors to perform the project.A sensitivity analysis can be performed to check the sensitivity of the ®nal decisions to minor changes in judgements.The paper presents group decision-making using the AHP.The AHP implementation steps will be simpli®ed by using the `Expert Choice'professional soft-ware that is available commercially and designed for implementing AHP.It is hoped that this will encourage the application of the AHP by project management professionals.#2000Elsevier Science Ltd and IPMA.All rights reserved.Keywords:Analytical hierarchy process;AHP;Project management;Contractor prequali®cation1.IntroductionThe Analytical Hierarchy Process (AHP)is a deci-sion-aiding method developed by Saaty [24±27].It aims at quantifying relative priorities for a given set of alter-natives on a ratio scale,based on the judgment of the decision-maker,and stresses the importance of the intuitive judgments of a decision-maker as well as the consistency of the comparison of alternatives in the decision-making process [24].Since a decision-maker bases judgments on knowledge and experience,then makes decisions accordingly,the AHP approach agrees well with the behavior of a decision-maker.The strength of this approach is that it organizes tangible and intan-gible factors in a systematic way,and provides a struc-tured yet relatively simple solution to the decision-making problems [29].In addition,by breaking a pro-blem down in a logical fashion from the large,descend-ing in gradual steps,to the smaller and smaller,one is able to connect,through simple paired comparison judgments,the small to the large.The objective of this paper is to introduce the appli-cation of the AHP in project management.The paper will brie¯y review the concepts and applications of the multiple criteria decision analysis,the AHP's imple-mentation steps,and demonstrate AHP application on the contractor prequali®cation problem.It is hoped that this will encourage its application in the whole area of project management.2.Multiple criteria decision analysis (MCDA)Project managers are faced with decision environ-ments and problems in projects that are complex.The elements of the problems are numerous,and the inter-relationships among the elements are extremely compli-cated.Relationships between elements of a problem may be highly nonlinear;changes in the elements may not be related by simple proportionality.Furthermore,human value and judgement systems are integral ele-ments of project problems [15].Therefore,the ability to make sound decisions is very important to the success of a project.In fact,Schuyler [28]makes it a skill that is certainly near the top of the list of project management skills,and notices that few of us have had formal train-ing in decision making.0263-7863/00/$20.00#2000Elsevier Science Ltd and IPMA.All rights reserved.P I I :S 0263-7863(99)00038-1International Journal of Project Management 19(2001)19±27/locate/ijproman*Tel.:+966-3-860-3312;fax:+966-3-860-3287.E-mail address:harbi@.sa (K.M.Al-S.Al-Harbi).Multiple criteria decision-making(MCDM)approa-ches are major parts of decision theory and analysis. They seek to take explicit account of more than one criterion in supporting the decision process[5].The aim of MCDM methods is to help decision-makers learn about the problems they face,to learn about their own and other parties'personal value systems,to learn about organizational values and objectives,and through exploring these in the context of the problem to guide them in identifying a preferred course of action [5,12,20,32,34,35].In other words,MCDA is useful in circumstances which necessitate the consideration of di erent courses of action,which can not be evaluated by the measurement of a simple,single dimension[5]. Hwang and Yoon[14]published a comprehensive survey of multiple attribute decision making methods and applications.Two types of the problems that are common in the project management that best®t MCDA models are evaluation problems and design problems. The evaluation problem is concerned with the evaluation of,and possible choice between,discretely de®ned alternatives.The design problem is concerned with the identi®cation of a preferred alternative from a poten-tially in®nite set of alternatives implicitly de®ned by a set of constraints[5].3.The analytical hierarchy process(AHP)Belton[4]compared AHP and a simple multi-attri-bute value(MAV),as two of the multiple criteria approaches.She noticed that both approaches have been widely used in practice which can be considered as a measure of success.She also commented that the greatest weakness of the MAV approach is its failure to incorporate systematic checks on the consistency of judgments.She noticed that for large evaluations,the number of judgments required by the AHP can be somewhat of a burden.A number of criticisms have been launched at AHP over the years.Watson and Freeling[33]said that in order to elicit the weights of the criteria by means of a ratio scale,the method asks decision-makers mean-ingless questions,for example:`Which of these two cri-teria is more important for the goal?By how much?' Belton and Gear[6]and Dyer[9]pointed out that this method can su er from rank reversal(an alternative chosen as the best over a set of X,is not chosen when some alternative,perhaps an unimportant one,is exclu-ded from X).Belton and Gear[7]and Dyer and Wendel [10]attacked the AHP on the grounds that it lacks a ®rm theoretical basis.Harker and Vargas[13]and Perez [19]discussed these major criticisms and proved with a theoretical work and examples that they are not valid. They commented that the AHP is based upon a®rm theoretical foundation and,as examples in the literature and the day-to-day operations of various governmental agencies,corporations and consulting®rms illustrate, the AHP is a viable,usable decision-making tool. Saaty[24±27]developed the following steps for applying the AHP:1.De®ne the problem and determine its goal.2.Structure the hierarchy from the top(the objec-tives from a decision-maker's viewpoint)through the intermediate levels(criteria on which sub-sequent levels depend)to the lowest level which usually contains the list of alternatives.3.Construct a set of pair-wise comparison matrices(size nÂn)for each of the lower levels with one matrix for each element in the level immediately above by using the relative scale measurement shown in Table1.The pair-wise comparisons are done in terms of which element dominates the other.4.There are n nÀ1a judgments required to developthe set of matrices in step3.Reciprocals are auto-matically assigned in each pair-wise comparison.5.Hierarchical synthesis is now used to weight theeigenvectors by the weights of the criteria and the sum is taken over all weighted eigenvector entries corresponding to those in the next lower level of the hierarchy.6.Having made all the pair-wise comparisons,theconsistency is determined by using the eigenvalue, l m x,to calculate the consistency index,CI as fol-lows:gs l m xÀna nÀ1,where n is the matrix size.Judgment consistency can be checked by taking the consistency ratio(CR)of CI with the appropriate value in Table2.The CR is accep-table,if it does not exceed0.10.If it is more,the judgment matrix is inconsistent.To obtain a con-sistent matrix,judgments should be reviewed and improved.7.Steps3±6are performed for all levels in the hier-archy.Table1Pair-wise comparison scale for AHP preferences[24±27] Numerical rating Verbal judgments of preferences 9Extremely preferred8Very strongly to extremely7Very strongly preferred6Strongly to very strongly5Strongly preferred4Moderately to strongly3Moderately preferred2Equally to moderately1Equally preferred20K.M.A.-S.Al-Harbi/International Journal of Project Management19(2001)19±27Fortunately,there is no need to implement the steps manually.Professional commercial software,Expert Choice,developed by Expert Choice,Inc.[11],is avail-able on the market which simpli®es the implementa-tion of the AHP's steps and automates many of its computations.4.Group decision makingThe AHP allows group decision making,where group members can use their experience,values and knowl-edge to break down a problem into a hierarchy and solve it by the AHP steps.Brainstorming and sharing ideas and insights(inherent in the use of Expert Choice in a group setting)often leads to a more complete representation and understanding of the issues.The following suggestions and recommendations are sug-gested in the Expert Choice software manual[11].1.Group decisions involving participants with com-mon interests are typical of many organizational decisions.Even if we assume a group with com-mon interests,individual group members will each have their own motivations and,hence,will be in con¯ict on certain issues.Nevertheless,since the group members are`supposed'to be striving for the same goal and have more in common than in con¯ict,it is usually best to work as a group and attempt to achieve consensus.This mode max-imizes communication as well as each group member's stake in the decision.2.An interesting aspect of using Expert Choice isthat it minimizes the di cult problem of`group-think'or dominance by a strong member of the group.This occurs because attention is focused ona speci®c aspect of the problem as judgments arebeing made,eliminating drift from topic to topic as so often happens in group discussions.As a result,a person who may be shy and hesitant to speak up when a group's discussion drifts from topic to topic will feel more comfortable in speak-ing up when the discussion is organized and attention turns to his area of expertise.Since Expert Choice reduces the in¯uences of group-think and dominance,other decision processes such as the well known Delphi technique may no longer be attractive.The Delphi technique wasdesigned to alleviate groupthink and dominance problems.However,it also inhibits communica-tion between members of the group.If desired, Expert Choice could be used within the Delphi context.3.When Expert Choice is used in a group session,thegroup can be shown a hierarchy that has been prepared in advance.They can modify it to suit their understanding of the problem.The group de®nes the issues to be examined and alters the prepared hierarchy or constructs a new hierarchy to cover all the important issues.A group with widely varying perspectives can feel comfortable with a complex issue,when the issue is broken down into di erent levels.Each member can pre-sent his own concerns and de®nitions.Then,the group can cooperate in identifying the overall structure of the issue.In this way,agreement can be reached on the higher-order and lower-order objectives of the problem by including all the con-cerns that members have expressed.The group would then provide the judgments.If the group has achieved consensus on some judg-ment,input only that judgment.If during the pro-cess it is impossible to arrive at a consensus on a judgment,the group may use some voting techni-que,or may choose to take the`average'of the judgments.The group may decide to give all group members equal weight,or the group members could give them di erent weights that re¯ect their position in the project.All calculations are done automatically on the computer screen.4.The Group Meeting:While Expert Choice is anideal tool for generating group decisions through a cohesive,rigorous process,the software does not replace the components necessary for good group facilitation.There are a number of di erent approaches to group decision-making,some better than others.Above all,it is important to have a meeting in which everyone is engaged,and there is buy-in and consensus with the result.5.Application of the AHP in project managementIn this paper,contractor prequali®cation(an evalua-tion problem)will be used as an example of the possi-bility of using AHP in project management. Prequali®cation is de®ned by Moore[17]and Stephen [30]as the screening of construction contractors by project owners or their representatives according to a predetermined set of criteria deemed necessary for suc-cessful project performance,in order to determine the contractors'competence or ability to participate in the project bid.Another formal de®nition by Clough[8]is that prequali®cation means that the contracting®rmTable2Average random consistency(RI)[24±27]Size of matrix12345678910Random consistency000.580.9 1.121.241.321.411.451.49K.M.A.-S.Al-Harbi/International Journal of Project Management19(2001)19±2721wishing to bid on a project needs to be quali®ed before it can be issued bidding documents or before it can submit a proposal.Prequali®cation of contractors aims at the elimination of incompetent contractors from the bidding process. Prequali®cation can aid the public and private owner in achieving successful and e cient use of their funds by ensuring that it is a quali®ed contractor who will con-struct the project.Furthermore,because of the skill, capability and e ciency of a contractor,completion of a project within the estimated cost and time is more probable.A number of studies have focused on contractor pre-quali®cation.Lower[16]reviewed the guidelines of the prequali®cation process in di erent States in the US.He also discussed how prequali®cation can provide the owner with appropriate facilities representing an e ec-tive and e cient expenditure of money.Nguyen[18]argued that the prequali®cation process remains largely an art where subjective judgment,based on individual experience,becomes an essential part of the process.Russel and Skibniewski[22]mentioned that the actual process of contractor prequali®cation had received little attention in the past.Russel and Skibniewski[23]tried to describe the contractor prequali®cation process along with the decision-making strategies and the factors that in¯uence the process.They reported®ve methods that they found in use for contractor prequali®cation: dimensional weighting,two-step prequali®cation, dimension-wide strategy,prequali®cation formula,and subjective judgment.In the dimensional weighting method[22],the choice selection criteria and their weights are dependent on the owner.All contractors are ranked on the basis of the criteria.A contractor's total score is calculated by sum-ming their ranks multiplied by the weight of the respec-tive criteria.Then,contractors are ranked on the basis of their total scores,and this rank order of the con-tractors is used for prequali®cation.The problem with this method is deciding the weight of the respective cri-teria,something for which the AHP does provide a methodology.The two-step prequali®cation method[22]is a mod-i®cation of the dimensional weighting method.In the ®rst step,screening of contractors is done on pre-liminary factors.They must get through this step to be eligible for the second phase of prequali®cation.In the second step,the dimensional weighting technique is used for more specialized factors.This method is useful for quick removal of ineligible candidates.This is con-sistent with the`elimination by aspect'method sug-gested by Tversky[31].In dimension-wide strategy method[22],a list of the most important prequali®cation criteria is developed in descending order depending on how important the cri-teria is.Contractors are then evaluated on these factors. If a candidate fails to meet any of the criteria,the can-didate is removed from the prequali®cation process.The method continues until contractors are measured on all criteria[18].The prequali®cation formula method[22]prequali®es contractors on the basis of a formula that calculates the maximum capability of a contractor.The maximum capability is de®ned as the maximum amount of uncompleted work in progress that the contractor can have at any one time.In this method,the contractor's prequali®cation is dependent on the contractors max-imum capability,current uncompleted work and the size of the project under consideration.If the di erence between the contractor's capability and current uncom-pleted work is less than the project works,then the contractor is removed from the bidding process.The previous methods were devised with a common goal to introduce an e cient and systematic procedure for contractor prequali®cation.In some instances,own-ers may base their contractor selection decision on sub-jective judgment and not on a structured approach.The judgment may be in¯uenced by owner biases,such as previous experience with the contractor or how well the contractor's®eld sta operates.Aitah[1]studied the bid awarding system used in Saudi Arabia.He evaluated public building construc-tion projects,and concluded that the projects awarded to the lowest bidder have lower performance quality and schedule delays as compared to the projects which were awarded based on speci®c prequali®cation criteria.Al-Alawi[2]conducted a study on contractor pre-quali®cation for public projects in Bahrain.He surveyed the market and determined the most important criteria in the prequali®cation process,and developed a com-puterized tool for implementing it.Russel[21]analyzed contractor failure in the US and recommended that an owner should have two means of avoiding or minimize the impact of contractor failure: (1)analyzing the contractor quali®cation prior to con-tract award;and(2)monitoring the contractor's per-formance after contract award.Al-Ghobali[3]surveyed the Saudi construction mar-ket and listed a number of factors against which con-tractors should be considered for prequali®cation.This included experience,®nancial stability,past perfor-mance,current workload,management sta ,manpower resources availability,contractor organization,famil-iarity with the project's geographic location,project management capabilities,quality assurance and control, previous failure to complete a contract,equipment resources,purchase expertise and material handling, safety consciousness,claim attitude,planning/schedul-ing and cost control,and equipment repairing and maintenance yard facilities.22K.M.A.-S.Al-Harbi/International Journal of Project Management19(2001)19±276.ExampleA simpli®ed project example of contractor pre-quali®cation will be demonstrated here for illustration purposes.To simplify calculations,the factors that will be used in the project example for prequali®cation are experience,®nancial stability,quality performance, manpower resources,equipment resources,and current workload.Other criteria can be added if necessary, together with a suggestion that a computer be used to simplify calculations.Table3presents a project example for which con-tractors A,B,C,D and E wish to prequalify.An argu-ment could be presented that contractor E is not meeting the minimum criteria.Descriptions presented in Table3under`Contractor E',such as`bad organiza-tion'and`unethical techniques',quali®es him for immediate elimination from the list by the project owner.This is quite consistent with the method`elim-ination by aspect'suggested by Tversky[31].Never-theless,it is the choice of the decision-maker to eliminate contractor E immediately since he/she does not meet the minimum criteria.Contractor E could be left on the list(the choice in this paper for demon-stration purposes)so that he appears at the end of the list of`best contractors in descending order',as will be shown at the end of the example.The matter is safeguarded by checking the consistency of the pair-wise comparison which is a part of the AHP proce-dure.By following the AHP procedure described in the Section5,the hierarchy of the problem can be devel-oped as shown in Fig.1.For step3,the decision-makers have to indicate preferences or priority for each decision alternative in terms of how it contributes to each criter-ion as shown in Table4.Table3ExampleContractor A Contractor B Contractor C Contractor D Contractor EExperience5years experience7years experience8years experience10yearsexperience 15years experienceTwo similar projects One similar project No similar project Two similarprojects No similar projectSpecial procurement experience 1international projectFinancial stability $7M assets$10M assets$14M assets$11M assets$6M assets High growth rate$5.5M liabilities$6M liabilities$4M liabilities$1.5M liabilities No liability Part of a group ofcompaniesGood relationwith banksQuality performance Good organization Average organization Good organization Good organization Bad organizationC.M.personnel C.M.personnel C.M.team Good reputation Unethical techniques Good reputation Two delayed projects Government award Many certi®cates One project terminated Many certi®cates Safety program Good reputation Cost raised insome projectsAverage quality Safety program QA/QC programManpower resources 150labourers100labourers120labourers90labourers40labourers10special skilledlabourers200by subcontract Good skilled labors130bysubcontract260by subcontractAvailability in peaks25special skilledlabourersEquipment resources 4mixer machines6mixer machines1batching plant4mixer machines2mixer machines1excavator1excavator2concrete transferringtrucks1excavator10others15others1bulldozer2mixer machines9others2000sf steel formwork 20others1excavator6000sf wooden formwork15,000sf steel formwork1bulldozer16others17,000sf steel formworkCurrent works load 1big project ending2projects ending(1big+1medium)1medium project started2big projectsending2small projects started2projects in mid(1medium+1small)2projects ending(1big+1medium)1medium projectin mid3projects ending(2small+1medium) K.M.A.-S.Al-Harbi/International Journal of Project Management19(2001)19±2723Then,the following can be done manually or auto-matically by the AHP software,Expert Choice:1.synthesizing the pair-wise comparison matrix (example:Table 5);2.calculating the priority vector for a criterion such as experience (example:Table 5);3.calculating the consistency ratio;4.calculating l m x ;5.calculating the consistency index,CI;6.selecting appropriate value of the random con-sistency ratio from Table 2;and7.checking the consistency of the pair-wise compar-ison matrix to check whether the decision-maker's comparisons were consistent or not.The calculations for these items will be explained next for illustration purposes.Synthesizing the pair-wise comparison matrix is performed by dividing each elementof the matrix by its column total.For example,the value 0.08in Table 5is obtained by dividing 1(from Table 4)by 12.5,the sum of the column items in Table 4(1 3 2 6 1a 2).The priority vector in Table 5can be obtained by ®nding the row averages.For example,the priority of contractor A with respect to the criterion `experience'in Table 5is calculated by dividing the sum of the rows (0X 08 0X 082 0X 073 0X 078 0X 118)by the number of contractors (columns),i.e.,5,in order to obtain the value 0.086.The priority vector for experience,indi-cated in Table 5,is given below.0X 0860X 2490X 1520X 4570X 055P T T T T R Q U U U U S I Now,estimating the consistency ratio is asfollows:Fig.1.Hierarchy of the project example..Table 4Pair-wise comparison matrix for experience Exp.A B C D E A 11/31/21/62B 3121/24C 21/211/33D 62317E1/21/41/31/71Table 5Synthesized matrix for experience a Exp.A B C D E Priority vectorA 0.080.0820.0730.0780.1180.086B 0.240.2450.2930.2330.2350.249C 0.160.1220.1460.1550.1760.152D 0.480.4890.4390.4660.4120.457E0.040.0610.0490.0660.0590.0550X 999al m x 5X 037,gs 0X 00925, s 1X 12,g 0X 0082`0X 1OK.24K.M.A.-S.Al-Harbi /International Journal of Project Management 19(2001)19±270X08613261a2PT TT TRQU UU US0X2491a311a221a4PT TT TRQU UU US0X1521a22131a3PT TT TRQU UU US0X4571a61a21a311a7PT TT TRQU UU US0X05524371PT TT TRQU UU US0X4311X2590X7662X3120X276PT TT TRQU UU USweighted sum m trixPDividing all the elements of the weighted sum matrices by their respective priority vector element,we obtain:0X431 0X086 5X012Y1X2590X2495X056Y0X7660X1525X039Y2X312 0X457 5X059Y0X2760X0555X018QWe then compute the average of these values to obtain l m xl m x5X012 5X056 5X039 5X059 5X01855X037 R Now,we®nd the consistency index,CI,as follows:gs l m xÀnnÀ15X037À55À10X00925 SSelecting appropriate value of random consistency ratio,RI,for a matrix size of®ve using Table2,we®nd RI=1.12.We then calculate the consistency ratio,CR, as follows:g gss0X009251X120X0082 TAs the value of CR is less than0.1,the judgments areacceptable.Similarly,the pair-wise comparison matricesand priority vectors for the remaining criteria can befound as shown in Tables6±10,respectively.In addition to the pair-wise comparison for the deci-sion alternatives,we also use the same pair-wise com-parison procedure to set priorities for all six criteria interms of importance of each in contributing to theoverall goal.Table11shows the pair-wise comparisonmatrix and priority vector for the six criteria.Now,the Expert Choice software can do the restautomatically,or we manually combine the criterionpriorities and the priorities of each decision alternativerelative to each criterion in order to develop an overallpriority ranking of the decision alternative which istermed as the priority matrix(Table12).The calcula-tions for®nding the overall priority of contractors aregiven below for illustration purposes:yver ll priority of ontr tor e0X3720X0860X2930X4250X1560X2690X1510X0390X0840X0870X1440X222 UTable7Pair-wise comparison matrix for quality performance(QP)aQP A B C D E Priority vectorA171/3280.269B1/711/51/440.074C351490.461D1/241/4160.163E1/81/41/91/610.0310X998a l m x 5X38,gs 0X095, s 1X12,g 0X085`0X1OK.Table8Pair-wise comparison matrix for manpower resources(MPR)aMPR A B C D E Priority vectorA11/21/4250.151B211/3570.273C431460.449D1/21/51/4120.081E1/51/71/61/210.0450X999a l m x 5X24,gs 0X059, s 1X12,g 0X053`0X1OK.Table6Pair-wise comparison matrix for®nancial stability(FS)aFS A B C D E Priority vectorA163270.425B1/611/41/230.088C1/3411/350.178D1/223170.268E1/71/31/51/710.0390X998a l m x 5X32,gs 0X08, s 1X12,g 0X071`0X1OK.K.M.A.-S.Al-Harbi/International Journal of Project Management19(2001)19±2725。

Portfolio Management: An OverviewOne measure of the benefits of diversification is the diversification ratio. It is calculated as the ratio of the risk of an equally weighted portfolio of n securities (measured by its standard deviation of returns) to the risk of a single security selected at random from the n securities.例子:If the average standard deviation of returns for the n stocks is 25%, and the standard deviation of returns for an equally weighted portfolio of the n stocks is 18%, the diversification ratio is 18 / 25 = 0.72.Foundations and endowments typically have long investment horizons, high risk tolerance, and, aside from their planned spending needs, little need for additional liquidity.Banks seek to keep risk low and need adequate liquidity to meet investor withdrawals as they occur.Insurance companies invest customer premiums with the objective of funding customer claims as they occur. Life insurance companies have a relatively long-term investment horizon, while property and casualty财产和意外保险(P&C) insurers have a shorter investment horizon because claims are expected to arise sooner than for life insurers.Sovereign wealth funds refer to pools of assets owned by a government.A defined contribution pension plan is a retirement plan in which the firm contributes a sum each period to the employee’s retirement account.In a defined benefit pension plan, the firm promises to make periodic payments to employees after retirement.There are three major steps in the portfolio management process:Step 1: The planning step begins with an analysis of the investor’s risk tolerance, return objectives, time horizon, tax exposure, liquidity needs, income needs, and any unique circumstances or investor preferences.This analysis results in an investment policy statement (IPS)that details the investor’s investment objectives and constraints.Step 2: The execution step involves an analysis of the risk and return characteristics of various asset classes to determine how funds will be allocated to the various asset types.in what is referred to as a top-down analysis, a portfolio manager will examine current economic conditions and forecasts of such macroeconomic variables as GDP growth, inflation, and interest rates, in order to identify the asset classes that are most attractive.Step 3: The feedback step is the final step. Over time, investor circumstances will change, risk and return characteristics of asset classes will change, and the actual weights of the assets in the portfolio will change with asset prices.Mutual funds are one form of pooled investments (i.e., a single portfolio that contains investment funds frommultiple investors). Each investor owns shares representing ownership of a portion of the overall portfolio. The total net value of the assets in the fund (pool) divided by the number of such shares issued is referred to as the net asset value (NA V) of each share.With an open-end fund, investors can buy newly issued shares at the NA V. Newly invested cash is invested by the mutual fund managers in additional portfolio securities. Investors can redeem their shares (sell them back to the fund) at NA V as well. All mutual funds charge a fee for the ongoing management of the portfolio assets, which is expressed as a percentage of the net asset value of the fund. No-load funds免佣基金do not charge additional fees for purchasing shares (up-front fees) or for redeeming shares (redemption fees). Load funds charge either up-front fees, redemption fees, or both.Closed-end funds are professionally managed pools of investor money that do not take new investments into the fund or redeem investor shares. The shares of a closed-end fund trade like equity shares (on exchanges or over-the-counter). As with open-end funds, the portfolio management firm charges ongoing management fees.T ypes of Mutual Funds:Money market funds invest in short-term debt securities and provide interest income with very low risk of changes in share value.Bond mutual funds invest in fixed-income securities. They are differentiated by bond maturities, credit ratings, issuers, and types.A great variety of stock mutual funds are available to investors. Index funds are passively managed; that is, the portfolio is constructed to match the performance of a particular index, such as the Standard & Poor’s 500 Index. Actively managed funds refer to funds where the management selects individual securities with the goal of producing returns greater than those of their benchmark indexes.Other Forms of Pooled Investments:Exchange-traded funds (ETFs) are similar to closed-end funds in that purchases and sales are made in the market rather than with the fund itself.【相同之处】【ETFs和close end fund不同之处】While closed-end funds are often actively managed, ETFs are most often invested to match a particular index (passively managed). With closed-end funds, the market price of shares can differ significantly from their NA V due to imbalances between investor supply and demand for shares at any point in time. Special redemption provisions for ETFs are designed to keep their market prices very close to their NA Vs.【ETFs和open end fund不同之处】ETFs can be sold short, purchased on margin, and traded at intraday盘中交易价prices, whereas open-end funds are typically sold and redeemed only daily, based on the share NA V calculated with closing asset prices.Investors in ETFs must pay brokerage commissions when they trade, and there is a spread between the bid price at which market makers will buy shares and the ask price at which market makers will sell shares.With most ETFs, investors receive any dividend income on portfolio stocks in cash, while open- end funds offer thealternative of reinvesting dividends in additional fund shares.One final difference is that ETFs may produce less capital gains liability compared to open- end index funds. This is because investor sales of ETF shares do not require the fund to sell any securities. If an open-end fund has significant redemptions that cause it to sell appreciated portfolio shares, shareholders incur a capital gains tax liability.A separately managed account is a portfolio that is owned by a single investor and managed according to that investor’s needs and preferences. No shares are issued, as the single investor owns the entire account.Portfolio Risk and Return: Part IHolding period return (HPR) is simply the percentage increase in the value of an investment over a given time period:The geometric mean return is a compound annual rate. When periodic rates of return vary from period to period, the geometric mean return < the arithmetic mean return:The money-weighted rate of return is the internal rate of return on a portfolio based on all of its cash inflows and outflows.Gross return refers to the total return on a security portfolio before deducting fees for the management and administration of the investment account. Net return refers to the return after these fees have been deducted.Note that commissions on trades and other costs that are necessary to generate the investment returns are deducted in both gross and net return measures.Pretax nominal return refers to the return prior to paying taxes.After-tax nominal return refers to the return after the tax liability is deducted.year when inflation is 2%. The investor’s approximate real return is simply 7 - 2 = 5%. The investor’s exact real return is slightly lower, 1.07 / 1.02 - 1 = 0.049 = 4.9%.A leveraged return refers to a return to an investor that is a multiple of the return on the underlying asset.The leveraged return is calculated as the gain or loss on the investment as a percentage of an investor’s cash investment. An investment in a derivative security, such as a futures contract, produces a leveraged return because the cash deposited is only a fraction一小部分of the value of the assets underlying the futures contract. Leveraged investments in real estate are very common: investors pay for only part of the cost of the property with their own cash, and the rest of the amount is paid for with borrowed money.small-capitalization stocks have had the greatest average returns and greatest risk over the period.Covariance measures the extent to which two variables move together over time. A positive covariance means that the variables (e.g., rates of return on two stocks) tend to move together. Negative covariance means that the two variables tend to move in opposite directions.Here we will focus on the calculation of the covariance between two assets’ returns using historical data.The covariance of the returns of two securities can be standardized by dividing by the product of the standard deviations of the two securities. This standardized measure of co-movement is called correlation and is computed as:A risk-averse investor is simply one that dislikes risk (i.e., prefers less risk to more risk). Given two investments that have equal expected returns, a risk-averse investor will choose the one with less risk (standard deviation).A risk-seeking (risk-loving) investor actually prefers more risk to less and, given equal expected returns, willchoose the more risky investment. A risk-neutral investor has no preference regarding risk and would be indifferent between two such investments.The variance of returns for a portfolio of two risky assets is calculated as follows:Note that portfol io risk falls as the correlation between the assets’ returns decreases. This is an important result of the analysis of portfolio risk: The lower the correlation of asset returns, the greater the risk reduction (diversification) benefit of combining assets in a portfolio. If asset returns were perfectly negatively correlated, portfolio risk could be eliminated altogether for a specific set of asset weights.For each level of expected portfolio return, we can vary the portfolio weights on the individual ass ets to determine the portfolio that has the least risk. These portfolios that have the lowest standard deviation of all portfolios with a given expected return are known as minimum-variance portfolios. T ogether they make up the minimum-variance frontier. On a risk versus return graph, the portfolio that is farthest to the left (has the least risk) is known as the global minimum-variance portfolio整体最小方差投资组合.Assuming that investors are risk averse, investors prefer the portfolio that has the greatest expected return when choosing among portfolios that have the same standard deviation of returns. Those portfolios that have the greatest expected return for each level of risk (standard deviation) make up the efficient frontier.An investor’s utility function效用函数represents the investor’s preferences in terms of risk and return (i.e., his degree of risk aversion).An indifference curve is a tool from economics that, in this application, plots combinations of risk (standard deviation) and expected return among which an investor is indifferent.a more risk-averse investor will have steeper indifference curves, reflecting a higher risk aversion coefficient. Combining a risky portfolio with a risk-free asset is the process that supports the two- fund separation theorem, which states that all investors’ optimum portfolios will be made up of some combination of an optimal portfolio of risky assets and the risk-free asset. The line representing these possible combinations of risk-free assets and theoptimal risky asset portfolio is referred to as the capital allocation line.Now that we have constructed a set of the possible efficient portfolios (the capital allocation line) Portfolio Risk and Return: Part IIThe line of possible portfolio risk and return combinations given the risk-free rate and the risk and return of a portfolio of risky assets is referred to as the capital allocation line (CAL).A simplifying assumption underlying modern portfolio theory (and the capital asset pricing model, which is introduced later in this topic review) is that investors have homogeneous expectationsDepending on their preferences for risk and return (their indifference curves), investors may choose different portfolio weights for the risk-free asset and the risky (tangency) portfolio. Every investor, however, will use the same risky portfolio. When this is the case, that portfolio must be the market portfolio of all risky assets because all investors that hold any risky assets hold the same portfolio of risky assets.只有与有效边界相切的那条才是CML。